Posts tagged ‘sports’

Stocks Winning vs. Weak Competitors

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (June 2, 2014). Subscribe on the right side of the page for the complete text.

Winning at any sport is lot easier if you can compete without an opponent. Imagine an NBA basketball MVP LeBron James driving to the basket against no defender, or versus a weakling opponent like a 44-year-old investment manager. Under these circumstances, it would be pretty easy for James and his team, the Miami Heat, to victoriously dominate without even a trace of sweat.

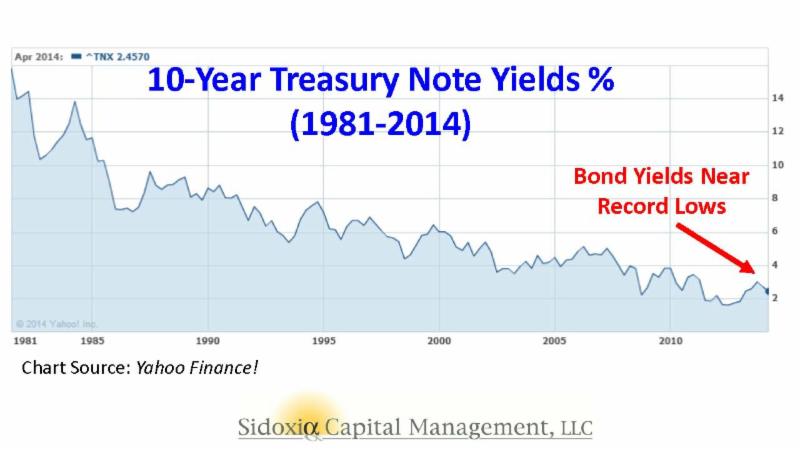

Effectively, stocks have enjoyed similar domination in recent years, while steamrolling over the bond competition. To put the stock market’s winning streak into perspective, the S&P 500 index set a new all-time record high in May, with the S&P 500 advancing +2.1% to 1924 for the month, bringing the 2013-2014 total return to about +38%. Not too shabby results over 17 months, if you consider bank deposits and CDs are paying a paltry 0.0-1.0% annually, and investors are gobbling up bonds yielding a measly 2.5% (see chart below).

The point, once again, is that even if you are a skeptic or bear on the outlook for stocks, the stock market still offers the most attractive opportunities relative to other asset classes and investment options, including bonds. It’s true, the low hanging fruit in stocks has been picked, and portfolios can become too equity-heavy, but even retirees should have some exposure to equities.

As I wrote last month in Buy in May and Dance Away, why would investors voluntarily lock in inadequate yields at generational lows when the earnings yield on stocks are so much more appealing. The approximate P/E (Price-Earnings) ratio for the S&P 500 currently averages approximately +6.2% with a rising dividend yield of about +1.8% – not much lower than many bonds. Over the last five years, those investors willing to part ways with yield-less cash have voted aggressively with their wallets. Those with confidence in the equity markets have benefited massively from the approximate +200% gains garnered from the March 2009 S&P 500 index lows.

For the many who have painfully missed the mother of all stock rallies, the fallback response has been, “Well, sure the market has tripled, but it’s only because of unprecedented printing of money at the QE (Quantitative Easing) printing presses!” This argument has become increasingly difficult to defend ever since the Federal Reserve announced the initiation of the reduction in bond buying (a.k.a., “tapering”) six months ago (December 18th). Over that time period, the Dow Jones Industrial Average has increased over 800 points and the S&P 500 index has risen a healthy 8.0%.

