Posts tagged ‘Ben Bernanke’

Confessions of a Bond Hater

Source: stock.xchng

Hi my name is Wade, and I’m a bond hater. Generally, the first step in addressing any type of personal problem is admitting you actually have a problem. While I am not proud of being a bond hater, I have been called many worse things during my life. But as we have learned from the George Zimmerman / Trayvon Martin case, not every situation is clear-cut, whether we are talking about social issues or bond investing. For starters, let me be clear to everyone, including all my detractors, that I do not hate all bonds. In fact, my Sidoxia clients own many types of fixed income securities. What I do hate however are low yielding, long duration bonds.

Duration…huh? Most people understand what “low yielding” means, when it comes to bonds (i.e., low interest, low coupon, low return, etc.), but when the word duration is uttered, the conversation is usually accompanied by a blank stare. The word “duration” may sound like a fancy word, but in reality it is a fairly simple concept. Essentially, high-duration bonds are those fixed income securities with the highest sensitivity to changes in interest rates, meaning these bonds will go down most in price as interest rates rise.

When it comes to equity markets, many investors understand the concept of high beta stocks, which can be used to further explain duration. There are many complicated definitions for beta, but the basic principle explains why high-beta stock prices generally go up the most during bull markets, and go down the most during bear markets. In plain terms, high beta equals high octane.

If we switch the subject back to bonds, long duration equals high octane too. Or stated differently, long duration bond prices generally go down the most during bear markets and go up the most during bull markets. For years, grasping the risk of a bond bear market caused by rising rates has been difficult for many investors to comprehend, especially after witnessing a three-decade long Federal Funds tailwind taking the rates from about 20% to about 0% (see Fed Fatigue Setting In).

The recent interest rate spike that coincided with the Federal Reserve’s Ben Bernanke’s comments on QE3 bond purchase tapering has caught the attention of bond addicts. Nobody knows for certain whether this short-term bond price decline is the start of an extended bear market in bonds, but mathematics would dictate that there is only really one direction for interest rates to go…and that is up. It is true that rates could remain low for an indefinite period of time, but neither scenario of flat to down rates is a great outcome for bond holders.

Fixes to Fixed-Income Failings

Even though I may be a “bond hater” of low yield, high duration bonds, currently I still understand the critical importance and necessity of a fixed income portfolio for not only retirees, but also for the diversification benefits needed by a broader set of investors. So how does a bond hater reconcile investing in bonds? Easy. Rather than focusing on lower yielding, longer duration bonds, I invest more client assets in shorter duration and/or higher yielding bonds. If you harbor similar beliefs as I do, and believe there will be an upward bias to the trajectory of long-term interest rates, then there are two routes to go. Investors can either get compensated with a higher yield to counter the increased interest rate risk, and/or they can shorten duration of bond holdings to minimize capital losses.

Worth noting, there is an alternative strategy for low yielding, long duration bond lovers. In order to minimize interest rate risk, these bond lovers may accept sub-optimal yields and hold bonds to maturity. This strategy may be associated with short-term price volatility, but if the bond issuer does not default, at least the bond investor will get the full principal at maturity to help relieve the pain of meager yields.

Now that you’ve survived all this bond babbling, let me cut to the chase and explain a few ways Sidoxia is taking advantage of the recent interest rate volatility for our clients:

Floating Rate Bonds: Duration of these bonds is by definition low, or near zero, because as interest rates rise, coupons/interest payments are advantageously reset for investors at higher rates. So if interest rates jump from 2% to 3%, the investor will receive +50% higher periodic payments.

Inflation Protection Bonds: These bonds come in long and short duration flavors, but if interest rates/inflation rise higher than expected, investors will be compensated with higher periodic coupons and principal payments.

Shorter Duration: One definition of duration is the weighted average of time until a bond’s fixed cash flows are received. A way of shortening the duration of your bond portfolio is through the purchase of shorter maturity bonds (e.g., buying 3-year bonds rather than 30-year bonds).

High Yield Bonds: Investing in the high yield bond category is not limited to domestic junk bond purchases, but higher yields can also be earned by investing in international and/or emerging market bonds.

Investment Grade Corporate Bonds: Similar to high yield bonds, investment grade bonds offer the potential of capital appreciation via credit improvement. For instance, credit rating upgrades can provide gains to help offset price declines caused by rising interest rates.

Despite my bond hater status, the recent taper tantrum and interest rate spike, highlight some advantages bonds have over stocks. Even though prices declined, bonds by and large still have lower volatility than stocks; provide a steady stream of income; and provide diversification benefits.

To the extent investors have, or should have, a longer-term time horizon, I still am advocating a stock bias to client portfolios, subject to each investor’s risk tolerance. For example, an older retired couple with a conservative target allocation of 20%/80% (equity/fixed income) may consider a 25% – 30% allocation. A shift in this direction may still meet the retirees’ income needs (especially if dividend-paying stocks are incorporated), while simultaneously acknowledging the inflation and interest rate risks impacting bond positions. It’s important to realize one size doesn’t fit all.

Higher Volatility, Higher Reward

Frequent readers of Investing Caffeine have known about my bond hating tendencies for quite some time (see my 2009 article Treasury Bubble has not Burst…Yet), but the bond baby shouldn’t be thrown out with the bath water. For those investors who thought bonds were as safe as CDs, the recent -6% drop in the iShares Aggregate Bond Index (AGG) didn’t feel comfortable for most. Although I am still an enthusiastic stock cheerleader (less so as valuation multiples expand), there has been a cost for the gargantuan outperformance of stocks since March of ’09. While stocks have outperformed bonds (S&P vs. AGG) by more than +140%, equity investors have had to endure two -10% corrections and two -20% corrections (e.g.,Flash Crash, Debt Ceiling Debate, European Financial Crisis, and Sequestration/Elections). If investors want to earn higher long-term equity returns, this desire will translate into more volatility than bonds…and more Tums.

