Posts tagged ‘U.S. Debt’

More Treats, Less Tricks

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 2, 2015). Subscribe on the right side of the page for the complete text.

Have you finished licking the last of your Halloween chocolate-covered fingers and scheduled your next cavity-filled dental appointment? After a few challenging months, the normally spooky month of October produced an abundance of sweet treats rather than scary tricks for stock market investors. In fact, the S&P 500 index finished the month with a whopping +8.3% burst, making October the tastiest performing month since late 2010. This came in stark contrast to the indigestion experienced with the -8.7% decline over the previous two months.

What’s behind all these sweet gains? For starters, fears of a Chinese economic sugar-high ending in a crash have abated for now. With that said, “Little Red Riding Hood” is not out of the woods quite yet. Like a surprising goblin or ghost popping out to scare you at a Halloween haunted house, China could still rear its ugly head in the future due to its prominent stature as the second largest global economy. We have been forced to deal with similar on-again-off-again concerns associated with Greece.

The good news is the Chinese government and central bank are not sitting on their hands. In addition to interest rate cuts and corruption crackdowns, Chinese government officials have even recently halted its decades-long one-child policy. China’s new two-child policy is designed to spur flagging economic growth and also reverse the country’s aging demographic profile.

Also contributing to the stock market’s sugary October advances is an increasing comfort level with the Federal Reserve’s eventual interest rate increase. Just last week, the central bank released the statement from its October Federal Open Market Committee meetings stating it will determine whether it will be “appropriate” to increase interest rates at its next meetings, which take place on December 15th and 16th. Interest rate financial markets are now baking in a roughly 50% probability of a Fed interest rate hike next month. Initially, the October Fed statement was perceived negatively by investors due to fears that higher rates could potentially choke off economic growth. Within a 30 minute period after the announcement, stock prices reversed course and surged higher. Investors interpreted the Fed signal of a possible interest rate hike as an upbeat display of confidence in a strengthening economy.

As I have reiterated on numerous occasions (see also Fed Fatigue), a +0.25% increase in the Federal Funds rate from essentially a level of 0% is almost irrelevant in my eyes – just like adjusting the Jacuzzi temperature from 102 degrees down to 101 degrees is hardly noticeable. More practically speaking, an increase from 14.00% to 14.25% on a credit card interest rate will not deter consumers from spending, just like a 3.90% mortgage rising to 4.15% will not break the bank for homebuyers. On the other hand, if interest rates were to spike materially higher by 3.00% – 4.00% over a very short period of time, this move would have a much more disruptive impact, and would be cause for concern. Fortunately for equity investors, this scenario is rather unlikely in the short-run due to virtually no sign of inflation at either the consumer or worker level. Actually, if you read the Fed’s most recent statement, Fed Chairwoman Janet Yellen indicated the central bank intends to maintain interest rates below “normal” levels for “some time” even if the economy keeps chugging along at a healthy clip.

