Posts tagged ‘Spending’

Cash Is Trash

The S&P 500 stock market index took a breather and ended its six-month winning streak, declining -4.8% for the month. Even after this brief pause, the S&P has registered a very respectable +14.7% gain for 2021, excluding dividends. Nevertheless, even though the major stock market indexes are roaming near all-time record highs, FUD remains rampant (Fear, Uncertainty, Doubt).

As the 10-Year Treasury Note yield has moved up to a still-paltry 1.5% level this month, the talking heads and peanut gallery bloggers are still fretting over the feared Federal Reserve looming “tapering”. More specifically, Jerome Powell, the Fed Chairman and the remainder of those on the FOMC (Federal Open Market Committee) are quickly approaching the decision to reduce monthly bond purchases (i.e., “tapering”). The so-called, quantitative easing (QE) program is currently running at about $120 billion per month, which was established with the aim to lower interest rates and stimulate the economy. Now that the COVID recovery is well on its way, the Fed is effectively trying to decrease the size of the current, unruly punch-keg down to the volume of a more manageable punch bowl.

Stated differently, even when the arguably overly-stimulative current bond buying slows or stops, the Federal Funds Rate is still effectively set at 0% today, a level that still offers plenty of accommodative fuel to our economy. Although interest rates will not stay at 0% forever, many people forget that between 2008 and 2015, the Fed Funds Rate stubbornly stayed sticky at 0% (i.e., a full punch bowl) for seven years, even without any spike in inflation.

Because the economy continues to improve, current consensus projections by economists show the first interest rate increase of this cycle (i.e., “liftoff”) to occur sometime in 2022 and subsequently climb to a still extraordinarily low level of 2.0% by 2024 (see “Dot Plot” below). For reference, the projected 2.0% figure would still be significantly below the 6.5% Fed Funds Rate we saw in the year 2000, the 5.3% in 2007, or the 2.4% in 2019. If history is any guide, under almost any scenario, Chairman Powell is very much a dove and is likely to tap the interest rate hike brakes very gently.

Low But Not the Lowest

In a world of generationally low interest rates, what I describe as our low bond yields here in the United States are actually relatively high, if you consider rates in other major industrialized economies and the trillions of negative-interest-rate bonds littered all over the rest of the world (see August’s article, $16.5 Trillion in Negative-Yielding Debt). Although our benchmark government rates are hovering around 1.5%, as you can see from the chart below, Germany is sitting considerably lower at -0.2%, Japan at 0.1%, France at 0.2%, and the United Kingdom at 1.0%.

Taper Schmaper

As with many government related policies, the Federal Reserve often gets too much credit for successes and too much blame for failures, as it relates to our economy. I have illustrated the extent of how globally interconnected our world of interest rates is, and one taper announcement is unlikely to reverse a four-decade disinflationary declining trend in interest rates.

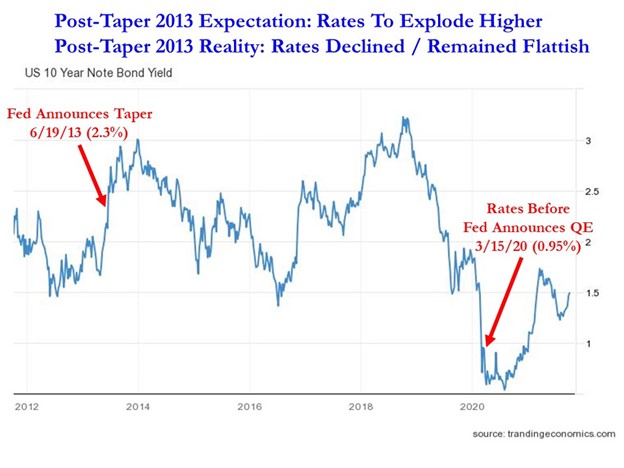

Back in 2013, after of five years of quantitative easing (QE) that began in 2008, investors were terrified that interest rates were artificially being depressed by a money-printing Fed that had gone hog-wild in bond buying. At that time, pundits feared an imminent explosion higher in interest rates once the Fed began tapering. So, what happened after Federal Reserve Chairman Ben Bernanke broached the subject of tapering on June 19, 2013? The opposite occurred. Although 10-Year yields jumped 0.1% to 2.3% on the day of the announcement, interest rates spent the majority of the next six years declining to 1.6% in 2019, pre-COVID. As COVID began to spread globally, rates declined further to 0.95% in March of 2020, the day before Jerome Powell announced a fresh new round of quantitative easing (see chart below).

