Posts tagged ‘yields’

Mission Accomplished?

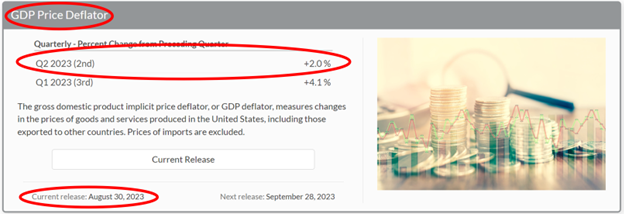

The Federal Reserve has a “dual mandate” designed to “foster economic conditions that achieve both stable prices and maximum sustainable employment.” The “dual mandate” is obviously a moving target, but it appears for now, based on the Fed’s explicit goals, Fed Chairman, Jerome Powell, has accomplished the central bank’s mission. More specifically, inflation, according to the just-reported BEA’s (Bureau of Economic Analysis) GDP Price Deflator statistics, has plummeted dramatically to the Fed’s goal of 2.0% from the sky-high inflation number of 9.1% a year ago (see chart below). Meanwhile, the economy continues to grow (+2.0% GDP growth in the 2nd quarter), and the long-awaited recession boogeyman has yet to appear.

Source: Bureau of Economic Analysis

Rate Pig Moving Through Economic Python

How has inflation plunged so quickly? For starters, in addition to the Fed’s restrictive policy of reducing the balance sheet, since the beginning of last year, the Fed has also effectively slammed the brakes on the economy by taking their target interest rate from 0% to 5.5%. The pace and scale of the interest rate increases have been reduced this year, however it is possible there might be more rate hikes ahead (currently, pundits are betting for no more rate increases this year, although a boost in November is possible if economic data accelerates). Like a pig working its way through the economic python, the large interest rate increases naturally take a while to work their way through the consumer, commercial, and government credit markets.

To put things in better perspective, a study done earlier this year showed the average 30-year monthly mortgage payment for a $500,000 home was higher by more than $800 (up +44%) versus a year ago! But wait, it’s not just consumers feeling the pinch of higher rates. Businesses and governments in all shapes and sizes have felt the pain as well from higher borrowing costs. Post-COVID supply chain constraints and disruptions have eased too, which have helped choke down the high inflation numbers. In the background, let’s not also forget about the disinflationary benefits of ever-expanding technology adoption coupled with the related productivity advantages (see also AI Revolution).

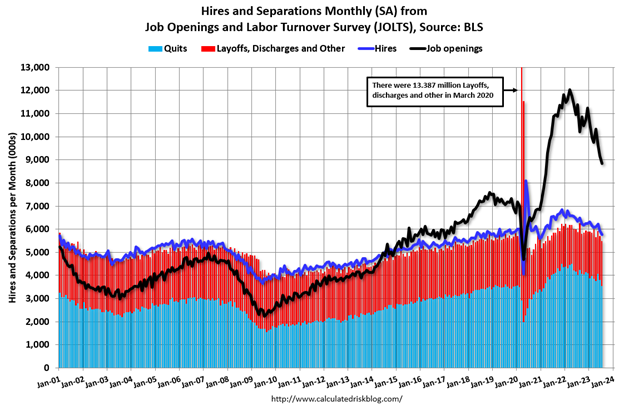

As a result of these dynamics, we are now starting to see cracks appear in our country’s employment foundation as this month’s JOLTs (Job Openings and Labor Turnover – see black line in chart below) and ADP monthly job additions data, which both came in disappointingly low compared to forecasts. Chairman Powell must be ecstatic inflation has plummeted, while the unemployment rate remains near multi-decade lows, and Gross Domestic Product (GDP) growth continues expanding (i.e., no recession in sight).

