Posts filed under ‘Trading’

Markets Surge Higher Despite Shutdown Anxiety Fire

Wars rage on in Ukraine and Gaza, political violence is on the rise at home, tariff-driven inflation remains debated, and anxiety over a looming government shutdown is intensifying. On the surface, this might sound like the perfect recipe for a market meltdown. But Wall Street seems unfazed. In fact, U.S. equities pushed to new record highs again this month, continuing the bull market’s relentless advance in the face of these concerns.

Here is a market performance snapshot for the month:

- S&P 500: +3.5% (+13.7% year-to-date)

- Dow Jones Industrial Average: +1.9% (+9.1% year-to-date)

- NASDAQ Composite: +5.6% (+17.3% year-to-date)

What’s fueling the optimism?

• A Strong Economy: The economy just produced a final +3.8% GDP growth for the 2nd quarter, and the Atlanta Federal Reserve is forecasting an even stronger economy for the 3rd quarter of +3.9% (see below).

• Robust Corporate Earnings: S&P 500 corporate profits surged by +11.8% in the 2nd quarter and consensus estimates call for 3rd quarter growth of +7.9%. Historically, CEOs tend to set conservative forecasts, therefore actual results often exceed low-bar expectations. Therefore, it’s very possible that Q3 earnings growth could achieve double-digit growth levels once again.

• A.I. Drive Still Alive: With trillions of dollars in A.I. spending plans already announced, hungry investors once again gobbled up A.I. tech stocks last month. For instance, Oracle Corp’s (ORCL) stock jumped +24% for the month in large part driven by a $317 billion increase in backlog orders during the company’s first fiscal quarter. Reportedly, the majority of the massive increase in orders came from one customer, OpenAI – the brains behind the A.I. juggernaut, ChatGPT. The rise in Oracle’s share price temporarily propelled CEO Larry Ellison past Tesla’s (TSLA) CEO Elon Musk as the world’s richest person, before markets began critically questioning whether OpenAI’s CEO (Sam Altman) can ultimately fund the hundreds of billions of dollars in Oracle commitments.

Source: Atlanta Federal Reserve

Shutdown Jitter History

Market anxiety has shifted from a hypothetical government shutdown nightmare to a scary reality, given the funding deadlines have already lapsed. Many investors are asking what this means for stocks. Fortunately, government shutdowns are nothing new. Our country has flourished over the last 50 years despite experiencing around two dozen shutdowns, many of which only lasted a few hours, a few days, or a few weeks. According to Kiplinger, since the 1970s, the stock market has averaged a +0.3% return during shutdown periods (see chart below).

Source: Kiplinger

In fact, the longest shutdown on record occurred most recently from December 2018 to January 2019 (35 days during President Trump’s first term) and resulted in a sharp +10% gain (see chart below).

Source: Kiplinger / YCharts

The partisan finger-pointing will continue, but history suggests that shutdowns are short-term noise with little bearing on long-term market direction. Long-term investors understand there is never a shortage of concerns during bad times (e.g., potential recessions, job losses, credit defaults, bankruptcies, etc.), or good times as well (e.g. fear of inflation, restrictive monetary policy, politics, etc.). Turning off the TV is often the best course of action (see also – Turn Off the TV).

What’s Next? Looking Ahead After more than 30 years of investing—including weathering the dot-com tech sense of purpose collapse in 2000—I’ve learned that markets always have a tendency of climbing a wall of worry, so it’s better to not react emotionally to daily news headlines. Rather, it’s better for investors to stay focused on those market leading, innovative companies and concentrate on those sectors experiencing long-term secular trends.

As we enter Q4 and head toward 2026, A.I. remains the defining theme. Since the launch of ChatGPT in November 2022, the S&P 500 has surged +24% in 2023, +23% in 2024, and +14% so far in 2025. Unfortunately, trees do not grow to the sky forever.

At Sidoxia Capital Management, we understand that valuations currently are stretched on a historic basis and that markets never move in a straight line. As a result, a correction at some point in stock prices should not come as a surprise to anyone. Nevertheless, whether you’re bullish on the productivity gains from large language models (LLMs) or skeptical of over-investment and hype, one thing is clear: A.I. is here to stay, and it doesn’t matter if you believe the government shutdown flames will grow into an inferno or fizzle out in smoke, which is usually the case.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in ORCL, TSLA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

A.I. Field of Dreams

In the 1989 Academy Award–nominated film Field of Dreams, the lead character Ray Kinsella (played by Kevin Costner) hears a mysterious voice whisper, “If you build it, he will come.” Acting on blind faith, Ray builds a baseball diamond in the middle of his Iowa cornfield, risking financial ruin. Against all logic, the field draws a flood of visitors.

Today, a similar “field of dreams” is being built—not with corn, but with data centers. Instead of baseball players, it is artificial intelligence (AI) models, applications, and users who are coming.

The Market’s AI Momentum

The AI boom has already reshaped markets with all three benchmarks hitting record highs. Last month, the S&P 500 climbed +1.9%, while the NASDAQ rose +1.6% and Dow Jones Industrial Average surged +3.2%. Year to date, the indexes are up +10%, +11%, and +7%, respectively.

Behind this surge lies an unprecedented wave of AI infrastructure investment. Hyperscalers—Amazon.com (AMZN), Microsoft Corp. (MSFT), Google-Alphabet (GOOGL), Meta Platforms (META), and others—are pouring hundreds of billions into AI, much of it flowing directly to NVIDIA Corp. (NVDA), the undisputed leader in GPUs (Graphic Processing Units) powering the world’s AI engines. How large is the spending? NVIDIA CEO Jensen Huang estimates $3 trillion to $4 trillion will be spent this decade to fuel the AI revolution.

Source: Visual Capitalist

The Scale of AI’s Buildout

To put this into perspective:

- Amazon is projected to spend over $100 billion in 2025 alone, more than its cumulative capital expenditures from 2000–2020 combined.

Meta is constructing its $10 billion+ Hyperion data center in Louisiana—a sprawling 4 million sq. ft. complex across 2,250 acres, powered by a $4 billion natural gas plant. The footprint is so gargantuan it could cover much of Manhattan (see graphic below).

- xAI’s Colossus, a 750,000 sq. ft. data center in Memphis, Tennessee was completed in just 122 days—equivalent to building 418 homes in half the time it normally takes to construct one house (see slide below).

Source: BOND (Global Technology Investment Firm)

This breakneck pace of spending underscores the urgency and competitive pressure driving the global AI arms race.

The Origin of the AI Floodgates Opening

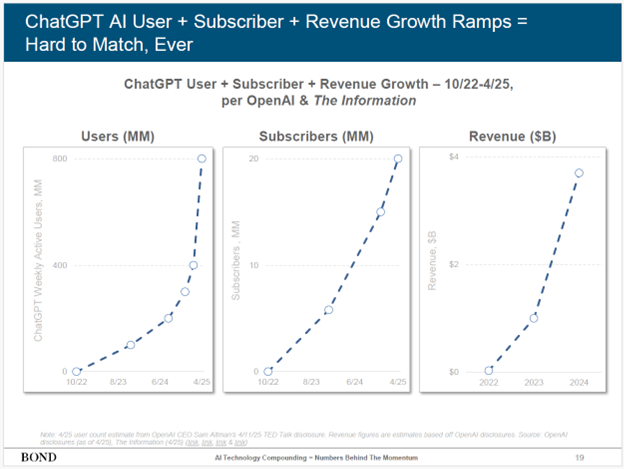

The spark was lit on November 30, 2022, when OpenAI released its LLM (large language model) called ChatGPT. Within two months, it amassed 100 million users.

Today, ChatGPT’s metrics have blasted much higher (see slide below):

- 800 million weekly active users

- 20 million paid subscribers

- $3.7 billion in revenue (as of April 2025)

Source: BOND (Global Technology Investment Firm)

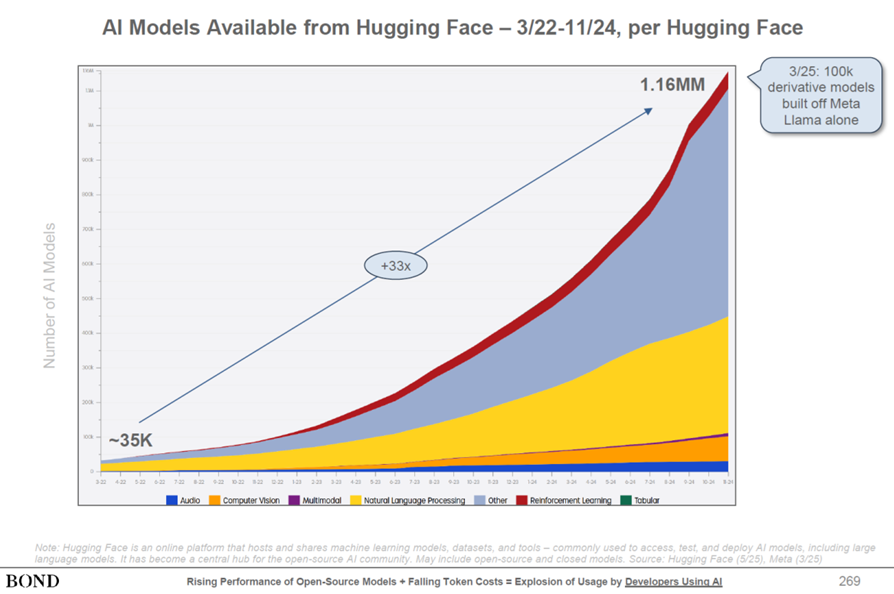

But OpenAI is far from alone. Google (Gemini), xAI (Grok), Anthropic (Claude), Meta (LLaMA), Amazon (Titan), Perplexity, and DeepSeek are all competing with their own LLMs. In total, over 1 million machine learning models now exist (see slide below) — each requiring costly compute power and pricey data centers.

Source: BOND (Global Technology Investment Firm)

Bubble or Productivity Breakthrough?

With trillions flowing into AI, a natural question arises: Is this a bubble?

Even OpenAI CEO Sam Altman admits we’re in an AI bubble :

“When bubbles happen, smart people get overexcited about a kernel of truth…Someone is going to lose a phenomenal amount of money… and a lot of people are going to make a phenomenal amount of money.”

Both realities can be true:

- Yes, hyperscalers are spending like “drunken sailors.”

- Yes, AI demand and productivity benefits are real and growing exponentially.

