Posts tagged ‘share repurchase’

NVEC: A Cash Plump Activist Target…For Icahn?

Some might call Carl Icahn a greedy capitalist, but at the core, the 78 year old activist has built his billions in fortunes by unlocking shareholder value in undervalued companies. His targets have come in many shapes and sizes, but one type of target is cash bloated companies without defined capital allocation strategies. A recent high profile example of a cash ballooned target of Icahn was none other than the $591+ billion behemoth Apple Inc. (AAPL).

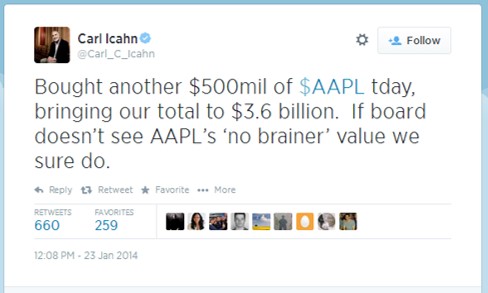

His initial tweet on August 13, 2013 announced his “large position” in the “extremely undervalued shares” of Apple ($67 split adjusted). We have been long-term shareholders of Apple ourselves and actually beat Carl to the punch three years earlier when the shares were trading at $35 – see Jobs: The Gluttonous Cash Hog. Icahn doesn’t just nonchalantly make outrageous claims…he puts his money where his mouth is. After Icahn’s initial proclamation, he went onto build a substantial $3.6 billion Apple position by January 2014.

Icahn initially demanded Apple’s CEO Tim Cook to execute a $150 billion share repurchase program before downgrading his proposal to a $50 billion buyback. After receiving continued resistance, Icahn eventually relented in February 2014. But Icahn’s blood, sweat, and tears did not go to waste. His total return in Apple from his initial announcement approximates +50%, in less than one year. And although Icahn wanted more action taken by the company’s management team, Apple has repurchased about $50 billion in stock and paid out $14 billion in dividends to investors over the last five quarters. Despite the significant amount of capital returned to shareholders over the last year, Apple still holds a gargantuan net cash position of $133.5 billion, up approximately $3 billion from the 2013 fiscal third quarter.

Icahn’s Next Cash Plump Target?

Mr. Icahn is continually on the prowl for new targets, and if he played in the small cap stock arena, NVE Corp. (NVEC) certainly holds the characteristics of a cash bloated company without a defined capital allocation strategy. Although I rarely write about my hedge fund stock holdings, followers of my Investing Caffeine blog may recognize the name NVE Corp. More specifically, in 2010 I picked NVEC as my top stock pick of the year (see NVEC: Profiting from Electronic Eyes, Nerves & Brains). The good news is that NVEC outperformed the market by approximately +25% that year (+36% vs 11% for the S&P 500). Over the ensuing years, the performance has been more modest – the +42% return from early 2010 has underperformed the overall stock market.

Rather than rehash my whole prior investment thesis, I would point you to the original article for a summary of NVE’s fundamentals. Suffice it to say, however, that NVE’s prospects are just as positive (if not more so) today as they were five years ago.

Here are some NVE data points that Mr. Icahn may find interesting:

- 60% operating margins (achieved by < 1% of all non-financial companies FINVIZ)

- 0% debt

- 15% EPS growth over the last seven years ($1.00 to $2.29)

- Cutting edge, patent protected, market leading spintronic technology

- +7% Free Cash Flow yield ($13m FCF / $194 adjusted market value) $294m market cap minus $100m cash.

- $100 million in cash on the balance sheet, equal to 34% of the company’s market value ($294m). For comparison purposes to NVE, Apple’s $133 billion in cash currently equates to about 23% of its market cap.

Miserly Management

As I noted in my previous NVE article, my beef with the management team has not been their execution. Despite volatile product sales in recent years, it’s difficult to argue with NVE CEO Dan Baker’s steering of outstanding bottom-line success while at the helm. Over Baker’s tenure, NVE has spearheaded meteoric earnings growth from EPS of $.05 in 2009 to $2.29 in fiscal 2013. Nevertheless, management not only has a fiduciary duty to prudently manage the company’s operations, but it also has a duty to prudently manage the company’s capital allocation strategy, and that is where NVE is falling short. By holding $100 million in cash, NVE is being recklessly conservative.

Is there a reason management is being so stingy with their cash hoard? Even with cash tripling over the last five years ($32m to $100m) and operating margins surpassing an incomprehensibly high threshold (60%), NVE still has managed to open their wallets to pursue these costly actions:

- Double Capacity: NVE doubled their manufacturing capacity in fiscal 2013 with minimal investment ($2.8 million);

- Defend Patents: NVE fought and settled an expensive patent dispute against Motorola spinoff (Everspin) as it related to the company’s promising MRAM technology;

- R&D Expansion: The company shored up its research and development efforts, as evidenced by the +39% increase in fiscal 2014 R&D expenditures, to $3.6 million.

