Posts tagged ‘banks’

Greece: The Slow Motion, Multi-Year Train Wreck

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2015). Subscribe on the right side of the page for the complete text.

Watching Greece fall apart over the last five years has been like watching a slow motion train wreck. To many, this small country of 11 million people that borders the Mediterranean, Aegean, and Ionian Seas is known more for its Greek culture (including Zeus, Parthenon, Olympics) and its food (calamari, gyros, and Ouzo) than it is known for financial bailouts. Nevertheless, ever since the financial crisis of 2008-2009, observers have repeatedly predicted the debt-laden country will default on its €323 billion mountain of obligations (see chart below – approximately $350 billion in dollars) and subsequently exit the 19-member eurozone currency membership (a.k.a.,”Grexit”).

Source: MoneyMorning.com and CNN

Now that Greece has failed to repay less than 1% of its full €240 billion bailout obligation – the €1.5 billion payment due to the IMF (International Monetary Fund) by June 30th – the default train is coming closer to falling off the tracks. Whether Greece will ultimately crash itself out of the eurozone will be dependent on the outcome of this week’s surprise Greek referendum (general vote by citizens) mandated by Prime Minister Alexis Tsipras, the leader of Greece’s left-wing Syriza party. By voting “No” on further bailout austerity measures recommended by the European Union Commission, including deeper tax increases and pension cuts, the Greek people would effectively be choosing a Grexit over additional painful tax increases and deeper pension cuts.

Ouch!

And who can blame the Greeks for being a little grouchy? You might not be too happy either if you witnessed your country experience an economic decline of greater than 25% (see Greece Gross Domestic Product chart below); 25% overall unemployment (and 50% youth unemployment); government worker cuts of greater than 20%; and stifling taxes to boot. Sure, Greeks should still shoulder much of the blame. After all, they are the ones who piled on $100s of billions of debt and overspent on the pensions of a bloated public workforce, and ran unsustainable fiscal deficits.

Source: TradingEconomics.com

For any casual history observers, the current Greek financial crisis should come as no surprise, especially if you consider the Greeks have a longstanding habit of not paying their bills. Over the last two centuries or so, since the country became independent, the Greek government has spent about 90 years in default (almost 50% of the time). More specifically, the Greeks defaulted on external sovereign debt in 1826, 1843, 1860, 1894 and 1932.

The difference between now and past years can be explained by Greece now being a part of the European Union and the euro currency, which means the Greeks actually do have to pay their bills…if they want to remain a part of the common currency. During past defaults, the Greek central bank could easily devalue their currency (the drachma) and fire up the printing presses to create as much currency as needed to pay down debts. If the planned Greek referendum this week results in a “No” vote, there is a much higher probability that the Greek government will need to dust off those drachma printing presses.

“Perspective People”

Protest, riots, defaults, changing governments, and new currencies make for entertaining television viewing, but these events probably don’t hold much significance as it relates to the long-term outlook of your investments and the financial markets. In the case of Greece, I believe it is safe to say the economic bark is much worse than the bite. For starters, Greece accounts for less than 2% of Europe’s overall economy, and about 0.3% of the global economy.

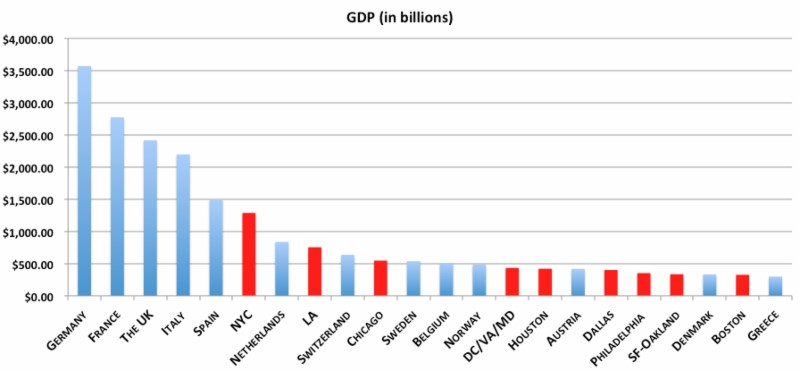

Since I live out on the West Coast, the chart below caught my fancy because it also places the current Greek situation into proper proportion. Take the city of L.A. (Los Angeles – red bar) for example…this single city alone accounts for almost 3x the size of Greece’s total economy (far right on chart – blue bar).

Give Me My Money!

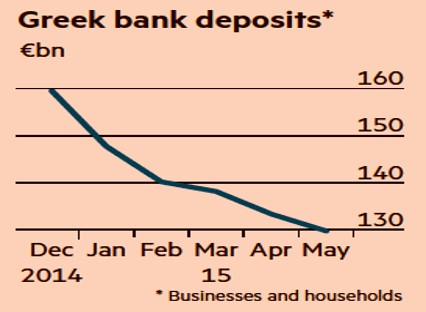

It hasn’t been a fun year for Greek banks. Depositors, who have been flocking to the banks, withdrew about $45 billion in cash from their accounts, over an eight month period (see chart below). Before the Greek government decided to mandatorily close the banks in recent days and implement capital controls limiting depositors to daily ATM withdrawals of only $66.