I may still be a bond hater, and the general public remains firm stock haters, but at some point in the multi-year future, I will not be surprised to hear myself say, “Hi my name is Wade, and I am addicted to bonds.” In the mean time, Sidoxia will continue to optimize its client bond portfolios for a rising interest rate environment, while also investing in attractive equity securities and ETFs. There’s nothing to hate about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including floating rate bonds/loan funds, inflation-protection funds, corporate bond ETF, high-yield bond ETFs, and other bond ETFs, but at the time of publishing, SCM had no direct position in AGG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

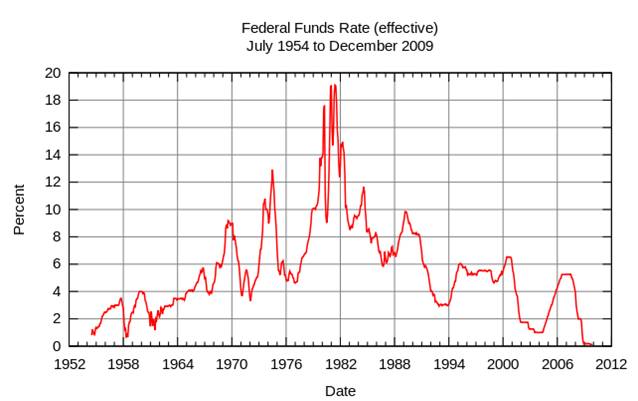

Fed Fatigue Setting In

Uncle…uncle! There you have it – I have finally cried “uncle” because I cannot take it anymore. I don’t think I can listen to another panel or read another story debating about the timing of Fed “tapering”, or heaven forbid the Fed actually “tighten” the Federal Funds rate (i.e., increasing the targeted rate for inter-bank lending). Type in the words “Bernanke” and “tapering” into Google and you will get back more than 41,000,000 results. The build up to the 600-word FOMC (Federal Open Market Committee) statement was almost deafening, so much so that live coverage of Federal Reserve Chairman Ben Bernanke was available at your fingertips:

Source: Yahoo! Finance

Like a toddler (or a California-based, investment blog writer) going to the doctor’s office to receive an inoculation, the anxiety and mental anguish caused in anticipation of the event is often more painful than the actual injection. As I highlighted in a previous Investing Caffeine article, the 1994 interest rate cycle wasn’t Armageddon for equity markets, and the same can be said for the rate hikes from 1.0% to 5.25% in the 2004-20006 period (see chart below). Even if QE3 ends in mid-2014 and the new Federal Reserve Chairman (thank you President Obama) raises rates in 2015, this scenario would not be the first (or last) time the Federal Reserve has tightened monetary policy.

Source: Wikipedia

Short Memories – What Have You Done for Me Lately?

People are quick to point out the one-day -350 Dow point loss earlier this week, but many of them forget about the +3,000 point moon shot in the Dow Jones Industrial index that occurred in six short months (November 2012 – May 2013). The same foggy recollection principle applies to interest rates. The recent rout in 10-year Treasury prices is easily recalled as rates have jumped from 1.5% to 2.5% over the last year, however amnesia often sets in for others if you ask them where rates were a few years ago. It’s easy to forget that 30-year fixed rate mortgages exceeded 5% and the 10-year reached 4% just three short years ago.

Bernanke: The Center of the Universe?

Does Ben Bernanke deserve credit for implementing extraordinary measures during extraordinary times during the 2008-09 financial crisis? Absolutely. But should every man, women, and child wait with bated breath to see if a word change or tonal adjustment is made in the eight annual FOMC meetings?

Like the public judging Ben Bernanke, my Sidoxia clients probably give me too much credit when things go well and too much blame when things don’t. I love how Bernanke gets blamed/credited for the generational low interest rates caused by his money printing ways and QE punch bowl tactics. Last I checked, the interest rate downtrend has been firmly in place over the last three decades, well before Bernanke came into the Fed and worked his monetary magic. How much credit/blame are we forgetting to give former Federal Reserve Chairmen Paul Volcker, Alan Greenspan, and other government policy-makers? Regardless of what happens economically for the remainder of 2013, Bernanke will do whatever he can to solidify his legacy in the waning sunset months of his term.

Another forgotten fact I like to point out: There is more than one central banker living on this planet. If you haven’t been asleep over the last few decades, our financial markets have increasingly become globally interconnected with the assistance of technology. I know our 10-year Treasury rates are hovering around 2.50%, and our egotistical patriotism leads us to hail Bernanke as a monetary god, but don’t any other central bankers or government officials around the world deserve any recognition for achieving yields even lower than ours? Here’s a partial list (June 22, 2013 – Financial Times):

- Japan – 0.86%

- Germany – 1.67%

- Canada – 2.33%

- U.K. – 2.31%

- France – 2.27%

- Sweden – 2.15%

- Austria – 2.09%

- Switzerland – 0.92%

- Netherlands – 2.07%

Although it may be fun to look at Ben Bernanke as our country’s financial Superman who is there to save the day, there are a lot more important factors to consider than the 47 words added and 19 subtracted from the latest FOMC statement. If investing was as easy as following central bank monetary policy, everyone would be continually jet setting to their private islands. Rather than wasting your time listening to speculative blathering about direction of Fed monetary policy, why not focus on finding solid investment ideas and putting a long-term investment plan in place. Now please excuse me – Fed fatigue has set in and I need to take a nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No Free Lunch, No Free Sushi

Everybody loves a free lunch, myself included, and many in Japan would like free sushi too. Despite the short term boost in Japanese exports and Nikkei stock prices, there are no long-term free lunches (or free sushi) when it comes to global financial markets. Following in the footsteps of the U.S. Federal Reserve, the Bank of Japan (BOJ) has embarked on an ambitious plan of doubling its monetary base in two years and increasing inflation to a 2% annual rate – a feat that has not been achieved in more than two decades. By the BOJ’s estimate, it will take a $1.4 trillion injection into economy to achieve this goal by the end of 2014.

Lunch is tasty right now, as evidenced by a tasty appetizer of +3.5 % Japanese first quarter GDP and this year’s +46% spike in the value of the Nikkei. Japan is hopeful that its mix of monetary, fiscal, and structural policies will spur demand and increase the appetite for Japanese exports, however, we know fresh sushi can turn stale quickly.

Quantitative easing (QE) and monetary stimulus from central banks around the globe have been hailed as a panacea for sluggish global growth – most recently in Japan. Commentators often oversimplify the benefits of money printing without acknowledging the pitfalls. Basic economics and the laws of supply & demand eventually prevail no matter the fiscal or monetary policy implemented. Nonetheless, there can be temporary disconnects between current equity prices and exchange rates, before underlying fundamentals ultimately drive true intrinsic values.