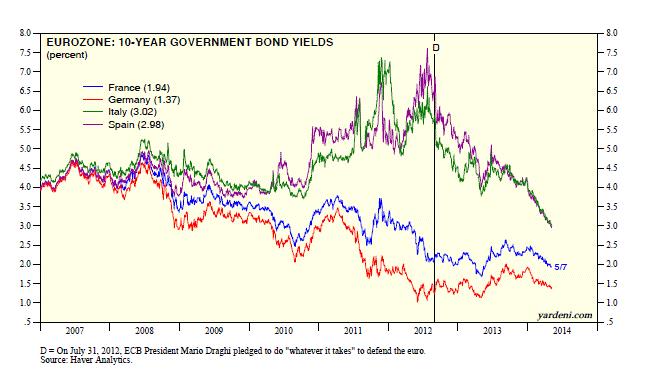

As much as everyone would like to blame (give credit to) the Fed for the bull market, the fact is the Federal Reserve doesn’t control the world’s interest rates. Sure, the Fed has an influence on global interest rates, but countries like Japan may have something to do with their own 0.57% 10-year government bond yield. For example, the economic/political policies and demographics in play might be impacting Japan’s stock market (Nikkei), which has plummeted about -62% over the last 25 years (about 39,000 to 15,000). Almost as shocking as the lowly rates in Japan and the U.S. and Japan, are the astonishingly low interest rates in Europe. As the chart below shows, France and Germany have sub-2% 10-year government bond yields (1.76% and 1.36%, respectively) and even economic basket case countries like Italy and Spain have seen their yields pierce below the 3% level.

Source: Dr. Ed’s Blog

Source: Dr. Ed’s Blog

Suffice it to say, yield is not only difficult to find on our shores, but it is also challenging to find winning bond returns globally.

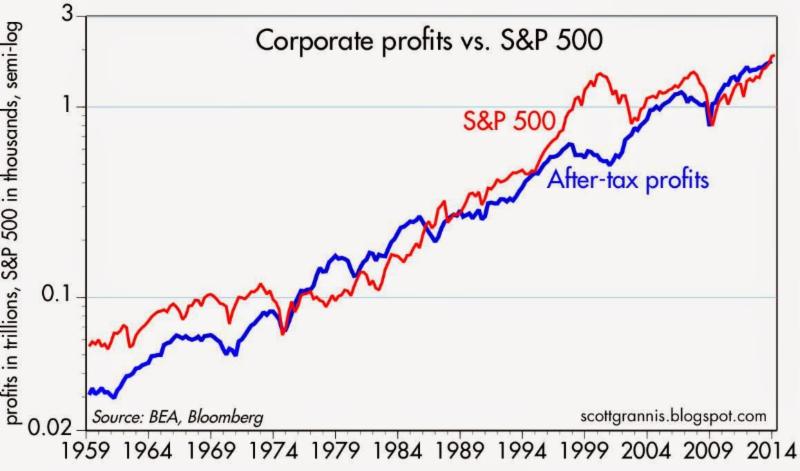

Well if low interest rates and the Federal Reserve aren’t the only reasons for a skyrocketing stock market, then how come this juggernaut performance has such long legs? The largest reason in my mind boils down to two words…record profits. Readers of mine know I follow the basic tenet that stock prices follow earnings over the long-term. Interest rates and Fed Policy will provide headwinds and tailwinds over different timeframes, but ultimately the almighty direction of profits determines long-run stock performance. You don’t have to be a brain surgeon or rocket scientist to appreciate this correlation. Scott Grannis (Calafia Beach Pundit) has beautifully documented this relationship in the chart below.

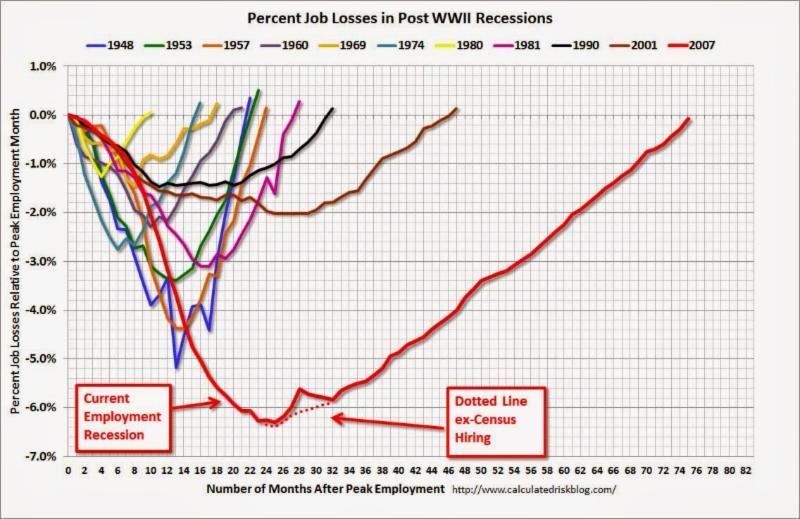

Supporting this concept, profits help support numerous value-enhancing shareholder activities we have seen on the rise over the last five years, which include rising dividends, share buybacks, and M&A (Mergers & Acquisitions) activity. Eventually the business cycle will run its course, and during the next recession, profits and stock prices will be expected to decline. A final contributing factor to the duration of this bull market is the abysmally slow pace of this economic recovery, which if measured in job creation terms has been the slowest since World War II. Said differently, the slower a recovery develops, the longer the recovery will last. Bill McBride at Calculated Risk captured this theme in the following chart:

Despite the massive gains and new records set, skeptics abound as evidenced by the nearly -$10 billion of withdrawn money out of U.S. stock funds over the last month (most recent data).