Source: The Financial Times

But once again, let’s put the situation into context. From an overall Greek banking sector perspective, the four largest Greek Banks (Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank) account for about 90% of all Greek banking assets. Combined, these banks currently have an equity market value of about $14 billion and assets on the balance sheets of $400 billion – these numbers are obviously in flux. For comparison purposes, Bank of America Corp. (BAC) alone has an equity market value of $179 billion and $2.1 trillion in assets.

Anxiety Remains High

Skeptical bears will occasionally acknowledge the miniscule-ness of Greece, but then quickly follow up with their conspiracy theory or domino effect hypothesis. In other words, the skeptics believe a contagion effect of an impending Grexit will ripple through larger economies, such as Italy and Spain, with crippling force. Thus far, as you can see from the chart below, Greece’s financial problems have been largely contained within its borders. In fact, weaker economies such as Spain, Portugal, Ireland, and Italy have fared much better – and actually improving in most cases. In recent days, 10-year yields on government bonds in countries like Portugal, Italy, and Spain have hovered around or below 3% – nowhere near the peak levels seen during 2008 – 2011.

Source: Business Insider

Other doubting Thomases compare Greece to situations like Lehman Brothers, Long Term Capital Management, and the subprime housing market, in which underestimated situations snowballed into much worse outcomes. As I explain in one of my newer articles (see Missing the Forest for the Trees), the difference between Greece and the other financial collapses is the duration of this situation. The Greek circumstance has been a 5-year long train wreck that has allowed everyone to prepare for a possible Grexit. Rather than agonize over every news headline, if you are committed to the practice of worrying, I would recommend you focus on an alternative disaster that cannot be found on the front page of all newspapers.

There is bound to be more volatility ahead for investors, and the referendum vote later this week could provide that volatility spark. Regardless of the news story du jour, any of your concerns should be occupied by other more important worrisome issues. So, unless you are an investor in a Greek bank or a gyro restaurant in Athens, you should focus your efforts on long-term financial goals and objectives. Ignoring the noisy news flow and constructing a diversified investment portfolio across a range of asset classes will allow you to avoid the harmful consequences of the slow motion, multi-year Greek train wreck.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Markets Soar and Investors Snore

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (August 1, 2013). Subscribe on the right side of the page for the complete text.

If you haven’t been paying close attention, or perhaps if you were taking a long nap, you may not have noticed that the stock market was up an astounding +5% in July (+78% if compounded annualized), pushing the S&P 500 index up +18% for the year to near all-time record highs. Wait a second…how can that be when that bald and grey-bearded man at the Federal Reserve has hinted at bond purchase “tapering” (see also Fed Fatigue)? What’s more, I thought the moronic politicians were clueless about our debt and deficit-laden economy, jobless recovery, imploding eurozone, Chinese real estate bubble, and impending explosion of inflation – all of which are expected to sink our grandchildren’s grandchildren into a standard of living not seen since the Great Depression. Okay, well a dash of hyperbole and sarcasm never hurt anybody.

This incessant stream of doom-and-gloom pouring over our TVs, newspapers, and internet devices has numbed Americans’ psyches. To prove my point, the next time you are talking to somebody at the water cooler, church, soccer game, or happy hour, gauge how excited your co-worker, friend, or acquaintance gets when you bring up the subject of the stock market. If my suspicions are correct, they are more likely to yawn or pass out from boredom than to scream in excitement or do cartwheels.

You don’t believe me? Reality dictates the wounds from the 2008-2009 financial crisis are still healing. Panic and fear may have disappeared, but skepticism remains in full gear, even though stocks have more than doubled in price in recent years. Here is some data to support my case there are more stock detractors than defenders:

Record Savings Deposits

|

| Source: Calafia Beach Pundit |

Although there are no signs of an impending recession, defensive cash hoarded in savings deposits has almost increased by $3 trillion since the end of the financial crisis.

Blah Consumer Confidence

|

| Source: Calafia Beach Pundit |

As you can see from the chart above, Consumer Confidence has bounced around quite a bit over the last 30+ years, but there is no sign that consumer sentiment has turned euphoric.

15-Year Low Stock Market Participation

|

|

Source: Gallup Poll

|

There has been a trickling of funds into stocks in 2013, yet participation in the stock market is at a 15-year low. Investors remain nervous.

Lack of Equity Fund Buying

|

| Source: ICI & Calafia Beach Pundit |

After a short lived tax-driven purchase spike in January, the buying trend quickly turned negative in the ensuing months. Modest inflows resumed into equity funds during the first few weeks of July (source: ICI), but the meager stock fund investments represent < 95% of 2012 positive bond flows ($15 billion < $304 billion, respectively). Moreover, these modest stock inflows pale in comparison to the hundreds of billions in investor withdrawals since 2008. See also Fund Flows Paradox – Investing Caffeine.

Decline in CNBC Viewership

In spite of the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (source: Value Walk). Stock investing apparently isn’t very exciting when prices go up.

The Hater’s Index:

And if that is not enough, you can take a field trip to the hater’s comment section of my most recent written Seeking Alpha article, The Most Hated Bull Market Ever. Apparently the stock market more than doubling creates some hostile feelings.

