Posts tagged ‘tax reform’

‘Tis the Season for Giving

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2017). Subscribe on the right side of the page for the complete text.

Holiday season is in full swing, and that means it’s the primetime period for giving. The stock market has provided its fair share of giving to investors in the form of a +2.7% monthly return in the S&P 500 index (up +18% in 2017). For long-term investors, stocks have been the gift that keeps on giving. As we approach the 10-year anniversary of the 2008 Financial Crisis, stocks have returned +68% from the October 2007 peak and roughly +297% from the March 2009 low. If you include the contributions of dividends over the last decade, these numbers look even more charitable.

Compared to stocks, however, bonds have acted more like a stingy Ebenezer Scrooge than a generous Mother Theresa. For the year, the iShares Core Aggregate bond ETF (AGG) has returned a meager +1%, excluding dividends. Contributing to the lackluster bond results has been the Federal Reserve’s miserly monetary policy, which will soon be managed under new leadership. In fact, earlier this week, Jerome Powell began Congressional confirmation hearings as part of the process to replace the current Fed chair, Janet Yellen. As the Dow Jones Industrial Average rose for the 8th consecutive month to 24,272 (the longest winning streak for the stock index in 20 years), investors managed to take comfort in Powell’s commentary because he communicated a steady continuation of Yellen’s plan to slowly reverse stimulative policies (i.e., raise interest rate targets and bleed off assets from the Fed’s balance sheet).

Because the pace of the Federal Funds interest rate hikes have occurred glacially from unprecedented low levels (0%), the resulting change in bond prices has been relatively meager thus far in 2017. In that same deliberate vein, the Fed is meeting in just a few weeks, with the expectation of inching the Federal Funds rate higher by 0.25% to a target level of 1.5%. If confirmed, Powell plans to also chip away at the Fed’s gigantic $4.5 trillion balance sheet over time, which will slowly suck asset-supporting liquidity out of financial markets.

Economy Driving Stocks and Interest Rates Higher

Presents don’t grow on trees and stock prices also don’t generally grow without some fundamental underpinnings. With the holidays here, consumers need money to fulfill the demanding requests of gift-receiving individuals, and a healthy economy is the perfect prescription to cure consumers’ empty wallet and purse sickness.

Besides the Federal Reserve signaling strength by increasing interest rates, how do we know the economy is on firm footing? While economic growth may not be expanding at a barn-burning rate, there still are plenty of indications the economy keeps chugging along. Here are a few economic bright spots to highlight:

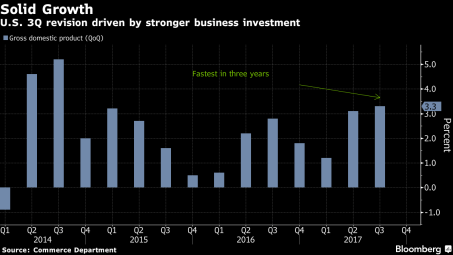

- Accelerating GDP Growth: As you can see from the chart below, broad economic growth, as measured by Gross Domestic Product (GDP), accelerated to a very respectable +3.3% growth rate during the third quarter of 2017 (the fastest percentage gain in three years). These GDP calculations are notoriously volatile figures, nevertheless, the recent results are encouraging, especially considering these third quarter statistics include the dampening effects of Hurricane Harvey and Irma.

Source: Bloomberg

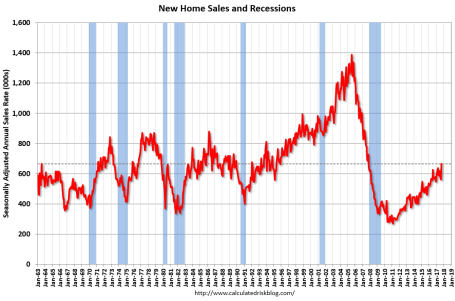

- Recovering Housing Market: The housing market may not have rebounded as quickly and sharply as the U.S. stock market since the Financial Crisis, but as the chart below shows, new home sales have been on a steady climb since 2011. What’s more, a historically low level of housing inventory should support the continued growth in home prices and home sales for the foreseeable future. The confidence instilled from rising home equity values should also further encourage consumers’ cash and credit card spending habits.