Obviously, every economic period is different from previous ones, and fearing to fall off the floor to lower interest rate levels is likely misplaced at such minimal current rates (1.5%). However, panicking over potential exploding interest rates, as in 2013 (which did not happen), again may not be the most rational behavior either.

What to Do?

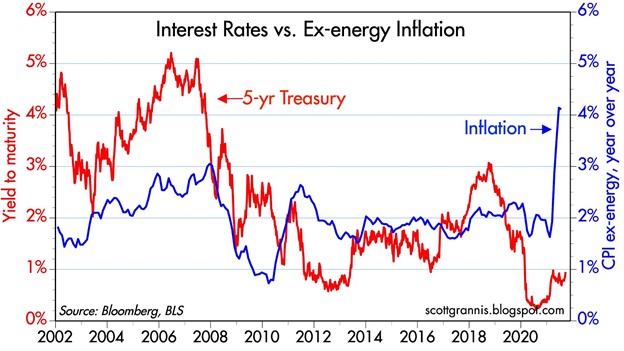

If interest rates are low, and inflation is high (see chart below), then what should you do with your money? Currently, if your money is sitting in cash, it is losing 4-5% in purchasing power due to inflation. If your money is sitting in the bank earning minimal interest, you are not going to be doing much better than that. Everybody’s time horizon and risk tolerance is different, but regardless of your age or anxiety level, you need to efficiently invest your money in a diversified portfolio to counter the insidious, degrading effects of inflation and generationally low interest rates. The “do-nothing” strategy will only turn your cash into trash, while eroding the value of your savings and retirement assets.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

April Flowers Have Investors Cheering Wow-sers!

Normally April showers bring May flowers, but last month the spring weather was dominated by sunshine that caused stock prices to blossom to new, all-time record highs across all major indexes. More specifically, the S&P 500 jumped +5.2% last month, the NASDAQ catapulted +5.4%, and the Dow Jones Industrial Average rose +2.7%. For the year, the Dow and S&P 500 index both up double-digit percentages (11%), while the NASDAQ is up a few percentage points less than that (8%).

What has led to such a bright and beaming outlook by investors? For starters, economic optimism has gained momentum as the global coronavirus pandemic appears to be improving after approximately 16 months. Not only are COVID-19 cases and hospitalizations rates declining, but COVID-19 related deaths are dropping as well. A large portion of the progress can be attributed to the 246 million vaccine doses administered so far in the United States.

Blossoming Economy

As a result of the improving COVID-19 health climate, economic activity, as measured by Gross Domestic Product (GDP), expanded by a healthy +6.4% rate during the first quarter. Economists are forecasting second quarter growth to accelerate to an even more brilliant rate of +10%.

