Posts tagged ‘Saving’

Invest or Die

Seventy-six million Baby Boomers are earning near 0% (or negative rates) and aren’t getting any younger in the process, which is forcing them and others to decide…invest or die. The risk of outliving your savings is becoming a larger reality these days. Demographics and economics are dictating that our aging population is living longer and earning less due to generationally low interest rates.

Richard Fisher, the former Dallas Federal Reserve president, understands these looming dynamics. Fisher has identified how low-interest rates are increasing investor discontent by pushing consumers to save more in order to meet retirement needs. The unintended consequence from low rates, he said, is “you’re going to have to save a hell of a lot more before you consume.”

Besides saving, the other option investors have is to lower your standard of living. For example, you could continually eat mac & cheese and sleep in a tent – that is indeed one way you could save money. However, your kids and/or desired lifestyle may make this way of life unpalatable for all. Rather, the proper approach to achieving a comfortable standard of living requires you to invest more efficiently and prudently.

What a lot of individuals fail to understand is that accepting too much risk can be just as dangerous as being too conservative, over the long run. Case in point, depositing your savings into a CD at current interest rates (near 0%) is the equivalent of burning your cash, as any income produced is overwhelmed by the deleterious effects of inflation. It would take more than a lifetime of CD interest income to equal equity returns earned over the last seven years. Since early 2009, stocks have more than tripled in value.

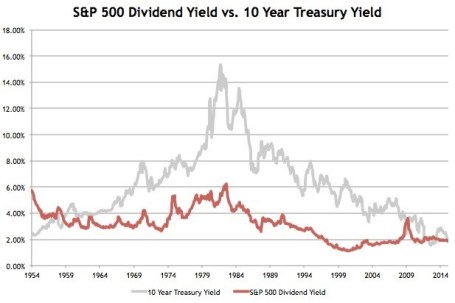

Given the prevailing economic and demographic trends, investors are slowly realizing the attractive income-producing nature of stocks relative to bonds. It has been a rare occurrence, but stocks, as measured by the S&P 500, continue to yield more than 10-Year Treasury Notes (2.0% vs. 1.6%, respectively) – see chart below. The picture for bonds looks even worse in many international markets, where $13 trillion in bonds are yielding negative interest rates. Unlike bonds, which generally pay fixed coupon payments for years at a time, stocks overall have historically increased their dividend payouts by approximately 6% annually.

Source: Avondale Asset Management

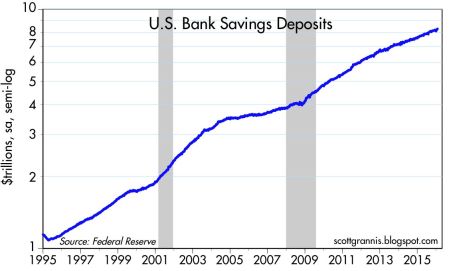

With a scarcity of attractive investment alternatives available, investors will eventually be forced to adopt higher levels of equity risk, like it or not. However, this dynamic has yet to happen. Currently, actions are speaking louder than words, and as you can see, risk aversion reigns supreme with Americans tucking over $8 trillion dollars under their mattress (see chart below), in the form of savings accounts, earning next to nothing and jeopardizing retirements.

Source: Calafia Beach Pundit

Even if you fall into the camp that believes rates are artificially low by central bank printing presses, that doesn’t mean every company is recklessly leveraging their balance sheets up to the hilt. Many companies are still scared silly from the financial crisis and conservatively managing every penny of expense, like a stingy retiree living on a fixed income. Thanks to this reluctance to spend and hire aggressively, profit margins are at/near record highs. This financial stewardship has freed up corporations’ ability to pay higher dividends and implement discretionary stock buybacks as means to return capital to shareholders.

With the dovish Fed judiciously raising interest rates – only one rate hike of 0.25% over a decade (2006 – 2016) – there are no signs this ultra-low interest rate environment is going to turn aggressively higher anytime soon. Until economic growth, inflation, and interest rates return with a vengeance, and the persistent investor risk aversion abates, it behooves all the cash hoarders to….invest or die!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Compounding: A Penny Saved is Billions Earned

What is “compounding” and why is it so great? It sounds like such a fancy financial term. One can think of compounding as a snowball rolling down a hill – the longer the snowball rolls (or the higher up the mountain you begin), the more compounding will expand the size of your snowball. Expanding your investment portfolio through compounding should be your major goal.

Albert Einstein, arguably one of the most intelligent people to walk this planet, was asked to describe mankind’s greatest discovery. His answer: “compound interest.” He went so far as to call it one of the “Eight Wonders of the World.” The benefits of compounding can be demonstrated via famous explorer, Christopher Columbus.

We all know the story, “In 1492, Christopher Columbus sailed the ocean blue.” To emphasize the benefits of compounding, let us suppose that Christopher Columbus made an investment in the historic year of 1492. If Chris had placed a single penny in a 6% interest-bearing account and instructed someone to remove the interest every year and put it in a piggybank, the total value collected in that piggybank would eventually accumulate to more than 30 cents. A pretty nice multiplier-effect on one penny, but not too much absolute cold hard cash to write home about…agreed?