I’ve been labeled a perma-bull by some, but over my 20+ years of investing experience I understand the importance of defensive positioning along with the benefits of shorting expensive, leveraged stocks during bear markets, like the ones in 2000-2001 and 2008-2009. When will I reverse my views and become bearish (negative) on stocks? Here are a few factors I’m tracking:

- Inverted Yield Curve: This was a good precursor to the 2008-2009 crash, but there are no signs of this occurring yet.

- Overheated Fund Inflows: When everyone piles into stocks, I get nervous. In the last four weeks of domestic ICI fund flow data, we have seen the opposite…about -$9.5 billion outflows from stock funds.

- Peak Employment: When things can’t get much better is the time to become more worried. There is still plenty of room for improvement, especially if you consider the stunningly low employment participation rate.

- Fed Tightening / Rising Bond Yields: The Fed has made it clear, it will be a while before this will occur.

- When Housing Approaches Record Levels: Although Case-Shiller data has shown housing prices bouncing from the bottom, it’s clear that new home sales have stalled and have plenty of head room to go higher.

- Financial Crisis: Chances of experiencing another financial crisis of a generation is slim, but many people have fresh nightmares from the 2008-2009 financial crisis. It’s not every day that a 158 year-old institution (Lehman Brothers) or 85 year-old investment bank (Bear Stearns) disappear, but if the dominoes start falling again, then I guess it’s OK to become anxious again.

- Better Opportunities: The beauty about my practice at Sidoxia is that we can invest anywhere. So if we find more attractive opportunities in emerging market debt, convertible bonds, floating rate notes, private equity, or other asset classes, we have no allegiances and will sell stocks.

Every recession and bear market is different, and although the skies may be blue in the stock market now, clouds and gray skies are never too far away. Even with record prices, many fears remain, including the following:

- Ukraine: There is always geopolitical instability somewhere on the globe. In the past investors were worried about Egypt, Iran, and Syria, but for now, some uncertainty has been created around Ukraine.

- Weak GDP: Gross Domestic Product was revised lower to -1% during the first quarter, in large part due to an abnormally cold winter in many parts of the country. However, many economists are already talking about the possibility of a 3%+ rebound in the second quarter as weather improves.

- Low Volatility: The so-called “Fear Gauge” is near record low levels (VIX index), implying a reckless complacency among investors. While this is a measure I track, it is more confined to speculative traders compared to retail investors. In other words, my grandma isn’t buying put option insurance on the Nasdaq 100 index to protect her portfolio against the ramifications of the Thailand government military coup.

- Inflation/Deflation: Regardless of whether stocks are near a record top or bottom, financial media outlets in need of a topic can always fall back on the fear of inflation or deflation. Currently inflation remains in check. The Fed’s primary measure of inflation, the Core PCE, recently inched up +0.2% month-to-month, in line with forecasts.

- Fed Policy: When are investors not worried about the Federal Reserve’s next step? Like inflation, we’ll be hearing about this concern until we permanently enter our grave.

In the sport of stocks and investing, winning is never easy. However, with the global trend of declining interest rates and the scarcity of yields from bonds and other safe investments (cash/money market/CDs), it should come as no surprise to anyone that the winning streak in stocks is tied to the lack of competing investment alternatives. Based on the current dynamics in the market, if LeBron James is a stock, and I’m forced to guard him as a 10-year Treasury bond, I think I’ll just throw in the towel and go to Wall Street. At least that way my long-term portfolio has a chance of winning by placing a portion of my bets on stocks over bonds.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing: Coin Flip or Skill?

