Posts tagged ‘risk tolerance’

F.U.D. and Dividend Shock Absorbers

As the existential question remains open on whether Greece will remain a functioning entity within the eurozone, investor anxiety and manic behavior continues to be the norm. Rampant fear seems very counterintuitive for a stock market that has more than tripled in value from early 2009 with the S&P 500 index only sitting -3% below all-time record highs. Common sense would dictate that euphoric investor appetites have contributed to years of new record highs in the U.S. stock market, but that isn’t the case now. Rather, the enormous appreciation experienced in recent years can be better explained by the trillions of dollars directed towards buoyant share buybacks and mergers.

With a bull market still briskly running into its sixth year, where can we find the evidence for all this anxiety? Well, if you don’t believe all the nail biting concerns you hear from friends, family members, and co-workers about a Grexit (Greek exit from the euro), Chinese stock market bubble, Puerto Rico collapse, and/or impending Fed rate hike, then here are a few confirming data points.

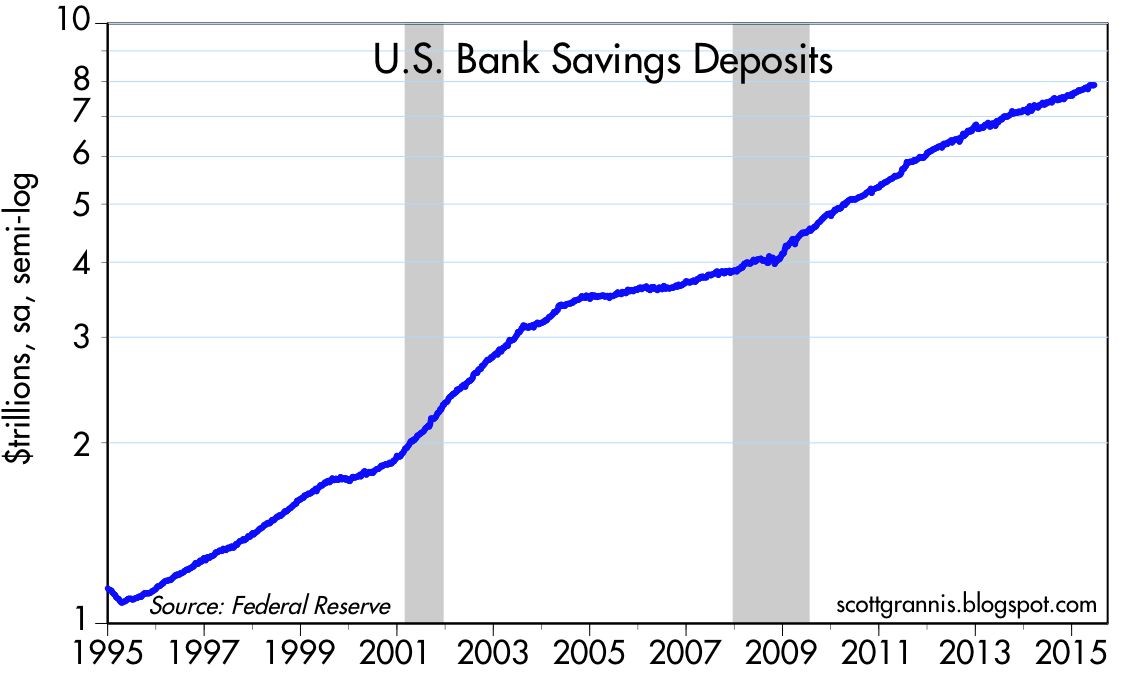

For starters, let’s take a look at the record $8 trillion of cash being stuffed under the mattress at near 0% rates in savings deposits (see chart below). The unbelievable 15% annual growth rate in cash hoarding since the turn of the century is even scarier once you consider the massive value destruction from the eroding impact of inflation and the colossal opportunity costs lost from gains and yields in alternative investments.