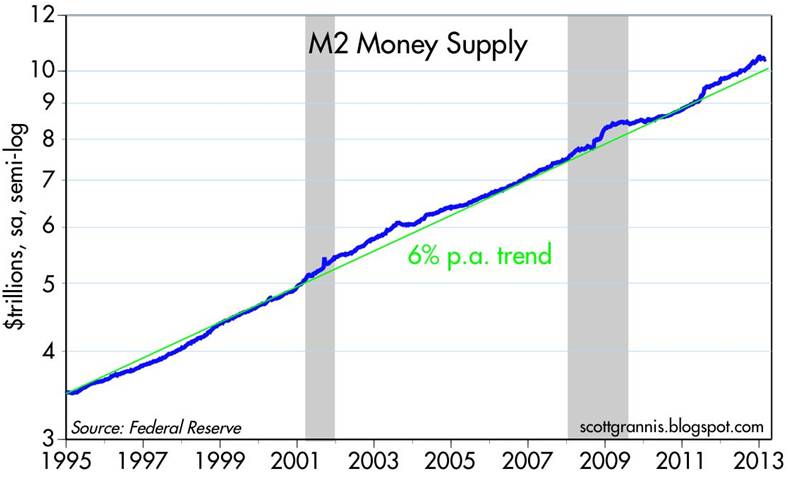

Impassioned critics of the Federal Reserve and its Chairman Ben Bernanke would have you believe the money supply is exploding, and hyperinflation is just around the corner. It’s difficult to quarrel with the trillions of dollars created by the Fed’s printing presses via QE1/QE2/QE3, but the fact remains that money supply growth has continued at a steady growth rate – not exploding (see Calafia Beach Pundit chart below).

Source: Calafia Beach Pundit

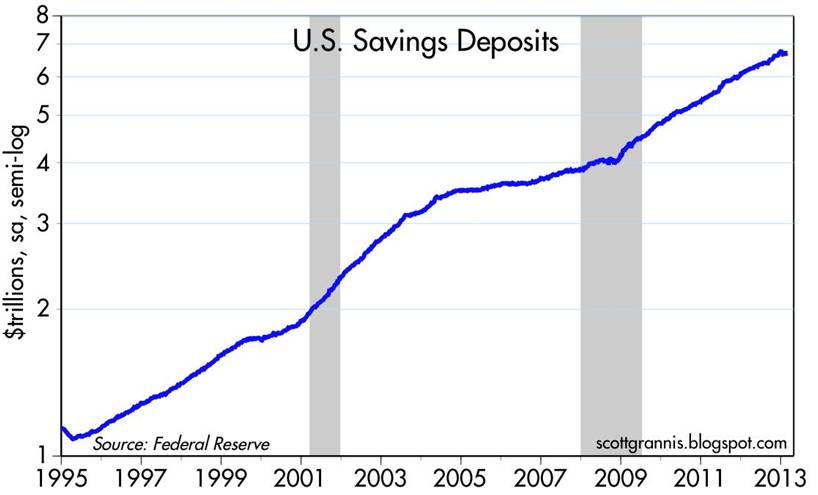

Why no explosion in the money supply? Simply, the trillions of dollars printed by the Fed have sat idly in bank vaults as reserves. Once nervous consumers stop hoarding trillions in cash held in savings deposit accounts (see chart below) and banks begin lending at a healthier clip, then money supply growth will accelerate. By definition, money supply growth in excess of demand for goods and services (i.e., GDP) is the main cause of inflation.

Source: Calafia Beach Pundit

Although inflationary pressure has not reared its ugly head yet, there are plenty of precursors indicating inflation may be on its way. The unemployment rate continues to tick downwards (7.5% in Aril) and the much anticipating housing recovery is gaining steam. Inflationary fear has manifested itself in part through the heightened number of conversations surrounding the Fed “tapering” its $85 billion per month bond purchasing program.

We’ve enjoyed a sustained period of low price level growth, however the Goldilocks period of little-to-no inflation cannot last forever. The differences between current prices and true value can exist for years, and as a result there are many different strategies attempted to capture profits. Like the gambling masses frequenting casinos, speculators can beat the odds in the short-run, but the house always wins in the long-run – hence the ever-increasing size and number of casinos. While a small number of professionals understand how to shift the unbalanced odds into their favor, most lose their shirt. On Wall Street, that is certainly the case. Studies show speculating day traders persistently lose about 80% of the time. Long-term investors are uniquely positioned to exploit these value disparities, if they have a disciplined process with the ability to patiently value assets.

Even though the Japanese economy and stock market have rebounded handsomely in the short-run, there is never a free lunch over the long-term. Unchecked policies of money printing, deficits, and debt expansion won’t lead to boundless prosperity. Eventually a spate of irresponsible actions will result in inflation, defaults, recessions, and/or higher unemployment rates. Unsustainable monetary and fiscal stimulus may lead to a tasty free lunch now, but if investors overstay their welcome, the sushi may turn bad and the speculators will be left paying the hefty tab.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Central Bank Dog Ate My Homework

It’s been a painful four years for the bears, including Peter Schiff, Nouriel Roubini, John Mauldin, Jimmy Rogers, and let’s not forget David Rosenberg, among others. Rosenberg was recently on CNBC attempting to clarify his evolving bearish view by explaining how central banks around the globe have eaten his forecasting homework. In other words, Ben Bernanke is getting blamed for launching the stock market into the stratosphere thanks to his quantitative easing magic. According to Rosenberg, and the other world-enders, death and destruction would have prevailed without all the money printing.

In reality, the S&P 500 has climbed over +140% and is setting all-time record highs since the market bottomed in early 2009. Despite the large volume of erroneous predictions by Rosenberg and his bear buddies, that development has not slowed the pace of false forecasts. When you’re wrong, one could simply admit defeat, or one could get creative like Rosenberg and bend the truth. As you can tell from my David Rosenberg article from 2010 (Rams Butting Heads), he has been bearish for years calling for outcomes like a double-dip recession; a return to 11% unemployment; and a collapse in the market. So far, none of those predictions have come to fruition (in fact the S&P is up about +40% from that period, if you include dividends). After being incorrect for so long, Rosenberg has switched his mantra to be bullish on pullbacks on selective dividend-paying stocks. When pushed whether he has turned bullish, here’s what Rosenberg had to say,

“So it’s not about is somebody bearish or is somebody bullish or whether you’re agnostic, it’s really about understanding what the principle driver of this market is…it’s the mother of all liquidity-driven rallies that I’ve seen in my lifetime, and it’s continuing.”

Rosenberg isn’t the only bear blaming central banks for the unexpected rise in equity markets. As mentioned previously, fear and panic have virtually disappeared, but these emotions have matured into skepticism. Record profits, cash balances, and attractive valuations are dismissed as artificial byproducts of a Fed’s monetary Ponzi Scheme. The fact that Japan and other central banks are following Ben Bernanke’s money printing lead only serves to add more fuel to the bears’ proverbial fire.