Source: Calculated Risk

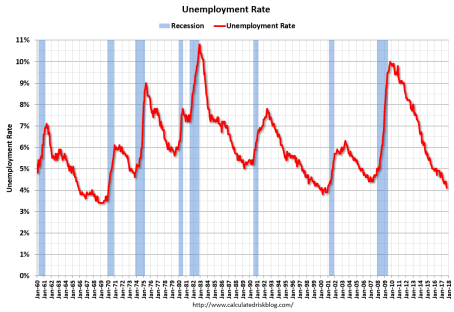

- Healthy Employment Gains: Growth in the U.S. coupled with global synchronous economic expansion in Europe, Asia, and South America have given rise to stronger corporate profits and increased job hiring. The graph highlighted below confirms the 4.1% unemployment rate is the lowest in 17 years, and puts the current rate more than 50% below the last peak of 10.0% hit in 2009.

Source: Calculated Risk

Turbo Tax Time

Adding fuel to the confidence fire is the prospect of the president signing the TCJA (Tax Cuts and Jobs Act). At the time this article went to press, Congress was still feverishly attempting to vote on the most significant tax-code changes since 1986. Republicans by-and-large all want tax reform and tax cut legislation, but the party’s narrow majority in the House and Senate leaves little wiggle room for disagreement. Whether compromises can be met in the coming days/weeks will determine whether a surprise holiday package will be delivered this year or postponed by the Grinch.

Unresolved components of the tax legislation include, the feasibility of cutting the corporate tax rate from 35% to 20%; the deductibility of state and local income taxes (SALT); the potential implementation of a tax cut limit “trigger”, if forecasted economic growth is not achieved; the potential repeal of the estate tax (a.k.a., “death tax”); mortgage interest deductibility; potential repeal of the Obamacare individual mandate; the palatability of legislation expanding deficits by $1 trillion+; debates over the distribution of tax cuts across various taxpayer income brackets; and other exciting proposals that will heighten accountants’ job security, if the TCJA is instituted.

Bitcoin Bubble?

If you have recently spent any time at the watercooler or at a cocktail party, you probably have not been able to escape the question of whether the digital blockchain currency, Bitcoin, is an opportunity of a lifetime or a vehicle to crush your financial dreams to pieces (see Bitcoin primer).

Let’s start with the facts: Bitcoin’s value traded below $1,000 at the beginning of this year and hit $11,000 this week before settling around $10,000 at month’s end (see chart below). In addition, blogger Josh Brown points out the scary reality that “Bitcoin has already crashed by -80% on five separate occasions over the last few years.” Suffice it to say, transacting in a currency that repeatedly loses 80% of its value can pose some challenges.

Source: CoinMarketCap.com

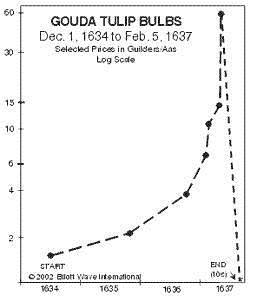

Bubbles are not a new phenomenon. Not only have I lived through numerous bubbles, but I have also written on the topic (see also Sleeping and Napping through Bubbles). I find the Dutch Tulip Bulb Mania that lasted from 1634 – 1637 to be the most fascinating financial bubble of all (see chart below). At the peak of the euphoria, individual Dutch tulip bulbs were selling for the same prices as homes ($61,700 on an inflation-adjusted basis), and one historical account states 12 acres of land were offered for a single tulip bulb.

Forecasting the next peak of any speculative bubble is a fool’s errand in my mind, so I choose to sit on the sidelines instead. While I may be highly skeptical of the ethereal value placed on Bitcoin and other speculative markets (i.e. ICOs – Initial Coin Offerings), I fully accept the benefits of the digital blockchain payment technology and also acknowledge Bitcoin’s value could more than double from here. However, without any tangible or intellectual process of valuing the asset, history may eventually place Bitcoin in the same garbage heap as the 1630 tulips.

For some of you out there, if you are anything like me, your digestion system is still recovering from the massive quantities of food consumed over the Thanksgiving holiday. However, when it comes to your personal finances, digesting record-breaking stock performance, shifting Federal Reserve monetary policy, tax legislation, and volatile digital currencies can cause just as much heartburn. In the spirit of “giving”, if you are having difficulty in chewing through all the cryptic economic and political noise, “give” yourself a break by contacting an experienced, independent, professional advisor. That’s definitely a gift you deserve!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Markets Fly as Media Noise Goes By

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2017). Subscribe on the right side of the page for the complete text.