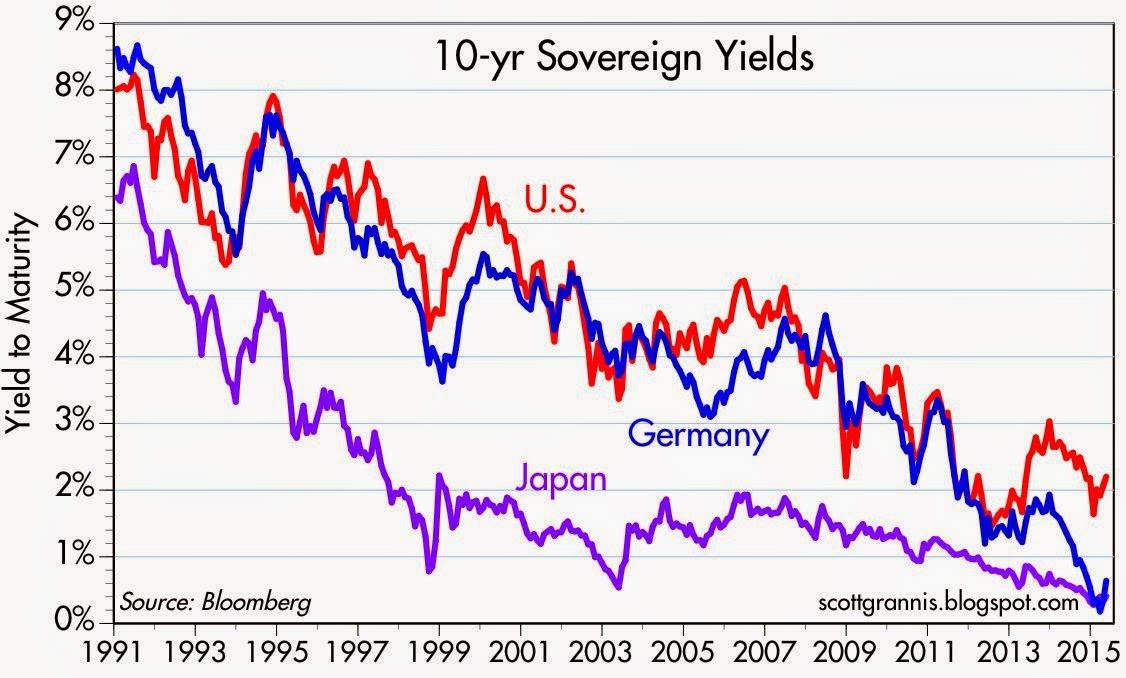

Next, you can witness the irrational risk averse behavior of investors piling into low (and negative) yielding bonds. Case in point are the 10-year yields in developing countries like Germany, Japan, and the U.S. (see chart below).

The 25-year downward trend in rates is a very scary development for yield-hungry investors. The picture doesn’t look much prettier once you realize the compensation for holding a 30-year bond (currently +3.2%) is only +0.8% more than holding the same Treasury bond for 10 years (now +2.4%). Yes, it is true that sluggish global growth and tame inflation is keeping a lid on interest rates, but these trends highlight once again that F.U.D. (fear, uncertainty, and doubt) has more to do with the perceived flight to safety and high bond prices (low bond yields).

In addition, the -$57 billion in outflows out of U.S. equity funds this year is further evidence that F.U.D. is out in full force. As I’ve noted on repeated occasions, when the tide turns on a sustained multi-year basis and investors dive head first into stocks, this will be proof that the bull market is long in the tooth and conservatism should be the default posture.

Dividend Shock Absorbers

There are always plenty of scary headlines that tempt investors to bail out of their investments. Today those alarming headlines span from Greece and China to Puerto Rico and the Federal Reserve. When the winds of fear, uncertainty, and doubt are fiercely swirling, it’s important to remember that any investment strategy should be constructed in a diversified manner that meshes with your time horizon and risk tolerance.

Consistent with maintaining a diversified portfolio, owning reliable dividend paying stocks is an important component of investment strategy, especially during volatile periods like we are experiencing currently. Sure, I still love to own high octane, non-dividend growth stocks in my personal and client portfolios, but owning stocks with a healthy stream of dividends serve as shock absorbers in bumpy markets with periodic surprise potholes.

