Posts filed under ‘Financial Planning’

Buy in May and Tap Dance Away

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (May 1, 2014). Subscribe on the right side of the page for the complete text.

The proverbial Wall Street adage that urges investors to “Sell in May, and go away” in order to avoid a seasonally volatile period from May to October has driven speculative trading strategies for generations. The basic premise behind the plan revolves around the idea that people have better things to do during the spring and summer months, so they sell stocks. Once the weather cools off, the thought process reverses as investors renew their interest in stocks during November. If investing was as easy as selling stocks on May 1 st and then buying them back on November 1st, then we could all caravan in yachts to our private islands while drinking from umbrella-filled coconut drinks. Regrettably, successful investing is not that simple and following naïve strategies like these generally don’t work over the long-run.

Even if you believe in market timing and seasonal investing (see Getting Off the Market Timing Treadmill ), the prohibitive transaction costs and tax implications often strip away any potential statistical advantage.

Unfortunately for the bears, who often react to this type of voodoo investing, betting against the stock market from May – October during the last two years has been a money-losing strategy. Rather than going away, investors have been better served to “Buy in May, and tap dance away.” More specifically, the S&P 500 index has increased in each of the last two years, including a +10% surge during the May-October period last year.

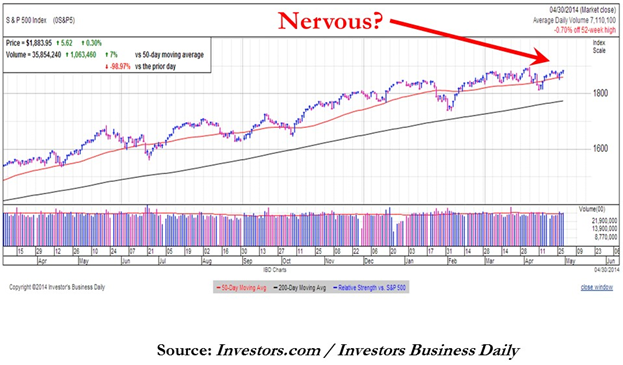

Nervous? Why Invest Now?

With the weak recent economic GDP figures and stock prices off by less than 1% from their all-time record highs, why in the world would investors consider investing now? Well, for starters, one must ask themselves, “What options do I have for my savings…cash?” Cash has been and will continue to be a poor place to hoard funds, especially when interest rates are near historic lows and inflation is eating away the value of your nest-egg like a hungry sumo wrestler. Anyone who has completed their income taxes last month knows how pathetic bank rates have been, and if you have pumped gas recently, you can appreciate the gnawing impact of escalating gasoline prices.

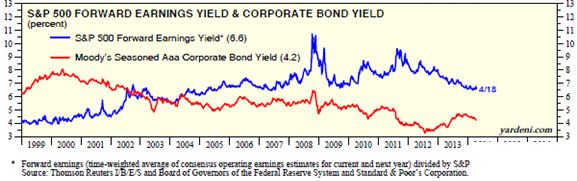

While there are selective opportunities to garner attractive yields in the bond market, as exploited in Sidoxia Fusion strategies, strategist and economist Dr. Ed Yardeni points out that equities have approximately +50% higher yields than corporate bonds. As you can see from the chart below, stocks (blue line) are yielding profits of about +6.6% vs +4.2% for corporate bonds (red line). In other words, for every $100 invested in stocks, companies are earning $6.60 in profits on average, which are then either paid out to investors as growing dividends and/or reinvested back into their companies for future growth.

Source: Dr. Ed’s Blog

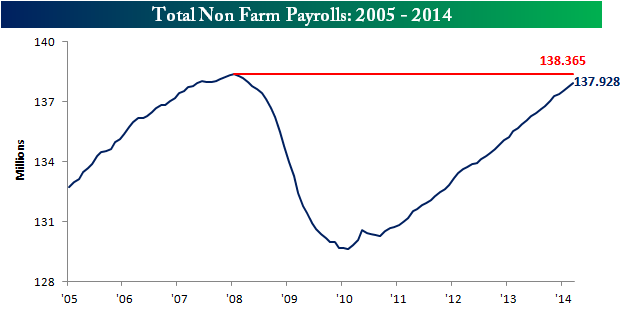

Hefty profit streams have resulted in healthy corporate balance sheets, which have served as ammunition for the improving jobs picture. At best, the economic recovery has moved from a snail’s pace to a tortoise’s pace, but nevertheless, the unemployment rate has returned to a more respectable 6.7% rate. The mended economy has virtually recovered all of the approximately 9 million private jobs lost during the financial crisis (see chart below) and expectations for Friday’s jobs report is for another +220,000 jobs added during the month of April.

