Posts filed under ‘Stocks’

Hunting for Tennis Balls and Dead Cats

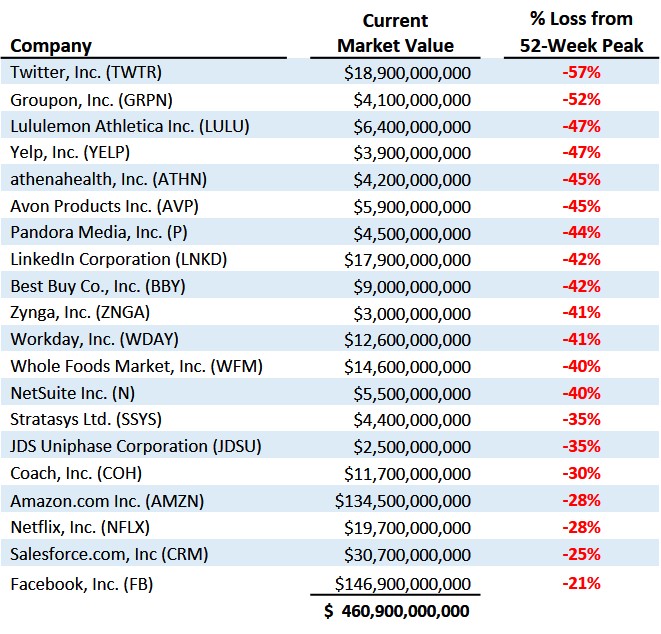

When it comes to gravity, people understand what goes up, must come down. But the reverse is not always true for stocks. What goes down, does not necessarily need to come back up. Since the 2008-09 financial crisis there have been a large group of multi-billion dollar behemoth stocks that have defied gravity, but over the last few months, many of these highfliers have come back to earth. Despite the pause in some of these major technology, consumer, and internet stocks, the overall stock market appears relatively calm. In fact, the Dow Jones Industrials index is currently sitting at all-time record highs and the S&P 500 index is hovering around -1% from its peak. But below the surface, there is a large undercurrent resulting in an enormous rotation out of pricier momentum and growth stocks into more defensive and yield-heavy sectors of the market, like utilities and real estate.

To expose this concealed trend I have highlighted a group of 20 stocks below, valued at close to half a trillion dollars. Over the last 12 months, this selective group of technology, consumer, and internet stocks have lost over -$200,000,000,000 from their peak values. Here’s a look at the highlighted stocks:

With respect to all the punished stocks, the dilemma for investors amidst this depreciating price carnage is how to profitably hunt for the bouncing tennis balls while avoiding the dead cat bounces. By hunting bouncing tennis balls, I am referring to the identification of those companies that have crashed from indiscriminate selling, even though the companies’ positive business fundamentals remain fully intact. The so-called dead cats reflect those overpriced companies that lack the earnings power or trajectory to support a rebounding stock price. Like a cat falling from a high-rise building, there may exist a possibility of a small rebound, but for many severely broken momentum stocks, minor bounces are often short-lived.

For long-term investors, much of the recent rotation is healthy. Some of the froth I’ve been writing about in the biotech, internet, and technology has been mitigated. As a result, in many instances, outrageous or rich stock valuations have now become fairly priced or attractive.

Profiting from Collapses

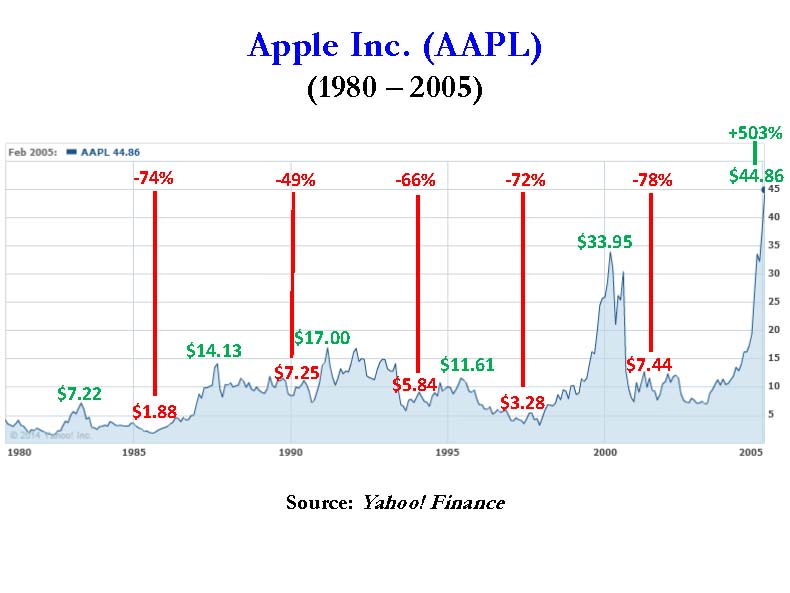

Many investors do not realize that some of the greatest stocks of all-time have suffered multiple -50% drops before subsequently doubling, tripling, quadrupling or better. History provides many rebounding tennis ball examples, but let’s take a brief look at the Apple Inc. (AAPL) chart from 1980 – 2005 to drive home the point:

As you can see, there were at least five occasions when the stock got chopped in half (or worse) over the selected timeframe and another five occasions when the stock doubled (or better), including a +935% explosion in the 1997–2000 period, and a +503% advance from 2002–2005 when shares reached $45. The numbers get kookier when you consider Apple’s share price eventually reached $700 and closed early last week above $600.

These feast and famine patterns can be discovered for virtually all of the greatest all-time stocks. The massive volatility explains why it’s so difficult to stick with theses long-term winners. A more recent example of a tennis ball bounce would be Facebook Inc (FB). The -58% % plummet from its $42 IPO peak has been well-documented, and despite the more recent -21% pullback, the stock is still up +223% from its $18 lows.

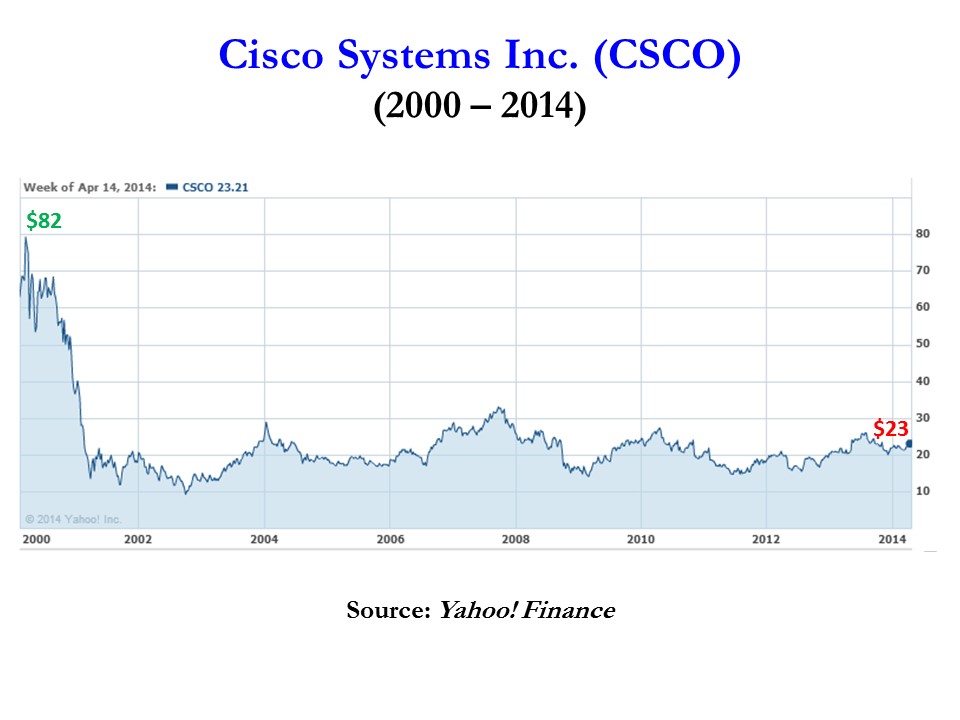

On the flip side, an example of a dead cat bounce would include Cisco Systems Inc (CSCO). After the bursting of the 2000 technology bubble, Cisco has never fully recovered from its $82 peak value. There have been many fits and starts, including some periods of 50% declines and 100% gains, but due to excessive valuations in the late 1990s and changing competitive trends, Cisco still sits at $23 today (see chart below).