"It's magic, I can turn pennies into billions."

However, if the young explorer had placed the same paltry investment of one cent into the same interest-bearing account, but LEFT the remaining earned interest to compound (thereby earning interest upon the previously earned interest) the results would be drastically different.

What would you guess the compounded account would be worth in 2009?

$10,000? $100,000? $1 million? $10 million? $100 million?

“NO” is the correct answer to all these guesses.

The correct answer: $121,096,709,346.21! Your eyes do not deceive you. That one penny invested in 1492 would have grown to $121 billion dollars today. If you don’t believe me, pull out your calculator and multiply $.01 * 1.06%, and repeat 517 times. Surely, we will not live 517 years to collect on an investment of such long duration. However, with proper planning everyone has the ability to invest quite a bit more than one cent to significantly build future wealth.

As an advisor, the problems related to compounding I see investors commit most are two-fold:

1) Investors are constantly shifting money in and out of their accounts (usually at suboptimal points) due to apprehension and greed, thereby nullifying the benefits of compounding.

2) Because of overpowering fear relating to current economic conditions, investors are parking their money in low yielding CDs (Certificates of Deposit), savings accounts, checking accounts, money market accounts, or other low returning investment vehicles. This strategy is equivalent to pushing the aforementioned snowball over the sidewalk, rather than down a long, steep hill.

In order to reap the rewards of compounding and dramatically expand your investment portfolio, a systematic, disciplined approach to investing needs to be followed. A system that more likely than not has a 20 year horizon rather than 20 days. Now go start saving those pennies!

Avoid Chasing Your 401k Tail

David Laibson, a professor of economics at Harvard University, has done extensive research on the savings habits of Americans in their 401k retirement accounts. What he discovers is that workers, like a dog chasing their tail, allocate more of their investments to the areas that have done well and sell the underperforming segments. In short, workers attempt to “time the market.”

Professor Laibson demonstrates this pyramiding strategy has not worked out so well and provides the following advice:

“We know that individual investors are terrible in terms of their market timing. They tend to buy at the tops, they tend to sell at the bottoms. So don’t try to time the market. Don’t think about recouping – just think about a long term strategy.”

That long term strategy he advocates entails a diversified allocation of stocks and bonds that reduces exposure to equities as a person gets older. In short, he says, “Hold a diversified portfolio appropriate for your age.”

He advises those aged in their 20s and 30s to allocate nearly 100% of their portfolio to equities, or investments with commensurate risk. Alternatively, if investors don’t want to adjust the allocation themselves, people should consider life-cycle funds or Self Directed 401k options (Read story here). For those in retirement, he recommends a portfolio with the following characteristics:

“30, 40, 50% should be equities, more as you’re younger…simply hold a long term portfolio with less and less allocation to equities as you age.”

Jason Zweig, a journalist at The Wall Street Journal, recently chimed in with similar thoughts on performance chasing:

“…to buy more of what has gone up, precisely because it has gone up, is to fall for the belief that stocks become safer as their prices rise. That is the same fallacy that led investors straight into disaster in 1929, 1972, 1999, 2007 and every other market bubble in history.”

There are many different strategies for making money in the market, but a plan based solely on emotion is doomed for failure – Professor Laibson’s data supports that assertion. So the next time you are considering re-allocating the mix of investments in your 401k, implement a disciplined, systematic approach. That approach should include the following:

1) Invest Your Age in Fixed Income Securities. John Bogle, Chairman at Vanguard Group, has long made this argument, with the balance placed in equities. For example a sixty year old should have 60% of their assets in bonds and 40% in stocks. This rule of thumb is a good starting point, but the picture becomes cloudier once you account for other assets such as real estate, convertible bonds, and income generated from private businesses.

2) Periodically Rebalance. Rather than investing more into outperforming areas, harvest your gains and redeploy into underperforming segments of your asset allocation. There obviously is an art to knowing “when to hold them and when to fold them,” nonetheless I concur with Professor Laibson that chasing winners is not the proper strategy.

3) Diversify. Spread your assets across multiple asset classes, segments, and styles, including equities, fixed income, commodities, real estate, inflation protection, growth, value, etc. Too much concentration in any one category can really come back to haunt you.

The key to successful retirement planning is to implement an unemotional systematic approach, so you don’t end up chasing your 401k tail.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: At the time of publishing, Sidoxia Capital Management and some of its clients owned certain exchange traded funds, but had no direct positions in any other security referenced.

Tips for Survival and Prosperity in Challenging Economic Times

Survival requires multiple strategies

We have all been impacted in some shape or form by the worst financial crisis experienced in a generation. The question now becomes what did we learn from this mess and how can we better prepare for a more prosperous financial future?

