Posts tagged ‘robotics’

The Fallacy Behind Populism and Automation Fears

The rise of global populism and anti-immigration sentiments, coupled with the perpetual rising trend of automation and robotics has stoked the fear fires of job security. Many stories perpetuate erroneous stereotypes and falsehoods. The news reports and blog articles come in various flavors, but in a nutshell the stories state the U.S. is hemorrhaging jobs due to the thieves of illegal immigration and heartless robotics. The job displacement theory is built upon the idea that these two sources of labor (immigrants & robots) are cheaper and more productive than traditional blue collar and white collar American workers.

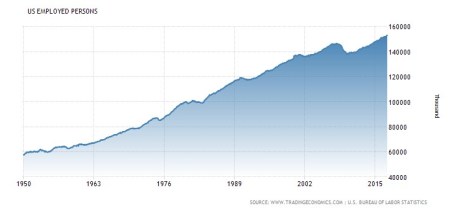

Although these logical beliefs make for great soundbites, and may sell subscriptions and advertising, unfortunately the substance behind the assertions holds little water. Let’s take a look at the facts. In the most recent April jobs report, nonfarm payrolls employment increased by 211,000 jobs, according to the U.S. Bureau of Labor Statistics. Since early 2009 the unemployment rate has plummeted from 10.0% down to a historically low level of 4.4%. Over the similar timeframe, the economy has added over 15,000,000 new jobs. Does this sound like an environment in which immigrants and robots are killing all American jobs?

Sounds like a bunch of phoney-baloney, if you ask me. Just look at the employed person chart below, which shows a rising employment trend over the last seven decades, with the exception of some brief recessionary periods.

As I point out in a previous article (see Rise of the Robots), from the beginning of the United States, the share of the largest segment of the economy (agriculture) dropped by more than 98%, yet the standard of living and output in the agriculture sector have still exploded. There may not have been robots two and a half centuries ago, but technology and automation were alive and well, just as they are today. Although there were no self-driving cars, no internet, no biotech drugs, and no mobile phones, there were technological advances like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds over time.

Source: Carpe Diem

And while there most certainly were farmers who regrettably were displaced by these technologies, there were massive new industries fostered by the industrial revolution, which redeployed labor to new burgeoning industries like manufacturing, aerospace, transportation, semiconductors, medicine, and many more.

While it may be difficult to fathom what industries will replace the workers displaced by self-service kiosks at restaurants, airports, and retail stores, famed economist Milton Friedman summed it up best when he stated:

“Human wants & needs are infinite, and so there will always be new industries, there will always be new professions.”

As globalization and technology continue permeating through society, it is true, the importance of education becomes more critical. Billions of people around the globe in developing markets, along with automation technology, will be stealing lower-paying American jobs that require repetitive processes. Educating our workforce up the value-add food chain is imperative.

The bottom-line is that integration of technology and automation will improve the standard of living for the masses. Sure, immigration will displace some workers, but if legislative policy can be designed to cherry-pick (attract) the cream of the skilled foreign crop (and retrain displaced workers), skilled immigrants will keep on innovating and creating higher valued jobs. Just consider a recent study that shows 51% of U.S. billion-dollar startups were founded by immigrants.

The populist drum may continue to pound against immigration, and horror stories of job-stealing robots may abound, however the truth cannot be erased. Over the long-run, the fallacies behind populism and automation will be uncovered. The benefits and truths surrounding highly skilled immigrants and robots will be realized, as these dynamics dramatically improve the standard of living and productivity of our great economy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Tech Toy Time

Why would I and 175,000 other humans from over 150 countries possible gather in one spot to look and play with a bunch of toys and gadgets? The answer can be explained with three letters…CES, otherwise known as the Consumer Electronics Show, which has been held primarily in Las Vegas, Nevada since 1967 – a few years before I was born. More than 7,500 media professionals from around the world also attended the world’s largest consumer technology tradeshow to write millions of online articles and messages about the latest and greatest hardware, software, and services.

I have attended CES multiple times, but more amazing than the massive scale of the 2.5 million square feet of exhibition space is the pace and magnitude of the innovation.