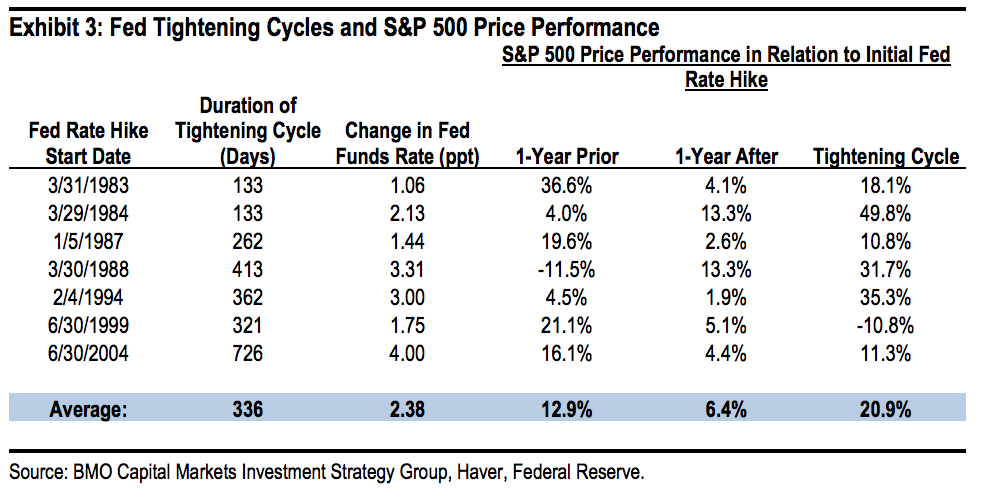

If you think my interest rate perspective is the equivalent of me whistling past the graveyard, history proves to be a pretty good guide of what normally happens after the Fed increases interest rates. Bolstering my argument is data observed over the last seven Federal Reserve interest rate hike cycles from 1983 – 2006 (see table below). As the statistics show, stock prices increased an impressive +20.9% on average over Fed interest rate “Tightening Cycles.” It is entirely conceivable that the announcement of a December interest rate hike could increase short-term volatility. We saw this rate hike fear phenomenon a few months ago, and also a few years ago in 2013 (see also Will Rising Rates Murder Market?) when Federal Reserve Chairman Ben Bernanke threatened an end to quantitative easing (a.k.a., “Taper Tantrum”), but eventually people figured out the world was not going to end and stock prices ultimately moved higher.

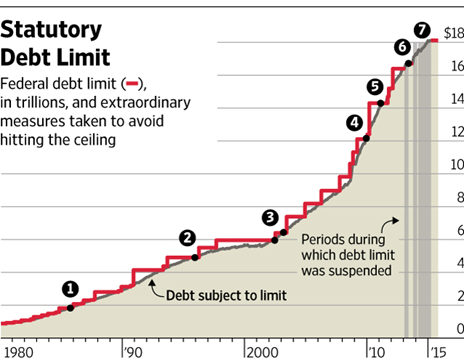

Besides increased comfort with Fed interest rate policies, another positive contributing factor to the financial market rebound was the latest Congressional approval of a two-year budget deal that prevents the government from defaulting on its debt. Not only does the deal suspend the $18.1 trillion debt limit through March 2017 (see chart below), but the legislation also lowers the chance of a government shutdown in December. Rather than creating a contentious battle for the fresh, incoming Speaker of the House (Paul Ryan), the approved budget deal will allow the new Speaker to start with a clean slate with which he can use to negotiate across a spectrum of political issues.

Source: Wall Street Journal

Remain Calm – Not Frightened

Humans, including all investors, are emotional beings, but the best investors separate fear from greed and are masters at making unemotional, objective decisions. Just as everything wasn’t a scary disaster when stocks declined during August and September, so too, the subsequent rise in October doesn’t mean everything is a bed of roses.

Every three months, thousands of companies share their financial report cards with investors, and so far with more than 65% of the S&P 500 companies reporting their results this period, corporate America is not making the honor roll. Collapsing commodity prices, including oil, along with the rapid appreciation in the value of the U.S. dollar (i.e., causing declines in relatively expensive U.S. exports), third quarter profit growth has declined -1%. If you exclude the energy sector from the equation, corporations are still not making the “Dean’s List,” however the report cards look a lot more respectable through this lens with profits rising +6% during the third quarter. A sluggish third quarter GDP (Gross Domestic Product) growth report of +1.5% is further evidence the economy has plenty of room to improve the country’s financial GPA.