Source: Bespoke

Wondrous Wing Woman

Investing can be scary for some individuals, but having an accommodative Fed Chair like Janet Yellen on your side makes the challenge more manageable. As I’ve pointed out in the past (with the help of Scott Grannis), the Fed’s stimulative ‘Quantitative Easing’ program counter intuitively raised interest rates during its implementation. What’s more, Yellen’s spearheading of the unprecedented $40 billion bond buying reduction program (a.k.a., ‘Taper’) has unexpectedly led to declining interest rates in recent months. If all goes well, Yellen will have completed the $85 billion monthly tapering by the end of this year, assuming the economy continues to expand.

In the meantime, investors and the broader financial markets have begun to digest the unwinding of the largest, most unprecedented monetary intervention in financial history. How can we tell this is the case? CEO confidence has improved to the point that $1 trillion of deals have been announced this year, including offers by Pfizer Inc. – PFE ($100 billion), Facebook Inc. – FB ($19 billion), and Comcast Corp. – CMCSA ($45 billion).

Source: Entrepreneur

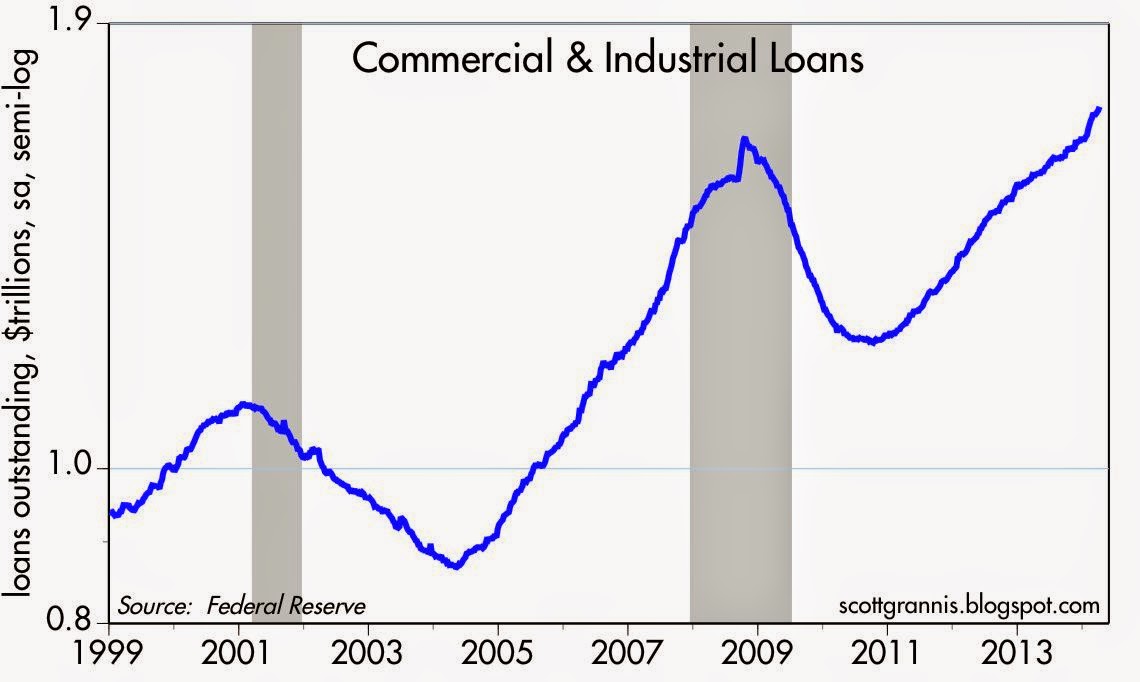

Banks are feeling more confident too, and this is evident by the acceleration seen in bank loans. After the financial crisis, gun-shy bank CEOs fortified their balance sheets, but with five years of economic expansion under their belts, the banks are beginning to loosen their loan purse strings further (see chart below).

The coast is never completely clear. As always, there are plenty of things to worry about. If it’s not Ukraine, it can be slowing growth in China, mid-term elections in the fall, and/or rising tensions in the Middle East. However, for the vast majority of investors, relying on calendar adages (i.e., selling in May) is a complete waste of time. You will be much better off investing in attractively priced, long-term opportunities, and then tap dance your way to financial prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE, CMCSA, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in FB or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Passive vs. Active Investing: Darts, Monkeys & Pros

Bob Turner is founder of Turner Investments and a manager of several funds at the investment company. In a recent article he reintroduces the all-important, longstanding debate of active management (“hands-on”) versus passive management (“hands off”) approaches to investing. Mr. Turner makes some good arguments for the active management camp, however some feel differently – take for example Burton Malkiel. The Princeton professor theorizes in his book A Random Walk Down Wall Street that “a blindfolded monkey throwing darts at a newspaper’s stock page could select a portfolio that would do just as well as one carefully selected by experts.” In fact, The Wall Street Journal manages an Investment Dartboard contest that stacks up amateur investors’ picks against the pros’ and random stock picks selected by randomly thrown darts. In many instances, the dartboard picks outperform the professionals. Given the controversy, who’s right…the darts, monkeys, or pros? Distinguishing between the different categorizations can be difficult, but we will take a stab nevertheless.