With approximately 4,000 exhibiting companies showing off their gadgets and services, you can probably imagine there were quite a few categories flaunted, including the following:

- Drones

- Augmented & Virtual Reality

- Internet of Things (IoT) and Smart Home Technologies

- Televisions, Televisions, and more Televisions

- Driverless Cars

- 3D Printers

- Robotics

- Wearables

- Electronic Gaming

- Automobile Entertainment/Audio

As I point out in the Birth of Silicon Valley – Traitorous 8, even after 50 years, “Moore’s Law” is still alive and well today. Moore’s Law, which was established by the Intel Corporation (INTC) founder Gordon Moore, states the number of transistors (i.e., a chip’s computing power) generally doubles every 1-2 years. CES epitomized the Moore’s Law trend, which has allowed technology companies to make hardware exponentially faster, smaller, and more battery efficient (i.e., longer life).

Accelerating Innovation

Moore’s Law has contributed to the acceleration of innovation by driving storage costs down a constant path towards zero, while semiconductor technology continues to explode computing power at the edge of networks (cell phones) and at the core of networks (the “cloud”). There are already approximately five billion cell phone subscribers worldwide, and two billion of those are effectively supercomputers in the form of smartphones. This global mobile computing explosion has opened up an infinite number of potential applications, limited only by the number of creative ideas. Many new and existing killer applications are being created by the multi-billion dollar cloud-based data centers that Amazon Web Services (AWS) and other competing tech behemoths are creating. The glue necessary to connect the explosion of computing power at the core and edge is software, which is why there is such massive demand for software programmers (“coders”) in Silicon Valley.

I found the advancements in augmented reality, connected homes, and drones to be especially fascinating areas at the show, but here are a couple of the more quirky finds I discovered:

One S1 Segway: Yes, it’s true that Hoverboards literally caught fire last holiday season, but CES highlighted a sister product, the One S1 Segway at the show. Essentially the gadget is a miniature unicycle that meets mobile phone app. I captured a brief video here:

Petcube: As a pet owner, I was also intrigued by Petcube, a cloud-based interactive pet monitor service that allows consumers to remotely communicate and play with their pets through their phones. In addition to speaking to the pet through the Petcube, the user can also remotely play with their pet by activating a moving laser. The company also has made a remote treat-dispensing device to reward and feed lonely pets. Here is a video summary:

If you have never been to CES and are contemplating a visit, please be aware the sheer size and magnitude of the event can be a bit overwhelming for newcomers. However, the benefits far outweigh the costs, and any preconceived notions that the pace of technology is slowing will quickly be dispelled. Of course, I would never consider mixing business with pleasure while in Las Vegas (cough, cough), however if you do decide to attend, you will have an opportunity to partake in some of the local eating, gaming, shopping, and entertainment after you get burnt out on all the gadgets and technologies. Thanks again CES, and goodbye…for now!

*See also, CES Summary from last year: CLICK HERE*

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AMZN, INTC and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in Segway, Petcube, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rise of the Robots

We’re losing our jobs to robots, and they will destroy our economy. It makes for a great news soundbite, but has no factual basis in reality, if you look at the actual trajectory of automation and technology innovations throughout history. The global economy did not collapse when the steam engine replaced the oar; the automobile supplanted the horse; the computer became a substitute for the abacus; and the combine killed off the farmer. The same notion holds true today as robots become more ubiquitous in our daily commercial and personal lives.

From the early, post-revolutionary birth of our country in the 18th century, the agrarian economy accounted for upwards of 90% of jobs and financial activity…until farming technology evolved (see chart below). As new agricultural advancements were introduced, like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds, human capital (jobs) were redeployed into other growth sectors of the economy (e.g., factories, aerospace, semiconductors, medicine, etc.).

Source: Carpe Diem

Given that human labor accounts for about 2/3 of an average company’s expense structure, it should come as no surprise that corporations are looking to reduce costs by introducing more robotics and automation into their processes. The advantages to robotics adoption are numerous and I describe many of the reasons in my article, Chainsaw Replaces Paul Bunyan:

A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue for discrimination or sexual harassment.

