Posts tagged ‘tech bubble’

Confusing Fear Bubbles with Stock Bubbles

With the Dow Jones Industrial Average approaching and now breaking the 16,000 level, there has been a lot of discussion about whether the stock market is an inflating bubble about to burst due to excessive price appreciation? The reality is a fear bubble exists…not a valuation bubble. This fear phenomenon became abundantly clear from 2008 – 2012 when $100s of billions flowed out of stocks into bonds and trillions in cash got stuffed under the mattress earning near 0% (see Take Me Out to the Stock Game). The tide has modestly turned in 2013 but as I’ve written over the last six months, investor skepticism has reigned supreme (see Most Hated Bull Market Ever & Investors Snore).

Volatility in stocks will always exist, but standard ups-and-downs don’t equate to a bubble. The fact of the matter is if you are reading about bubble headlines in prominent newspapers and magazines, or listening to bubble talk on the TV or radio, then those particular bubbles likely do not exist. Or as strategist and investor Jim Stack has stated, “Bubbles, for the most part, are invisible to those trapped inside the bubble.”

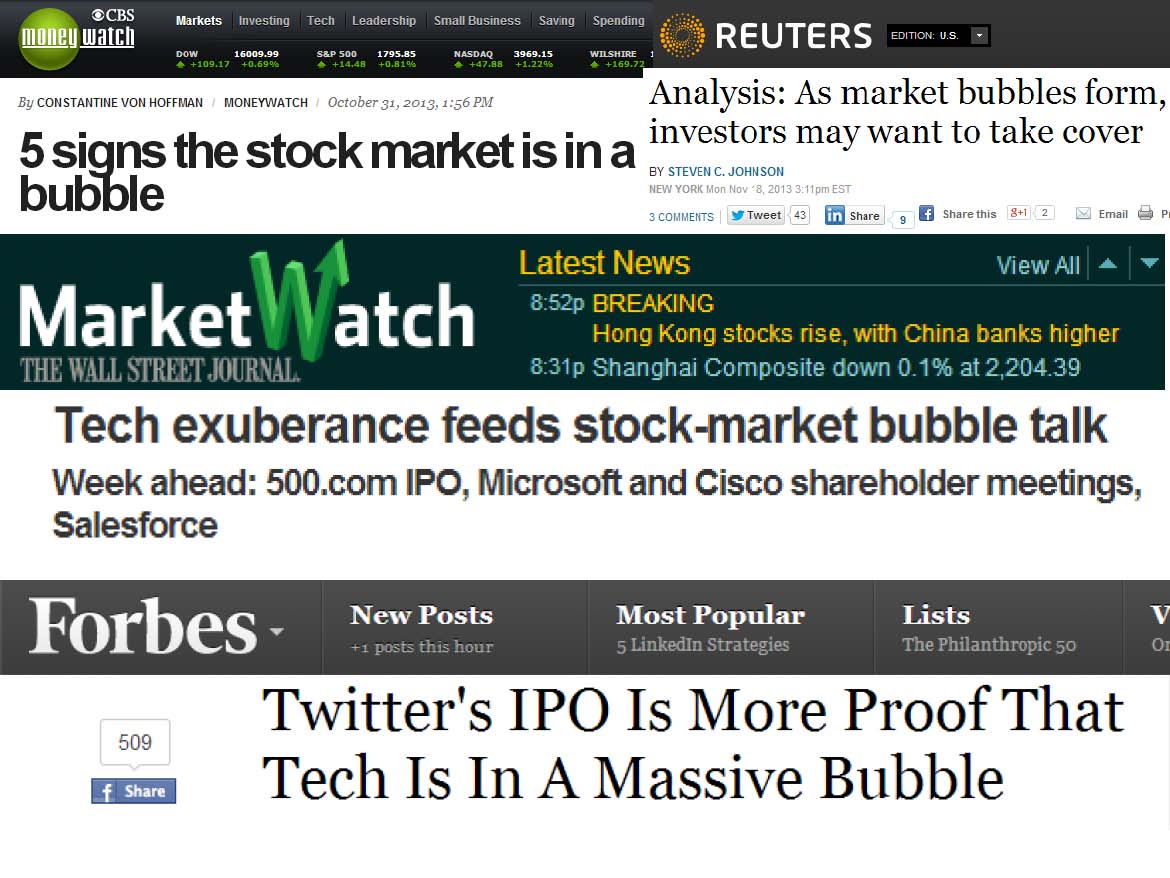

All the recent bubble talk scattered over all the media outlets only bolsters my fear case more. If we actually were in a stock bubble, you wouldn’t be reading headlines like these:

From 1,300 Bubble to 5,000

If you think identifying financial bubbles is easy, then you should buy former Federal Reserve Chairman Alan Greenspan a drink and ask him how easy it is? During his chairmanship in late-1996, he successfully managed to identify the existence of an expanding technology bubble when he delivered his infamous “irrational exuberance” speech. The only problem was he failed miserably on his timing. From the timing of his alarming speech to the ultimate pricking of the bubble in 2000, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000).

Current Fed Chairman Ben Bernanke was no better in identifying the housing bubble. In his remarks made before the Federal Reserve Board of Chicago in May 2007, Bernanke had this to say:

“…We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well.”

If the most powerful people in finance are horrible at timing financial market bubbles, then perhaps you shouldn’t stake your life’s savings on that endeavor either.

Bubbles History 101

Each bubble is unique in its own way, but analyzing previous historic bubbles can help understand future ones (see Sleeping Through Bubbles):

• Dutch Tulip-Mania: About 400 years ago in the 1630s, rather than buying a new house, Dutch natives were paying over $60,000 for tulip bulbs.

• British Railroad Mania: The overbuilding of railways in Britain during the 1840s.