Arguments for Active Management

Turner contends, active management outperforms in periods of high volatility and he believes the industry will be entering such a phase:

“Active managers historically have tended to perform best in a market in which the performance of individual stocks varies widely.”

He also acknowledges that not all active managers outperform and admits there are periods where passive management will do better:

“The reason why most active investors fail to outperform is because they in fact constitute most of the market. Even in the best of times, not all active managers can hope to outperform…The business of picking stocks is to some degree a zero-sum game; the results achieved by the best managers will be offset at least somewhat by the subpar performance of other managers.”

Buttressing his argument for active management, Turner references data from Advisor Perspectives showing an inconclusive percentage (40.5%-67.8%) of the actively managed funds trailing the passively managed indexes from 2000 to 2008.

The Case for Passive Management

Turner cites one specific study to support his active management cause. However, my experience gleaned from the vast amounts of academic and industry data point to approximately 75% of active managers underperforming their passively managed indexes, over longer periods of time. Notably, a recent study conducted by Standard & Poor’s SPIVA division (S&P Indices Versus Active Funds) discovered the following conclusions over the five year market cycle from 2004 to 2008:

- S&P 500 outperformed 71.9% of actively managed large cap funds;

- S&P MidCap 400 outperformed 79.1% of mid cap funds;

- S&P SmallCap 600 outperformed 85.5% of small cap funds.

Read more about the dirty secrets shrinking your portfolio. According to the Vanguard Group and the Investment Company Institute, about 25% of institutional assets and about 12% of individual investors’ assets are currently indexed (passive strategies). If you doubt the popularity of passive investment strategies, then look no further than the growth of Exchange Traded Funds (ETFs – see chart), index funds, or Vanguard Groups more than $1 trillion dollars in assets under management.

Although I am a firm believer in passive investing, one of its shortcomings is mean reversion. This is the idea that upward or downward moving trends tend to revert back to an average or normal level over time. Active investing can take advantage of mean reversion, conversely passive investing cannot. Indexes can get very top-heavy in weightings of outperforming sectors or industries, meaning theoretically you could be buying larger and larger shares of an index in overpriced glamour stocks on the verge of collapse. We experienced these lopsided index weightings through the technology bubbles in the late 1990s and financials in 2008. Some strategies may be better than other over the long run, but every strategy, even passive investing, has its own unique set of deficiencies and risks.

Professional Sports and Investing

As I discuss in my book, there are similarities that can be drawn between professional sports and investing with respect to active vs. passive management. Like the scarce number of .300 hitters in baseball, I believe there are a select few investment managers who can consistently outperform the market. In 2007, AssociatedContent.com did a study that showed there were only 22 active career .300 hitters in Major League Baseball. I recognize in the investing world there can be a larger role for “luck,” which is difficult, if not impossible, to measure (luck won’t help me much in hitting a 100 mile per hour fastball thrown by Nolan Ryan). Nonetheless, in the professional sports arena, there are some Hall of Famers (prospects) that have proved they could (can) consistently outperform their peers for extended durations of time. Experience is another distinction I would highlight in comparing sports and investing. Unlike sports, in the investment world I believe there is a positive correlation between age and ability. The more experience an investor gains, generally the better long-term return achieved. Like many professions, the more experience you gain, the more valuable you become. Unfortunately, in many sports, ability deteriorates and muscles atrophy over time.

Size Matters

Experience alone will not make you a better investor. Some investors are born with an innate gift or intellect that propels them ahead of the pack. However, most great investors eventually get cursed by their own success thanks to accumulating assets. Warren Buffet knows the consequences of managing large amounts of dollars, “gravity always wins.” Having managed a $20 billion fund, I fully appreciate the challenges of investing larger sums of money. Managing a smaller fund is similar to navigating a speed boat – not too difficult to maneuver and fairly easy to dodge obstacles. Managing heftier pools of money can be like captaining a supertanker, but unfortunately the same rapid u-turn expectations of the speedboat remain. Managing large amounts of capital can be crippling, and that’s why captaining a supertanker requires the proper foresight and experience.