The Sidoxia Monthly Newsletter will be released in a few days (subscribe on right side of the page), so here is an Investing Caffeine classic to tide you over until then:

Everyone believes they are above-average drivers and most investors believe successful investing can be attributed to skill. Michael Mauboussin, author and Chief Investment Strategist at Legg Mason Capital Management, tackles the issue of how important a role luck plays in various professional activities, including investing (read previous IC article on Mauboussin) in his meaty 42-page thought piece, Untangling Skill and Luck.

Skill Litmus Test

Whenever someone becomes successful or a sports team wins, doubters often respond with the response, “Well, they are just lucky.” For some, the intangible factor of luck can be difficult to measure, but for Mauboussin, he has a simple litmus test to evaluate the level of skill and luck credited to a professional activity:

“There’s a simple and elegant test of whether there is skill in an activity: ask whether you can lose on purpose. If you can’t lose on purpose, or if it’s really hard, luck likely dominates that activity. If it’s easy to lose on purpose, skill is more important.”

Mauboussin uses various sports and games as tools to explain the relative importance that skill (or lack thereof) plays in determining an outcome. At one extreme end of the spectrum you have a brain game like chess, in which a skillful chess pro could beat an amateur 1,000 times in a 1,000 matches. In the field of professional sports, at the other end of the spectrum, Mauboussin hammers home the relative significance luck contributes in professional baseball:

“In major league baseball the worst team will beat the best team in a best-of-five series about 15 percent of the time.“

Here is a skill-luck continuum provided by Mauboussin:

Source: Legg Mason Capital Management

Streaks vs. Mean Reversion

Mr. Mauboussin spends a great deal of time exploring the implications of skill and luck in relation to streaks and mean reversion. In the streak department, Mauboussin uses Joe DiMaggio’s record 56-consecutive game hitting stretch. He acknowledges the presence of luck, but skill is a prerequisite:

“Not all skillful performers have streaks, but all long streaks of success are held by skillful performers.”

When detailing streaks, Mauboussin may also be defending his fellow Legg Mason colleague Bill Miller (see Revenge of the Dunce), who had an incredible 15 consecutive year of besting the S&P 500 index before mean reverting back to lousy human-like returns.

This is a nice transition into his discussion about mean reversion because Mauboussin basically states this reversion concept dominates activities laden with luck (as shown in the Skill-Luck Continuum chart above). Time will tell whether Miller’s streak was due to skill, if he can put together another streak, or whether his streak was merely a lucky fluke. Unlike the judicial world, investment managers are often treated as guilty until proven innocent. For now, Miller’s 1991-2005 streak is being treated as luck by many in the investment community, rather than skill.

Nobel-prize winner Paul Samuelson may believe differently since he concedes the existence of skillful investing:

“It is not ordained in heaven, or by the second law of thermodynamics, that a small group of intelligent and informed investors cannot systematically achieve higher mean portfolio gains with lower average variabilities. People differ in their heights, pulchritude, and acidity. Why not their P.Q. or performance quotient?”

Peter Lynch’s +29% annual return from 1977-1990 is another streak on which historians can chew (read more on Lynch). I, like Samuelson, will give Lynch the benefit of the doubt.

Creating a Skillful Analytical Edge

Unlike the process of mowing lawns, in which more applied work time generally equates to more lawns cut (i.e., more profits), the investment world doesn’t quite work that way. Many people could work all day, stare at their screen for 23 hours, trade off of useless information, and still earn lousy returns. When it comes to investing, more work does not necessarily produce better results. Mauboussin’s prescription is to create an analytical edge. Here is how he describes it:

“At the core of an analytical edge is an ability to systematically distinguish between fundamentals and expectations.”

Thinking like a handicapper is imperative to win in this competitive game, and I specifically addressed this in my previous Vegas-Wall Street article. Steven Crist sums up this indispensable concept beautifully:

“There are no “good” or “bad” horses, just correctly or incorrectly priced ones.”

A disciplined, systematic approach will incorporate these ideas, however all good investors understand the good processes can lead to bad outcomes in the short-run. By continually learning from mistakes, and refining the process with a constant feedback loop, the investment process can only get better. On the other hand, schizophrenically reacting to an endless flood of ever-changing information, or fearfully chasing the leadership du jour will only lead to pain and sorrow. Fortunately for you, you have skillfully completed this article, meaning financial luck should now be on your side.

