Posts tagged ‘S&P 500’

Time in the Market Beats Timing the Market

It was another great year in the stock market. But predicting the timing of a bear or bull market is more challenging. Fortunately for investors, the stock market is up a lot more of the time than it is down. More specifically, over the last century, the stock market has been up 73% of the time for one-year periods and 94% of the time for 10-year periods (see graphic below and Time is What Matters). That’s why investors’ time in the market beats the fools’ errand strategy of trying to time the market. The long-term, consistent upward trend in stock prices makes investing in the stock market akin to sailing around the world with a persistent tailwind for the whole trip.

Source: Capital Group and S&P 500 Index

Many people believe investing in the stock market is gambling, but 73% and 94% odds for stock market gains seem a lot better than the probabilities of making money in Las Vegas. I explored this concept further in one of my recent articles (see Elections Status Quo). Even with those favorable, lopsided odds, recessions do occur, albeit infrequently. As you can see from the chart below, since World War II, we have experienced a dozen recessions averaging 10 months in duration. And guess what? Successful post-recession recoveries have equaled 100% (12 for 12). Despite the short-lived bear markets, stock prices have appreciated more than 30x-fold since the end of World War II.

Source: Yardeni.com

2024 Predictions

There were plenty of pundits and talking heads who falsely predicted a recession in 2024, but the odds certainly worked in investors’ favor. For 2024, the S&P 500 index gained +23%, and this comes on the heels of a banner 2023, which was up +24%. Experiencing back-to-back +20%-years is a rare occurrence, which hasn’t occurred since the late-1990s. As we look into 2025, achieving three consecutive positive years in the stock market is not unprecedented, but as I mentioned earlier, predicting the timing of a down market can be tricky.

Case in point, predicting the outcome of stock returns, even with perfect information can be very daunting. What would have been your prediction of the 2024 stock market return, if I told you the following events were to occur this year (in no particular order)?

- Two assassination attempts on a presidential candidate

- An ongoing bloody war between Russia and Ukraine that reaches one million deaths

- Brutal Israeli-Hamas war in Gaza moves into its second year

- Nationwide Palestinian protests across college campuses

- Israeli-Hezbollah war commences in Lebanon

- Rebels in Syria topple the Assad regime

- A hotly contested presidential election triggering fears of a civil war

- A Baltimore bridge collapses killing six people and costing the overall economy upwards of $10 billion

- After crypto exchange goes bankrupt, CEO is sentenced to 25 years in prison for fraud

Most intelligently honest people would not have predicted a +23% return, but that is exactly what happened. As part of this extended bull market, some major stock market milestones were achieved: 1.) the Dow Jones Industrial average eclipsed 40,000; 2.) the main benchmark S&P 500 index surpassed 6,000; and 3.) the NASDAQ index temporarily triumphed the 20,000 level. The market took a breather in December (the Dow -5.3% and S&P -2.5%), so we have momentarily pulled back from some of these key levels.

What Next in 2025?

As I alluded to earlier, pulling off a three-peat in 2025 with a third consecutive year of gains may be a difficult feat, but not impossible. There remains some room for optimism. First of all, we have an accommodative Federal Reserve that has cut interest rates three times in 2024 (see chart below) from a target of 5.5% to 4.5% (see red line). Currently, expectations are set for the Fed to make another two interest rate cuts in 2025. All else equal, this should provide some mild stimulus for both borrowers and investors in 2025.

Source: Yardeni.com

Next, we have a new pro-business administration entering the White House that has promised lower taxes and less regulation, which should aid business profits. Tariff policies remain a wildcard, but if used judiciously for negotiation purposes, perhaps there could be more bark than bite from the rhetoric. Time will tell.

The 2024 chapter has closed, and we have started the 2025 chapter. Regardless of the outcome this year, history teaches us the time in the market is much more important than timing the market. This philosophy has served Sidoxia Capital Management and its clients well over the long-run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 2, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Bad News is Good News?

Remember that global pandemic back in 2020 called COVID-19 that killed over 350,000 people in the U.S.? That same year, the unemployment rate reached a sky-high level of 14.9% (vs. 3.9% most recently) and the economy went into recession with GDP (Gross Domestic Product) declining by -2.2%. With the whole population locked in their homes and 9.4 million businesses closed, this debacle doesn’t sound like a real great environment for the stock market. What did the stock market actually do in 2020? The S&P 500 surged +16.3% (see chart below). Bad economic news turned out to be good news for stocks.

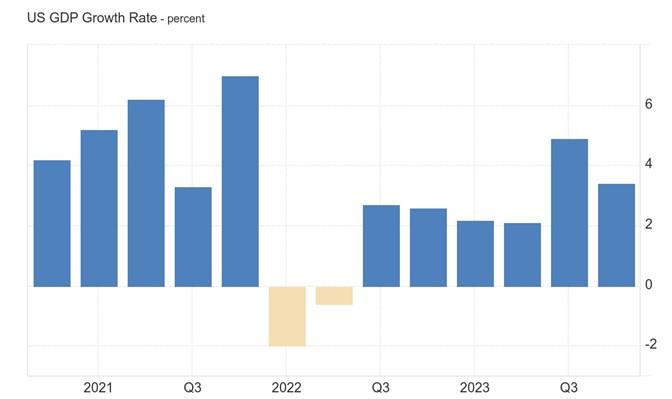

On the flip side, during 2022, the economy was firing on all cylinders. GDP was advancing at a reasonable +1.9% growth rate, and the unemployment rate stood at a near generationally low rate of 3.6%. What did the stock market do? It fell -19%. This time around, good economic news meant bad news for stock prices, primarily because the Federal Reserve was slamming the brakes on the economy by increasing the Federal Funds interest rate target.

These examples are powerful reminders that the direction of economic trends does not necessarily move in tandem with the direction of the stock market. Just this last month, investors experienced this same phenomenon when GDP growth figures were revised lower from +1.6% to +1.3%, and pending home sales dropped by -7.7% to the lowest level in four years during the pandemic. What did the stock market do last month? The S&P climbed +4.8% and the NASDAQ soared +6.9%. Once again, bad news has equaled good news due to higher hopes for Fed interest rate cuts.

For the year, the S&P has already appreciated a very respectable +10.6%. This stellar performance has come despite heated election concerns, persistent wars overseas, nervousness over the Federal Reserve’s monetary policy, and wild volatility in the cryptocurrency markets.

Fighting against these headwinds has been the tsunami of corporate investing dollars piling into the Artificial Intelligence (AI) spending tidal wave. I have been writing about this trend for a while (see AI World) and NVIDIA Corp (NVDA) confirmed this trend a couple weeks ago, when the AI juggernaut reported its fiscal first quarter financial results. Not only did NVIDIA more than triple its revenue above $26 billion for the three-month period compared to last year, but the company also increased its net profit by more than seven-fold to almost $15 billion for the quarter, in addition to announcing a 10-for-1 stock split (see chart below).

What these examples teach you is that it is a fruitless effort for investors to try to time the market based on economic news headlines. Yet, every day you turn on the television or comb through the avalanche of news headlines through various media outlets, there is always some Armageddon story about an impending market crash, or some other speculative, get-rich-quick scheme. As Warren Buffett states, “Investing is like dieting. Easy to understand, but difficult to execute.”

