Posts tagged ‘trade war’

Tariffs & Free Trade by Wade

Tariffs and trade have dominated the media headlines since the beginning of the year, creating a volatile rollercoaster ride in the financial markets and broader economy. What were screams of fear just last month turned into cheers of optimism after a trade deal between the U.S. and the U.K. was announced earlier this month.

This agreement—combined with hopes for future trade deals and the absence of runaway inflation or economic collapse—sparked a rally in stock prices. The minimum 10% baseline tariff in the U.K. agreement has fueled optimism that a simplified framework might extend to other international trade pacts. For the month, the S&P 500 surged by +6.2%, the Dow Jones Industrial Average climbed +3.9%, and the tech-heavy NASDAQ soared by +9.6%.

However, tariffs and trade haven’t faded into the background. In fact, just this week, a federal court ruled that the president’s tariff policies were illegal, citing misuse of emergency powers under the International Emergency Economic Powers Act (IEEPA) of 1977. Subsequently, the same court has granted the Trump administration a reprieve pending appeal—potentially escalating the issue to the Supreme Court. Even if the ruling stands, the president has alternative avenues to impose tariffs through other legal mechanisms.

So, what is all this fuss over tariffs and trade really about? I’ve previously written extensively on the topic (“Tariff Sheriff”), but some fundamental economic concepts still get lost in the tariff chaos noise.

It’s true that many countries engage in unfair trade practices against the U.S.—including subsidies, currency manipulation, non-tariff barriers, dumping, quotas, complex permitting, and value-added taxes (VAT). However, the powerful benefits of free trade are often underappreciated or poorly explained by the pundits.

Tariffs and Free Trade 101: China & France Experiment

To illustrate, let’s reference an example drawn from an op-ed by Princeton economist Burton Malkiel, author of the legendary finance book A Random Walk Down Wall Street.

Every country enjoys a comparative advantage in producing certain goods. For example, China historically benefits from low labor costs, making it a global manufacturing hub. Meanwhile, the U.S. leads in technological innovation, and countries like Brazil leverage vast land resources to dominate agricultural exports—such as being the world’s top coffee exporter. Let’s consider a simplified example using two countries: China and France, each with 100 labor hours available, and only able to produce T-shirts and wine.

China’s Output (see graphic above) – China’s comparative advantage in making more T-shirts than bottles of wine results in the following:

- 50 hours = 50 T-shirts

- 50 hours = 10 bottles of wine

France’s Output (see graphic above) – France’s comparative advantage in making more bottles of wine than T-shirts results in the following:

- 50 hours = 50 bottles of wine

- 50 hours = 20 T-shirts

Combined Total (China + France): 70 T-shirts + 60 bottles of wine = 130 total units of goods.

Example #2: Production Plan #2 (Each country specializes in their comparative advantage)

China’s Output (T-shirt specialization):

- 100 hours = 100 T-shirts

France’s Output (Wine specialization):

- 100 hours = 100 bottles of wine

Combined Total: 100 T-shirts + 100 bottles of wine = 200 total units of goods.

But here’s the challenge: the Chinese still want wine, and the French still want T-shirts. That’s where free trade comes in – see next example (graphic below).

Example #3: Production Plan #2 + Free Trade

Through free trade, each country can specialize in what they do best and then trade for other goods wanted or needed. If China trades 50 T-shirts for 50 bottles of wine with France, both countries end up with:

- China: 50 T-shirts + 50 bottles of wine

- France: 50 bottles of wine + 50 T-shirts

This plan produces 54% more total goods than the original production plan (200 vs. 130 – Example #1), with no increase in labor hours. China gets 300% more wine, and France gets 150% more T-shirts—a clear win-win.

Today’s Tariff Reality

In 2024, the U.S. trade deficit stood at $918 billion. President Trump’s aggressive tariff strategy aims to reduce this gap by incentivizing domestic manufacturing, increasing exports, and reducing imports. The challenge is that tariffs also raise prices for consumers and disrupt the benefits of free trade.

If the administration succeeds in establishing fairer rules for a level trading field, increasing government revenue, and narrowing the trade deficit, then history will likely view President Trump’s tariff policy favorably. But if tariffs lead to higher prices, inflation, and a weaker economy, the tariff policy may be judged as a costly misstep. The stock market, voters, and time will ultimately serve as the principal judges.

