Posts tagged ‘behavioral finance’

Cleaning Out Your Investment Fridge

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2016). Subscribe on the right side of the page for the complete text.

Summer is quickly approaching, but it’s not too late to do some spring cleaning. This principle not only applies to your cluttered refrigerator with stale foods but also your investment portfolio with moldy investments. In both cases, you want to get rid of the spoiled goods. It’s never fun discovering a science experiment growing in your fridge.

Over the last three months, the stock market has been replenished after a rotten first two months of the year (S&P 500 index was down -5.5% January through February). The +1.5% increase in May added to a +6.6% and +0.3% increase in March and April (respectively), resulting in a three month total advance in stock prices of +8.5%. Not surprisingly, the advance in the stock market is mirroring the recovery we have seen in recent economic data.

After digesting a foul 1st quarter economic Gross Domestic Product (GDP) reading of only +0.8%, activity has been smelling better in the 2nd quarter. A recent wholesome +3.4% increase in April durable goods orders, among other data points, has caused the Atlanta Federal Reserve Bank to raise its 2nd quarter GDP estimate to a healthier +2.9% growth rate (from its prior +2.5% forecast).

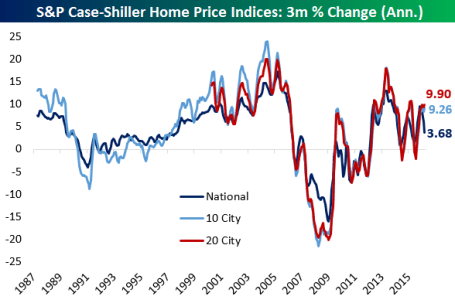

Consumer spending, which accounts for roughly 70% of our country’s economic activity, has been on the rise as well. The improving employment picture (5.0% unemployment rate last month) means consumers are increasingly opening their wallets and purses. In addition to spending more on cars, clothing, movies, and vacations, consumers are also doling out a growing portion of their income on housing. Housing developers have cautiously kept a lid on expansion, which has translated into limited supply and higher home prices, as evidenced by the Case-Shiller indices charted below.

Source: Bespoke

Spoiling the Fun?

While the fridge may look like it’s fully stocked with fresh produce, meat, and dairy, it doesn’t take long for the strawberries to get moldy and the milk to sour. Investor moods can sour quickly too, especially as they fret over the impending “Brexit” (British Exit) referendum on June 23rd when British voters will decide whether they want to leave the European Union. A “yes” exit vote has the potential of roiling the financial markets and causing lots of upset stomachs.

Another financial area to monitor relates to the Federal Reserve’s monetary policy and its decision when to further increase the Federal Funds interest rate target at its June 14th – 15th meeting. With the target currently set at an almost insignificantly small level of 0.25% – 0.50%, it really should not matter whether Chair Janet Yellen decides to increase rates in June, July, September and/or November. Considering interest rates are at/near generational lows (see chart below), a ¼ point or ½ point percentage increase in short-term interest rates should have no meaningfully negative impact on the economy. If your fridge was at record freezing levels, increasing the temperature by a ¼ or ½ degree wouldn’t have a major effect either. If and when short-term interest rates increase by 2.0%, 3.0%, or 4.0% in a relatively short period will be the time to be concerned.

Source: Scott Grannis

Keep a Fresh Financial Plan

As mentioned earlier, your investments can get stale too. Excess cash sitting idly earning next-to-nothing in checking, savings, CDs, or in traditional low-yielding bonds is only going to spoil rapidly to inflation as your savings get eaten away. In the short-run, stock prices will move up and down based on frightening but insignificant headlines. However, in the long-run, the more important issues are determining how you are going to reach your retirement goals and whether you are going to outlive your savings. This mindset requires you to properly assess your time horizon, risk tolerance, income needs, tax situation, estate plan, and other unique circumstances. Like a balanced diet of various food groups in your refrigerator, your key personal financial planning factors are dependent upon you maintaining a properly diversified asset allocation that is periodically rebalanced to meet your long-term financial goals.

Whether you are managing your life savings, or your life-sustaining food supply, it’s always best to act now and not be a couch potato. The consequences of sitting idle and letting your investments spoil away are a lot worse than letting the food in your refrigerator rot away.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Market Inefficiencies Give Black-Eyes to Classic Economists

Markets are efficient. Individuals behave rationally. All information is reflected in prices. Huh…are you kidding me? These are the beliefs held by traditional free market economists (“rationalists”) like Eugene Fama (Economist at the University of Chicago and a.k.a. the “Father of the Efficient Market Hypothesis”). Striking blows to the rationalists are being thrown by “behavioralists” like Richard Thaler (Professor of Behavioral Science and Economics at the University of Chicago), who believes emotions often lead to suboptimal decisions and also thinks efficient market economics is a bunch of hogwash.

Individual investors, pensions, endowments, institutional investors, governments, were left sifting through the rubble in the aftermath of the 2008-2009 financial crisis because common beliefs were thrown out the window. Experts and non-experts are still attempting to figure out how this mass destruction occurred and how it can be prevented in the future. Economists, as always, are happy to throw in their two cents. Right now traditional free market economists like Fama have received a black eye and are on the defensive – forced to explain to the behavioral finance economists (Thaler et. al.) how efficient markets could lead to such a disastrous outcome.

Religion and Economics

Like religious debates, economic rhetoric can get heated too. Religion can be divided up in into various categories (e.g., Christianity, Islam, Judaism, Hinduism, Buddhism, and other), or more simply, religion can be divided into those who believe in a god (theism) and those who do not (atheism). There are multiple economic categorizations or schools as well (e.g., Keynsians, monetarists, libertarians, behavioral finance economists, etc.). Debates and disagreements across the rainbow of religions and economic schools have been going on for centuries, and the arrival and departure of the 2008-09 financial crisis further ignited the battle between the “behavioralists” (behavioral finance economists) and the “rationalists” (traditional free market economists).

Behavioral Finance on the Offensive

In the efficient market world of the “rationalists,” market prices reflect all available information and cannot be wrong at any moment in time. Effectively, individuals are considered human calculators that optimize everything from interest rates and costs to benefits and inflation expectations in every decision. What classic economists fail to account for are the emotional and behavioral flaws made by individuals.

Claiming financial market decisions are not impacted by emotions becomes more challenging to defend, if you consider the countless irrational anomalies occurring throughout history. Consider the following:

- Tulip Mania: Bubbles are nothing new – they have persisted for hundreds of years. Let’s reflect on the tulip bulb mania of the 1600s. For starters, I’m not sure how classic economists can explain the irrational exchanging of homes or a thousand pounds of cheese for a tulip bulb? Or how peak prices of $60,000+ in inflation-adjusted dollars were paid for a bulb at the time (C-Cynical)? These are tough questions to answer for the rationalists.

- Flash Crash: Seeing multiple stocks and Exchange Traded Funds (ETFs) temporarily plummet -99% in minutes is not exactly the sign of an efficient market. Stalwarts like Procter & Gamble also collapsed -37%, only to rebound minutes later near pre-collapse levels. All this volatility doesn’t exactly ooze with efficiency (see Making Millions in Minutes).

- Negative Interest Rates: Plenty of so-called pundits are arguing that equity markets are expensive, but what about the $8 trillion in negative interest rate bonds? Prices for many of these bonds are astronomical. Paying someone to take my money doesn’t make a lot of sense, but trillions in speculative investments are still being made today.