• Roaring 20s: Preceding the Wall Street Crash of 1929 (-90% plunge in the Dow Jones Industrial average) and Great Depression, the U.S. economy experienced an extraordinary boom during the 1920s.

• Nifty Fifty: During the early 1970s, investors and traders piled into a set of glamour stocks or “Blue Chips” that eventually came crashing down about -90%.

• Japan’s Nikkei: The value of the Nikkei index increased over 450% in the eight years leading up to the peak of 38,957 in December 1989. Today, almost 25 years later, the index stands at about 15,382.

• Tech Bubble: Near the peak of the technology bubble in 2000, stocks like JDS Uniphase Corp (JDSU) and Yahoo! Inc (YHOO) traded for over 600x’s earnings. Needless to say, things ended pretty badly once the bubble burst.

As long as humans breathe, and fear and greed exist (i.e., forever), then we will continue to encounter bubbles. Unfortunately, we are unlikely to be notified of future bubbles in mainstream headlines. The objective way to unearth true economic bubbles is by focusing on excessive valuations. While stock prices are nowhere near the towering valuations of the technology and Japanese bubbles of the late 20th century, the bubble of fear originating from the 2008-2009 financial crisis has pushed many long-term bond prices to ridiculously high levels. As a result, these and other bonds are particularly vulnerable to spikes in interest rates (see Confessions of a Bond Hater).

Rather than chasing bubbles and nervously fretting over sensationalistic headlines, you will be better served by devoting your attention to the creation of a globally diversified investment portfolio. Own a portfolio that integrates a wide range of asset classes, and steers clear of popularly overpriced investments that the masses are talking about. When fear disappears and everyone is clamoring to buy stocks, you can be confident the stock bubble is ready to burst.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, JDSU, YHOO or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ken Heebner: Dr. Adrenaline

Is the market making you feel a little lost, down, or disconnected? Then perhaps what you need is a prescription of adrenaline in the form of some CGM Focus Fund shares (CGMFX). Ken Heebner has captained the CGM Focus Fund since its 1997 inception. This hyper-volatile fund is not for the faint of heart. The concentrated fund holds a narrow portfolio (often 20-30 positions), which is managed with a very itchy trigger-finger. The eye-popping 363% turnover last year is proof of Heebner’s rapid fire approach, which equates to an average stock holding period of around three months. Although “Dr. Adrenaline” has earned the top Morningstar ranking for his Focus Fund on a 10-year basis (annualized +11.8% vs. +2.1% S&P 500 – Morningstar 6/9/11), Heebner is dead last on a 3-year basis (annualized -19.9% vs. +.4% S&P 500).