Room for All

As I’ve stated before, I believe the market is efficient in the long run, but can be terribly inefficient in the short-run, especially when the behavioral aspects of emotion (fear and greed) take over. The “wait for me, I want to play too” greed from the late 1990s technology craze and the credit-based economic collapse of 2008-2009 are further examples of inefficient situations that can be exploited by active managers. However, due to multiple fees, transaction costs, taxes, not to mention the short-term performance/compensation pressures to perform, I believe the odds are stacked against the active managers. For those experienced managers that have played the game for a long period and have a track record of success, I feel active management can play a role. At Sidoxia Capital Management, I choose to create investment portfolios that blend a mixture of passive and active investment strategies. Although my hedge fund has outperformed the S&P 500 in 4 of the last 5 years, that fact does not necessarily mean it’s the appropriate sole approach for all clients. As Warren Buffet states, investors should stick to their “circle of competence” so they can confidently invest in what they know. That’s why I generally stick to the areas of my expertise when I’m actively investing in stocks, and fill in the remainder of client portfolios with transparent, low-cost, tax-efficient equity and fixed income products (i.e., Exchange Traded Funds). Even though the actively managed Turner Funds appear to have a mixed-bag of performance numbers relative to passively managed strategies, I appreciate Bob Turner’s article for addressing this important issue. I’m sure the debate will never fully be resolved. In the meantime, my client portfolios will aim to mix the best of both worlds within active and passive management strategies in the eternal quest of outwitting the darts, monkeys, and other pros.

Read the full Bob Turner article on Morningstar.com

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds but had no direct position in stocks mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

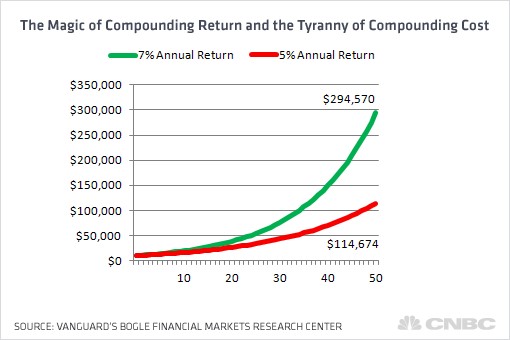

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia’s Slome Hits Airwaves

Sidoxia’s President & Founder Conducts Series of Radio Interviews Spanning Topics Ranging from the Stock Market & Syria to Financial Planning & Government Debt

Click on Interview Links Below:

Memphis

Memphis

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. Radio interviews included opinions of Wade Slome – not advice. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sleeping like a Baby with Your Investment Dollars

Amidst the recent, historically high volatility in the financial markets, there have been a large percentage of investors who have been sleeping like a baby – a baby that stays up all night crying! For some, the dream-like doubling of equity returns achieved from the first half of 2009 through the first half of 2011 quickly turned into a nightmare over the last few weeks. We live in an inter-connected, globalized world where news travels instantaneously and fear spreads like a damn-bursting flood. Despite the positive returns earned in recent years, the wounds of 2008-2009 (and 2000 to a lesser extent) remain fresh in investors’ minds. Now, the hundred year flood is expected every minute. Every European debt negotiation, S&P downgrade, or word floating from Federal Reserve Chairman Ben Bernanke’s lips, is expected to trigger the next Lehman Brothers-esque event that will topple the global economy like a chain of dominoes.

Volatility Victims

The few hours of trading that followed the release of the Federal Reserve’s August policy statement is living proof of investors’ edginess. After initially falling approximately -400 points in a 30 minute period late in the day, the Dow Jones Industrial Average then climbed over +600 points in the final hour of trading, before experiencing another -400 point drop in the first hour of trading the next day. Many of the day traders and speculators playing with the explosively leveraged exchange traded funds (e.g., TNA, TZA, FAS, FAZ), suffered the consequences related to the panic selling and buying that comes with a VIX (Volatility Index) that climbed about +175% in 17 days. A VIX reading of 44 or higher has only been reached nine times in the last 25 years (source: Don Hays), and is normally associated with significant bounce-backs from these extreme levels of pessimism. Worth noting is the fact that the 2008-2009 period significantly deteriorated more before improving to a more normalized level.

Keys to a Good Night’s Sleep

The nature of the latest debt ceiling negotiations and associated Standard & Poor’s downgrade of the United States hurt investor psyches and did little to boost confidence in an already tepid economic recovery. Investors may have had some difficulty catching some shut-eye during the recent market turmoil, but here are some tips on how to sleep comfortably.

• Panic is Not a Strategy: Panic selling (and buying) is not a sustainable strategy, yet we saw both strategies in full force last week. Emotional decisions are never the right ones, because if they were, investing would be quite easy and everyone would live on their own personal island. Rather than panic-sell, investments should be looked at like goods in a grocery store – successful long-term investors train themselves to understand it is better to buy goods when they are on sale. As famed growth investor Peter Lynch said, “I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.”