In other words, there is no simple solution to investing. It requires patience, discipline, and financial emotional wherewithal to allow the power of long-term compounding to grow your retirement nest egg. Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risk tolerance. These items are not static, and can change over time, therefore it’s important to revisit your asset allocation periodically as financial circumstances and life events change your objectives.

Of course, improving economic news can also lead to rising stock prices, just as deteriorating economic news can result in declining prices. Regardless, attempting to time the market is a fool’s errand. Rather than trying to maneuver in and out of the stocks, long-term investors should focus more intently on the four key factors that drive the direction of the stock market: corporate profits, interest rates, valuations, and investor sentiment (see also Don’t Be a Fool, Follow the Stool). If you understand the stock market doesn’t logically follow the daily headlines, and instead you follow the key fundament factors driving equity markets, then your investment portfolio should be blessed with plenty of good news.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 3, 2024). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks , certain exchange traded funds (ETFs), including NVDA,, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dow Knocking on the Door of 40,000

The stock market rang the doorbell of the New Year with a bang during the 1st quarter. The S&P 500 index built on last year’s +24% gain with another +10% advance during the first three months of the year. And as a result of these increases, the Dow Jones Industrial Average index is knocking on the door of the 40,000 milestone – more specifically, the Dow closed the month at 39,807 (see chart below). To put his into context, when I was born more than 50 years ago, the Dow was valued at less than 1,000 – not a bad run. This is proof positive of what Einstein called the 8th Wonder of the World, “compounding”. At Sidoxia Capital Management, we view investing as a marathon, not a sprint. You cannot realize the benefits of compounding without having a long-term time horizon. The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow.

If you are one of the people who thinks the stock market is too high, then you should definitely ignore Warren Buffett, arguably the greatest investor of all-time. Buffett predicted the Dow will reach an astronomical level of one million (1,000,000) within the next 100 years. I’m not sure I will still be around to witness this momentous achievement, however, if history repeats itself, this targeted timeframe could prove conservative.

Despite the magnitude and duration of this bull market, there is still a lot of angst and anxiety over the upcoming election. Nevertheless, investors are choosing instead to focus on the strong fundamentals of the economy. Just this last week, we saw the broadest measurement of economic activity, GDP (Gross Domestic Product), get revised higher to +3.4% growth during the 4th quarter of 2023 (see chart below). On the jobs front, the unemployment picture remains healthy (3.9%), near a generational low.

Source: Trading Economics and Bureau of Economic Analysis

And when it comes to the all-important inflation data, the Federal Reserve’s preferred inflation measure, Core PCE index (Core Personal Consumption Expenditures), was also just released in-line with economists’ projections at 2.5% (see chart below), very near the Fed’s long-term 2.0% inflation target and well below the Core PCE’s recent peak near 6%.

Source: The Wall Street Journal and Commerce Department

This resilient economic data, when combined with the declining inflation figures, has resulted in the Federal Reserve sticking with its plan of cutting its Federal Funds interest rate target three times this year. If inflation reverses course or remains stubbornly high, then there is a higher likelihood that interest rate cuts will be delayed. On the flip side, if economic data slows significantly or the country goes into a recession, then the probability of sooner and/or more Fed interest-rate cuts will increase.

In other news, here are some of the other major financial headlines this month:

- Francis Scott Key Baltimore Bridge Collapse: Six people died when a large container ship crashed into the Francis Scott Key bridge in the Port of Baltimore. An estimated 50 million tons of goods valued at $80 billion flows through this port, making this one of the top 10 ports in the country. The auto and coal industry supply chains will be disproportionately affected, but the good news is much of these goods will be diverted to other larger ports (e.g., Port of New York and Port of New Jersey).

- DJT Debut: A lot of hype surrounded the trading debut of Trump Media & Technology Group, which began trading last week under the initials of our country’s former president, Donald J. Trump (Ticker: DJT). Despite only posting a few million in revenue and -$50 million in losses during the first nine months of 2023, the stock skyrocketed +65% in its first week of trading and attained a $9 billion valuation. Time will tell if Trump’s Truth Social media platform will gain traction and justify the stock’s price, or rather suffer the declining fate of other meme stocks like GameStop Corp. (GME) or AMC Entertainment Holdings (AMC).

- SBF Sentenced to 25 Years: The former CEO of cryptocurrency exchange company FTX, Sam Bankman-Fried (SBF), was sentenced to 25 years in prison due to his conviction on seven counts of fraud and what is believed to be $8 billion in stolen client funds. SBF didn’t help his own cause by perjuring himself, tampering with witnesses, and showing a lack of remorse, according to the judge.

We are only 25% of the way through the year, but the Dow is knocking on the 40,000-milestone door. The way things look now, investors are wiping their feet on the welcome doormat and ready to walk right in.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2024). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks , certain exchange traded funds (ETFs), and notes including AMC 2026, but at the time of publishing had no direct position in DJT, GME, AMC or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Mission Accomplished?

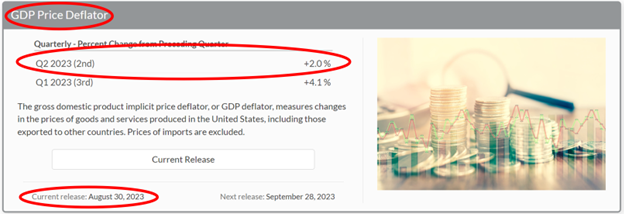

The Federal Reserve has a “dual mandate” designed to “foster economic conditions that achieve both stable prices and maximum sustainable employment.” The “dual mandate” is obviously a moving target, but it appears for now, based on the Fed’s explicit goals, Fed Chairman, Jerome Powell, has accomplished the central bank’s mission. More specifically, inflation, according to the just-reported BEA’s (Bureau of Economic Analysis) GDP Price Deflator statistics, has plummeted dramatically to the Fed’s goal of 2.0% from the sky-high inflation number of 9.1% a year ago (see chart below). Meanwhile, the economy continues to grow (+2.0% GDP growth in the 2nd quarter), and the long-awaited recession boogeyman has yet to appear.

Source: Bureau of Economic Analysis

Rate Pig Moving Through Economic Python

How has inflation plunged so quickly? For starters, in addition to the Fed’s restrictive policy of reducing the balance sheet, since the beginning of last year, the Fed has also effectively slammed the brakes on the economy by taking their target interest rate from 0% to 5.5%. The pace and scale of the interest rate increases have been reduced this year, however it is possible there might be more rate hikes ahead (currently, pundits are betting for no more rate increases this year, although a boost in November is possible if economic data accelerates). Like a pig working its way through the economic python, the large interest rate increases naturally take a while to work their way through the consumer, commercial, and government credit markets.

To put things in better perspective, a study done earlier this year showed the average 30-year monthly mortgage payment for a $500,000 home was higher by more than $800 (up +44%) versus a year ago! But wait, it’s not just consumers feeling the pinch of higher rates. Businesses and governments in all shapes and sizes have felt the pain as well from higher borrowing costs. Post-COVID supply chain constraints and disruptions have eased too, which have helped choke down the high inflation numbers. In the background, let’s not also forget about the disinflationary benefits of ever-expanding technology adoption coupled with the related productivity advantages (see also AI Revolution).