Read full Mauboussin article (Untangling Skill and Luck) here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. Radio interviews included opinions of Wade Slome – not advice. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Top 10 (or so) Things I’m Thankful For

With the holidays now upon us, this period provides me the opportunity to briefly escape the daily investment rat race, and reflect on the numerous aspects of my life for which I am grateful. There is so much to be thankful for, but it’s easy to lose sight of what’s important, especially when time is flying by in the blink of an eye. As the old saying goes, “Life is like a roll of toilet paper. The closer you get to the end, the faster it goes.” The proliferation of gray hair, coupled with my sprouting kids, is a constant reminder that life is not slowing down for me, but actually speeding up.

As I lay here like a slug on the couch, which is slowly absorbing me, I take no shame in unbuttoning my top pant button to relieve the belly-busting pressure of excessive turkey and mash potato consumption. The cranberry sauce on my chin and pumpkin pie crust on my shirt does not distract me from the football game or prevent me from reflecting upon my life’s gifts.

In that vein, here is a list of my top 10 things for which I am grateful:

10. Sugar: Without sweets, being relegated to a life of bread, water, and broccoli would be a boring challenge. Thankfully, once I became a grown adult earning a paycheck, I also earned the right to eat Cap’n Crunch (with Crunch Berries) for breakfast; peanut butter-Nutella & banana sandwich for lunch; apple fritter & milk for dinner; and some Double Stuf Oreos for dessert (yes, only one ‘f’ in Stuf!).

9. College Sports: Watching professional sports is fun, but when A-Rod earns $275 million for the NY Yankees and rides the pine during the playoffs, the business aspects take a little allure away from the sport. Although college athletes may sneak a few bucks under the table, they are nonetheless a lot less corrupted, and the electric atmosphere of a live college event cannot be replicated. The opportunities are fewer due to adult responsibilities, but nothing beats a crisp fall afternoon on the couch with a bowl of hot chili, a frosty beverage, and a remote control, while flipping through a series of college football games.

8. Gadgets: Seems like yesterday when I was introduced to my first computer, a 1983 Compaq Portable computer that weighed 28 pounds; had a 9 inch green screen; integrated two 320k drives; and retailed originally for about $3,500….ouch! Today, my iPhone 5 is more than 99% lighter, stores 100,000 times more information, and costs a fraction of the price. If you add my iPad, Kindle, Roku video streaming box, my DVR set-top box, my GPS, and other electronic gadgets, it’s hard to imagine how I could have lived a life without these luxuries five years ago.

7. Cards: I analyze numbers, probabilities, and emotions in my day job every day, it’s no wonder that I somehow need to do the same thing in my leisure time. No-Limit Texas Hold ‘Em is the name of the game, and I was introduced to it by world champion “poker brat” Phil Helmuth when he personally taught a group of us at an investment conference in 2003. I haven’t entered the $10,000 World Series of Poker in Las Vegas yet, but it’s on my bucket list.

6. Challenges: I’m a washed up basketball hack after an insignificant high school career and about 12 years of old-man basketball leagues, but my competitive juices keep flowing today. In hopes of not turning to a fully gelatinous blob, I have periodically pushed myself to some competitive athletic challenges, including a hike to the peak of Mt. Whitney; a couple half marathons; a sprint triathlon; a Colorado bike trip; and a few seasons of indoor co-ed soccer. Next up, I’m training for a “century” bike ride – a 100 mile race in early 2013 near Santa Barbara. I guess I better work off some of that stuffing, mash potatoes, and gravy.

5. Good Books: I pretty much read for a living on average 8-12 hours per day, but I suppose I’m a glutton for punishment. Given all my other interests and responsibilities, it’s tough to find the free time to curl up to a good book, but if I can squeeze in a book every quarter, I give myself a pat on the back. Nothing beats true, real-life experiences, but I’ve learned a tremendous amount through all the books I’ve read (for leisure and schooling). Regrettably diversity has gotten the short end of the stick, since about half the books I read are investment related, including a few that I’ve reviewed here on my blog like The Big Short, Too Big to Fail, The Greatest Trade Ever, and Winning the Loser’s Game (to name a few). Currently, I’m reading a fascinating New York Times Bestseller on world religions, called Religious Literacy, which leads me to my next Top 10 item…

4. Spirituality: While I am probably a lot more apathetic and ignorant in the area of religion as compared to the average person, nevertheless I have learned to appreciate the importance and benefits of religion and spirituality through my life experiences. From Judaism to Islam, and Buddhism to Christianity, there is no denying the moral lessons and spiritual balance these religions provide billions of people around the globe. I have a long way to go on my spiritual journey, but I’m slowly learning and progressing. On days where the Dow plummets a few hundred points or when the share price of a top holding tanks, I’m quickly reminded of the importance of spiritual balance.