Source: Calculated Risk and U.S. Bureau of Labor Statistics

Hot Summer, Hot Stocks

Economic activity clearly can and will change, but the stock market has been like the weather this summer…hot. However, after experiencing up-months in six out of the first seven months of 2023, the S&P 500 index decided to take a small breather this month. For August, the S&P slipped -1.8%, but the month was a tale of two cities. By the middle of the month, the index had fallen by roughly -6% on fears of potentially more aggressive interest rate hikes by the Federal Reserve due to better than anticipated economic data. In other words, inflation fears were on the rise and the 10-Year Treasury Note yield temporarily climbed to a 52-week high. By the end of the month, economic data cooled, interest rates dropped a little, and stock prices rebounded smartly by +4.0% to finish the month on a strong note.

For the year, the S&P’s remain strongly positive, up +17.4%. As I have written in the past, the seven largest companies in the S&P 500 index (a.k.a., The Magnificent 7: Apple Inc.; Microsoft Corp.; Alphabet Inc.; Amazon.com, Inc.; NVIDIA Corp.; Tesla, Inc.; and Meta Platforms, Inc.) have contributed to a significant portion of the year’s gains – the average Magnificent 7 stock has skyrocketed an eye-popping +99.0% with NVIDIA being the largest winner, more than tripling in value during the first eight months of the year.

The Federal Reserve can admit they were late to the game in taming out-of-control inflation, but Fed Chair Powell has been swift in moving to preserve his legacy as an inflation fighter. Now that inflation is coming under control and the economy is beginning to cool, Powell needs to make sure he doesn’t murder the economy into recession with overzealous future interest rate increases. Time will tell if the mission has already been accomplished, but so far, the Fed has been delicately balancing an economic soft landing and stock market investors like it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, MSFT, GOOGL, AMZN, NVDA, TSLA, META, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ohhh Omicron! From Panic to Possibility

If you have recovered from your Thanksgiving turkey and stuffing food coma, you have probably woken up to the sound of a new health scare alarm …Omicron. Where does the name Omicron come from, and why is it named after a Greek alphabet letter? The short answer is the system was created to avoid public confusion with complicated scientific names (e.g., B.1.1.529) and also to mitigate the stigma assigned to a region of origination. Apparently, Spaniards weren’t happy with the name “Spanish Flu” and China didn’t appreciate the “Wuhan Virus” moniker. More specifically, Omicron is the new COVID variant originating from South Africa and believed to be more contagious than other forms of COVID, albeit potentially not as severe.

I am not an epidemiologist and also not a COVID expert, but I do know it is a little early to panic over something scientists have not fully researched with fewer than 100 identified cases as of last week. The good news is that early data is showing mild symptoms in infected individuals and the vast majority of these people impacted by Omicron have been unvaccinated (87%), therefore implying the vaccines are indeed providing protection.

Omicron isn’t the first COVID variant and will likely not be the last. Like the flu, which produces new strains every year, new COVID strains such as Omicron are likely to surface on a regular basis. Luckily, our country is home to the world’s most prolific vaccine makers and reformulated boosters are likely to be a common staple in our healthcare regimen. In fact, the CEO of Pfizer, Inc. (PFE) believes it’s possible to have an Omicron vaccine in 100 days, if needed.

Even if Omicron ends up spreading faster than other variants like Alpha, Beta, Gamma, Delta, Lambda, Mu, and Nu, our healthcare system is much better equipped to deal with Omicron compared to previous pandemic variants. Not only do we have access to the strongest supply of vaccines on the planet, but the United States also has built a stronger testing infrastructure (the CDC shows more than 13 million tests conducted over the last week, excluding California). What’s more, pharmaceutical companies have created very effective therapeutics, including Paxlovid, a game-changing antiviral pill manufactured by Pfizer. The recent Paxlovid trial conducted in combination with the antiviral drug ritonavir showed a reduction in hospitalization and deaths by -89%.

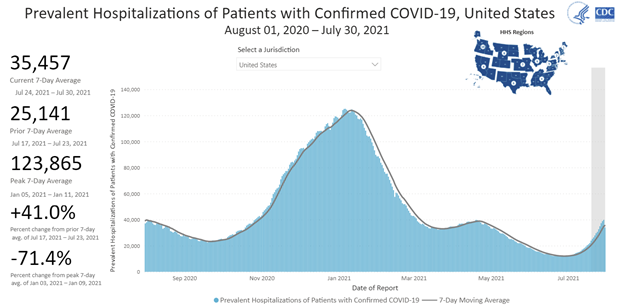

Another fortunate aspect to this new variant is that the rise of Omicron is occurring amidst an improving backdrop of plummeting hospitalizations and COVID-related deaths here in the U.S. (deaths after the recent surge are down more than -50%).