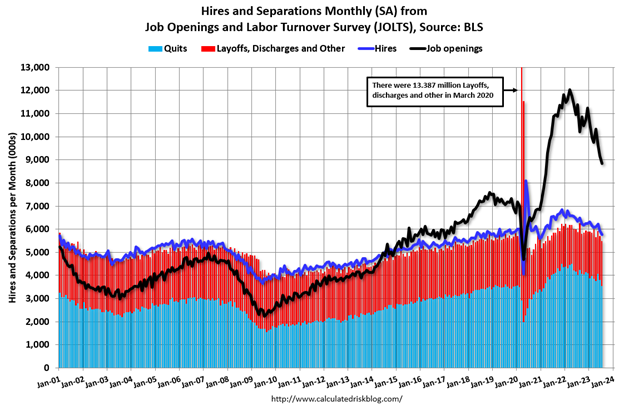

As a result of these dynamics, we are now starting to see cracks appear in our country’s employment foundation as this month’s JOLTs (Job Openings and Labor Turnover – see black line in chart below) and ADP monthly job additions data, which both came in disappointingly low compared to forecasts. Chairman Powell must be ecstatic inflation has plummeted, while the unemployment rate remains near multi-decade lows, and Gross Domestic Product (GDP) growth continues expanding (i.e., no recession in sight).

Source: Calculated Risk and U.S. Bureau of Labor Statistics

Hot Summer, Hot Stocks

Economic activity clearly can and will change, but the stock market has been like the weather this summer…hot. However, after experiencing up-months in six out of the first seven months of 2023, the S&P 500 index decided to take a small breather this month. For August, the S&P slipped -1.8%, but the month was a tale of two cities. By the middle of the month, the index had fallen by roughly -6% on fears of potentially more aggressive interest rate hikes by the Federal Reserve due to better than anticipated economic data. In other words, inflation fears were on the rise and the 10-Year Treasury Note yield temporarily climbed to a 52-week high. By the end of the month, economic data cooled, interest rates dropped a little, and stock prices rebounded smartly by +4.0% to finish the month on a strong note.

For the year, the S&P’s remain strongly positive, up +17.4%. As I have written in the past, the seven largest companies in the S&P 500 index (a.k.a., The Magnificent 7: Apple Inc.; Microsoft Corp.; Alphabet Inc.; Amazon.com, Inc.; NVIDIA Corp.; Tesla, Inc.; and Meta Platforms, Inc.) have contributed to a significant portion of the year’s gains – the average Magnificent 7 stock has skyrocketed an eye-popping +99.0% with NVIDIA being the largest winner, more than tripling in value during the first eight months of the year.

The Federal Reserve can admit they were late to the game in taming out-of-control inflation, but Fed Chair Powell has been swift in moving to preserve his legacy as an inflation fighter. Now that inflation is coming under control and the economy is beginning to cool, Powell needs to make sure he doesn’t murder the economy into recession with overzealous future interest rate increases. Time will tell if the mission has already been accomplished, but so far, the Fed has been delicately balancing an economic soft landing and stock market investors like it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, MSFT, GOOGL, AMZN, NVDA, TSLA, META, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Movie Deja Vu – Coronavirus

I have seen this movie before. I love the stock market, but I do actually have other outside interests, including seeing movies. What better indoor winter activity than watching movies?! The Hollywood excitement continues this Sunday for the 92nd Academy Awards. My popcorn consumption has been generous this year as I have seen seven of the nine Best Picture nominated films with the exception of Jojo Rabbit and Little Women.

With a lifetime of movie watching under my belt, there is no shortage of redundant movie themes, whether it’s happy endings in romantic comedies, triumphant patriotism in war flicks, or gory blood spatters in horror films. Just as repetitive as these story lines have been in films, the redundant theme of pandemic health panics continues to plague investors every time a new contagious disease is announced. The newest debut is coronavirus. While coronavirus is playing on the big screen, the presidential impeachment trial, and January 31st Brexit deadline have been sideshows. Stay tuned for that breaking news!

Doctor Wade’s Diagnosis

Although I have not added M.D. to my list of professional credentials (CFA, CFP), Dr. Wade has enough medical experience to identify historical patterns. Most recently, the media covering the Wuhan coronavirus originating in the central Chinese province of Hubei (see map below) has unnecessarily terrorized the global masses with F.U.D. (Fear, Uncertainty, Doubt). While we likely know the ending of this health scare movie (i.e., humanity survives and life goes on), the timing, and scope remain uncertain.

2020: Sickness After Healthy Start

After an healthy start to the 2020 stock market show (S&P 500 index zoomed +3.3% higher), investors viewing the coronavirus plot unfold subsequently were sickened with an S&P decline of -3.4% to finish the month slightly down from year-end (-0.2% from December 31st to January 31st). The Dow Jones Industrial Average was hit slightly worse, down 282 points for the month to 28,256, or -1.0%.

How do we know this infectious coronavirus disease scare shall too pass? Well, over the last few decades, there have been many more lethal diseases that have been put to bed. Here’s a list of some of these high profile, safely-controlled infectious diseases:

- Severe Acute Respiratory Syndrome (SARS)

- Middle East Respiratory Syndrome (MERS)

- Ebola

- Zika Virus

- Bird Flu

- Swine Flu

- H1N1 Virus

- Mad Cow

- Hoof-and-Mouth

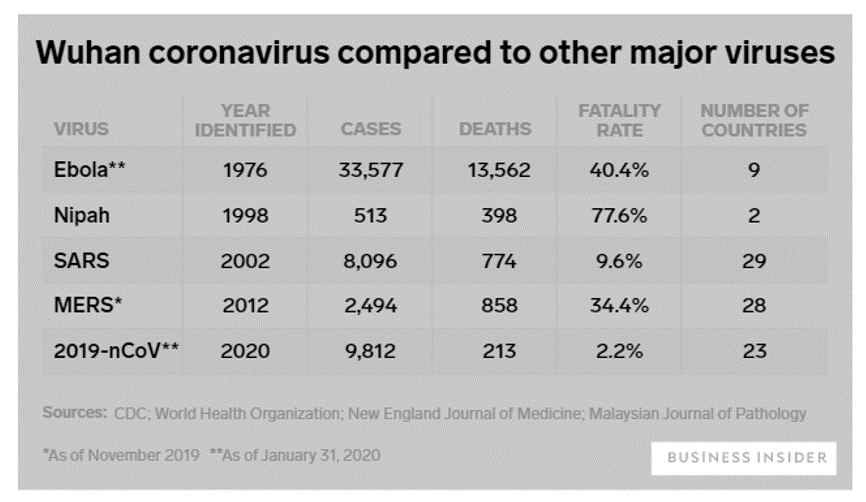

A chart comparing the severity and timing of some of the major viruses can be seen below.

While the human impact has been tragic, coronavirus has also struck a blow to the global economy. The pandemic prequel that mostly closely matches coronavirus is SARS, which also originated in China during 2003 in the province of Guandong. Most notable to me is the fatality rate for coronavirus of just 2.2% versus 9.6% for SARS. While coronavirus is less deadly than SARS, coronavirus is objectively more contagious than SARS and could have an incubation period of 14 days (significantly longer than SARS, which could increase the rate of infections). In fact, there were more confirmed cases of coronavirus in one month than all the reported cases of SARS identified over a span of nine months. Even so, as the chart shows, coronavirus deaths remain the lowest.