It is important to remember that just because a stock goes down -50% in value doesn’t mean that it’s going to double or triple in value in the future. Price momentum can drive a stock in the short run, but in the long run, the important variables to track closely are cash flows and earnings (see It’s the Earnings, Stupid) . The level and direction of these factors ultimately correlate best with the ultimate fair value of stock prices. Therefore, if you are fishing in the growth or momentum stock pond, make sure to do your homework after a stock price collapses. It’s imperative that you carefully hunt down rebounding tennis balls and avoid the dead cat bounces.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AMZN, long NFLX bond, short NFLX stock, short LULU, and long CSCO (in a non-discretionary account), but at the time of publishing SCM had no direct position in TWTR, GRPN, YELP, ATHN, AVP, P, LNKD, BBY, ZNGA, WDAY, WFM, N, SSYS, JDSU, COH, CRM, FB or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Buy in May and Tap Dance Away

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (May 1, 2014). Subscribe on the right side of the page for the complete text.

The proverbial Wall Street adage that urges investors to “Sell in May, and go away” in order to avoid a seasonally volatile period from May to October has driven speculative trading strategies for generations. The basic premise behind the plan revolves around the idea that people have better things to do during the spring and summer months, so they sell stocks. Once the weather cools off, the thought process reverses as investors renew their interest in stocks during November. If investing was as easy as selling stocks on May 1 st and then buying them back on November 1st, then we could all caravan in yachts to our private islands while drinking from umbrella-filled coconut drinks. Regrettably, successful investing is not that simple and following naïve strategies like these generally don’t work over the long-run.

Even if you believe in market timing and seasonal investing (see Getting Off the Market Timing Treadmill ), the prohibitive transaction costs and tax implications often strip away any potential statistical advantage.

Unfortunately for the bears, who often react to this type of voodoo investing, betting against the stock market from May – October during the last two years has been a money-losing strategy. Rather than going away, investors have been better served to “Buy in May, and tap dance away.” More specifically, the S&P 500 index has increased in each of the last two years, including a +10% surge during the May-October period last year.

Nervous? Why Invest Now?

With the weak recent economic GDP figures and stock prices off by less than 1% from their all-time record highs, why in the world would investors consider investing now? Well, for starters, one must ask themselves, “What options do I have for my savings…cash?” Cash has been and will continue to be a poor place to hoard funds, especially when interest rates are near historic lows and inflation is eating away the value of your nest-egg like a hungry sumo wrestler. Anyone who has completed their income taxes last month knows how pathetic bank rates have been, and if you have pumped gas recently, you can appreciate the gnawing impact of escalating gasoline prices.

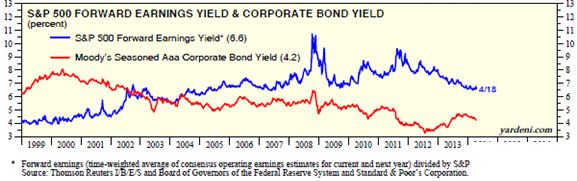

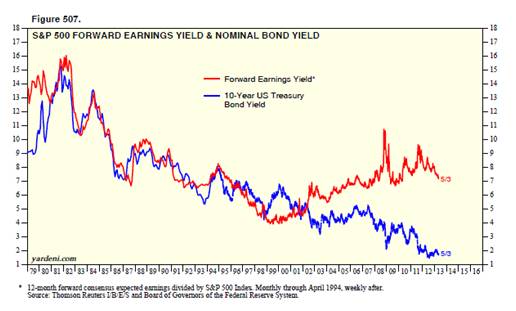

While there are selective opportunities to garner attractive yields in the bond market, as exploited in Sidoxia Fusion strategies, strategist and economist Dr. Ed Yardeni points out that equities have approximately +50% higher yields than corporate bonds. As you can see from the chart below, stocks (blue line) are yielding profits of about +6.6% vs +4.2% for corporate bonds (red line). In other words, for every $100 invested in stocks, companies are earning $6.60 in profits on average, which are then either paid out to investors as growing dividends and/or reinvested back into their companies for future growth.

Source: Dr. Ed’s Blog

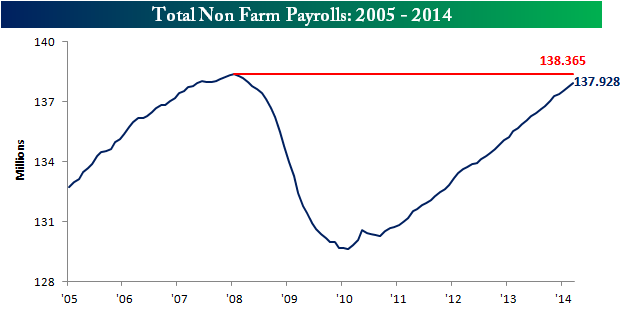

Hefty profit streams have resulted in healthy corporate balance sheets, which have served as ammunition for the improving jobs picture. At best, the economic recovery has moved from a snail’s pace to a tortoise’s pace, but nevertheless, the unemployment rate has returned to a more respectable 6.7% rate. The mended economy has virtually recovered all of the approximately 9 million private jobs lost during the financial crisis (see chart below) and expectations for Friday’s jobs report is for another +220,000 jobs added during the month of April.

Source: Bespoke

Wondrous Wing Woman

Investing can be scary for some individuals, but having an accommodative Fed Chair like Janet Yellen on your side makes the challenge more manageable. As I’ve pointed out in the past (with the help of Scott Grannis), the Fed’s stimulative ‘Quantitative Easing’ program counter intuitively raised interest rates during its implementation. What’s more, Yellen’s spearheading of the unprecedented $40 billion bond buying reduction program (a.k.a., ‘Taper’) has unexpectedly led to declining interest rates in recent months. If all goes well, Yellen will have completed the $85 billion monthly tapering by the end of this year, assuming the economy continues to expand.

In the meantime, investors and the broader financial markets have begun to digest the unwinding of the largest, most unprecedented monetary intervention in financial history. How can we tell this is the case? CEO confidence has improved to the point that $1 trillion of deals have been announced this year, including offers by Pfizer Inc. – PFE ($100 billion), Facebook Inc. – FB ($19 billion), and Comcast Corp. – CMCSA ($45 billion).