Looking ahead, two key dates are on the calendar:

- July 9 marks the end of the 90-day reciprocal tariff pause. Without new trade agreements, tariffs will spike on imports from many countries — raising costs for consumers.

- July 4 is not only Independence Day, but also the target date for Senate Republicans to pass the “One Big Beautiful Bill”, which packages several of President Trump’s top priorities: tax cuts, welfare reform, energy expansion, and border security. While the bill could stimulate growth, critics warn of its potential to balloon the national deficit.

Most Americans support the idea of fairer global trade. The question is whether aggressive tariffs across the globe are the right tool to achieve that goal — and whether trading partners will agree to new deals. Regardless of the outcome, this crash course in Tariffs & Free Trade 101 underscores the enduring value of specialization and free trade, even amid today’s turbulent tariff battles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 2, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

New Year, New AI Era & New Tariff Sheriff

The first month of 2025 started with a bang when newly-inaugurated President Donald Trump announced a groundbreaking AI (artificial intelligence) program led by business titan thought leaders called Stargate, which promises to spend a half trillion dollars on AI data center infrastructure projects and create hundreds of thousands of jobs. Just one week later, a wet blanket was placed on the Stargate euphoria when a Chinese AI upstart announced a technological breakthrough. Stocks moved lower on the last day of the month when Trump added insult to injury by confirming 25% Mexican/Canadian tariffs and 10% additional Chinese tariffs would be implemented immediately.

Regardless, positive economic and corporate data coupled with other pro-business fiscal policies (e.g., deregulation and lower proposed taxes) allowed the financial markets to finish the month with respectable gains. More specifically, the S&P 500 surged higher by +2.7%; the NASDAQ +1.6%; and the Dow Jones Industrial Average +4.7%.

DeepSeek = Deep AI Trouble?

Ever since OpenAI launched its ChatGPT language model (LLM) at the end of 2022, the global AI gold rush began. Just as the United States appeared to be dominating the AI race to global superiority, a bombshell was recently released, when a new Chinese AI upstart, DeepSeek, released a white paper claiming the company’s R1 large language model (LLM) rivaled competitors’ LLMs like OpenAI’s ChatGPT, Meta’s Llama (META), Anthropic’s Claude, and Alibaba’s Qwen (BABA) for a small fraction of the price spent by DeepSeek’s American rivals. The “DeepSeek Freak” caused a chain reaction of selling across a wide swath of companies (including NVIDIA Corp – NVDA) that have benefitted from hundreds of billions in AI infrastructure spending. The fear that Chinese AI competition may leapfrog U.S. companies, and potentially dramatically reduce AI-related capital expenditures caused the NASDAQ to almost fall -2% last week, and AI juggernaut NVIDIA shed more than a half trillion dollars in the company’s market value in a single day. Overall, U.S. stocks lost more than a trillion dollars in value on the day of the DeepSeek Freak unveiling.

Although investors were initially panicked by the DeepSeek revelations, not all of the Chinese claims have been substantiated. In fact, a just-released report by SemiAnalysis, a semiconductor research and consulting firm, states that DeepSeek’s costs for its R1 LLM likely exceed $500 million, much higher than the $6 million training costs stated in DeepSeek’s initial pronouncement.

Source: NBC News

New Tariff Sheriff in Town

While many investors were hoping for a delay in the implementation of President Trump’s tariffs on Mexico, Canada, and China, Trump decided to move full steam ahead with a February 1st start date. In 2023, Mexico was the U.S.’s largest trade partner and Canada was the second largest. These Mexican and Canadian tariffs are very broad based and impact many different industries, including autos, agricultural products, and crude oil. You can see the extent of the impact in the graphic below graphic below.

Source: VisualCapitalist.com

But what does this mean for the economy? In short, it will mean higher prices for U.S. consumers and businesses. The Tax Foundation, an 85-year-old, non-partisan, tax policy non-profit attempted to quantify some of the potential impacts from the proposed tariffs. The bottom-line findings from the Tax Foundation were that tariffs would “shrink economic output by -0.4% and increase taxes by $1.2 trillion between 2025 and 2034 on a conventional basis, amounting to an average tax increase of more than $830 per US household in 2025.” Please, also see table below (Scenario 2).

