Playing the Field with Your Investments

For some, casually dating can be fun and exciting. The same goes for trading and speculating – the freedom to make free- wheeling, non-committal purchases can be exhilarating. Unfortunately the costs (fiscally and emotionally) of short-term dating/investing often outweigh the benefits.

Fortunately, in the investment world, you can get to know an investment pretty well through fundamental research that is widely available (e.g., 10Ks, 10Qs, press releases, analyst days, quarterly conference calls, management interviews, trade rags, research reports). Unlike dating, researching stocks can be very cheap, and you do not need to worry about being rejected.

Dating is important early in adulthood because we make many mistakes choosing whom we date, but in the process we learn from our misjudgments and discover the important qualities we value in relationships. The same goes for stocks. Nothing beats experience, and in my long investment career, I can honestly say I’ve dated/traded a lot of pigs and gained valuable lessons that have improved my investing capabilities. Now, however, I don’t just casually date my investments – I factor in a rigorous, disciplined process that requires a serious commitment. I no longer enter positions lightly.

One of my investment heroes, Peter Lynch, appropriately stated, “In stocks as in romance, ease of divorce is not a sound basis for commitment. If you’ve chosen wisely to begin with, you won’t want a divorce.”

Charles Ellis shared these thoughts on relationships with mutual funds:

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship comes without wild swings, and stocks are no different. If you want to survive the volatile ups and downs of a relationship (or stock ownership), you better do your homework before blindly jumping into bed. The consequences can be punishing.

Buy and Hold is Dead…Unless Stocks Go Up

If you are serious about your investments, I believe you must be mentally willing to commit to a relationship with your stock, not for a day, not for a week, or not for a month, but rather for years. Now, I know this is blasphemy in the age when “buy-and-hold” investing is considered dead, but I refute that basic premise whole-heartedly…with a few caveats.

Sure, buy-and-hold is a stupid strategy when stocks do nothing for a decade – like they have done in the 2000s, but buying and holding was an absolutely brilliant strategy in the 1980s and 1990s. Moreover, even in the miserable 2000s, there have been many buy-and-hold investments that have made owners a fortune (see Questioning Buy & Hold ). So, the moral of the story for me is “buy-and-hold” is good for stocks that go up in price, and bad for stocks that go flat or down in price. Wow, how deeply profound!

To measure my personal commitment to an investment prospect, a bachelorette investment I am courting must pass another test…a test from another one of my investment idols, Phil Fisher, called the three-year rule. This is what the late Mr. Fisher had to say about this topic:

“While I realized thoroughly that if I were to make the kinds of profits that are made possible by [my] process … it was vital that I have some sort of quantitative check… With this in mind, I established what I called my three-year rule.” Fisher adds, “I have repeated again and again to my clients that when I purchase something for them, not to judge the results in a matter of a month or a year, but allow me a three year period.”

Certainly, there will be situations where an investment thesis is wrong, valuation explodes, or there are superior investment opportunities that will trigger a sale before the three-year minimum expires. Nonetheless, I follow Fisher’s rule in principle in hopes of setting the bar high enough to only let the best ideas into both my client and personal portfolios.

As I have written in the past, there are always reasons of why you should not invest for the long-term and instead sell your position, such as: 1) new competition; 2) cost pressures; 3) slowing growth; 4) management change; 5) valuation; 6) change in industry regulation; 7) slowing economy; 8 ) loss of market share; 9) product obsolescence; 10) etc, etc, etc. You get the idea.

Don Hays summed it up best: “Long term is not a popular time-horizon for today’s hedge fund short-term mentality. Every wiggle is interpreted as a new secular trend.”

Peter Lynch shares similar sympathies when it comes to noise in the marketplace:

“Whatever method you use to pick stocks or stock mutual funds, your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

Every once in a while there is validity to some of the concerns, but more often than not, the scare campaigns are merely Chicken Little calling for the world to come to an end.

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down irrespective of the daily headlines. Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually date a stock position, perhaps you should commit to a long-term relationship and divorce your field-playing habits. Now that sounds like a sweet kiss of success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investors Take a Vacation

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 3, 2015). Subscribe on the right side of the page for the complete text.

It’s summertime and the stock market has taken a vacation, and it’s unclear when prices will return from a seven month break. It may seem like a calm sunset walk along the beach now that Greek worries have temporarily subsided, but concerns have shifted to an impending Federal Reserve interest rate hike, declining commodity prices, and a Chinese stock market crash, which could lead to a painful sunburn.

If you think about it, stock investors have basically been on unpaid vacation since the beginning of the year, with the Dow Jones Industrial Index (17,690) down -0.7% for 2015 and the S&P 500 (2,104) up + 2.2% over the same time period (see chart below). Despite mixed results for the year, all three main stock indexes rebounded in July (including the tech-heavy NASDAQ +2.8% for the month) after posting negative returns in June. Overall for 2015, sector performance has been muddled. There has been plenty of sunshine on the Healthcare sector (+11.7%), but Energy stocks have been stuck in the doldrums (-13.4%), over the same timeframe.

Source: Yahoo! Finance

Chinese Investors Suffer Heat Stroke

Despite gains for U.S. stocks in July, the overheated Chinese stock marketcaused some heat stroke for global investors with the Shanghai Composite index posting its worst one month loss (-15%) in six years, wiping out about $4 trillion in market value. Before coming back down to earth, the Chinese stock market inflated by more than +150% from 2014.

Driving the speculative fervor were an unprecedented opening of 12 million monthly accounts during spring, according to Steven Rattner, a seasoned financier, investor, and a New York Times journalist. Margin accounts operate much like a credit card for individuals, which allowed these investors to aggressively gamble on the China market upswing, but during the downdraft investors were forced to sell stocks to generate proceeds for outstanding loan repayments. It’s estimated that 25% of these investors only have an elementary education and a significant number of them are illiterate. Further exacerbating the sell-off were Chinese regulators artificially intervening by halting trading in about 500 companies on the Shanghai and Shenzhen exchanges last Friday, equivalent to approximately 18% of all listings.

Although China, as the second largest economy on the globe, is much more economically important than a country like Greece, recent events should be placed into proper context. For starters, as you can see from the chart below, the Chinese stock market is no stranger to volatility. According to Fundstrat Global Advisors, the Shanghai composite index has experienced 10 bear markets over the last 25 years, and the recent downdraft doesn’t compare to the roughly -75% decline we saw in 2007-2008. Moreover, there is no strong correlation between the Chinese stock market. Only 15% of Chinese households own stocks, or measured differently, only 6% of household assets are held in stocks, says economic-consulting firm IHS Global Insight. More important than the question, “What will happen to the Chinese stock market?,” is the question, “What will happen to the Chinese stock economy?,” which has been on a perennial slowdown of late. Nevertheless, China has a 7%+ economic growth rate and the highest savings rate of any major country, both factors for which the U.S. economy would kill.

Source: Yardeni.com

Don’t Take a Financial Planning Vacation

While the financial markets continue to bounce around and interest rates oscillate based on guesswork of a Federal Reserve interest rate hike in September, many families are now returning from vacations, or squeezing one in before the back-to-school period. The sad but true fact is many Americans spend more time planning their family vacation than they do planning for their financial futures. Unfortunately, individuals cannot afford to take a vacation from their investment and financial planning. At the risk of stating the obvious, planning for retirement will have a much more profound impact on your future years than a well-planned trip to Hawaii or the Bahamas.

We live in an instant gratification society where “spend now, save later” is a mantra followed by many. There’s nothing wrong with splurging on a vacation, and to maintain sanity and family cohesion it is almost a necessity. However, this objective does not have to come at the expense of compromising financial responsibility – or in other words spending within your means. Investing is a lot like consistent dieting and exercising…it’s easy to understand, but difficult to sustainably execute. Vacations, on the other hand, are easy to understand, and easy to execute, especially if you have a credit card with an available balance.