• Long-Term is Right-Term: Everybody would like to retire at a young age, and once retired, live like royalty. Admirable goals, but both require bookoo bucks. Unless you plan on inheriting a bunch of money, or working until you reach the grave, it behooves investors to pull that money out from under the mattress and invest it wisely. Let’s face it, entitlements are going to be reduced in the future, just as inflation for food, energy, medical, leisure and other critical expenses continue eroding the value of your savings. One reason active traders justify their knee-jerk actions and derogatory description of long-term investors is based on the stagnant performance of U.S. equity markets over the last decade. Nonetheless, the vast number of these speculators fail to recognize a more than tripling in average values in markets like Brazil, India, China, and Russia over similar timeframes. Investing is a global game. If you do not have a disciplined, systematic long-term investment strategy in place, you better pray you don’t lose your job before age 70 and be prepared to eat Mac & Cheese while working as a Wal-Mart (WMT) greeter in your 80s.

• Diversification: Speaking of sleep, the boring topic of diversification often puts investors to sleep, but in periods like these, the power of diversification becomes more evident than ever. Cash, metals, and certain fixed income instruments were among the investments that cushioned the investment blow during the 2008-2009 time period. Maintaining a balanced diversified portfolio across asset classes, styles, size, and geographies is crucial for investment survival. Rebalancing your portfolio periodically will ensure this goal is achieved without taking disproportionate sized risks.

• Tailored Plan Matching Risk Tolerance: An 85 year-old wouldn’t go mountain biking on a tricycle, and a 10 year-old shouldn’t drive a bus to his fifth grade class. Sadly, in volatile times like these, many investors figure out they have an investment portfolio mismatched with their goals and risk tolerance. The average investor loves to take risk in up-markets and shed risk in down-markets (risk in this case defined as equity exposure). Regrettably, this strategy is designed exactly backwards for long-term investors. Historically, actual risk, the probability of permanent losses, is much lower during downturns; however, the perceived risk by average investors is viewed much worse. Indeed, recessions have been the absolute best times to purchase risky assets, given our 11-for-11 successful track record of escaping post World War II downturns. Could this slowdown or downturn last longer than expected and lead to more losses? Absolutely, but if you are planning for 10, 20, or 30 years, in many cases that issue is completely irrelevant – especially if you are still adding funds to your investment portfolio (i.e., dollar-cost averaging). On the flip side, if an investor is retired and entirely dependent upon an investment portfolio for income, then much less attention should be placed on risky assets like equities.

If you are having trouble sleeping, then one of two things is wrong: 1.) You are taking on too much risk and should cut your equity exposure; and/or 2.) You do not understand the risk you are taking. Volatile times like these are great for reevaluating your situation to make sure you are properly positioned to meet your financial goals. Talking heads on TV will tell you this time is different, but the truth is we have been through worse times (see History Never Repeats, but Rhymes), and lived to tell the tale. All this volatility and gloom may create anxiety and cause insomnia, but if you want to quietly sleep through the noise like a content baby, make yourself a long-term financial bed that you can comfortably sleep in during good times and bad. Focusing on the despondent headline of the day, and building a portfolio lacking diversification will only lead to panic selling/buying and results that would keep a baby up all night crying.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market ETFs) and WMT, but at the time of publishing SCM had no direct position in TNA, TZA, FAS, FAZ, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Getting & Staying Rich 101

Fred J. Young worked 27 years as a professional money manager and investment counselor in the trust department at Harris Bank in Chicago. While working there he learned a few things about wealth accumulation and preservation, which he outlines in his book How to Get Rich and Stay Rich.

There is more than one way to skin a cat, and when it comes to getting rich, Young describes the only three ways of getting loaded:

1.) Inherit It: Using this method on the path to richness generally doesn’t take a lot of blood, sweat, and tears (perhaps a little brown-nosing wouldn’t hurt), but young freely admits you can skip his book if you are fortunate enough to garner boatloads of cash through your ancestry.

2.) Marry It: This approach to wealth accumulation can require a bit more effort than method number one. However, Young explains that if the Good Lord intended you to find your lifetime lover through destiny, then if your soul-mate has a lot of dough Young advises, “You [should] graciously accept the situation. Don’t fight it.”

3.) Spend < Earn: Normally this avenue to champagne and caviar requires the most effort. How does one execute option number three? “You spend less than you earn and invest the difference in something you think will increase in value and make you rich,” simply states Young. Sounds straightforward, but what does one invest their excess cash in? Young succinctly lists the customary investment tools of choice for wealth creation:

- Real estate

- Own their own business

- Common stocks

- Savings accounts (thanks to the magic of compound interest rates) – see also Penny Saved is Billions Earned

Rich Luck

If faced with choosing between good luck and good judgment, here is Fred Young’s response:

“You should take good luck. Good luck, by definition, denotes success. Good judgment can still go wrong.”

Like many endeavors, it’s good to have some of both (good luck and good judgment).