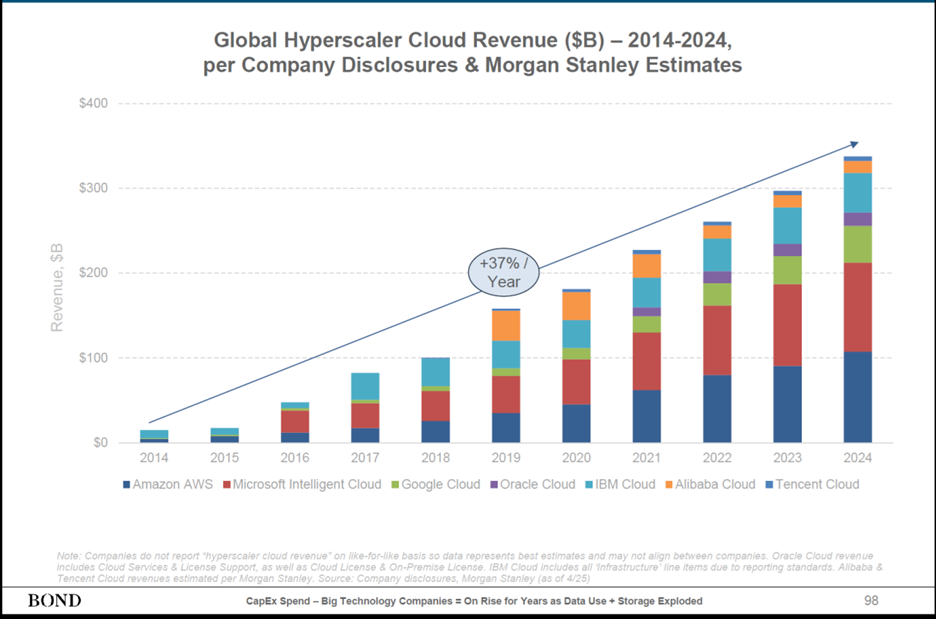

Consider the trajectory of global cloud revenues: from nearly $0 a decade ago to $300 billion today—a +37% CAGR (see chart below).

Source: BOND (Global Technology Investment Firm)

And the primary reason for cloud growth can be attributed to AI productivity benefits. A recent SAP survey found that workers using AI save nearly one hour per day on average. That’s transformative for companies: higher productivity without needing proportional hiring.

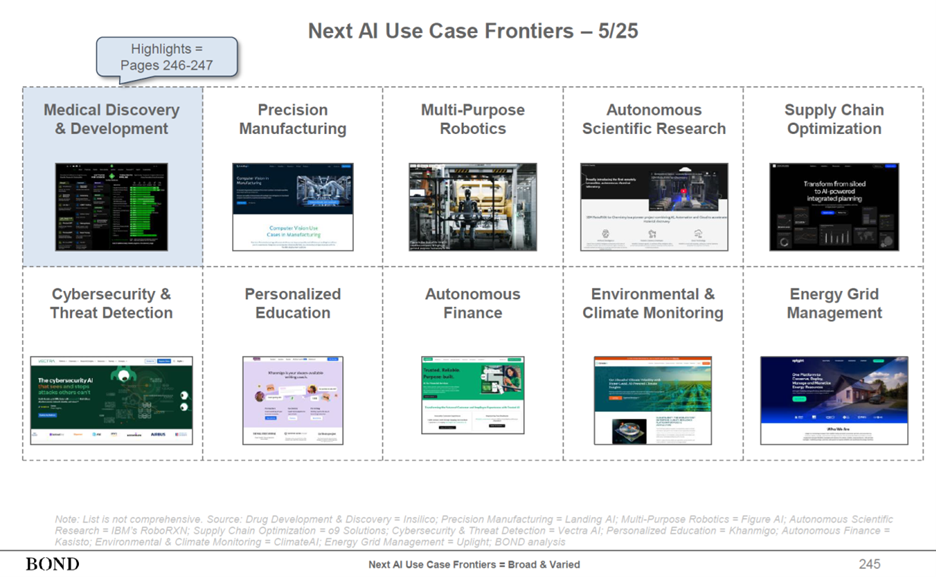

AI Use Cases Expanding Aggressively

AI’s applications now span nearly every sector (see slide below):

- Technology – software engineering, code generation

- Customer Service & Marketing – customer support and call centers

- Transportation – autonomous vehicles and logistics

- Healthcare – drug discovery and development

- Supply Chains – precision manufacturing and optimization

- Automation – multi-purpose robotics

- Cybersecurity – threat detection and prevention

- Education – personalized lessons and curriculums

- Energy – grid optimization and demand forecasting

Source: BOND (Global Technology Investment Firm)

The New Field of Dreams

Throughout history, every great leap—printing press, steam engine, electricity, internet—has required massive upfront investment before the payoff arrived. AI is following the same path. Today, we are in the midst of building a new AI Field of Dreams. However, now, the data centers are the new baseball fields. And as with Ray Kinsella’s diamond, the masses are indeed coming.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GOOGL, META, AMZN, MSFT, NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SAP or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Trade & OBBB Deals Sealed, Fed Dread, and AI/Meme Dreams

As the stock market reached new all-time highs, investors had plenty to juggle—both in Washington, D.C., and on Wall Street. The S&P 500 climbed +2.2%, the NASDAQ surged +3.7%, and the Dow Jones Industrial Average edged higher by +0.1% for the month.

The One Big Beautiful Bill

What has fueled the rally? A major catalyst was President Trump’s signing of the One Big Beautiful Bill Act (OBBB) on July 4th. The nearly 900-page legislation spans a broad range of economic issues including tax reform, healthcare, energy policy, and national security.

According to the Congressional Budget Office (CBO), the combined impact of tax cuts, new spending, and spending reductions will result in a net cost of $3.4 trillion over 10 years (see chart above). Supporters of the bill argue that this projection underestimates the long-term stimulative effects of tax relief and strategic investments. Whether the deficit widens as the CBO projects, or narrows thanks to a stronger, growing economy, remains to be seen.

Trade Deals Sealed

Since Liberation Day on April 2nd, trade negotiations have progressed unevenly. The administration’s reciprocal tariff hikes were paused through August 1st to allow final agreements to be reached. Following months of tough rhetoric, multiple major trading partners ultimately signed deals before the deadline—including the European Union, Japan, the United Kingdom, Vietnam, and South Korea—thereby avoiding punitive tariffs.

Talks with our two key trading partners, Mexico and Canada, remain ongoing. While Mexico was granted a 90-day extension amid constructive dialogue, Trump slapped a 35% tariff on Canada (from 25%) due to what the White house said was “continued inaction and retaliation.” The tariff pause with China stops on August 12th.

Here’s a list of the new country tariffs released by the president late yesterday: CLICK HERE

Regardless of all the tariff uncertainty, investor sentiment improved last month as the terms of the signed deals were significantly milder than originally feared.

Adding to the optimism:

- Core inflation in June remained modest at 2.8% (Reuters), and

- Tariff revenues collected through July reached $126 billion, beating initial estimates (Politico) – see chart below. Strategist Ed Yardeni forecasts that 2025 tariff revenues could surge to between $400 billion and $500 billion (Barron’s).

Source: Politico

Fed Dread

Of course, when it comes to financial markets, everything can’t just be rainbows and unicorns without something for investors to worry about—and this month, a key concern remains Federal Reserve policy. Critics, including the president, argue that interest rates are too high, with the Federal Funds Rate currently set at 4.25%–4.50% (Yardeni Research) – see chart below.

By comparison:

- The European Central Bank’s Deposit Facility Rate stands at 2.00%, and

- The Bank of Japan’s overnight rate is only 0.50%.

Source: Yardeni Research

Fed Chair Jerome Powell has held off on further cuts, citing the need for more clarity on inflation and labor market data, especially in light of recent tariffs. Ironically, when the Fed last cut rates by -1.00% late last year, the 10-year Treasury yield rose by roughly +1% (see chart above), reflecting fears of rising inflation.

This week, the Fed held rates steady for the fifth consecutive meeting (YouTube). Notably, two FOMC members—Christopher Waller and Michelle Bowman—dissented, voting in favor of a rate cut. It was the first dual dissent by Fed governors in over 30 years—a clear signal of division inside the central bank.

Meme Dreams

With the major indexes at new highs, speculation has returned in full force. Money-losing, struggling companies like Opendoor Technologies, GoPro Inc., and Kohl’s Corp. saw their shares double, triple, or even quadruple over a short span (WSJ) – see chart below. We saw similar trends occur during the GameStop and AMC meme craze in 2021.

Source: The Wall Street Journal

Adding fuel to the fire:

- Cryptocurrency prices are on the rise again.

- Euphorically priced IPOs (Initial Public Offerings) like Figma, Inc. (FIG), which more than tripled in value ($115 per share) on its first trading day above its offering price ($33 per share) valuing the company above $50 billion – more than 30 times next year’s forecasted revenues.

- SPACs (Special Purpose Acquisition Companies)—often criticized for poor governance—are staging a comeback.

Combined, all these trends raise concerns about froth, which investors have experienced at previous peaks.

Climb in AI Stocks Persists

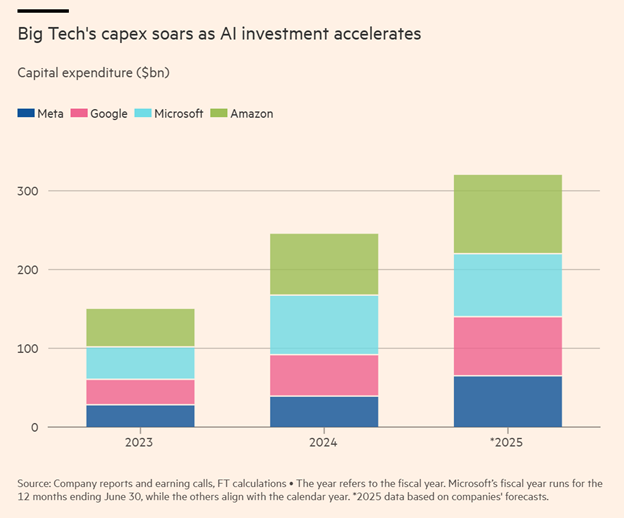

No discussion of this rally would be complete without highlighting the AI mega-cap giants. Companies like Alphabet (Google), Meta (Facebook), Microsoft, and Amazon all recently announced capital expenditures for 2025 that will likely exceed an astounding $350 billion —most of it allocated to AI infrastructure.

Meanwhile, NVIDIA Corp., the AI-chip juggernaut and major beneficiary of all the AI capex, has seen its share price soar +63% in just three months, reaching a staggering $4.4 trillion market value.

Source: Yardeni Research

Valuations High but Fundamentals Remain Strong

While stock valuations remain elevated above historical averages (the S&P 500 red line trades at 22x forward earnings, according to Yardeni) – see chart above, the macro backdrop remains supportive:

- The economy is strong,

- Unemployment is low,

- Corporate profits are growing, and

- Monetary policy may turn more accommodative in coming months.