It’s never too late to work on your financial planning muscle. As I discuss in a previous article (Getting to Your Number) , one of the first key steps is to calculate an annual budget relative to your income, so one can somewhat accurately determine how much money can be saved/invested for retirement. Circumstances always change, but having a base-case scenario will help determine whether your retirement goals are achievable. If expectations are overly optimistic, spending cuts, revenue enhancing adjustments, and/or retirement date changes can still be made.

When it comes to the stock market, there are never a shortage of concerns. Today, worries include a Greek eurozone exit (“Grexit”); decelerating China economic growth and a declining Chinese stock market; and the viability of Donald’s Trump’s presidential campaign (or lack thereof). While it may be true that stock prices are on a temporary vacation, your financial and investment planning strategies cannot afford to go on vacation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Supply & Demand: The Key to Oil, Stocks, and Pork Bellies

Commodity prices, including oil, are “crashing” according to the pundits and fears are building that this is a precursor to another stock market collapse. Are we on an irreversible path of repeating the bloodbath carnage of the 2008-2009 Great Recession?

Fortunately for investors, markets move in cycles and the fundamental laws of supply and demand hold true in both bull and bear markets, across all financial markets. Whether we are talking about stocks, bonds, copper, gold, currencies, or pork bellies, markets persistently move like a pendulum through periods of excess supply and demand. In other words, weakness in prices create stronger demand and less supply, whereas strength in prices creates weakening demand and more supply.

Since energy makes the world go round and the vast majority of drivers are accustomed to filling up their gas tanks, the average consumer is familiar with recent negative price developments in the crude oil markets. Eighteenth-century economist Adam Smith would be proud that the laws of supply and demand have help up just as well today as they did when he wrote Wealth of Nations in 1776.

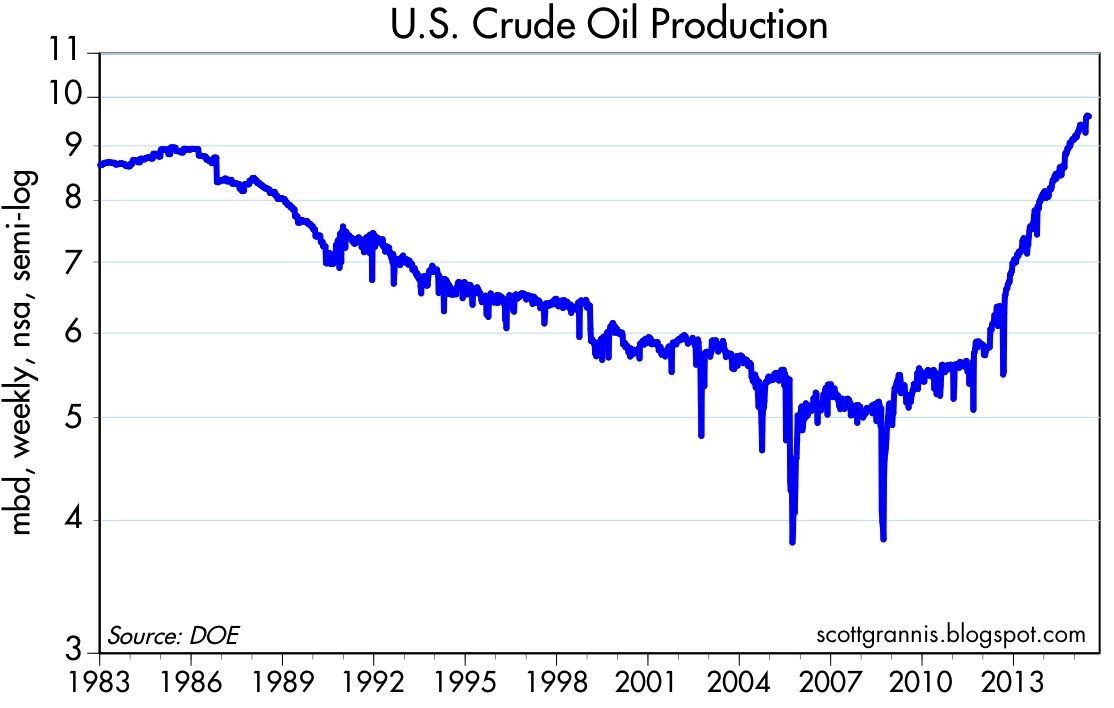

It is true that overall stagnation in global economic demand in recent years, along with the strengthening of the U.S. dollar (because of better relative growth), has contributed to downward trending oil prices. It is also true that supply factors, such as Saudi Arabia’s insistence to maintain production and the boom in U.S. oil production due to new fracking technologies (see chart below), have arguably had a larger negative impact on the more than -50% deterioration in oil prices. Fears of additional Iranian oil supply hitting the global oil markets as a result of the Iranian nuclear deal have also added to the downward pressure on prices.

Source: Scott Grannis

What is bad for oil prices and the oil producers is good news for the rest of the economy. Transportation is the lubricant of the global economy, and therefore lower oil prices will act as a stimulant for large swaths of the global marketplace. Here in the U.S., consumer savings from lower energy prices have largely been used to pay down debt (deleverage), but eventually, the longer oil prices remain depressed, incremental savings should filter into our economy through increased consumer spending.

But prices are likely not going to stay low forever because producers are responding drastically to the price declines. All one needs to do is look at the radical falloff in the oil producer rig count (see chart below). As you can see, the rig count has fallen by more than -50% within a six month period, meaning at some point, the decline in global production will eventually provide a floor to prices and ultimately provide a tailwind.

Source: Scott Grannis

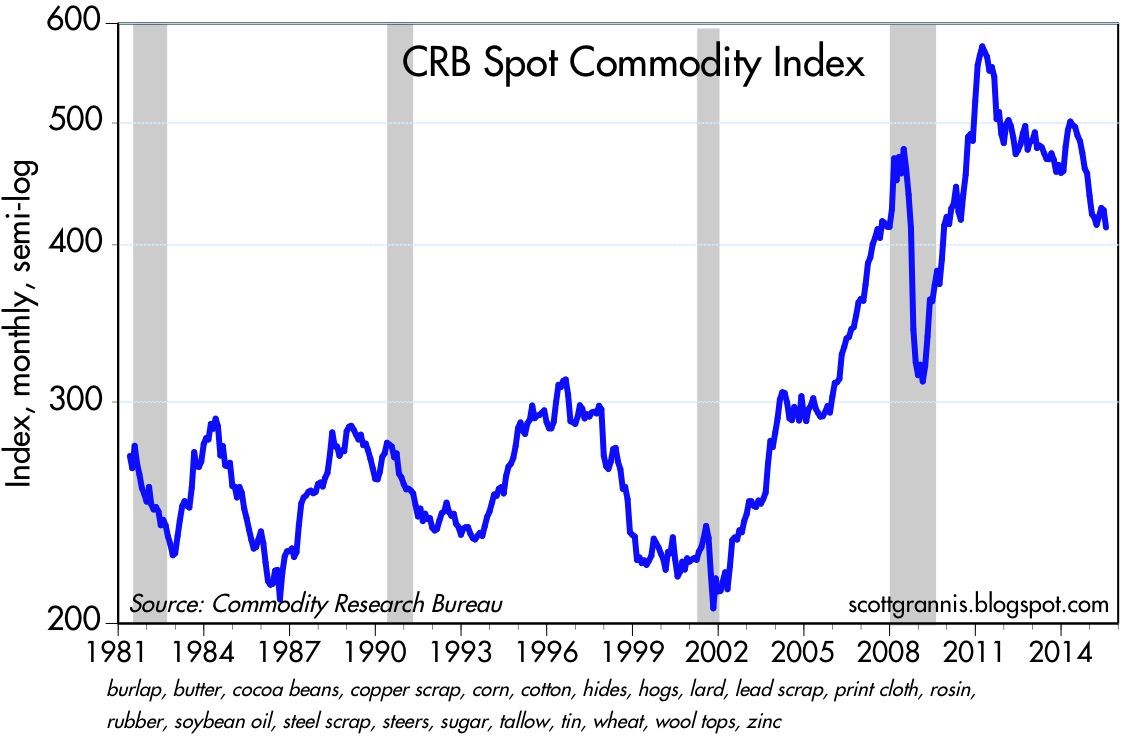

If we broaden our perspective beyond just oil, and look at the broader commodity complex, we can see that the recent decline in commodity prices has been painful, but nowhere near the Armageddon scenario experienced during 2008-2009 (see chart below – gray areas = recessions).