Markets Remain Near Record Highs

With all these scary Omicron headlines, one would expect a collapse in equity markets. Well, at least not yet. The S&P 500 was actually down less than -1% for the month and remains up a whopping +22% for 2021 (see 5-year chart above). And the tech-heavy NASDAQ index did even better, closing slightly higher for the month and up a similar amount for the year (+21%).

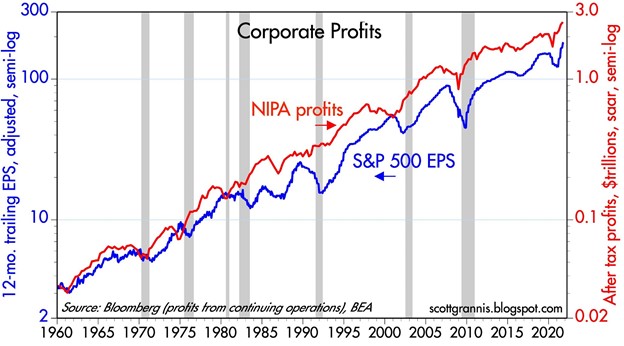

Driving the buoyant stock market performance this year, on the heels of a strong stock market last year (S&P 500 climbed +16%), has been the surge in corporate profits (see chart below). As I like to point out to investors, over the long-run, stock prices follow the direction of earnings, whether we are talking about the overall stock market or individual stocks. Although prices and earnings have both moved up and to the right, neither prices nor profits move in a straight line. One must assume price volatility (i.e. risk) if you want to experience the reward (i.e., long-term returns that substantially beat inflation).

Other Flies in the Ointment

Besides Omicron, there are still some prominent flies in the ointment. Federal Reserve Chairman Jerome Powell just signaled to Congress yesterday that the Fed’s reduction in its bond-buying stimulus program (i.e., “tapering”) could finish a few months early. In other words, the Fed could remove the punch bowl sooner than anticipated – perhaps by as early as this March. Subsequent to the completion of the tapering, industry observers now expect a greater than 50% probability for the first interest hike to occur by June 2022.