- Technology and Real Estate Bubbles: Both of these asset classes were considered “can’t lose” investments in the late 1990s and mid-2000s, respectively. Many tech stocks were trading at unfathomable values (more than 100 x’s annual profits) and homebuyers were inflating real estate prices because little-to-no money was required for the purchases.

- ’87 Crash: October 19, 1987 became infamously known as “Black Monday” since the Dow Jones Industrial Average plunged over -22% in one day (-508 points), the largest one-day percentage decline ever.

The ever-growing list of nonsensical anomalies only makes the rationalists’ jobs that much tougher in refuting the illogical behavior. Risk aversion has been alive and well in the post financial crisis environment as wild swings have resulted from a wide range of concerns, including: the U.S. debt downgrade; Arab Spring; potential Greek exit from the EU; Sequestration; Fed Taper Tantrum; Obamacare implementation; Russian invasion of Ukraine; Gaza conflict; Fukashima disaster; Ebola outbreak; Ferguson tensions; Paris/San Bernardino/Brussels terrorist attacks; China recessionary fears; oil price volatility; Mideast turmoil – ISIS expansion; Federal Reserve rate increases; and many other worries. Often, the human lizard brain is what leads to sub-optimal decision making. Maybe the rationalists can use the same efficient market framework to help explain to my wife why I ate a whole box of Twinkies in one sitting?

Rationalist Rebuttal

The growing list of market inefficiencies has given the rationalists a black eye, but they are not going down without a fight. Here are some quotes from Fama and fellow Chicago rationalist pals:

On the Crash-Related Attacks from Behavioralists: Behavioralists say traditional economics has failed in explaining the irrational decisions and actions leading up to the 2008-09 crash. Fama states, “I don’t see this as a failure of economics, but we need a whipping boy, and economists have always, kind of, been whipping boys, so they’re used to it. It’s fine.”

Rationalist Explanation of Behavioral Finance: Fama doesn’t deny the existence of irrational behavior, but rather believes rational and irrational behaviors can coexist. “Efficient markets can exist side by side with irrational behavior, as long as you have enough rational people to keep prices in line,” notes Fama. John Cochrane treats behavioral finance as a pseudo-science by replying, “The observation that people feel emotions means nothing. And if you’re going to just say markets went up because there was a wave of emotion, you’ve got nothing. That doesn’t tell us what circumstances are likely to make markets go up or down. That would not be a scientific theory.”

Description of Panics: “Panic” is not a term included in the dictionary of traditional economists. Fama retorts, “You can give it the charged word ‘panic,’ if you’d like, but in my view it’s just a change in tastes.” Calling these anomalous historic collapses a “change in tastes” is like calling American Idol judge Simon Cowell, “diplomatic.” More likely, what’s really happening is these severe panics are driving investors’ changes in preferences.

Throwing in White Towel Regarding Crash: Not all classic economists are completely digging in their heels like Fama and Cochrane. Gary Becker, a rationalist disciple, acknowledged the blind-siding of the 2008-2009 financial crisis when he admitted, “Economists as a whole didn’t see it coming. So that’s a black mark on economics, and it’s not a very good mark for markets.”

Settling Dispute with Lab Rats

The boxing match continues, and the way the behavioralists would like to settle the score is through laboratory tests. In the documentary Mind Over Money, numerous laboratory experiments are run using human subjects to tease out emotional behaviors. Here are a few examples used by behavioralists to bolster their arguments:

- The $20 Bill Auction: Zach Burns, a professor at the University of Chicago, conducted an auction among his students for a $20 bill. Under the rules of the game, as expected, the highest bidder wins the $20 bill, but as an added wrinkle, Burns added the stipulation that the second highest bidder receives nothing but must still pay the amount of the losing bid. Traditional economists would conclude nobody would bid higher than $20. See the not-so rational auction results here at minute 1:45.

- $100 Today or $102 Tomorrow? This was the question posed to a group of shoppers in Chicago, but under two different scenarios. Under the first scenario, the individuals were asked whether they would prefer receiving $100 in a year from now (day 366) or $102 in a year and one additional day (day 367)? Under the second scenario, the individuals were asked whether they would prefer receiving $100 today or $102 tomorrow? The rational response to both scenarios would be to select $102 under both scenarios. See how the participants responded to the questions here at minute 4:30.

Rationalist John Cochrane is not fully convinced. “These experiments are very interesting, and I find them interesting, too. The next question is, to what extent does what we find in the lab translate into how people…understanding how people behave in the real world…and then make that transition to, ‘Does this explain market-wide phenomenon?,’” he asks.

As I alluded to earlier, religion, politics, and economics will never fall under one universal consensus view. The classic rationalist economists, like Eugene Fama, have in aggregate been on the defensive and taken a left-hook in the eye for failing to predict and cohesively explain recurring market inefficiencies, including the financial crash of 2008-09. On the other hand, Richard Thaler and his behavioral finance buds will continue on the offensive, consistently swinging at the classic economists over this key economic mind versus money dispute.

See Complete Mind Over Money Program

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PG and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ceasefires & Investor Quagmires

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (March 1, 2015). Subscribe on the right side of the page for the complete text.

Considering the following current event headlines, who would have guessed the stock market is trading near record, all-time highs and the NASDAQ index breaking 5,000 for the first time since the year 2000?

- Russia Lies Over Ukraine Ceasefire

- ISIS Beheadings and Jihadi John

- Strong Dollar, Weak Global Economy

- Fed’s Yellen: Rate Rise & Inflation

- Iranian Negotiations & Nuclear Weapons

- Grexit: The Likelihood of Greece’s Exit from the Euro

- The Chinese Bubble Pops

- Ebola and the Fear Epidemic

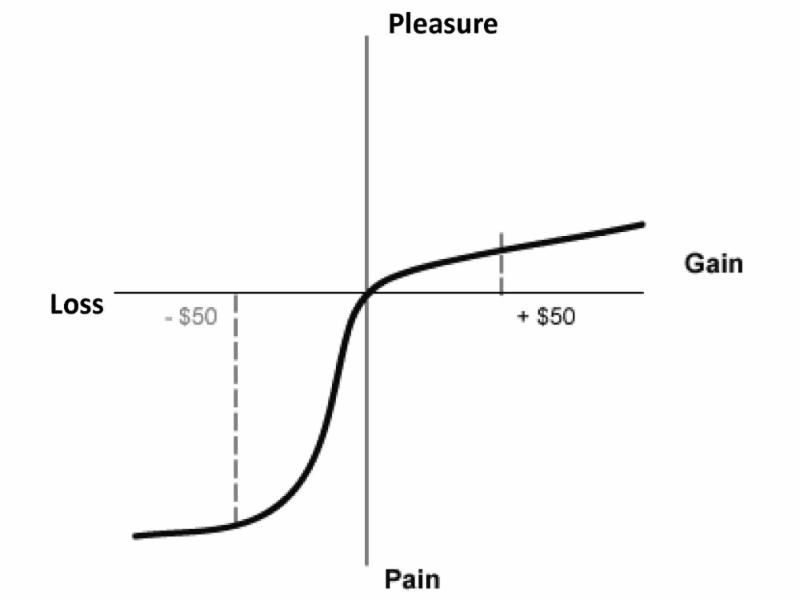

After reading all these depressing stories, I feel more like taking a Prozac pill than I do venturing into the investing world. Unfortunately, in the media world, the overarching motto driving the selection of published stories is, “If it bleeds, it leads!” Plainly and simply, bad news sells. The media outlets prey on our human behavioral shortcomings. Specifically, people feel the pain from losses at a rate more than double the feelings of pleasure (see Controlling the Lizard Brain and chart below).

