Posts tagged ‘Sir John Templeton’

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Brexit-Schmexit

Do you remember the panic-inducing headlines related to PIIGS, Crimea, Ebola, Cyprus, and the Flash Crash? Probably not. But if you do remember, these false alarms have likely been relegated to the financial memory graveyard, along with the many other sensationalist news events that have been killed off in the post-financial crisis era. Time will tell whether Brexit dies off or becomes a resurrected concern, like the repeating fears of a China slowdown or Greek collapse. Regardless, as the S&P 500 stock index reaches new all-time record highs, investors are currently shrug off the noise while muttering, “Brexit-Schmexit.”

Individuals have tried to use scary headlines as a timing tool to consistently time market corrections for all of recorded history. Unfortunately, emotional, knee-jerk reactions to alarming news stories rarely is the best strategy. Famed fund manager Peter Lynch said it best when he noted,

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Having invested for some 25 years, experience has taught me not only is conventional wisdom often wrong, but it also is frequently an accurate contrarian indicator. In other words, frightening news often should be an indicator to buy…not sell. Case in point is the U.K. European Union referendum. The Brexit referendum “Leave” vote caught virtually everyone by surprise, but the rebound in stock prices to new record highs may be even more surprising to most observers. However, for investors following the key factors of interest rates, profits, valuation, and sentiment (see also Don’t Be a Fool, Follow the Stool), may not be shocked by the positive price action.

- Interest Rates: For starters, you don’t have to be a genius to realize that stocks become more attractive when there is a scarcity of investment alternatives. When there are an estimated $13 trillion of negative interest rate bonds, a layman can quickly understand a 2%, 3%, or 4% dividend yield offered on certain stocks (and funds) can represent a much more attractive opportunity. With interest rates at record lows (see chart below), the overall dividend yield of stocks has provided a floor for stock prices and has limited the depth and duration of sell-offs and corrections.

Source: Calafia Beach Pundit

- Profits: Corporate profits are near record highs but have been sluggish due to several factors, including the negative impact of the strong dollar on multinational exports; the depressing effect of declining interest rates on the banking sector’s net interest profit margins; the general decline in oil and commodity prices; and general lethargic economic growth overall in international markets (emerging and developed economies). Encouragingly, a stabilization in the value of the U.S. dollar, along with a rebound in energy prices augurs well for a potential shift back to earnings growth in the coming quarters.

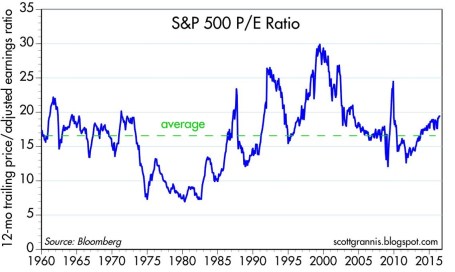

- Valuation: On a valuation basis, the Price/Earnings ratio of the stock market is about 10-15% above historical averages (see chart below). The average S&P 500 stock price trades around 19x’s the value of trailing twelve-month earnings. However, in the context of all-time record low-interest rates, a premium valuation is well deserved, especially for those companies paying a dividend and growing their bottom line.

Source: Calafia Beach Pundit

- Sentiment: Since the Great Financial Crisis / Recession, there has been about $1.5 trillion in equity investments that have been pulled out of U.S. equity mutual funds. This statistic is a clear sign of the extreme risk aversion and pervasive pessimism. Despite money flowing out of equity funds, corporations have bolstered the upward trajectory in stock prices with hundreds of billions in corporate stock buybacks and trillions in mergers & acquisition transactions. With all the universal jitteriness, I like to remind investors of Warren Buffett’s credo, “Buy fear, and sell greed.”

Brexit-Schmexit NOT Brexit-Panic

Despite the risk aversion in the marketplace, stock prices in the U.S. continue to grind higher to record levels. The stock market is currently communicating interest rates, profits, valuation, and sentiment are more important factors to price direction than are Brexit and other geopolitical concerns.