Economic Impact

The damaging economic impact of the coronavirus pandemic continues to escalate rapidly on a daily basis as governments, global health agencies, corporations, and individuals respond. Even though coronavirus appears to be much less lethal than SARS, we can scale current economic estimates based on the relative costs incurred during SARS. Some reports show the 2003 SARS situation costing the global economy $40 – $60 billion and 2.8 milllion Chinese jobs, while the potential hit in lost global growth from coronavirus could total $160 billion, according to Warwick McKibbin, a Australian National University economics professor.

The Chinese government fully realizes the amount of financial destruction caused by the SARS outbreak, and therefore is not sitting idly as it relates to the coronavirus. Back during SARS, the government did not institute quarantine measures nor publish the SARS’ genome (necessary to test and track virus) until four months had passed. After the first coronavirus patient was diagnosed around December 1st (two months ago) and the spread of the virus accelerated, the Chinese local governments expanded mandatory factory shutdowns for the Lunar New Year from January 31st to February 9th. What’s more, Wuhan, a city of 11 million residents at the epicenter of the illness, recently closed the area’s outgoing airport and railway stations and suspended all public transport. Chinese government officials have since extended the travel ban to 16 neighboring cities with a combined population of more than 50 million people, including Huanggang, a city next to Wuhan with 7.5 million people, essentially placing those cities on lock down.

Private companies are taking action as well. Companies such as Disney, Tesla, Amazon, Google, Apple, McDonalds, Starbucks, and more than a dozen airlines, cruise lines, casinos, and other global companies with significant footprints in China are suspending operations, temporarily shutting factories and instituting travel restrictions.

No Need to Panic Yet

Before you quarantine yourself in your basement, and take full-body showers in hand sanitizer, let’s take a look at some of those annoying things called facts:

- There have been zero (0) coronavirus deaths in the United States, and eight diagnosed cases (at time of press).

- There have been approximately 10,000 Americans killed by the flu since October 2019.

Apparently casual American observers are unable to filter out the true signals being lost in the avalanche of blood-curdling, panicked virus headlines. Tufts Medical Center infectious disease specialist Dr. Shira Doron highlighted this message when she stated the following, “The likelihood of an American being killed by the flu compared to being killed by the coronavirus is probably approaching infinity.” Of the limited number of coronavirus deaths thus far, one study of 41 Wuhan coronavirus death cases showed the median age is around 75 years old. For most people (i.e., those who are not elderly or young children), I guess the moral of this story is to turn the TV off, go get your flu shot, and fall asleep with few worries.

There may be some more coronavirus pain and suffering ahead until this tragic human and economic pandemic comes under control. During the SARS outbreak (November 2002 – July 2003), peak-to-trough stock prices temporarily fell by -16% before marching upwards to new record highs. However, if this movie finishes like so many other similar infectious diseases, the coronavirus fever should break soon enough, and investors will be satisfied with new opportunities and another happy ending to the story.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 3, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFS) and DIS, TSLA, AMZN, GOOGL, AAPL, and MCD, but at the time of publishing had no direct position in SBUX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

March Madness Leads to Gladness

As usual, there was plenty of “madness” in March, and this year did not disappoint. Just as is the case with the annual NCAA basketball tournament, certain investors suffered the agony of defeat in the financial markets, but overall, the thrill of victory triumphed in March. So much so that the S&P 500 index posted its largest first-quarter gain in more than 20 years. Not only did the major indexes post gains for the month, but the winning record looks even better for the year-to-date results. For 2019, the S&P 500 index is up +13.1%; the Dow Jones Industrial Average +11.2%; and the tech-heavy NASDAQ index +16.5% for the year. The monthly gains in the major indexes were more muted, ranging from 0% for the Dow to +2.6% for the NASDAQ.

Busy? Listen to Wade discuss this article and other topics each week on the Weekly Grind podcast:

While 2018 ended with a painful injury (S&P 500 -6.2% in Q4), on fears of a deteriorating China trade deal and a potentially overly aggressive Federal Reserve hiking interest rates, the stock market ultimately recovered in 2019 on changing perceptions. Jerome Powell, the Federal Reserve Chairman, indicated the Fed would be more “patient” going forward in increasing interest rates, and President Trump’s tweet-storm on balance has been optimistic regarding the chances of hammering out a successful trade deal with China.

With the new cautious Fed perspective on interest rates, the yield on the 10-Year Treasury Note fell by -0.28% for the quarter from 2.69% to 2.41%. In fact, investors are currently betting there is a greater than 50% probability the Fed will cut interest rates before year-end. Moreover, in testimony before Congress, Powell signaled the economic dampening policy of reducing the Fed’s balance sheet was almost complete. All else equal, the shift from a perceived rate-hiking Fed to a potentially rate-cutting Fed has effectively turned an apparent headwind into tailwind. Consumers are benefiting from this trend in the housing market, as evidenced by lower 30-year fixed mortgage rates, which in some cases have dropped below 4%.

Economy: No Slam Dunk

However, not everything is a slam dunk in the financial markets. Much of the change in stance by the Fed can be attributed to slowing economic growth seen both here domestically and abroad, internationally.

Here in the U.S., the widely followed monthly jobs number last month only showed a gain of 20,000 jobs, well below estimates of 180,000 jobs. This negative jobs surprise was the biggest miss in more than 10 years. Furthermore, the overall measure for our nation’s economic activity, growth in Gross Domestic Product (GDP), was revised downward to +2.2% in Q4, below a previous estimate of +2.6%. The so-called “inverted yield curve” (i.e., short-term interest rates are higher than long-term interest rates), historically a precursor to a recession, is consistent with slowing growth expectations. This inversion temporarily caused investors some heartburn last month.

If you combine slowing domestic economic growth figures with decelerating manufacturing growth in Europe and China (e.g. contracting Purchasing Managers’ Index), then suddenly you end up with a slowing global growth picture. In recent months, the U.S. economy’s strength was perceived as decoupling from the rest of the world, however recent data could be changing that view.

Fortunately, the ECB (European Central Bank) and China have not been sitting on their hands. ECB President Mario Draghi announced three measures last month that could cumulatively add up to some modest economic stimulus. First, it “expects the key ECB interest rates to remain at their present levels at least through the end of 2019.” Second, it committed to reinvesting all maturing bond principal payments in new debt “for an extended period of time.” And third, the ECB announced a new batch of “Targeted Long-Term Refinancing Operations” starting in September. Also, Chinese Premier Li Keqiang announced the government will reduce taxes, primarily Value Added Taxes (VAT) and social security taxes (SST). Based on the rally in equities, it appears investors are optimistic these stimulus efforts will eventually succeed in reigniting growth.

Volume of Political Noise Ratcheted Higher

While I continually try to remind investors to ignore politics when it comes to their investment portfolios, the deafening noise was especially difficult to overlook considering the following:

- Mueller Report Completed: Robert Mueller’s Special Counsel investigation into potential collusion as it relates Russian election interference and alleged obstruction of justice concluded.

- Michael Cohen Testifies: Former President Trump lawyer, Michael Cohen, testified in closed sessions before the House and Senate intelligence committees, and in public to the House Oversight Committee. In the open session, Cohen, admitted to paying hush money to two women during the election. Cohen called President Trump a racist, a conman, and a cheat but Cohen is the one heading to jail after being sentenced for lying to Congress among other charges.