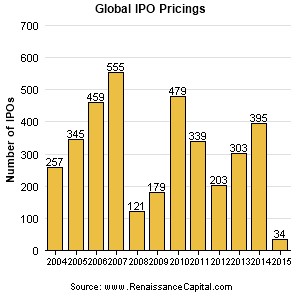

This phenomenon leaves Americans and the overall investing public choking on the daily doom and gloom headlines. Investor skepticism caused by the 2008-2009 financial crisis is evidenced by historically low stock ownership statistics and stagnant equity purchase flow data. Talk of another stock bubble has been introduced again now that the NASDAQ is approaching 5,000 again, but we are not seeing signs of this phenomenon in the IPO market (Initial Public Offering) – see chart below. IPOs are on the rise, but the number of filings is more than -50% below the peak of 845 IPOs seen in the late 1990s when former Federal Reserve Chairman Alan Greenspan made his famous “irrational exuberance” speech (see also Irrational Exuberance Deja Vu and chart below).

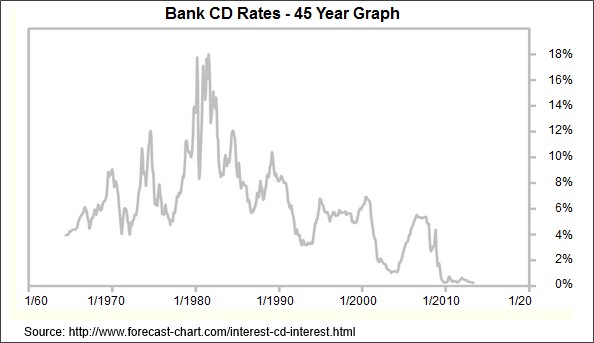

Uggh! 0.08% Really?

Compounding the never-ending pessimism problem is the near-0% interest rate environment. Times are long gone when you could earn 18% on a certificate of deposit (see chart below). Today, you can earn 0.08% on a minimum $10,000 investment in a Bank of America (BAC) Certificate of Deposit (CD). Invest at that rate for more than a decade and you will have almost accumulated a $100 (~1%) – probably enough for a single family meal…without tip. To put these paltry interest rates into perspective, the U.S. stock market as measured by the S&P 500 index was up a whopping +5.5% last month and the Dow Jones Industrials climbed +5.6% (+968 points to 18,133). Granted, last month’s S&P 500 percentage increase was the largest advance since 2011, but if I wanted to earn an equivalent +5.5% return by investing in that Bank of America CD, it would take me to age 100 years old before I earned that much!

Globally, the interest rate picture doesn’t look much prettier. In fact, the negative interest rate bonds offered in Switzerland and other neighboring countries, including France and Germany, have left investors in these bonds with guaranteed losses, if held to maturity (see also Draghi Beer Goggles).

Money Seeking Preferred Treatment

Investors and followers of mine have heard me repeatedly declare that “money goes where it is treated best.” When many investments are offering 0% (or negative yields), it comes as no surprise to me that dividend paying stocks have handily outperformed the overall bond market in recent years. Hard to blame someone investing in certain stocks offering between 2-6% in dividends when the alternative is offered at or near 0%.

While at Sidoxia we are still finding plenty of opportunities in the equity markets, I want to extend the reminder that not everyone can (or should) increase their equity allocation because of personal time horizon and risk tolerance constraints. Regardless, the current, restricting global financial markets are highlighting the scarcity of investment alternatives available.

As we will continue to be bombarded with more cease fires, quagmires and other bleeding headlines, investors will be better served by ignoring the irrelevant headlines and instead create a long-term financial plan with an asset allocation designed to meeting their personal goals. By following this strategy, you can let the dooms-dayers bleed while you succeed.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Market Champagne Sits on Ice

Summer may be coming to an end, but the heat in the stock market has not cooled down, as the stock market registered its hottest August performance in 14 years (S&P 500 index up +3.8%). With these stellar results, one would expect the corks to be popping, cash flowing into stocks, and the champagne flowing. However, for numerous reasons, we have not seen this phenomenon occur yet. Until the real party begins, I suppose the champagne will stay on ice.

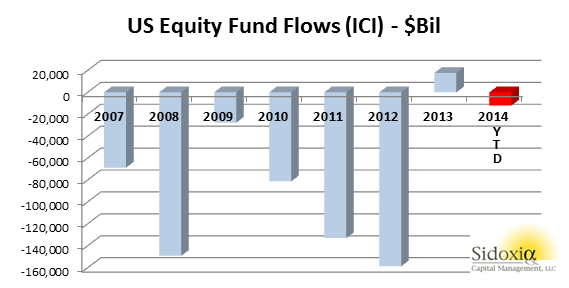

At the end of last year, I wrote further about the inevitable cash tsunami topic in an article entitled, “Here Comes the Dumb Money.” At that point in time, stocks had remarkably logged an approximate +30% return, and all indications were pointing towards an upsurge of investor interest in the stock market. So far in 2014, the party has continued as stocks have climbed another +8.4% for the year, but a lot of the party guests have not arrived yet. With the water temperature in the pool being so enticing, one would expect everyone to jump in the stock market pool. Actually, we have seen the opposite occur as -$12 billion has been pulled out of U.S. stock funds so far in 2014 (see ICI chart below).

How can the market be up +8.4% when money is coming out of stocks? For starters, companies are buying stock by the hundreds of billions of dollars. An estimated $480 billion of stock was purchased by corporations last year via share repurchase authorizations. Adding fuel to the stock fire are near record low interest rates. The ultra-low rates have allowed companies to borrow money at unprecedented rates for the purpose of not only buying back chunks of stock, but also buying the stock of whole companies (Mergers & Acquisitions). Thomson Reuters estimates that M&A activity in 2014 has already reached $2.2 trillion, up more than +70% compared to the same period last year.

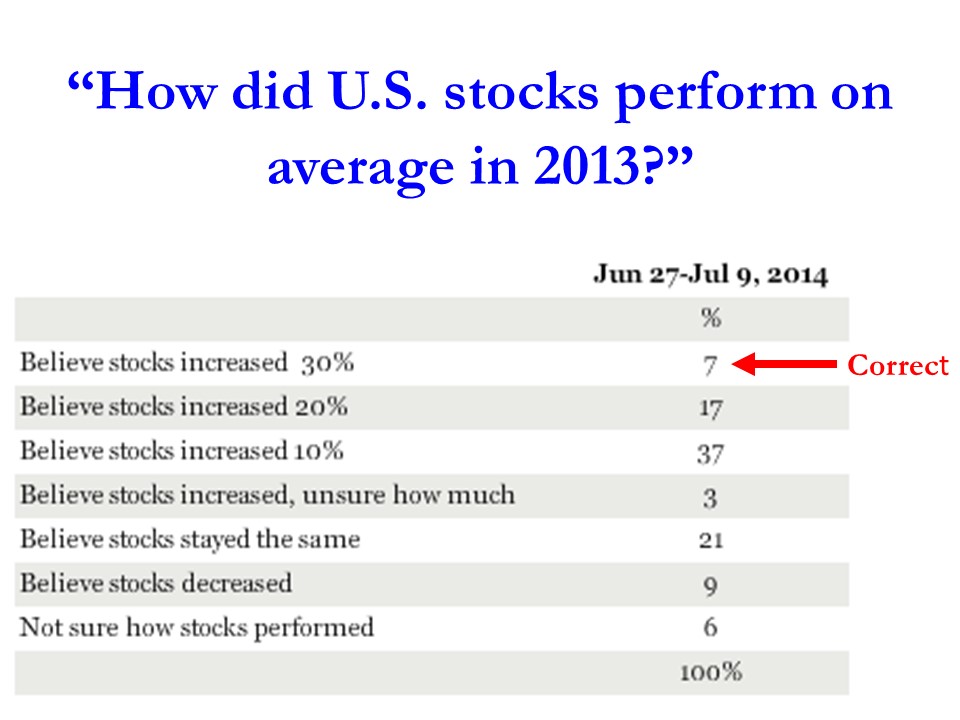

Another factor contributing to the lackluster appetite for stocks is the general public’s apathy and disinterest in the market. This disconnected sentiment was captured beautifully by a recent Gallup survey, which asked people the following question:

As you can see, only 7% of the respondents realized that stocks were up by more than +30% in 2013. More specifically, the S&P 500 (Large Cap) index was up +29.6%, S&P 600 (Small Cap) +39.7%, and the S&P 400 (Mid Cap) +31.6% (all percentages exclude dividends). Despite these data points, if taken with near 15-year low household stock ownership data, the results prove sentiment is nowhere near the euphoric phases reached before the 2000 bubble burst or the 2006-2008 real estate collapse.

Beyond the scarring effects of the 2008-2009 financial crisis, tempered moods regarding stocks can also be attributed to fresher geopolitical concerns (i.e., military tensions in Ukraine, Islamic extremists in Iraq, and missile launches from the Gaza Strip). The other area of never-ending anxiety is Federal Reserve monetary policy. The stock market, which has tripled in value from early 2009, has skeptics continually blaming artificial Quantitative Easing/QE policies (stimulative bond purchases) as the sole reason behind stocks advance. With current Fed Chair Janet Yellen pulling 70% of the QE punch bowl away (bond purchases now reduced to $25 billion per month), the bears are having a difficult time explaining rising stock prices and declining interest rates. Once all $85 billion in monthly QE purchases are expected to halt in October, skeptics will have one less leg on their pessimistic stool to sit on.

Economy and Profits Play Cheery Tune

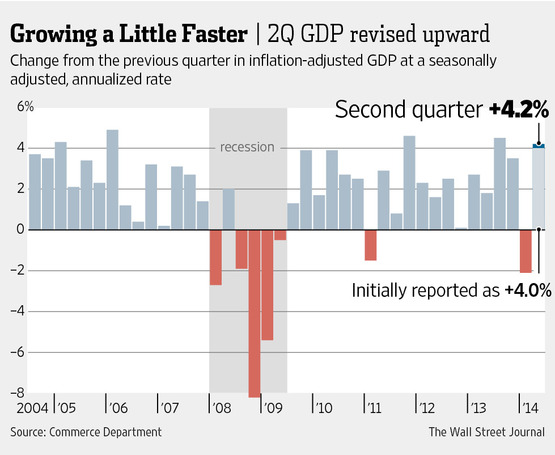

While geopolitical and Federal Reserve clouds may be preventing many sourpusses from joining the stock party, recent economic and corporate data have party attendees singing a cheery tune. More specifically, the broadest measurement of economic activity, GDP (Gross Domestic Product), came in at a higher-than-expected level of +4.2% for the 2nd quarter (see Wall Street Journal chart below).

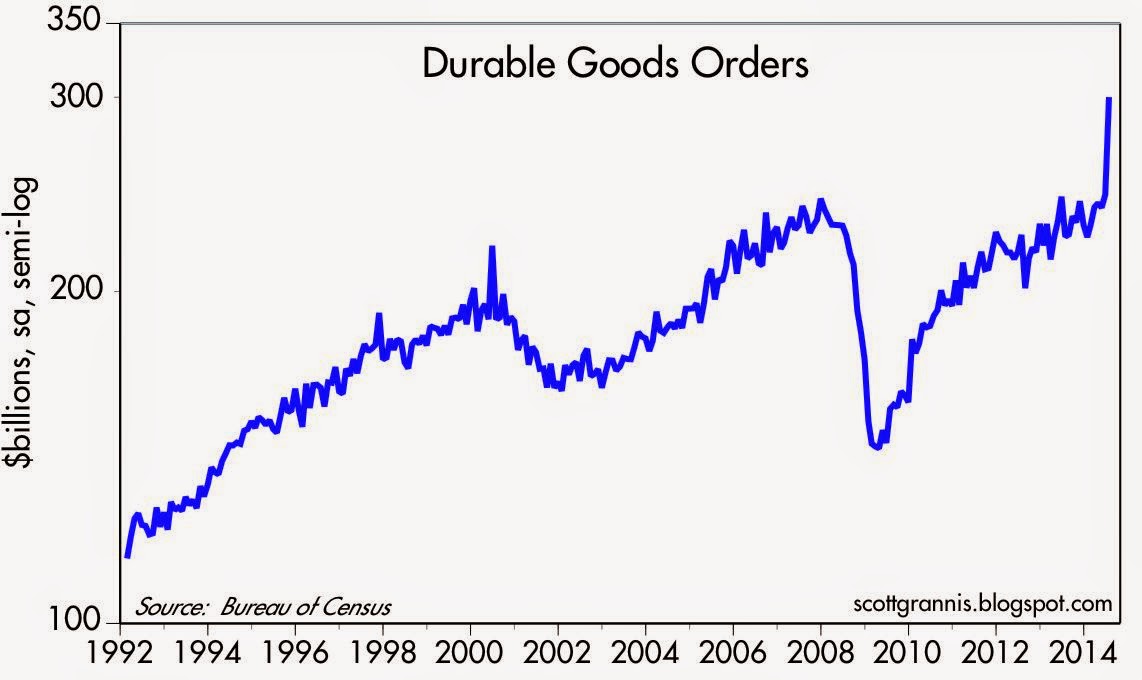

Moreover, the spike in July’s Durable Goods orders also paints a healthy economic picture (see chart below). The data is volatile (i.e., Boeing Co orders – BA), nevertheless, CEO confidence is on the rise. Improved confidence results in executives opening up their wallets and investing more into their businesses.

Source: Calafia Beach Pundit

Last but not least, the lifeblood of appreciating stock prices (earnings/profits) have been accelerating higher. In the most recent quarterly results, we saw a near doubling of the growth rate from 1st quarter’s +5% growth rate to 2nd quarter’s +10% growth rate (see chart below).

Source: Dr. Ed’s Blog

With the S&P 500 continuing to make new record highs despite scary geopolitical and Federal Reserve policy concerns, the stock market party is still waiting for guests to arrive. When everyone arrives and jumps in the pool, it will be time to pop the corks and sell. Until then, there is plenty of appreciation potential as the champagne sits on ice.

The Thrill of the Chase

Men (and arguably women to a lesser extent) enjoy the process of hunting for a mate. Chasing the seemingly unattainable event aligns with man’s innate competitive nature. But the quest for the inaccessible is not solely limited to dating. When it comes to other aspirational categories, humans also want what they cannot have because they revel in a challenge. Whether it’s a desirable job, car, romantic partner, or even an investment, people bask in the pursuit.

For many investment daters and trading speculators, 2008-2009 was a period of massive rejection. Rather than embracing the losses as a new opportunity, many wallowed in cash, CDs, bonds, and/or gold. This strategy felt OK until the massive 5-year bull market went on a persistent, upward tear beginning in 2009. Now, as the relentless bull market has continued to set new all-time record highs, the negative sentiment cycle has slowly shifted in the other direction. Back in 2009, many investors regretted owning stocks and as a result locked in losses by selling at depressed prices. Now, the regret of owning stocks has shifted to remorse for not owning stocks. Missing a +23% annual return for five years, while getting stuck with a paltry 0.25% return in a savings account or 3-4% annual return achieved in bonds, can harm the psyche and make savers bitter.