3. Travel: While many people have hardly ventured from their hometown during their lifetime, I have been blessed with the fortune of seeing many places around the world. Not only have I lived on the East Coast, West Coast, and in the Midwest, but I have also traveled to five different continents. Appreciating different cultures and viewpoints is what truly makes life more interesting for me.

2. Friends: The digital age has not only brought friends closer together through social networks like Facebook (FB) and LinkedIn (LNKD), but has also pushed us further apart because vicariously spying on someone online is much easier than calling someone or grabbing coffee with them. Thankfully, I have a core set of friends that I can share my life’s ups and downs.

1a. Investing: Enough said. I’ve been investing for close to 20 years, and this blog is evidence of the blood, sweat, and tears I’ve dedicated to this endeavor. Various investments will go in and out of favor, and economic cycles will go up and down, but one trend that I know will persist is that I will be investing for the rest of my life.

1b. Health: It goes without saying, but if I don’t have my own good health, then very little on my top 10 list is possible. I’ve outlived two close family members of mine, so needless to say, I am very thankful to be breathing and living.

1c. Family: Having all these great experiences, including al the highs and lows, means absolutely nothing, if you have nobody to share them with. My family means the world to me, and days like Thanksgiving remind me of how lucky I really am.

Although this list was originally scheduled for 10 items, it looks like it has unintentionally expanded to a few more. But how can you blame me? I’ve had some tough times like everyone, but it is virtually impossible to not be thankful for the life I get to live now. Not only do I get to do what I love, but I also get paid to do it.

Last but not least, a special thanks needs to also go out to you, my devoted blog reader. I know you’re devoted, because you have made it to the end of this lengthy article. Without you, I wouldn’t have the motivation to continually scribble down my random thoughts.

Happy Thanksgiving and happy holidays!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AMZN, and AAPL, and a short position in NFLX. At the time of publishing SCM had no direct positions in LNKD, FB, HPQ or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What Happens in Vegas, Stays on Wall Street

What happens in Vegas, stays in Vegas, unless it’s a habit of betting, in which case that habit will follow you back to Wall Street. Just as there are a million ways to make or lose money by investing or speculating in the market, the same principles apply to sports betting as well. Anybody who has been to Las Vegas and gone to the sportsbook knows how incredibly and insanely accurate the oddsmakers are – I speak from immature experience having traveled there for a healthy number of investment conferences and vacations. The oddsmakers are so accurate; you could say they are almost “efficient” at what they do.

But like the market, in the sports world too, efficiency has a tendency to breakdown occasionally and form bubbles. This dynamic leaves both a huge threat of substantial losses and a potential for windfall gains. Where there are bubbles forming, you are bound to find a large number of excited individuals jumping on a bandwagon. Now, let’s take a look at how the worlds of Wall Street and wagers collide and see if any lessons can be learned.

Jumping on the Stock Bandwagon

band·wag·on [band-wag-uhn]: a party, cause, movement, etc., that by its mass appeal or strength readily attracts many followers.

Photo source: Freshpics.blogspot.com

Everybody loves a winner and no one more so than a fresh fan jumping on the bandwagon. Living in Southern California, the bandwagon is presently fully-loaded with proclaimed Los Angeles Laker fans and USC fans, although the Trojan wagon is currently undergoing repair. It’s easy to identify bandwagoners in sports – just find the face painter, guy with a rainbow afro, Boston native sporting a Kobe Bryant jersey, or the fanatic betting on the team favored by three touchdowns. In the game of stocks, identifying the fickle but passionate followers is a little more subtle. Bandwagon status is not measured by the extent of point spreads (predicted scoring differential between two opponents), but rather by level of P/E ratios (Price-Earnings ratio) or other valuation metric of choice.