The Journey from First to Worst

How does a manager go from first to worst? Well, given the fund’s “go anywhere” mandate, Heebner became a hero when he shorted technology and internet stocks in 2000 and 2001during the bubble burst (yes, that’s correct, the Focus Fund has the ability to short securities as well). Simultaneously, Heebner went long the homebuilders and watched the massive appreciation transpire as the real estate bubble inflated. This clever maneuvering earned the fund a whopping +54% return in 2000 and an encore +47% advance in 2001, while the S&P 500 index plummeted -9% and -12%, respectively.

While Heebner captured the inflection of the tech bubble bursting, he has fared less well through the financial crisis and recovery of 2008-2011. After riding the commodities boom in 2007, on the way to an +80% killing, Heebner overstayed his welcome at the trough. Not only did his commodity stocks tank, he prematurely piled into financials and insurance companies (e.g., BAC, C, WFC, HIG). Like many other managers, Heebner underestimated the severity and scope of the financial crisis and he and his investors suffered the consequences (underperformed the S&P 500 by -11% in 2008 and -16% in 2009).

This is what Heebner had to say about the housing market in late 2007:

“It’s a narrow sector. Globally the US housing market is not that important. I think it may flatten out our retail sales and our economy may go sidewise, but I don’t think that’s going to derail this global economy.”

That forecast didn’t really pan out as expected and this year hasn’t exactly gotten off to a rosy start either. The fund is already down -12% in 2011, trailing the S&P 500 by an overwhelming -15% margin.

Behind the Brains

The grey-haired, 70-year-old Heebner has accumulated a lot of real world schooling before starting CGM (Capital Growth Management) in 1990. Heebner started his career as an economist with A & H Kroeger in 1965, before he decided to get his feet wet in money management as a portfolio manager at Scudder, Stevens & Clark, as well as Loomis Sayles & Co.

Heebner does not follow your ordinary run of the mill investment strategy. As the antithesis of a traditional value investor, Heebner typically buys stocks that have already appreciated in price. He is looking for stocks with a “pattern of earnings development in excess of consensus.” Or as Heebner clarifies, “I try and find a situation where the development of the fundamentals is going to be more positive than other investors are experiencing.” When investing in the fund, Heebner combines fundamental analysis with an overlay of a top-down macroeconomic assessment.

At last check in April, Heebner was still optimistic about the prospects for equities, despite the outlook for inflation:

“I ran money from 1976 to 1980. The inflation rate went from 6 to 15. There was a lot of money to be made.”

In inflationary environments, Heebner advocates finding companies with earnings growth profiles that will expand faster than the compression in price-earnings ratios.

Vodpod videos no longer available.Heebner Not Alone

Ken Heebner is certainly not the only hot-shot manager in history to suffer a cold-spell. After setting records and beating the S&P 500 index for 15 consecutive years, Bill Miller has found his fund (Legg Mason Capital Management Value Fund – LMVTX) firmly in the bottom decile of his peer group on a 1-year, 3-year, 5-year, and 10-year basis (see also Revenge of the Dunce). Moreover, Morningstar’s fund manager of the decade, Bruce Berkowitz of the Fairholme Fund (FAIRX), has also recently been hit by the performance ugly stick (see also The Invisible Giant), albeit less bad than Heebner and Miller.