In this momentum environment, the market should continue its productive juggling, but if the frothy or economic winds worsen, investors should be prepared for a dropped ball.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GOOGL, META, AMZN, MSFT, NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in OPEN, GPRO, KSS, GME, AMC, FIG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Mideast War an Investor Bore as Markets Soar

If I told you at the beginning of the year that the U.S. would bomb key nuclear sites in Iran, would you have guessed that Middle East stability would follow—and that global financial markets would soar to record highs? Personally, I wouldn’t have bet on that outcome. But that’s exactly what happened last month. While geopolitical dynamics remain fluid, markets shrugged off the chaos. The S&P 500 rallied +5.0%, the Dow Jones Industrial Average climbed +4.3%, and the NASDAQ catapulted +6.6%, powered largely by artificial intelligence stocks like NVIDIA Corp., which surged +16.9% for the month to a market value of $3.9 trillion (more on AI below). This is an important reminder that trading off of news headlines is a fool’s errand.

Economy Resilient Despite Tariffs and Geopolitical Turmoil

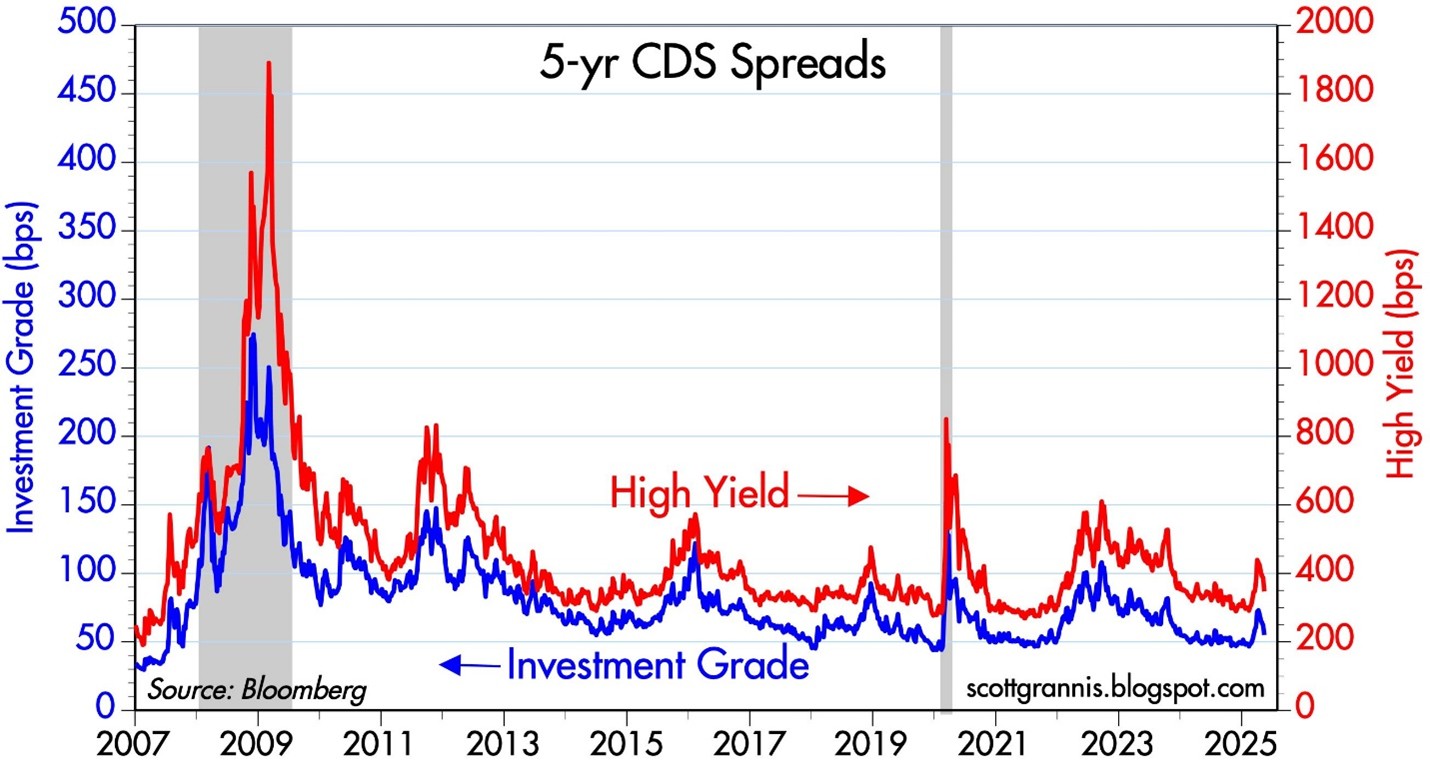

Source: Calafia Beach Pundit

Credit Default Swaps (CDS) act as insurance contracts that protect investors against corporate debt defaults. During financial stress—like the 2008 crisis or the COVID crash in 2020—CDS prices surge as investors seek protection. Today, however, CDS prices are falling across both high-yield (junk bonds) and investment-grade (Blue Chip) debt. As seen in the chart above, the cost to insure corporate bonds has declined steadily over the past two years. This signals bond investors aren’t worried about a recession or a wave of defaults, despite tariff policy uncertainty, geopolitical risk, and modest GDP growth.

Inflation Tame as Tariffs Loom

President Trump has repeatedly criticized Fed Chair Jerome Powell for not cutting interest rates, calling him everything from a “dummy” to a “major loser” and a “stupid person” to a “numbskull”. While the name-calling is colorful, the economic pressure is real: U.S. GDP contracted -0.5% in Q1 2025. Powell, however, wants to see the full impact of upcoming tariffs before making a move. . A new tariff deadline looms on July 9th, and the market is anxiously awaiting clarity. But even if tariffs are implemented, many economists believe the inflationary impact will be temporary—what’s known as a one-time price shock.

Source: Calafia Beach Pundit

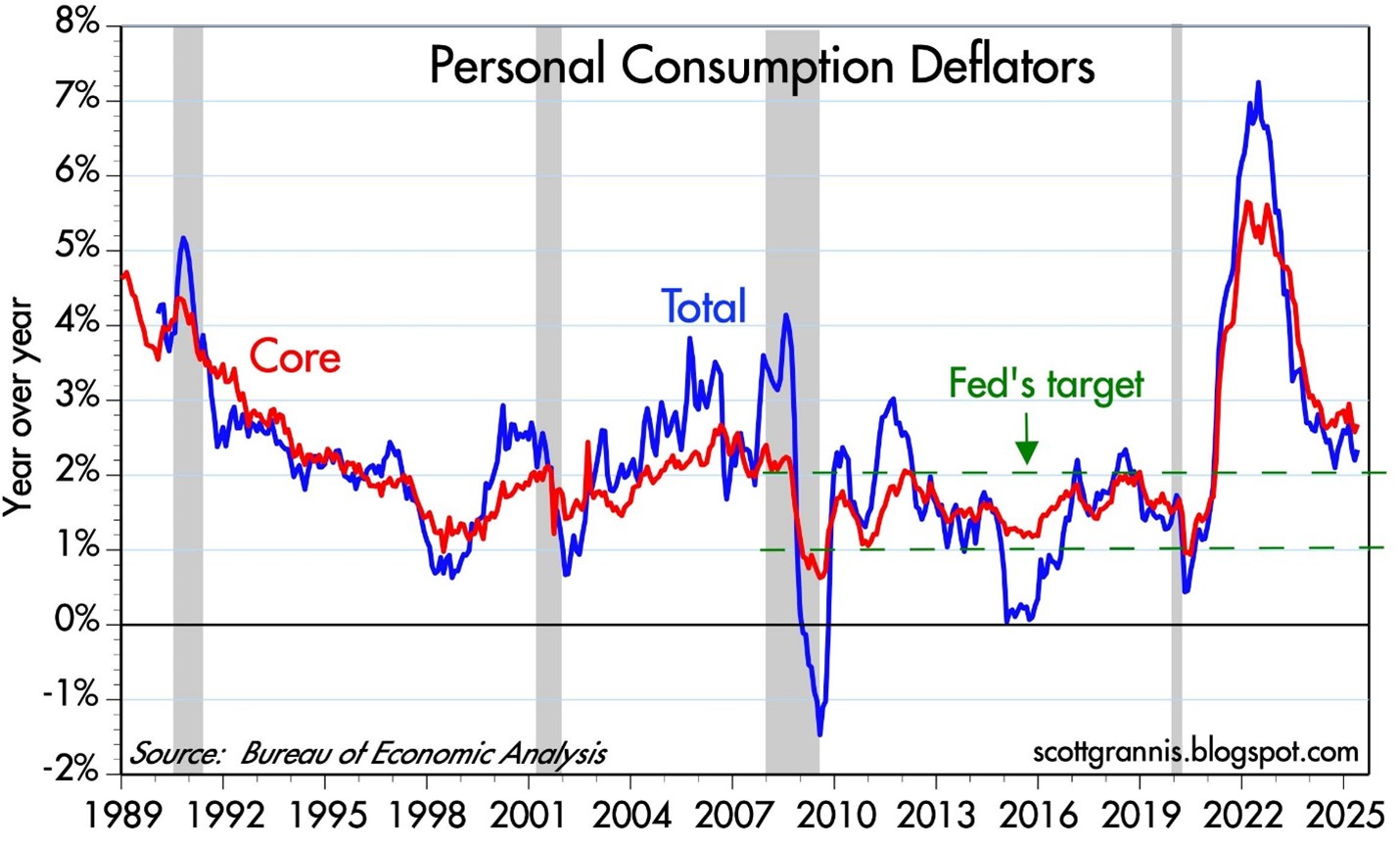

The Fed’s preferred inflation gauge—the Personal Consumption Expenditure (PCE) index—has been easing and is now near the 2% target (see chart above). With inflation cooling, Trump’s case for rate cuts gains credibility. Still, the Fed appears in no rush. It will take time to understand the lasting effects of the tariff rollout.

AI Wave Fueling Markets

For a generation, the semiconductor revolution has quietly powered innovation, guided by Moore’s Law—the principle that chip performance doubles roughly every two years (see my article The Traitorous 8). Sixty years after Gordon Moore wrote his seminal article, “Cramming More Components onto Integrated Circuits”, the power of software is catching up. NVIDIA’s Grace Blackwell GB200 chip contains an astronomical 208 billion transistors, supercharging AI software models like ChatGPT.