Source: Scott Grannis

Although this conversation has focused on commodities, the same supply-demand principles apply to the stock market as well. Stock market prices as measured by the S&P 500 index have remained near record levels, but as I have written in the past, the records cannot be attributed to the lackluster demand from retail investors (see ICI fund flow data).

Although U.S. stock fundamentals remain relatively strong (e.g., earnings, interest rates, valuations, psychology), much of the strength can be explained by the constrained supply of stocks. How has stock supply been constrained? Some key factors include the trillions in dollars of supply soaked up by record M&A activity (mergers and acquisition) and share buybacks.

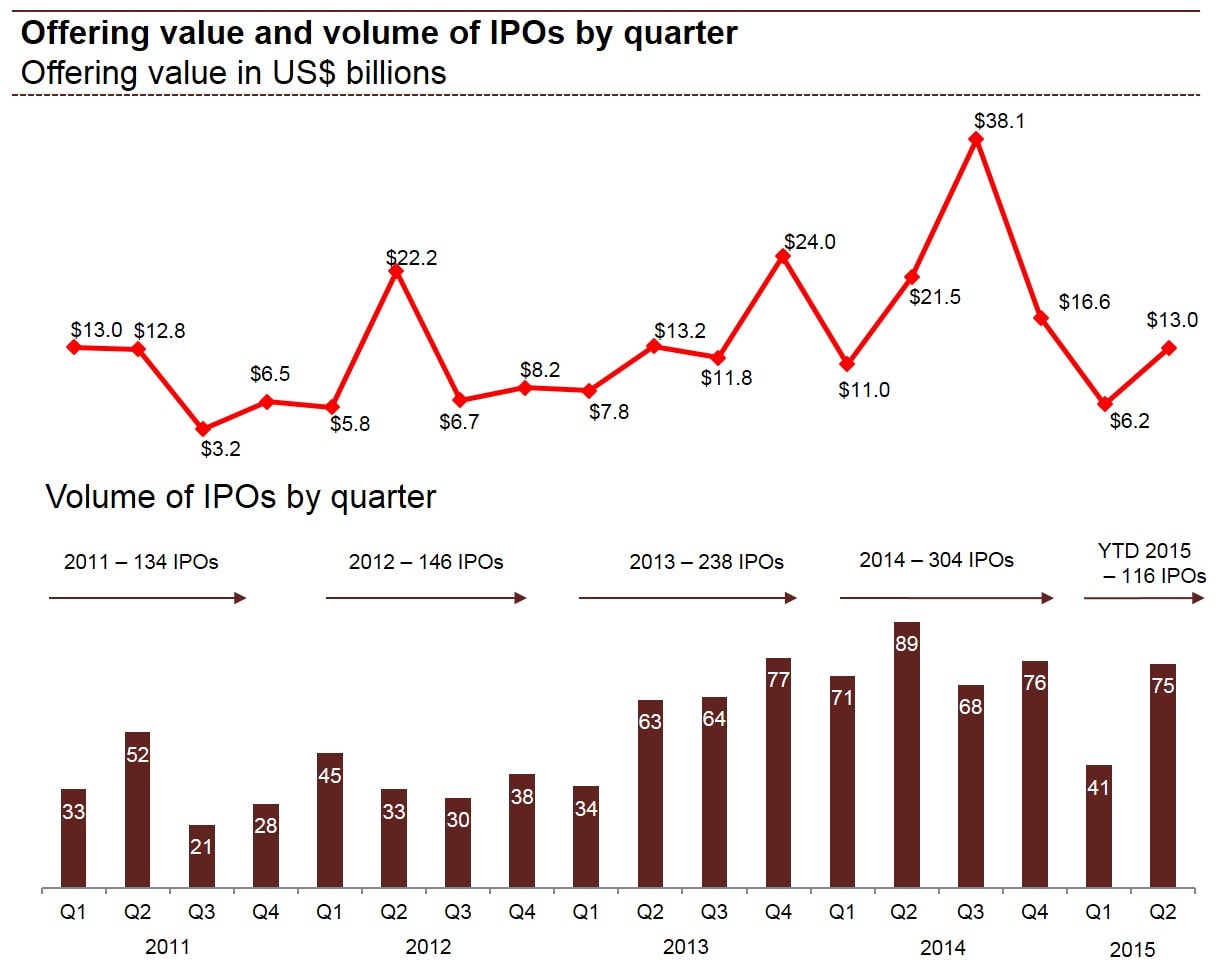

In addition to the declining stock supply from M&A and share buybacks, there has been limited supply of new IPO issues (initial public offerings) coming to market, as evidenced by the declines in IPO dollar and unit volumes in the first half of 2015, as compared to last year. More specifically, first half IPO dollar volmes were down -41% to $19.2 billion and the number of 2015 IPOs has declined -27% to 116 from 160 for the same time period.

Price cycles vary dramatically in price and duration across all financial markets, including stocks, bonds, oil, interest rates, currencies, gold, and pork bellies, among others. Not even the smartest individual or most powerful computer on the planet can consistently time the short-term shifts in financial markets, but using the powerful economic laws of supply and demand can help you profitably make adjustments to your investment portfolio(s).

See Also – The Lesson of a Lifetime (Investing Caffeine)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stock Market Tug-of-War

Image by © Royalty-Free/Corbis

Some things never change. There are several certainties in life, including death and taxes. And when it comes to investing, there are several other certainties: the never-ending existence of geopolitical concerns, and incessant worries over Fed policy.

Let’s face it, since the dawn of mankind, humans have been programmed to worry, whether it stemmed from avoiding a man-eating lion or foraging for food to survive (see Controlling the Investment Lizard Brain). Investors function in much the same way.

There is always a constant tug-of-war between bulls and bears, and if you are obsessed with following the relentless daily headlines about a Grexit (European Greek Exit) and an imminent Federal Reserve rate hike, you like many other investors will continue to experience sweaty palms, heart palpitations, and underperformance.

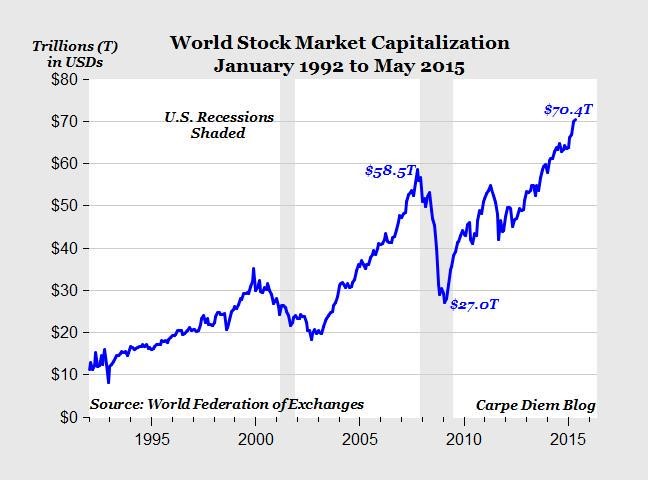

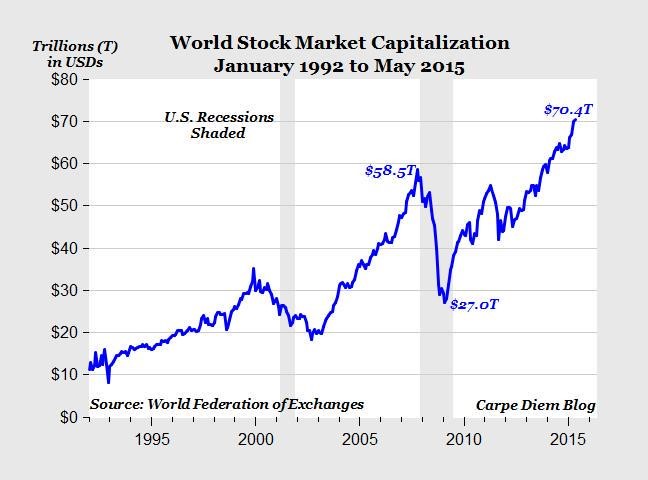

Despite the gloomy headlines, the bulls are currently winning the tug-of-war as measured by the 6-year boom in global stock prices, which has breached a record $70 trillion in value (see chart below).