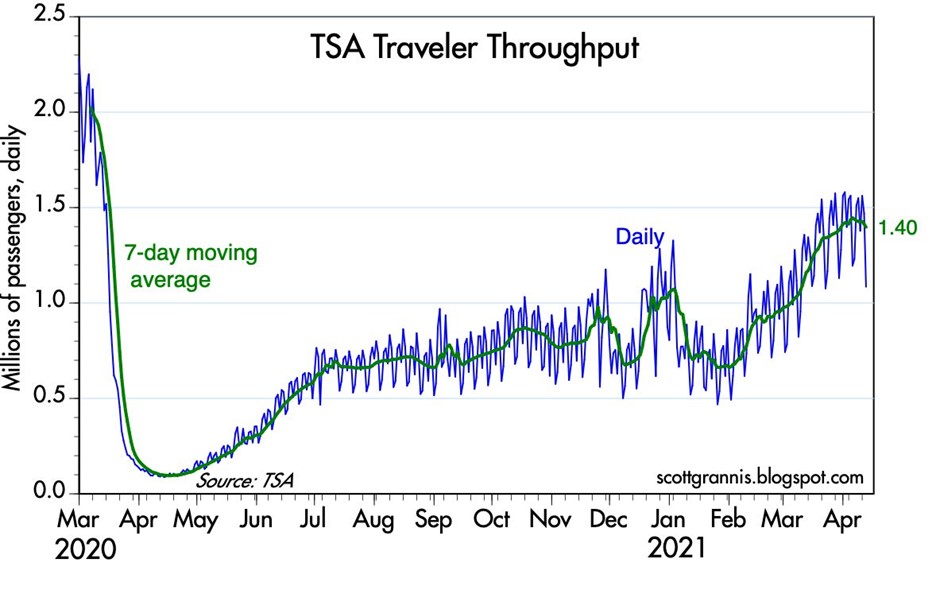

As the economy further re-opens and pent-up consumer demand is unleashed, activity is sprouting up in areas like airlines, hotels, restaurants, bars, movie theaters and gyms. An example of consumer demand climbing can be seen in the volume of passenger traffic in U.S. airports, which has increased substantially from the lows a year ago, as shown below in the TSA (Transportation Security Administration) data.

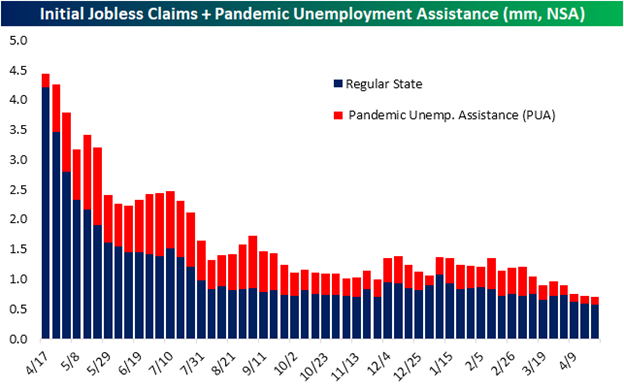

A germinating economy also means a healthier employment market and more jobs. The chart below shows the dramatic decline in the number of jobless receiving benefits and pandemic unemployment assistance.

Fed Fertilizer & Congressional Candy

Monetary and fiscal stimulus are creating fertile ground for the surge in growth as well. The Federal Reserve has been clear in their support for the economy by effectively maintaining its key interest rate target at 0%, while also maintaining its monthly bond buying program at $120 billion – designed to sustain low interest rates for the benefit of consumers and businesses.

From a fiscal perspective, Congress is serving up some sweet candy by doling out free money to Americans. So far, roughly $4 trillion of COVID-19 related stimulus and relief have passed Congress (see also Consumer Confidence Flies), and now President Biden is proposing roughly an additional $4 trillion of stimulus in the form of a $2 trillion jobs and infrastructure plan and a $1.8 trillion American Families Plan.

Candy and Spinach

While Congress is serving up trillions in candy, eventually, Americans are going to have to eat some less appetizing spinach in the form of higher taxes. Generally speaking, nobody likes higher taxes, so the question becomes, how does the government raise the most revenue (taxes) without upsetting a large number of voters? As 17th century French statesman Jean-Baptiste Colbert proclaimed, “The art of taxation consists in so plucking the goose as to get the most feathers with the least hissing.”

President Biden has stated he will only increase income taxes on people earning more than $400,000 annually and increase capital gains taxes for those earning more than $1,000,000 per year. According to CNBC, those earning more than $400,000 only represents 1.8% of total taxpayers.

Bitter tasting spinach for Americans may also come in the form of higher inflation (i.e., a general rise in a basket of goods and services), which silently eats away at everyone’s purchasing power, especially those retirees surviving on a fixed income. Federal Reserve Chairman Jerome Powell sees any increase in inflation as transitory, but if prices keep rising, the Federal Reserve will be forced to increase interest rates. Such a reversal in rates could choke off economic growth and potentially force the economy into a recession.