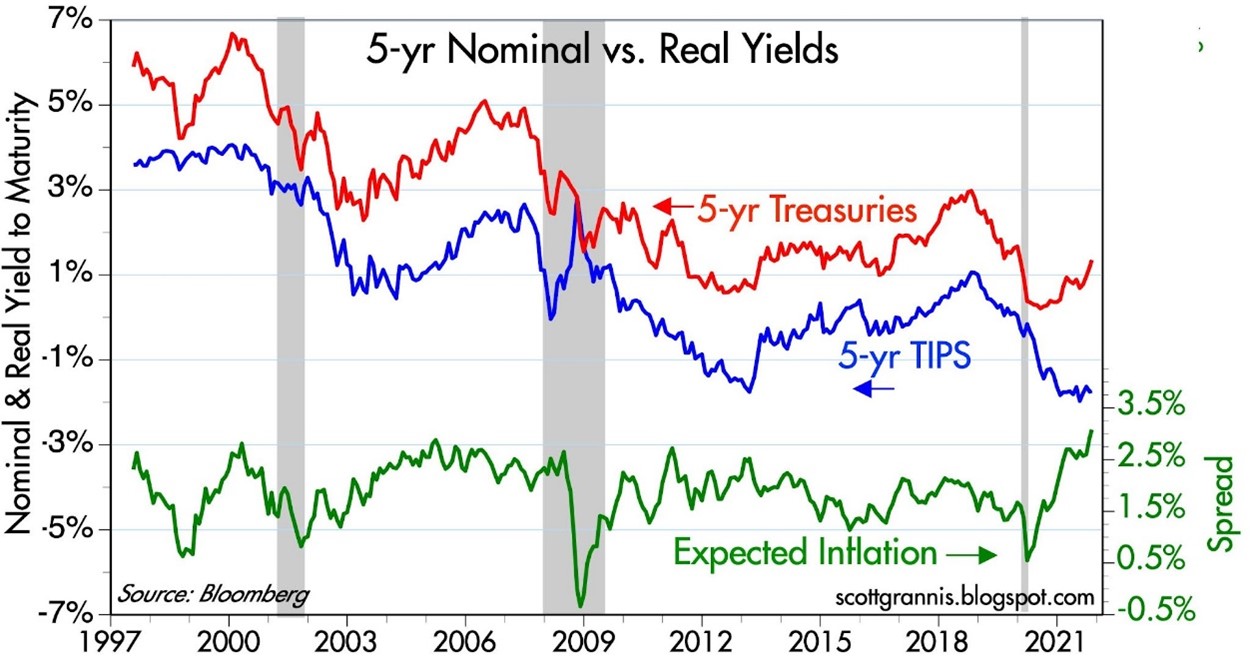

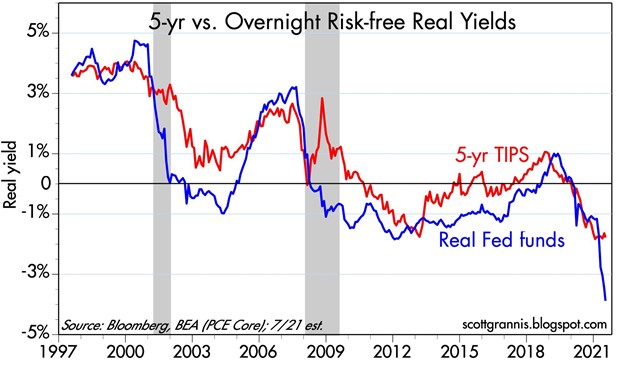

If this is not enough to ruffle your post-Thanksgiving feathers, then consider the threat of persistent inflation. Even Fed Chair Powell threw in the towel by officially removing the word “transitory” from his description of inflation. Inflation is not exploding to the double-digit extremes of the 1980s, but as you can see from the chart below (green line), five-year inflation expectations now exceed 3%.

Lastly, the other date to mark on your December calendar, besides the Christmas holiday, is the 15th because that is the date Congress could hit the debt ceiling limit. This high-stakes game of chicken occurs every year or so. This contest between Democrats and Republicans is used as a negotiating tool in the hopes of advancing political agendas. If an agreement is not reached to increase the debt limit, a government shutdown, and then ultimately a government default would transpire. History tells us this will never happen, but the mere game of political brinksmanship could rattle markets in the short-run.

All these risks and fears are nothing new. Financial markets have flourished in the face of worse crises than Omicron, monetary policy changes, inflation, and debt ceilings. The key to sustainable wealth creation is taking a long-term view and being opportunistic in the face of volatility. Shrewdly pivoting your perspective from panic to possibility is essential on the path to prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sleeping on Expensive Financial Pillows

Everybody loves a good night’s sleep and that requires a comfortable pillow. Unfortunately, many investors are overpaying for their pillows in the form of overpriced, interest-rate sensitive bonds. If you aren’t careful, your retirement dreams could turn into financial nightmares. More specifically, if the composition of your investment portfolio is overly skewed towards bonds, you stand to lose substantial amounts of money if/when interest rates and inflation persistently increase.

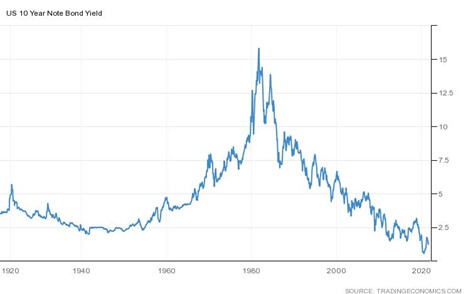

In the short-run, pillows manufactured in the form of bonds can feel cozy in a world of low volatility and generationally-low interest rates. However, investors should also ask themselves, how much longer can this unprecedented 40-year bull market in bonds last? Interest rates approached 20% in 1980 and they stand closer to 1% today (1.24% to be more precise). What may now seem like a cozy bond portfolio may eventually lead to unnerving insomnia.