Source: Mark J. Perry (Carpe Diem)

If you become hostage and react to the headlines about Greece, China, Fed policy, Ukraine, ISIS, Russia, Ebola, North Korea, QE Tapering, etc., not only are you ignoring the key positives fueling this bull market (see also Don’t Be a Fool, Follow the Stool) but you are also costing yourself a lot of money. While I have been watching the “sideliners” for years, they have missed a market driven by generationally low interest rates; improved employment picture (10% to 5%); tame inflation; steady improvement in housing market; fiscal deficit reductions; record corporate profits; record share buybacks and dividends; contrarian investor sentiment (leaving plenty of room for converts to join the party), and other fundamentally positive factors.

Yes, stocks will eventually go down by a significant amount – they always do. Stocks can temporarily go down based on the fear du jour (like the 10-20% declines in 2010, 2011, 2012, and 2014), but the nastier hits to stock markets always come from good old fashion cyclical recessions. As I’ve discussed before, there are no signs of a recession on the horizon, and the yield curve has been a great predictor of this trigger (see Dynamic Yield Curve in Digesting Stock Gains). Until then, the bears will be fighting an uphill battle.

Independent of recession timing, investing is a very challenging game, even for the most experienced professionals. The best long-term investors, including the likes of Warren Buffett and Peter Lynch, understand the never-ending geopolitical and Fed policy headlines are absolutely meaningless over the long run. However, media outlets, blogs, newspapers, and radio shows make money by peddling fear as economic and political concerns jump like a frog from one lily pad to the next. At Sidoxia we have a disciplined and systematic approach to creating diversified portfolios with our proprietary S.H.G.R. model (“sugar”) that screens for attractively valued investments. We believe this is the way to win the long-term tug-of-war.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

F.U.D. and Dividend Shock Absorbers

As the existential question remains open on whether Greece will remain a functioning entity within the eurozone, investor anxiety and manic behavior continues to be the norm. Rampant fear seems very counterintuitive for a stock market that has more than tripled in value from early 2009 with the S&P 500 index only sitting -3% below all-time record highs. Common sense would dictate that euphoric investor appetites have contributed to years of new record highs in the U.S. stock market, but that isn’t the case now. Rather, the enormous appreciation experienced in recent years can be better explained by the trillions of dollars directed towards buoyant share buybacks and mergers.

With a bull market still briskly running into its sixth year, where can we find the evidence for all this anxiety? Well, if you don’t believe all the nail biting concerns you hear from friends, family members, and co-workers about a Grexit (Greek exit from the euro), Chinese stock market bubble, Puerto Rico collapse, and/or impending Fed rate hike, then here are a few confirming data points.