When all is said and done, the flexibility afforded to Ken Heebner in managing the CGM Focus Fund has served long-term investors very well – if they were not prematurely spooked out the investments due to volatility. For those not invested in the CGM Focus Fund, or for those bored individuals looking for rollercoaster returns, Dr. Heebner may have just the adrenaline prescription you were looking for…a healthy dosage of CGM Focus Fund shares!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in CGMFX, LMVTX, FAIRX, BAC, C, WFC, HIG, MORN, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Killing Patients to Investment Prosperity

All investors are optimistic, every time they open up a position, but just like surgeons, sometimes the outcome doesn’t turn out as well as initially anticipated. When it comes to investing, I think this old Hindu proverb puts things into perspective:

“No physician is really good before he has killed one or two patients.”

So too, an investor does not become really good until he kills off some investment positions. But like surgeons, investors also have to understand the most important aspect of tragic events is learning from them. In many cases, unexpected outcomes are out of our control and cannot be prevented. This conclusion, in and of itself, can provide valuable insights. But on many occasions, there are procedures, processes, and facts that were missed or botched, and learning from those mistakes can prove invaluable when it comes to refining the process in the future – in order to further minimize the probability of a tragic outcome.

My Personal Killers

Professionally, I have killed some stocks in my career too, or they have killed me, depending on how you look at the situation. How did these heartrending incidents occur? There are several categories that my slaughtered stocks fell under:

- Roll-Up, Throw-Up: Several of my investment mistakes have been tied to roll-up or acquisition-reliant growth stories, where the allure of rapid growth shielded the underlying weak fundamentals of the core businesses. Buying growth is easier to create versus organically producing growth. Those companies addicted to growth by acquisition eventually experience the consequences firsthand when the game ends (i.e., the quality of deals usually deteriorates and/or the prices paid for the acquisitions become excessive).

- Technology Kool-Aid: Another example is the Kool-Aid I drank, during the technology bubble days, related to a “story” stock – Webvan, a grocery delivery concept. How could mixing Domino’s pizza delivery (DZP) with Wal-Mart’s (WMT) low-priced goods not work? I’m just lazy enough to demand a service like that. Well, after spending hundreds of millions of dollars and never reaching the scale necessary to cover the razor thin profit margins, Webvan folded up shop and went bankrupt. But don’t give up hope yet, Amazon (AMZN) is refocusing its attention on the grocery space (mostly non-perishables now) and could become the dominant food delivery retailer.

- Penny Stocks = Dollars Lost: Almost every seasoned investor carries at least one “penny stock” horror story. Unfortunately for me, my biotech miracle stock, Saliva Diagnostics (SALV), did not take off to the moon and provide an early retirement opportunity as planned. On the surface it sounded brilliant. Spit in a cup and Saliva Diagnostic’s proprietary test would determine whether patients were infected with the HIV virus. With millions of HIV/AIDS patients spread around the world, the profit potential behind ‘Saliva’ seemed virtually limitless. The technology unfortunately did not quite pan out, and spit turned into tears.

The Misfortune Silver Lining

These stock tragedies are no fun, but I am not alone. Fortunately for me, and other professionals, there is a nine-lives feline element to investing. One does not need to be right all the time to outperform the indices. “If you’re terrific in this business you’re right 6 times out of 10 – I’ve had stocks go from $11 to 7 cents (American Intl Airways),” admitted investment guru Peter Lynch. Growth stock investing expert, Phil Fisher, added: “Fortunately the long-range profits earned from really good common stocks should more than balance the losses from a normal percentage of such mistakes.”

Warren Buffett takes a more light-hearted approach when he describes investment mistakes: “If you were a golfer and you had a hole in one on every hole, the game wouldn’t be any fun. At least that’s my explanation of why I keep hitting them in the rough.”

Some investors purposely forget traumatic investment experiences, but explicitly sweeping the event under the rug will do more harm than good. So the next time you suffer a horrendous stock price decline, do your best to log the event and learn from the situation. That way, when the patient (stock) has been killed (destroyed), you will become a better, more prosperous doctor (investor).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, and AMZN but at the time of publishing SCM had no direct position in DZP, Webvan, Saliva Diagnostics, American intl Airways, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}