Source: Entrepreneur

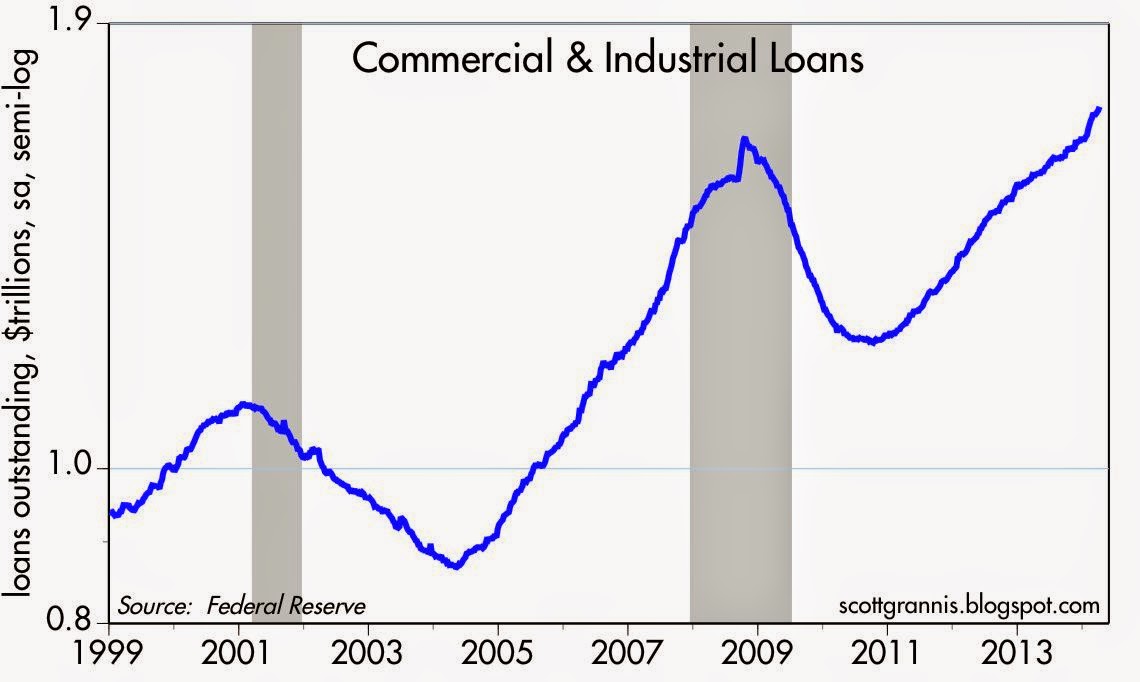

Banks are feeling more confident too, and this is evident by the acceleration seen in bank loans. After the financial crisis, gun-shy bank CEOs fortified their balance sheets, but with five years of economic expansion under their belts, the banks are beginning to loosen their loan purse strings further (see chart below).

The coast is never completely clear. As always, there are plenty of things to worry about. If it’s not Ukraine, it can be slowing growth in China, mid-term elections in the fall, and/or rising tensions in the Middle East. However, for the vast majority of investors, relying on calendar adages (i.e., selling in May) is a complete waste of time. You will be much better off investing in attractively priced, long-term opportunities, and then tap dance your way to financial prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE, CMCSA, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in FB or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

You Can’t Kiss Every Pretty Girl (…or Handsome Boy)

There are a lot of pretty girls in the world, and there are a lot of sexy stocks in the stock market, but not even the most eligible bachelor (or bachelorettes) are able to kiss all the beautiful people in the world. The same principle applies to the stock market. The most successful investors have a disciplined process of waiting for the perfect mate to cross their path, rather than chasing every tempting mistress.

Happily married to my current portfolio, I continually bump into attractive candidates that try to seduce me into buying. For me, these sexy equities typically come in the shape of high P/E ratios (Price/Earnings) and rapid sales growth rates. It’s fun to date (or rent) these sexy stocks, but the novelty often wears off quickly and the euphoric sensation can disappear rapidly – just like real-world dating. Case in point is the reality dating shows, the Bachelor and Bachelorette. Over 27 combined seasons, of which I sheepishly admit seeing a few, only five of the couples remain together today. While it may be enjoyable to vicariously watch bevies of beautiful people hook-up, the harsh reality is that the success rate is abysmal, similar to the results in chasing darling stocks (see also Riding the Wave).

Well-known strategist and investor Barton Biggs once said, “A bull market is like sex. It feels best just before it ends.” The same goes with chasing pricey momentum stocks – what looks pretty in the short-run can turn ugly in a blink of the eye. For example, if you purchased the following basket of top 10 performing stocks of 2012 (+118% average return excluding dividends), you would have underperformed the market by -16% if you owned until today.

Warren Buffett understands hunting for short-term relationships may be thrilling, but this strategy often leads to tears and heartbreak. Buffett summarized the importance of selectivity here:

“I could improve your ultimate financial welfare by giving you a ticket with only twenty slots in it so that you had twenty punches – representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all. Under those rules, you’d really think carefully about what you did, and you’d be forced to load up on what you’d really thought about. So you’d do so much better.”

Rather than hungering for the spiciest stocks, it’s best to find a beauty before she becomes Miss America, because at that point, everybody wants to date her and the price is usually way too expensive. If you stay selective and patient while realizing you can’t kiss every pretty girl, then you can prevent the stock market from breaking your heart.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in PHM, MHO, CVI, EXPE, HFS, DDS, LEN, MPC. TSO, GPS, BRKA/B, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Passive vs. Active Investing: Darts, Monkeys & Pros

Bob Turner is founder of Turner Investments and a manager of several funds at the investment company. In a recent article he reintroduces the all-important, longstanding debate of active management (“hands-on”) versus passive management (“hands off”) approaches to investing. Mr. Turner makes some good arguments for the active management camp, however some feel differently – take for example Burton Malkiel. The Princeton professor theorizes in his book A Random Walk Down Wall Street that “a blindfolded monkey throwing darts at a newspaper’s stock page could select a portfolio that would do just as well as one carefully selected by experts.” In fact, The Wall Street Journal manages an Investment Dartboard contest that stacks up amateur investors’ picks against the pros’ and random stock picks selected by randomly thrown darts. In many instances, the dartboard picks outperform the professionals. Given the controversy, who’s right…the darts, monkeys, or pros? Distinguishing between the different categorizations can be difficult, but we will take a stab nevertheless.

Arguments for Active Management

Turner contends, active management outperforms in periods of high volatility and he believes the industry will be entering such a phase:

“Active managers historically have tended to perform best in a market in which the performance of individual stocks varies widely.”

He also acknowledges that not all active managers outperform and admits there are periods where passive management will do better:

“The reason why most active investors fail to outperform is because they in fact constitute most of the market. Even in the best of times, not all active managers can hope to outperform…The business of picking stocks is to some degree a zero-sum game; the results achieved by the best managers will be offset at least somewhat by the subpar performance of other managers.”

Buttressing his argument for active management, Turner references data from Advisor Perspectives showing an inconclusive percentage (40.5%-67.8%) of the actively managed funds trailing the passively managed indexes from 2000 to 2008.

The Case for Passive Management

Turner cites one specific study to support his active management cause. However, my experience gleaned from the vast amounts of academic and industry data point to approximately 75% of active managers underperforming their passively managed indexes, over longer periods of time. Notably, a recent study conducted by Standard & Poor’s SPIVA division (S&P Indices Versus Active Funds) discovered the following conclusions over the five year market cycle from 2004 to 2008:

- S&P 500 outperformed 71.9% of actively managed large cap funds;

- S&P MidCap 400 outperformed 79.1% of mid cap funds;

- S&P SmallCap 600 outperformed 85.5% of small cap funds.

Read more about the dirty secrets shrinking your portfolio. According to the Vanguard Group and the Investment Company Institute, about 25% of institutional assets and about 12% of individual investors’ assets are currently indexed (passive strategies). If you doubt the popularity of passive investment strategies, then look no further than the growth of Exchange Traded Funds (ETFs – see chart), index funds, or Vanguard Groups more than $1 trillion dollars in assets under management.

Although I am a firm believer in passive investing, one of its shortcomings is mean reversion. This is the idea that upward or downward moving trends tend to revert back to an average or normal level over time. Active investing can take advantage of mean reversion, conversely passive investing cannot. Indexes can get very top-heavy in weightings of outperforming sectors or industries, meaning theoretically you could be buying larger and larger shares of an index in overpriced glamour stocks on the verge of collapse. We experienced these lopsided index weightings through the technology bubbles in the late 1990s and financials in 2008. Some strategies may be better than other over the long run, but every strategy, even passive investing, has its own unique set of deficiencies and risks.