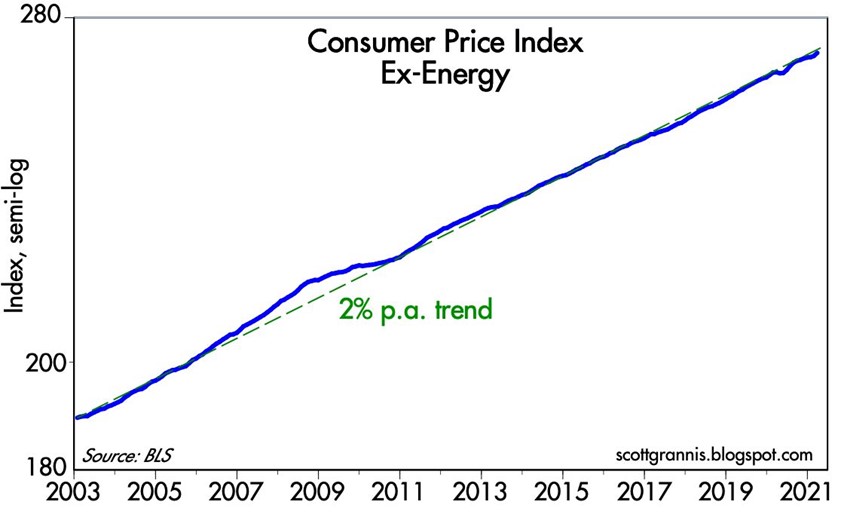

If you strip out volatile energy prices, the good news is that underlying inflation has not spiraled higher out of control, as you can see from the chart below.

In addition to the concerns of potential higher taxes, inflation, and rising interest rate policies from the Federal Reserve, for many months I have written about my apprehension about the speculation in SPACs (Special Purpose Acquisition Companies) and cryptocurrencies like Bitcoin. There are logical explanations to invest selectively into SPACs and purchase Bitcoin as a non-correlated asset for diversification purposes and a hedge against the dollar. But unfortunately, if history repeats itself, speculators will eventually end up in a pool of tears.

While there are certainly some storm clouds on the horizon (e.g., taxes, inflation, rising interest rates, speculative trading), April bloomed a lot of flowers, and the near-term forecast remains very sunny as the economy emerges from a global pandemic. As long as the government continues to provide candy to millions of Americans; the Federal Reserve remains accommodative in its policies; and the surge in pent-up demand persists to drive economic growth, we likely have some more time before we are forced to eat our spinach.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 3, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

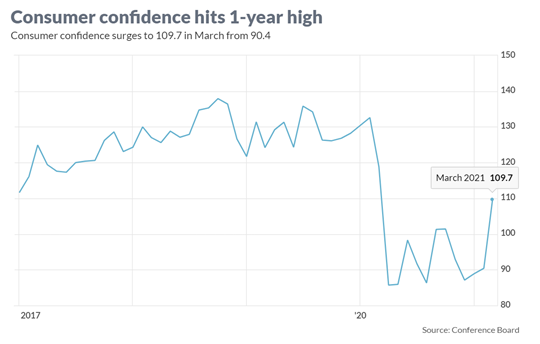

Consumer Confidence Flies as Stock Market Hits New Highs

As the economy starts reopening from a global pandemic that is improving, consumers and businesses are beginning to see a light at the end of the tunnel. The surge in the recently reported Consumer Confidence figures to a new one-year high (see chart below) is evidence the recovery is well on its way. A stock market reaching new record highs is further evidence of the reopening recovery. More specifically, the Dow Jones Industrial Average catapulted 2,094 points higher (+6.2%) for the month to 32,981 and the S&P 500 index soared +4.2%. A rise in interest rate yields on the 10-Year Treasury Note to 1.7% from 1.4% last month placed pressure on technology growth stocks, which led to a more modest gain of +0.4% in the tech-heavy NASDAQ index during March.