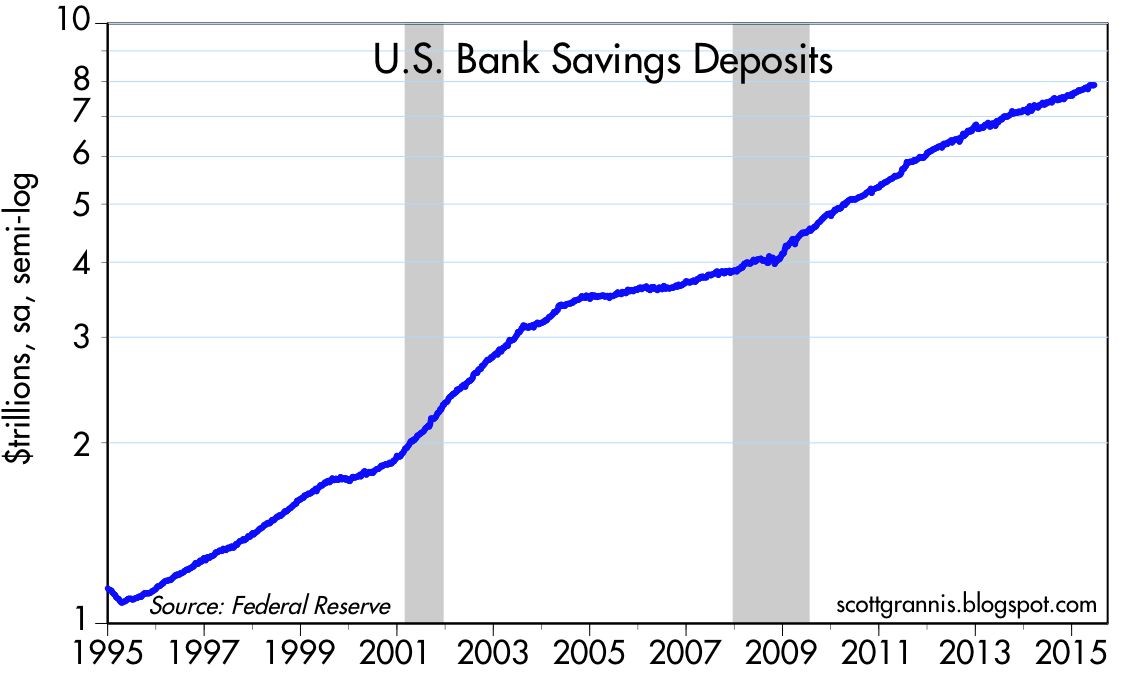

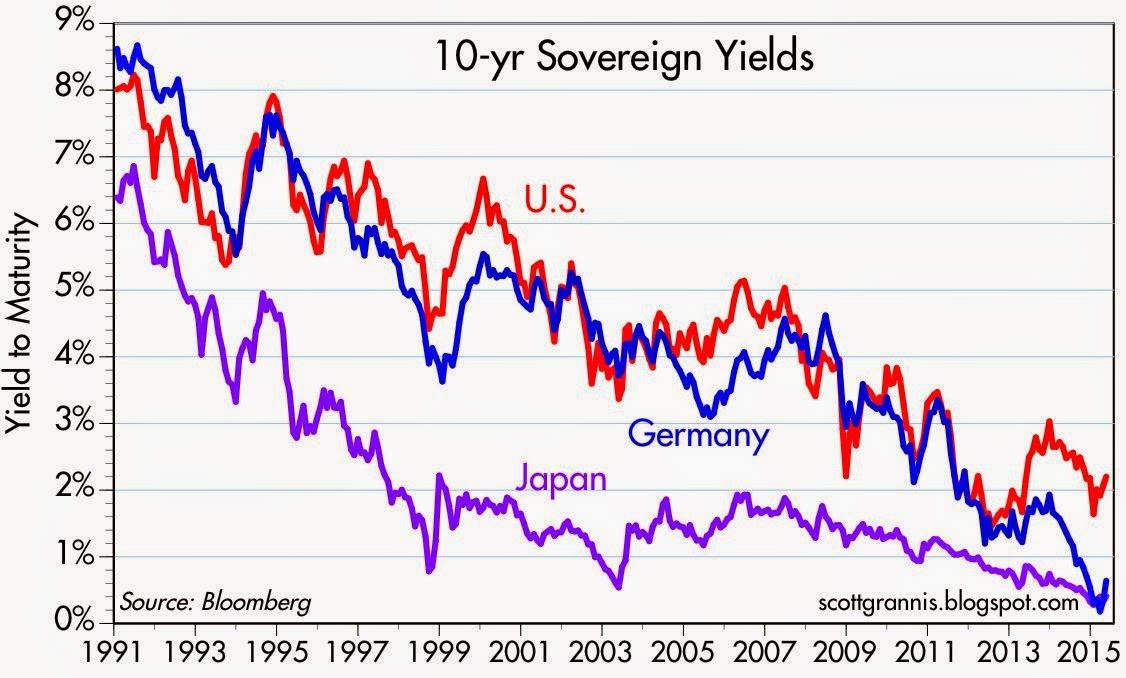

For starters, let’s take a look at the record $8 trillion of cash being stuffed under the mattress at near 0% rates in savings deposits (see chart below). The unbelievable 15% annual growth rate in cash hoarding since the turn of the century is even scarier once you consider the massive value destruction from the eroding impact of inflation and the colossal opportunity costs lost from gains and yields in alternative investments.

Next, you can witness the irrational risk averse behavior of investors piling into low (and negative) yielding bonds. Case in point are the 10-year yields in developing countries like Germany, Japan, and the U.S. (see chart below).

The 25-year downward trend in rates is a very scary development for yield-hungry investors. The picture doesn’t look much prettier once you realize the compensation for holding a 30-year bond (currently +3.2%) is only +0.8% more than holding the same Treasury bond for 10 years (now +2.4%). Yes, it is true that sluggish global growth and tame inflation is keeping a lid on interest rates, but these trends highlight once again that F.U.D. (fear, uncertainty, and doubt) has more to do with the perceived flight to safety and high bond prices (low bond yields).

In addition, the -$57 billion in outflows out of U.S. equity funds this year is further evidence that F.U.D. is out in full force. As I’ve noted on repeated occasions, when the tide turns on a sustained multi-year basis and investors dive head first into stocks, this will be proof that the bull market is long in the tooth and conservatism should be the default posture.

Dividend Shock Absorbers

There are always plenty of scary headlines that tempt investors to bail out of their investments. Today those alarming headlines span from Greece and China to Puerto Rico and the Federal Reserve. When the winds of fear, uncertainty, and doubt are fiercely swirling, it’s important to remember that any investment strategy should be constructed in a diversified manner that meshes with your time horizon and risk tolerance.

Consistent with maintaining a diversified portfolio, owning reliable dividend paying stocks is an important component of investment strategy, especially during volatile periods like we are experiencing currently. Sure, I still love to own high octane, non-dividend growth stocks in my personal and client portfolios, but owning stocks with a healthy stream of dividends serve as shock absorbers in bumpy markets with periodic surprise potholes.

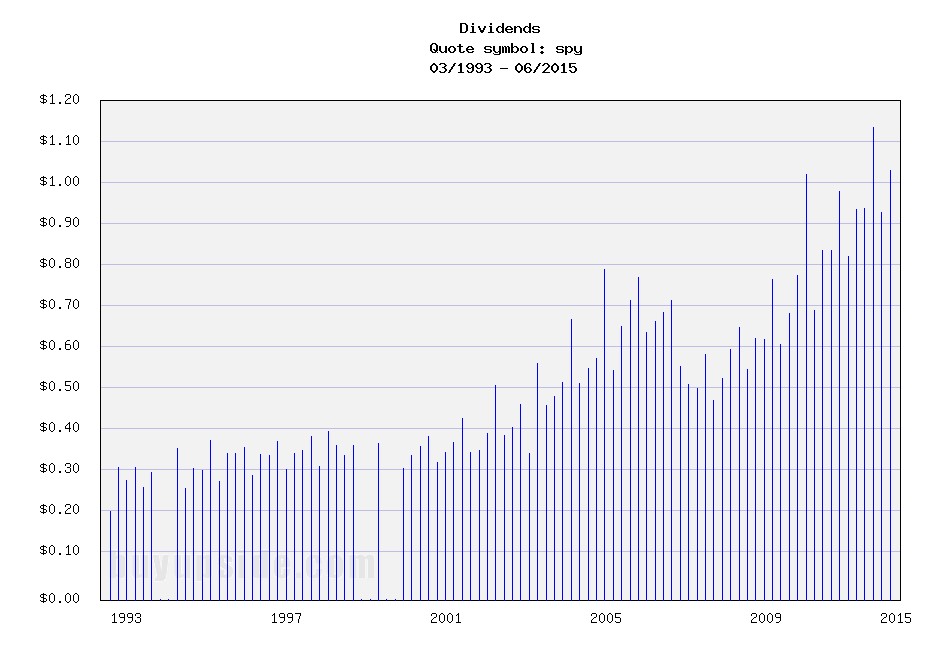

As I’ve note before, bond issuers don’t call up investors and raise periodic coupon payments out of the kindness of their hearts, but stock issuers can and do raise dividends (see chart below). Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500.

Source: BuyUpside.com

Markets will continue to move up and down on the news du jour, but dividends overall remain fairly steady. In the worst financial crisis in a generation, dividends dipped temporarily, but as I explain in a previous article (The Gift that Keeps on Giving), dividends have been on a fairly consistent 6% growth trajectory over the last two decades. With corporate dividend payout ratios well below long term historical averages of 50%, companies still have plenty of room to maintain (and grow) dividends – even if the economy and corporate profits slow.

Don’t succumb to all the F.U.D., and if you feel yourself beginning to fall into that trap, re-evaluate your portfolio to make sure your diversified portfolio has some shock absorbers in the form of dividend paying stocks. That way your portfolio can handle those unexpected financial potholes that repeatedly pop up.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Greece: The Slow Motion, Multi-Year Train Wreck

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2015). Subscribe on the right side of the page for the complete text.

Watching Greece fall apart over the last five years has been like watching a slow motion train wreck. To many, this small country of 11 million people that borders the Mediterranean, Aegean, and Ionian Seas is known more for its Greek culture (including Zeus, Parthenon, Olympics) and its food (calamari, gyros, and Ouzo) than it is known for financial bailouts. Nevertheless, ever since the financial crisis of 2008-2009, observers have repeatedly predicted the debt-laden country will default on its €323 billion mountain of obligations (see chart below – approximately $350 billion in dollars) and subsequently exit the 19-member eurozone currency membership (a.k.a.,”Grexit”).

Source: MoneyMorning.com and CNN

Now that Greece has failed to repay less than 1% of its full €240 billion bailout obligation – the €1.5 billion payment due to the IMF (International Monetary Fund) by June 30th – the default train is coming closer to falling off the tracks. Whether Greece will ultimately crash itself out of the eurozone will be dependent on the outcome of this week’s surprise Greek referendum (general vote by citizens) mandated by Prime Minister Alexis Tsipras, the leader of Greece’s left-wing Syriza party. By voting “No” on further bailout austerity measures recommended by the European Union Commission, including deeper tax increases and pension cuts, the Greek people would effectively be choosing a Grexit over additional painful tax increases and deeper pension cuts.

Ouch!

And who can blame the Greeks for being a little grouchy? You might not be too happy either if you witnessed your country experience an economic decline of greater than 25% (see Greece Gross Domestic Product chart below); 25% overall unemployment (and 50% youth unemployment); government worker cuts of greater than 20%; and stifling taxes to boot. Sure, Greeks should still shoulder much of the blame. After all, they are the ones who piled on $100s of billions of debt and overspent on the pensions of a bloated public workforce, and ran unsustainable fiscal deficits.

Source: TradingEconomics.com

For any casual history observers, the current Greek financial crisis should come as no surprise, especially if you consider the Greeks have a longstanding habit of not paying their bills. Over the last two centuries or so, since the country became independent, the Greek government has spent about 90 years in default (almost 50% of the time). More specifically, the Greeks defaulted on external sovereign debt in 1826, 1843, 1860, 1894 and 1932.