JOLLY & JOVIAL MEMO

Keeping the previous objective and subjective data points in mind, it’s clear to me the doom-and-gloom memo has been adequately distributed to the masses. Less clear, however, is the dissemination success of the jolly-and-jovial memo. I think Ron Bailey, an author and science journalist at Reason.com (VIDEO), said it best, “News is always bad news. Good news is simply not news…that is our [human] bias.” If you turn on your local TV news, I think you may agree with Ron. Nevertheless, there are actually plenty of happier news items to report, so here are some positive bullet points to my economic and stock market memo:

16th Consecutive Positive GDP Quarter*

|

| Source: Quartz.com |

The broadest measure of economic activity, GDP (Gross Domestic Product), was reported yesterday and came in better than expected in Q2 (+1.7%) for the 16th straight positive reported quarter (*Q1-2011 was just revised to fractionally negative). Obviously, the economists and dooms-dayers who repeatedly called for a double-dip recession were wrong.

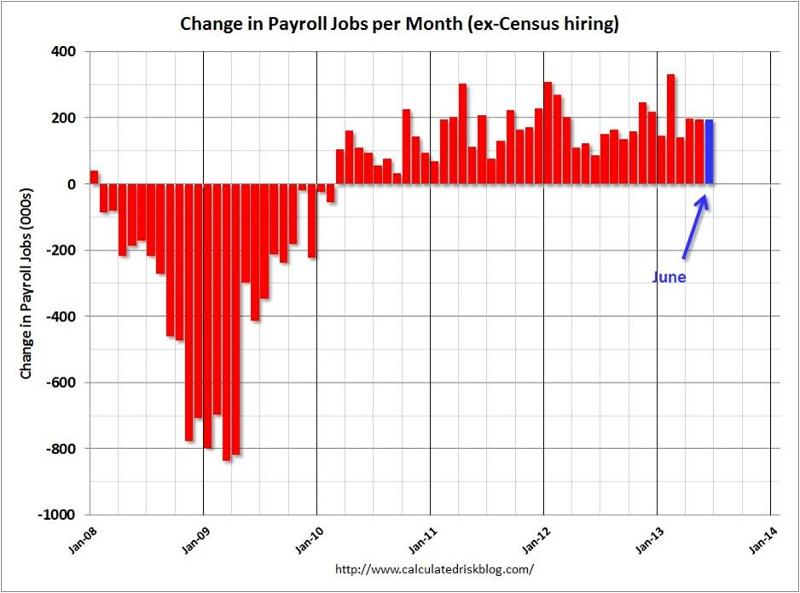

40 Consecutive Months & 7 Million Jobs

Source: Calculated Risk

The economic recovery has been painfully slow, but nevertheless, the U.S. has experienced 40 consecutive months of private sector job additions, representing +7.2 million jobs created. With about -9 million jobs lost during the most recent recession, there is still plenty of room for improvement. We will find out if the positive job creation streak will continue this Friday when the July total non-farm payroll report is released.

Housing on the Mend

|

| Source: Calafia Beach Pundit |

New home sales are up significantly from the lows; housing starts have risen about 40% over the last two years; and Case Shiller home prices rose by +12.2% in the latest reported numbers. The housing market foundation is firming.

Auto Sales Rebound

|

| Source: Calafia Beach Pundit |

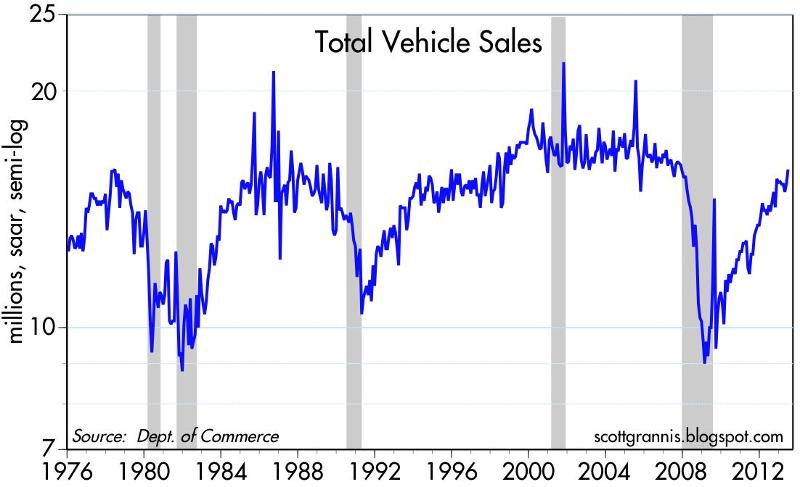

Auto sales remain on a tear, reaching an annualized level of 15.9 million vehicles, the highest since November 2007, and up +12% from June 2012. Car sales have almost reached pre-recessionary levels.

Record Corporate Profits

|

| Source: Dr. Ed’s Blog |

Optimistic forecasts have been ratcheted down, nonetheless corporate profits continue to grind to all-time record highs. As you can see, operating earnings have more than doubled since 2003. Given reasonable historical valuations in stocks, as measured by the P/E (Price Earnings) ratio, persistent profit growth should augur well for stock prices.

Bad Banks Bounce Back

Europe on the Comeback Trail

|

| Source: Calafia Beach Pundit |

There are signs of improvement in the Eurozone after years of recession. Talks of a European Armageddon have recently abated, in part because of Markit manufacturing manager purchasing statistics that are signaling expansion for the first time in two years.