Greed hasn’t fully set in like we witnessed in the late period of the 1990s tech boom, but nevertheless, some of the previous overly cautious “sideliners” feel compelled to now get into the stock game (see Get Out of Stocks!*) or increase their equity allocation. Like a desperate, testosterone-amped teen chasing a prom date, some speculators are chasing stocks, regardless of the price paid. As I’ve noted before, the overall valuation of the stock market seems quite reasonable (see PE ratio chart in Risk Aversion Declining – S. Grannis), despite selective pockets of froth popping up in areas like biotech stocks, internet companies, and junk bonds.

Even if chasing is a bad general investment practice, in the short-run, chasing stocks (or increasing equity allocations) may work because overall prices of stocks remain about half the price they were at the 2000 bubble peak (see Siegel Bubblicious article). How can stocks be -50% off when stock prices today (S&P 500) are more than +25% higher today than the peak in 2000? Plain and simply, it’s the record earnings (see It’s the Earnings Stupid). In the latest Sidoxia newsletter we highlighted the all-time record corporate profits, which are conveniently excluded from most stock market discussions in the blogosphere and other media outlets.

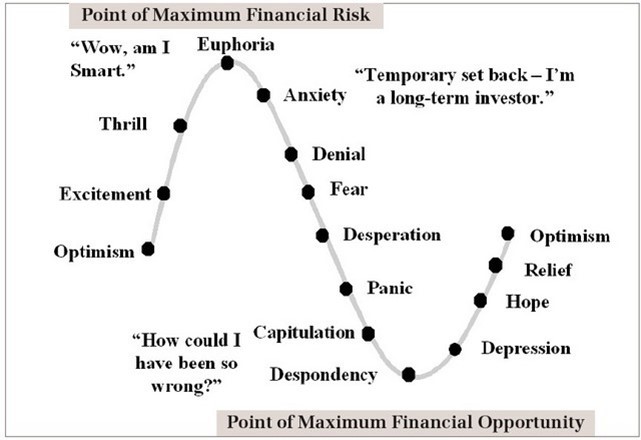

The Investor’s Emotional Roller Coaster (Perceived Risk vs Actual Risk)

The “Thrill of the Chase” is but a single emotion on the roller coaster sentiment spectrum (see Barry Ritholtz chart in Sentiment Cycle of Fear and Greed). The problem with the above chart is many investors confuse actual risk from perceived risk. Many investors perceive the “euphoric” stage of an economic cycle (top of the chart) as low-risk, when in actuality this point reflects peak risk. One can look back to the late 1990s and early 2000 when technology shares were priced at more than 100x years in earnings and every hairdresser, cabdriver and relative were plunging their life savings into stocks. The good news from my vantage point is we are a ways from that euphoric state (asset fund flows and consumer confidence are but a few data points to support this assertion).

The key to reversing the sentiment roller coaster is to follow the thought process of investment greats who learned to avoid euphoria in up markets:

“I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.” -Peter Lynch

“Be fearful when others are greedy, and be greedy when others are fearful.” –Warren Buffett

While the “Thrill of the Chase” can seem exciting and a rational strategy at the time, successful long-term investors are better served by remaining objective, unemotional, and numbers-driven. If you don’t have the time, interest, or emotional fortitude to be disciplined, then find an experienced investment manager or advisor to assist you. That will make your emotional roller coaster ride even more thrilling.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

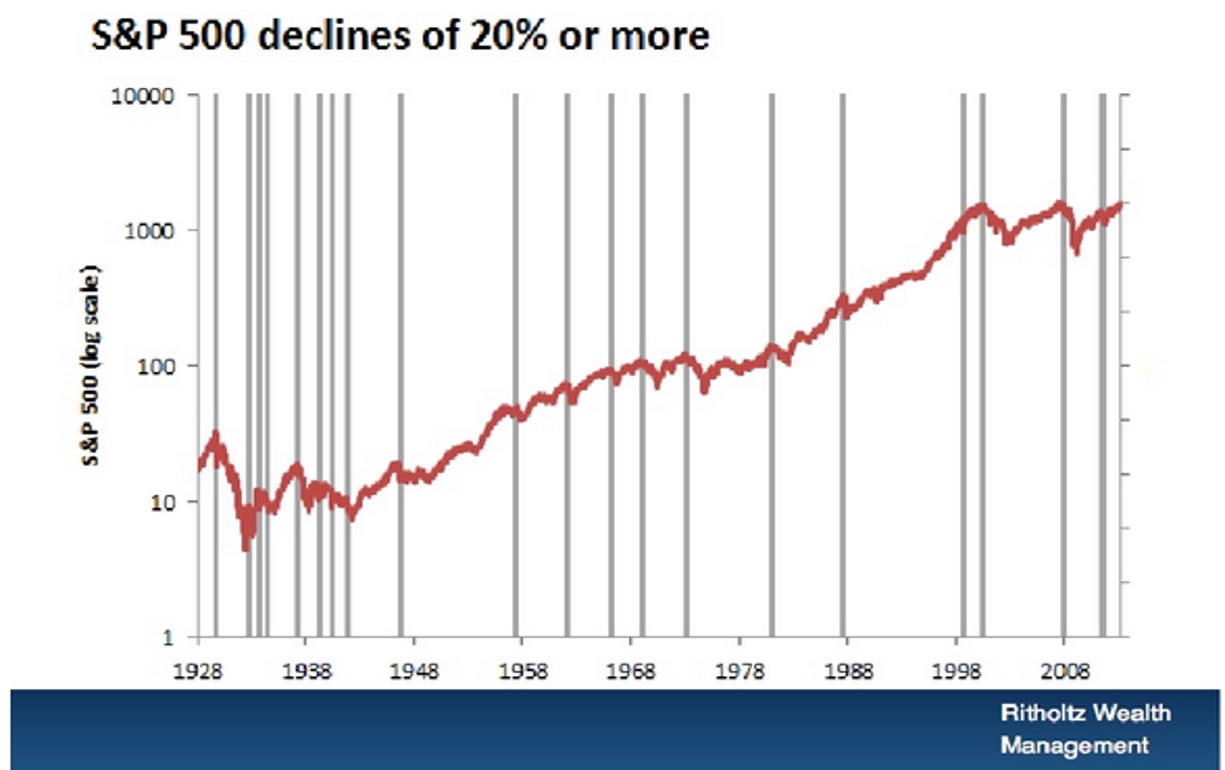

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Searching for the Market Boogeyman

With the stock market reaching all-time record highs (S&P 500: 1900), you would think there would be a lot of cheers, high-fiving, and back slapping. Instead, investors are ignoring the sunny, blue skies and taking off their rose-colored glasses. Rather than securely sleeping like a baby (or relaxing during a three-day weekend) with their investment accounts, people are biting their fingernails with clenched teeth, while searching for a market boogeyman in their closets or under their beds.

If you don’t believe me, all you have to do is pick up the paper, turn on the TV, or walk over to the office water cooler. An avalanche of scary headlines that are spooking investors include geopolitical concerns in Ukraine & Thailand, slowing housing statistics, bearish hedge fund managers (i.e., Tepper Einhorn, Cooperman), declining interest rates, and collapsing internet stocks. In other words, investors are looking for things to worry about, despite record corporate profits and stock prices. Peter Lynch, the manager of the Magellan Fund that posted +2,700% in gains from 1977-1990, put short-term stock price volatility into perspective:

“You shouldn’t worry about it. You should worry what are stocks going to be 10 years from now, 20 years from now, 30 years from now.”