Speculative bubbles are not easy to identify before-the-fact, however they typically involve a combination of excessive valuations and/or massive amounts of leverage. In hindsight we experienced these dynamics in the technology collapse of the late-1990s (tech companies traded at over 100x’s earnings) and the leverage-induced housing crisis of the mid-2000s ($100s of billions used to speculate on subprime mortgages and real estate).

I’m OK with the argument that there are trillions of dollars being used for speculative buying, but if I understand correctly, the trillions of dollars in global liquidity being injected by central banks across the world is not being used to buy securities in the stock market? Rather, all the artificial, pending-bubble discussions should migrate to the bond market…not the stock market. All credit markets, to some degree, are tied to the trillions of Treasuries and mortgage-backed securities purchased by central banks, yet many pundits (i.e., see El-Erian & Bill Gross) choose to focus on claims of speculative buying in stocks, and not bonds.

While bears point to the Shiller 10 Price-Earnings ratio as evidence of a richly priced stock market, more objective measurements through FactSet (below 10-year average) and Wall Street Journal indicate a forward P/E of around 14. A reasonable figure if you consider the multiples were twice as high in 2000, and interest rates are at a generational low (see also Shiller P/E critique).

The news hasn’t been great, volatility measurements (i.e., VIX) have been signaling complacency, and every man, woman, and child has been waiting for a “pullback” – myself included. The pace of the upward advance we have experienced over the last six months is not sustainable, but when we finally get a price retreat, do not listen to the bears like Rosenberg. Their credibility has been shot, ever since the central bank dog ate their homework.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Debuts Video & Goes to the Movies

Article is an excerpt from previously released Sidoxia Capital Management’s complementary February 1, 2013 newsletter. Subscribe on right side of page.

The red carpet was rolled out for the stock market in January with the Dow Jones Industrial Average rising +5.8% and the S&P 500 index up an equally impressive +5.0% (a little higher rate than the 0.0001% being earned in bank accounts). Movie stars are also strutting their stuff down the red carpet this time of the year as they collect shiny statues at ritzy award shows like the Golden Globes and Oscars. Given the vast volumes of honors bestowed, we thought what better time to put on our tuxes and create our own 2013 nominations for the economy and financial markets. If you are unhappy with our selections, you are welcome to cast your own votes in the comments section below.

By award category, here are Sidoxia’s 2013 selections:

Best Drama (Government Shutdown & Debt Ceiling): Washington D.C. has provided no shortage of drama, and the upcoming blockbusters of Shutdown & Debt Ceiling are worthy of its Best Drama nomination. If Congressional Democrats and Republicans don’t vote in favor of a new “Continuing Resolution” by March 27th, then our United States government will come to a grinding halt. At issue is Republican’s desire for additional government spending cuts to lower our deficit, which is likely to exceed $1 trillion for the fifth consecutive year. If you like more heart pumping drama, the Senate has just passed a Debt Ceiling extension through May 18th…mark those calendars!

Best Horror Film (Sequestration): Most people have already seen the scary prequel, The Fiscal Cliff, but the sequel Sequestration deserves the horror film honors of 2013. This upcoming blood-filled movie about broad, automatic, across-the-board government cost cuts will make any casual movie-watcher scream in terror. The $1.2 trillion in spending cuts (over 10 years) are so gory, many viewers may voluntarily leave the theater early. If you are waiting for the release, Sequestration is coming to a theater near you on March 1st, unless Congress, in an unlikely scenario, cancels the launch.

Best Director (Ben Bernanke): Federal Reserve Chairman Ben Bernanke’s film, entitled, The U.S. Economy, had a massive budget of about $16 trillion dollars, based on estimates of last year’s GDP (Gross Domestic Product). Nevertheless, Bernanke managed to do whatever it took (including trillions of dollars in bond buying) to prevent the economic movie studio from collapsing into bankruptcy. While many movie-goers were critical of his directorial debut, inflation has remained subdued thus far, and he has promised to continue his stimulative monetary policies (i.e., keep interest rates low) until the national unemployment rate falls below 6.5% or inflation rises above 2.5%.

Best Foreign Film (China): Americans are not the only people who produce movies globally. A certain country with a population of nearly 1.4 billion people also makes movies too…China. In the most recently completed 4th quarter, China’s economy experienced blockbuster growth in the form of +7.9% GDP expansion. This was the fastest pace achieved by China in two whole years. To put this metric into perspective, compare China’s heroic growth to the bomb created by the U.S. economy, which registered a disappointing -0.1% contraction at the economic box office. China’s popularity should bring in business all around the globe.

Best Special Effects (Japan): After coming out with a series of continuous flops, Japan recently launched some fresh new special effects in the form of a $116 billion emergency stimulus package. The country also has plans to superficially enhance the visual portrayal of its economy by implementing its own faux money-printing program modeled after our country’s quantitative easing actions (i.e., the Federal Reserve stimulus). As a result of these initiatives, the Japanese Nikkei index – their equivalent of our Dow Jones Industrial index – has risen by +29% in less than 3 months to a level of 11,138.66 (click here for chart). But don’t get too excited. This same Nikkei index peaked at 38,957 in 1989, a far cry from its current level.

Best Action Film (Icahn vs. Ackman): This surprisingly entertaining action film features a senile 76-year-old corporate raider and a white-haired, 46-year-old Harvard grad. The investment foes I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. In addition to terms such as crybaby, loser, and liar, the 27-minute verbal spat (view more here) between Icahn (his net worth equal to about $15 billion) and Ackman (net worth approaching $1 billion) includes some NC-17 profanity. The clash of these investment titans stems from a decade-old lawsuit, in addition to a recent disagreement over a controversial short position in Herbalife Ltd. (HLF), a nutritional multi-level marketing firm.

Best Documentary (Europe): As with a lot of reality-based films, many don’t receive a lot of attention. So too has been the commentary regarding the eurozone, which has been relatively peaceful compared to last spring. Despite the comparative media silence, European unemployment reached a new high of 11.8% late last year. This European documentary is not one you should ignore. European Central Bank (ECB) President Mario Draghi just stated, “The risks surrounding the outlook for the euro area remain on the downside.”