We already have negative interest rates in numerous countries around the world and inflation (a rise in general price levels) is running hot at about 5% annually. What this means is investing in a 10-Year Treasury Note yielding 1.24% effectively means you are losing almost -4% per year in purchasing power, if inflation remains at 5% (see chart below). There are numerous investing strategies used to fight inflation, but historically stocks’ ability to raise prices through pricing power has been a useful vehicle to fend off the melting of money’s value.

Despite short-term increases in inflation, getting a good night sleep hasn’t been an issue in 2021 as it relates to the stock market. For the month, the S&P 500 stock index was up +2.3% to a new record, and for the year it has surged +17%. The story for the Dow Jones Industrial Average looks similar – for the month rising +1.3% and year-to-date to +14%.

Thankfully, there haven’t been any night terrors yet either in the bond market. Nevertheless, short-term results have been more of a mixed bag. For the month, the iShares Aggregate Bond Market ETF (Exchange Traded Fund – AGG) rose +1.0% and for 2021 slipped -2%.

In spite of stocks being a great place to invest over the last decade or so, solely investing in stocks is not always rainbows and unicorns. The price you pay for longer-term stock outperformance is shorter-term volatility, which can be disruptive to your sleeping patterns. Case in point, the -35% drop in the S&P 500 index at the start of the COVID-19 global pandemic when anxiety and volatility were at extreme levels.

Despite the market continuously hitting new highs, investors are not completely out of the woods yet as spiking Delta variant cases threaten the trajectory of the current economic recovery.

Although stocks can feel like stiff, uncomfortable pillows in the short-term, in the long-run, historically those stiff, uncomfortable stocks become vastly more comfortable than bonds. Over the last five years, stock prices have dramatically outperformed bonds by +99% (S&P vs. AGG).

Determining your asset allocation is a monumental decision that should be driven by various factors, including risk tolerance, time horizon, income needs, taxes, and other factors such as your personal objectives. Therefore, even if you subscribe to the premise that stocks outperform in the long run, that doesn’t necessarily mean all retirees should load up solely on a diet of stocks.

Retirees who need income or other risk-averse investors generally can’t afford to lose substantial amounts of their net worth, if stocks tank significantly during a recession. Not only could an all-stock portfolio not generate adequate income, an equity-heavy portfolio could also could lead to emotional sales after market declines, thereby locking in permanent losses at low levels. After these potential losses, there may not be enough time for stock losses to be recouped by retirees. If possible, most investors approaching retirement do not want to be forced to work as a greeter at Wal-Mart to compensate for stock losses.

Everybody’s financial situation is different, and everyone has varying risk tolerances and unique needs. As such, working with an independent, experienced, and professional advisor like Sidoxia Capital Management (www.Sidoxia.com) can assist you with structuring a proper asset allocation, so your investment pillows can help you achieve a good night sleep.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Glass Half Empty Becomes Record Glass Half Full

Oh my! What a difference a few months makes. Originally, what looked like an economic glass half empty in December has turned into a new record glass half full. What looked like Armageddon in December has turned into a v-shaped bed of roses to new all-time record stock market highs for the S&P 500 index (see chart below). For the recent month, the S&P 500 climbed another +3.9% to 2,945, bringing total 2019 gains to an impressive +17.5% advance. Before you get too excited, it’s worth noting stocks were down in value during 2018. When you combine 2018-2019, appreciation over the last 16 months equates to a more modest +10.2% expansion. Worth noting, since the end of 2017, profits have climbed by more than +20%, which means stocks are cheaper today as measured by Price-Earnings ratios (P/E) than two years ago (despite the historic, record levels). For any confused investors, we can revisit this topic for discussion in a future writing.