That loud pitched noise is not a frightening scream from Halloween, but rather what you are likely hearing is the deafening noise coming from Washington D.C or cries from concerned Americans watching senseless acts of terrorism. Thanks to the explosion of real-time social media and smart phones, coupled with the divisive politics and depressing headlines blasted across all media outlets, it is almost impossible to ignore the daily avalanche of informational irrelevance.

As I have been writing for some time, the good news for long-term investors is the financial markets continue to plug their ears and ignore poisonous politics and the spread of F.U.D. (Fear, Uncertainty & Doubt). There is a financial benefit to turning off the TV and disregarding political rants over your Facebook feed. Regardless of your political views, President Trump’s approval ratings have objectively been going down, but that really doesn’t matter…the stock market keeps going up (see chart below).

Source: Bespoke

While politicians on both sides scream at each other, investment portfolios have been screaming higher. Stock prices are more focused on the items that really matter, which include corporate profits, interest rates, valuations (price levels), and sentiment (i.e., determining whether investors are too optimistic or too pessimistic). The proof is in the pudding. Stock prices continue to set new records, as witnessed by the 7th consecutive monthly high registered by the Dow Jones Industrial Average to a level of 23,377. For the month, these results translate into an astonishing +4.3% gain. For the year, this outcome equates to an even more impressive +18.3% return. This definitely beats the near-0% rate earned on your checking account and cash stuffed under the mattress.

On the surface, 2017 has been quite remarkable, but over the last decade, stock market returns have proved to be even more extraordinary. Bolstering my contention that politics rarely matter to your long-term pocketbook, one can simply observe history. We are now approaching the 10-year anniversary of the 2008-2009 Financial Crisis – arguably the worst recession experienced in a generation. Over the last decade, despite political power in Washington bouncing around like a hot potato, stock performance has skyrocketed. From early 2009, when the Dow briefly touched a low of 6,470, the index has almost quadrupled above the 23,000 threshold (see chart below).

Source: Barchart.com

To place this spectacular period into better context, one should look at the political control dynamics across Congress and the White House over the same time frame (see the right side of the chart below). Whether you can decipher the chart or not, anyone can recognize that the colors consistently change from red (Republican) to blue (Democrat), and then from blue to red.

More specifically, since the end of 2007, the Democrats have controlled the Senate for approximately 80% of the time; the Republicans have controlled the House of Representatives for 60% of the time; and the Oval Office has switched between three different presidents (two Republicans and one Democrat). And if that is not enough diversity for you, we have also had two Federal Reserve Chairs (Ben Bernanke and Janet Yellen) who controlled the world’s most powerful monetary system, and a Congressional mid-term election taking place in twelve short months. There are two morals to this story: 1) No matter how sad or excited you are about your candidate/political party, you can bank on the control eventually changing; and 2) One person alone cannot save the economy, nor can that same person singlehandedly crater the economy.

Source: Wikipedia

Waterfall of Worries

If you simply read the newspapers and watched the news on TV all day, you would be shocked to learn about the magnificent magnitude of this equity bull market. Reaching these new highs has not been a walk in the park for most investors. There certainly has been no shortage of issues to worry about, including the following:

- Special Counsel Indictments: After the abrupt firing of former FBI Director James Comey by President Donald Trump, Deputy Attorney General Rod Rosenstein established a special counsel in May and appointed ex-FBI official and attorney Robert Mueller to investigate potential Russian meddling into the 2016 presidential elections. Just this week, Mueller indicted Paul Manafort, the former Trump campaign chairman, and Manafort’s business partner and Trump campaign volunteer, Rick Gates. The special counsel also announced the guilty plea of George Papadopoulos, a former foreign policy adviser for the Trump campaign who admitted lying to the FBI regarding interactions between Russian officials and the Trump campaign.

- Terrorist Attacks: Senseless murders of eight people in New York by a 29-year-old man from Uzbekistan, and 59 people shot dead by a 64-year-old shooter from a Las Vegas casino have created a chilling blanket of concern over American psyches.

- New Money Chief? The term of current Federal Reserve Chair, Janet Yellen, ends this February. President Trump has fueled speculation he will announce the appointment of a new Fed chief as early as this week. Although the president has recently praised Yellen, a registered Democrat, many pundits believe Trump wants to select Jerome Powell, a Republican, who currently sits on the Federal Board of Governors.

- North Korea Rocket Launches: So far in 2017, North Korea has launched 22 missiles and tested a hydrogen bomb, while simultaneously threatening to fire missiles over the US territory of Guam and conduct an atmospheric nuclear test. Saber rattling has diminished somewhat in recent weeks since the last North Korean missile launch took place on September 15th. Nevertheless, tensions could rise at any moment, if missile launches resume.