Best Original Song (National Anthem): We won’t read anything politically into Beyonce’s lip-synced rendition of The Star-Spangled Banner at the presidential inauguration, but she is still worthy of the Sidoxia nomination because music we hear in the movies is also recorded. I’m certain her rapping husband Jay-Z agrees whole-heartedly with this viewpoint.

Best Motion Picture (Sidoxia Video): It may only be three minutes long, but as my grandmother told me, “Great things come in small packages.” I may be a little biased, but judge for yourself by watching Sidoxia’s Oscar-worthy motion picture debut:

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Helicopter Ben to QE3 Rescue

Faster than a speedy credit default swap, more powerful than a federal funds interest rate cut, and able to leap a tall Mario Draghi in a single bound, look…it’s Helicopter Ben! How did Federal Reserve Chairman Ben Bernanke become a monetary superhero with such a cool nickname as Helicopter Ben (a.k.a. “HB”)? Bernanke, a former Princeton University professor, has widely been known to be a diligent student of the Great Depression, and his aviation nickname stems from a 2002 speech in which he referenced dropping money from a helicopter to combat deflation. While investors may worry about HB’s ability to fight the inflation thugs, there should be no questions about his willingness to implement accommodative, deflation-fighting monetary policies.

Chairman Bernanke may not epitomize your ideal superhero, however this slightly past middle-aged bearded and balding man has helped mastermind some of the most creative and aggressive monetary rescue efforts our country and globe has seen in the history of man (and woman). This week’s money-printing QE3 announcement solidified Bernanke’s historic capital saturating ranking.

Since Helicopter Ben’s heroic appointment as Federal Reserve Chairman in 2006 by George W. Bush, Bernanke has instituted numerous monetary gadgets in hopes of meeting the Federal Reserve’s dual mandate, which is i) to achieve low inflation and ii) to strive for maximum employment. Arguably, given the anemic growth here in the U.S.; the recession in Europe; and slowing growth in the emerging markets (i.e., China, Brazil, India, etc.), slack in the economy and static labor wages have largely kept inflation in check. With the first part of the dual mandate met, Bernanke has had no problem putting his monetary superpowers to work.

As referenced earlier, Bernanke’s bazooka launch of QE3, an open ended MBS (Mortgage Back Securities) bond binging program, will add $40 billion of newly purchased assets to the Fed’s balance sheet on a monthly basis until the labor market improves “substantially” (whatever that means). What’s more, in addition to the indefinite QE3, Bernanke has promised to keep the federal funds rate near zero “at least through mid-2015,” even for a “considerable time after the economic recovery strengthens.”

HB’s Track Record

Throughout superhero history, Superman, Spider-man, and Batman have used a wide-array of superhuman powers, extraordinary gadgets, and superior intellect to conquer evil-doers and injustices across the globe. Bernanke has also forcefully put his unrivaled money-printing talents to work in an attempt to cure the financial ills of the world. Here’s a quick multi-year overview of how Bernanke has put his unique talents to print trillions of dollars and keep interest rates suppressed:

Rate Cuts (September 2007 – December 2008): Before “quantitative easing” was a part of our common vernacular, the Fed relied on more traditional monetary policies, such as federal funds rate targeting, conducted through purchases and sales of open market securities. Few investors recall, but before HB’s fed funds rate cut rampage of 10 consecutive reductions in 2007 and 2008 (the fed funds rate went from 5.25% to effectively 0%), Bernanke actually increased rates three times in 2006.

Crisis Actions (2007 – 2009): Love him or hate him, Bernanke has been a brave and busy soul in dealing with the massive proportions of the global financial crisis. If you don’t believe me, just check out the Financial Crisis Timeline listed at the St. Louis Federal Reserve. Many investors don’t remember, but Bernanke helped orchestrate some of the largest and most unprecedented corporate actions in our history, including the $30 billion loan to JPMorgan Chase (JPM) in the Bear Stearns takeover; the $182 billion bailout of AIG; the conversion of Morgan Stanley (MS) and Goldman Sachs Group Inc. (GS) into bank holding companies; and the loan/asset-purchase support to Fannie Mae (FNMA) and Freddie Mac (FMCC). These actions represented just the tip of the iceberg, if you also consider the deluge of liquidity actions taken by the Fed Chairman.

HB Creates Acronym Soup

In order to provide a flavor of the vastness in emergency programs launched since the crisis, here is an alphabet soup of program acronyms into which the Fed poured hundreds of billions of dollars:

- Term Asset-Backed Securities Loan Facility (TALF)

- Term Auction Facility (TAF)

- Money Market Investor Funding Facility (MMIFF)

- Commercial Paper Funding Facility (CPFF)

- Primary Dealer Credit Facility (PDCF)

- Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF)

- Temporary Reciprocal Currency Arrangements (Swap lines)

- Term Securities Lending Facility (TSLF)

Plenty of acronyms to go around, but these juicy programs have garnered most of investors’ attention:

QE1 (November 2008 – March 2010): In hopes of lowering interest rates for borrowers and stimulating the economy, HB spearheaded the Fed’s multi-step, $1 trillion+ buying program of MBS (mortgage backed securities) and Treasuries.

QE2 (November 2010 – June 2011): Since the Fed felt QE1 didn’t pack enough monetary punch to keep the economy growing at a fast enough clip, the FOMC (Federal Open Market committee) announced its decision to expand its holdings of securities in November 2010. The Committee maintained its existing policy of reinvesting principal payments from its securities holdings and to also purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011 (an equivalent pace of about $75 billion per month).

Operation Twist (September 2011 – December 2012): What started out as a $400 billion short-term debt for longer-term debt swap program in September 2011, expanded to a $667 billion program in June 2012. With short-term rates excessively low, Bernanke came up with this Operation Twist scheme previously used in the early 1960s. Designed to flatten the yield curve (bring down long-term interest rates) to stimulate economic activity, Bernanke thought this program was worth another go-around. Unlike quantitative easing, Operation Twist does not expand the Fed’s balance sheet – the program merely swaps short-term securities for long-term securities. Currently, the program is forecasted to conclude at the end of this year.

The Verdict on HB

So what’s my verdict on the continuous number of unprecedented actions that Helicopter Ben and the Fed have taken? Well for starters, I have to give Mr. Bernanke an “A-” on his overall handling of the financial crisis. Had his extreme actions not been taken, the pain and agony experienced by all would likely be significantly worse, and the financial hole a lot deeper.