Professional Sports and Investing

As I discuss in my book, there are similarities that can be drawn between professional sports and investing with respect to active vs. passive management. Like the scarce number of .300 hitters in baseball, I believe there are a select few investment managers who can consistently outperform the market. In 2007, AssociatedContent.com did a study that showed there were only 22 active career .300 hitters in Major League Baseball. I recognize in the investing world there can be a larger role for “luck,” which is difficult, if not impossible, to measure (luck won’t help me much in hitting a 100 mile per hour fastball thrown by Nolan Ryan). Nonetheless, in the professional sports arena, there are some Hall of Famers (prospects) that have proved they could (can) consistently outperform their peers for extended durations of time. Experience is another distinction I would highlight in comparing sports and investing. Unlike sports, in the investment world I believe there is a positive correlation between age and ability. The more experience an investor gains, generally the better long-term return achieved. Like many professions, the more experience you gain, the more valuable you become. Unfortunately, in many sports, ability deteriorates and muscles atrophy over time.

Size Matters

Experience alone will not make you a better investor. Some investors are born with an innate gift or intellect that propels them ahead of the pack. However, most great investors eventually get cursed by their own success thanks to accumulating assets. Warren Buffet knows the consequences of managing large amounts of dollars, “gravity always wins.” Having managed a $20 billion fund, I fully appreciate the challenges of investing larger sums of money. Managing a smaller fund is similar to navigating a speed boat – not too difficult to maneuver and fairly easy to dodge obstacles. Managing heftier pools of money can be like captaining a supertanker, but unfortunately the same rapid u-turn expectations of the speedboat remain. Managing large amounts of capital can be crippling, and that’s why captaining a supertanker requires the proper foresight and experience.

Room for All

As I’ve stated before, I believe the market is efficient in the long run, but can be terribly inefficient in the short-run, especially when the behavioral aspects of emotion (fear and greed) take over. The “wait for me, I want to play too” greed from the late 1990s technology craze and the credit-based economic collapse of 2008-2009 are further examples of inefficient situations that can be exploited by active managers. However, due to multiple fees, transaction costs, taxes, not to mention the short-term performance/compensation pressures to perform, I believe the odds are stacked against the active managers. For those experienced managers that have played the game for a long period and have a track record of success, I feel active management can play a role. At Sidoxia Capital Management, I choose to create investment portfolios that blend a mixture of passive and active investment strategies. Although my hedge fund has outperformed the S&P 500 in 4 of the last 5 years, that fact does not necessarily mean it’s the appropriate sole approach for all clients. As Warren Buffet states, investors should stick to their “circle of competence” so they can confidently invest in what they know. That’s why I generally stick to the areas of my expertise when I’m actively investing in stocks, and fill in the remainder of client portfolios with transparent, low-cost, tax-efficient equity and fixed income products (i.e., Exchange Traded Funds). Even though the actively managed Turner Funds appear to have a mixed-bag of performance numbers relative to passively managed strategies, I appreciate Bob Turner’s article for addressing this important issue. I’m sure the debate will never fully be resolved. In the meantime, my client portfolios will aim to mix the best of both worlds within active and passive management strategies in the eternal quest of outwitting the darts, monkeys, and other pros.

Read the full Bob Turner article on Morningstar.com

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds but had no direct position in stocks mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Buyback Bonanza Boost

With the S&P 500 off -1% from its all-time record high, many bears have continued to wait for and talk about a looming crash. For the naysayers, the main focus has been on the distorted monetary policies instituted by the Federal Reserve, but as I pointed out in Fed Fatigue is Setting In, QE and tapering talk are not the end-all, be-all of global financial markets. One need not look further than the dozen or so countries listed in the FT that have bond yields below the abnormally low yields we are experiencing in the U.S. (10-Year Treasury +2.75%).

Although there are many who believe a freefall is coming, much like a trampoline, a naturally occurring financial mechanism has provided a relentless bid to boost stock prices higher…a buyback bonanza! How significant have corporate stock repurchases been to spring prices higher? Jason Zweig, in his Intelligent Investor column, wrote the following:

In the Russell 3000, a broad U.S. stock index, repurchased $567.6 billion worth of their own shares—a 21% increase over 2012, calculates Rob Leiphart, an analyst at Birinyi Associates, a research firm in Westport, Conn. That brings total buybacks since the beginning of 2005 to $4.21 trillion—or nearly one-fifth of the total value of all U.S. stocks today.

To further put this gargantuan buyback bonanza into perspective, a recent Fox Business article described it this way:

Companies spent an estimated $477 billion on share buybacks last year. That’s enough to buy every NFL team 12 times over, run the federal government for 50 days or host the next nine Olympic Games with several billion left to spare. This year, companies are expected to ramp up buybacks by 35%, according to Goldman Sachs.

The bears continue to scream, while purple in the face, that the Fed’s QE and zero interest rate program (ZIRP) shenanigans are artificially propping up stock prices. The narrative then states the tapering and inevitable Fed Funds rate reversal will cause the market to come crashing down. While there is some truth behind this commentary, history reminds us that not all rate rising cycles end in bloodshed (see 1994 Bond Repeat or Stock Defeat?). Even if you believe in Armageddon, this rate reversal scenario is unlikely to happen until mid-2015 or beyond.

And for those worshipping the actions of Ms. Yellen at the Fed altar, believe it or not, there are other factors besides monetary policy that cause stock prices to go up or down. In addition to stock buybacks, there are dynamics such as record corporate profits, rising dividends, expanding earnings, reasonable valuations, improving international economies, and other factors that have contributed to this robust bull market.

At the end of the day, as I have continued to argue for some time, money goes where it is treated best – and generally that is not in savings accounts earning 0.003%. There is no reason to be a perma-bull, and I have freely acknowledged the expansion of froth in areas such as social media, biotech, Bitcoin and other areas. Regardless, there is, and will always be areas of speculation, in bull and bear markets (e.g., gold in the 2008-2009 period).