The silver lining behind severe investor skepticism is the creation of additional investment opportunities. As famous investor Sir John Templeton stated regarding stock market cycles, “Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.” Even the most objective observers have difficulty pointing to a broad set of indicators signaling euphoria, and the recent Turkish military coup attempt and domestic gun violence incidents will not squash out the negativity. Until optimism and elation rule the day, there’s no need to worry-schworry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sidoxia’s Investor Hall of Fame

Investing Caffeine has profiled many great investors over the months and years, so I thought now would be a great time to compile a “Hall of Fame” summarizing some of the greatest of all-time. Nothing can replace experience, but learning from the greats can only improve your investing results – I’ve benefitted firsthand and so have Sidoxia’s clients. Here is a partial list from the Pantheon of investing greats along with links to the complete articles (special thanks to Kevin Weaver for helping compile):

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

William O’Neil – After graduating from Southern Methodist University, O’Neil started his career as a stock broker. Soon thereafter, at the ripe young age of 30, O’Neil purchased a seat on the New York Stock Exchange and started his own company, William O’Neil + Co. Incorporated. Following the creation of his firm, O’Neil went on to pioneer the field of computerized investment databases. He used his unique proprietary data as a foundation to unveil his next entrepreneurial baby, Investor’s Business Daily, in 1984. (READ COMPLETE ARTICLE)

Sir John Templeton – After Yale and Oxford, Templeton moved onto Wall Street, borrowed $10,000 to purchase more than 100 stocks trading at less than $1 per share (34 of the companies were in bankruptcy). Only four of the investments became worthless and Templeton made a boatload of money. Templeton bought an investment firm in 1940, leading to the Templeton Growth Fund in 1954. A $10,000 investment made at the fund’s 1954 inception would have compounded into $2 million in 1992 (translating into a +14.5% annual return). (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

Bruce Berkowitz -Bruce Berkowitz has not exactly been a household name. With his boyish looks, nasally voice, and slicked-back hair, one might mistake him for a grad student. However, his results are more than academic, which explains why this invisible giant was recently named the equity fund manager of the decade by Morningstar. The Fairholme Fund (FAIRX) fund earned a 13% annualized return over the ten-year period ending in 2009, beating the S&P 500 by an impressive 14%. (READ COMPLETE ARTICLE)

Thomas Rowe Price, Jr. – Known as the “Father of Growth Investing,” in 1937 he founded T. Rowe Price Associates (TROW) and successfully ramped up the company before the launch of the T. Rowe Price Growth Stock Fund in 1950. Expansion ensued until he made a timely sale of his company in the late 1960s. His Buy and Hold strategy proved successful. For example, in the early 1970s, Price had accumulated gains of +6,184% in Xerox (XRX), which he held for 12 years, and gains of +23,666% in Merck (MRK), which he held for 31 years. (READ COMPLETE ARTICLE)

There you have it. Keep investing and continue reading about investing legends at Investing Caffeine, and who knows, maybe you too can join Sidoxia’s Hall of Fame?!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in MOT, TROW, XRX, MRK, FAIRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Gospel from 20th Century Investment King

Source: Compendius.com

Exceptional returns are not achieved by following the herd, and Sir John Templeton, the man Money magazine called the greatest global stock investor of the 20th century, followed this philosophy to an extreme. This contrarian, value legend put his money where his mouth was early on in his career. After graduating from Yale and becoming a Rhodes Scholar at Oxford, Templeton moved onto Wall Street. At the ripe young age of 26, and in the midst of World War II tensions, Templeton borrowed $10,000 (a lot of dough back in 1939) to purchase 100 shares in more than 100 stocks trading at less than $1 per share (34 of the companies were in bankruptcy). When all was said and done, only four of the investments became worthless and Templeton made a boatload of money. This wouldn’t be the end of Templeton’s success, but rather the beginning to a very long, prosperous career -Templeton ended up living a full life to age 95 (1912 – 2008).