Overall, corporations are achieving record profits and sitting on mountains of cash. The economy is continuing on a broad, steady recovery, however investors remain skeptical. Domestic stocks are at historic levels, but buying stocks solely because they are going up is never the right reason to invest. Alternatively, bunkering away excessive cash in useless, inflation depreciating assets is not the best strategy either. If nervousness and/or anxiety are driving your investment strategy, then perhaps now is the time to create a long-term plan to secure your financial future. However, if your goal is to soak up the endless doom-and-gloom and watch your money melt away to inflation, then perhaps you are better off just taking another nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Wall Street Meets Greed Street

For investors, the emotional pendulum swings back and forth between fear and greed. Wall Street and large financial institutions, however, are driven by one single mode…and that is greed. This is nothing new and has been going on for generations. Over the last few decades, cheap money, loose regulation, and a relatively healthy economy have given Wall Street and financial institutions free rein to take advantage of the system.

Not only did the financial industry explode, but the large got much larger. The FCIC (Financial Crisis Inquiry Commission), a government appointed commission, highlighted the following:

“By 2005, the 10 largest U.S. commercial banks held 55% of the industry’s assets, more than double the level held in 1990. On the eve of the crisis in 2006, financial sector profits constituted 27% of all corporate profits in the United States, up from 15% in 1980.”

What’s more, the obscene profits were achieved with obscene amounts of debt:

“From 1978 to 2007, the amount of debt held by the financial sector soared from $3 trillion to $36 trillion, more than doubling as a share of gross domestic product.”

Times have changed, and financial institutions have gone from victors to villains. Sluggish economic growth in developed countries and choking levels of debt have transitioned political policies from stimulus to austerity. This in turn has created social unrest. Who’s to blame for all of this? Well if you watch the evening news and Occupy Wall Street movement, it becomes very easy to blame Wall Street. Certainly, fat cat bankers deserve a portion of the blame. As one can see from the following list, over the last few years, the financial industry has paid for its sins with the help of a checkbook:

CLICK TO ENLARGE

The disgusting amount of inequitable excess is smeared across the whole industry in this tiny, partial list. Billions of dollars in penalties and disgorged assets isn’t insignificant, but besides Bernie Madoff and Raj Rajaratnam, very little time has been scheduled behind bars for the perpetrators.

Whom Else to Blame?

Are the greedy bankers and financial institution operators the only ones to blame? Without doubt, lack of government enforcement and adequate regulation, coupled with a complacent, debt-loving public, contributed to the creation of this financial crisis monster. When the economy was rolling along, there was no problem in turning a blind-eye to subversive activity. Now, the greed cannot be ignored.

At the end of the day, voters have to correct this ugly situation. The general public and Occupy Wall Street-ers need to boycott corrupt institutions and vote in politicians who will institute fair and productive regulations (NOT more regulations). Sure corporate financial lobbyists will try to tip the scales to their advantage, but a vote from a lobbyist attending a $10,000 black-tie dinner carries the same weight as a vote coming from a Occupy Wall Street-er paying $5 for a foot-long sandwich at Subway. As Thomas Jefferson stated, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.”

Investor Protocol

Besides boycotting greedy institutions and using the voting booth, what else should individuals do with their investments in this structurally flawed system? First of all, find independent firms with a fiduciary duty to act in your best interest, like an RIA firm (Registered Investment Advisor). Brokers, financial consultants, financial advisors, or whatever euphemism-of-the-day is being used for an investment product pusher, may not be evil, but their incentives typically are not aligned to protect and grow your financial future (see Fees, Exploitation, and Confusion and Letter Shell Game).

There is a lot of blame to be spread around for the financial crisis, and the intersection of Wall Street and Greed Street is a major contributing factor. However, investors and voters need to wake up to the brutal realities of our structurally flawed system and take matters into their own hands. Only then can Main Street and Wall Street peacefully coexist.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MS, UBS, C, JPM, WFC, SCHW, AMTD, BAC, GS, STT, Galleon, RBC, Subway, Amer Home, Brookside Captl, Morgan Keegan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Short-Termism & Extremism: The Death Knell of our Future

In recent times, American society has been built on a foundation of instant gratification and immediate attacks, whether we are talking about politics or economics. Often, important issues are simply presented as black or white in a way that distorts the truth and rarely reflects reality, which in most cases is actually a shade of grey. President Obama is discovering the challenges of governing a global superpower in the wake of high unemployment, a fragile economy, and extremist rhetoric from both sides of the political aisle. Rather than instituting a promise of change, President Obama has left the natives restless, wondering whether a “change for worse” is actually what should be expected in the future.

Massachusetts voters made a bold and brash statement when they elected Republican Senator Scott Brown to replace the vacated Massachusetts Senate seat of late, iconic Democratic Senator Edward Kennedy – a position he held as a Democrat for almost 47 years. Obama’s response to this Democratic body blow and his fledging healthcare reform was to go on a populist rampage against the banks with a tax and break-up proposal. Undoubtedly, financial reform is needed, but the timing and tone of these misguided proposals unfortunately does not attack the heart of the financial crisis causes – excessive leverage, lack of oversight, and irresponsible real estate loans (see also, Investing Caffeine article on the subject).

With that said, I would not write President Obama’s obituary quite yet. President Reagan was left for dead in 1982 before his policies gained traction and he earned a landslide reelection victory two years later. In order for President Obama to reverse his plummeting approval ratings and garner back some of his election campaign mojo, he needs to lead more from the center. Don’t take my word for it, review Pew Research’s data that shows Independents passing up both Republicans and Democrats. The overall sour mood is largely driven by the economic malaise experienced by all in some fashion, and unfortunately has contributed to short-termism and extremism.