The difference between now and past years can be explained by Greece now being a part of the European Union and the euro currency, which means the Greeks actually do have to pay their bills…if they want to remain a part of the common currency. During past defaults, the Greek central bank could easily devalue their currency (the drachma) and fire up the printing presses to create as much currency as needed to pay down debts. If the planned Greek referendum this week results in a “No” vote, there is a much higher probability that the Greek government will need to dust off those drachma printing presses.

“Perspective People”

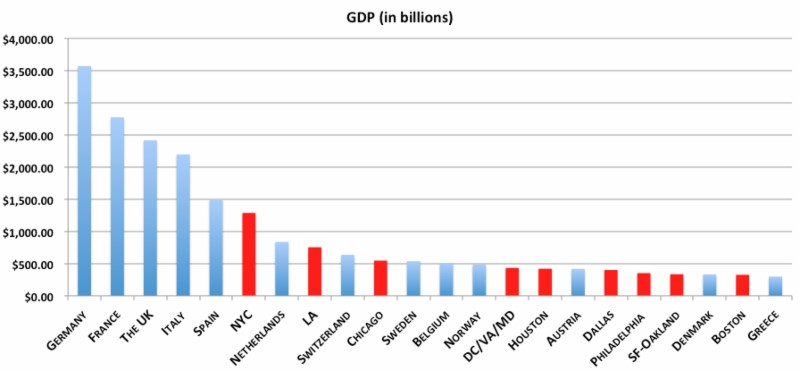

Protest, riots, defaults, changing governments, and new currencies make for entertaining television viewing, but these events probably don’t hold much significance as it relates to the long-term outlook of your investments and the financial markets. In the case of Greece, I believe it is safe to say the economic bark is much worse than the bite. For starters, Greece accounts for less than 2% of Europe’s overall economy, and about 0.3% of the global economy.

Since I live out on the West Coast, the chart below caught my fancy because it also places the current Greek situation into proper proportion. Take the city of L.A. (Los Angeles – red bar) for example…this single city alone accounts for almost 3x the size of Greece’s total economy (far right on chart – blue bar).

Give Me My Money!

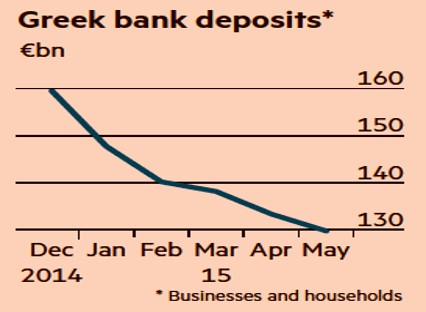

It hasn’t been a fun year for Greek banks. Depositors, who have been flocking to the banks, withdrew about $45 billion in cash from their accounts, over an eight month period (see chart below). Before the Greek government decided to mandatorily close the banks in recent days and implement capital controls limiting depositors to daily ATM withdrawals of only $66.

Source: The Financial Times

But once again, let’s put the situation into context. From an overall Greek banking sector perspective, the four largest Greek Banks (Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank) account for about 90% of all Greek banking assets. Combined, these banks currently have an equity market value of about $14 billion and assets on the balance sheets of $400 billion – these numbers are obviously in flux. For comparison purposes, Bank of America Corp. (BAC) alone has an equity market value of $179 billion and $2.1 trillion in assets.

Anxiety Remains High

Skeptical bears will occasionally acknowledge the miniscule-ness of Greece, but then quickly follow up with their conspiracy theory or domino effect hypothesis. In other words, the skeptics believe a contagion effect of an impending Grexit will ripple through larger economies, such as Italy and Spain, with crippling force. Thus far, as you can see from the chart below, Greece’s financial problems have been largely contained within its borders. In fact, weaker economies such as Spain, Portugal, Ireland, and Italy have fared much better – and actually improving in most cases. In recent days, 10-year yields on government bonds in countries like Portugal, Italy, and Spain have hovered around or below 3% – nowhere near the peak levels seen during 2008 – 2011.

Source: Business Insider

Other doubting Thomases compare Greece to situations like Lehman Brothers, Long Term Capital Management, and the subprime housing market, in which underestimated situations snowballed into much worse outcomes. As I explain in one of my newer articles (see Missing the Forest for the Trees), the difference between Greece and the other financial collapses is the duration of this situation. The Greek circumstance has been a 5-year long train wreck that has allowed everyone to prepare for a possible Grexit. Rather than agonize over every news headline, if you are committed to the practice of worrying, I would recommend you focus on an alternative disaster that cannot be found on the front page of all newspapers.

There is bound to be more volatility ahead for investors, and the referendum vote later this week could provide that volatility spark. Regardless of the news story du jour, any of your concerns should be occupied by other more important worrisome issues. So, unless you are an investor in a Greek bank or a gyro restaurant in Athens, you should focus your efforts on long-term financial goals and objectives. Ignoring the noisy news flow and constructing a diversified investment portfolio across a range of asset classes will allow you to avoid the harmful consequences of the slow motion, multi-year Greek train wreck.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Missing the Forest for the Trees

Just days ago, billionaire investor and corporate activist Carl Icahn called the stock market “extremely overheated,” especially as it relates to high yield bonds. He communicated these comments over Twitter after saying markets are “sailing in dangerous unchartered waters.” Given recent Greek developments regarding its inability to strike a debt repayment deal with eurozone leaders, Mr. Icahn might get exactly the volatility he expected when he made those comments. There’s no question a Greek default could definitely cause a short-term contagion effect, but there will be much larger fish to fry than domestic equity markets (I will have much more to say on the Greek topic in my monthly newsletter).