- Manafort Sentenced: Former Trump Campaign Chairman Paul Manafort was sentenced to prison on bank and tax fraud charges.

- North Korea No Nuke Deal: In geopolitics,President Trump flew 21 hours to Vietnam to meet for a second time with North Korean leader Kim Jong Un on denuclearization of the Korean peninsula. The U.S. president ended up leaving early, empty handed, without signing an agreement, after talks broke down over sanction differences.

- Brexit Drama Continues: The House of Commons in the lower house of the U.K. Parliament continued to stifle Prime Minister Theresa May’s plan to exit the European Union with repeated votes rejecting her proposals. Brexit outcomes remain in flux, however the European Union did approve an extension to May 22 to work out kinks, if the House can approve May’s plan.

Positive Signals Remain

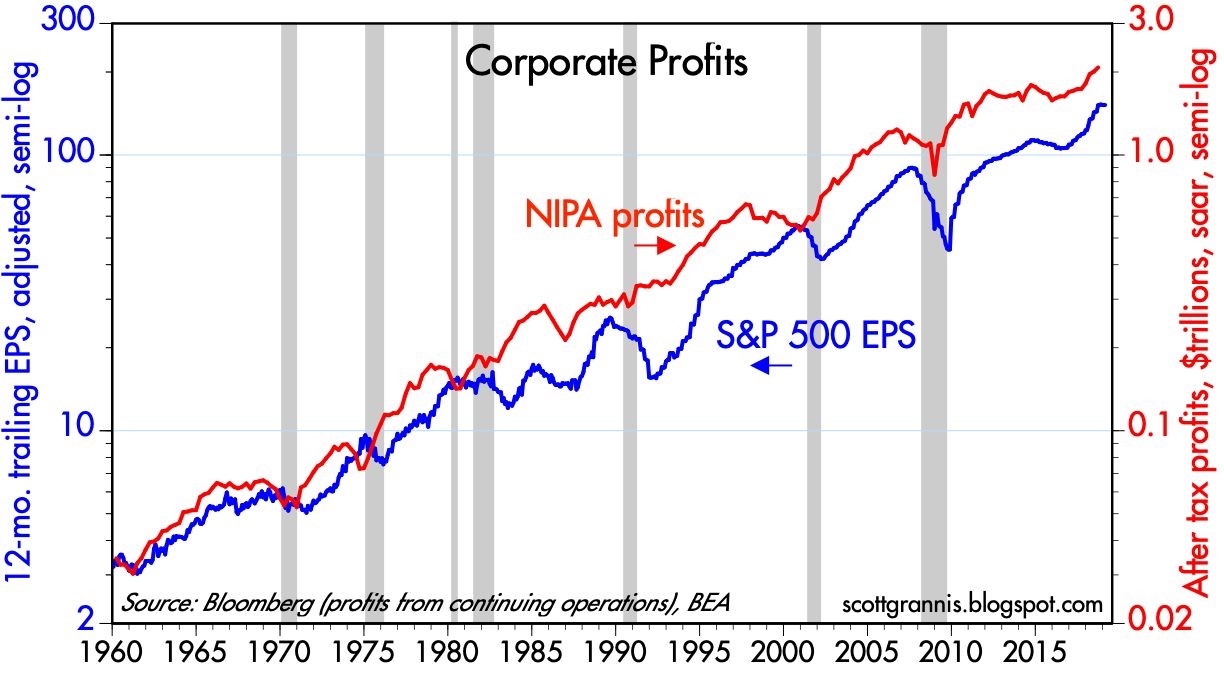

March Madness reminds us that a big lead can be lost quickly, however a few good adjustments can also swiftly shift momentum in the positive direction. Although growth appears to be slowing both here and internationally, corporate profits are not falling off a cliff, and earnings remain near record highs (see chart below).

Source: Calafia Beach Pundit

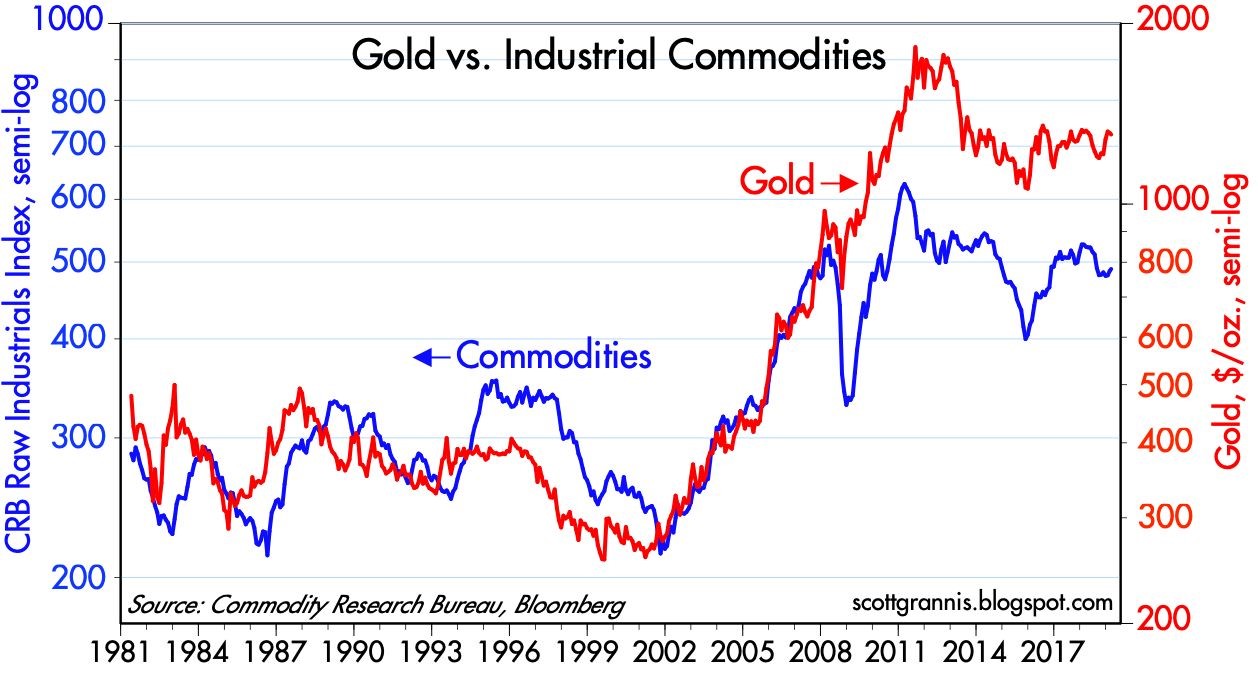

Similar to the stock market, commodities can be a good general barometer of current and future economic activity. As you can see from the chart below, not only have commodity prices remained stable in the face of slowing economic data, but gold prices have not spiked as they did during the last financial crisis.