Technology has flattened the world and accelerated the exchange of information globally at the speed of light. Any action, recommendation, or gaffe that deviates from the approved script immediately becomes a permanent fixture on someone’s lifetime resume. Our comments and decisions become instant fodder for the worldly court of opinion, thanks to 24/7 news cycles and millions of passionate opinions blasted immediately through cyberspace and around the globe.

Short-termism and extremism can be just as poisonous in the economic world as in the political world. This dynamic became evident in the global financial crisis. Short-termism is just another phrase for short-term profit focus, so when more and more leverage led to more and more profits and higher asset prices, the financial industry became blinded to the long-term consequences of their short-term decisions.

Solutions:

- Small Bites First: Rather than trying to ram through half-baked, massive proposals laced with endless numbers of wasteful pork barrel projects, why not focus on targeted and surgical legislation first? If education, deficit-reduction, and job creation are areas of common interest for Republicans and Democrats, then start with small legislation in these areas first. More ambitious agendas can be sought out later.

- Embrace Globalization: Based on the “law of large numbers” and the scale of the United States economy, our slice of the global economic pie is inevitably going to shrink over time. How does the $14 trillion U.S economy manage to grow if its share is declining? Simple. By eschewing protectionist policies, and embracing globalization. Developing country populations are joining modern society on a daily basis as they integrate productivity-enhancing innovations used by developed worlds for decades. In a flat world, the narrowing of the productivity gap is only going to accelerate. The question then becomes, does the U.S. want to participate in this accelerating growth of developing markets or sit idly on the sideline watching our competitors eat our lunch?

- Hail Long-Termism and Centrism: Regulations and incentives need to be instituted in such a fashion that irresponsible behavior occurring in the name of instant short-term profits is replaced with rules that induce sustainable profits and competitive advantages over our economic neighbors. Much of the financial industry is scratching and screaming in the face of any regulatory reform suggestions. The bankers’ usual response to reform is to throw out scare tactics about the inevitable damage caused by reform to the global competitiveness of our banking industry. No doubt, the case of “anti-competiveness” is a valid argument and any reforms passed could have immediate negative impacts on short-term profits. Like the bitter taste of many medicines, I can accept regulatory remedies now, if the long-term improvements outweigh the immediate detrimental aspects.

The focus on short-termism and extremism has created an acidic culture in both Washington and on “Main Street,” making government changes virtually impossible. If President Obama wants to implement the change he campaigned on, then he needs to take a more centrist view that concentrates on enduring benefits – not immediate political gains.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Article first submitted to Alrroya.com before being published on Investing Caffeine.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds but at the time of publishing had no direct positions in securities mentioned in the article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Banking Surgery or Amputation?

Photo Source: (c)iStockphoto.com Artist: Powerofforever

Deciding whether to sever the proprietary trading arms of the commercial banks, rather than instituting regulation, seems a lot like deciding whether amputation is a healthier path for those suffering terrible frostbite cases. Even if this legislation is unlikely to pass, I find the recommendations severe in relation to other measured alternatives. I’m no right-wing conspiracy theorist, but I don’t think the timing of the Obama administration’s announcement is coincidental. Why is this proposal surfacing two years into the financial crisis and a whole year after the President entered office?

Politicians have always been masterful at introducing coincidental distractions at opportune times, in order to generate patriotic voter sympathies. Some examples include, Margaret Thatcher in the Falkand Islands; George Bush #41 in the Iraqi war; and President Obama’s current ant-banker populist brigade. Perhaps miserable and declining approval ratings and a healthcare bill on the verge of collapse may have something to do with the timing? I want President Obama to succeed, and he may have good intentions, but let’s not rush to an overzealous knee-jerk reactions before other less-draconian solutions are thoroughly explored.

Glass-Steagall Redux

Theoretically, the argument of forcing banks to adopt lower risk sounds great on paper. Overall, I think this initiative is a worthy one Americans could buy into. As a matter of fact, investment guru Jeremy Grantham makes the same argument in my Investing Caffeine article (“Too Big to Sink”). However, I think a more relevant question is, “How do we implement more responsible risk taking by the banks, without a massive overhaul to the system?” Certainly there were some regulators asleep at the switch, and some financial institutions that pushed the envelope on risk assumption, but I’m not convinced a return to Glass-Steagall (or Glass-Steagall Lite) is going to bring miracles. If the regulators cannot adequately curb risk taking by the banks, then cross the more dangerous bridge later. The economy is presently in the midst of a fragile recovery and we do not want to change the airplane engine during mid-flight.

Political Pendulum Swings

This isn’t the first time Washington has reversed previous decisions. If the cries of voters reach a feverish pitch, and these wishes coincide with a politician’s re-election agenda, then the probabilities of sub-optimal, rushed legislation increases. Consider AT&T (T), which because of antitrust concerns was forced to split operations in 1982. Lo and behold, some twenty years later, we witnessed the re-consolidation of the “Baby Bells” back into AT&T. Now, Glass-Steagall is the topic of conversation and with an unambiguous scapegoat needed by politicians, Washington is targeting the banks with taxes and operations splitting.

