Posts tagged ‘tax cuts’

Arm Wrestling the Economy & Tariffs

Financial markets have been battling back and forth like a championship arm-wrestling match as economic and political forces continue to collide. Despite these clashing dynamics, capitalism won the arm wrestling match this month as investors saw the winning results of the Dow Jones Industrial Average adding +4.7% and the S&P 500 index advancing +3.6%.

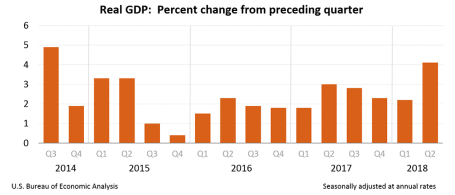

Fueling the strength this month was U.S. economic activity, which registered robust 2nd quarter growth of +4.1% – the highest rate of growth achieved in four years (see below).

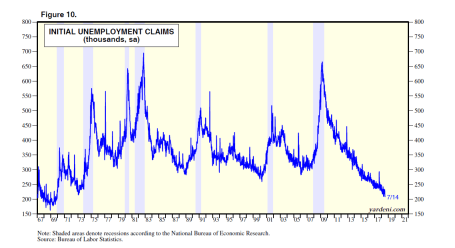

The job market is on fire too with U.S. jobless claims hitting their lowest level in 48 years (see chart below). This chart shows the lowest number of people in a generation are waiting in line to collect unemployment checks.

Source: Dr. Ed’s Blog

If that isn’t enough, so far, the record corporate profits being reported for Q2 are up a jaw-dropping +23.5% from a year ago. What can possibly be wrong?

Excess Supply of Concern

While the economic backdrop is largely positive, there is never a shortage of things to worry about – even during decade-long bull market of appreciation. More specifically, investors have witnessed the S&P 500 index more than quadruple from a March 2009 low of 666 to 2,816 today (+322%). Despite the massive gains achieved over the last decade, there have been plenty of volatility and geopolitics to worry about. Have you already forgotten about the Flash Crash, Arab Spring, Occupy Wall Street, Government Shutdowns, Sequestration, Taper Tantrum, Ebola, Iranian nuclear threat, plunging oil prices, skyrocketing oil prices, Brexit, China scares, Elections, and now tariffs, trade, and the Federal Reserve monetary policy?

Today, tariffs, trade, Federal Reserve monetary policy, and inflation are top-of-mind investor concerns, but history insures there will be new issues to worry about tomorrow. Ever since the bull market began a decade ago, there have been numerous perma-bears incorrectly calling for a deathly market collapse, and I have written a substantial amount about these prognosticators’ foggy crystal balls (see Emperor Schiff Has No Clothes [2009] & Clashing Views with Dr. Roubin [2009]. While these doomsdayers get a lot less attention today, similar bears like John Hussman, who like a broken record, has erroneously called for a market crash every year for the last seven years (click chart link).

Although many investment accounts are up over the last 10 years, many people quickly forget it has not been all rainbows and unicorns. While the stock market has more than quadrupled in value since 2009, we have lived through about a dozen alarming corrections, including the worrisome -12% pullback we experienced in February. If we encounter another -5 -10% correction this year, this is perfectly healthy, normal, and should not be surprising. More often than not, these temporary drops provide opportunistic openings to scoop up valued bargains.

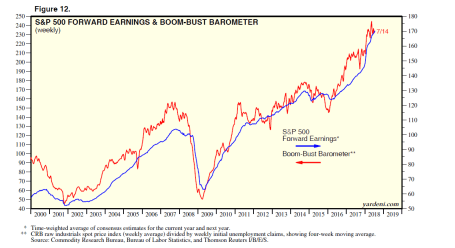

Longtime readers and followers of Sidoxia’s investment philosophy and Investing Caffeine understand the majority of these economic predictions and political headlines are useless noise. Social media, addiction to smart phones, and the 24/7 news cycle create imaginary, scary mountains out of harmless molehills. As I have preached for years, the stock market does not care about politics and opinions – the stock market cares about 1) corporate profits (at record levels) – see chart below; 2) interest rates (rising, but still near historically low levels); 3) the price of the stock market/valuation (which is getting cheaper as profits soar from tax cuts); and 4) sentiment (a favorable contrarian indicator until euphoria kicks in).