Source: Tax Foundation

In addition to American consumers having to pay higher taxes and prices for tariffed import products, there will be an estimated -344,000 jobs lost and there could be unintended consequences from retaliatory tariffs imposed on U.S. exports (i.e., our goods shipped internationally will be priced uncompetitively). In fact, Canada and Mexico just jointly announced tit-for-tat tariffs on U.S. goods and services, which will hurt these U.S. sales abroad.

With all of that said, the bark of the 25% tariffs on Mexico and Canada, along with the 10% in additional tariffs on China could be worse than the actual bite. Especially, if Trump uses these tariffs successfully as a negotiating tool and provides foreign countries with significant exemptions.

It’s also important to keep the size of these tariffs in context. Imports of foreign good and services only represented 13.9% of the Unted States’ Gross Domestic Product in 2023. Of that small percentage of imports, Mexico, Canada, and China only represent a fraction of that. It’s true that imports subtract from our country’s economic activity, but even if tariffs on foreign goods lead to the consumption of more American manufactured products, those benefits will be somewhat offset by higher inflated prices that will pinch consumer wallets. The new year marks an exciting new era of AI and global trade, but with that comes many new threats and opportunities. Throughout our 17-year history at Sidoxia Capital Management, we have successfully navigated these pivot points, and we are excited about effectively managing through this current transitional period.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 3, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in META, NVDA, certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BABA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Investors Give Thanks and Feast on New Record

There were many things to be grateful over the Thanksgiving holiday, including personal finances for many. Stock market investors were especially thankful for the new record highs achieved in the S&P 500 index, which rose a heaping +3.4% last month, bringing 2019 stock market gains to a whopping +25.3%. Any concerns over politics, China trade, global monetary policy, Brexit negotiations, slowing economic growth, and other fears have been overshadowed by record corporate profits, generationally low interest rates, historically low unemployment rates, rising wages, strong consumer confidence, and hopes of an economic recovery abroad.

Despite the strong advances, concerns remain over a bubble or a stratospheric stock market. These worries of inflated gains seem overblown, if you consider stocks were down -6.2% in 2018. In other words, if you combine 2018-2019, so far, the two-year period averages an +8.4% annualized return – a more reasonable advance. One thing is for sure, this bull market, which started in early-2009, has been no turkey. Since the S&P 500 bottomed at 666 in March of 2009, the index finished the month at over 3,140 – almost a quintuple in value over a 10-year period (not too shabby).

I get the question a lot, “Wade, don’t you think the stock market is crazy now and it is going to crash soon? It’s gone up so much and is at a record high.” Just because the stock market hits a record level doesn’t mean it will stop going up. In fact, since 2013, the S&P 500 has hit 38 new, monthly record highs (see chart below). For each of these new records, I have listened to anxious investors brace themselves for another crash resembling the 2008 financial collapse. The only problem is the 100-year flood normally doesn’t come every 10 years, and as history often proves, record highs often beget future new record highs.

Be Careful to Whom You Listen

There are always varying opinions about the level and direction of future stock prices, but I always warn investors to be careful about following the judgments of television talking heads, especially when it comes to economists, strategists, and analysts, all of whom typically have very little experience in actually investing. These prognosticators typically are very articulate and persuasive but have little-to-no experience of really managing money. Traders generally fall into the useless camp as well because their opinions are moving at the speed of light based on the everchanging headlines du jour, thereby making this fickle advice worthless and ineffective. Instead, investors should pay attention to successful long-term investors who have proven the ability to make and preserve wealth through years of up-and-down markets. You don’t have to believe me, but when the most successful investor of all-time, Warren Buffett, says the stock market is “ridiculously cheap,” it probably makes sense to pay more attention to his words of wisdom versus the latest political headline or dangerous and speculative day trader advice to buy-buy-buy or sell-sell-sell!