Comeback from COVID

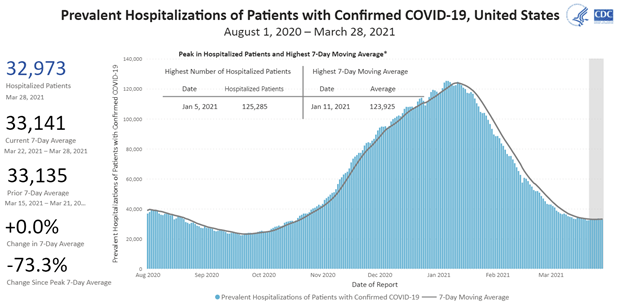

With a combination of 150 million vaccine doses administered and 30 million cumulative COVID cases, the U.S. population has creeped closer toward herd immunity protection against the virus and pushed down hospitalizations dramatically (see chart below).

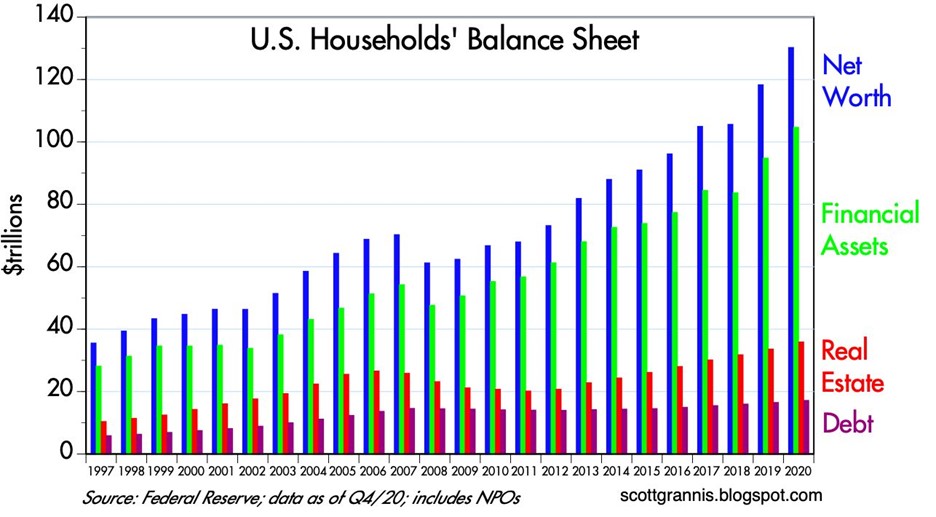

Also contributing to investor optimism have been the rising values of investments and real estate assets thanks to an improving economy and COVID case count. As you can see from the chart below, the net worth of American households has more than doubled from the 2008-2009 financial crisis to approximately $130 trillion dollars, which in turn has allowed consumers to responsibly control and manage their personal debt. Unfortunately, the U.S. government hasn’t been as successful in keeping debt levels in check.

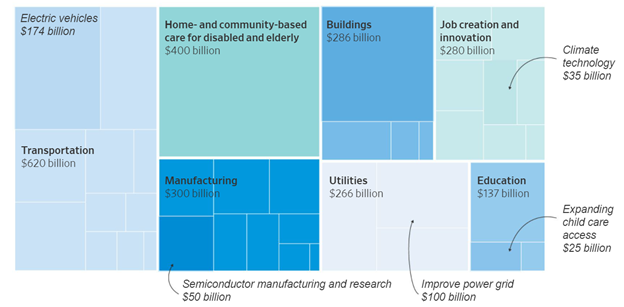

Spending and Paying for Infrastructure Growth

Besides focusing on positive COVID trends, investors have also centered their attention on the passage of a $1.9 trillion stimulus bill last month and a new proposed $2.3 trillion infrastructure bill that President Biden unveiled details on yesterday. At the heart of the multi-trillion dollar spending are the following components (see also graphic below):

- $621 billion modernize transportation infrastructure

- $400 billion to assist the aging and disabled

- $300 billion to boost the manufacturing industry

- $213 billion to build and retrofit affordable housing

- $100 billion to expand broadband access

With over $28 trillion in government debt, how will all this spending be funded? According to The Fiscal Times, there are four main tax categories to help in the funding:

Corporate Taxes: Raising the corporate tax rate to 28% from 21% is expected to raise $730 billion over 10 years

Foreign Corporate Subsidiary Tax: A new global minimum tax on foreign subsidiaries of American corporations is estimated to raise $550 billion

Capital Gains Tax on Wealthy: Increasing income tax rates on capital gains for wealthy individuals is forecasted to raise $370 billion

Income Tax on Wealthy: Lifting the top individual tax rate back to 39.6% for households earning more than $400,000 per year is seen to bring in $110 billion

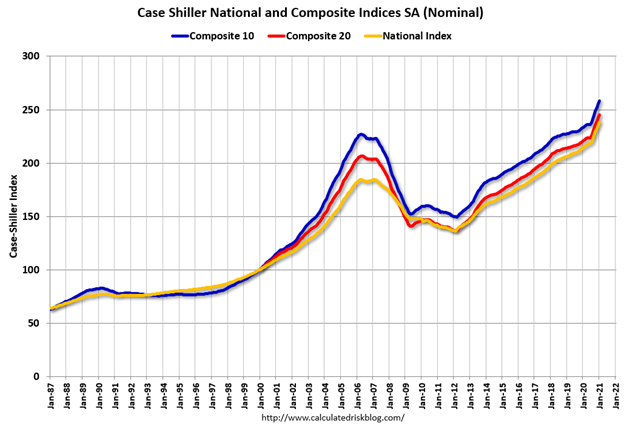

Besides the economy being supported by government spending, growth and appreciation in the housing market are contributing to GDP growth. The recently released housing data shows housing prices accelerating significantly above the peak levels last seen before the last financial crisis (see chart below).

Although the economy appears to be on solid footing and stock prices have marched higher to new record levels, there are still plenty of potential factors that could derail the current bull market advance. For starters, increased debt and deficit spending could lead to rising inflation and higher interest rates, which could potentially choke off economic growth. Bad things can always happen when large financial institutions take on too much leverage (i.e., debt) and speculate too much (see also Long-Term Capital Management: When Genius Failed). The lesson from the latest, crazy blow-up (Archegos Capital Management) reminds us of how individual financial companies can cause billions in losses and cause ripple-through effects to the whole financial system. And if that’s not enough to worry about, you have rampant speculation in SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (e.g., GameStop Corp. – GME), cryptocurrencies, and NFTs (Non-Fungible Tokens).

Successful investing requires a mixture of art and science – not everything is clear and you can always find reasons to be concerned. At Sidoxia Capital Management, we continue to find attractive opportunities as we strive to navigate through areas of excess speculation. At the end of the day, we remain disciplined in following our fundamental strategy and process that integrates the four key legs of our financial stool: corporate profits, interest rates, valuations, and sentiment (see also Don’t Be a Fool, Follow the Stool). As long as the balance of these factors still signal strength, we will remain confident in our outlook just like consumers and investors are currently.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ration or Tax: Eating Cake Not an Option

We live in an instant gratification society that would like everything for free ( like my pal Bill Maher), which explains why we want to have our healthcare cake and eat it too. I think George Will said it best when discussing universal healthcare coverage, “If you think health care is expensive now, just wait until it is free.” Look, I love free stuff too, like the rest of us, whether it’s free sausage sample at Costco (COST) or a breath mint at the Olive Garden (DRI). But regrettably, exploding deficits come at a price.

With midterm elections coming up, the issue of healthcare is once again front and center. The majority party feels like a checkbook is a solution to healthcare prosperity. Can you really look me in the eyes and say covering additional 32 million uninsured Americans is going to save us money. The government hasn’t exactly built a ton of credibility with the disastrous train-wreck we call Medicare, which is already carrying 45 million covered passengers.

The minority party hasn’t done a lot better with the layering of the 2006 unsustainable Medicare Part D drug plan. Conservatives are campaigning on “repeal and replace” and that is great, but where are the cuts?