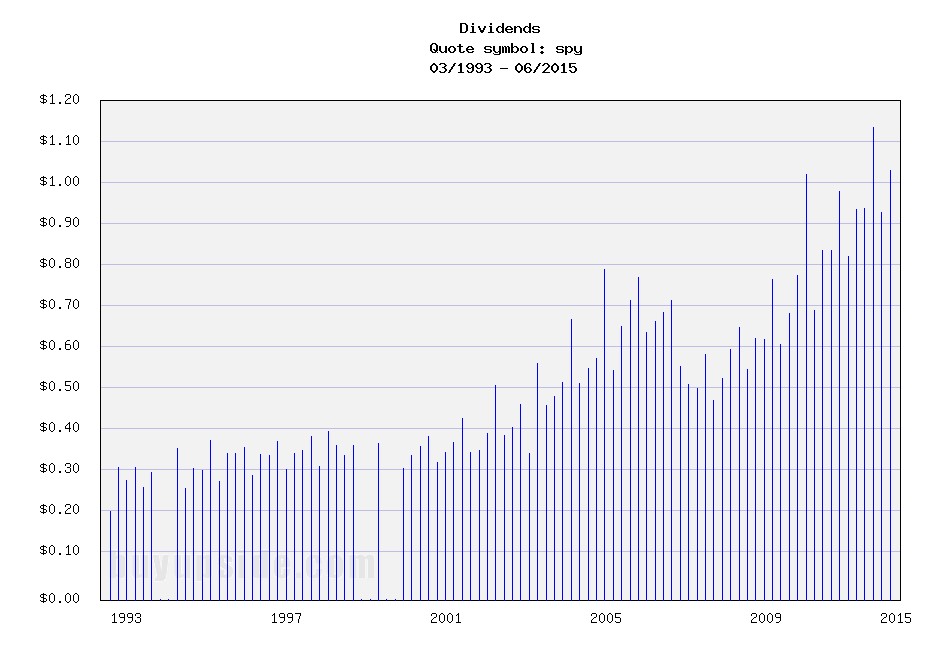

As I’ve note before, bond issuers don’t call up investors and raise periodic coupon payments out of the kindness of their hearts, but stock issuers can and do raise dividends (see chart below). Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500.

Source: BuyUpside.com

Markets will continue to move up and down on the news du jour, but dividends overall remain fairly steady. In the worst financial crisis in a generation, dividends dipped temporarily, but as I explain in a previous article (The Gift that Keeps on Giving), dividends have been on a fairly consistent 6% growth trajectory over the last two decades. With corporate dividend payout ratios well below long term historical averages of 50%, companies still have plenty of room to maintain (and grow) dividends – even if the economy and corporate profits slow.

Don’t succumb to all the F.U.D., and if you feel yourself beginning to fall into that trap, re-evaluate your portfolio to make sure your diversified portfolio has some shock absorbers in the form of dividend paying stocks. That way your portfolio can handle those unexpected financial potholes that repeatedly pop up.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Building Your All-Star NBA Portfolio

Image by © Royalty-Free/Corbis

You may or may not care, but the NBA (National Basketball Association) playoffs are in full swing. If you were an owner/manager of an NBA team, you probably wouldn’t pick me as a starting player on your roster – and if you did, we would need to sit down and talk. I played high school basketball (“played” is a loose term) in my youth, and even played in my early 40s against other over-aged veterans with knee braces, goggles, and headbands. Once my injuries began to pile up and my playing time was minimized by the spry, millennial team members, I knew it was time to retire and hang up my jockstrap.

The great thing about your investments is that you can create an All-Star NBA portfolio without the necessity of a salary market cap or billions of dollars like Mark Cuban. You can actually put the greatest professional players in the world (stocks/bonds) into your portfolio whether you invest $1,000 or $10,000,000. Sure, transactions costs can eat away at the smaller portfolios, but if investors are correctly managing their funds over years, and not months, then virtually everyone can create a cost-efficient elite team of stocks, bonds, and alternatives.