Here are some important tips to follow:

Save and Invest: Before paying others, pay yourself first. You can achieve this goal by saving and investing your money. Given the weak state of our government “safety net” programs, such as Medicare and Social Security, it has become more important than ever to save. Life spans are extending as well, meaning a larger “nest egg” is needed for retirement. If you don’t have the time, discipline, or emotional make-up to manage your own money, then seek out a fee-only advisor* who does not have a conflict of interest in regards to building your wealth.

Tighten Belt: In order to save and invest you need to be in a position where you are creating excess income. Cutting costs is one way to generate additional income. Eating out less, buying used, taking more affordable vacations, conserving energy, purchasing private label goods are a few easy ways to save money that will accumulate over time. If those efforts are still not adequate, one should then contemplate adjusting their living situation (i.e., down-size) or pursue additional income opportunities – either through a pay raise or higher paying job alternatives.

Pay Down Debt: If your credit card company is charging you a 15-20% rate on unpaid credit card balances and gouging you for late-fees and cash advances, then look for other sources of affordable financing. A home equity line of credit or second mortgage may make sense for some, if the fees and lower interest rates make economic sense. Contact a financial planner or tax professional to determine the appropriateness of these debt alternatives. Ultimately, the goal is to reduce debt and create more financial flexibility.

Take Free Money: If your employer offers matching payments to your retirement plan contributions, they are effectively offering you free money. Take it! The government offers you some tax deferral savings through IRA (Individual Retirement Account) contributions, so take advantage of that benefit as well.

Form a 6-Month Emergency Fund: The economy may be in a bottoming-out phase; however we are not out of the woods yet. Unemployment is approaching 10% and many companies and industries continue to struggle. Build a protective financial cushion should you or your family hit a bump in the road.

Invest in Yourself: Investing for retirement is crucial, however investing in yourself is just as, if not more, important than traditional investing. What I’m referring to is job training, education, and health awareness. We live in a globalized economy and in order to compete against those starving for our jobs, we need to improve our skills and education. Lastly, we cannot neglect our health. Finances need to be put in perspective. Our health should be a top priority and a disciplined balance between diet and exercise will not only reduce stress, but it will also improve mental health.

Times have been challenging, but when the going gets rough, the tough go saving. Take control of your financial future rather than letting economic circumstances control you. Financial success however should not come at the expense of your health, so also focus on a balanced program of diet and exercise. There are no free lunches in this world, but following these steps will help lead you on a path to prosperity – even in these challenging economic times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Wade W. Slome, CFA, CFP is President and Founder of Sidoxia Capital Management, LLC (www.Sidoxia.com), a fee-only Registered Investment Advisory firm headquartered in Newport Beach, California.

Building Your Financial Future – Mistakes Made in Investment Planning

Building Your Dream Future Requires a Plan

Building your retirement and financial future can be likened with the challenge of designing and building your dream home. The tools and strategies selected will determine the ultimate cost and outcome of the project.

I constantly get asked by investors, “Wade, is this the bottom – is now the right time to get in the markets?” First of all, if I precisely knew the answer, I would buy my own island and drink coconut-umbrella drinks all day. And secondarily, despite the desire for a simple, get-rich quick answer, the true solution often is more complex (surprise!). If building your financial future is like designing your dream home, then serious questions need to be explored before your wealth building journey begins:

1) Do I have enough money, and if not, how much money do I need to develop my financial future?

2) Can I build it myself, or do I need the help of professionals?

3) Do I have contingency plans in place, should my circumstances change?

4) What tools and supplies do I need to effectively bring my plans to life?

Most investors I run into have no investment plan in place, do not know the costs (fees) of the tools and strategies they are using, and if they are using an advisor (broker) they typically are in the dark with respect to the strategy implemented.

For the “Do-It-Yourselfers”, the largest problem I am witnessing right now is excessive conservatism. Certainly, for those who have already built their financial future, it does not make sense to take on unnecessary risk. However, for most, this is a losing strategy in a world laden with inflation and ever-growing entitlements like Medicare and Social Security. There’s clearly a difference between stuffing money under the mattress (short-term Treasuries, CDs, Money Market, etc.) and prudent conservatism. This is a credo I preach to my clients.

In many cases this conservative stance merely compounds a previous misstep. Many investors undertook excessive risk prior to the current financial crisis – for example piling 100% of investment portfolios into five emerging market commodity stocks.

What these examples prove is that the average investor is too emotional (buys too much near peaks, and capitulates near bottoms), while paying too much in fees. If you don’t believe me, then my conclusions are perfectly encapsulated in John Bogle’s (Vanguard) 1984-2002 study. The analysis shows the average investor dramatically underperforming both the professionally managed mutual fund (approximately by 7% annually) and the passive (“Do Nothing”) strategy by a whopping 10% per year.

Building your financial future, like building your dream home, requires objective and intensive planning. With the proper tools, strategies and advice, you can succeed in building your dream future, which may even include a coconut-umbrella drink.

{kind=link}