Although media headlines are often depressing, F.U.D. will never go away – it’s only the list of worries that change over time. As noted earlier, the entrepreneurial DNA of the financial markets is focused on more important economic factors like the economy, rather than politics or terrorism. One barometer of economic health can be gauged by the chart below – Consumer Confidence is at the highest level since 2000.

Source: Bespoke

This trend is important because consumers make up approximately 70% of our nation’s economic output. Therefore, it should come as no surprise that Americans are feeling considerably better due to the following factors:

- Strong Job Market: The 4.2% unemployment rate is at the lowest level in 16 years.

- Strong Economy: Despite the dampening effect of the hurricanes, the economy is poised to register its best six-month performance of at least 3% growth in three years.

- Strong Housing Market: Just-released data shows an acceleration in national home price appreciation by +6.1% compared to a year ago.

- Low Interest Rates: Inflation has been low, credit has been cheap, and the Federal Reserve has been cautious in raising interest rates. These low rates have improved the affordability of credit, which has been stimulative for the economy.

Tax Reform Could be the Norm

The icing on the stock market cake has been the optimism surrounding the potential passage of tax reform, likely in the shape of corporate & personal tax cuts, foreign profit repatriation, and tax simplification. The process has been slow, but by passing a budget, the Republican-led Congress was able to pave the way for substantive new tax reform, something not seen since the Ronald Reagan administration, some 30-years ago. Everybody loves paying lower taxes, but victory cannot be claimed yet. Democrats and some fiscally conservative Republicans are not interested in exploding our country’s already-large deficits and debt levels. In order to achieve responsible tax legislation, Congress is looking to remove certain tax loopholes and is negotiating precious tax breaks such as mortgage interest deductibility, state/local tax deductibility, 401(k) tax incentives, and corporate interest expense deductibility, among many other possible iterations. Although corporate tax discussions have been heated, the chart below demonstrates individual income tax legislation is much more important for tax reform legislation because the government collects a much larger share of taxes from individuals vs. corporations.

Source: Calafia Beach Pundit

In spite of all the deafening political noise heard over social media and traditional media, it’s important to block out all the F.U.D. and concentrate on how to achieve your long-term financial goals. If you don’t have the time, energy, or emotional fortitude to follow a disciplined financial plan, I urge you to find an experienced investment advisor who is also a fiduciary. If you need assistance finding one, I am confident Sidoxia Capital Management can help you with this endeavor.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and FB, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The September to Remember

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 2, 2017). Subscribe on the right side of the page for the complete text.

Given the volume of recent memorable events, it appears September will become a month to remember. Not only did we witness horrific natural disasters in Texas, Florida, Puerto Rico, and Mexico but Americans have also had to digest the saber rattling by the North Korean “Rocket Man“ leader, Kim Jong Un*. If that wasn’t enough, there were a slew of headlines detailing the Washington gridlock and dysfunction over healthcare legislation / tax reform; hackings at Equifax affecting up to 143 million credit accounts; the planned unwinding of the Federal Reserves $4.2 trillion bond portfolio; and a controversy over NFL football players kneeling during the national anthem.

Despite all these notable events, the Dow Jones Industrial Average just posted its 8th consecutive quarter of advances. For the three months ending in September, the Dow impressively climbed more than 1,000 points (+4.7%) to a new record high of 22,381. For the year, the Dow remarkably has risen approximately +13%, excluding dividends, which translates into a total 2017 return of more than +15%, thus far.

However, not everybody has participated in the financial party. Negative political headlines have by and large paralyzed the hearts and minds of the general public, but as I have been writing for some time, stocks do not care much about governmental affairs – stock prices care about fundamentals. There have been two critical, fundamental components fueling the repetitive new highs experienced in the stock market: 1) The extraordinarily persistent surge in corporate profits (see chart below); and 2) The stubbornly declining interest rates, which are near generationally-low levels. When investors are offered next-to-nothing interest rates in their bank accounts, and coupon payments on Treasury bonds remain paltry (10-Year Treasury closed month at a yield of 2.33%), suddenly stock opportunities can look much more attractive in a scarce investment environment.