The AI revolution is fueling trillions in global investment and rapidly transforming industries – from data centers and self-driving cars to robotics and drug discovery. It’s important to realize that this AI arms race is not just occurring in the United States. AI investment spending extends way beyond Silicon Valley to countries like Saudi Arabia, Singapore, and China.

The AI boom is not a U.S.-only phenomenon. Countries like China, Saudi Arabia, and Singapore are pouring capital into AI, creating a global arms race in tech. In the U.S., the four biggest hyperscalers—Amazon, Microsoft, Google, and Meta—are projected to spend over $300 billion on capital expenditures in 2025 alone (see chart below).

To illustrate the scale: Amazon is forecasted to spend more than $100 billion in CapEx this year. For context, that’s 40% more than the company spent over the entire 2000–2020 period combined.

Source: The Financial Times

The Stargate Initiative: AI Infrastructure on a Galactic Scale

A prime example of the AI gold rush is the $500 billion Stargate initiative, with Phase 1 already underway in Abilene, Texas (see rendering below). The initial construction includes two buildings totaling 1,000,000 square feet. Ultimately, the full project will cove about 1,000 acres and be powered by an on-site natural gas facility generating 360 megawatts—enough to support 300,000 homes.

A huge portion of the project costs are dedicated to the budget for NVIDIA super chips. Oracle Corp. has committed $40 billion to purchase 400,000 of NVIDIA’s GB200 chips, making this project a centerpiece of the global AI infrastructure boom. Just this week, Oracle also announced a new $30 billion cloud deal, which will soak up a good chunk of the data center supply created by the database and enterprise software company.

Source: CoStar

The Big Picture: Volatility and Opportunity

There’s no shortage of risk—geopolitics, inflation, Fed uncertainty, tariffs. But the economy is showing surprising resilience. If tariff clarity improves, interest rate cuts materialize, and AI capital spending accelerates, a “boring” market could rapidly turn into a soaring one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Turn Off TV – Emperor Media Has No Clothes!

Famous Danish author Hans Christian Andersen told a renowned fairy tale of an emperor who was conned into believing he is wearing an invisible suit. The crowd was too embarrassed to acknowledge his nakedness, so they pretend to not notice – until a young boy shouted, “The emperor has no clothes!”

Much like the fairy tale, when it comes to pointing out the many shortcomings of the financial media, I have no problem yelling, “The Emperor Media has no clothes!”

Media Spreads Fear and Misinformation

Mark Twain famously stated, “If you don’t read the newspaper, you’re uninformed. If you read the newspaper, you’re misinformed.” That sentiment rings especially true amid today’s swirl of alarming headlines. Here’s a sampling of recent media-induced worries:

- Global trade war caused by tariffs

- Declining value of the U.S. dollar

- Rising interest rates due to foreign debt sales

- Doubts over the U.S. dollar’s global reserve currency status

- Recession anxiety

- Stagflation fears

- Concerns about Executive Branch overreach

- Threats to remove the Federal Reserve Chairman

Is the sky falling? Is now the time to sell stocks, as the media often implies? Or are these risks being overstated and distorted by media outlets that chase monetary gains?

Issues are More Gray Than Black or White

Journalists – most of whom have little investing experience – like to authoritatively paint economic issues in black-or-white terms. But most reasonable people understand that these matters are complex, and the truth lies somewhere in the gray. To claim the media offers a balanced view of both the positives and negatives of complicated financial topics would be disingenuous.

I have been investing for over 30 years, and while I’ve never faced a global rebalancing of trade impacting trillions in economic activity, I’ve lived through far more uncertain times. Not only have my investments survived those volatile periods, but they have also thrived – repeatedly hitting new record highs.

F.U.D. Sells!

Does the media want you to believe the accurate, long-term stock market prosperity story? Hardly. As the saying goes, “If it bleeds, it leads.” Fear, uncertainty, and doubt (F.U.D.) sell more ads, subscriptions, newspapers, and magazines. The more blood, sweat, and anxiety in the headlines, the more money the media makes from distressed readers.

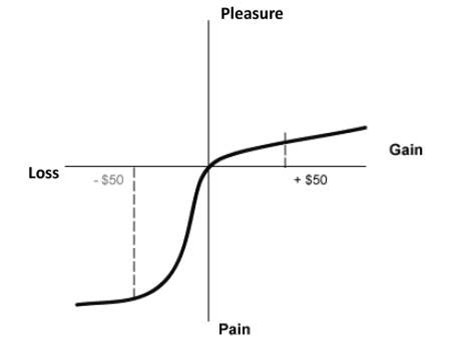

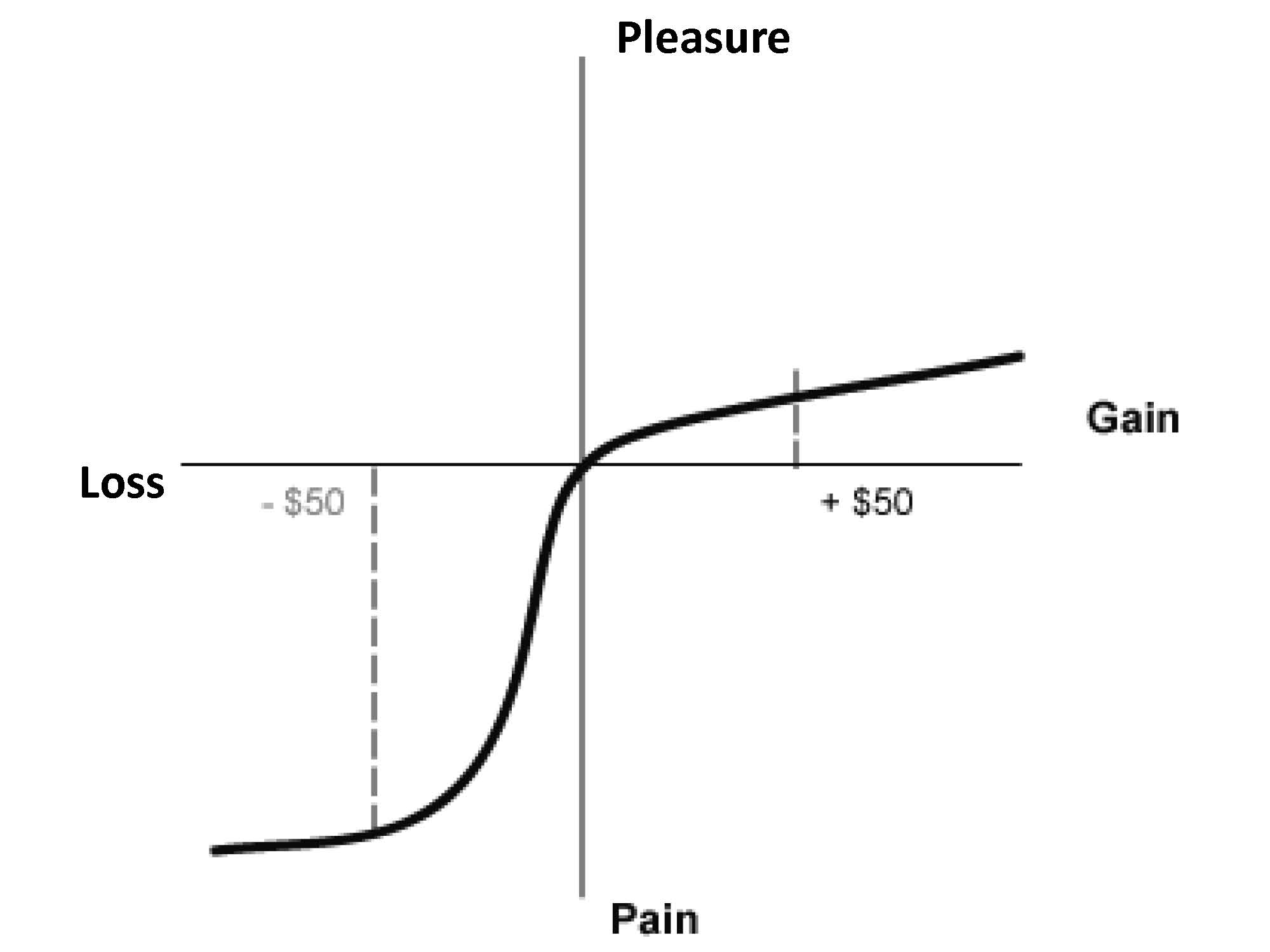

Behavioral finance pioneers, Nobel Prize winner Daniel Kahneman and Amos Tversky, showed that losses feel twice as painful as the pleasure of gains (see the Pleasure/Pain diagram below). Their Prospect Theory remains just as relevant today as when it was introduced in the late 1970s.

The greatest investor of all-time, Warren Buffett, once said, “Be fearful when others are greedy, and greedy when others are fearful.” Unfortunately, the media pushes the opposite mantra: “sell fear and buy greed.” When markets fall, they sell Armageddon. When markets soar, they sell nirvana. During periods of over-optimism, they also exploit FOMO (Fear of Missing Out) by feasting on investors’ emotional cycle of excitement.

Reassuring long-term investors that everything will be okay—or that dips are buying opportunities—doesn’t generate as much media profits and ad sales. Fear does.

History Doesn’t Repeat Itself, But It Often Rhymes

Too many investors suffer from short-term thinking and goldfish-like memory. But as Mark Twain wisely stated, “History doesn’t repeat itself, but It often rhymes.” And history has shown that listening to the media during times of extreme market volatility often leads to poor decisions.

Let’s take a look at some key examples where media-driven fear was more misleading than helpful over the decades:

The Nifty Fifty Collapse (1973-1974)

In the early 1970s, long before the “Magnificent 7” stocks came to the fore, we had the “Nifty Fifty” stocks. These large-cap blue chip stocks traded at lofty P/E (Price-Earnings) ratios and were seen as invincible before they came crashing down in 1973-1974. Suffice it to say, the media headlines were horrific during this period.

Here is some context for this period:

- The U.S. was exiting the Vietnam War

- Economy was undergoing a major recession

- Watergate scandal and presidential resignation

- 9% unemployment

- The Arab Oil Embargo

- Surging inflation

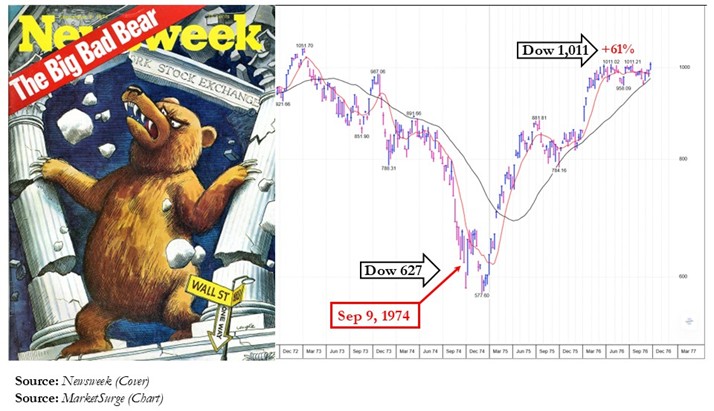

The media’s response? Doom and gloom. Here’s an example of this sentiment from the Newsweek cover, “The Big Bad Bear,” published on September 9, 1974.