Source: Dr. Ed’s Blog

Famed investor manager, Peter Lynch, who earned +29% annually from 1977-1990 also urged investors to ignore attempts of predicting the direction of the economy. Lynch stated, “I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

I pay more attention to successful long-term investors, like Warren Buffett (the greatest investor of all-time), who remains optimistic about the stock market. As I’ve noted before, although we remain constructive on the markets over the intermediate to long-term periods, nobody has been able to consistently prophesize about the short-term direction of financial markets.

At Sidoxia, rather than hopelessly try to predict every twist and turn in the market, or react to every meaningless molehill, we objectively analyze the available data without getting emotional, and then take advantage of the opportunities presented to us in the marketplace. Certain asset classes, stocks, and bonds, will constantly move in and out of favor, which allows us to continually find new opportunities. A contentious arm wrestling struggle between uncertain tariffs/rising interest rates and stimulative tax cuts/strong economy is presently transpiring. As always, we will continually monitor the evolving data, but for the time being, the economy is flexing its muscle and winning the battle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

‘Tis the Season for Giving

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2017). Subscribe on the right side of the page for the complete text.

Holiday season is in full swing, and that means it’s the primetime period for giving. The stock market has provided its fair share of giving to investors in the form of a +2.7% monthly return in the S&P 500 index (up +18% in 2017). For long-term investors, stocks have been the gift that keeps on giving. As we approach the 10-year anniversary of the 2008 Financial Crisis, stocks have returned +68% from the October 2007 peak and roughly +297% from the March 2009 low. If you include the contributions of dividends over the last decade, these numbers look even more charitable.

Compared to stocks, however, bonds have acted more like a stingy Ebenezer Scrooge than a generous Mother Theresa. For the year, the iShares Core Aggregate bond ETF (AGG) has returned a meager +1%, excluding dividends. Contributing to the lackluster bond results has been the Federal Reserve’s miserly monetary policy, which will soon be managed under new leadership. In fact, earlier this week, Jerome Powell began Congressional confirmation hearings as part of the process to replace the current Fed chair, Janet Yellen. As the Dow Jones Industrial Average rose for the 8th consecutive month to 24,272 (the longest winning streak for the stock index in 20 years), investors managed to take comfort in Powell’s commentary because he communicated a steady continuation of Yellen’s plan to slowly reverse stimulative policies (i.e., raise interest rate targets and bleed off assets from the Fed’s balance sheet).

Because the pace of the Federal Funds interest rate hikes have occurred glacially from unprecedented low levels (0%), the resulting change in bond prices has been relatively meager thus far in 2017. In that same deliberate vein, the Fed is meeting in just a few weeks, with the expectation of inching the Federal Funds rate higher by 0.25% to a target level of 1.5%. If confirmed, Powell plans to also chip away at the Fed’s gigantic $4.5 trillion balance sheet over time, which will slowly suck asset-supporting liquidity out of financial markets.

Economy Driving Stocks and Interest Rates Higher

Presents don’t grow on trees and stock prices also don’t generally grow without some fundamental underpinnings. With the holidays here, consumers need money to fulfill the demanding requests of gift-receiving individuals, and a healthy economy is the perfect prescription to cure consumers’ empty wallet and purse sickness.

Besides the Federal Reserve signaling strength by increasing interest rates, how do we know the economy is on firm footing? While economic growth may not be expanding at a barn-burning rate, there still are plenty of indications the economy keeps chugging along. Here are a few economic bright spots to highlight:

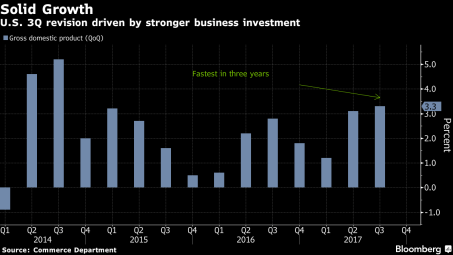

- Accelerating GDP Growth: As you can see from the chart below, broad economic growth, as measured by Gross Domestic Product (GDP), accelerated to a very respectable +3.3% growth rate during the third quarter of 2017 (the fastest percentage gain in three years). These GDP calculations are notoriously volatile figures, nevertheless, the recent results are encouraging, especially considering these third quarter statistics include the dampening effects of Hurricane Harvey and Irma.