Source: Yardeni.com

And geographically speaking, the rise in corporate profits has not been limited to the U.S. There has also been a synchronized escalation in corporate earnings globally. Whether we are talking about Europe, China, or emerging markets, in general, the economic recovery in these regions is now occurring coincidentally with the U.S. Case in point is the Purchasing Managers Index (PMI), which serves as a broad indicator of the economic health of the manufacturing sector. The chart below highlights the clear recovery that has been ongoing in the global manufacturing sector over the last year and a half.

Source: Yardeni.com

In addition to these numerous positive factors, a cheaper (weaker) U.S. dollar has also contributed to our nation’s economic tailwind. More specifically, a lower valued dollar makes American goods sold abroad cheaper for foreign buyers. This currency exchange rate dynamic is important because 43% of Fortune 500 sales (S&P 500) are derived from American products and services sold in foreign countries.

Tax Reform to be Born?

You probably don’t need me to tell you that gridlock in Washington D.C. is alive and well, but new details surrounding potential tax reform legislation that surfaced last week has lifted short-term investor optimism. As you can see from the chart below, the U.S. has the highest corporate tax rate among 35 developed countries in the OECD (Organisation for Economic Co-operation and Development), thereby making U.S. business less competitive globally. In hopes of reversing this trend, a basic framework was introduced by the President that proposed a top corporate rate of 20%, top small business rate of 25%, and streamlined personal tax brackets of 12%, 25%, and 35% (down from 7 brackets). Other key elements of the tax plan include, a doubling of the standard deduction for middle-class Americans; the elimination of the estate tax for the wealthy; the repeal of the alternative minimum tax; and immediate tax write-offs for business capital investments.

Source: The Financial Times

Many other important details have yet to be released and further specifics remain to be negotiated on Capitol Hill. For example, the removal of deductions for state and local taxes was announced, however additional information explaining how the estimated $2.2 trillion in tax cuts will be funded has yet to surface.

Regardless of the tax reform outcome, the economy continues to chug along at a healthy clip. Most recently, Gross Domestic Product (GDP), the central statistic in measuring the health of the U.S. economy, was revised higher to a respectable +3.1% rate in the second quarter. The latest natural disasters may clip third quarter growth temporarily, however, the consensus remains the economic expansion stands on firm ground, despite the financial drag of the hurricanes.

While geopolitical, meteorological, and athletic anthem headlines have made this a “September to Remember,” fundamental strength and other factors have contributed to this enduring and unforgettable bull market. There will be many more noteworthy headlines to occur in coming months and years, but placing these events in the proper context and investing wisely will lead to a much more positive, memorable existence.

*The article was written before the Las Vegas tragedy on October 1, 2017.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in EFX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Glass Half Full or Half Empty?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2017). Subscribe on the right side of the page for the complete text.

We live in a time of confusing dichotomies, which makes deciphering the flood of daily data quite challenging. In that context, determining whether the current economic fundamentals should be viewed from a glass half empty of glass half full perspective can be daunting.

More specifically, stock markets have again recently hit new all-time record highs, yet if you read the newspaper headlines, you might think we’re in the midst of Armageddon. Last month, the Dow Jones Industrial Average stock index eclipsed 21,000 and the technology-heavy NASDAQ index surpassed the psychologically important 6,000 threshold. In spite of the records, here’s a sampling of the steady stream of gloomy feature stories jamming the airwaves:

- French Elections – Danger of European Union Breakup

- Heightened Saber Rattling by U.S. Towards North Korea

- Threat of U.S. Government Shutdown

- First 100 Days – Obamacare repeal failure, tax reform delays, no significant legislation

- NAFTA Trade Disputes

- Russian Faceoff Over Syrian Civil War & Terrorism

- Federal Reserve Interest Rate Hikes Could Derail Stock Market

- Slowing GDP / Economic Data

Given all this doom, how is it then that stock markets continue to defy gravity and continually set new record highs? Followers of my writings understand the crucial, driving dynamics of financial markets are not newspaper, television, magazine, and internet headlines. The most important factors are corporate profits, interest rates, valuations, and investor sentiment. All four of these elements will bounce around, month-to-month, and quarter-to-quarter, but for the time being, these elements remain constructive on balance, despite the barrage of negative, gut-wrenching headlines.