The Role of Courage

Courage is especially important when it comes to equity investing because buying stocks includes a very counterintuitive behavioral aspect that requires courage. Following the herd of average investors and buying stocks at new highs is easy and does not require a lot of courage. Young describes the various types of courage required for successful investing:

“The courage to buy when others are selling; the courage to buy when stocks are hitting new lows; the courage to buy when the economy looks bad; courage to buy at the bottom…The times when the gloom was the thickest invariably turned out to have been the best times to buy stocks.”

Keeping the Cash

Becoming rich is only half the challenge. In many cases staying rich can be just as difficult as accumulating the wealth. Young points out the intolerable pain caused by transitioning from wealth to poverty. What is Young’s solution to this tricky problem? Seek professional help. The risks undertaken to build wealth still exist when you are rich, and those same risks have the capability of tearing financial security away.

There are three paths to riches according to Fred Young (inheritance, marriage, and prudent investing). Some of these directions leading to mega-money require more effort than others, but if you are lucky enough to have deep pockets of riches, make sure you have the discipline and focus necessary to maintain that wealth – those deep pockets could have a hole.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Annuity Trap

Like the infamous Roach Motel, annuities allow investors to check-in while making it very difficult to check out. In many instances, getting out of annuities can be cost prohibitive (fees, charges, commissions, expenses, etc.), even if escaping these fee-laden products is in the investors’ best financial interest.

In an article dated April 13th, 2010, Jay Peroni warned others by outlining a typical annuity fee structure as follows:

- Mortality and Expense Charge 1.50%

- Sub Account Management Fees 1.00%

- Unreported trading costs 0.78%

- Annual Administrative Expenses 0.15%

TOTAL ANNUAL EXPENSES 3.43%

What aren’t included in these numbers above are the surrender charges, which effectively can lock you into the annuity if you are averse to paying hefty surrender charges. Normally, the surrender charges vary from up to a 10% charge for large withdrawals in year one, decreasing to something like 1% in year 10. Worth noting, steep sales commissions can be layered on top of the previous charges or mysteriously embedded in the fee structure categories above.

The Big Sell

Driving the push for these 3%+ annual fees are lucrative financial institutions hiring aggressive salespeople. Typically annuities are sold under the guise of safe tax shelter investments. What the broker won’t tell you is that only a fraction (“exclusion ratio”) of the annuity payments is shielded from taxes, and the rest of the payments are taxed at the higher, unfavorable ordinary income tax rate (relative to qualified dividends and capital gains from other securities). Much of the time, many of the salespeople, who call themselves “financial advisors,” know little about these complex annuity products (see Financial Sharks article). What these brokers do understand are the big, fat commissions they stand to collect upon fleecing unsuspecting investors.

Scores of these so-called advisors are actually “registered representatives” who do not carry a fiduciary duty (meaning they are NOT required to make investment decisions in the best interest of their clients). Certainly, there are some situations where annuities might be appropriate, but from my experience there are very few cases where the egregious charges and expenses outweigh the benefits. I believe the vast majority of brokers/registered reps/salespeople are more concerned about padding their wallets than building and protecting client portfolios.

The Alternatives

If safety and tax advantages are features you are looking for then I encourage you to look at more efficient options such as the following:

- 401k Defined Contribution Retirement Plan (or other “Qualified Plan”): Allows you to achieve tax deferral often with free money given to you in the form of a match to your contributions.

- IRA (Individual Retirement Account): Whether you consider a traditional or Roth IRA, there are tax deferral advantages with lower fees.

- Low Turnover, High Dividend Portfolios: Using a tax efficient management strategy with better tax treatment of income is another approach that I firmly believe will outperform most annuities.

- Tax-Exempt Muni Bonds or Corporates: The tax-exempt status of municipal bonds affords investors a tax advantaged status. The after-tax yield on corporate bonds can be compared to the returns promised on annuities (AFTER all fees, charges, and commissions). Holding individual bonds until maturity can help avoid interest rate risk.

- Ladder Zero Coupon Bonds: If safe fixed payments are what you are looking for, then staggered purchases of zero coupon bonds can be purchased as well.

These are only a few options that could and should be considered when reviewing your personal objectives and circumstances. With regard to the insurance component of an annuity contract, there are more cost effective ways of paying for insurance – most notably, term insurance.

At the end of the day, no matter the financial product, it is important you understand the underlying fees charged on any strategy, along with how the person selling you stuff is compensated. If you don’t do your homework on these extremely complex products (many not regulated by the NASD or SEC), then you may find yourself checking into the annuity hotel, but unable to check out.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Do as I Say, Not as I Do

“Be smart…but don’t pay attention to me.”