For those who sold in fear, the results were disastrous. The Dow bottomed shortly after the magazine was released and the market rebounded +61% in less than two years. Panic was the wrong move.

“The Death of Equities” (1979)

Inflation plagued the 1970s, and just before one of the longest bull markets in history, BusinessWeek declared “The Death of Equities” on its now-infamous September 1979 cover. Once again, the media acted as a perfect contrarian indicator with the Dow quadrupling over the next decade.

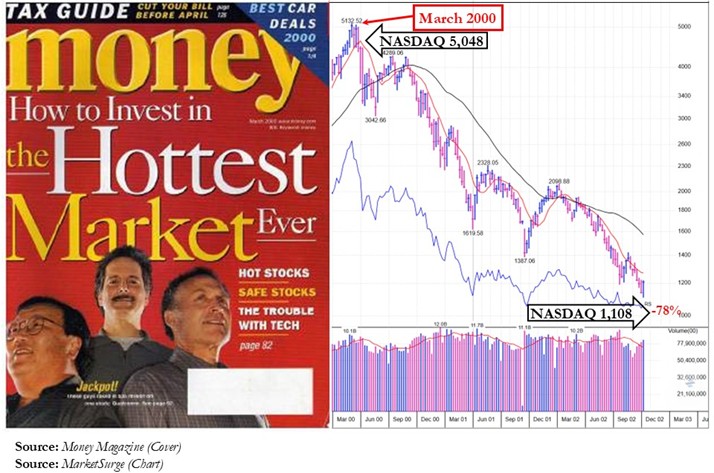

Dot-Com Bubble: “The Hottest Market Ever” (2000)

In March 2000, at the peak of the tech bubble, Money magazine ran a cover story: “How to Invest in the Hottest Market Ever.” Weeks later, the bubble burst. Suboptimal timing once again.

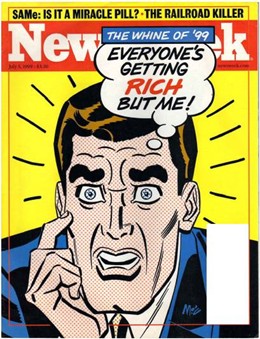

In that same timeframe, Newsweek captured the essence of FOMO with its July 5, 1999 cover: “Everyone Is Getting Rich but Me.” Right when risk was at its peak, most investors were blind to it and got sucked into the downdraft.

Source: NewsWeek

Financial Crisis – Depression 2.0 (2008)

In October 2008, the Time magazine cover encapsulated the zeitgeist of the period with a 1929 photo that included a line of desperate people waiting for food donations at a soup kitchen. Many feared a second Great Depression. Yet it was one of the best times in history to buy stocks with the Dow tripling over the next decade.

Brexit Panic (2016)

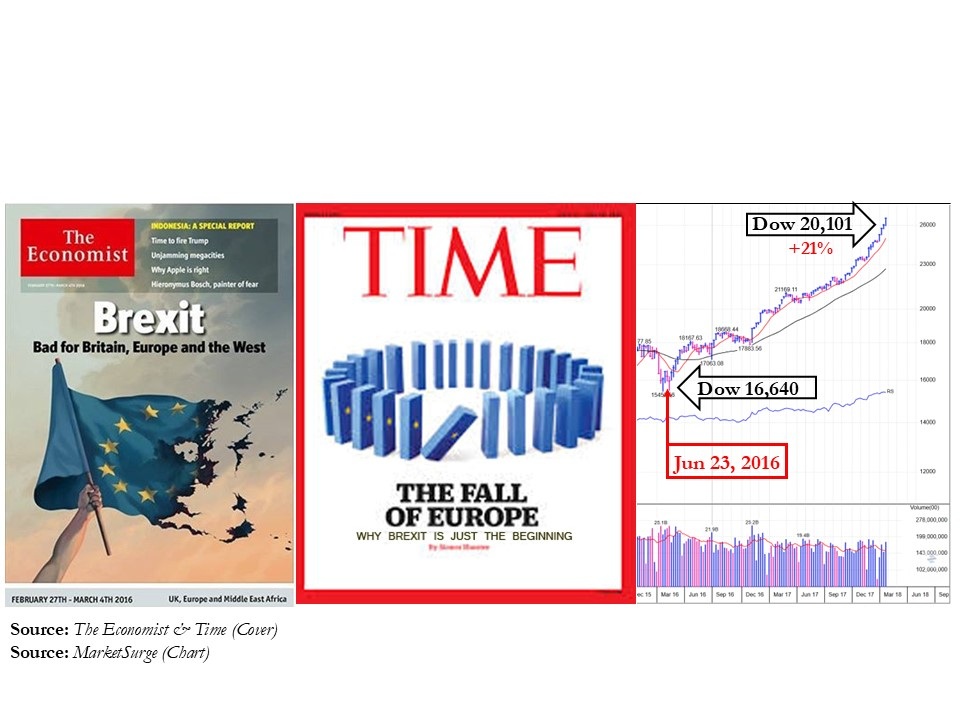

Media coverage around the U.K.’s Brexit vote to leave the EU (European Union) painted a picture of imminent recession and contagion. Instead, the media blitz surrounding Brexit turned out to be more molehill than mountain. Markets rebounded strongly and reached new highs in the subsequent months.

“Rocketman” and North Korea Missiles (2017)

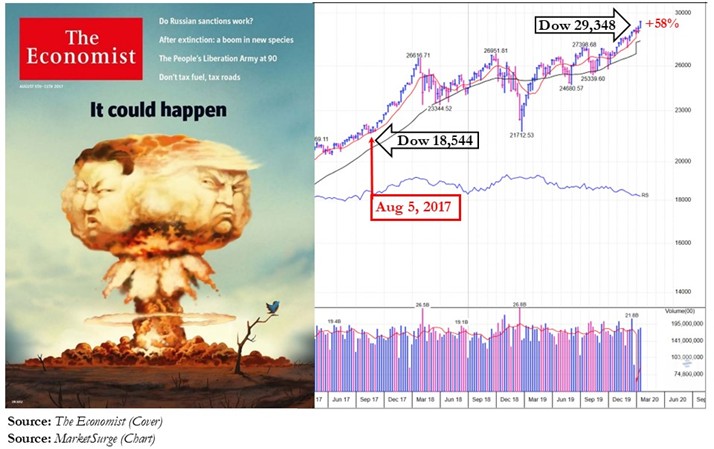

Tensions flared in 2017 as North Korea tested missiles and President Trump threatened retaliation against dictator Kim Jong Un by bombing Pyongyang and “Rocket Man”. The media went into overdrive regarding the nuclear unease, but the market brushed it off and continued climbing +58% over the next few years.

COVID-19 Pandemic (2020)

With over 3 million deaths worldwide and a grinding halt to the global economy, markets initially fell roughly -35%. But as consumers stockpiled toilet paper, fast vaccine development and stimulus sparked a powerful rebound, with stocks finishing the year up +16%. Over the next two years, the Dow almost doubled.

Hostage to Our Lizard Brain

Why are we so susceptible to the sensationalist tendencies of the media? Evolution holds the answer. Humans’ DNA and brains are hard-wired to flee prey. The small almond-shaped tissue in our brain called the amygdala—or what author Seth Godin calls the “lizard brain”—evolved to respond instantly to danger. When headlines scream “crash” or “war,” our emotional brain overrides our logical one, which leads to poor long-term results. As Seth Godin explains, we’re wired to react, not reflect (Watch here). And the media knows it.

Headlines Change but the Long-Term Market Trend Doesn’t

Despite a barrage of negative headlines, stocks have remained resilient over the long run. The market has overcome wars, assassinations, currency crises, banking failures, terrorist attacks, pandemics, natural disasters, impeachments, tax hikes, recessions, restrictive Fed policies, debt downgrades, inflation, and yes, even tariffs (see chart below). Since WWII, we’ve had 12 recessions—each followed by a full recovery to new record highs. In baseball terms, the economy has batted a perfect 1.000 (12-for-12) with recession recoveries.

How to Survive the Avalanche of Media Headlines

Here are five key strategies:

- Turn off the TV: Don’t obsess over headlines. Emotional reactions result in poor decisions.

Buying high (greed) and selling low (fear) is not a recipe for long-term investment success.

- Diversify Your Investments: A well-balanced portfolio across asset classes helps reduce panic.

- Invest According to Time Horizon: Are you young? Assuming more risk and higher exposure to the stock market is generally fine. Are you near retirement? Don’t jeopardize your retirement goals – de-risk accordingly.

- Ignore Talking Heads: Most pundits don’t invest and their credibility is compromised by monetary conflicts of interest. It’s much more beneficial to follow seasoned professionals with real track records through multiple bull and bear markets.

- Avoid the Herd: Continually following the herd into the most popular investments often leads to underperformance. The grass is greener, and the food sources are more plentiful, off the beaten path trampled by the herd. Contrarian thinking works even though it can feel scary.

In the age of constant connectivity, headlines and the 24/7 news cycle are addictive. But if you’re tired of being a pawn in the media’s game, I invite you to join my fight by acknowledging that the Emperor Media has no clothes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Animal Spirits to Animal Hibernation

Investor mood or sentiment can change rather quickly. Immediately after the 2024 presidential elections, positive animal spirits catapulted the stock market higher due to hopes of stimulating tax cuts and deregulation legislation. However, those warm and fuzzy feelings soured last month, as investor focus shifted to on-again, off-again tariff talks, and stagflation concerns, which have converted animal spirits into gloomy feelings of hibernation.

As a result, the advancing bull market took a breather and transformed into a weary bear during March. For the month, the S&P 500 (-5.8%), NASDAQ (-8.2%), and the Dow Jones Industrial Average (-4.2%) all fell significantly in the wake of tariffs, inflation, and recession worries.

Lovely Liberation Day or Tariff Trouble?

Since the President took office in January, he has announced, reversed, and implemented tariffs across a wide range of countries and sectors, including China, Canada, Mexico, the EU, Colombia, Venezuela, steel, aluminum, oil, automobiles, digital services taxes, and more.