Rather than focusing on immediate stock market volatility and other factors out of your control, why not prioritize your time on things you can control. What investors can control is their asset allocation and spending levels (budget), subject to their personal time horizons and risk tolerances. Circumstances always change, but if people spent half the time on investing that they devoted to planning holiday vacations, purchasing a car, or choosing a school for their child, then retirement would be a lot less stressful. After realizing 99% of all the short-term news is nonsensical noise, the next important realization is stocks are volatile securities, which frequently go down -10 to -20%. As much as amateurs and professionals say or think they can profitably predict these corrections, they very rarely can. If your stomach can’t handle the roller-coaster swings, then you shouldn’t be investing in the stock market.

Bear-markets generally coincide with recessions, and since World War II, Americans experience about two economic contractions every decade. And as I pointed out earlier in A Series of Unfortunate Events, even during the current massive bull market, a recession has not been required to suffer significant short-term losses (e.g., Flash Crash, Greece, Arab Spring, Obamacare, Cyprus, etc.). Seasoned veterans understand these volatile periods provide incredible investment opportunities. As Warren Buffett states, “Be fearful when others are greedy, and be greedy when others are fearful.” Fear and panic may be behind us, but skepticism is still firmly in place. Buying during current skepticism is still not a bad thing, as long as greed hasn’t permeated the masses, which remains the case today.

Overly emotional people that make investment decisions with their gut do more damage to their savings accounts than conservative, emotional investors who understand their emotional shortcomings. On the other hand, the problem with investing too conservatively, for those that have longer-term time horizons (10+ years), is multi-pronged. For starters, overly conservative investments made while interest rate levels hover near historical lows lead to inflationary pressures gobbling up savings accounts. Secondly, the low total returns associated with excessively conservative investments will result in a later retirement (e.g., part-time Wal-Mart greeter in your 80s), or lower quality standard of living (e.g., macaroni & cheese dinners vs. filet mignon).

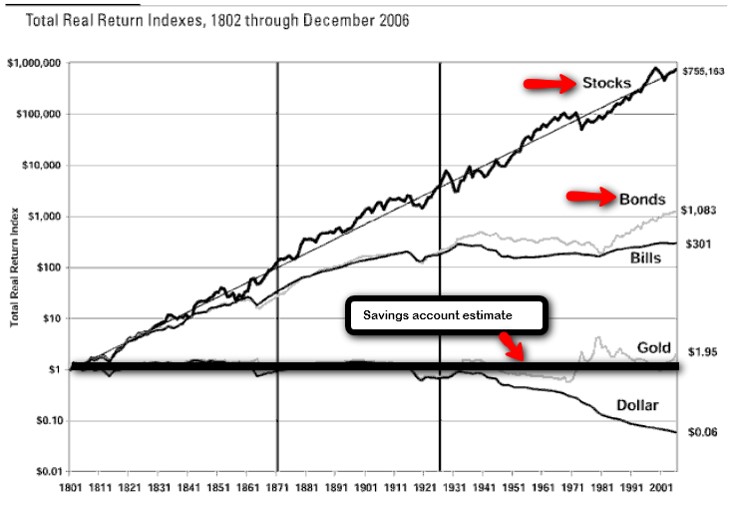

Most people say they understand the trade-offs of risk and return. Over the long-run, low-risk investments result in lower returns than high risk investments (i.e., bonds vs. stocks). If you look at the following chart and ask anyone what their preferred path would be over the long-run, almost everyone would select the steep, upward-sloping equity return line.

Source: Betterment.com / Stocks for the Long Run

Yet, stock ownership and attitudes towards stocks remain at relatively low and skeptical levels (see Gallup survey in Markets Soar and Investors Snore). It’s true that attitudes are changing at a glacial pace and bond outflows accelerated in 2013, but more recently stock inflows remain sporadic and scared money is returning to bonds. Even though it has been over five years, the emotional scars from 2008-2009 apparently still need some time to heal.

Investing in stocks can be very scary and hazardous to your health. For those millions of investors who realize they do not hold the emotional fortitude to withstand the ups and downs, leave the worrying responsibilities to the experienced advisors and investment managers like me. That way you can focus on your job and retirement, while the pros can remain responsible for hunting and slaying the boogeyman.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Controlling the Investment Lizard Brain

“Normal fear protects us; abnormal fear paralyses us.”

– Martin Luther King, Jr.

Investing is challenging enough without bringing emotions into the equation. Unfortunately, humans are emotional, and as a result investors often place too much reliance on their feelings, rather than using objective information to drive rational decision making.

What causes investors to make irrational decisions? The short answer: our “amygdala.” Author and marketer Seth Godin calls this almond-shaped tissue in the middle of our head, at the end of the brain stem, the “lizard brain” (video below). Evolution created the amygdala’s instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions.

Over time, the threat of lions eating people in our modern lives has dramatically declined, but the human’s “lizard brain” is still running in full gear, worrying about other fear-inducing warnings like Iran, Syria, Obamacare, government shutdowns, taxes, Cyprus, sequestration, etc. (see Series of Unfortunate Events)

When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.

With this genetically programmed tendency of constantly fearing the next lion or stock market crash, how does one control their lizard brain from making sub-optimal, rash investment decisions? Well, the first thing you should do is turn off the TV. And by turning off the TV, I mean stop listening to talking head commentators, economists, strategists, analysts, neighbors, co-workers, blogger hacks, newsletter writers, journalists, and other investing “wannabes”. Sure, you could throw my name into the list of people to ignore if you wanted to, but the difference is, at least I have actually invested real money for over 20 years (see How I Managed $20,000,000,000.00), whereas the vast majority of those I listed have not. But don’t take my word for it…listen or read the words of other experienced investors Warren Buffett, Peter Lynch, Ron Baron, John Bogle, Phil Fisher, and other investment titans (see also Sidoxia Hall of Fame). These investment legends have successful long-term investment track records and they lived through wars, recessions, financial crises, and other calamities…and still managed to generate incredible returns.

Another famed investor, William O’Neil, summed this idea nicely by adding the following:

“Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

The Harmful Consequence of Brain on Pain

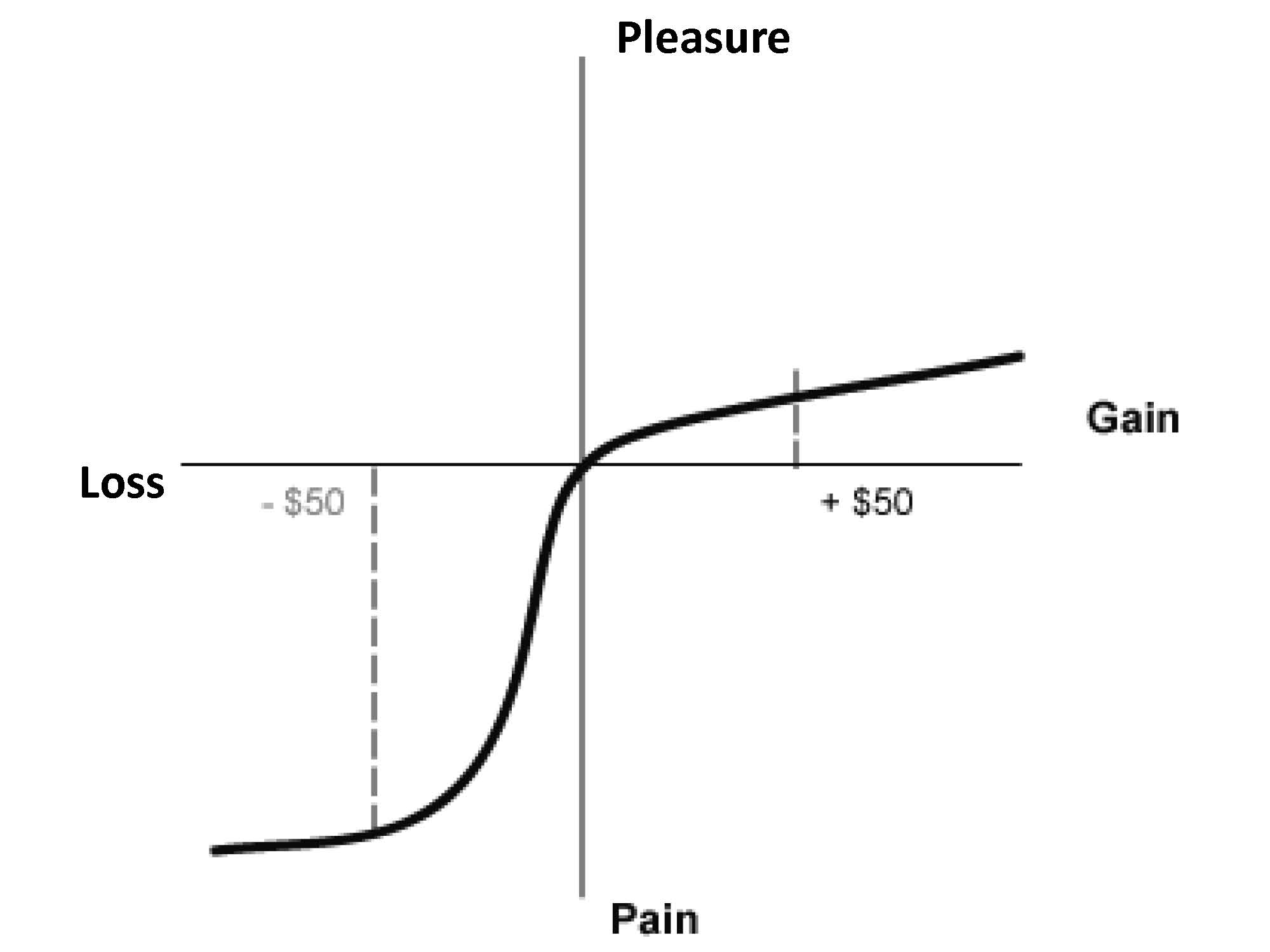

Besides forcing damaging decisions, another consequence of our lizard brain is its ability to distort reality. Behavioral economists Daniel Kahneman (Nobel Prize winner) and Amos Tversky through their research demonstrated the pain of $50 loss is more than twice as painful as the pleasure from $50 gain (see Pleasure/Pain Principle). Common sense would dictate our brains would treat equivalent scenarios in a proportional manner, but as the chart below shows, that is not the case:

Source: Investopedia

Kahneman adds to the decision-making relationship of the amygdala and prefrontal cortex by describing the concepts of instinctual and deliberative choices in his most recent book, Thinking Fast and Slow (see Decision Making on Freeways).

Optimizing Risk

Taking excessive risks in technology stocks in the 1990s or in housing in the mid-2000s was very damaging to many investors, but as we have seen, our lizard brains can cause investors to become overly risk averse. Over the last five years, many people have personally experienced the ill effects of unwarranted conservatism. Investment great Sir John Templeton summed up this risk by stating, “The only way to avoid mistakes is not to invest – which is the biggest mistake of all.”

Every person has a different perception and appetite for risk. The optimal amount of risk taken by any one investor should be driven by their unique liquidity needs and time horizon…not a perceived risk appetite. Typically risk appetites go up as markets peak, and conservatism reaches a fearful apex near market bottoms – the opposite tendency of rational decision making. Besides liquidity and time horizon, a focus on valuation coupled with diversification across asset class (stocks/bonds), geography (domestic/international), size (small/large), style (value/growth) is critical in controlling risk. If you can’t determine your personal, optimal risk profile, then find an experienced and knowledgeable investment advisor to assist you.

With the advent of the internet and mobile communication, our brains and amygdala continually get bombarded with fearful stimuli, leading to disastrous decision-making and damaging portfolio outcomes. Turning off the TV and selectively choosing the proper investment advice is paramount in keeping your amygdala in check. Your lizard brain may protect you from getting eaten by a lion, but falling prey to this structural brain flaw may eat your investment portfolio alive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sitting on the Sidelines: Fear & Selective Memory

Fear is a motivating (or demotivating) emotion that can force individuals into suboptimal actions. The two main crashes of the 2000s (technology & housing bubbles) coupled with the mini-crises (e.g., flash crash, European crisis, debt ceiling, sequestration, fiscal cliff, etc.) have scared millions of investors and trillions of dollars to sit on the sidelines. Financial paralysis may be great in the short-run for bruised psyches and egos, but for the passive onlookers, the damage to retirement accounts can be crippling.

Selective memory is a great coping mechanism for those investors sitting on the sidelines as well. Purposely forgetting your wallet at a group dinner may be beneficial in the near-term, but repeated incidents will result in lost friends over the long-run. Similarly, most gamblers frequenting casinos tend to pound their chests when bragging about their wins, however they tend to conveniently forget about all the losses. These same reality avoidance principles apply to investing.

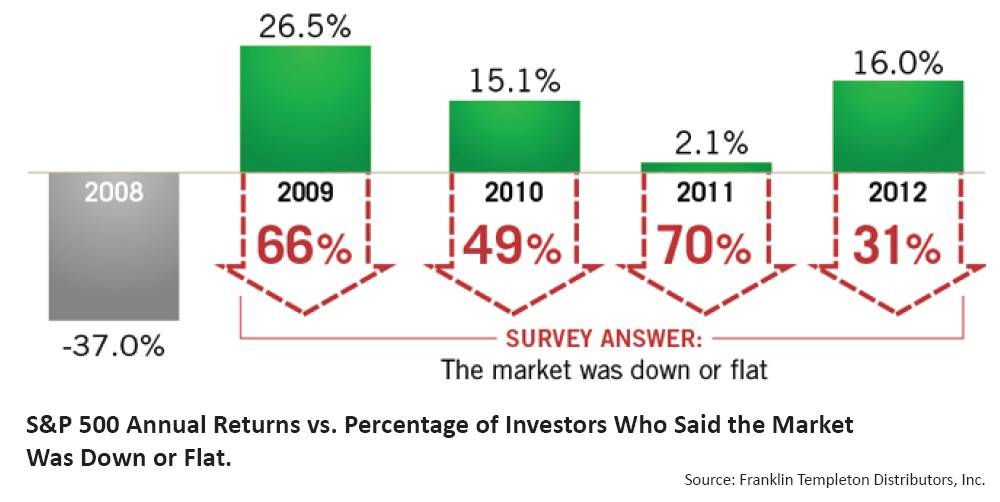

A recent piece written by CEO Bill Koehler at Tower Wealth Managers, entitled The Fear Bubble highlights a survey conducted by Franklin Templeton. In the study, investors were asked how the stock market performed in 2009-2012. As you can see from the chart below, perception is the polar opposite of reality (actual gains far exceeded perceived losses):

Source: Franklin Templeton via Tower Wealth Managers

With so many investors sitting on the sidelines in cash or concentrated in low-yielding bonds and gold, I suppose the results shouldn’t be too surprising. Once again, selective memory serves as a wonderful tool to bury the regrets of missing out on a financial market recovery of a lifetime.