Watching Goldman Sachs (GS) executives sweat it out under the hot lamps of Senator questioning makes for gripping television (see Goldman article), but as we all know the ethical standing of a significant number of politicians calls into question whether the pot should be calling the kettle black. Ever since I was a kid, I was told by seemingly responsible adults to “do as I say and not what I do.” I suppose the Goldman execs should follow the advice of Congress, but not their actions.

Based on a recent Wall Street Journal article that studied the investment activity of Congressional members (and spouses) during the financial crisis, the analysis discovered 13 of them were betting against the market. Just as Goldman and hedge fund manager John Paulson partnered to bet against the housing market via shorting synthetic CDOs (Collateralized Debt Obligations), Congressmen and their spouses were wagering against the market through the use of debt loaded (leveraged) exchange traded funds, which integrate derivatives.

Were any of the Congressional investment activities illegal? Likely not, but some question the ethical appearance of such behavior. The former head of the House Ethics Committee and past Representative Joel Hefley of Colorado believes such conduct “doesn’t look real great when the economy is tanking and people are blaming the government.” Facing similar challenges, the SEC’s (Security and Exchange Commission’s) squishy fraud charge complaint against Goldman Sachs is expected to encounter significant difficulty in proving the investment bank’s guilt.

Source: The Wall Street Journal (Yellow Dots = Shorting Exposure Trades)

Other politicians were critical of Wall Street too, despite apparent hypocritical behavior. For example, Representative Shelley Berkley of Nevada chided Wall Street for its reckless activities. “No casino on the planet behaves as irresponsibly and recklessly as Wall Street does. Wall Street ought to be ashamed, and take a lesson from the casino industry.” Nearly at the same time, Shelley’s husband Lawrence Lehrner placed 57 bearish trades.

I find it very amusing the same politicians shredding apart the Wall Street firms are in many cases the same politicians stretching the bounds of ethical behavior. Various politicians do a great job pontificating about the latest shortcomings of the financial industry, but fail to take some accountability for missing one of the greatest real estate booms of all-time. Where were the regulators and politicians when the debt bubble was bursting? Unfortunately, “reactive” is a much larger part of a politician’s lexicon than “proactive.” Responding to populist fervor is easier than leaning against consensus views, even if going against consensus makes more strategic sense.

For those having difficulty in deciphering the advice given by esteemed Congressmen, just remember to “do what they say, and not what they do.”

Read Full Wall Street Journal Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GS, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Filet or Mac & Cheese? Investing for Retirement

The financial crisis of 2008-2009 placed a large swath of investors into paralysis based on a fear the United States and the rest of the world was on the verge of irreversible destruction. Regardless of what the newspaper headlines are reading and television pundits are spouting, individuals have to shrewdly plan for retirement no matter what the economy is doing. So then the question becomes, do you want to be eating macaroni & cheese in retirement, or does filet mignon or alternate five-star cuisine sound more appealing? I vote for the latter.

Despite what the government statistics are saying about the current state of benign inflation, you do not need to be a genius to see medical costs are exploding, energy charges have skyrocketed, and even more innocuous items such as movie ticket prices continue to rise. If that’s not a burden enough, depending on your age, there’s a legitimate concern the Social Security and Medicare safety nets may not be there for you in retirement. It is more important than ever to take control of your financial future by investing your money in a more efficient manner (see Fusion), focusing on long-term, low-cost, tax-efficient strategies. Whatever the direction of the financial markets (up, down, or sideways), if you don’t wisely invest your money, you will run the risk of working as a Wal-Mart (WMT) greeter into your 80s and relegated to eating mac & cheese (for lunch and dinner).

Broaden Your Horizons

The last decade has been tough for domestic equities. It’s true that not a lot of compounding of returns has occurred in the domestic equity markets over the last decade (see Lost Decade), but that weakness is not necessarily representative of the next decade’s performance or the past relative strength seen in areas like emerging markets, materials and certain fixed income markets. These alternatives, including cash, would have added significant diversification benefits to investor portfolios during previous years. Rather than focusing on what’s best for the investor, so much financial industry attention has been placed on high cost, high fee, high commission domestic stock funds or insurance-based products. Due to many inherent conflicts of interest, many individual investors have lost sight of other more attractive opportunities, like exchange traded funds, international strategies, and fixed-income investment vehicles.

Rule of 72

Depending on your risk profile, objectives and constraints, the “Rule of 72” implies your retirement portfolio should double from a $100,000 investment now to roughly $200,000 in seven years (to $400,000 in 14 years, $800,000 in 21 years, etc.), assuming your portfolio can earn a 10% annual return. Unfortunately, this snowballing effect of money growth does not work if you are paying out significant chunks of your returns to aggressive brokers and salespeople in the forms of high commissions, fees, and taxes (see a Penny Saved is Billions Earned). For example, if you are paying out total annual expenses of 2-3% to a broker, advisor, or investment manager, the doubling effect of the Rule of 72 will be stretched out to 9-10 years (rather than the above mentioned seven years). If you do not know what you are paying in fees and expenses (like the majority of people), then do yourself a favor and educate yourself about the fee structures and tax strategies utilized in your investments (see also Investor Confusion). If you haven’t started investing, or you are shoveling out a lot of money in fees, expenses, and taxes, then you should reconsider your current investment stretegy. Otherwise, you may just want to begin stockpiling a lot of macaroni & cheese in your retirement pantry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and shares in WMT, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC “Contact” page for more information.