There are only two solutions to our current healthcare problem: ration or tax (read Plucking Feathers of Taxpaying Geese). Is healthcare a right or privilege? I don’t know, but if we want to cover current obligations, or add 32 – 50 million more uninsured, then we will be required to cut expenses (ration) to pay for increased benefits and/or increase taxes to cover additional benefits. I would love to cover all Americans, along with the starving children in Africa too, but unfortunately we are limited by our resources. Writing checks with borrowed money will only last for so long.

How severe are the exploding healthcare costs, which are covering the graying of the 76 million baby boomers? Here’s how Forbes describes the unsustainable Medicare obligations:

The Medicare Trustees tell us that Medicare’s expected future obligations exceeded premiums and dedicated taxes by $89 trillion (measured in current dollars). No, that’s not a misprint. To put that number in perspective, Medicare’s liability is about 5 1/2 times the size of Social Security’s ($18 trillion) and about six times the size of the entire U.S. economy.

Not a pretty picture. These estimates look pretty far in the future, but even more bare bone figures arrive at a still frightening $33 trillion. Take a look at healthcare spending forecasts as a percentage of GDP – even the lowest estimates are depressing:

Source: National Center for Policy Analysis via Forbes

In our increasingly flat globalized world, competition between countries is becoming even more intense. We are in a marathon race for improved standards of living, and all these debts and deficits are dragging us down like an anchor tied to our legs. Even without considering other massive entitlements like Social Security, healthcare alone has the potential of grinding our economy to a halt. Politicians are great at promising more benefits and tax cuts in exchange for your votes, but true leadership requires delivering the sour medicine necessary for future prosperity. Before we eat the healthcare cake, let’s raise the money to buy the cake first.

Read more about the Medicare Explosion on Forbes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in COST, DRI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Debt Control: Turn Off Costly Sprinklers When Raining

By living in Southern California, I am acutely aware of the water shortage issues we face in this region of the country. We all have our pet peeves, and one that eats at me repeatedly occurs when I drive by a neighbor’s house and notice they are blasting the sprinklers in the pouring rain. I get the same sensation when I read about out-of control government spending confronting our current and future generations in light of the massive debt loads we presently carry.

I, like most people, love free stuff, whether it comes in the form of tooth-pick skewered, teriyaki meatball samples at Costco Wholesale Corp. (COST), or free government education from our school systems. But in times of torrential downpours, at a minimum, we need to be a little more cost conscious of our surroundings and turn off the spending sprinklers.

Certainly, when it comes to government spending, there’s no getting around the entitlement elephant in the room, which accounts for the majority of our non-discretionary government spending (see D-E-B-T: New Four Letter Word article). Unfortunately, layering on new entitlements on top of already unsustainable promises is not aiding our cause. For example, showering our Americans with free drugs as part of Medicare Part D program, and paying for tens of millions into a fantasy-based universal healthcare package (purported to save money…good luck) only serves to fatten up the elephant squeezed into our room.

Reform is absolutely necessary and affordable healthcare should be made available to all, but it is important to cut spending first. Then, subsequently, we will be in a better position to serve the needy with the associated savings. Instead, what we chose appears to have been a jamming of a massive, complex, divisive bill through Congress.

Slome’s Spending Rules

In an effort to guide ourselves back onto a path of sensibility, I urge our government legislators to follow these basic rules as a first step:

Rule #1 – Don’t Pay Dead People: I know we have an innate maternal/paternal instinct to help out others, but perhaps our government could stop doling out taxpayer dollars to buried individuals underground or those people incarcerated in jail? Over the last three years the government sent $180 million in benefit checks to 20,000 corpses, and also delivered $230 million to 14,000 convicted felons (read more).

Rule #2 – Pay for Our Own First: Before we start spending money on others outside our borders, I propose we tend to our flock first. For starters, our immigration policies are a disaster. As I wrote earlier (read Our Nation’s Keys to Success), I am a big proponent of legal immigration for productive, higher-educated individuals – not elitist, just practical. If you don’t believe me, just count the jobs created by the braniac immigrant founders at the likes of Google Inc. (GOOG), Intel Corp. (INTC), and Yahoo! Inc. (YHOO). These are the people who will create jobs and out-battle scrappy, resourceful international competitors that want to steal our jobs and our economic leadership position in the world. What I don’t support is illegal immigration – paying for the healthcare and education of foreign criminals with our country’s maxed-out credit cards. This is the equivalent of someone breaking into my house, and me making their bed and feeding them breakfast…ridiculous. I do not support the immigration law passed in Arizona, but this unfortunate chain of events thankfully puts a spotlight on the issue.