Historically speaking, October has been a scary period, if you consider the 1929 and 1987 stock market crashes occurred during this Halloween month. Now that investors have survived this frightening period, we will see if the “Santa Claus Rally” will arrive early this season. Stock market treats have been sweet in recent weeks, but investors cannot lose sight of the long-term. With interest rates near generational lows, investors need to make sure they are efficiently investing their investment funds in a low-cost, tax-efficient, diversified manner, subject to personal time horizons and risk tolerances. Over the long-run, meeting these objectives will create a lot more treats than tricks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Foreign Frights & Debt Doubts

Excerpts from Sidoxia monthly newsletter (Subscribe on right side of page)

Over the last few years the globalized nature of the financial crisis has forced a diverse set of world leaders to deal with obscure international flare-ups in countries ranging from Iceland to Dubai, and Greece to Tunisia. The crisis du jour is the popular revolt in Egypt against 30-year president Hosni Mubarak and his autocratic, authoritarian government. The situation for the U.S. becomes a little sticky because Egypt, although creating a GDP (Gross Domestic Product) of less than the state of Illinois, is still the largest Arab country by population (approximately 82 million – even larger than Iran); a staunch ally with the U.S. in keeping peace with Israel; has contributed important intelligence to our country’s war on terror; and has been a responsible partner in controlling commerce through the all-important Suez Canal. The problem with Egypt and Mubarak’s regime is that the Egyptian economy is in relative shambles (they do not have oil reserves like their neighbors), unemployment is through the roof, and the government has been slow to push democratic advancements forward for the Egyptian people.

As emerging market “haves” increasingly join the ranks of the middle class, the people representing the “have-nots” of Yemen, Jordan, Algeria, Tunisia, Egypt, and others are thirsting for a cocktail of democracy and a higher standard of living, like some of their wealthier neighbors. These autocratic, authoritarian regimes can do their best to slow or delay the democratizations of their countries, but they cannot put the genie back in the bottle. Information is flowing faster than ever, and societies previously kept in the dark are now seeing the light of democracy.

Like any volatile government situation, there are threats and opportunities, depending on whether Mubarak stays in power, and if not, the nature of the new leadership. If an extremist government fills the leadership void, the U.S. may wish to rewind the clock and put the slow-moving reformist, Mubarak, back in power.

The short-term impact of the popular revolt may create additional volatility in the markets, but in the long-run, if the turmoil introduces more open, transparent, less corrupt, and democratic ideals to the new agenda, then the world will become a better place.

Bitter Debt Pill Tough to Swallow

There is never a shortage of issues to worry about, and from an economic standpoint, the suffocating amount of debt our country is dealing with is at the top of the concern list. The 2008-2009 financial crisis hole that we are still climbing our way out of is a friendly reminder of what happens to countries adopting irresponsible fiscal policies. The choking amount of debt the U.S. is swallowing remains a central issue for the current administration and will be a core topic to be debated through the 2012 Presidential election cycle.

How serious is the issue? The problem is serious enough the Congressional Budget Office (CBO) just raised its budget deficit forecast for fiscal 2011 to hit a record $1.5 trillion (9.8% of GDP), a level higher than $1.3 trillion in fiscal 2010. The blame for the new record can be largely attributed to the recent extension of the $858 billion in Bush tax-cuts and other benefits/breaks. Kicking the can down the road recently led Moody’s Investors Services of threatening the U.S. with a downgrade of its triple-A rated debt.

Source: The Peterson Institute

The President addressed some of our fiscal problems in his State of the Union Address recently (e.g., proposing a freeze on discretionary spending), but the rubber really hits the road when he comes out with his budget proposal later this month. How serious is he about reducing our hemorrhaging deficits? We’ll soon find out when the individual budget line-items are distributed for everyone to see. Shortly thereafter, around the end of March, the debt ceiling impasse will become a game of political “chicken.” Each side, Democrats and Republicans, will attempt to withdraw concessions from the other party, in exchange for a vote that will prevent a disastrous default of our government’s debt payments. Basically, our government is effectively looking to expand its credit card credit line, because our government credit limit is maxed out.

The situation isn’t hopeless if our politicians can show leadership by making difficult, unpopular fiscal decisions, but if America ignores our painful debt problems and does not take its bitter medicine, then prepare for an economy on the verge of keeling over.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}