The massive surge in cash after these significant expenditures highlights the indefensible logic behind holding such a large cash mound. How can we put NVE’s pile of cash into perspective? Well for starters, $100 million is enough cash to pay for 110 years of CAPEX (capital expenditures), if you simply took the company’s five year spending average. Currently, the company is adding to the money mountain at a clip of $13,000,000 annually, so the amount of cash will only become more ridiculous over time, if the management team continues to sit on their hands.

To their credit, NVE dipped half of a pinky toe in the capital allocation pool in 2009 with a share repurchase program announcement. Since the share repurchase was approved, the cash on the balance sheet has more than tripled from the then $32 million level. To make matters worse, the authorization was for a meaningless amount of $2.5 million. Over a five year period since the initial announcement, the company has bought an irrelevant 0.5% of shares outstanding (or a mere 25,393 shares).

A Prudent Proposal

The math does not require a Ph.D. in rocket science. With interest rates near a generational low, management is destroying value as inflation eats away at the growing $100 million cash hoard. I believe any CFO, including NVE’s Curt Reynders, can be convinced that earning +7% on NVE shares (or +15% if earnings compound at historical rates for the next five years) is better than earning +2% in the bank. Or in other words, buying back stock by NVE would be massively accretive to EPS growth. Conceptually, if NVE used all $100 million of its cash to buy back stock at current prices, NVE’s current EPS of $2.59 would skyrocket to $3.63 (+40%).

A more reasonable proposal would be for NVE management to buy back 10% of NVE’s stock and simultaneously implement a 2% dividend. At current prices, these actions would still leave a healthy balance of about $75 million in cash on the balance sheet by the end of the fiscal year, which would arguably still leave cash at levels larger than necessary.

Despite the capital allocation miscues, NVE has incredibly bright prospects ahead, and the recently reported quarterly results showing +37% revenue growth and +57% EPS growth is proof positive. As a fellow long-term shareholder, I share management’s vision of a bright future, in which NVE continues to proliferate its unique and patented spintronic technology. With market leadership in nanotechnology sensors, couplers, and MRAM memory, NVE is uniquely positioned to take advantage of game changing growth in markets such as nanotechnology biosensors, electric drive vehicles (EDVs), consumer electronic compassing, and next generation MRAM technology. If NVE can continue to efficiently execute its business plan and couple this with a consistent capital allocation discipline, there’s no reason NVE shares can’t reach $100 per share over the next three to five years.

While NVE continues to execute on their growth vision, they can do themselves and their shareholders a huge favor by implementing a shareholder enhancing capital return plan. Carl Icahn is all smiles now after his successful investments in Apple and Herbalife (HLF), but impatient investors and other like-minded activists may be lurking and frowning, if NVE continues to irresponsibly ignore its swelling $100 million cash hoard.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in Apple Inc. (AAPL), NVE Corp. (NVEC), and certain exchange traded funds, but at the time of publishing SCM had no direct position in TWTR, MOT, Everspin, HLF, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Share Buybacks and Bathroom Violators

We all have our own unique pet peeves that drive us crazy, and I am no exception. More grating than fingernails scraping down the chalkboard or rude drivers who refuse to let you merge lanes are those citizens that unabashedly exercise poor public bathroom etiquette. The only thing worse than listening to the loud-mouth cell phone talker in the neighboring stall is watching a restroom participant move straight from zipper closure (if they remember), immediately to the bathroom exit. I mean really, would it kill you at a minimum to pay a visit to the sink and feign a phantom hand-swipe under some running water? Don’t those people understand that I have to grab the same handle they use to exit the facility after they conduct their bathroom business? OK, now that I have gotten this issue off my chest, I feel better and I can get off my soapbox (no pun intended).

Something Stinks in Share Buyback Land

Beyond potty etiquette, there is another maddening pet peeve that drives me nuts in the realm of corporate capital allocation. I like to call this particular scheme the “empty share buyback.” Those companies that announce the empty share buyback do it with the intention of either getting a quick, short-term jump in stock price, or use the ploy as a way to indirectly line their pockets with future stock and option grants.

Here are a few ways on how the ruse works:

Scheme #1 – The Empty Pump-Fake: In one form or another, here is what the CEO basically says, “We plan to buyback zillions of shares from time to time, based on market conditions, and do not have any set expiration date for the plan.” In other words, the company executives are committing to absolutely nothing, but are hoping to confuse traders into buying shares to temporarily increase the stock price, so management can unload their shares for a swift profit. In actuality the management team is not obligated to purchase one share and may keep the pseudo-share buyback plan in place for years with no benefit to shareholders.