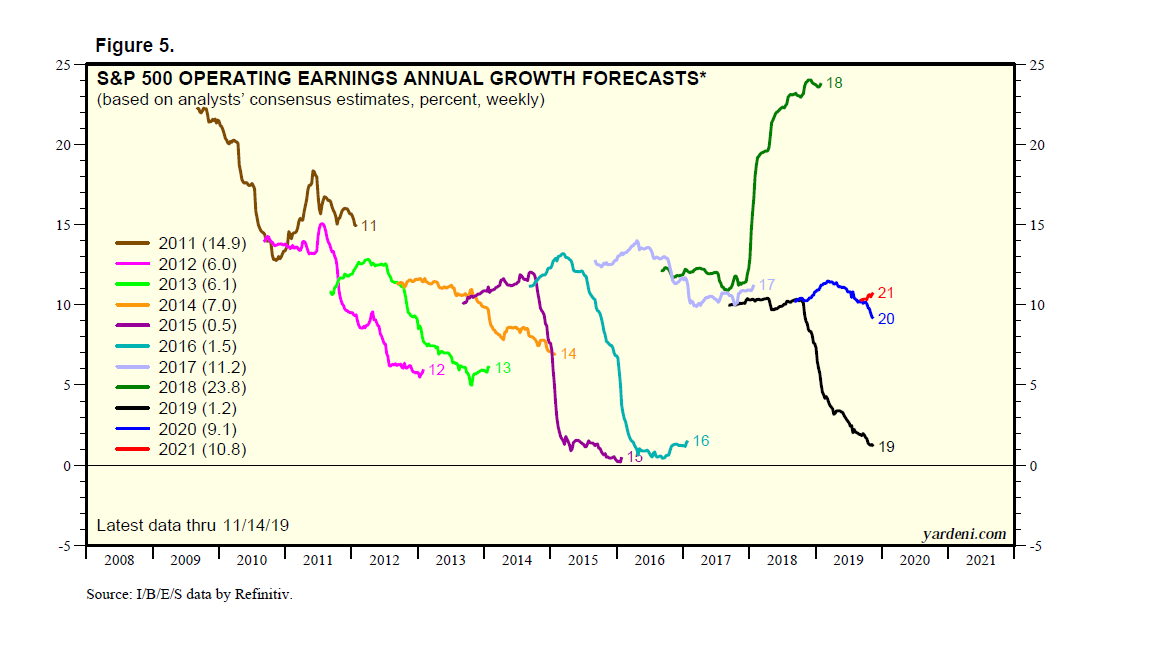

Although Warren Buffett freely provides his opinions, he openly admits he has no idea what direction stock prices will do in the short-run. So, if the greatest investor of all-time cannot predict short-term direction of stocks, then maybe you shouldn’t try to predict either? Case in point, corporate profits were up over 20% in 2018 (see chart below) and stock prices went down, while this year corporate profits have been essentially flat and stock prices have catapulted approximately +25%. This goes to show you that short-term stock movements can be incredibly difficult to predict. You will be much better off by focusing on making sound investments and following a suitable strategy based on your unique objectives and constraints.

Source: Dr. Ed’s Blog

You may have gotten some heartburn by feasting on too much turkey, mashed potatoes, stuffing, and gravy, however investors are feasting on new record stock market highs despite investor anxiety. When the anxiety eventually turns to euphoria and gluttony, from fear and skepticism, then that will be the time to reach for the Tums antacid.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 2, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chinese Checkers or Chess?

There’s been a high stakes economic game of trade going on between the United States and China, but it’s unclear what actual game is being played or what the rules are? Is it Chinese checkers, chess, or some other game?

Currently, the rules of the U.S.-China trade war game are continually changing. Most recently, the U.S. has implemented 15% in added tariffs (on approximately $125 billion in Chinese consumer imports) on September 1st. The president and his administration appreciate the significance of trade negotiations, especially as it relates to his second term reelection campaign, which is beginning to swing into full gear. However, game enthusiasts also understand you can’t win or truly play a game, if you don’t know the rules? In that same vein, investors have been confused about the U.S.-China trade game as the president’s Twitter account has been blowing up with tariff threats and trade discussion updates. As a negotiating tactic, the current unpredictable trade talks spearheaded by the Trump administration have been keeping investors guessing whether there will be a successful deal payoff. Until then, market participants have been sitting on the sidelines watching the stock market volatility unfold, one tweet at a time.

Here’s what the president has planned for other tariffs:

- October 1: Tariffs on $250 billion in Chinese goods rise to 30%.

- November 17: Europe auto tariff deadline.

- December 15: 15% tariffs on $160 billion in Chinese goods.