At Sidoxia Capital Management we opportunistically identified this growing trend quite early as evidenced by our initial 2012 investment in KUKA AG (Ticker: KUKAF), a German manufacturer of industrial robots. KUKA has recently made headlines due to a bid received from Chinese home-appliance company (Midea Group: Ticker – 000333.SZ) that values the dominant German robotics leader at $5 billion. Despite KUKA’s +273% share price appreciation from the end of 2012, not many people have heard of the company. While KUKA may not have caught the attention of many U.S. investors, the company has captured a bevy of blue-chip global customers, including Daimler, Airbus Group, Volkswagen, Fiat, Boeing, and Tesla.

Rather than sitting on its hands, KUKA has done its part to develop a higher profile. In fact, President Barack Obama and German Chancellor Angela Merkel recently received a robotics demonstration from KUKA’s CEO Till Reuter at the world’s largest industrial technology trade fair in Hannover, Germany this April (picture below)

Source: Bloomberg

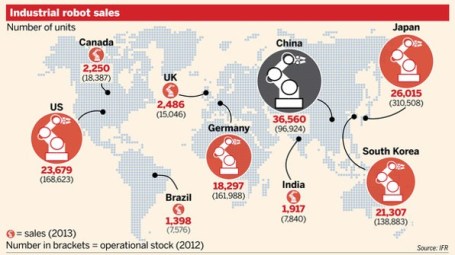

The recent multi-billion dollar bid by Midea Group has turned some onlookers’ heads, but what the potential deal really signals is the vast opportunity for robotics expansion in Asia. Rising labor costs in China, coupled with the enormous efficiency benefits of automation, have pushed China to become the largest purchasing country of robots in the world, ahead of the U.S., Japan, Korea and Germany (see chart below). However, according to the International Federation of Robotics (IFR), in 2015, Japan remained the country with the largest number of installed robots. IFR does not expect Japan to remain the “king” of the installed robotics hill forever. Actually, IFR estimates China will leapfrog Japan over the next few years to become both the largest purchaser of robots, along with maintaining the largest installed base of robots.

Source: Financial Times

In the coming months and years, there will be a steady stream of sensationalist headlines talking about the rise of the robots, and the destruction of jobs. We’ve repeatedly seen this movie before throughout history. Rather than a scary bloodbath ending, over the long-run we’ll likely see another happy ending. Any potential job losses will likely be outweighed by productivity gains, coupled with the benefits associated with more efficiently deployed labor to new growth sectors of the economy.

Even KUKA realizes the automation dynamics of the 21st century will serve as a net labor enhancer not detractor. If you don’t believe me, just ask Timo Boll, world champion table tennis player, who tested this theory vs. a KUKA robot (see video below). Ultimately, the rise of robots will lead to the rise of global growth and productivity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), KUKAF, BA, and TSLA, but at the time of publishing had no direct position in Daimler, Airbus Group, Volkswagen, Fiat Chrysler, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Why 0% Rates? Tech, Globalization & EM (Not QE)

Recently I have written about the head-scratching, never-ending, multi-decade decline in long-term interest rates (see chart below). Who should care? Well, just about anybody, if you bear in mind the structure of interests rates impacts the cost of borrowing on mortgages, credit cards, automobiles, corporate bonds, savings accounts, and practically every other financial instrument you can possibly think of. Simplistic conventional thinking explains the race to 0% global interest rates by the loose monetary Quantitative Easing (QE) policies of the Federal Reserve. But validating that line of thinking becomes more challenging once you consider QE ended months ago. What’s more, contrary to common belief, rates declined further rather than climb higher after QE’s completion.

Source: Calafia Beach Pundit

More specifically, if you look at rates during this same time last year, the yield on the 10-Year Treasury Note had more than doubled in the preceding 18 months to a level above 3.0%. The consensus view then was that the eventual wind-down of QE would only add gasoline to the fire, causing bond prices to decline and rates to extend an indefinite upwards march. Outside of bond guru Jeff Gundlach, and a small minority of prognosticators, the herd was largely wrong – as is usually the case. As we sit here today, the 10-Year Note currently yields a paltry 2.26%, which has led to the long-bond iShares 20-Year Treasury ETF (TLT) jumping +22% year-to-date (contrary to most expectations).