Scheme #2 – The Pocket Swap: Another one of my favorites, I like to call the pocket swap. Management effectively exchanges money from one pocket to the other. Typically management starts off by stating, “We treasure investor feedback, so we have initiated a new program to return capital to our valued shareholders in the form of a share buyback.” What they usually don’t tell investors is that the shares are being purchased (with shareholder money), so the executives can give more shares back to themselves (and a few other fortunate employees). That’s great for them, but what about me?!

At the end of the day, if the management team is truly working for the shareholder, the game is all about reducing the outstanding share count, which thereby increases earnings per share (and better yet free cash flow per share). Despite the recent climb in interest rates, yields are still near multi-decade lows. Corporations are flush with cash after cutting expenses to the bone, delaying hiring, and riding the global recovery wave. For those real investors not trading a position for a few days, weeks, or months, it behooves you to hold management’s feet to the fire to make sure “empty pump-fakes” or “pocket swap” share buybacks are not occurring.

If you have difficulty gauging the integrity of those management teams announcing share buybacks, I have a litmus test that can be used to judge the executive’s true intentions. It’s quite simple – just follow the CEO into the bathroom (same gender required) and see whether they honorably follow bathroom etiquette by washing their hands after completing their duty. Sleuth work can be tricky, but failure in determining the genuine purpose of management’s capital allocation decisions can lead to a share buyback program that will get flushed down the toilet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Microsoft Makes Dividend Splash

Source: ActingLikeAnimals.com

I’ve talked about growing profits and cash piles for a while now (read more), but at some point investors and board members get restless and demand action (Steve Jobs has not yet). The most recent blue-chip company to make a splash, when it comes to capital management, is Microsoft Corp. (MSFT), which just announced a significant +23% increase in its dividend in conjunction with $4.75 billion in debt offerings. These capital structure changes still leave plenty of room for additional share repurchases and acquisitions.

Debt Offering – Are You Sure?

Huh? What in the heck is Microsoft doing borrowing money? I mean, does a company with $44 billion in cash and investments, generating a whopping additional $22 billion in free cash flow in fiscal 2010 (ended in June), really need access to additional capital? The short answer is “NO.” But a company like Microsoft borrowing $4.75 billion is like Donald Trump borrowing $50 on his credit card. Well wait, “The Donald” has actually had some hair and Chapter 11 problems, so the more appropriate analogy would be Bill Gates borrowing $20 on his credit card. Not only is it a rounding error, but it’s a good financial management practice for corporations to take advantage of the debt tax shield (read definition).

What makes Microsoft’s debt issuance that much more incredible is the astonishingly low rates the company is paying investors on the debt. According to Dealogic, Microsoft set a record low for yield paid on corporate unsecured debt. For the separate maturities ranging from 2013 to 2040, Microsoft paid a stunningly low 25-83 basis point spread over Treasuries. I don’t want to get into government credit worthiness today, but who knows, maybe Microsoft will pay lower debt rates than the U.S. Treasury, in the not too distant future?!

Regardless of the array of capital structure management strategies used by other companies, Microsoft is not alone in dealing with its cash hoarding problems. Cisco Systems Inc. (CSCO), another blue-chip cash printing press, just announced the initiation of a 1-2% dividend to be paid by the end of their fiscal year ending in July 2011 (read more about dividend cash “un-hoarding”).

But Who Cares?

Who cares about Microsoft’s wimpy 2.62% yield anyway? Well, for one, I sure care! A 10-year Treasury Note is yielding a measly, static 2.55%. If Microsoft continued on the same dividend path growth over the next five years as it did over the last five years, investors could potentially be talking about a 5.2% yield on our initial investment, and this excludes any potential stock price appreciation. With only roughly a 25% payout ratio on Microsoft’s fiscal 2010 free cash flow, the company has a lot of freedom to hike future dividends, even if earnings don’t grow. Microsoft has also enhanced shareholder value by putting its money where its mouth is by purchasing over $30 billion of company stock over the last three years.

Nice trend in dividend growth.

The extreme case of dividend growth is Wal-Mart Stores (WMT), which if purchased in 1972 would provide a +2,300% yield on the original investment, excluding any benefit from the massive price appreciation ($.05 split-adjusted per share to $53.65). Microsoft is no young chick like Wal-Mart 40 years ago, but you get the gist (read Dividend Sapling to Fruit Tree).

So while strategists and economists fret about the possibilities of a “double dip” recession, in the interim there have been 179 companies in the S&P 500 index that have hiked dividends in 2010 (versus only 3 companies that have cut). Microsoft has been no slouch either, growing revenues by +22% and EPS (Earnings Per Share) by +50% in their most recent fiscal fourth quarter. Although Microsoft’s stock is down -20% for 2010, the capital management and dividend splash recently announced by Microsoft (and other companies) should eventually capture the eye of investors currently earning squat on overpriced bonds and almost worthless Certificates of Deposit.

Read complete Microsoft dividend story

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, CSCO, nd WMT, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}