Magical Math

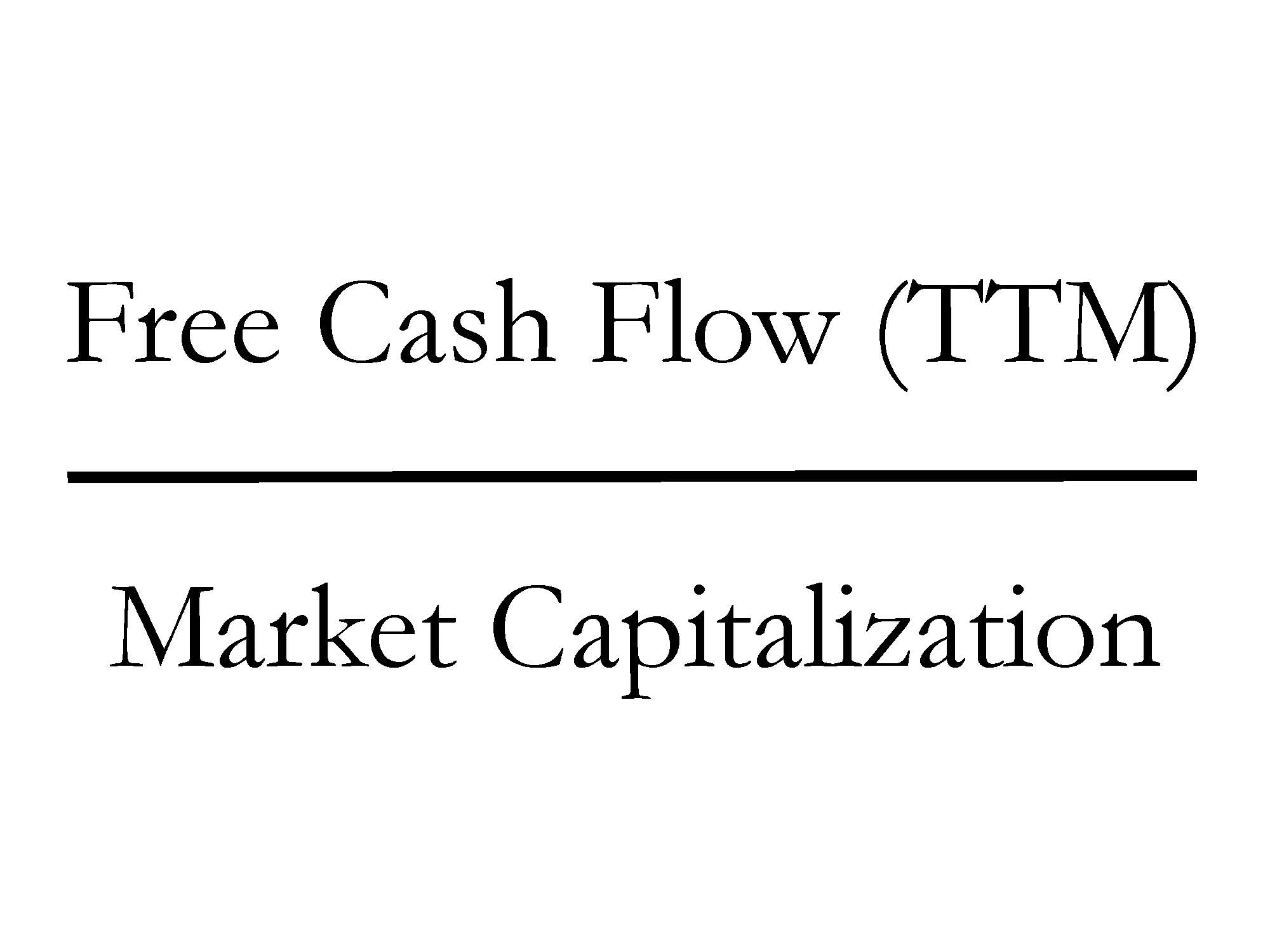

Investing involves a mixture of art and science, but with a few exceptions (i.e., fraud), numbers do not lie, and using math when investing is a good place to start. A simple but powerful mathematical formula instituted at Sidoxia Capital Management is the “Free Cash Flow Yield”, which is a metric we integrate into our proprietary SHGR (a.k.a.,“Sugar”) quantitative model (see Investing Holy Grail).

Quite simply, Free Cash Flow (FCF) is computed by taking the excess cash generated by a company after ALL expenses/expenditures (marketing, payroll, R&D, CAPEX, etc.) over a trailing twelve month period (TTM), then dividing that figure by the total equity value of a company (Market Capitalization). Mechanically, FCF is calculated by taking “Cash Flow from Operations” and subtracting “Capital Expenditures” – both figures can be found on the Cash Flow Statement. The Free Cash Flow ratio may sound complicated, but straightforwardly this is the leftover cash generated by a business that can be used for share buybacks, dividends, acquisitions, investments, debt pay-down, and/or placed in a banking account to pile up.

The great thing about FCF yields is that this ratio (%) can be compared across asset classes. For example, I can compare the FCF yield of Apple Inc – AAPL (+9.5%) versus a 10-Year Treasury (+2.75%), 1-year CD (+0.85%), Tesla Motors – TSLA (0.0%), Netflix, Inc – NFLX (-0.001%), or Twitter, Inc – TWTR (-0.003%). For growth and capital intensive companies, I can make adjustments to this calculation. However, what you quickly realize is that even if you assume massive growth in the coming years (i.e., $100s of millions in FCF), the prices for many of these momentum stocks are still astronomical.

An important insight about the current corporate buyback bonanza is that much of this price boost is being fueled by the colossal free cash flow generation of corporate America. Sure, some companies are borrowing through the debt markets to buy back stock, but if you were the Apple CFO sitting on $159,000,000,000 in cash earning 1%, it doesn’t make a lot of sense to sit on the cash earning nothing. It also doesn’t take a genius (or Carl Icahn) to figure out borrowing at record low rates (2.75% 10-year) while earning +10% on a stock buyback will increase shareholder value and earnings per share (EPS). More specifically, when Apple borrowed $17 billion at interest rates ranging from 0.5% – 3.9%, a shrewd, rational human being would borrow to the max all day long at those rates, if you could earn +10% on that investment. It is true that Apple’s profitability could drop and the numerator in our FCF ratio could decrease, but with $45 billion smackers coming in every year on top of $142 billion in net cash on the balance sheet, Apple has a healthy margin of safety to make the math work.

Where the math doesn’t compute is in insanely priced deals. For example, the recent merger in which Facebook Inc (FB) paid $19 billion (1,000 x’s the estimated 2013 annual revenues) for a 50-person, money-losing company (WhatsApp) that is offering a free service, makes zero financial sense to me. Suffice it to say, the FCF yield on WhatsApp could cause Warren Buffett to have a coronary event. Yes, diamond covered countertops would be nice to have in my kitchen, but I probably wouldn’t get much of a return on that investment.

Share buybacks are not a magical elixir to endless prosperity (see Share Buybacks & Bathroom Violators), but given the record profits and record low interest rates, basic math shows that even if stock prices correct (as should be expected), the trampolining effect of this buyback bonanza will provide support to the market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AAPL and a short position in NFLX, but at the time of publishing SCM had no direct position in TSLA, TWTR, FB, Bitcoin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

NASDAQ and the R&D-Tech Revolution

It’s been a bumpy start for stocks so far in 2014, but the fact of the matter is the NASDAQ Composite Index is up this year and hit a 14-year high in the latest trading session (highest level since 2000). The same cannot be said for the Dow Jones Industrial and S&P 500 indices, which are both lagging and down for the year. Not only did the NASDAQ outperform the Dow by almost +12% in 2013, but the NASDAQ has also trounced the Dow by over +70% over the last five years.

Is this outperformance a fluke or random coincidence? I’d beg to differ, and we will explore the reasons behind the NASDAQ being treated like the Rodney Dangerfield of indices. Or in other words, why the NASDAQ gets “no respect!” (see also NASDAQ Ugly Step Child).

Compared to the “bubble” days of the nineties, today’s discussions more rationally revolve around profits, cash flows, and valuations. Many of us old crusty veterans remember all the crazy talk of the “New Economy,” “clicks,” and “eyeballs” that took place in the mid-to-late 1990s. Those metrics and hyperbole are used less today, but if NASDAQ’s dominance extends significantly, I’m sure some new and old descriptive euphemisms will float to the conversational surface.

The technology bubble may have burst in 2000, and scarred memories of the -78% collapse in the NASDAQ (5,100 to 1,100) from 2000-2002 have not been forgotten. Despite that carnage, technology has relentlessly advanced through Moore’s Law, while internet connectivity has proliferated in concert with globalization. FedEx’s (FDX) Chief Information Officer Rob Carter summed it up nicely when he noted, “The sound we heard wasn’t the [tech] bubble bursting; it was the big bang.”

Even with the large advance in the NASDAQ index in recent years, valuations of the tech-heavy index remain within reasonable ranges. Accurate gauges of the NASDAQ Composite price-earnings ratio (P/E) are scarce, but just a few months ago, strategist Ned Davis pegged the index P/E at 21, well below the peak of 49 at the end of 1999. For now, the scars and painful memories of the 2000 crash have limited the amount of frothiness, although pockets of it certainly still exist (greed will never be fully eradicated).

Why NASDAQ & Technology Continue to Flourish

Regardless of how one analyzes the stock market, ultimately long-term stock prices follow the direction of profits and cash flows. Profits and cash flows don’t however grow out of thin air. Sustainable growth requires competitiveness. For most industries, a long-term competitive advantage requires a culture of innovation and technology adoption. As you can see from the NASDAQ listed companies BELOW, there is no shortage of innovation.