Hasty legislation is nothing new with the populist flames fanning in the background. Sarbanes-Oxley is another example of less-than-ideal legislation introduced in the wake of relatively low number of corporate scandals, such as Enron, WorldCom, and Tyco (TYC).

Regulation Reform Solution

Here are 3 constructive steps:

1) Institute transparent trading of derivatives (i.e., Credit default Swaps) over exchanges with adequately capitalized clearing houses.

2) Require higher capital requirements for banks conducting proprietary trading and mandate adequate disclosure.

3) Consolidation of regulators, thereby creating a more simplified, accountable structure (see also Regulatory Web article). Savings from redundant costs could be used to hire additional regulatory oversight staff.

Blood is in the streets and with mid-term elections just around the corner, the Obama administration is looking to salvage anything they can bring back to the voters. Frost bite (and greedy bankers) is a painful and horrible predicament, however if healthy functioning limbs can be saved with targeted surgery rather than amputation, then I vote for this solution.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including VFH), and at the time of publishing had no direct positions in T, TYC. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Cash Pile Still Growing

Despite the sluggish economic reports, corporate cash piles have been expanding (see “Nest Egg” chart), thanks to aggressive cost-cutting, stabilization in GDP numbers, and meager capital programs. As part of stingy CFOs and executives controlling expenses, companies have been slow to hire despite an expected two quarters of economic growth. Job hiring is likely to remain scarce since capacity utilization and capital expenditures will probably remain priorities before job payrolls expand. It may be that jobs were the first area cut as the crisis unfolded and the last aspect to rebound in the economic expansion.

Source: The Wall Street Journal and Capital IQ

As the saying goes, “A bank only lends to those people whom do not need it.” Common knowledge has it that most jobs are created from small and medium sized businesses (SMBs). Unfortunately, the inaccessibility of loans for these SMBs has contributed to the lackluster job recovery. The hemorrhaging of jobs has slowed to a trickle, but sustainable recovery will eventually require new, substantive job creation. Rather than fund what appear to be risky loans to SMBs, banks are choosing to repair their weary balance sheets to reap the benefits of a very steep yield curve (borrowing at low short-term interest rates and lending at relatively high long-term interest rates). Bankers are not the only people stockpiling cash (see other article on cash). On the capital raise side, larger corporations have had more success in tapping the capital credit markets since bond issuance has been flowing nicely.

Source: Haver Analytics and Gluskin Sheff

As multi-national corporations continue to benefit from a relatively weak dollar and Wall Street persists to underestimate the trajectory of the U.S. corporate profit rebound, banks are hoarding more capital, which is leading to a larger cash pile. When will all this cash reflow back into the marketplace? The timing is unclear, but if the profitability and hoarding trends continue, the low-yielding cash piles spoiling on the balance sheets are likely to be released into the economy in the form of capital expenditures and rehiring. Job seekers will breathe a sigh of relief once these corporate wallets become too uncomfortably fat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (such as VFH), but at time of publishing had no direct position in any company mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Too Big to Fail (Review)

Some call Andrew Ross Sorkin’s new behind-the-scenes book about the financial crisis of 2008-2009 “Too Big to Read” due to its meaty page count at 624 pages (a tad more than my book). But actually, once you crack the first chapter of Too Big to Fail you become immediately sucked in. In creating the “fly on the wall” perspective covering the elite power brokers of Wall Street and Washington, Sorkin utilizes 500 hours of interviews with more than 200 individuals.

Through the detailed and vivid conversations, you get the keen sense of overwhelming desperation and self-preservation that overtakes the executives of the sinking financial system. Some of the chief participants failed, some were triumphant, and some were pathetically bailed out. History will ultimately be the arbiter of whether government and Wall Street averted, mitigated, postponed, or contributed to the financial collapse. Regardless, Sorkin brilliantly encapsulates this emotionally panicked period in our history that will never be erased from our memories.

Here are a few passages that capture the feeling and mood of the book:

Merger Musical Chairs

The terror-induced insanity of merger musical chairs is best depicted through the notepad of Timothy Geithner, then the president of the New York Federal Reserve Bank:

“On a pad that morning, Geithner started writing out various merger permutations: Morgan Stanley and Citigroup. Morgan Stanley and JP Morgan Chase. Morgan Stanley and Mitsubishi. Morgan Stanley and CIC. Morgan Stanley and Outside Investor. Goldman Sachs and Citigroup. Goldman Sachs and Wachovia. Goldman Sachs and Outside Investor. Fortress Goldman. Fortress Morgan Stanley. It was the ultimate Wall Street chessboard.”

AIG Bombshell

The book is also laced with financial nuggets to put the scope of the crisis in perspective. Here Sorkin examines the distressed call of assistance from AIG CEO, Bob Willumstad, to Timothy Geithner:

“A bombshell that Willumstad was confident would draw Geithner’s attention-was a report on AIG’s counterparty exposure around the world, which included ‘$2.7 trillion of notional derivative exposures, with 12,000 individual contracts.” About halfway down the page, in bold, was the detail that Willumstad hoped would strike Geithner as startling: “$1 trillion of exposures concentrated with 12 major financial institutions.’”

Bernanke’s Bumbled Spelling Bee

In setting the stage for the drama that unfolds, Sorkin also provides a background on the key players in the book. For example in describing Ben Bernanke you learn he was

“born in 1953 and grew up in Dillon South Carolina, a small town permeated by the stench of tobacco warehouses. As an eleven-year-old, he traveled to Washington to compete in the national spelling championship in 1965, falling in the second round, when he misspelled ‘Edelweiss.’”