While it is clear sports bandwagoners root for the “favorites,” in the realm of investing this translates into piling onto the “growth or momentum” stocks (see Momentum Investing article) – I hate generalizing terms but that’s what we bloggers do. Value investors, on the other hand, root for (buy) the “underdogs.”

To illustrate my point, let’s take a look at a few past bandwagon momentum stocks:

- JDS Uniphase Corp. (JDSU): In 2000 we saw these bandwagoners valuing investor favorites like JDS Uniphase at a whopping $99 billion – meaning investors were willingly paying over 100x’s revenues and 600 x’s trailing earnings to own the stock. At the time, JDSU was a “New Economy” stock that was going to revolutionize the proliferation of bandwidth around the globe with their proprietary optical laser components. For those of you keeping score at home, today JDSU’s stock is valued at approximately $2 billion ($9.97), or -98% less than the market value in March 2000 (split-adjusted peak share price of $1,227.38 per share). If it wasn’t for a 1-for-8 reverse stock split in 2006, then a share of JDSU would fetch you $1.25 today, or less than the amount needed to cover an out of network ATM penalty fee.

- Crocs Inc. (CROX): Crox is another one of my favorite bandwagon stocks, because this loud plastic eyesore footwear was clearly a fad that couldn’t sustain its growth once popularity waned, despite my wife being a bandwagon-ee. Like other fad product-related stocks, the company could no longer maintain its growth once they completed stuffing the channel and their customers cried uncle from choking on inventory. Making matters worse for CROX, knockoff versions were offered for a fraction of the cost at local grocery stores and mall kiosks. After about 20 months post its IPO (Initial Public Offering), the music stopped and within 13 months the stock cratered from a $75 per share peak to $0.79 in 2008. The stock never traded at the absurd dot-com levels, but the lofty 37x P/E in 2007 quickly turned negative after close to $200 million in losses were realized in 2008 and 2009. The stock has since rebounded to $12 and change, and maybe their new Crocs high-heel line of $99.00 shoes (see here) will propel the stock higher…cough, cough.

Point Spread, Point Spread, Point Spread

In sports betting the three most important factors in making a winning bet are point spread, point spread, and point spread. Unlike the March Madness college basketball pool in which you may have participated, in the real world the participant needs to do more than just pick the winning teams – the participant must determine by how much a team will win by. Let’s take a gander at a few actual examples.

- Florida Gators vs. Charleston Southern Buccaneers (9/5/09): Without knowing a lot about the powerhouse squad from South Carolina, 99% of respondents, when asked before the game who would win, would select Florida – a consistently dominant national-powerhouse program. The question gets a little trickier when asked the question: “Will the Florida Gators win by more than 63 points?” That’s exactly the point spread sports bettors faced when deciding whether or not to place the bet – somewhat analogous to the question whether JDSU was a prudent investment at 600x’s earnings? Needless to say, although the Buccs kept it close in the first half, and only trailed by 42-3 at halftime, the Gators still managed to squeak by with a 62-3 victory. Worth noting, the 59 point margin of victory resulted in a losing wager for anyone picking the Gators.

- USC Trojans vs. Stanford Cardinal (10/6/2007): Ranked as the presumptive #1 team of the country pre-season, and entering the game with a 35-0 home-game winning streak, USC was a whopping 41 point favorite over Stanford. On the flip side, the Cardinal came into the game fresh off of a 1-11 losing season the prior year, and in the previous year the Cardinal lost to the Trojans 42-0. Stanford ended up winning the 2007 match-up by a score of 24-23, not only pulling off one of the greatest upsets of all-time, but also spoiling USC’s chances of winning the national championship.

Read more about the greatest upsets of all-time.

Beyond the Point Spread

As you can surmise from our discussion, the same point spread standards apply to investing, but when discussing stocks the spread is measured by various valuation metrics based on earnings, cash flows, book value, EBITDA, sales, and other fundamental growth factors.

Of course, in Las Vegas and on Wall Street not everyone follows traditional fundamental analysis. Some gamblers and speculators will transact solely based on less conventional methods, for example quantitative models, technical analysis and trend review (read Technical Analysis: Astrology or Lob Wedge). For example in sports, handicappers may only wager on teams with five-game winning streaks and winning home records. Whereas on Wall Street, speculators may only trade stocks with positive earnings surprises or “head-and-shoulder” patterns. Hot technicians come and go, but very few real investors survive the long haul without using fundamental analysis and valuation as key components of their winning strategies.