Countering the perpetual flow of gloomy, cringe-worthy headlines, we have seen a number of positive developments:

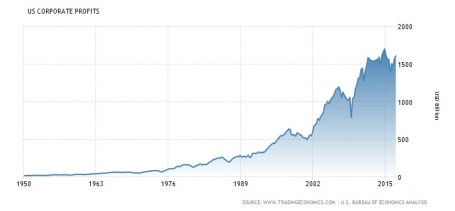

- Record Breaking Corporate Profits: Profits are the chief propellant for higher stock prices, and so far, for the 1st quarter, S&P 500 company profits are estimated to have risen +12.4% – the highest rate since 2011, according to Thomson Reuters I/B/E/S. As I like to remind my readers, stock prices follow profits over the long-run, which is evidenced by the chart below.

Source: Trading Economics

- Interest Rates Low: With interest rate levels still near generational lows (10-Year Treasury @ 2.28%), and inflation relatively stable around 2%, this augurs well for most asset prices. For U.S. consumers there are many stimulative effects to lower interest rates, whether you are buying a house, purchasing a car, paying off a school loan, and/or reducing credit card debt. Lower rates equal lower payments.

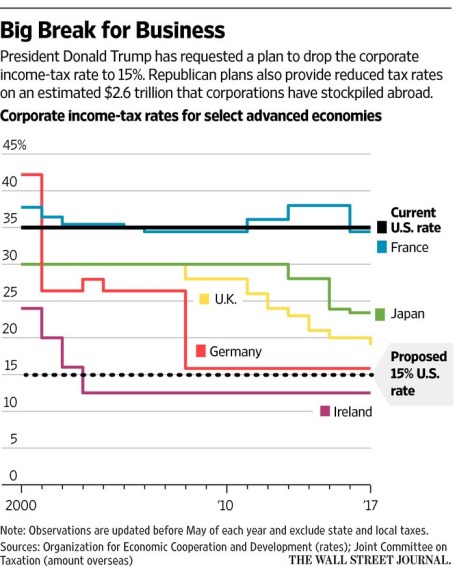

- Potential Tax Reform: There are numerous stimulative components to the largest planned tax-cut in history. First of all, cutting the tax rate from 35% to 15% for corporations and small businesses (i.e. pass-through entities like LLCs and S-Corps) would place a lot of dollars back in the pockets of taxpayers and should stimulate economic growth. Other components of the White House proposal include the termination of the estate tax, the elimination of the AMT (Alternative Minimum Tax) targeted at wealthier households, and the doubling of the standard deduction to help middle-income families. All of this sounds great on paper, but not a lot of details have been provided yet on how these benefits will be paid for – removing state tax deductions alone is unlikely to fully offset revenue declines. The chart below highlights how high U.S. corporate income tax rates are relative to other foreign counterparts.

Source: The Wall Street Journal

- Business Spending & Confidence on the Rise: Ever since the 2008-09 Great Recession, the U.S. has been a better house in a bad neighborhood relative to other global developed economies. However, the recovery has been gradual and muted due to tight-fisted companies being slow to hire and invest. Although recent Q1 GDP economic data came in at a sluggish +0.7% growth rate, the bright spot embedded in the data was a +12% annualized increase in private fixed investment. This is consistent with the spike we’ve seen in recent business and consumer confidence surveys (see chart below). Although this confidence has yet to translate into an acceleration in broader economic data, the ramp in capital spending and positive business sentiment could be a leading indicator for faster economic growth to come. Stimulative legislation enacted by Congress (i.e., tax reform, infrastructure spending, foreign repatriation, etc.) could add further fuel to the economic growth engine.

Source: Trading Economics

- Economy Keeps Chugging Along: As the wealthiest country on the planet, we Americans can become a little spoiled with success, which helps explain the media’s insatiable appetite for growth. Nevertheless, the broader economic data show a continuing trend of improvement. Simply consider the trend occurring in these major areas of the economy:

- Unemployment – The jobless rate has been chopped by more than half from a 10.0% cycle peak to 4.5% today.

- Housing – The number of annual existing home sales has increased by more than +60% from the cycle low to 5.7 million units, which still leaves plenty of headroom for growth before 2006 peak sales levels are reached.

- Consumer Spending – This segment accounts for roughly 70% of our country’s economic activity. Although we experienced a soft patch in Q1 of 2017, as you can see from the chart below, we Americans have had no problem spending more to keep our economy functioning.

Source: Trading Economics

While key economic statistics remain broadly constructive, there will come a time when prudence will dictate the pursuit of a more defensive investment strategy. When will that be? In short, the time to become more cautious will be when we see a combination of the following occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

To date, there is no objective evidence indicating these dynamics are in place, so until then, I will remain thirsty and grab my half glass full of water.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}