With that said, am I happy about the announcement of QE3 and the explosion in the Fed’s money printing activities? The short answer is “NO”. It’s difficult to support a program with questionable short-run interest rate benefits, when the menacing inflationary pressures are likely to outweigh the advantages. The larger problem in my mind is the massive fiscal problem we are experiencing (over $16 trillion in debt and endless trillion dollar deficits). More importantly, this bloated fiscal position is creating an overarching, nagging crisis of confidence. A resolution to the so-called “fiscal cliff,” or the automated $600 billion in tax increases and spending cuts, is likely to have a more positive impact on confidence than a 0.05% – 0.25% reduction in mortgage rates from QE3. Once adequate and sustained growth returns, and inflation rears its ugly head, how quickly Helicopter Ben tightens policy will be his key test.

Until then, Bernanke will probably continue flying around while gloating in his QE3 cape, hoping his quantitative easing program will raise general confidence. Unfortunately, his more recent monetary policies appear to be creating diminishing returns. Even before QE3’s implementation, Helicopter Ben has witnessed his policies expand the Fed’s balance sheet from less than $900 billion at the beginning of the recession to almost $3 trillion today. Despite these gargantuan efforts, growth and confidence have been crawling forward at only a modest pace.

No matter the outcome of QE3, as long as Ben Bernanke remains Federal Reserve Chairman, and growth remains sluggish, you can stay confident this financial man of steel will continue dumping money into the system from his helicopter. If Bernanke wants to create a true legendary superhero ending to this story, the kryptonite-like effects of inflation need to be avoided. This means, less money-printing and more convincing of Congress to take action on our out-of-control debt and deficits. Now, that’s a comic book I’d pay to read.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in JPM, AIG, MS, GS, FNMA, FMCC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Financial Olympics: Chasing Gold, Siver & Bronze

Article is an excerpt from previously released Sidoxia Capital Management’s complementary August 1, 2012 newsletter. Subscribe on right side of page.

As a record number of 204 nations compete at the XXX Olympic Games in London, and millions of couch-watchers root on their favorite athletes, a different simultaneous competition is occurring…the 2012 Financial Olympics. So far, both Olympics have provided memorable moments for all. While the 2012 London Olympic viewers watched James Bond and Queen Elizabeth II parachute into a stadium filled with 80,000 cheering fans, investors cheered the Dow Jones Industrial Average above the 13,000 level on the same day of the opening ceremony. We have already witnessed a wide range of emotions displayed by thousands of athletes chasing gold, silver, and bronze, and the same array of sentiments associated with glory and defeat have been observed in the 2012 Financial Olympics. There is still a way to go, but despite all the volatility, the stock market is still up a surprising +10% in 2012.

Here were some of the key Financial Olympic events last month:

Draghi Promises Gold for Euro: Some confident people promise gold medals while others promise the preservation of a currency – European Central Bank President (ECB) Mario Draghi personifies the latter. Draghi triggered the controversy with comments he made at the recent Global Investment Conference in London. In the hopes of restoring investor confidence Draghi emphatically proclaimed, “The ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” To view this excerpt, click video link here.

U.S. Economy Wins Bronze: Whereas Europe has been disqualified from the Financial Olympics due to recessionary economic conditions (Markit predicts a -0.6% contraction in Q3 eurozone GDP), the U.S. posted respectable Q2 GDP results of +1.5%. This surely is an effort worthy of a bronze medal given the overall sluggish, global demand. Fears over a European financial crisis contagion; undecided U.S. Presidential election; and uncertain “fiscal cliff” (automatic tax hikes and spending cuts) are factors contributing to the modest growth. Nevertheless, the US of A has posted 12 consecutive quarters of economic growth (see chart below) and if some clarity creeps back into the picture, growth could reaccelerate.

Source (Calafia Beach Pundit)

No Podium for Spain: Spain’s recent economic achievements closely mirror those of the athletic team, which thus far has failed to secure a sporting medal of any color. Why no Spanish glory? Recently, the Bank of Spain announced the country’s economy was declining at a -1.6% annual rate. Shortly thereafter, Spain estimated its economy would contract by -0.5% in 2013 instead of expanding +0.2%, as previously expected. Adding insult to injury, Valencia (Spain’s most indebted region) said central government support would be needed to repay its debts. These factors, and others, have forced the Spanish government to adopt severe austerity measures to cut its budget deficit by $80 billion through 2015. Spanish banks have negotiated a multi-billion-euro bailout, but they will have to hand control over to European institutions as a concession. Considering these facts, combined with an unemployment rate near 25%, one can appreciate the dominant and pervading losing spirit.

Global Central Banks Inject Financial Steroids: The challenging and competitive global growth environment is not new news to central bankers around the world. As a result, finance leaders around the world are injecting financial steroids into their countries via monetary stimulus (mostly rate cuts and bond buying). Like steroids, these actions may have short-term invigorating effects, but these measures can also have longer-term negative consequences (i.e., inflation). Here are some of the latest country-specific examples (also see chart below):

- U.S. Federal Reserve Chairman Ben Bernanke has already shot a couple “Operation Twist” and “QE” (Quantitative Easing) bullets, but as global growth continues to slow, he has openly acknowledged his willingness to dig into his toolbox for additional measures under the right circumstances, including QE3.

- The PBOC (People’s Bank of China) surprised many observers by employing its second rate cut in less than a month. The PBOC lowered its one-year lending rate by 0.31% to 6%.

- The ECB (European Central Bank) lowered its key lending rate by 0.25% to an all-time low of 0.75% and also cut its overnight deposit rate (the equivalent of our Federal Funds rate) by 0.25% to 0%.

- Brazil’s central bank recently cut its benchmark Selic rate for the 8th time in a year to an all-time low of 8% from 12.5%.

- South Korea’s central bank lowered its key interest rates by 0.25% to 3%, its first such action in three years.

- The BOE (Bank of England) raised its quantitative easing goal by 50 billion pounds (~$78 billion).

Source (Calafia Beach Pundit)

Source (Calafia Beach Pundit)

Banks Disqualified from Libor Games: As a result of the Libor (London Interbank Offered Rate) rigging scandal, Barclays CEO Robert Diamond resigned from the bank and agreed to forfeit $31 million in bonus money. Libor is a measure of what banks pay to borrow from each other and, perhaps more importantly, it acts as a measuring stick for determining rates on mortgages and other financial contracts. In an attempt to boost the perceived financial strength of their financial condition, multiple banks artificially manipulated the calculation of the Libor rate. Ironically, this scandal likely helped consumers with lower mortgage and credit card rates.

