Posts tagged ‘Ted Williams’

Waiting for the Fat Pitch

Fall is here and the leaves are beginning to change, which means it’s baseball playoffs time and the World Series is quickly approaching. Investing in some respects is similar to baseball because they both require discipline and patience. One investing legend who embodies those characteristics is Warren Buffett, and he has repeatedly spoken about Ted Williams and waiting for the “fat pitch.”

John Huber, over at BHI, did a great job summarizing Ted Williams’ hitting philosophy here:

“Ted Williams was famous for “waiting for the fat pitch”. He would only look to swing at pitches in the part of the strike zone where he knew he had a higher probability of getting a hit. There were parts of his strike zone where he batted .230 and there were other parts of the strike zone where he batted .400. He knew that if he waited for a pitch over the heart of the plate and didn’t swing at pitches in the .230 part of the strike zone—even though they were strikes—he would improve his odds of getting a hit and increase his overall batting average.”

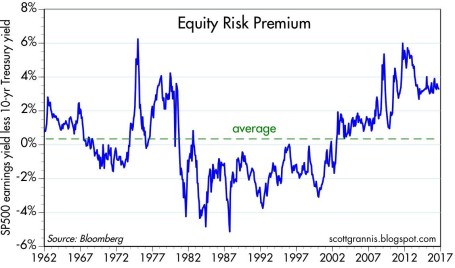

This lesson of patience and discipline is critical for your investment portfolio. Too many people speculate by chasing a hot tip or good stock story, or on the flip side, panic by selling based upon transitory negative news headlines. Today, we see risk aversion happening on steroids. Consider there is over $8 trillion sitting in savings accounts earning effectively nothing – the equivalent of stuffing money under the mattress (see also Invest or Die). In other words, investors are paying extremely high prices (chasing) for safer (less volatile) securities – bonds and cash, while equities are yielding a much higher rate as measured by the earnings yield of the S&P 500 (S&P operating profits / index value). Scott Grannis at Calafia Beach Pundit calls this dynamic the equity risk premium (chart below).

Source: Scott Grannis

As you can see from the chart, ever since the financial crisis occurred, stocks have been compensating investors at significantly higher levels (almost 4% currently) than the yields on 10-Year Treasury Notes, a phenomenon not experienced for the previous three decades.

When will this equity premium revert back towards the mean? There are number of factors that could correct this disparity.

1). The economy enters recession and profits decline to a point at which bonds offer a more compelling risk-reward ratio than stocks.

2). Interest rates rise (bond prices decline) to a point at which bonds offer a more compelling risk-reward ratio than stocks.

3). Investors bid stocks significantly higher to a point at which bonds offer a more compelling risk-reward ratio than stocks.

Most people are worried about scenario #1, but there is plenty objective data that splashes cold water on that view. Consider the unemployment rate has been chopped in half since 2009 with about 15 million jobs added; corporate profits are at/near record highs; auto sales are at/near record highs; home sales continue on an improving trajectory; and the yield curve remains positive, among other factors. If you absorb that information, it clearly doesn’t resemble a recessionary environment, but that doesn’t prevent people from worrying.

Regarding scenario #2, rising rates are an eventuality, but an absence of meaningful inflation, coupled with sluggish global growth are likely to keep a lid on interest rates for some time. Any casual observer would realize that interest rates have been on a downward trend for more than 35 years (see also Fall is Here: Change is Near). Even with a potential second rate increase in a decade initiated by the Fed this upcoming December, the long-term downward trend in rates will likely remain intact.

While the media likes to focus on the half-glass full scenarios (#1 & #2), very little time has been expended on the possibility of scenario #3, which contemplates a rise in stock prices to erase the discount in stock prices relative to bond prices (i.e., elevated equity risk premium).

While many people are ignoring the probability of scenario #3 occurring, like a disciplined hitter in baseball, successful investing requires patience while you wait for your fat investment pitch.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

{kind=link}