The American Ostrich

Like an ostrich sticking its head in the sand, us egocentric Americans tend to ignore details relating to others, especially if the analyzed data is occurring outside the borders of our own soil. Unbeknownst to many, here are some key country interest rates below U.S. yields:

- Switzerland: 0.33%

- Japan: 0.34%

- Germany: 0.60%

- Finland: 0.70%

- Austria: 0.75%

- France: 0.88%

- Denmark: 0.89%

- Sweden: 0.98%

- Ireland: 1.29%

- Spain: 1.69%

- Canada 1.80%

- U.K: 1.85%

- Italy: 1.93%

- U.S.: 2.26% (are our rates really that low?)

Outside of Japan, these listed countries are not implementing QE (i.e., “Quantitative Easing”) as did the United States. Rather than QE being the main driver behind the multi-decade secular decline in interest rates, there are other more important disinflationary forces at work driving interest rates lower.

Technology, Globalization, and Emerging Market Competition (T.G.E.M.)

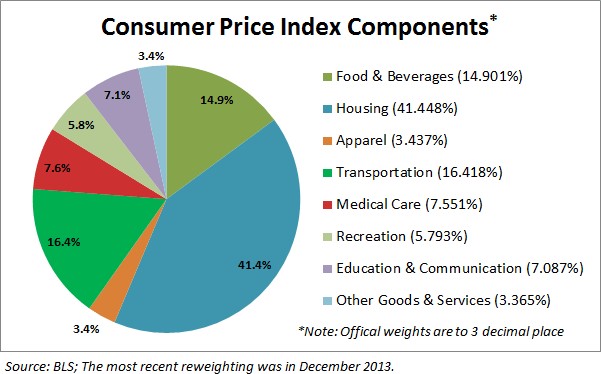

While tracking the endless monthly inflation statistics is a useful exercise to understand the tangible underlying pricing components of various industry segments (e.g., see 20 pages of CPI statistics), the larger and more important factors can be attributed to the somewhat more invisible elements of technology, globalization, and emerging market competition (T.G.E.M).

Starting with technology, to put these dynamics into perspective, consider the number of transistors, or the effective horsepower, on a semiconductor (a.k.a. computer “chip”) today. The overall impact on global standards of living is nothing short of astounding. Take an Intel chip for example – it had approximately 2,000 transistors in 1971. Today, semiconductors can cram over 10,000,000,000 (yes billions – 5 million times more) transistors onto a single semiconductor. Any individual can look no further than their smartphone to understand the profound implications this has not only on pricing in general, but society overall. To illustrate this point, I would direct you to a post highlighted by Professor Mark J. Perry, who observed the cost to duplicate an iPhone during 1991 would have been more than $3,500,000!

There are an infinite number of examples depicting how technology has accelerated the adoption of globalization. More recently, events such as the Arab Spring point out how Twitter (TWTR) displaced costly military engagement alternatives. The latest mega-Chinese IPO of Alibaba (BABA) was also emblematic of the hunger experienced in emerging markets to join the highly effective economic system of global capitalism.

I think New York Times journalist Tom Friedman said it best in his book, The World is Flat, when he made the following observations about the dynamics occurring in emerging markets:

“My mom told me to eat my dinner because there are starving children in China and India – I tell my kids to do their homework because Chinese and Indians are starving for their jobs”.

“France wants a 35 hour work week, India wants a 35 hour work day.”

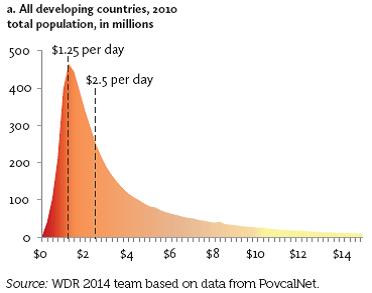

There may be a widening gap between rich and poor in the United States, but technology and globalization is narrowing the gap across the rest of the world. Consider nearly half of the world’s population (3 billion+ people) live in poverty, earning less than $2.50 a day (see chart below). Technology and globalization is allowing this emerging middle class climb the global economic ladder.

These impoverished individuals may not be imminently stealing our current jobs and driving general prices lower, but their children, and the countless educated millions in other international markets are striving for the same economic security and prosperity we have. The educated individuals in the emerging markets that have tasted capitalism are giving new meaning to the word “urgency”, which is only accelerating competition and global pricing pressures. It comes as no surprise to me that this generational migration from the poor to the middle class is putting a lid on inflation and interest rates around the world.