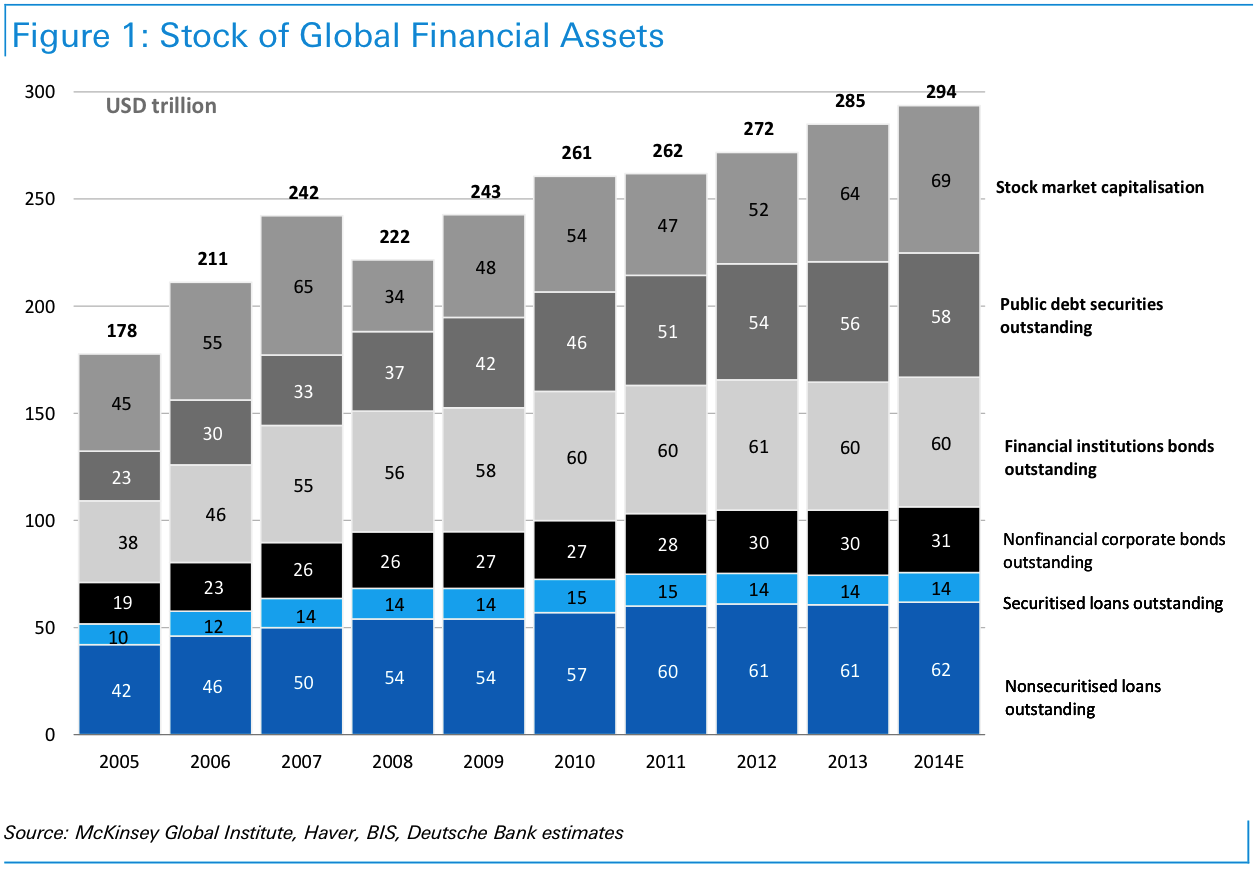

While it’s difficult to argue with Carl Icahn’s long-term investment track record, currently there is little objective data (unemployment, yield curve, corporate profits, GDP, etc.) signaling an imminent recession or economic collapse. Whether you are an optimist or pessimist, there is no doubt we have come a long ways since the lows of 2009 – see Global Stock Market chart below:

Source: Mark Perry (Carpe Diem)

The rapid price appreciation has been undeniable, but Mr. Icahn and other equity bears may be missing the forest for the trees. There has been a disproportional increase in the value of bond assets versus equity assets. More specifically, as can be seen from the chart below, the value of global financial assets increased an estimated +21.5% to $294 trillion from 2007 to 2014. Of the $52 trillion increase in global financial assets, 92% of the increase ($48 trillion) was derived from expanding debt obligations – not stocks. I’ve said it many times before, but if you are worried about the pricking of an equity bubble, make sure to buy some heavy-duty industrial ear plugs for eventual pricking of the bond bubble.

Source: Business Insider / McKinsey

Former Treasury Secretary and Harvard President Larry Summers recently commented in an interview that a potential “Grexit” could have unforeseen consequences just like the situations leading to the collapse of Lehman Brothers, Long Term Capital Management, and the subprime market. At the time, those particular circumstances were underestimated and characterized as being “contained”. Today, we are hearing the opposite regarding Greece.

In a post financial crisis world, every financial molehill is made into a crisis mountain as it spreads through social media and appears on every TV show, blog, newspaper, and magazine article. In a post financial crisis world characterized with ultra-low central bank interest rate policies, a combination of excessive conservatism from individual investors and opportunistic corporate actions (e.g., share buybacks and M&A), has led to a lopsided increase in debt issuance. Case in point is the bloated debt balances held by the Greek government. There will inevitably be pain associated with a Greek default and potential exit from the euro, but due to its size (<2% of European GDP), Greece should be treated more like a pimple than a body rash.

If you want to reach your financial goals, you need to prudently manage your risk through a broad asset allocation and realize that experiencing turbulence is part of the investing game. The impending Greece default will not be the first financial crisis, nor the last one. Extreme growth in debt should be more of a concern than a tiny, financially irresponsible country missing a debt payment. But rather than panicking, it is wiser to maintain a long-term investment strategy coupled with a globally diversified portfolio across asset classes, which will allow you to not miss the forest for the trees.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Standing on the Shoulders of a Growth Giant: Phil Fisher

Sir Isaac Newton

Since it’s Father’s Day weekend, it seems appropriate to write about about the “Father of Growth Investing”…Phil Fisher.

It was English physicist, astronomer, philosopher, and mathematician Sir Isaac Newton who in 1675 stated, “If I have seen further it is by standing on the shoulders of giants.” Investors too can stand on the shoulders of market giants by studying the timeless financial knowledge from current and past market legends. The press, all too often, focuses on the hot managers of our time while forgetting or kicking to the curb those managers whom are temporarily out of favor. Famous and enduring value managers typically have gained the press spotlight, rightfully so in the case of current greats like Warren Buffett or past talents like Benjamin Graham, because they managed to prosper through numerous economic cycles. However, when it comes to growth legends like Phil Fisher, author of the must-read classic Common Stocks and Uncommon Profits, many people I bump into have never heard of him. Hopefully that will change over time.

The Career

Born on September 8, 1907, Mr. Fisher lived until the ripe age of 96 when he passed on March 4, 2004. Fisher was no dummy – he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. His son, Ken, currently heads his own investment firm, Fisher Investments, writes for Forbes magazine, and has authored multiple investment books. Unlike his dad, Ken has more of a natural bent towards value stocks.

Buy-And-Hold

Philip A. Fisher

Phil Fisher’s iconic book, Common Stocks and Uncommon Profits, was published in 1958. Mr. Fisher believed in many things and perhaps would have been thrown under the bus today for his long-term convictions in “buy-and-hold.” Or as Mr. Fisher put it, “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. Generally, he gave initial stock purchases a three-year leash before considering a change to his investment position. If the conviction to purchase a stock for such duration is not present, then the investment opportunity should be ignored.

Fisher’s concentration on growth stocks also shaped his view on dividends. Dividends were not important to Fisher – he was more focused on how the company is investing retained earnings to achieve its earnings growth. Like Fisher, Peter Lynch is another growth hero of mine that also felt there is too much focus on the Price/Earnings (PE) ratio rather than the long-term earnings potential.

“Scuttlebutt”

Another classic trademark of Fisher’s investing style was his commitment to fundamental research. He was focused on accumulating data covering a broad range of areas including, customers, suppliers, and competitors. Fisher also emphasized factors like market share, return on invested capital, margins, and the research & development budget. What Mr. Fisher called his varied approach to gathering diverse sets of information was “scuttlebutt.”

Buying & Selling Points

Although Fisher believed firmly in buy and hold, he was not scared to sell when the firm no longer met the original buying criteria or his original assessment for purchased was deemed incorrect.

When buying, Fisher preferred to buy stocks in downturns or temporary problems – contrary to your typical momentum growth manager today (read article on momentum). Fisher has this to say on the topic: “This matter of training oneself to not go with the crowd but to be able to zig when the crowd zags, in my opinion, is one of the most important fundamentals of the investment success.”

Learning from Mistakes

Like all great investors I have studied, Phil Fisher also believed in learning from your mistakes:

“I have always believed that the chief difference between a fool and a wise man is that the wise man learns from his mistakes, while the fool never does.”

He expanded on the topic by saying the following:

“Making mistakes is inherent cost of investing just like bad loans are for the finest lending institutions. Don’t blindly accept dominant opinion and don’t be contrary for the sake of being contrary.”

I could only dream of having a fraction of Mr. Fisher’s career success – he retired in 1999 at the age of 91 (not bad timing). As my investment management and financial planning firm matures (Sidoxia Capital Management, LLC), I will continue to study the legendary giants of investing (past and present) to sharpen my investing skills.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in MSI, BRKA/B, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Who Gives a #*&$@%^?!

The stock market is just a big rigged casino, fueled by a reckless money printing Fed that is artificially inflating a global asset bubble, right? That seems to be the mentality of many investors as evidenced by the lack of meaningful domestic stock fund buying/inflows (see also Digesting Stock Gains). Underlying investor skepticism is a foundation of mistrust and detachment caused by the unprecedented 2008-09 financial crisis, when regulators fell asleep at the switch.