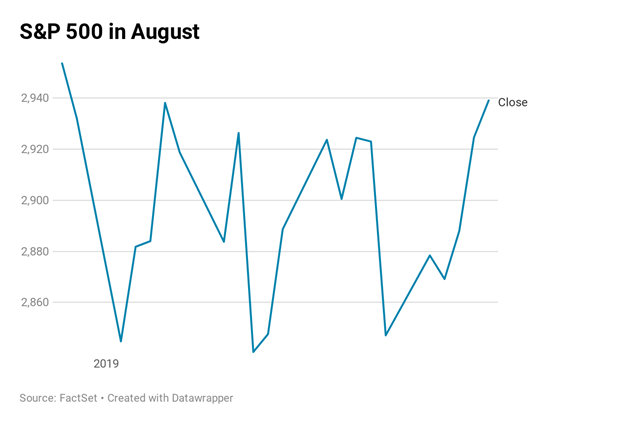

This uncertain game translated into all the major stock market averages vacillating to an eventual decline last month, with a price chart resembling a cardiogram. More specifically, after bouncing around wildly, the S&P 500 decreased -1.8% last month (see chart below), the Dow Jones Industrial Average dropped -1.7%, and the tech-heavy Nasdaq fell -2.6%.

Politically, there is bipartisan support to establish new trade rules and there is acknowledgement that China has been cheating and breaking trade rules for decades. The consensus among most constituencies is especially clear as it relates to Chinese theft of our intellectual property, forced technology transfer, and barriers for U.S. companies to invest in China.

Beyond trade talks, China has been stirring the geopolitical pot through its involvement in the political instability occurring in Hong Kong, which is a Special Administrative Region (SAR) of China. For over five months Hong Kong has had to deal with mass demonstration and clashes with police primarily over a proposed extradition bill that Hong Kong people fear would give mainland China control and jurisdiction over the region. Time will tell whether the protests will allow Hong Kong to remain relatively independent, or the Chinese Communist party will eventually lose patience and use an authoritarian response to the protesters.

Inverted Yield Curve: Fed No Longer Slamming Breaks in Front of Feared Recession

Another issue contributing to recent financial market volatility has been the so-called “inverted yield curve.” Typically, an economic recession has been caused by the Federal Reserve slamming the breaks on an overheated economy by raising short-term interest rates (Federal Funds target rate). Historically, as short-term rates rise and increase borrowing costs (i.e., slow down economic activity), long-term interest rates eventually fall amid expected weak economic activity. When declining long-term interest rates fall below short-term interest rates…voila, you have an inverted yield curve. Why is this scary? Ever since World War II, history has informed us that whenever this phenomenon has occurred, this dynamic has been a great predictor for a looming recession.

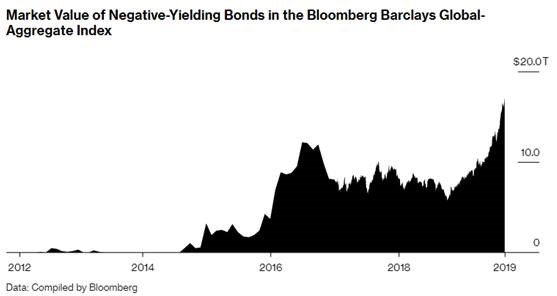

What’s different this time? Unlike the past, is it possible the next recession can be averted or delayed? One major difference is the explosion in negative interest rate yielding bonds now reaching $17 trillion.

Yes, you read that correctly, investors are lining up in droves for guaranteed losses – if these bonds are held until maturity. This widespread perception as a move to perceived safety has not protected the U.S. from the global rate anchor sinking our long-term interest rates. United States interest rates have not turned negative (yet?), but rates have fallen by more than half over the last 10 months from +3.24% to +1.51% on the 10-Year Treasury Note. Will this stimulate businesses to borrow and consumers to buy homes (i.e., through lower cost mortgages), or are these negative rates a sign of a massive global slowdown? The debate continues, but in the meantime, I’m going to take advantage of a 0%-interest rate loan to buy me an 85″ big screen television for my new home!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 3, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Arm Wrestling the Economy & Tariffs

Financial markets have been battling back and forth like a championship arm-wrestling match as economic and political forces continue to collide. Despite these clashing dynamics, capitalism won the arm wrestling match this month as investors saw the winning results of the Dow Jones Industrial Average adding +4.7% and the S&P 500 index advancing +3.6%.