Declining costs of human labor from emerging markets however is not the only issue putting a ceiling on general prices. Robotics, an area in which Sidoxia holds significant investments, continues to be an area of fascination for me. With human labor accounting for the majority of business costs, it’s no wonder the C-suite is devoting more investment dollars towards automation. Rather than hire and train expensive workers, why not just buy a robot? This is not just happening in the U.S. – in fact the Chinese purchased more robots than Americans last year. And why not? An employer does not have to pay a robot overtime compensation; a robot never shows up late; robots never sue for discrimination or harassment; robots receive no healthcare or retirement benefits; and robots work 24 hours/day, 7 days/week, and 365 days/year.

While newspapers, bloggers, and talking heads like to point to the simplistic explanation of loose, irresponsible monetary policies of global central banks as the reason behind a four decade drop in interest rates that is only a small part of the story. Investors and policy makers alike should be paying closer attention to the factors of technology, globalization, and emerging market competition as the more impactful dynamics systematically driving down long term interest rates and inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including long positions in certain exchange traded fund positions and INTC (short position in TLT), but at the time of publishing SCM had no direct position in BABA, TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

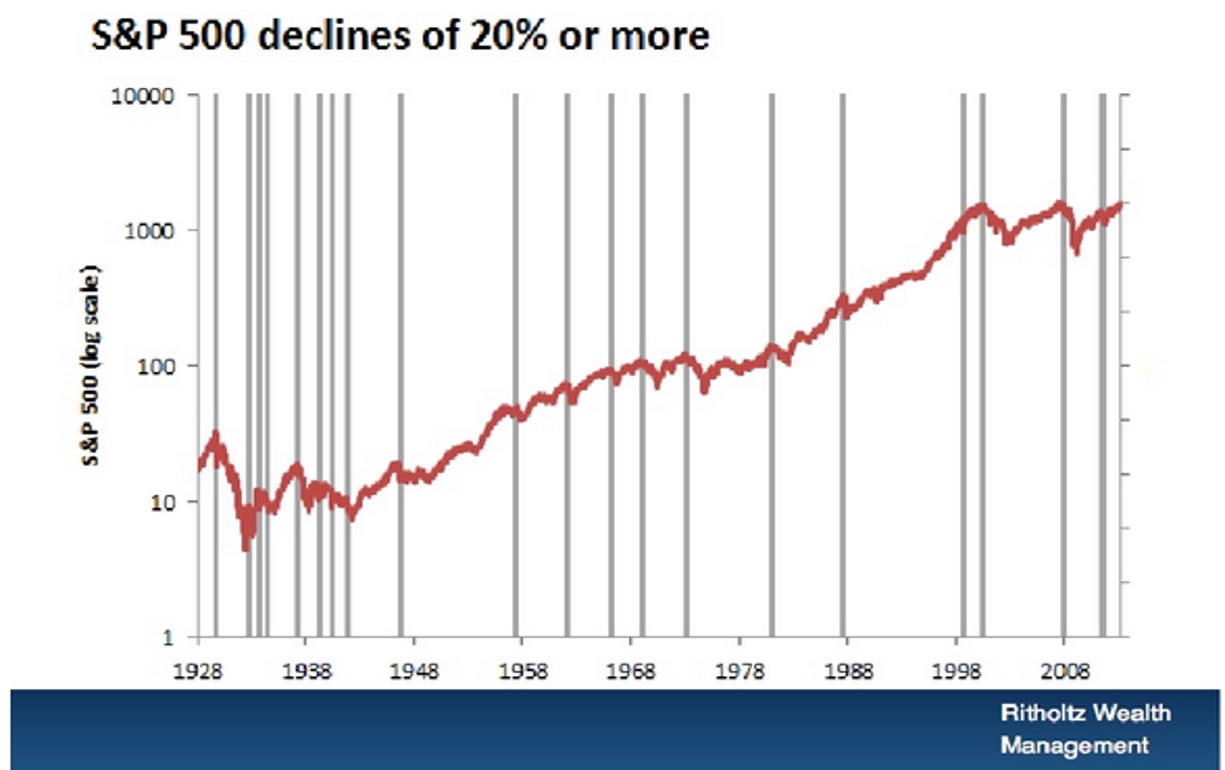

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}