Rule #2a. – Stop Being the Globe’s Free Police: If we are going to comb the caves of Tora Bora as part of funding two wars and chasing terrorists all over the world, then we not only should be spending our defense budget more efficiently (non-Cold War mentality), but also charging freeloaders for our services (directly or indirectly). We are spending a whopping 20 cents of each federal tax dollar on defense, so let’s spend it wisely and charge those outside our borders benefiting from our monetary and physical sacrifices. And, oh by the way, sending $400 million to the territory controlled by Hamas (read more) doesn’t sound like the brightest decision given our fiscal and human challenges at home. I sure hope there are some tangible, accountable benefits accruing to the right people when we have 25 million people here in the U.S. unemployed, underemployed, or discouraged from finding a job.

Rule #3: Put the Obese Elephant on a Diet – As I alluded to above, our government doesn’t need to serve our overweight, entitlement-fed elephant more chocolate, pizza, and ice cream in the form of more entitlements we are not capable of funding. Let’s cut our spending first before we buy off the voters with new spending.

There are obviously a wide ranging set of economic, political, and even religious perspectives on the best ways of managing our hefty debt and deficits. I do not pretend to have all the answers, but what I do know is it is not wise to blast the sprinklers when it is pouring rain outside.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct positions in COST, YHOO, INTC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Building Your Financial Future – Mistakes Made in Investment Planning

Building Your Dream Future Requires a Plan

Building your retirement and financial future can be likened with the challenge of designing and building your dream home. The tools and strategies selected will determine the ultimate cost and outcome of the project.

I constantly get asked by investors, “Wade, is this the bottom – is now the right time to get in the markets?” First of all, if I precisely knew the answer, I would buy my own island and drink coconut-umbrella drinks all day. And secondarily, despite the desire for a simple, get-rich quick answer, the true solution often is more complex (surprise!). If building your financial future is like designing your dream home, then serious questions need to be explored before your wealth building journey begins:

1) Do I have enough money, and if not, how much money do I need to develop my financial future?

2) Can I build it myself, or do I need the help of professionals?

3) Do I have contingency plans in place, should my circumstances change?

4) What tools and supplies do I need to effectively bring my plans to life?

Most investors I run into have no investment plan in place, do not know the costs (fees) of the tools and strategies they are using, and if they are using an advisor (broker) they typically are in the dark with respect to the strategy implemented.

For the “Do-It-Yourselfers”, the largest problem I am witnessing right now is excessive conservatism. Certainly, for those who have already built their financial future, it does not make sense to take on unnecessary risk. However, for most, this is a losing strategy in a world laden with inflation and ever-growing entitlements like Medicare and Social Security. There’s clearly a difference between stuffing money under the mattress (short-term Treasuries, CDs, Money Market, etc.) and prudent conservatism. This is a credo I preach to my clients.

In many cases this conservative stance merely compounds a previous misstep. Many investors undertook excessive risk prior to the current financial crisis – for example piling 100% of investment portfolios into five emerging market commodity stocks.

What these examples prove is that the average investor is too emotional (buys too much near peaks, and capitulates near bottoms), while paying too much in fees. If you don’t believe me, then my conclusions are perfectly encapsulated in John Bogle’s (Vanguard) 1984-2002 study. The analysis shows the average investor dramatically underperforming both the professionally managed mutual fund (approximately by 7% annually) and the passive (“Do Nothing”) strategy by a whopping 10% per year.

Building your financial future, like building your dream home, requires objective and intensive planning. With the proper tools, strategies and advice, you can succeed in building your dream future, which may even include a coconut-umbrella drink.

{kind=link}