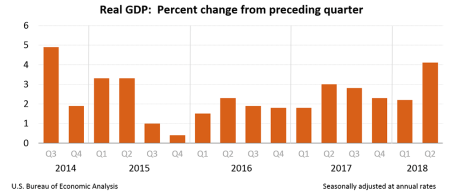

Fueling the strength this month was U.S. economic activity, which registered robust 2nd quarter growth of +4.1% – the highest rate of growth achieved in four years (see below).

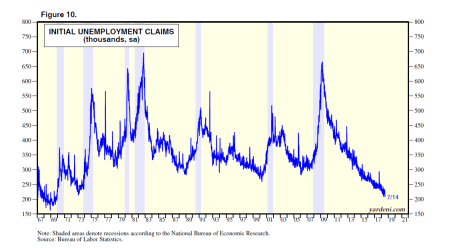

The job market is on fire too with U.S. jobless claims hitting their lowest level in 48 years (see chart below). This chart shows the lowest number of people in a generation are waiting in line to collect unemployment checks.

Source: Dr. Ed’s Blog

If that isn’t enough, so far, the record corporate profits being reported for Q2 are up a jaw-dropping +23.5% from a year ago. What can possibly be wrong?

Excess Supply of Concern

While the economic backdrop is largely positive, there is never a shortage of things to worry about – even during decade-long bull market of appreciation. More specifically, investors have witnessed the S&P 500 index more than quadruple from a March 2009 low of 666 to 2,816 today (+322%). Despite the massive gains achieved over the last decade, there have been plenty of volatility and geopolitics to worry about. Have you already forgotten about the Flash Crash, Arab Spring, Occupy Wall Street, Government Shutdowns, Sequestration, Taper Tantrum, Ebola, Iranian nuclear threat, plunging oil prices, skyrocketing oil prices, Brexit, China scares, Elections, and now tariffs, trade, and the Federal Reserve monetary policy?

Today, tariffs, trade, Federal Reserve monetary policy, and inflation are top-of-mind investor concerns, but history insures there will be new issues to worry about tomorrow. Ever since the bull market began a decade ago, there have been numerous perma-bears incorrectly calling for a deathly market collapse, and I have written a substantial amount about these prognosticators’ foggy crystal balls (see Emperor Schiff Has No Clothes [2009] & Clashing Views with Dr. Roubin [2009]. While these doomsdayers get a lot less attention today, similar bears like John Hussman, who like a broken record, has erroneously called for a market crash every year for the last seven years (click chart link).

Although many investment accounts are up over the last 10 years, many people quickly forget it has not been all rainbows and unicorns. While the stock market has more than quadrupled in value since 2009, we have lived through about a dozen alarming corrections, including the worrisome -12% pullback we experienced in February. If we encounter another -5 -10% correction this year, this is perfectly healthy, normal, and should not be surprising. More often than not, these temporary drops provide opportunistic openings to scoop up valued bargains.

Longtime readers and followers of Sidoxia’s investment philosophy and Investing Caffeine understand the majority of these economic predictions and political headlines are useless noise. Social media, addiction to smart phones, and the 24/7 news cycle create imaginary, scary mountains out of harmless molehills. As I have preached for years, the stock market does not care about politics and opinions – the stock market cares about 1) corporate profits (at record levels) – see chart below; 2) interest rates (rising, but still near historically low levels); 3) the price of the stock market/valuation (which is getting cheaper as profits soar from tax cuts); and 4) sentiment (a favorable contrarian indicator until euphoria kicks in).

Source: Dr. Ed’s Blog

Famed investor manager, Peter Lynch, who earned +29% annually from 1977-1990 also urged investors to ignore attempts of predicting the direction of the economy. Lynch stated, “I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

I pay more attention to successful long-term investors, like Warren Buffett (the greatest investor of all-time), who remains optimistic about the stock market. As I’ve noted before, although we remain constructive on the markets over the intermediate to long-term periods, nobody has been able to consistently prophesize about the short-term direction of financial markets.

At Sidoxia, rather than hopelessly try to predict every twist and turn in the market, or react to every meaningless molehill, we objectively analyze the available data without getting emotional, and then take advantage of the opportunities presented to us in the marketplace. Certain asset classes, stocks, and bonds, will constantly move in and out of favor, which allows us to continually find new opportunities. A contentious arm wrestling struggle between uncertain tariffs/rising interest rates and stimulative tax cuts/strong economy is presently transpiring. As always, we will continually monitor the evolving data, but for the time being, the economy is flexing its muscle and winning the battle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}