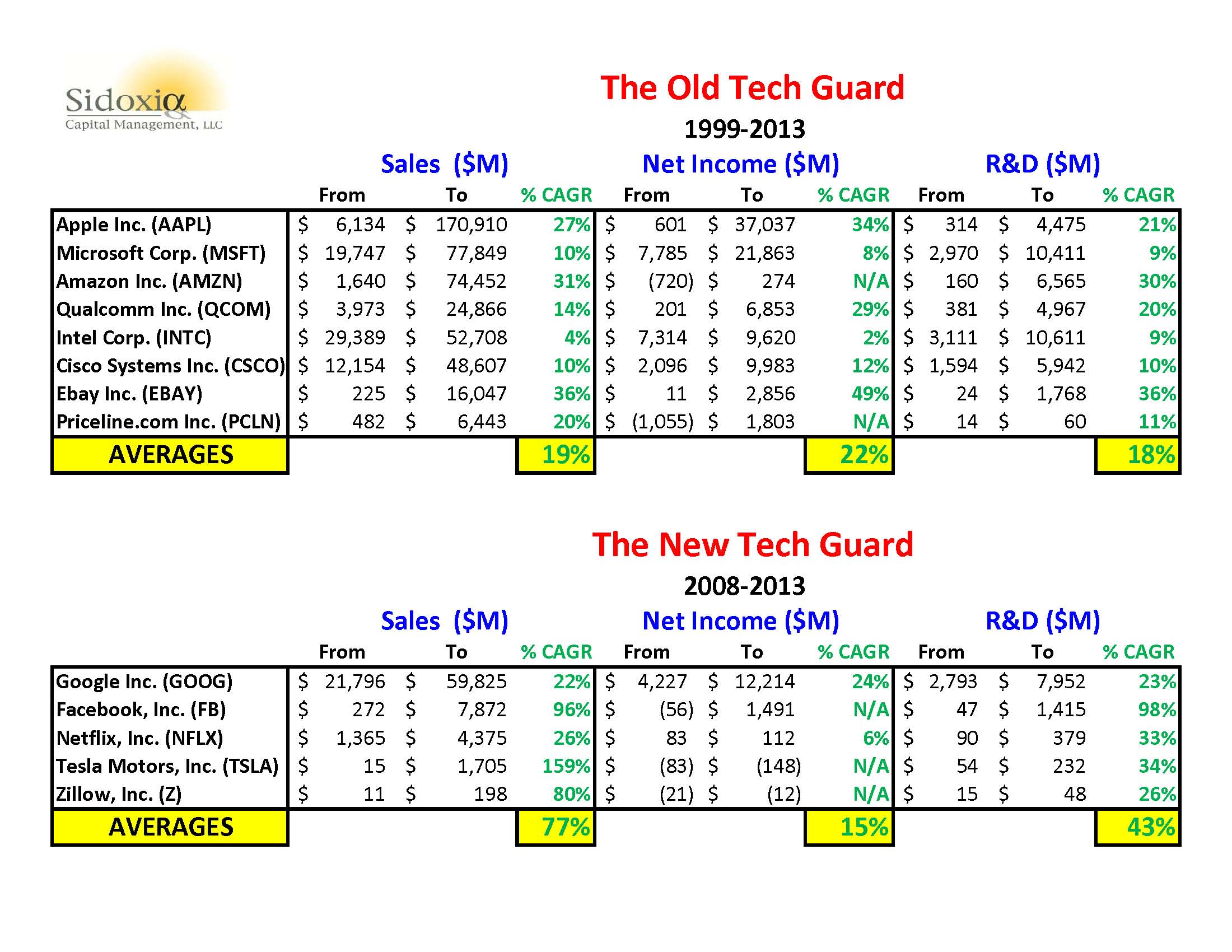

CLICK TO ENLARGE

Sources: ADVFN, SEC, Other

I’ve divided the largest technology companies in the NASDAQ 100 index that survived the bursting of the 2000 technology bubble into “The Old Tech Guard.” This group of eight stocks represents a total market value of about $1.5 trillion – equivalent to almost 10% of our country’s Gross Domestic Product (GDP). Incredibly, this select collection of companies achieved an average sales growth rate of +19%; income growth of +22%; and research & development growth of +18% over a 14-year period (1999-2013).

The second group of younger stocks (a.k.a., The New Tech Guard) that launched their IPOs post-2000 have accomplished equally impressive results. Together, these handful of companies have earned a market value of over $625 billion. There’s a reason investors are gobbling up these stocks. Over the last five years, The New Tech Guard companies have averaged an unbelievable +77% sales growth rate, coupled with a remarkable +43% expansion in average annual R&D expenditures.

Innovation Dead?

Who said innovation is dead? Not me. Combined, these 13 companies (Old Guard + New Guard) are spending about $55,000,000,000 on research and development…annually! If you consider the hundreds and thousands of other technology companies that are also investing aggressively for the future, it should come as no surprise that the pace of innovation is only accelerating.

While newscasters, bloggers, and newspapers will continue to myopically focus on the Dow and S&P 500 indices, do your investment portfolio a favor by not forgetting about the relentless R&D and tech revolution taking place within the innovative and often overlooked NASDAQ index.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AAPL, GOOG, AMZN, FDX, QCOM, and a short position in NFLX, but at the time of publishing SCM had no direct discretionary position in MSFT, INTC, CSCO, EBAY, PCLN, FB, TSLA, Z, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What’s Going on with This Crazy Market?!

The massive rally of the stock market since March 2009 has been perplexing for many, but the state of confusion has reached new heights as the stock market has surged another +2.0% in May, surpassing the Dow 15,000 index milestone and hovering near all-time record highs. Over the last few weeks, the volume of questions and tone of disbelief emanating from my social circles has become deafening. Here are some of the questions and comments I’ve received lately:

“Wade, why in the heck is the market up so much?”; “This market makes absolutely no sense!”; “Why should I buy at the peak when I can buy at the bottom?”; “With all this bad news, when is the stock market going to go down?”; “You must be shorting (betting against) this market, right?”

If all the concerns about the Benghazi tragedy, IRS conservative targeting, and Federal Reserve bond “tapering” are warranted, then it begs the question, “How can the Dow Jones and other indexes be setting new all-time highs?” In short, here are a few reasons:

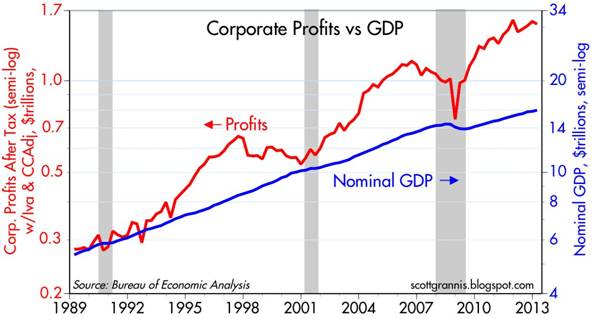

You hear a lot of noise on TV and read a lot of blathering in newspapers/blogs, but what you don’t hear much about is how corporate profits have about tripled since the year 2000 (see red line in chart above), and how the profit recovery from the recent recession has been the strongest in 55 years (Scott Grannis). The profit collapse during the Great Recession was closely chronicled in nail-biting detail, but a boring profit recovery story sells a lot less media advertising, and therefore gets swept under the rug.

II.) Reasonable Prices (Comparing Apples & Oranges):

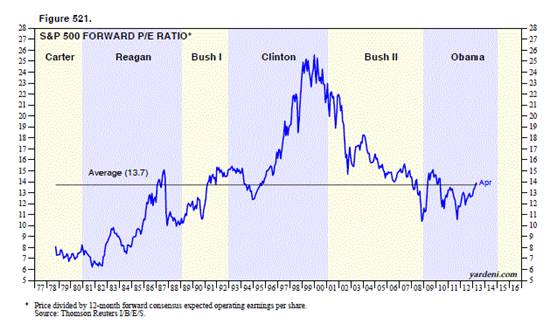

Source: Dr. Ed’s Blog

The Price-Earnings ratio (P/E) is a general barometer of stock price levels, and as you can see from the chart above (Ed Yardeni), current stock price levels are near the historical average of 13.7x – not at frothy levels experienced during the late-1990s and early 2000s.