Rates Running Backwards: Sports betting on teams and events is measured by point spreads and numerical odds. In the global debt markets, betting is measured by interest rates. So while losing, debt-laden countries like Greece and Spain have seen their interest rates explode upwards, winning, fiscally responsible countries (including Switzerland, Austria, Denmark, Netherlands, Germany, and Finland) have seen their bond yields turn NEGATIVE. That’s right, investors are earning a negative return. Rather than making a bet on higher yielding bonds, many investors are flocking to the perceived safety of these interest-losing bonds (see chart below). This game cannot last forever, especially for individual and institutional investors who require income to meet liquidity and return requirements.

Source (The Financial Times)

China Wins GDP Gold Medal but No World Record: China currently leads in both the Olympic Games gold medal count (China 13 vs. U.S. 9 through July 31st) and GDP competition. Given the fiscal and monetary stimulus measures the government has implemented, it appears their economy is bottoming. Despite the tremendous anxiety over China’s growth, China’s National Bureau of Statistics just announced a +7.6% Q2 GDP growth rate (see chart below), down from +8.1% in Q1. Although this is the slowest growth since the global financial crisis, Even though this was the slowest GDP growth rate in over three years, most countries would die for this level of growth. Adding evidence to the bottoming storyline, HSBC recently reported the preliminary Chinese PMI manufacturing index rose to 49.5 in July, up from 48.2 in June – the highest reading since early this year (February).

Source (Calafia Beach Pundit)

Higgs Wins God Particle Gold: Michael Phelps and Missy Franklin are not the only people to win gold medals in their fields. Peter Higgs and fellow scientists had 50-years of their physics research validated when the Large Hadron Collider discovered the long-sought Higgs boson (a.k.a., the “god particle”). The collider, located on the Franco-Swiss border, measured approximately 17 miles in length, took years to build, and cost about $8 billion to finish. Pundits are declaring the unearthing of Higgs boson as the greatest scientific discovery since the sequencing of the human genome. Higgs’s gold medal may just come in the form of a Nobel Prize in Physics.

Source (The Financial Times)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Barclays or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Markets Race Out of 2012 Gate

Article includes excerpts from Sidoxia Capital Management’s 2/1/2012 newsletter. Subscribe on right side of page.

Equity markets largely remained caged in during 2011, but U.S. stocks came racing out of the gate at the beginning of 2012. The S&P 500 index rose +4.4% in January; the Dow Jones Industrials climbed +3.4%; and the NASDAQ index sprinted out to a +8.0% return. Broader concerns have not disappeared over a European financial meltdown, high U.S. unemployment, and large unsustainable debts and deficits, but several key factors are providing firmer footing for financial race horses in 2012:

• Record Corporate Profits: 2012 S&P operating profits were recently forecasted to reach a record level of $106, or +9% versus a year ago. Accelerating GDP (Gross Domestic Product Growth) to +2.8% in the fourth quarter also provided a tailwind to corporations.

• Mountains of Cash: Companies are sitting on record levels of cash. In late 2011, U.S. non-financial corporations were sitting on $1.73 trillion in cash, which was +50% higher as a percentage of assets relative to 2007 when the credit crunch began in earnest.

• Employment Trends Improving: It’s difficult to fall off the floor, but since the unemployment rate peaked at 10.2% in October 2009, the rate has slowly improved to 8.5% today. Data junkies need not fret – we have fresh new employment numbers to look at this Friday.

• Consumer Optimism on Rise: The University of Michigan’s consumer sentiment index showed optimism improved in January to the highest level in almost a year, increasing to 75.0 from 69.9 in December.

• Federal Reserve to the Rescue: Federal Reserve Chairman, Ben Bernanke, and the Fed recently announced the extension of their 0% interest rate policy, designed to assist economic expansion, through the end of 2014. In addition, Bernanke did not rule out further stimulative asset purchases (a.k.a., QE3 or quantitative easing) if necessary. If executed as planned, this dovish stance will extend for an unprecedented six year period (2008 -2014).

Europe on the Comeback Trail?

Source: Calafia Beach Pundit

Europe is by no means out of the woods and tracking the day to day volatility of the happenings overseas can be a difficult chore. One fairly easy way to track the European progress (or lack thereof) is by following the interest rate trends in the PIIGS countries (Portugal, Ireland, Italy, Greece, and Spain). Quite simply, higher interest rates generally mean more uncertainty and risk, while lower interest rates mean more confidence and certainty. The bad news is that Greece is still in the midst of a very complex restructuring of its debt, which means Greek interest rates have been exploding upwards and investors are bracing for significant losses on their sovereign debt investments. Portugal is not in as bad shape as Greece, but the trends have been moving in a negative direction. The good news, as you can see from the chart above (Calafia Beach Pundit), is that interest rates in Ireland, Italy and Spain have been constructively moving lower thanks to austerity measures, European Central Bank (ECB) actions, and coordination of eurozone policies to create more unity and fiscal accountability.

Political Horse Race

Source: Real Clear Politics via The Financial Times

The other horse race going on now is the battle for the Republican presidential nomination between former Massachusetts governor Mitt Romney and former House of Representatives Speaker Newt Gingrich. Some increased feistiness mixed with a little Super-Pac TV smear campaigns helped whip Romney’s horse to a decisive victory in Florida – Gingrich ended up losing by a whopping 14%. Unlike traditional horse races, we don’t know how long this Republican primary race will last, but chances are this thing should be wrapped up by “Super Tuesday” on March 6th when there will be 10 simultaneous primaries and caucuses. Romney may be the lead horse now, but we are likely to see a few more horses drop out before all is said and done.

Flies in the Ointment

As indicated previously, although 2012 has gotten off to a strong start, there are still some flies in the ointment:

• European Crisis Not Over: Many European countries are at or near recessionary levels. The U.S. may be insulated from some of the weakness, but is not completely immune from the European financial crisis. Weaker fourth quarter revenue growth was suffered by companies like Exxon Mobil Corp (XOM), Citigroup Inc. (C), JP Morgan Chase & Co (JPM), Microsoft Corp (MSFT), and IBM, in part because of European exposure.

• Slowing Profit Growth: Although at record levels, profit growth is slowing and peak profit margins are starting to feel the pressure. Only so much cost-cutting can be done before growth initiatives, such as hiring, must be implemented to boost profits.

• Election Uncertainty: As mentioned earlier, 2012 is a presidential election year, and policy uncertainty and political gridlock have the potential of further spooking investors. Much of these issues is not new news to the financial markets. Rather than reading stale, old headlines of the multi-year financial crisis, determining what happens next and ascertaining how much uncertainty is already factored into current asset prices is a much more constructive exercise.