Shortly after his penny stock buying binge in 1939, Templeton parlayed those profits into buying an investment firm in 1940 – this move served as a precursor for his Templeton Growth Fund that was launched in 1954. How successful was Templeton’s fund? So successful that an initial $10,000 investment made at the fund’s 1954 inception would have compounded into $2 million in 1992 (translating into a +14.5% annual return) when Templeton’s company was sold to Franklin Resources Inc. (BEN) for $913 million.

Mixing Religion & Science

But this pioneer of global investing didn’t stop after accumulating big bucks from all his investments. His pursuit for investment divinity was coupled with a thirst for spiritual knowledge. In 1987 he established the Templeton Foundation, which grew total assets to well north of $1 billion in the 2000s. The mission of the Templeton Foundation was to reconcile science and religion. Here is what Templeton had to say about the foundation:

“We are trying to persuade people that no human has yet grasped 1% of what can be known about spiritual realities. So we are encouraging people to start using the same methods of science that have been so productive in other areas, in order to discover spiritual realities.”

Going Against the Tide

Central to Templeton’s contrarian investment philosophy was to purchase superior stocks at cheap prices at points of “maximum pessimism.” Like a lot of excellent investors, Templeton was never afraid to go against the tide and make big bets.

In the 1960s, Templeton held more than 60% of his fund’s assets in Japan. More than three decades later he was astute enough to recognize the tech bubble in 1999 and to profit from this trend by shorting the tech sector. He famously predicted that 90% of the new internet companies would go bankrupt within five years.

Templeton’s Tutelage

Although Sir John Templeton is no longer with us, he has left numerous books and writings that investors of all shapes and sizes can draw upon. One of the best distilled pieces of knowledge distributed by Templeton is his 22 investment maxims.

1.) For all long-term investors, there is only one objective-“maximum total real return after taxes.”

2.) Achieving a good record takes much study and work, and is a lot harder than most people think.

3.) It is impossible to produce a superior performance unless you do something different from the majority.

4.) The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.

5.) To put “Maxim 4” in somewhat different terms, in the stock market the only way to get a bargain is to buy what most investors are selling.

6.) To buy when others are despondently selling and to sell what others are greedily buying requires the greatest fortitude, even while offering the greatest reward.

7.) Bear markets have always been temporary. Share prices turn upward from one to twelve months before the bottom of the business cycle.

8.) If a particular industry or type of security becomes popular with investors, that popularity will always prove temporary and, when lost, won’t return for many years.

9.) In the long run, the stock market indexes fluctuate around the long-term upward trend of earnings per share.

10.) In free-enterprise nations, the earnings on stock market indexes fluctuate around the book value of the shares of the index.

11.) If you buy the same securities as other people, you will have the same results as other people.

12.) The time to buy a stock is when the short-term owners have finished their selling, and the time to sell a stock is often when the short-term owners have finished their buying.

13.) Share prices fluctuate more widely than values. Therefore, index funds will never produce the best total return performance.

14.) Too many investors focus on “outlook” and “trend.” Therefore, more profit is made by focusing on value.

15.) If you search worldwide, you will find more bargains and better bargains than by studying only one nation. Also, you gain the safety of diversification.

16.) The fluctuation of share prices is roughly proportional to the square root of the price.

17.) The time to sell an asset is when you have found a much better bargain to replace it.

18.) When any method for selecting stocks becomes popular, then switch to unpopular methods. As has been suggested in “Maxim 3,” too many investors can spoil any share-selection method or any market-timing formula.

19.) Never adopt permanently any type of asset, or any selection method. Try to stay flexible, open-minded, and skeptical. Long-termy changing from popular to unpopular the types of securities you favor and your methods of selection.

20.) The skill factor in selection is largest for the common-stock part of your investments.

21.) The best performance is produced by a person, not a committee.

22.) If you begin with prayer, you can think more clearly and make fewer stupid mistakes.

Sir John Templeton lived a rich life of many interests spanning investments, science, and religion. Applying a few points of this investor of the 20th century can only improve your results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in BEN, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}