The day of reckoning begins on April 2nd, designated Liberation Day by the president. This is when the president and the White House officially announce global reciprocal tariffs on foreign countries in an attempt to reverse the nation’s large trade deficit (see chart below) and bring manufacturing back to the United States. For example, if Germany subsidizes BMW cars sold in the U.S. while simultaneously placing tariffs (i.e., additional taxes) on American Ford Explorers sold in Germany, the president wants to impose equivalent reciprocal tariffs on those same BMWs sold in the U.S. in an effort to level the trading playing field. On the surface, a $131 billion trade deficit sounds very significant, but when compared to a $30 trillion economy (Gross Domestic Product – GDP), this negative trade balance represents less than 0.5% of GDP – effectively a rounding error. I have previously written how tariffs represent more of a molehill than a mountain (see Tariff Sheriff), in part because consumer spending and services make up the vast majority of our country’s economic activity, whereas trade and manufacturing are relatively smaller segments.

Source: Trading Economics

Driving home the point that tariffs are more bark than bite, Senior White House trade and manufacturing counselor Peter Navarro recently stated the 2025 tariffs could add $700 billion annually to U.S. revenues, including $100 billion from the recently announced 25% auto tariffs. Many economists believe this collection estimate is too optimistic. However, even if this target is achievable, $700 billion only represents a measly 2% of overall GDP.

Tariffs = Recession or Stagflation?

With the recent stock market downdraft and growing concerns related to tariffs, some economists and pundits are raising the probability of a recession and the possibility of inflation accompanying an economic downturn (i.e., stagflation).

Economic data should clear some of the fog. Fresh employment numbers will be released this Friday, which should shine some light on the health of the economy. Irrespective of this month’s results, the most recent 4.1% unemployment rate (see chart below), though slightly higher over the last two years, does not strongly indicate a recession.

Source: Trading Economics

Other “hard” data, such as GDP, also suggest a slowing economy rather than a recession. For instance, a recent survey of 14 economists estimates the economy is growing at a paltry +0.3% rate in Q1 – 2025 versus +2.3% in Q4 – 2024. Data is continually changing, but if a looming recession were imminent, corporate earnings would likely be trending downward, not upwards, as evident in the chart below.

Source: Yardeni Research

Tariff Inflation Has Yet to Arrive

There is no doubt tariffs function as a tax hike on consumers because U.S. companies that pay the tariffs on imported goods are eventually forced to raise prices to maintain profit margins or limit margin degradation.

Nonetheless, inflation did not spike under President Trump’s first term. Even if the president’s new policies result in more aggressive tariff actions this go-around, inflation will likely remain in check due to the point mentioned earlier – imported goods represent a small percentage of overall consumer and business purchases.

Tariff implementation is just beginning, so only time will tell how pervasive inflation will become. However, what we do know now is that inflation has declined dramatically over the last couple of years and has not yet spiked (see Consumer Price Index chart below).

Source: Calafia Beach Pundit

Where Could I Be Wrong?

I have explained how some of the lagging “hard” data does not signal recession or stagflation, but what could I be missing? For starters, some of the leading “soft” data (e.g., surveys) indicate various cracks in the economic foundation are forming. Take the recent Consumer Confidence data (see chart below), which has weakened dramatically from pre-COVID and even post-COVID levels.

Source: Trading Economics

It’s not just consumers who are feeling uneasy about the economic environment; businesses are as well. Another soft data point flashing red is the NFIB Small Business Uncertainty index, which recently reported its second-highest reading in 48 years (see chart below). Even if my argument that tariffs are too small to materially impact the economy holds, if the psychological effects of tariff uncertainty paralyzes consumer and business economic activity to a standstill, then tariffs could indeed become a substantial factor.

Source: National Federation of Independent Business (NFIB)

What Comes Next After Liberation Day?

Liberation Day is unlikely to trigger an immediate and sustained V-shaped recovery in the stock market because international trading partners will be forced to announce retaliatory tariffs in response to President Trump’s reciprocal tariffs, potentially leading to additional reactionary tariffs by the U.S.

Additionally, the reciprocal tariffs announced on April 2nd will likely serve as a starting point for subsequent negotiations with trading partners. Without a comprehensive resolution, investor sentiment will likely remain somewhat unresolved and unsettled. Regardless of your views on the size and impact of tariffs, Liberation Day will at least bring some clarity and reduce the uncertainty surrounding the current murky and chaotic environment.

The multi-year bull market continued its charge after the presidential election, but investor sentiment has weakened the bull run due to tariff uncertainty. In response, the excited bull has temporarily turned into a sleepy bear. Depending on how these tariff events unfold, we will soon find out whether Liberation Day will awaken the bear to hunt for bulls or send it into deep hibernation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in F or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Investing in Pigs and Kidneys: Building a $100 Billion Empire and Revolutionizing Organ Transplants

How does one create a $100 billion empire while pioneering an endless supply of transplantable organs that could save millions of lives? The first step is launching a multi-billion-dollar satellite company (SiriusXM – SIRI). The next step? Founding a biotechnology company with nothing more than a high school-level biology education — all in a desperate attempt to save the life of your seven-year-old daughter from a rare heart disease that claims lives within three to five years.

This is the extraordinary path of Martine Rothblatt, CEO and visionary of United Therapeutics Corp. (UTHR), who began this journey 35 years ago.

Transforming Industries: From SiriusXM to Organ Transplants

Few individuals have singlehandedly transformed entire industries. One name that comes to mind is Steve Jobs – who revolutionized consumer electronics and laid the foundation for Apple Inc.’s (AAPL) meteoric rise to a multi-trillion dollar company before he passed away. While Rothblatt and United Therapeutics may not yet be household names, she is undeniably reshaping the healthcare industry and steering it toward a future of unprecedented, life-extending medical advancements.

How can these ambitious, world-changing goals be achieved? A whole aisle of books could be written about Rothblatt’s impressive lifetime accomplishments, but the unique investment opportunity for investors cannot be fully understood without appreciating the person that created United Therapeutics 29 years ago in 1996.

Rothblatt has accomplished more than most humans could in multiple lifetimes – here is a partial sampling of her achievements:

- Earned a Bachelor of Arts, a Juris Doctor (JD), and Master of Business Administration (MBA) degrees from the University of California, Los Angeles (UCLA).

- Finished her PhD at The London School of Medicine (Barts)

- Practiced law at the Covington & Burling law firm representing the television broadcasting industry before the Federal Communications Commission (FCC).

- Hired by NASA to seek approval from the FCC for NASA systems used to track and relay satellite data.

- Created the multi-billion-dollar satellite radio company SiriusXM in 1990 with the inspiration of physicist Gerard O’Neill, the same Princeton professor who motivated Amazon CEO, Jeff Bezos to create Blue Origin.

- Invented the Terasem Movement, an organization with the mission of human life extension that uses cognitive and artificial intelligence software. Terasem’s technology has created a lifelike robot (BINA48), which is modeled after her spouse, Bina Rothblatt.

- Pioneered EV (electric) helicopter transportation through the company’s Unither Bioelectronics division with the purpose of cutting energy consumption and speeding up organ delivery times.

The United Therapeutics Story

In 1996, while leading SiriusXM, Rothblatt faced every parent’s worst nightmare. Doctors diagnosed her seven-year-old daughter, Jenesis, with Pulmonary Arterial Hypertension (PAH) — a rare, devastating disease with no known cure. Determined to save her daughter, Rothblatt initially funded research grants totaling over a million dollars to a narrow group of five doctors studying the disease. When the scientists failed to find a cure, she took matters into her own hands.

With no formal medical background, she quit SiriusXM, immersed herself in biology, and founded United Therapeutics. Against all odds, armed with her mantra that “persistence leads to omnipotence,” Rothblatt’s relentless pursuit paid off when she discovered a cure. Today, decades later, Jenesis is 42 years old and thriving as a high-profile manager at United Therapeutics.

Addressing the Organ Shortage Crisis

United Therapeutics’ advancements in PAH treatment have allowed patients like Jenesis to live long, productive lives. However, many eventually require organ transplants – the company is already assisting hundreds of patients with lifesaving human lung transplants. Despite some progress, the current organ shortage crisis is staggering:

- Over 100,000 people are on the national transplant waiting list.

- More than 92,000 of them need a kidney due to kidney failure or End-Stage Renal Disease (ESRD).

To address the organ shortage, United Therapeutics recently made history last month when the FDA approved the first-ever clinical trial for its UKidney xenotransplantation procedure for kidney failure patients.

The severity of the organ shortage problem is clear-cut if you examine the numbers. In addition to the 92,000 patients on the kidney transplant waitlist mentioned above, there are approximately 500,000 additional ESRD dialysis patients not on the national transplant list. Roughly 10% of these ESRD patients die each year due to dialysis-related complications.

If you combine the wait list population with the dialysis patient population you get to a total of around 600,000 people total. Regrettably, the vast majority of these patients do not receive an organ. In fact, only 27,759 kidney transplants were performed in the U.S. last year. In other words, despite the enormous demand for transplantable organs, less than 5% of the addressable market have actually benefited from a new kidney.

The Future of Organ Transplants: Profitable Pig Potential

How can this massive undersupply of transplants be fixed? One word…pigs. With a very scarce supply of human donors, pigs may hold the key to solving the organ shortage. United Therapeutics has pioneered genetically engineered pig organs (xenotransplantation) by modifying 10 key genes to prevent immune system rejection. As part of the xenotransplantation trial, United Therapeutics has built multiple DPF (designated pathogen free) facilities that house the pigs carrying the gene-modified kidneys.

All of this may sound like science fiction, but the dream of xenotransplantation has already become reality. Just last November, a genetically engineered pig kidney was transplanted into a patient (Towana Looney) under a compassionate use basis granted by the FDA. With its new clinical trial now underway, United Therapeutics is planning to transplant up to 50 patients with modified pig kidneys in the coming months.

And UKidney is just the beginning. United Therapeutics has a deep organ transplant pipeline that extends beyond kidneys into livers, hearts, and lungs (see graphic below). The company is also working on the “holy grail” of transplants – 3D printed organs using the cells of organ recipients to build the tissue structure, which dramatically reduces or eliminates the risk of organ rejection.

If UKidney is successful, United Therapeutics and Martine Rothblatt will be one step closer to realizing the company’s vision of manufacturing an endless supply of transplantable organs.

Source: United Therapeutics

Investment Opportunity of a Lifetime?

Nothing in life is certain, and there are risks to making any investment, but betting against Martine Rothblatt over the years has been a major losing proposition. From an investment standpoint, the core PAH drug business is trading at an immense discount, and investors are essentially valuing the organ transplant business at $0.