Stocks on Sale for a Discount

Source: Calafia Beach Pundit

A lot of the previous concerns (flies) mentioned is not new news to investors and many of these worries are already factored into the cheap equity prices we are witnessing. If everything was all roses, stocks would not be selling for a significant discount to the long-term averages.

A key ratio measuring the priceyness of the stock market is the Price/Earnings (P/E) ratio. History has taught us the best long-term returns have been earned when purchases were made at lower P/E ratio levels. As you can see from the 60-year chart above (Calafia Beach Pundit), stocks can become cheaper (resulting in lower P/Es) for many years, similar to the challenging period experienced through the early 1980s and somewhat analogous to the lower P/E ratios we are presently witnessing (estimated 2012 P/E of approximately 12.4). However, the major difference between then and now is that the Federal Funds interest rate was about 20% back in the early-’80s, while the same rate is closer to 0% currently. Simple math and logic tell us that stocks and other asset-based earnings streams deserve higher prices in periods of low interest rates like today.

We are only one month through the 2012 financial market race, so it much too early to declare a Triple Crown victory, but we are off to a nice start. As I’ve said before, investing has arguably never been as difficult as it is today, but investing has also never been as important. Inflation, whether you are talking about food, energy, healthcare, leisure, or educational costs continue to grind higher. Burying your head in the sand or stuffing your money in low yielding assets may work for a wealthy few and feel good in the short-run, but for much of the masses the destructive inflation-eroding characteristics of purported “safe investments” will likely do more damage than good in the long-run. A low-cost diversified global portfolio of thoroughbred investments that balances income and growth with your risk tolerance and time horizon is a better way to maneuver yourself to the investment winner’s circle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in XOM, MSFT, JPM, IBM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

A Serious Situation in Jackson Hole

Source: Daily Fill

Federal Reserve Chairman Ben Bernanke graced his presence once again upon the glorious skyline of the Grand Tetons in Jackson Hole, Wyoming for the annual Economic Policy Symposium organized by the Federal Reserve Bank of Kansas City. The event has been made famous for Bernanke’s famous 2010 QE2 (quantitative easing) speech and he once again did his best to confuse people this year with his cryptic and masterful “Fed Speak” techniques. While reporters from around the globe covered the event, we at Investing Caffeine were fortunate enough to access MTV’s Jersey Shore cast member’s, Mike “The Situation” Sorrentino, exclusive interpretation of Bernanke’s speech. Here’s how “The Situation” translated Bernanke’s talk:

Mr Bernanke: “The financial crisis and the subsequent slow recovery have caused some to question whether the United States, notwithstanding its long-term record of vigorous economic growth, might not now be facing a prolonged period of stagnation.”

The Situation’s Take: “Looks like this economy is f’d up big time. This is gonna be some sick dry-spell.”

Mr. Bernanke: “The pace of recovery in the United States has, for the most part, proved disappointing thus far… it is clear that the recovery from the crisis has been much less robust than we had hoped.”

The Situation’s Take: “These economist chumps would have more luck chucking darts at Snooki’s booty than they would hitting their predictions. Let’s call Joey, my booky, and I’ll show you how the Situation works his magic.”

Mr. Bernanke: “Manufacturing production in the United States has risen nearly 15 percent since its trough, driven substantially by growth in exports. Indeed, the U.S. trade deficit has been notably lower recently than it was before the crisis, reflecting in part the improved competitiveness of U.S. goods and services.”

The Situation’s Take: “Trashed girls at the clubs like me a lot more after some drinks, just like the trashed value of the dollar makes foreigners like our exports.”

Mr. Bernanke: “Temporary factors, including the effects of the run-up in commodity prices on consumer and business budgets and the effect of the Japanese disaster on global supply chains and production, were part of the reason for the weak performance of the economy in the first half of 2011; accordingly, growth in the second half looks likely to improve as their influence recedes.”

The Situation’s Take: “When I’m chasing tail, hangovers temporarily slow me down sometimes too. What Big Ben and the U.S. financial situation needs is some 5-Hour Energy drink, a tanning session, and a quick pump of the biceps at the gym.”

Mr. Bernanke: “We indicated that economic conditions–including low rates of resource utilization and a subdued outlook for inflation over the medium run–are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.”

The Situation’s Take: “I feel you Benjamin. Keeping rates low is like having a permanent 2-for-1 happy hour at the club for the next two years. Now, that’s what I’m talkin’ bout!”

Mr. Bernanke: “The Federal Reserve has a range of tools that could be used to provide additional monetary stimulus. The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools as appropriate to promote a stronger economic recovery.”

The Situation’s Take: “I hear ya Ben. Sometimes you gotta pull out the secret weapon, just like I have to flash my secret weapon…boom – these monster abs! Keep those secret tools coming Benny. I don’t care if it’s QE3, QE4, QE-infinity – just don’t listen to the haters.”

Mr. Bernanke: “I have confidence that our European colleagues fully appreciate what is at stake in the difficult issues they are now confronting and that, over time, they will take all necessary and appropriate steps to address those issues effectively and comprehensively.”

The Situation’s Take: “Everybody needs to put faith in their wingman sometimes.”

Mr. Bernanke: “Our K-12 educational system, despite considerable strengths, poorly serves a substantial portion of our population.”

The Situation’s Take: “Don’t mess with me Benny. C’mon, just take a look at me. I’m living proof of how our schools are the bomb! After all, the Situation learned his best moves with the ladies during high school.”

Mr. Bernanke: “Most of the economic policies that support robust economic growth in the long run are outside the province of the central bank…As I have emphasized on previous occasions, without significant policy changes, the finances of the federal government will inevitably spiral out of control.”

Situation’s Take: “Don’t let them politician punks make you do all the heavy lifting and flush the economy down the toilet. Looking this good ain’t easy and fixing the U.S. of A. ain’t either.”

Federal Reserve Chairman Ben Bernanke covered a lot of ground in his Jackson Hole speech. Given the mounds of complex data and dismal state of our economic situation, who better to translate and provide cutting edge analysis than Mike “The Situation” Sorrentino. Investing Caffeine appreciates the exclusive access given to us, but now I’m off to more important tasks at hand – before I do my fist pumping at the club tonight, I need to go work my abs and apply a nice spray tan.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: For those taking this article seriously, please look up “parody” in the dictionary. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

{kind=link}