As I have argued, there are many ways to make (and lose) money on Wall Street or in Las Vegas, and consistently jumping on the bandwagon is a sure way to lose. For the successful minority whose performance has endured the test of time, a common thread connecting the two disciplines is the ability to determine and profit from a prudently calculated point spread/valuation. History teaches us that the same effective handicapping skills happening in Las Vegas are the same abilities needed to stay on Wall Street and win.

Wade W. Slome, CFA, CFP®

P.S. See how a pro handicapper conquered Las Vegas and placed sportsbooks on the run.

Plan. Invest. Prosper.

*DISCLOSURE: The undergraduate alma mater of Sidoxia Capital Management’s (SCM) President happens to be UCLA, so although I believe any reference to rival school USC is not provided with any malicious agenda, nonetheless there may exist an inherent conflict of interest. SCM and some of its clients own certain exchange traded funds, but at the time of publishing, SCM had no direct position in JDSU, CROX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sports & Investing: Why Strong Earnings Can Hurt Stock Prices

There are many similarities between investing in stocks and handicapping in sports betting. For example, investors (bettors) have opposing views on whether a particular stock (team) will go up or down (win or lose), and determine if the valuation (point spread) is reflective of the proper equilibrium (supply & demand). And just like the stock market, virtually anybody off the street can place a sports bet – assuming one is of legal age and in a legal betting jurisdiction.

Right now investors are poring over data as part of the critical, quarterly earnings ritual. Thus far, roughly 20% of the companies in S&P 500 index have reported their results and 78% of those companies have beaten Wall Street expectations (CNBC). Unfortunately for the bulls, this trend has not been strong enough to push market prices higher in 2010.

So how and why can market prices go down on good news? There are many reasons that short-term price trends can diverge from short-run fundamentals. One major reason for the price-fundamental gap is the following factor: expectations. Just last week, the market had climbed over +70% in a ten month period, before issues surrounding the Massachusetts Senatorial election, President Obama’s banking reform proposals, and Federal Reserve Bank Chairman Ben Bernanke’s re-appointment surfaced. With such a large run-up in the equity markets come loftier expectations for both the economy and individual companies. So when corporate earnings unveiled from companies like Google (GOOG), J.P. Morgan (JPM), and Intel (INTC) outperform relative to forecasts, one explanation for an interim price correction is due to a significant group of investors not being surprised by the robust profit reports. In sports betting lingo, the sports team may have won the game this week, but they did not win by enough points (“cover the spread”).

Some other reasons stock prices move lower on good news:

- Market Direction: Regardless of the underlying trends, if the market is moving lower, in many instances the market dip can overwhelm any positive, stock- specific factors.

- Profit Taking: Many times investors holding a long position will have price targets or levels, if achieved, that will trigger selling whether positive elements are in place or not.

- Interest Rates: Certain valuation techniques (e.g. Discounted Cash Flow and Dividend Discount Model) integrate interest rates into the value calculation. Therefore, a climb in interest rates has the potential of lowering stock prices – even if the dynamics surrounding a particular security are excellent.

- Quality of Earnings: Sometimes producing winning results is not enough (see also Tricks of the Trade article). On occasion, items such as one-time gains, aggressive revenue recognition, and lower than average tax rates assist a company in getting over a profit hurdle. Investors value quality in addition to quantity.

- Outlook: Even if current period results may be strong, on some occasions a company’s outlook regarding future prospects may be worse than expected. A dark or worsening outlook can pressure security prices.

- Politics & Taxes: These factors may prove especially important to the market this year, since this is a mid-term election year. Political and tax policy changes today may have negative impacts on future profits, thereby impacting stock prices.

- Other Exogenous Items: Natural disasters and security attacks are examples of negative shocks that could damage price values, irrespective of fundamentals.

Certainly these previously mentioned issues do not cover the full gamut of explanations for temporary price-fundamental gaps. Moreover, many of these factors could be used in reverse to explain market price increases in the face of weaker than anticipated results.

For those individuals traveling to Las Vegas to place a wager on the NFL Super Bowl, betting on the hot team may not be enough. If expectations are not met and the hot team wins by less than the point spread, don’t be surprised to see a decline in the value of the bet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and GOOG, but at the time of publishing had no direct positions in JPM and INTC. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}