Despite its groundbreaking advancements and tremendous profit growth, United Therapeutics has huge stock price appreciation potential. Here’s why:

Stock is Dirt Cheap: At $317 per share, the stock currently trades at roughly a 50% discount to the trailing S&P 500 Price-Earnings ratio (PE) – 13x P/E vs. 26x index P/E. In other words, the shares should be trading north of $600 (double the price), if United Therapeutics was afforded an “average” company P/E multiple. But United Therapeutics clearly is not an average company.

Over the last two years, the company has grown revenues +48% from $1.9 billion to $2.9 billion and seen earnings explode +64% higher from $15.00 per share to $24.64. The stock becomes even cheaper on a forward P/E multiple (11x P/E) if the company can meet 2025 Wall Street expectations of 15% growth in its EPS to $28.23. Its superior products, execution, and competitive moats should afford the company a significant premium, not a drastic discount. Short-term investors are missing the boat by ignoring the gargantuan market potential for the company.

Is it possible for a $15 billion company to reach a $100 billion market value? This is not difficult to imagine if the company can bring its innovative and revolutionary pipeline products to market and take its current revenue base of almost $3 billion to $16 billion (see graphic below). The company certainly will not reach $16 billion in revenues tomorrow, but if you applied an average market multiple to those projections, and the company were able to maintain its current profit margin profile, a $3,000 per share stock price would be well within reason, equating to a market value well above $100 billion.

Source: United Therapeutics

Many Irons (Catalysts) in the Fire: United Therapeutics is no one-trick pony. Besides the company’s organ transplant plans, and their core commercial PAH and PH-ILD franchise, which includes, Remodulin, Orenitram, and Adcirca, United Therapeutics has many more irons in the fire that can be catalysts for stock price appreciation over the next 12 – 24 months (see graphic below).

Here is a more detailed description of the drivers:

- New Markets for Core Drugs: Any biotech or pharmaceutical company is in the business of searching for new markets to sell its products. United Therapeutics has found that in both the IPF (Idiopathic Pulmonary Fibrosis) and PPF (Progressive Pulmonary Fibrosis) markets, which are two different forms of chronic lung disease that are characterized by the gradual scarring and thickening of the lung tissue, which is called fibrosis. These patients can be administered with modified formulations of its existing Tyvaso molecule. The revenue potential is huge if the efficacy data comes in as planned because the pools of patients suffering from these horrible, progressive lung diseases could more than double the size of the present addressable market. Data from the company’s TETON 1 (IPF), TETON 2 (IPF), and TETON PPF studies will be released over the next few years, starting as early as next quarter.

- Improved Drug Formulation: United Therapeutics is also waiting for groundbreaking data from a drug called Ralinepag, the first once-per-day prostacyclin pill that is an improvement over its existing drugs of Remodulin, Tyvaso, and Orenitram. The company is releasing the Ralinepag data from its ADVANCE OUTCOMES study next year, and if the data proves to be positive, this could represent another multi-billion dollar opportunity for the company and investors.

- Other Near-Term Catalysts: Although perhaps representing a less meaningful potential from a long-term revenue standpoint, the company’s Centralized Lung Evaluation System (CLES) program is awaiting an FDA decision this year – CLES is designed to expand the supply of donor lungs. Last, but not least, data from United Therapeutics’ microliverELAP study represents another sizeable revenue opportunity for liver transplants.

Source: United Therapeutics

Fly in the Ointment: Failing Capital Allocation Grade

United Therapeutics deserves an A+ grade for developing the critical, world-class therapeutics that serve the PAH and PH-ILD market and the massive potential pipeline in xenotransplantation and alternative organ platforms. However, the company receives a failing grade for the implementation of its capital allocation strategy. United Therapeutics holds an excessively bloated cash surplus on its balance sheet, which has exploded higher from $1.0 billion in 2015 to $4.7 billion in 2024.

Sadly, the problem is only getting worse, as the company is on pace to add more than $1 billion more to the cash balance this year, and in subsequent years. This is woefully inefficient and becoming an alarmingly growing percentage (approximately 30% currently) of the company’s market value. To put this issue into perspective, investors should consider the company has enough cash on its balance sheet to effectively fund two decades of capital expenditure requirements. Profitable companies in United Therapeutics’ hand-selected proxy peer group hold a much more responsible amount of cash, representing about 4% of their market values.

If you had $100k of annual spending requirements, would you negligently place $2 million dollars in a low-single-digit yielding checking account or multi-year CD at your bank, when you could responsibly earn a 10% or higher return by paying down credit card debt? This is what United Therapeutics is doing. The company is essentially burning shareholder money by letting cash sit idly on its balance sheet earning a pittance when it could be earning significantly more. Why invest in government Treasuries when you could invest in your own company, compounding at rates greater than 10%?

The solution is clear. Implement a meaningful share repurchase program that is immediately EPS-accretive with the company’s bloated mountain of cash and bring down to responsible levels that are consistent with profitable growth peers. And rather than limiting your share repurchase to a one-time accelerated stock repurchase (ASR) program, expand the buyback to be more open ended on top of immediate purchases. This strategy provides the company with the flexibility to opportunistically purchase shares at a discount when the share price is depressed – like now, when shares are down -24% over the last five months.

Unfortunately, my message appears to be falling on deaf ears. I was hoping to gain clarity through communications with the company along with a letter sent to management and the board of directors. In my letter, I attempted to remind management of the importance of upholding its rigorous corporate governance standards and exercise its fiduciary duty when it comes to the company’s allocation strategy. However, regrettably, up to this point, there has been no indication to the market or me that there is any urgency to take advantage of the massively discounted United Therapeutics share price that exists today.

READ RECENT LETTER SENT TO MANAGEMENT & BOARD OF DIRECTORS BY CLICKING HERE

Investors Should Not Miss the Forest for the Trees

Although the company receives a failing capital allocation grade from my perspective, investors should not miss the forest from the trees. United Therapeutics’ share price is currently trading at a gigantic discount, yet it boasts unparalleled profitability and a groundbreaking organ transplant pipeline.

This lack of appreciation for the shares is surprising given how wildly profitable the company is and its tremendous long-term track record of success. But the company is not sitting on its hands – United Therapeutics has ambitious plans to expand its current annual revenue base by more than five-fold from $3 billion to $16 billion due to full cupboard of pipeline products.

With Martine Rothblatt at the helm—a visionary with a track record rivaling Steve Jobs—the company is poised to revolutionize healthcare. The world is a better place due to Martine Rothblatt, and your portfolio will be a better place with an investment in United Therapeutics.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in UTHR, AAPL, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SIRI or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Par for the Course

Stocks have been in a multi-year bull market, but just as investors cannot earn positive returns every month, golfers also cannot achieve a hole-in-one or birdie on every hole, either. A challenging performance is exactly what happened last month when stocks recorded a bogey on the scorecard.

More specifically, this is how far out-of-bounds the major indexes were last month:

- S&P 500: -1.4%

- Dow Jones Industrial Average -1.6%

- NASDAQ: -4.0%

Technology stocks and the Magnificent 7 stocks felt the largest brunt of the force last month as tariffs and the impact of Chinese AI (Artificial Intelligence) competition gave investors heartburn as they digested the information (see New Year, New AI ERA & New Tariff Sheriff).

Tariffs – More Molehill Than Mountain

As mentioned, a large part of last month’s volatility can be explained by the policy uncertainty surrounding the impending tariffs on China, Canada, and Mexico. Despite the absence of new tariffs being implemented, in an attempt to lock in cheaper imported goods, U.S. corporations and consumers have been stockpiling foreign goods before prices move higher due to tariffs. The 25% proposed tariffs on Canadian and Mexican goods are set to be applied as soon as March 4th. A flat 25% tariff on imported steel and aluminum products is expected to begin on March 12th – these particular tariffs are expected to have a disproportionately negative impact on the automotive industry.

Regarding other proposed reciprocal trade agreements, the White House’s analysis on tariffs for all other countries (beyond China, Canada, and Mexico) is expected to arrive on the president’s desk on April 2nd.

All these proposed changes are having an immediate economic impact whether intended or not. Not only are consumers buying more overseas products now, as they brace for higher prices, but businesses are also shifting supply chains to countries outside of China, Canada, and Mexico, in hopes of finding temporary tariff loopholes.

The bottom-line is our country’s imports have been spiking up recently, especially in the first quarter. Imports by definition subtract from America’s economic activity, so if businesses and consumers are rationally stockpiling foreign goods before prices go up from tariffs, investors should not be surprised that GDP (Gross Domestic Product) growth is set to go negative in the first quarter (-1.5%), according to the Federal Reserve Bank of Atlanta.

This short-term spike in foreign product purchases should be temporary until the tariffs are officially put in place. Subsequently, demand for relatively cheaper U.S. goods should rise because foreign goods will be pricier. In other words, buyers may begin purchasing more American-made t-shirts on Amazon because those shirts could be cheaper than the Chinese-made t-shirts after the additional tariffs commence on China.

How large are these overall tariffs? When it comes to Mexico and Canada, the size of these countries’ imports is estimated at $918 billion (see the 2023 import breakdown below for the two countries). On the surface, this sounds like a very large number, and it is. However, if you consider the size of the U.S. GDP ($29.4 trillion), these tariffs will mathematically have less than a 1% impact on the direction of our country’s economic activity.

However, if demand for American products goes up after the tariffs begin, as mentioned above, then it is perfectly logical to expect the drag from imports can be diminished or possibly completely reversed, if consumers decide to buy more American goods.

Source: Visual Capitalist

Also worth noting, as I documented last month in my Investing Caffeine blog, imports only account for 13.9% of our country’s economic activity (see New Tariff Sheriff). So, while tariffs make for great scary headlines, the reality of the numbers paints a different picture. Overall, the uncertainty surrounding the discussion of tariffs is having a much larger economic impact than the actual tariffs themselves. In other words, what we are discussing is more molehill than mountain. We saw this same movie before during the administration’s first-term when tariffs did not crater the economy into recession or create disproportionately high inflation.

War at the White House

A geopolitical soap opera played out on global television last Friday during a meeting between Ukraine’s President Volodymyr Zelensky and President Trump in the Oval Office. The meeting was designed to be a celebratory signing of a minerals deal in which the U.S. would gain access to strategically important Ukrainian rare earth metals in exchange for continued U.S. aid and military support. A signed deal would increase the probability of a peace deal between Russia and Ukraine dramatically. What actually happened was a war of words at the White House, which resulted in Zelensky getting kicked out of the White House with no signed deal.