Simmons Wants to Kiss Life Insurance Worries Away

The Makeup Master

Gene Simmons, lead singer of rock group Kiss, was born as Chaim Witz in Israel 60 years ago. After 40 years of rocking & rolling, the band is still alive and well and touring this spring in the U.K. I am no stranger to Gene Simmons – as a matter of fact, Kiss was the first concert I attended as a kid at the San Francisco Cow Palace in the 1970s. Despite his early professional career success, all the limelight and money was not enough for Gene Simmons, so he put his entrepreneurial skills to the test and aggressively added a broad Kiss merchandising line (over 3,000 licensed/merchandise items), including everything from Kiss baby clothing and Kiss wine to Kiss dart boards and Kiss caskets. Yep, soup to nuts, from the cradle to the grave, and you can even purchase the merchandise with your Kiss Visa credit card!

All Aboard the Premium Financing Train

Now, Mr. Simmons has expanded his business interests to a broader set of financial services. Specifically, Simmons has co-founded a company (Cool Springs Life) that sells premium finance life insurance targeted at high net worth individuals. Simmons and CEO Samuel Watson stopped off at Bloomberg to spread the premium finance gospel:

Premium financing arrangements set up for life insurance are primarily designed for wealthy individuals with large, multi-million dollar estates. This explains a little about whom are the prime targets for life insurance premium financing, but why would wealthy individuals potentially want this financing tool?

Premium Financing Benefits:

- Pay for Estate Taxes: The primary advantage of life insurance for the wealthy is to provide liquidity to beneficiaries (in the form of a death benefit) at the death of the “insured” to fund future estate taxes. Estate tax legislation is still up in the air, but in my view will likely increase to a hefty 45% to 55% rate over the next year. The tax-free liquidity (see a knowledgeable CPA to confirm tax status) provided to the surviving beneficiary by the insurance policy can be especially important if the deceased person’s assets are tied up in illiquid assets like real estate. The government is impatient in regards to tax collections, so gaining immediate access to the death benefit proceeds is a more attractive alternative than forced sales of illiquid assets (potentially at fire-sale prices).

- Other People’s Money: Some people prefer to purchase things with other people’s money. The cost of the financing can be another benefit to the strategy. The interest rate owed on a premium financing deal may be lower than the return a client can earn on alternative investments. If the investment strategy proves successful, the borrower will earn a positive spread on the loan (borrow low, invest high).

- Lower Estate Value: By gifting life insurance assets to a trust (e.g., an Irrevocable Life Insurance Trust – ILIT), there are ways for a wealthy donor to lower his estate value by employing gifting strategies and other estate planning structures. These estate planning tactics often preserve asset values for designated beneficiaries, rather than forking over unnecessarily high taxes to the IRS (Internal Revenue Service). In some cases a knowledgeable attorney can structure premium payments in such a fashion that exemption allowances alleviate any potential gift tax consequence.

Normally nothing in life comes risk-free and the same principle applies to life insurance premium financing.

Premium Financing Risks:

- Interest Rate Risk: Many of these contracts are constructed based on a floating interest rate structure like LIBOR (London Interbank Offered Rate) , therefore if interest rates rise, the borrowers could expose themselves to higher interest payments.

- Credit Risk of Lender: Heaven forbid we go through another financial crisis of the same scale as 2008-2009, but insurance players such as AIG were large players in the premium financing market during this period and caused significant disruption to all relevant participants in the premium financing food chain. Failure of a lender could compromise the integrity of the life insurance and estate planning strategy.

- Risk of Deteriorating Borrower Assets: Depending on the circumstances and facts surrounding the premium financing structure, the lender may require different forms of borrower collateral (i.e., stocks, bonds, real estate, letter of credit, etc.) on top of the cash value/surrender value of the life insurance policy. If the borrower’s collateral value decreases below a certain threshold, the borrower may be forced to supply additional collateral.

For those people who want to rock and roll all night and party every day, perhaps life insurance premium financing is not for you. However, if you got a lot of dough and want to preserve the value of your estate, maybe you should give Gene Simmons a call. With a signed contract, he might even include a Kiss casket for your future funeral plans.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and a derivative security of an AIG insurance subsidiary, but at time of publishing had no direct positions in AIG. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}