Making matters worse, the proliferation of the Internet, smart phones, and social media, has forced investors to digest a never-ending avalanche of breaking news headlines and fear mongering. Here is a partial list of the items currently frightening investors:

- Interest Rates: Will the Federal Reserve raise interest rates in June or September?

- Volatility: The Dow is up 200 points one day and then down 200 the next day. Keep me away.

- Greece: One day Greece is going to exit the eurozone and the next day it’s going to reach a deal with the IMF (International Monetary Fund) and European leaders.

- Terrorism / Middle East: ISIS is like a cancer taking over the Middle East, and it’s only a matter of time before they invade our home soil. And if ISIS doesn’t get us, then the Iranian boogeyman will attack us with their inevitable nuclear weapons.

- Inflation: The economy is slowing improving and as we approach full employment in the U.S., wage pressure is about to kick inflation into high gear. After falling significantly, oil prices are inching higher, which is also moving inflation in the wrong direction.

- Strong Dollar: Now that Europe is copying the U.S. by implementing quantitative easing, domestic exports are getting squeezed and revenue growth is slowing.

- Bubble? Stocks have had a monster run over the last six years, so we must be due for a crash…correct?

Seemingly, on a daily basis, some economist, strategist, analyst, or talking head pundit on TV articulately explains how the financial markets can fall off the face of the earth. Unfortunately, there is a problem with this type of analysis, if your evaluation is solely based upon listening to media outlets. Bottom line is you can always find a reason to sell your investments if you listen to the so-called experts. I made this precise point a few years ago when I highlighted the near tripling in stock prices despite the barrage of bad news (see also A Series of Unfortunate Events).

While I am certainly not asking anyone to blindly assume more risk, especially after such a large run-up in stock prices, I find it just as important to point out the following:

“Taking too much risk is as risky as not taking enough risk.”

In other words, driving 35 mph on the freeway may be more life threatening than driving 75 mph. In the world of investing, driving too slowly by putting all your savings in cash or low-yielding securities, as many Americans do, may feel safe. However this default strategy, which may feel comfortable for many, may actually make attaining your financial goals impossible.

At Sidoxia, we create customized Investment Policy Statements (IPS) for all our clients in an effort to optimize risk levels in a Goldilocks fashion…not too hot, and not too cold. Retirement is supposed to be relaxing and stress free. Do yourself a favor and create a disciplined and systematic investment plan. Being apathetic due to an infinite stream of worrisome sounding headlines may work in the short-run, but in the long-run it’s best to turn off the noise…unless of course you don’t give a &$#*@%^ and want to work as a greeter at Wal-Mart in your mid-80s.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Will Rising Rates Murder Market?

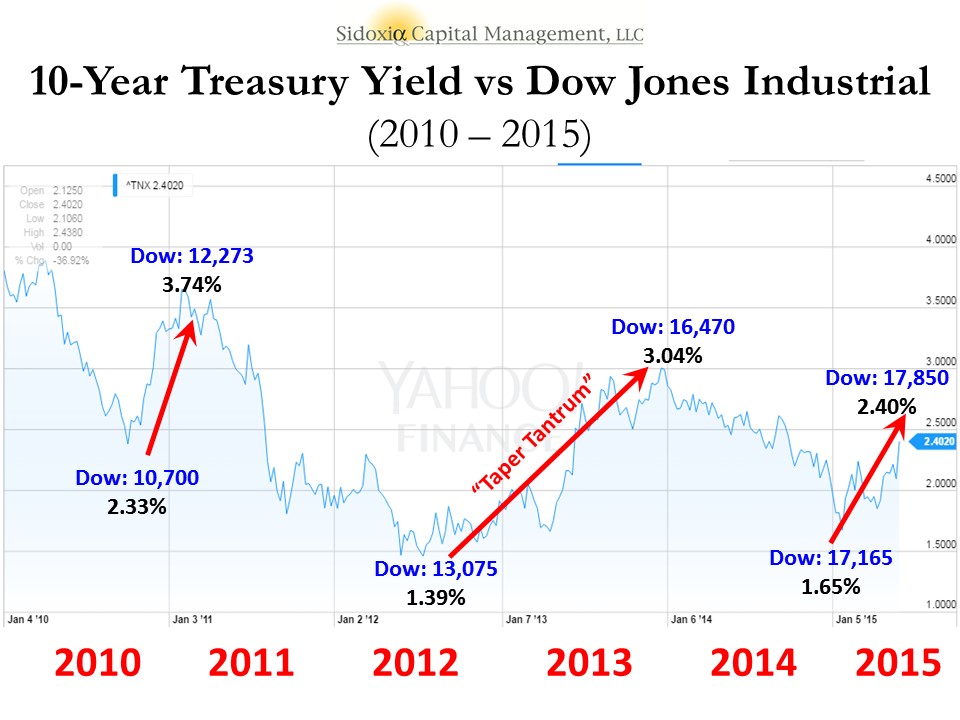

After an obituary of Mark Twain had been mistakenly published in the United States, Twain sent a cable from London stating, “The reports of my death have been greatly exaggerated.” Similar reports about the death of the stock market have been prematurely published as well. If you were to listen to the talking heads on TV or other self-proclaimed media pundits, the prevailing opinion is that rising interest rates will murder the stock market. In reality, the benchmark 10-Year Treasury Note has risen a whopping 0.23% so far this year. Could this be a start of a more prolonged increase in interest rates? It is certainly possible. Most investors have a very short memory because we have seen this movie before. It was just two short years ago that we witnessed a near doubling of 10-Year Treasury yields exploding from 1.76% to 3.03% in 2013. Did the stock market crater? In fact, quite the contrary. The S&P 500 index catapulted higher by a whopping +30%.

Even if we go back a litter further in recent history, interest rates were quite a bit higher. For example in early 2010, 10-Year Treasury yields breached 4.0%. Where was the Dow Jones Industrial index then? A mere 11,000 vs 17,850 today. Or in other words, when interest rates were significantly higher than today’s 2.40% yield, the stock market managed to climb +62% higher. Not too shabby, eh? As I have talked about in the past (see Don’t Be a Fool, Follow the Stool), there are other factors besides interest rates that are contributing to positive stock returns – primarily profits, valuations, and sentiment are the other key factors in determining stock prices. Suffice it to say, over the last five years, stocks have survived quite well in the face of multiple interest rate spikes; the 2013 “Taper Tantrum”; and the subsequent completion of quantitative easing – QE (see chart below).

Underlying Chart: Yahoo Finance!

Yield Curve on the Side of Bulls

Despite the trepidation over a series of potential Fed rate hikes, stocks continue to grind higher. If the fears are based on the expectation of a slowing economy on the horizon, then we would generally see two things happening. First, rising short-term interest rates would cause the yield curve to flatten, and then secondly, the yield curve would invert (typically a leading indicator for a recession). Currently, there are no signs of flattening or inverting. Actually, the recent better than expected jobs report for May (280,000 jobs added vs. estimate of 226,000) created a steeper yield curve – long-term interest rates increased more than short-term interest rates. Just as I wrote in 2009 about the recovery (see Steepening Yield Curve Recovery), right now the bond market is flashing recovery…not slowdown.

In the face of the mini-interest rate spike, bank stocks are also signaling economic recovery – evidenced by the 2.75% surge in the KBW Bank Index (KBX) last week. If there were signs of dark clouds on the horizon, a flattening yield curve would squeeze bank net interest margins and profits, which ultimately would send bank investors to the exit. That phenomenon will eventually happen later in the economic cycle, but right now investors are voting in the opposite direction with their dollars.

The media, economists, strategists, and other nervous onlookers will continue fretting over the Federal Reserve’s eventual rate increases. As long as dovish Janet Yellen is at the helm of the Fed, future rate increases will be measured, and rather than murdering the stock market, the policies will merely reflect a removal of the economy from artificial life support.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

{kind=link}

{kind=link}