Source: Bloomberg

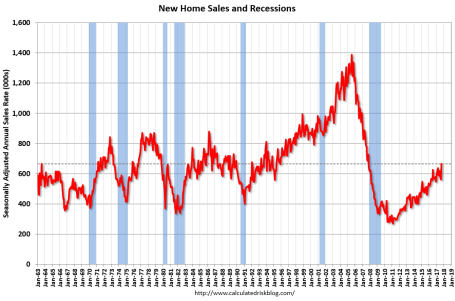

- Recovering Housing Market: The housing market may not have rebounded as quickly and sharply as the U.S. stock market since the Financial Crisis, but as the chart below shows, new home sales have been on a steady climb since 2011. What’s more, a historically low level of housing inventory should support the continued growth in home prices and home sales for the foreseeable future. The confidence instilled from rising home equity values should also further encourage consumers’ cash and credit card spending habits.

Source: Calculated Risk

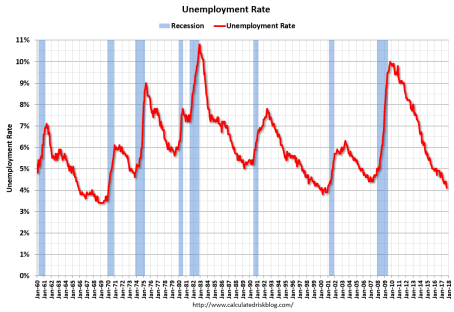

- Healthy Employment Gains: Growth in the U.S. coupled with global synchronous economic expansion in Europe, Asia, and South America have given rise to stronger corporate profits and increased job hiring. The graph highlighted below confirms the 4.1% unemployment rate is the lowest in 17 years, and puts the current rate more than 50% below the last peak of 10.0% hit in 2009.

Source: Calculated Risk

Turbo Tax Time

Adding fuel to the confidence fire is the prospect of the president signing the TCJA (Tax Cuts and Jobs Act). At the time this article went to press, Congress was still feverishly attempting to vote on the most significant tax-code changes since 1986. Republicans by-and-large all want tax reform and tax cut legislation, but the party’s narrow majority in the House and Senate leaves little wiggle room for disagreement. Whether compromises can be met in the coming days/weeks will determine whether a surprise holiday package will be delivered this year or postponed by the Grinch.

Unresolved components of the tax legislation include, the feasibility of cutting the corporate tax rate from 35% to 20%; the deductibility of state and local income taxes (SALT); the potential implementation of a tax cut limit “trigger”, if forecasted economic growth is not achieved; the potential repeal of the estate tax (a.k.a., “death tax”); mortgage interest deductibility; potential repeal of the Obamacare individual mandate; the palatability of legislation expanding deficits by $1 trillion+; debates over the distribution of tax cuts across various taxpayer income brackets; and other exciting proposals that will heighten accountants’ job security, if the TCJA is instituted.

Bitcoin Bubble?

If you have recently spent any time at the watercooler or at a cocktail party, you probably have not been able to escape the question of whether the digital blockchain currency, Bitcoin, is an opportunity of a lifetime or a vehicle to crush your financial dreams to pieces (see Bitcoin primer).

Let’s start with the facts: Bitcoin’s value traded below $1,000 at the beginning of this year and hit $11,000 this week before settling around $10,000 at month’s end (see chart below). In addition, blogger Josh Brown points out the scary reality that “Bitcoin has already crashed by -80% on five separate occasions over the last few years.” Suffice it to say, transacting in a currency that repeatedly loses 80% of its value can pose some challenges.

Source: CoinMarketCap.com

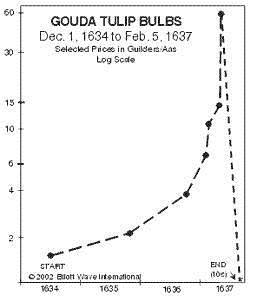

Bubbles are not a new phenomenon. Not only have I lived through numerous bubbles, but I have also written on the topic (see also Sleeping and Napping through Bubbles). I find the Dutch Tulip Bulb Mania that lasted from 1634 – 1637 to be the most fascinating financial bubble of all (see chart below). At the peak of the euphoria, individual Dutch tulip bulbs were selling for the same prices as homes ($61,700 on an inflation-adjusted basis), and one historical account states 12 acres of land were offered for a single tulip bulb.

Forecasting the next peak of any speculative bubble is a fool’s errand in my mind, so I choose to sit on the sidelines instead. While I may be highly skeptical of the ethereal value placed on Bitcoin and other speculative markets (i.e. ICOs – Initial Coin Offerings), I fully accept the benefits of the digital blockchain payment technology and also acknowledge Bitcoin’s value could more than double from here. However, without any tangible or intellectual process of valuing the asset, history may eventually place Bitcoin in the same garbage heap as the 1630 tulips.