Source: Calafia Beach Pundit

After 2018 brought record growth in corporate profits and negative returns, 2019 is producing a reverse mirror image – slow profit growth and record returns. The volatile ending to 2018 and triumphant beginning to 2019 is a reminder that “March Madness” does not need to bring sadness…it can bring gladness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

From Gloom to Boom

Gloomy clouds rolled in late last year in the form of a government shutdown; U.S. – China trade war tensions; hawkish Federal Reserve interest rate policies; a continued special counsel investigation by Robert Mueller into potential Russian election interference; a change in the Congressional balance of power; Brexit deal uncertainty; and U.S. recession concerns, among other worries. These fear factors contributed to a thundering collapse in stock prices during the September to December time frame of approximately -20% in the S&P 500 index (from the September 21st peak until the December 24th trough).

However, the dark storm clouds quickly lifted once Santa Claus delivered post-Christmas stock price gains that have continued through February. More specifically, since Christmas Eve, U.S. stocks have rebounded a whopping +18%. On a shorter term basis, the S&P 500 index and the Dow Jones Industrial Average have both jumped +11.1% in 2019. January showed spectacular gains, but last month was impressive as well with the Dow climbing +3.7% and the S&P +3.0%.

The rapid rise and reversal in negative sentiment over the last few months have been aided by a few positive developments.

- Strong Earnings Growth: For starters, 2018 earnings growth finished strong with an increase of roughly +13% in Q4-2018, thereby bringing the full year profit surge of roughly +20%. All else equal, over the long run, stock prices generally follow the path of earnings growth (more on that later).

- Solid Economic Growth: If you shift the analysis from the operations of companies to the overall performance of the economy, the results in Q4 – 2018 also came in better than anticipated (see chart below). For the last three months of the year, the U.S. economy grew at a pace of +2.6% (higher than the +2.2% GDP [Gross Domestic Product] growth forecast), despite headwinds introduced by the temporary U.S. federal government shutdown and the lingering Chinese trade spat. For the full-year, GDP growth came in very respectably at +2.9%, but critics are dissecting this rate because it was a hair below the coveted 3%+ target of the White House.

Source: The Wall Street Journal

- A More Accommodative Federal Reserve: As mentioned earlier, a major contributing factor to the late-2018 declines was driven by a stubborn Federal Reserve that was consistently raising their interest rate target (an economic-slowing program that is generally bad for stocks and bonds), which started back in late 2015 when the Federal Funds interest rate target was effectively 0%. Over the last three years, the Fed has raised its target rate range from 0% to 2.50% (see chart below), while also bleeding off assets from its multi-trillion dollar balance sheet (primarily U.S. Treasury and mortgage-backed securities). The combination of these anti-stimulative policies, coupled with slowing growth in major economic regions like China and Europe, stoked fears of an impending recession here in the U.S. Fortunately for investors, however, the Federal Reserve Chairman, Jerome Powell, came to the rescue by essentially implementing a more “patient” approach with interest rate increases (i.e., no rate increases expected in the foreseeable future), while simultaneously signaling a more flexible approach to ending the balance sheet runoff (take the program off “autopilot).

Source: Dr. Ed’s Blog

The Stock Market Tailwinds

For those of you loyal followers of my newsletter articles and blog articles over the last 10+ years, you understand that my generally positive stance on stocks has been driven in large part by a couple of large tailwinds (see also Don’t Be a Fool, Follow the Stool):

#1) Low Interest Rates – Yes, it’s true that interest rates have inched higher from “massively low” levels to “really low” levels, but nevertheless interest rates act as the cost of holding money. Therefore, when inflation is this low, and interest rates are this low, stocks look very attractive. If you don’t believe me, then perhaps you should just listen to the smartest investor of all-time, Warren Buffett. Just this week the sage billionaire reiterated his positive views regarding the stock market during a two hour television interview, when he once again echoed his bullish stance on stocks. Buffett noted, “If you tell me that 3% long bonds will prevail over the next 30 years, stocks are incredibly cheap… if I had a choice today for a ten-year purchase of a ten-year bond at whatever it is or ten years, or– or buying the S&P 500 and holding it for ten years, I’d buy the S&P in a second.”

#2) Rising Profits – In the short-run, the direction of profits (orange line) and stock prices (blue line) may not be correlated (see chart below), but over the long-run, the correlation is amazingly high. For example, you can see this as the S&P 500 has risen from 666 in 2009 to 2,784 today (+318%). More recently, profits rose about +20% during 2018, yet stock prices declined. Moreover, profits at the beginning of 2019 (Q1) are forecasted to be flat/down, yet stock prices are up +11% in the first two months of the year. In other words, the short-term stock market is schizophrenic, so focus on the key long-term trends when planning for your investments.

Source: Macrotrends

Although 2018 ended with a gloomy storm, history tells us that sunny conditions have a way of eventually returning unexpectedly with a boom. Rather than knee-jerk reacting to volatile financial market conditions after-the-fact, do yourself a favor and create a more versatile plan that deals with many different weather conditions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

P.S.

Wade’s Investing Caffeine Podcast Has Arrived!

Wade Slome, founder of Sidoxia Capital Management, author of How I Managed $20 Billion Dollars by Age 32, and lead editor of the Investing Caffeine blog has launched the Caffeine Corner investment podcast.

The Investing Caffeine podcast is designed to wake up your investment brain with weekly overviews of financial markets and other economic-related topics.

Don’t miss out! Follow us on either SoundCloud or PodBean to get a new episode each week. Or follow our InvestingCaffeine.com blog and watch for new podcast updates each week.

Will Santa Leave a Lump of Coal?

As we enter the last month of the year, the holiday season is kicking into full gear, decorations are popping up everywhere, and the burning question arises, “Will Santa Claus bring gifts for stock market investors, or will he leave a lump of coal in their stockings?”

It was a bumpy sleigh ride last month, but we ultimately entered December in a festive mood with joyful monthly gains of +1.7% in the Dow Jones Industrial Average, and +1.8% in the S&P 500. There have been some naughty and nice factors leading to some turbulent but modest gains in 2018. For the first 11 months of the year, the Dow has rejoiced with a +3.3% advance, and the S&P 500 has celebrated a rise of +3.2% – and these results exclude additional dividends of approximately 2%.

Despite the monthly gains, not everything has been sugar plums. President Trump has been repeatedly sparring with the Federal Reserve Chairman, Jerome Powell, treating him more like the Grinch due to his stingy interest rate increases than Santa. As stockholders have contemplated the future path of interest rates, the major stock indexes temporarily slipped into negative territory for the year, until Mr. Powell gave stock and bond investors an early Christmas present last week by signaling interest rates are “just below” the nebulous neutral target. The dovish comment implied we are closer to the end of the economy-slowing rate-hike cycle than we are to the beginning.

Trade has also contributed to the recent spike in stock market volatility, despite the fresh establishment of the trade agreement reached between the U.S., Mexico, and Canada (USMCA – U.S.-Mexico-Canada Agreement), a.k.a., NAFTA 2.0. Despite the positive progress with our Mexican and Canadian neighbors, uncertainty surrounding our country’s trade relations with China has been challenging due to multiple factors including, Chinese theft of American intellectual property, cyber-attacks, forced technology transfer, agricultural trade, and other crucial issues. Fortunately, optimism for a substantive agreement between the world’s two super-powers advanced this weekend at the summit of the Group of 20 nations in Argentina, when a truce was reached to delay an additional $200 billion in tariffs for 90 days, while the two countries further negotiate in an attempt to finalize a comprehensive trade pact.