Humans also have a predisposition to seek out people who share similar views, even though accumulating different viewpoints ultimately leads to better decisions. Morgan Housel at The Motley Fool just wrote an article, Putting a Gap Between You and Stupid, explaining how individuals should seek out others who can help protect them from harmful biases. A scientific study referenced in the article showed how the functioning of biased brains literally shuts down:

“During the 2004 presidential election, psychologist Drew Westen of Emory University and his colleagues studied the brains of 15 “committed” Democrats and 15 “committed” Republicans with an MRI scanner. Each group was shown a collection of contradictory statements made by George W. Bush and John Kerry. Not surprisingly, the partisans were quick to call out contradictions made by the opposing party, and made up all kinds of justifications to rationalize quotes made by their own side’s candidate. But here’s what’s scary: The participants weren’t just being stubborn. Westen found that areas of their brains that control reasoning and logic virtually shut down when confronted with a conflicting view of their preferred candidate.”

Rather than letting emotions rule the day, the proper approach is to stick to unbiased numbers like valuations, yields, fees, and volatility. If you continually make mistakes; you aren’t disciplined enough; or you don’t like investing; then find a trusted advisor who uses an objective financial approach. Opportunistically taking advantage of volatility, instead of knee-jerk reactions is the preferred approach. For those people sitting on the sidelines and using selective memory, you may feel better now, but you will eventually have to get in the game, if you don’t want to lose the retirement account game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Jobs and the DMV Economy

If you have ever gone to get your driver’s license at the Department of Motor Vehicles (DMV)…you may still be waiting in line? It’s a painful but often a mandatory process, and in many ways the experience feels a lot like the economic recovery we currently have been living through over the last four years. Steady progress is being made, but in general, people hardly notice the economy moving forward.

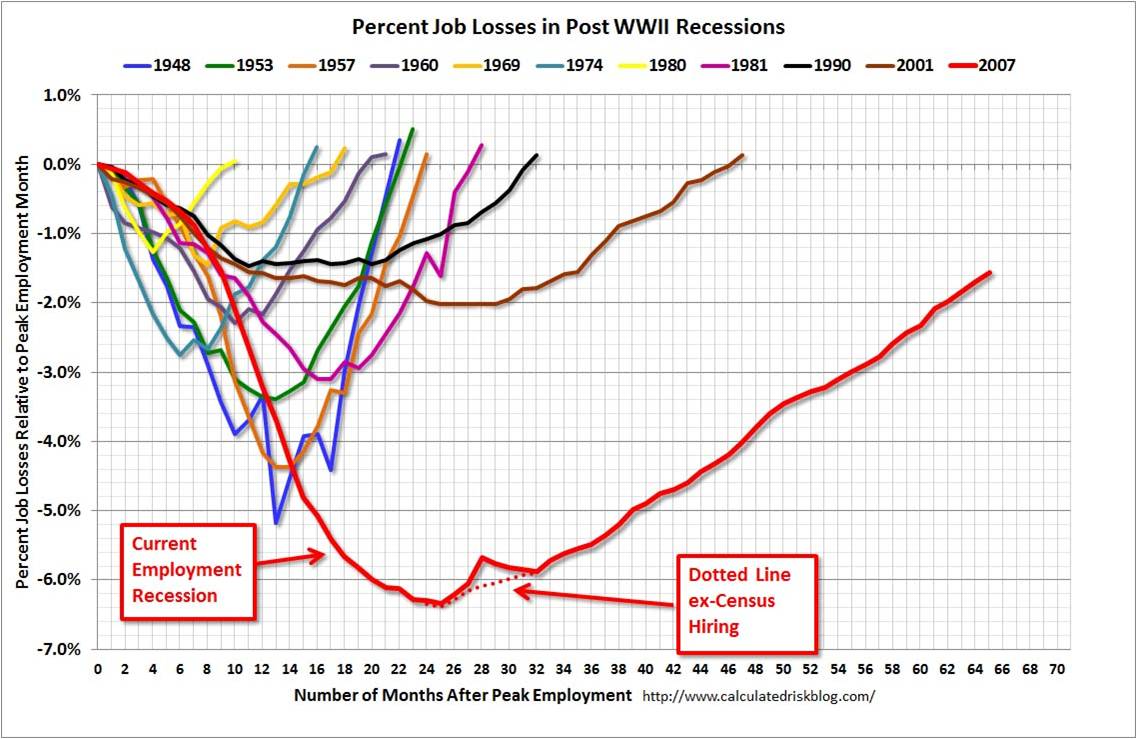

My geographic neighbor and blogger here in Orange County, California (Bill McBride – Calculated Risk) has some excellent visuals that compare our sluggish DMV economy with previous economic cycles dating back to 1948:

Source: Calculated Risk

As you can see from the chart above, the current economic recovery (red-line), as measured by job losses, is the slowest comeback in more than a half-century. Basically, over a two year period, the U.S. lost about nine million jobs, and during the following three years the economy regained approximately seven million of those jobs – still digging out of the hole. Last Friday’s June jobs report was welcomed, as it showed net jobs of +195,000 were added during the month, and importantly the previous two months were revised higher by another +70,000 jobs. These data points combined with last month’s Fed’s QE3 tapering comments by Ben Bernanke help explain why the continued rout in 10 year Treasury rates has continued in recent weeks, propelling the benchmark rate to 2.71% – almost double the 1.39% rate hit last year amidst continued European financial market concerns.

As with most recessions or crashes, the bursting of the bubble (i.e., damage) occurs much faster than the inflation (i.e., recovery), and McBride’s time series clearly shows this fact:

Source: Calculated Risk

While pessimists point to the anemic pace of the current recovery, the glass half-full people (myself included) appreciate that the sluggish rebound is likely to last longer than prior recoveries. There are two other key dynamics underlying the reported employment figures:

- Continued Contraction in Government Workers: Excessive government debt and deficits have led to continued job losses – state and local job losses appear to be stabilizing but federal cuts are ongoing.

- Decline in the Labor Force Participation Rate: Discouraged workers and aging Baby Boomer demographics have artificially lowered the short-term unemployment figures because fewer people are looking for work. If economic expansion accelerates, the participation contraction trend is likely to reverse.

Skepticism Reigns Supreme

Regardless of the jobs picture and multi-year expansion, investors and business managers alike remain skeptical about the sustainability of the economic recovery. Anecdotally I encounter this sentiment every day, but there are other data points that bolster my assertion. Despite the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (see Value Walk) and investments in the stock market are the lowest in 15 years (see Gallup poll chart below):

Source: Gallup

Why such skepticism? Academic research in behavioral finance highlights innate flaws in human decision-making processes. For example, humans on average weigh losses twice as much as gains as economist and Nobel prizewinner Daniel Kahneman explains in his book Thinking Fast and Slow (see Investing Caffeine article: Decision Making on Freeways and in Parking Lots). Stated differently, the losses from 2008-2009 are still too fresh in the minds of Americans. Until the losses are forgotten, and/or the regret of missing gains becomes too strong, many investors and managers will fearfully remain on the sideline.

The speed of our economic recovery is as excruciatingly agonizing, and so is waiting in line at the DMV. The act of waiting can be horrific, but obtaining a driver’s license is required for driving and investing is necessary for retirement. If you don’t want to go to investing jail, then you better get in the investing line now before job growth accelerates, because you don’t want to be sent to the back of the line where you will have to wait longer.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}