For some of you out there, if you are anything like me, your digestion system is still recovering from the massive quantities of food consumed over the Thanksgiving holiday. However, when it comes to your personal finances, digesting record-breaking stock performance, shifting Federal Reserve monetary policy, tax legislation, and volatile digital currencies can cause just as much heartburn. In the spirit of “giving”, if you are having difficulty in chewing through all the cryptic economic and political noise, “give” yourself a break by contacting an experienced, independent, professional advisor. That’s definitely a gift you deserve!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Trump: Bark Worse Than the Bite?

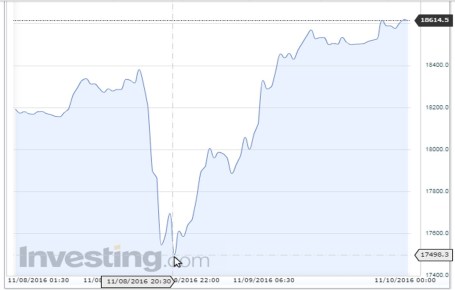

Unless you have been living in a cave this week, you are probably aware the country has elected a new president. Leading up to Election Day, the anxiety was palpable. A populist wave, much like the one experienced in the British Brexit vote earlier this year, resulted in economically disenfranchised voters coming out in full force to vote out the perceived establishment candidate, Hillary Clinton. Financial market pundits and media commentators predicted an immediate 11-13% decline in stock values if Donald Trump were to win. Could they have been more wrong? After a brief -5% decline in pre-trading Dow Jones Industrial Average future prices, the Dow subsequently skyrocketed more than 1,000 points higher to finish up +1.4% for the day (see chart below). For the week, the Dow amazingly rallied by +5.4%.

Source: Investing.com

As I have written on numerous occasions, politics have very little impact on the long-term direction of the financial markets. Yes, it is true that regulations and policies implemented by the president and Congress can influence specific industries or individual companies over the short-run. Hillary Clinton proved this assertion with her pharmaceutical industry tweet, which created a lasting hangover effect on the sector. But guess what? Regulations and politics have always changed throughout our country’s history, with various shifting policies impacting businesses asymmetrically – some positively and some negatively. The good news…in an ever-expanding global economy, accelerated through technology, capitalism forces businesses to adapt to political change.

Considering the amount of our nation’s political variation, what has been our country’s stock market and economic track record over the last 100 years under 17 different presidents (8 Democrats and 9 Republicans)? See chart below:

Source: Macrotrends

Not too shabby judging by the roughly 188x–fold increase in the Dow Jones Industrial Average (or > ~18,700%+ return) to a fresh all-time record high this week. While I am admittedly nervous about a full, Republican tri-power Trump administration (President/House/Senate), the reality is that Trump’s unconventional, unprecedented platform doesn’t fit squarely into the traditional Republican policy boxes. In fact, he has switched his party affiliation five times. President-elect Trump will therefore need to reach across the political aisle to Democrats, and work with Speaker of the House Paul Ryan to accomplish the platform agenda priorities he outlined during his presidential campaign.

While all this political election discussion has been stimulating and exhausting, fortunately, followers of my Investing Caffeine blog understand there are much more important factors than politics affecting the performance of the stock market and economy – namely corporate profits, interest rates, valuations, and sentiment (see Don’t Be a Fool, Follow the Stool).

As mentioned, the market’s returns are influenced by four key factors, but sentiment and stock market values are largely shaped by investor behavior. Trump has less control on investor behavior, but his policies can directly impact corporate profits and interest rates – two critical components of economic health. Part of the reason Trump won the election was due to campaign promises regarding many popular stimulative policies, including personal and corporate tax cuts; infrastructure spending; repatriation of foreign money; tax simplification and reform; Obamacare improvement; and immigration reform.

As it turns out, a good number of the issues relating to these policies happen to be bipartisan in nature. Given the Republican-controlled Congress, investors are perceiving these potential policy changes as positive for the market – at least for the first week of his presidential tenure.

For now, President-elect Trump has struck the proper conciliatory tone and made appropriate comments. In the coming days and weeks, investors are watching closely for tangible evidence and clues of his policy priorities, as he fills key political posts on his presidential team. Time will tell whether the early honeymoon will continue past Trump’s inauguration day, but currently, the consensus is his bark heard during Trump’s heated 18-month presidential campaign is worse than the actual bite of his election victory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

{kind=link}