Source: Trading Economics

From Famine to Feast

As I noted in my “December to Remember” article, there were no shortage of concerns ranging from impeachment to Brexit. How do those concerns look now? Let’s take a look:

Government Shutdown: The longest government shutdown in history (35 days) ended on January 25, 2019 with minimal broad-based economic damage.

Global Trade (China): Rhetoric coming from President Trump and his administration regarding a trade deal resolution with China has been rather optimistic. In fact, a CNBC survey shows 77% of respondents believe that the U.S. and China will complete a trade deal.

Federal Reserve Interest Rate Policy: After consistently increasing interest rates nine times since the end of 2015 until late 2018, Federal Reserve Chairman Jerome Powell signaled he was effectively taking monetary policy off rate-hiking “autopilot” and would in turn become “patient” as it relates to increasing future interest rates. Interestingly, traders are now forecasting a 70% chance of a rate cut before January 29, 2020.

Mueller Investigation: Special counsel Robert Mueller released his widely anticipated report that investigated Russian collusion and obstruction allegations by the president and his administration. In Mueller’s 22-month report he could “not establish that members of the Trump Campaign conspired or coordinated with the Russian government in its election interference activities.” As it relates to obstruction, Mueller effectively stated the president attempted to obstruct justice but was not successful in achieving that goal. Regardless of your political views, uncertainty surrounding this issue has been mitigated.

New Balance of Power in Congress: Democrats took Congressional control of the House of Representatives and reintroduced gridlock. But followers of mine understand gridlock is not necessarily a bad thing.

Brexit Deal Uncertainty: After years of negotiations for Britain to exit the European Union (EU), the impending Brexit deadline of March 29th came and went. EU an UK leaders have now agreed to extend the deadline to October 31st, thereby delaying any potential negative impact from a hard UK exit from the EU.

Recession Fears: Fears of a fourth quarter global slowdown that would bleed to a recession on U.S. soil appear to have been laid to bed. The recently reported first quarter economic growth (Gross Domestic Product – GDP) figures came in at a healthy+3.2% annualized growth rate, up from fourth quarter growth of +2.2%, and above consensus forecasts of 2.0%.

Curve Concern

The other debate swirling around the investment community this month was the terrifying but wonky “inverted yield curve.” What is an inverted yield curve? This is a financial phenomenon, when interest rate yields on long-term bonds are lower than interest rate yields on short-term bonds. Essentially when these dynamics are in place, bond investors are predicting slower economic activity in the future (i.e., recession). The lower future rates effectively act as a way to stimulate prospective growth amid expected weak economic activity. Furthermore, lower future rates are a symptom of stronger demand for longer-term bonds. It’s counterintuitive for some, but higher long-term bond prices result in lower long-term bond interest rate yields. If this doesn’t make sense, please read this. Why is all this inverted yield curve stuff important? From World War II, history has informed us that whenever this phenomenon has occurred, it has been a great predictor for a looming recession.

As you can see from the chart below, whenever the yield curve (red line) inverts (goes below zero), you can see that a recession (gray vertical bar) occurs shortly thereafter. In other words, an inverted yield curve historically has been a great way to predict recessions, which normally is almost an impossible endeavor – even for economists, strategists, and investment professionals.

Source: Calafia Beach Pundit

Although the curve inverted recently (red line below 0), you can see from the chart, historically recessions (gray vertical bars) have occurred only when inflation-adjusted interest rates (blue line) have climbed above 2%. Well, the data clearly shows inflation-adjusted interest rates are still well below 1%, therefore an impending recession may not occur too soon. Time will tell if these historical relationships will hold, but rest assured this is a dynamic I will be following closely.

It has been a crazy 6-9 months in the stock market with price swings moving 20% in both directions (+/-), but it has become increasingly clear that a multitude of 2018 fears causing the glass to appear half empty have now abated. So long as economic growth continues at a healthy clip, corporate profits expand to (remain at) record levels, and the previously mentioned concerns don’t spiral out of control, then investors can credibly justify these record levels…as they peer into a glass half full.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}