Source: Financial Times

Economic Tailwinds

Besides positive developments on the interest rate and trade fronts, the economy has benefited from tailwinds in some other important areas, such as the following:

Low Unemployment: The economy keeps adding jobs at a healthy clip with the unemployment rate reaching a 48-year low of 3.7%.

Source: Calculated Risk

Rising Consumer Confidence: Although there was a slight downtick in the November Consumer Confidence reading, you can see the rising long-term, 10-year trend has been on a clear upward trajectory.

Source: Chad Moutray

Solid Economic Growth: As the chart below indicates, the last two quarters of economic growth, measured by GDP (Gross Domestic Product), have been running at multi-year highs. Forecasts for the 4th quarter currently stand at a respectable mid-2% range.

Source: BEA

Uncertain Weather Forecast

Although the majority of economic data may have observers presently singing “Joy to the World,” the uncertain political weather forecast could require Rudolph’s red-nose assistance to navigate the foggy climate. The mid-term elections have created a split Congress with the Republicans holding a majority in the Senate, and the Democrats gaining control of the House of Representatives. As we learned in the last presidential term, gridlock is not necessarily a bad thing (see also, Who Said Gridlock is Bad?). For instance, a lack of government control can place more power in the hands of the private sector. Political ambiguity also surrounds the timing and outcome of Robert Mueller’s Special Counsel investigation into potential Russian interference and collusion, however as I have continually reminded followers, there are more important factors than politics as it relates to the performance of the stock market (see also, Markets Fly as Media Noise Goes By).

From an economic standpoint, some speculative areas have been pricked – for example the decline in FAANG stocks or the burst of the Bitcoin bubble as the price has declined from roughly $19,000 from its peak to roughly $4000 today (see chart below).

Source: Coindesk

On the housing front, unit sales of new and existing homes have not been immune to the rising interest rate policies of the Federal Reserve. Nevertheless, as you can witness below, housing prices remain at all-time record high prices, according to the recent Case-Shiller data.

Source: Calculated Risk

I like to point out to my investors there is never a shortage of things to worry about. Even when the economy is Jingle Bell Rocking, the issues of inflation and Fed policy inevitably begin to creep into investor psyches. While prognosticators and talking heads will continue trying to forecast whether Santa Claus will place presents or coal into investors’ stockings this season, at Sidoxia we understand predictions are a fool’s errand. Regardless of Santa’s generosity (or lack thereof), we continue to find attractive opportunities for our investors, as we look to balance the risk and rewards presented to us during both stable and volatile periods.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 3, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Will the Halloween Trick Turn into a Holiday Treat?

The interest rate boogeyman came out in October as fears of an overzealous Federal Reserve monetary policy paralyzed investors into thinking rising interest rates could murder the economy into recession. But other ghostly issues frightened the stock market last month as well, including mid-term elections, heightening trade war tensions, a weakening Chinese economy, a fragile European economy (especially Italy), rising oil prices, weakening emerging market economies, anti-Semitism, politically motivated bomb threats, and anxiety over a potential recession after an aged economic expansion embarks on its 10th consecutive year of gains.

This ghoulish short-term backdrop resulted in the Dow Jones Industrial Average suffering a -5.1% drop last month, and the technology-heavy NASDAQ index screamed even lower by -9.2%. The results for the full year 2018 look more constructive – the S&P 500 is up +1.4% and the NASDAQ has climbed +5.8%.

Should the dreadful October result be surprising? Historically speaking, seasonality in the stock market has been quite scary during the month of October, especially if you consider the spooky stock Market Crash of 1929 (-19.7%) , the 1987 Crash (-21.5%), and the bloody collapse during the October 2008 Financial Crisis (-16.8%). There is good news, however. Seasonally, the holiday months of November and December typically tend to treat investors more cheerfully during the so-called “Santa Claus Rally” period. Since 1950 through 2017, the average return for stocks during November has been +1.4% (45 up years and 23 down years). For December, the results are even better at +1.5% (51 up years and 17 down years).

| November (1950-2017) | December (1950-2017) | |||

| Up Years | Down Years | Up Years | Down Years | |

| 2017 2.40% | 2015 -0.02% | 2017 1.08% | 2015 -1.87% | |

| 2016 3.29% | 2011 -0.32% | 2016 1.76% | 2014 -0.33% | |

| 2014 2.45% | 2010 -0.44% | 2013 2.31% | 2007 -0.76% | |

| 2013 2.68% | 2008 -7.48% | 2012 0.70% | 2005 -0.10% | |

| 2012 0.28% | 2007 -4.18% | 2011 0.86% | 2002 -6.03% | |

| 2009 5.74% | 2000 -8.01% | 2010 5.99% | 1996 -2.15% | |

| 2006 1.66% | 1994 -3.93% | 2009 1.48% | 1986 -2.83% | |

| 2005 3.52% | 1993 -1.29% | 2008 1.65% | 1983 -0.87% | |

| 2004 3.86% | 1991 -4.39% | 2006 1.26% | 1981 -3.01% | |

| 2003 0.71% | 1988 -1.89% | 2004 3.25% | 1980 -3.39% | |

| 2002 5.71% | 1987 -8.51% | 2003 5.08% | 1975 -1.15% | |

| 2001 7.52% | 1984 -1.51% | 2001 0.76% | 1974 -1.78% | |

| 1999 1.92% | 1976 -0.78% | 2000 0.41% | 1969 -1.87% | |

| 1998 5.91% | 1974 -5.32% | 1999 5.78% | 1968 -4.16% | |

| 1997 4.46% | 1973 -11.39% | 1998 5.64% | 1966 -0.15% | |

| 1996 7.34% | 1971 -0.25% | 1997 1.57% | 1961 -0.32% | |

| 1995 4.10% | 1969 -3.41% | 1995 1.74% | 1957 -3.31% | |

| 1992 3.03% | 1965 -0.88% | 1994 1.26% | ||

| 1990 6.00% | 1964 -0.52% | 1993 0.98% | ||

| 1989 1.65% | 1963 -1.05% | 1992 1.01% | ||

| 1986 2.15% | 1956 -3.10% | 1991 11.19% | ||

| 1985 6.51% | 1951 -0.95% | 1990 2.48% | ||

| 1983 1.74% | 1950 -0.26% | 1989 2.14% | ||

| 1982 3.60% | 1988 1.48% | |||

| 1981 3.27% | 1987 7.28% | |||

| 1980 10.24% | 1985 4.51% | |||

| 1979 4.26% | 1984 2.24% | |||

| 1978 0.61% | 1982 1.50% | |||

| 1977 2.86% | 1979 1.68% | |||

| 1975 2.47% | 1978 1.16% | |||

| 1972 4.56% | 1977 0.28% | |||

| 1970 4.74% | 1976 5.25% | |||

| 1968 4.80% | 1973 1.79% | |||

| 1967 0.75% | 1972 1.18% | |||

| 1966 0.31% | 1971 8.62% | |||

| 1962 10.16% | 1970 5.68% | |||

| 1961 3.77% | 1967 2.63% | |||

| 1960 2.97% | 1965 0.90% | |||

| 1959 1.52% | 1964 0.39% | |||

| 1958 1.78% | 1963 2.44% | |||

| 1957 3.17% | 1962 1.35% | |||

| 1955 7.64% | 1960 5.08% | |||

| 1954 7.71% | 1959 2.03% | |||

| 1953 0.41% | 1958 4.78% | |||

| 1952 4.31% | 1956 1.50% | |||

| 1955 0.29% | ||||

| 1954 5.85% | ||||

| 1953 0.12% | ||||

| 1952 3.47% | ||||

| 1951 3.62% | ||||

| 1950 3.81% | ||||

While the last 31 days may have been distressing, at Sidoxia we understand that terrifying short-term volatility is a necessary requirement for long-term investors, if you desire the sweet appreciation of long-term gains. Fortunately at Sidoxia our long-term investors have benefited quite handsomely over the last 10 years from our half-glass-full perspective. The name Sidoxia actually is derived from the Greek word for “optimism” (aisiodoxia).