TARP Tidbits

On how the precise $700 billion TARP (Troubled Asset Relief Program) figure was created, Sorkin describes the scattered thought process of the program designer Neel Kashkari:

“They knew they could count on Kashkari to perform some sort of mathematical voodoo to justify it: ‘There’s around $11 trillion of residential mortgages, there’s around $3 trillion of commercial mortgages, that leads to $14 trillion, roughly five percent of that is $700 billion.’ As he plucked numbers from thin air even Kashkari laughed at the absurdity of it all.”

Mercedes Moment

Mixed in with the facts and downbeat conversations are a series of humorous anecdotes and one-liners. Here is one exchange between Goldman Sachs CEO, Lloyd Blankfein, and his Chief of Staff Russell Horwitz:

“’I don’t think I can take another day of this,’ Horowitz said wearily. Blankfein laughed. ‘You’re getting out of a Mercedes to go to the New York Federal Reserve – you’re not getting out of a Higgins boat* on Omaha Beach! Keep things in perspective.’”

*Blankfein’s quote: A reference to the bloody D-Day battle.

Too Big to Fail is an incredible time capsule for the history books. Let’s hope we do not have to relive a period like this in our lifetimes. I wouldn’t mind reading another Andrew Ross Sorkin book…just not another one about a future financial crisis.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but did not have any direct positions in any stock mentioned in this article at time of publication (including GS, AIG, WFC, MS, and C). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

China Executes Wall Street Solution

China is taking an innovative approach to white collar crime…execution. Yang Yanming, a rogue securities trader, completed his death sentence this week for embezzling $9.52 million (a daily rounding error for Goldman Sachs, I might add). Not exactly a cheery topic for the holiday season, but nonetheless, apparently an effective technique for cracking down on illegal behavior. Last I heard, there has been no mention of a $65 billion Chinese version of the Madoff Ponzi scheme? I wonder what kind of risks the financial division of AIG would have undertaken, if involuntary death sentences were considered as viable options in the back of their minds? China in fact carries out more annual executions (via lethal injection and gun) than any other country in the world.

Part of the recent financial crisis can be attributed to the culture of Wall Street and the investment industry, which centers on exploiting “OPM,” an acronym I use to describe “other people’s money.” Often, industry professionals (I use the term loosely) assume undue amounts of risk in hopes of securing additional income, no matter the potential impact on the client. The thought process generally follows: “Why should I risk my own capital to make a mega-bonus, when I can swing for the fences using someone else’s?” And if OPM cannot be secured from individuals, perhaps the capital can be borrowed from the banks – at least before the bailouts occurred.

OPM does come with some caveats, however. Say for example the OPM comes from the government. When TARP (Troubled Asset Relief Program) funds got crammed down the throats of the banking industry, the auspice of reduced bonuses didn’t sit very well with many of the fat-cat Wall Street executives. Financial institutions prefer their OPM with few strings and little to no accountability. Goldman Sachs (GS), JP Morgan (JPM), and Morgan Stanley (MS) weren’t big fans of the government’s pay scale, so these banks paid back the TARP funds at mid-year. Citigroup (C) is still negotiating with the U.S. Treasury and regulators to remove the scarlet phrase of “exceptional assistance” from their chests.

This subject of accountability brings up additional doses of blame to distribute. Not only are the gun-slinging bankers and advisers the ones to blame, but in many cases the clients themselves shoulder some of the responsibility. Either the clients’ start drinking the speculative “Kool-Aid” of their advisor or they neglect to ask a few basic questions for accountability. Just as Ronald Reagan stressed in his conversations with the Soviets, it is also imperative for clients to “trust but verify” the relationship with their advisor (read how to get your financial house in order).

One thing we learned from the crisis of 2008-2009 is that trust is a scarce resource. Investors can “luck” into a trustworthy relationship, but more often than not, just like anything else, it takes time and effort to build a worthy partnership.

The suppliers of OPM have gotten smarter and more skeptical after the crisis, however the managers of OPM haven’t discarded risk from their toolboxes. In addition to the general rebound in domestic equities, we have seen emerging markets, commodities, high-yield bonds, and foreign currencies (to name a few areas), also vault higher.

Regulatory reform for the financial industry is a hot topic for discussion, although virtually nothing substantive has been implemented yet. Incentives, accountability, and adequate capital requirements need to be put in place, so excessive risk-taking (like we saw at the AIG division handling Credit Default Swaps) doesn’t compromise the safety of our financial system. Also, traders need to be incentivized for making responsible decisions and punished adequately for participating in illegal activities. I know the President has a lot on his plate right now, but perhaps the Obama administration could set up a brief meeting with the capital punishment committee in Beijing. I’m confident the Chinese could assist us in “executing” a financial regulatory system solution.

Read Full Reuters Article on Rogue Chinese Trader

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) and BAC, but at time of publishing had no direct positions in GS, AIG, JPM, MS and C. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

FDIC: Busted Piggy Bank

Just as Bank of America (BAC) has decided to pay back $45 billion in TARP (Troubled Asset Relief Program) money, and the employment picture brightened with the recent improvement in the unemployment rate, our banking piggy bank, FDIC (Federal Deposit Insurance Corporation), has been busted. Recovering macroeconomic indicators haven’t allowed our banking system to get out of the woods quite yet. This struggling FDIC news comes even before the inexorable collapse expected in commercial real estate (see Wilbur Ross’ comments on the subject).