Comparing Apples & Oranges:

At the most basic level of analysis, investors are like farmers who choose between apples (stocks) and oranges (bonds). On the investment farm, growers are generally going to pick the fruit that generates the largest harvest and provide the best return. Stocks (apples) have historically offered the best prices and yielded the best harvests over longer periods of time, but unfortunately stocks (apples) also have wild swings in annual production compared to the historically steady crop of bonds (oranges). The disastrous apple crop of 2008-2009 led a massive group of farmers to flood into buying a stable supply of oranges (bonds). Unfortunately the price of growing oranges (i.e., buying bonds) has grown to the highest levels in a generation, with crop yields (interest rates) also at a generational low. Even though I strongly believe apples (stocks) currently offer a better long-term profit potential, I continue to remind every farmer (investor) that their own personal situation is unique, and therefore they should not be overly concentrated in either apples (stocks) or oranges (bonds).

Source: Dr. Ed’s Blog

Regardless, you can see from the chart above (Dr. Ed’s Blog), the red line (stocks) is yielding substantially more than the blue line (bonds) – around 7% vs. 2%. The key for every investor is to discover an optimal balance of apples (stocks) and oranges (bonds) that meets personal objectives and constraints.

III.) Skepticism (Market Climbs a Wall of Worry):

Source: Calafia Beach Pundit

Although corporate profits are strong, and equity prices are reasonably priced, investors have been withdrawing hundreds of billions of dollars from equity funds (negative blue lines in chart above – Calafia Beach Pundit). While the panic of 2008-2009 has been extinguished from average investors’ psyches, the Recession in Europe, slowing growth in China, Washington gridlock, and the fresh memories of the U.S. financial crisis have created a palpable, nervous skepticism. Most recently, investors were bombarded with the mantra of “Selling in May, and Going Away” – so far that advice hasn’t worked so well. To buttress my point about this underlying skepticism, one need not look any further than a recent CNBC segment titled, “The Most Confusing Market Ever” (see video below):

Source: CNBC

It’s clear that investors remain skittish, but as legendary investor Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” The sentiment pendulum has been swinging in the right direction (see previous Investing Caffeine article), but when money flows sustainably into equities and optimism/euphoria rules the day, then I will become much more fearful.

Being a successful investor or a farmer is a tough job. I’ll stop growing apples when my overly optimistic customers beg for more apples, and yields on oranges also improve. In the meantime, investors need to remember that no matter how confusing the market is, don’t put all your oranges (bonds) or apples (stocks) in one basket (portfolio) because the financial markets do not need to get any crazier than they are already.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Herbalife Strife: Icahn & Ackman Duke It Out

I have seen a lot of things in my two decades in the investment industry, but seeing a verbal cage fight between a senile 76 year-old corporate raider and a white-haired, 46 year-old Harvard grad makes for surprisingly entertaining viewing. The investment heavyweights I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. If getting a few billionaires yelling at each other on live TV is not enough to interest you, then how about adding some tongue-laced f-bombs coupled with blow-by-blow screaming from background traders?

What’s the source of the venomous, spitting hatred between these stock market tycoons? In short, it can be boiled down to a decade old lawsuit (profitable for both I might add), and a disagreement over the short position of a controversial stock, Herbalife (HLF). Regarding the legal spat, in 2003 the SEC was investigating Ackman while his Gotham Partners hedge fund was collapsing, so Ackman asked Icahn to buy shares of Hallwood Realty in hopes of salvaging his fund. Eventually, Icahn bought shares, but a difference in opinion over the transaction led to a lawsuit that Icahn lost, thereby forcing him to pay Ackman $9 million.

Icahn also had a beef with Ackman’s handling of Herbalife: Parading in front of hundreds of investors to self-indulgently create a bear raid on an unsuspecting company is poor form in Icahn’s view, and Carl wanted to make sure Ackman was aware of this investing faux pas.

Normally, investing reporting over cable television is rather mundane, unless you consider entertainers like Jim Cramer yelling “booyah” amusing (see also my article on Mr. Booyah)? On the other hand, if you enjoy billionaires embracing the spirit of the Jerry Springer Show by screaming purple-faced profanities, then you should check out the CNBC cage fight here in its entirety:

If you lack time in your busy schedule to soak in the full bloody battle, then here is a synopsis of my favorite highlights:

Icahn on Ackman the “Crybaby”: “I really sort of have had it with this guy Ackman….I get a call from this Ackman guy. I’m telling you, he’s like the crybaby in the schoolyard. I went to a tough school in Queens. They used to beat up the little Jewish boys. He was like a little Jewish boy crying that the world was taking advantage of him.”

Ackman Referring to Icahn as a “Bully” and Himself as “Roadkill on the Hedge Fund Highway”: “Why did he [Icahn] threaten to sue me? He was a bully. Okay? I was not in a good place in my business career. I was under investigation by Spitzer, winding down my fund. There was negative press about Gotham Partners. I was short MBIA (MBI). They were aggressively attacking me and Carl Icahn thought this guy [Ackman] is roadkill on the hedge fund highway… This is not an honest guy [Icahn] who keeps his word. This is a guy who takes advantage of little people.”

Agitated Icahn Tearing a New One for Scott Wapner (CNBC Commentator): “I didn’t get on to be bullied by you [Wapner]… I’m going to talk about what I want to talk about. Okay? If you want to take that position, I will never go on CNBC. You can say what the hell you want. I’m going to talk about what Ackman just said about me, not about Herbalife. I’ll talk about Herbalife when I want to, not when you ask me. I’m never going on a show with you again, that’s for damn sure. Let’s start with what I want to say. Ackman is a liar.”

Icahn on Another Ackman Rampage: “I will tell you something. As far as I’m concerned, he wanted to have dinner with me and I laughed. I couldn’t figure out if he was the most sanctimonious guy or the most arrogant… the guy takes inordinate risk…I don’t have an investment with Ackman. I wouldn’t have one if you paid me, if Ackman paid me to do it… I made a huge mistake getting involved with him…After he won [the lawsuit], he planted some article in the New York Times pounding his chest telling the world how great he was. You know, as far as I’m concerned the guy is a major loser.”

New CNBC Revenue Stream?

There hasn’t been this much fireworks since Professor Jeremy Siegel took Bill Gross to task on the Pimco Boss’s assessment that the “cult of equity is dying” last July. In retrospect, that minor tiff was child’s play relative to the Icahn vs. Ackman battle. With CNBC viewership down from pre-crisis levels, the network may strongly consider instituting a new pay-per-view revenue stream dedicated to battles between opposing investment enemies. I will even offer up my services to verbally smack down some of the enemies I’ve written about previously. If my phones don’t ring, then I can always offer up my American Investment Idol concept in which I can play Simon Cowell.

This may or may not be the last round of the Carl Icahn and Bill Ackman fight, but the ultimate bragging rights may depend on the ultimate outcome of Ackman’s Herbalife short. If Icahn makes a tender offer for Herbalife, I will anxiously wait for CNBC’s Scott Wapner to invite Carl back on the show. I can hardly wait…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, MBI, NYT, Hallwood Realty, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Gobbling Up the All-You-Can-Eat Data Buffet

Gorging oneself at an all-you-can eat buffet has its advantages, but managing the associated extra pounds and bloatedness carries its own challenges. In a similar fashion, businesses and consumers are devouring data at an exponential rate, while simultaneously attempting to slice, dice, manage, and store all of this information. Data is quickly becoming as cheap as oxygen, and there are virtually no limitations on the amount consumed.