Performance has been fruitful in recent years, but the almost decade-long bull market has not been all smooth sailing (see Series of Unfortunate Events), as you can see from the undulating 10-year chart below (2008-2018). Do you remember the Flash Crash, Debt Ceiling, Greek Crisis, Arab Spring, Crimea, Ebola, Sequestration, and Taper Tantrum, among many other events? Similar to the volatility experienced in recent weeks, all these aforementioned events caused scary downdrafts as well.

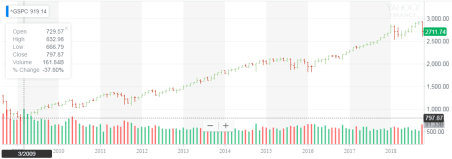

The S&P 500 hit a low of 666 in March 2009, but even with the significant fall last month, the stock market has more than quadrupled in value to 2,711 today.

The compounding benefits of long-term investing are quite evident over the last decade when you consider the record profits of the stock market. Compounding benefits apply to individual stocks as well, and Sidoxia and its clients have experienced this first hand through ownership in positions in stocks like Amazon.com Inc. (+2,692% in 10 years), Apple Inc. (+1,324%), and Google (parent Alphabet) (+507%), and many other less-familiar growth companies have allowed our client portfolios and hedge fund to outperform their benchmarks over longer periods of time. Although we are proud of our long-term performance, we have definitely had periods of under performance, and there will come a time in which a more defensive stance will be required. However, panicking is very rarely the best course of action when you are talking about your long-term investment strategy. Staying the course is paramount.

During periods of heightened volatility, like we experienced in October, the importance of owning a broadly diversified portfolio across asset classes (including stocks, bonds, real estate, commodities, emerging markets, growth, value, etc.) is worth noting. Of course an asset allocation should be followed according to a risk tolerance appropriate for your unique circumstances. As financial markets and interest rates gyrate, investors should get in the practice of rebalancing portfolios. For example, at Sidoxia, we are consistently harvesting our gains and opportunistically redeploying those proceeds into unloved areas in which we see better long-term appreciation opportunities. This whole investment process is designed for reducing risk and maximizing returns.

As in some famously scary stock market periods in the past, October turned out to be another frightening month for investors. The good news is that we have seen this scary movie many times in the past, and we have lived to tell the tale. The economy remains strong, corporate profits are at record levels and still rising, consumer and business confidence levels are near all-time highs, and interest rates remain historically low despite the Fed’s gradual interest rate hiking policy. While Halloween has definitely worried many investors, history tells us that previous tricks may turn into holiday treats!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, AMZN, GOOGL, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Dirty Little Stock Market Secret

Shhhh…don’t tell anyone, I have a dirty little secret. Are you ready? Are you sure? The world is not going to end…really.

Despite lingering trade concerns (see Trump Hits China with Tariffs on $200 Billion in Goods), Elon Musk being sued by the Securities and Exchange Commission (SEC) for tweeting his controversial intentions to take Tesla Inc. (TSLA) private, and Supreme Court nominee, Brett Kavanaugh, facing scandalous sexual assault allegations when he was in high school, life goes on. In the face of these heated headlines, stocks still managed to rise to another record in September (see Another Month, Another Record). For the month, the Dow Jones Industrial Average climbed +1.9% (+7.0% for 2018), the S&P 500 notched a +0.4% gain (+9.0% for 2018), while the hot, tech-laden NASDAQ index cooled modestly by -0.8% after a scorching +17.5% gain for the year.

If the world were indeed in the process of ending and we were looking down into the abyss of another severe recession, we most likely would not see the following tangible and objective facts occurring in our economy.

- New Revamped NAFTA (North American Free Trade Agreement) 2.0 trade deal between the U.S., Mexico, and Canada was finalized (new deal is called United States-Mexico-Canada Agreement).

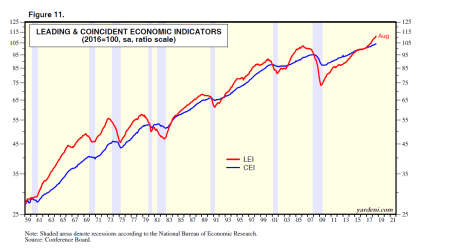

- Leading Economic Indicators are at a record high (a predictive statistic that historically falls before recessionary periods – in gray)

Source: Yardeni.com

- Unemployment Rate of 3.9% is near a record low

- Small Business Optimism is near record highs

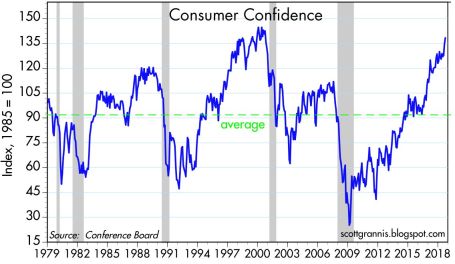

- Consumer Confidence is near record highs

Source: Scott Grannis

- Corporate Profits are at record highs

- Interest Rates remain at historically low levels despite the Federal Reserve’s actions to slowly migrate their interest rate target higher

- Economic Growth (GDP) accelerating to +4.2% growth rate in the recent quarter

Source: Scott Grannis

Are we closer to a recession with the stock market potentially falling 20-30% in value? As I have written on numerous occasions, so-called pundits have been falsely forecasting recessions over the last decade, for as long as this bull market has been alive (see Professional Double-Dip Guesses are “Probably” Wrong).

Why so much investor angst as stock prices continue to chug along to record levels? One reason is investors are used to historically experiencing a recession approximately twice a decade on average, and we have yet to suffer one since the Great Recession around 10 years ago. While the mantra “we are due” for a recession might be a true statement, the fact also remains that this economic recovery has been the slowest since World War II, which logically could argue for a longer expansionary period.

What also holds true is that corporate profits already experienced a significant “profit recession” during this economic cycle, post the 2008-2009 financial crisis. More specifically, S&P 500 operating profits declined for seven consecutive quarters from December 2014 through June 2016. The largest contributors to the 2014-2016 profit recession were collapsing oil and commodity prices, coupled with a rapid appreciation in the value of the U.S. dollar, which made our exports more expensive and squeezed multinational corporation profits. The stock market eventually digested these profit-crimping headwinds and resumed its ascent to record levels, but not before the S&P 500 remained flat to down for about a year and a half (2014-2016).

Doom-and-gloom, in conjunction with toxic politics, continue to reign supreme over the airwaves. If you want in on a beneficial dirty little secret, you and your investments would be best served by ignoring all of the media noise and realizing the world is not going to end any time soon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in TSLA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}