Sheila Bair, the Chairwoman of the FDIC, indicated with her sobering remarks that these trends will not disappear overnight:

“For now the credit adversity we have been discussing for some time remains with us, and we have been discussing for some time remains with us, and we expect that it will be at least a couple of more quarters before we see a meaningful improvement in that trend.”

With the FDIC adding 136 banks to its “problem list” in the third quarter (bringing the total to 552), the regulator was forced to pull out $38.9 billion from the piggy bank, officially draining the rainy day fund into the red.

Fixing the Problem

How will the FDIC replenish its hollow piggy bank? Ms. Bair has recently endorsed a letter sent to House Financial Services Committee Chairman (Barney Frank) that would force secured creditors (mainly banks) to create a slush fund for potential large bank failures that pose a threat to the system. Ms. Bair designed the program this way because all banks – big or small – would be forced to “evaluate the solvency of our largest financial firms.”

Due to the continuation of bank failures and loan loss deterioration, the FDIC fund balance slipped to a negative -$8.2 billion (the first time since dealing with the failing thrifts in 1992) for the September period. Therefore, Ms. Bair put forth an emergency measure that requires insured banks to prepay three years of insurance premiums by the end of 2009. This action is expected to raise approximately $45 billion in funds. Although the reserve piggy bank had an upside down balance, the FDIC can still keep the lights on and cover employee payroll because the regulatory entity still has $23.3 billion in cash and marketable securities on its balance sheet.

With the taxpayers flipping the bill for bailouts galore over the last two years, and Goldman Sachs (GS) wheelbarrowing out bonuses to their employees, Ms. Bair and politicians are looking to the industry to now shoulder more of the bank failure burden. Let’s hope the piggybank can be replenished so taxpayers don’t have to go scraping through their wallets again.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) and BAC, but at time of publishing had no direct positions in GS. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Meredith Whitney’s Cloudy Crystal Ball

Meredith Whitney, prominent banking analyst at her self-named advisory group, should have worn a bib to protect her from the adoring drool supplied by Maria Bartiromo in a recent CNBC interview. Ms. Whitney has quickly become a banking rock star during this “Great Recession” period. She was right at a critical juncture, and as a result she was thrust into the limelight. Much like Abby Joseph Cohen, the perma-bull Goldman Sachs strategist who gained notoriety in the late 1990s, Whitney (the perma-banking bear) will continue having difficulty living up to the lofty expectations demanded of her.

Despite the accolades, Whitney’s crystal ball has gotten cloudy in 2009. I suppose accuracy is not very important, judging by her bottom-half 2007 ranking (year of her major Citigroup call) in recommendation performance and 48%-ile ranking in the first half of 2008. Analysts, much like reporters, can avoid looking dumb by reporting the news du jour and by following the herd. Whitney has followed this formula with her continuous bearishness on the financial sector, excluding a brief but late upgrade of Goldman Sachs in July. Not only was her analysis tardy (Goldman’s stock tripled from the 2009 bottom), but her call has also underperformed the S&P 500 index since the upgrade.

Incoherent Inconsistencies

Like a bobbing and weaving wrestler (her husband John Layfield is a retired staged professional wrestler from the WWE), Whitney tries to concoct a completely mind-boggling narrative to explain her forecasts this year in the CNBC interview with Maria Bartiromo:

11/18/09 (XLF Price $14.60): “For the year, I have been at least ‘cover your shorts, go long.’ I haven’t been this bearish in a year.” (See Maria Bartiromo Interview)

Hmm, really? Are you kidding me? Wait a second…is this the same “go long” Meredith Whitney that expressed the following?

3/17/09: (XLF: 8.55 then, 14.60 now +71% ex-dividends): “These big banks are sitting on loans that were underwritten with bad math, and the stocks are going to go down…these stocks are uninvestable.”

(Fast forward to minute 8:20 for quote above)

2/4/09 (XLF: 8.97 then, 14.60 now +63% ex-dividends): “Investors should not even consider owning banks on an equity basis” (Click here and fast forward to minute 8:10 for quote).

The schizophrenic accounting of her postures are all the more confusing given her stance that the sector was “fairly valued” in October, according to the CNBC Bartiromo interview.

Don’t get me wrong, she made an incredible bearish call on Citigroup in the fall of 2007 and was expecting blood in the streets until a massive rebound in 2009 surprised her. Investors need to be wary of prognosticators that get thrust into the limelight (see Peter Schiff article) for a single prediction. The law of large numbers virtually guarantees a new breed of extreme forecasters will be rotated into the spotlight any time there is a major shift in the market direction. I choose to follow the footsteps of Warren Buffett and stay away from the game of market timing and market forecasts. I believe James Grant from the Interest Rate Observer states it best:

“The very best investors don’t even try to forecast the future. Rather, they seize such opportunities as the present affords them.”

Meredith Whitney may be a bright banking analyst and perhaps she’ll ultimately be proven right regarding the downward banking stock price trajectories, but like all bold forecasters she must live by the crystal ball, and die by the crystal ball.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and its clients own certain exchange traded funds (including VFH), but currently have no direct positions in C, GS, or XLF. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}