With the help of my handy smart phone, tablet, and digital camera, I can almost store and watch every moment of my life, very much like the movie The Truman Show. Social media and cloud services, coupled with inexpensive storage, have only made it simpler to digitally archive my life. Pretty soon, with the click of a mouse (or tap of the tablet) everyone will be able to instantaneously access every important moment of their life from cradle to grave.

Consuming Data Bytes at a Time

If you are in the mood for consuming free data, there are plenty of free multi-gigabyte services to choose from, including Dropbox, Mozy, and SkyDrive among other. For those chomping on more than 25 gigabytes of data, paid services like Amazon.com’s (AMZN) Simple Storage Service (a.k.a, “S3”) allow users to store a terabyte of data for about $0.01 – $0.05 per month. However, if renting storage is not your gig (no pun intended), you can own your personal storage device for next to nothing. In fact, you can buy a 1 terabyte (equal to 1,000 gigabytes) external hard drive today for less than $70. If that’s too rich for your blood, then just wait 12 months or so and pay $50 bucks. To put a terabyte in context, this amount of storage can hold approximately 625,000 high quality photos or 412 DVD quality movies, according to a Financial Times article talking about “big data.”

A terabyte may sound like a lot, but if we’re going to be honest, this amount of storage is Tiddly Winks. Once we start talking about petabytes (1,000 terabytes), exabytes (1,000,000 terabytes), and zettabytes (1 billion terabytes), things begin to get a little more interesting (see chart below). If you consider that 2012 global data center traffic estimates amount to 2.6 zettabytes (or 2.6 billion terabytes), it doesn’t take long to appreciate the enormity of the data management challenge facing billions of people.

Source: The Financial Times

The Financial Times also points out the following:

“From the beginning of recorded time until 2003, we created five exabytes of data. In 2011 the same amount was created every two days. By 2013 it’s expected that the time will shrink to 10 minutes.”

Digital World Driving Data Appetite

What’s driving the global gusher of data growth? There’s not just one answer, but one can start understanding the scope of the issue after contemplating the trillions of annual text messages; 1 billion Facebook (FB) users; 800 million monthly YouTube visitors watching 4 billion hours of videos; six billion cell phones worldwide; and a global 122 million tablet market (IDC).

I certainly wasn’t the first person to discover this megatrend, but I am not hesitating to invest both my client’s money and my money into benefiting from this massive growth trend. Businesses are prospering from the data tidal wave too, as evidenced in part by Oracle Corp’s (ORCL) stellar quarterly earnings results reported just a few days ago. The mass migration of services to the “cloud” (software delivered over the internet) combined with the need to manage and store exploding industry data, resulted in Oracle reporting growth of +18% in its profitable Software License Sales and Cloud Subscriptions segment. With results like these, no wonder Oracle’s founder and CEO Larry Ellison owns a 141-mile square island, a multi-hundred million yacht, and is worth $41 billion according to Forbes (#3 on the Forbes 400 list).

Whether you realize it or not, we are all consuming heaps of all-you-can eat data at the digital buffet. Rather than rolling over into a data consumption coma, you will be much better off figuring out how to profit from the exploding data trends.

See also: The Age of Information Overload

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), GOOG, and AMZN, but at the time of publishing SCM had no direct positions in FB, ORCL, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chewing on Some Apple Pie

Apple pie is an unrivaled American dessert that optimally mixes the elements of dough, sugar, cinnamon, and apples. With Thanksgiving just around the corner, I can already taste that Costco (COST) apple pie that is about to snap my belt buckle open as I proceed to eat pie for breakfast, lunch, and dinner. A different dessert of the stock variety, Apple Inc. (AAPL), recently received a sour reception after reporting its 3rd quarter financial results.

Despite reporting +27% year-over-year revenue growth and +23% earnings growth, investors have continued to spew the stock out as the share price has fallen from $700 per share down to $600 per share in about a month. With all this indigestion, is now the time to reach for the Tums or should we serve ourselves up another helping of some tasty Apple pie? Not everybody loves this particular fruity dessert, so let’s cut into the Apple pie stock and see if there is any dough to be made here.

Point #1 (Cash Giant): Apple Inc. is a profit machine with a fortress balance sheet. More specifically, Apple has around $121 billion dollars in cash in its checking account and generated over $42 billion in free cash flow in fiscal 2012. And by free cash flow, I mean the excess cash Apple gets to stuff in its pockets after ALL expenses have been paid AND after spending more than $8 billion in capital expenditures (including spending for their new 2.8 million sq. foot spaceship campus expected to open in 2015 and house 13,000 employees).

Point #2: (Brand): A brand has value that will not show up on a balance sheet, and according to Forbes, Apple’s brand is rated #1 on a global basis, outstripping iconic brands like IBM, McDonald’s (MCD) and Microsoft (MSFT). BrandZ, a division of advertising giant WPP, values Apple’s 2012 brand value at approximately $183 billion.

Point #3 (Product Pipeline): Apple is no one-trick pony. Apple’s iPhone sales account for about half of the company’s sales, but a whole new slate of products positions them well for the critical calendar fourth quarter period. Apple’s iPhone 5, iPad 3 (aka, “New iPad”), and iPad Mini should translate into robust holiday sales for Apple. What’s more, a +39% increase in Apple’s fiscal 2012 R&D (research and development) should mean a continued healthy pipeline of new products, including the ever-rumored new integrated version of Apple TV that could be coming in 2013.

Point #4 (Mobile & Tablets): Apple is at the center of the mobile revolution. There are approximately 5 billion cell phones globally, and about 2 billion new phones are sold each year. Of that 2 billion, Apple sold a paltry 125 million units (tongue firmly in cheek) with the market growing faster in Apple iPhone’s key smart phone market. As the approximately 500 million smart phone market grows to about 5 billion units over the next decade, Apple is uniquely positioned to capitalize on this trend. Beyond cell phones, the table market is bursting as traditional personal computer growth declines. Although Apple has made computers for 36 years, the company impressively generated +40% more revenue from fiscal 2012 iPad tablet sales, relative to Apple desktop and laptop sales.

Point #5 (Valuation): With all these positives, what type of premium would you pay for Apple’s stock? Does a +100% premium sound reasonable? OK, maybe a tad high, so how about a +50% premium? Alright, alright, I know you want a good bargain, so surely a +20% premium is warranted? Well in fact, if you account for Apple’s $121 billion cash hoard, Apple’s stock is currently trading at about a -22% DISCOUNT to the average S&P 500 stock on a P/E basis (Price-Earnings). You heard that correctly, a significant discount. If Apple is trading at a P/E discount, surely mature staple stocks like Procter & Gamble (PG) and Colgate Palmolive (CL), which both reported negative Q3 revenue declines coupled with meager bottom-line growth of 5%, deserve even steeper discounts…right? WRONG. These stocks trade at a 70-80% PREMIUM to Apple and a 35-40% PREMIUM to the overall market. Toilet paper and toothpaste I guess are a lot more popular than consumer electronics these days. Clear as mud to me.

Risks: I understand that Apple is not a risk-free Treasury security. Research in Motion’s (RIMM) rapid collapse over the last two years serves as a fresh reminder that in technology land, competition and obsolescence risks play a much larger role compared to other industries. Apple must still deliver on its product visions, and as the king of the hill Apple will have a big bulls-eye on its back from both competitors and regulators. Hence, we will continue to read overblown headlines about map application glitches and photographic purple haze.

In the end, a significant amount of pessimism is already built into Apple’s stock price (yes, I did say “pessimism” – even with the stock’s share price up +49% this year). If Apple can uphold the quality of its products and maintain modest growth, then I’m confident shareholders will happily eat another slice of Apple pie.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct positions in COST, IBM, MCD, CL, PG, MSFT, WPP, RIMM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}