Both sides have economic and strategic incentives to reengage in peace and mineral deal negotiations, but if the U.S.-Ukraine relationship totally crumbles, Europe and the other NATO (North Atlantic Treaty Organization) countries will need to pick up the slack in their military and economic aid to Ukraine. Regardless, increased European support is required to stave off a broader incursion by Russia and Vladimir Putin into a wider portion of Europe.

Tariffs, the Russia-Ukraine war, and AI issues may have heightened investor anxiety last month, but long-term investors understand that annual -5% and -10% corrections in the equity markets are considered par for the course. In fact, over the last 12 months, the S&P 500 index has declined -5% five times, and -10% one time, yet the stock market is still up +16% on a trailing 12-month basis (see chart below).

Source: Trading Economics

Financial markets end up in the rough plenty of the time, which often results in performance scorecard bogeys. However, long-term investors and Sidoxia Capital Management clients have won more often than not because the benefits of American capitalism have created many more birdies and pars over time.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 3, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in META, NVDA, certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BABA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

How to Profit from the Trump Crypto Wave

We were honored to have our white paper on the cryptocurrency market published by the California Business Journal last month. Please enjoy the article below.

Newly inaugurated President Donald Trump has wholeheartedly embraced the multi-trillion dollar cryptocurrency and digital asset industry. This is a seismic shift from the anti-crypto stance harbored by the previous administration. In the first week of his second term, President Trump not only appointed crypto-friendly Paul Atkins as the SEC Chairman, but Trump also named David Sacks as the first-ever White House Crypto Czar. If that was not a strong enough signal, Trump issued an executive order on his third day in the Oval Office, entitled, “Strengthening American Leadership in Digital Financial Technology.”

With this massive political and legislative tailwind behind the cryptocurrency industry, what is the best way to profit from this cryptocurrency wave? Is it just as easy as buying Bitcoin? Not exactly, if history repeats itself. Since Bitcoin was introduced in early 2009, the value of the cryptocurrency has fallen by more than -50% seven times. There have been many causes for Bitcoin’s historical volatility, including the hacking of the largest Bitcoin exchange in 2011 (Mt. Gox); China banning Bitcoin in 2013; and the COVID pandemic crash in 2020. Matters got worse for the cryptocurrency industry when FTX, one of the world’s largest crypto exchanges went bankrupt in 2022, and its founder and CEO, Sam Bankman-Fried, was subsequently arrested and convicted for fraud and money laundering.

Investing in a currency or asset class with that much volatility is very challenging. To compensate for volatility and risk, investors require the potential for higher returns backed by robust fundamentals. Unfortunately, to date, many of the broadest use cases for cryptocurrencies have been limited to illicit and illegal activities. There certainly are some speed and security advantages to the blockchain technology and the associated ledger structure of the major cryptocurrencies. However, the benefits have not been so clear-cut that Fortune 1000 companies and mass consumers have adopted it. A relatively small 15.5% of Americans (and 6.9% worldwide) are estimated to own a cryptocurrency, and a smaller fraction of that actually transact in a crypto.

Even though the practical use cases for cryptocurrencies over the last two decades have been extremely constrained, the speculative fervor surrounding this asset class has grown exponentially to the point there are over an estimated 10,000 cryptocurrencies that exist today, including speculative meme coins such as Dogecoin, the Trump coin, and other crude joke coins.

In my more than three decades of investing, I have repeatedly encountered extensive segments of the financial markets that would qualify as speculative bubbles, whether it was subprime mortgages and credit default swaps (CDS) in the 2008 Financial Crisis, or dot-com companies in the 2000 bursting of the technology bubble.

Today, in 2025, the current cryptocurrency wave definitely qualifies as another bubble. But depending on an investor’s time horizon, there is still potential to make significant profits during these frothy investment waves. For example, take Amazon.com, which was at the epicenter of the dot-com bubble as it saw its stock price crater approximately -95% in the 2000-2001 timeframe. Before Amazon’s stock collapsed, its price peaked at $5.65 per share at the end of 1999 – today, the stock price in 2025 has exceeded $240 per share (a more than 40-fold increase). Despite the bursting of the tech bubble, a tremendous amount of money has been made by long-term investors in Amazon and a select few other long-term technology winners.

I believe the same opportunity exists today in the cryptocurrency market. There are a few historical parallels that inform our crypto investment strategy at my investment firm, Sidoxia Capital Management. Let’s begin with the gambling industry that flourished in Las Vegas during the 1940s after the end of Prohibition. It was not the gamblers and speculators that made all the money, but rather the casinos, including some remaining today like the Flamingo and the Golden Nugget.

Currently, the dominant casino in the cryptocurrency industry is Coinbase Global Inc. (COIN). Coinbase is the 800-pound gorilla in the U.S. cryptocurrency exchange space, handling transactions that total more than $4 billion in daily trading volume across hundreds of cryptocurrencies, stable coins, meme coins and other digital assets. And the company is highly profitable with substantial growth. More specifically, the company has generated more than $5 billion in sales and greater than $1 billion in profits over the last year. Just like Las Vegas casinos make money off every gambler’s bets, so too does Coinbase make profits off every crypto speculator’s trades, whether those transactions in Bitcoin, Tether, Ethereum, or meme coins go up or down in value.

Another lucrative way for investors to look at the nascent cryptocurrency industry is to compare it to the California gold rush that occurred from 1848 – 1855. Hundreds of thousands of “forty-niners” (the peak year of gold rush immigration – 1849) flocked out west in hopes of discovering perceived limitless riches – an attitude held by many cryptocurrency purchasers presently. Unfortunately, it was not the forty-niners digging and panning for gold who made most of the money, it was the merchants selling all the picks and shovels to the gold rush speculators that profited the greatest.

The contemporary merchants in today’s cryptocurrency world are companies like NVIDIA Corp. (NVDA), the creator of the graphics processing unit (GPU) semiconductors that power the critical mining operations of cryptocurrencies like Bitcoin. The GPUs serve as the picks and shovels for crypto miners who receive rewards in the form of cryptocurrencies (i.e., Bitcoin) in return for performing computationally intensive calculations, which are necessary to verify transactions on a digital decentralized crypto ledger. NVIDIA GPUs have a broad range of applications beyond crypto mining, including data center applications for artificial intelligence (AI), video games, gene sequencing, virtual-augmented reality, and other large-scale markets. Over the last year, NVIDIA has produced more than $110 billion in sales and created more than $60 billion in net profits. Not only was NVDIA successful commercially, but equity investors were also rewarded handsomely last year with an appreciation of +171% in the share price.

There are plenty of reasons to remain skeptical about the euphoria surrounding the cryptocurrency industry, especially due to the lack of legitimate use cases across the avalanche of digital assets endlessly introduced. However, the pro-crypto wave of Trump regulations and policies allow plenty of ways for investors to profit from this digital gold rush, especially if you can find the winning crypto casino and leading merchant of digital picks and shovels.

By Wade W. Slome, CFA, CFP®, Exclusive to California Business Journal

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in NVDA, COIN, IBIT, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Time in the Market Beats Timing the Market

It was another great year in the stock market. But predicting the timing of a bear or bull market is more challenging. Fortunately for investors, the stock market is up a lot more of the time than it is down. More specifically, over the last century, the stock market has been up 73% of the time for one-year periods and 94% of the time for 10-year periods (see graphic below and Time is What Matters). That’s why investors’ time in the market beats the fools’ errand strategy of trying to time the market. The long-term, consistent upward trend in stock prices makes investing in the stock market akin to sailing around the world with a persistent tailwind for the whole trip.

Source: Capital Group and S&P 500 Index

Many people believe investing in the stock market is gambling, but 73% and 94% odds for stock market gains seem a lot better than the probabilities of making money in Las Vegas. I explored this concept further in one of my recent articles (see Elections Status Quo). Even with those favorable, lopsided odds, recessions do occur, albeit infrequently. As you can see from the chart below, since World War II, we have experienced a dozen recessions averaging 10 months in duration. And guess what? Successful post-recession recoveries have equaled 100% (12 for 12). Despite the short-lived bear markets, stock prices have appreciated more than 30x-fold since the end of World War II.

Source: Yardeni.com

2024 Predictions

There were plenty of pundits and talking heads who falsely predicted a recession in 2024, but the odds certainly worked in investors’ favor. For 2024, the S&P 500 index gained +23%, and this comes on the heels of a banner 2023, which was up +24%. Experiencing back-to-back +20%-years is a rare occurrence, which hasn’t occurred since the late-1990s. As we look into 2025, achieving three consecutive positive years in the stock market is not unprecedented, but as I mentioned earlier, predicting the timing of a down market can be tricky.

Case in point, predicting the outcome of stock returns, even with perfect information can be very daunting. What would have been your prediction of the 2024 stock market return, if I told you the following events were to occur this year (in no particular order)?

- Two assassination attempts on a presidential candidate

- An ongoing bloody war between Russia and Ukraine that reaches one million deaths

- Brutal Israeli-Hamas war in Gaza moves into its second year

- Nationwide Palestinian protests across college campuses

- Israeli-Hezbollah war commences in Lebanon

- Rebels in Syria topple the Assad regime

- A hotly contested presidential election triggering fears of a civil war

- A Baltimore bridge collapses killing six people and costing the overall economy upwards of $10 billion

- After crypto exchange goes bankrupt, CEO is sentenced to 25 years in prison for fraud

Most intelligently honest people would not have predicted a +23% return, but that is exactly what happened. As part of this extended bull market, some major stock market milestones were achieved: 1.) the Dow Jones Industrial average eclipsed 40,000; 2.) the main benchmark S&P 500 index surpassed 6,000; and 3.) the NASDAQ index temporarily triumphed the 20,000 level. The market took a breather in December (the Dow -5.3% and S&P -2.5%), so we have momentarily pulled back from some of these key levels.

What Next in 2025?

As I alluded to earlier, pulling off a three-peat in 2025 with a third consecutive year of gains may be a difficult feat, but not impossible. There remains some room for optimism. First of all, we have an accommodative Federal Reserve that has cut interest rates three times in 2024 (see chart below) from a target of 5.5% to 4.5% (see red line). Currently, expectations are set for the Fed to make another two interest rate cuts in 2025. All else equal, this should provide some mild stimulus for both borrowers and investors in 2025.

Source: Yardeni.com

Next, we have a new pro-business administration entering the White House that has promised lower taxes and less regulation, which should aid business profits. Tariff policies remain a wildcard, but if used judiciously for negotiation purposes, perhaps there could be more bark than bite from the rhetoric. Time will tell.

The 2024 chapter has closed, and we have started the 2025 chapter. Regardless of the outcome this year, history teaches us the time in the market is much more important than timing the market. This philosophy has served Sidoxia Capital Management and its clients well over the long-run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 2, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}