Now that we’ve established that anyone can create a championship caliber portfolio, the question then becomes, how does an owner go about selecting his/her team’s players? It may sound like a cliché, but diversification is paramount. Although centers Tim Duncan, Dwight Howard, Chris Bosh, Marc Gasol, and DeAndre Jordan may get a lot of rebounds for your team, it wouldn’t make sense to have those five starting centers on your team. The same principle applies to your investment portfolio.

Generally speaking, the best policy for investors is to establish exposure to a broad set of asset classes customized to your time horizon, risk tolerance, objectives, and constraints. In other words, it is prudent to have exposure to not only stocks and bonds, but other areas like real estate, commodities, alternatives, and emerging markets. Everybody has their own unique situation, and with interest rates and valuations continually changing, it makes sense that asset allocations across all individuals will be very diverse.

In basketball terms, the sizes and types of guards, forwards, and centers will be dependent on the objectives of the team’s owners/managers. For example, it is very logical to have Stephen Curry (see great video) as the starting guard for the fast-paced, highest scoring NBA team, Golden State Warriors but Curry would not be ideally suited for the slow, grind-em-up offense of the Utah Jazz (one of the lowest scoring teams in the NBA).

In order to build a consistent winning percentage for your portfolio, you need to have a systematic, disciplined process of choosing your all-star-team, which can’t just consist of picking the hottest player of the day. Not only could it be too expensive, the consequences of over-concentrating your portfolio with an expensive position can be painful….just ask Los Angeles Laker fans how they feel about overpaying for Kobe Bryant’s $23.5 million 2014-2015 salary. Investors who chased the overpriced tech sector in the late 1990s, with stock prices trading at over 100 times trailing 12-month earnings, understand how painful losses can be in the subsequent “bubble” burst.

Having a strong bench of players is crucial as well. This requires a research process that can prioritize opportunities based on quantitative and fundamental processes (at Sidoxia we use our SHGR model). Sometimes your starters get injured, fatigued, or bought out by a competitor. Interest rates, valuations, exchange rates, earnings growth rates and other economic factors are continually fluctuating, so having a bench of suitable investment ideas is critical for different financial environments.

Beating the market is a challenging endeavor, not only for individuals, but also for professionals. If you don’t believe me, then check out what Dalbar had to say about this subject in its annual report entitled, Quantitative Analysis of Investor Behavior:

Dalbar found that in 2014, the average investor in a stock mutual fund underperformed the S&P 500 by a margin of 8.19 percent. Fixed-income investors underperformed the Barclays Aggregate Bond Index by a margin of 4.81 percent.

Ouch! If you want to generate winning returns matching the likes of the 1,000-win club, which includes Gregg Popovich, Phil Jackson, and Pat Riley then you need to avoid some of the most common investor mistakes (see also 10 Ways to Destroy Your Portfolio). Chasing performance, ignoring diversification, emotionally reacting to news headlines, paying high fees, and over-trading are sure fire ways to get technical fouls and ejected from the investment game. Avoiding these mistakes and following a systematic, objective process will make you and your investment portfolio a successful all-star.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Why Buy at Record Highs? Ask the Fat Turkey

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (December 1, 2014). Subscribe on the right side of the page for the complete text.

I’ve fulfilled my American Thanksgiving duty by gorging myself on multiple helpings of turkey, mash potatoes, and pumpkin pie. Now that I have loosened my belt a few notches, I have had time to reflect on the generous servings of stock returns this year (S&P 500 index up +11.9%), on top of the whopping +104.6% gains from previous 5 years (2009-2013).

Conventional wisdom believes the Federal Reserve has artificially inflated the stock market. Given the perceived sky-high record stock prices, many investors are biting their nails in anticipation of an impending crash. The evidence behind the nagging investor skepticism can be found in the near-record low stock ownership statistics; dismal domestic equity fund purchases; and apathetic investor survey data (see Market Champagne Sits on Ice).

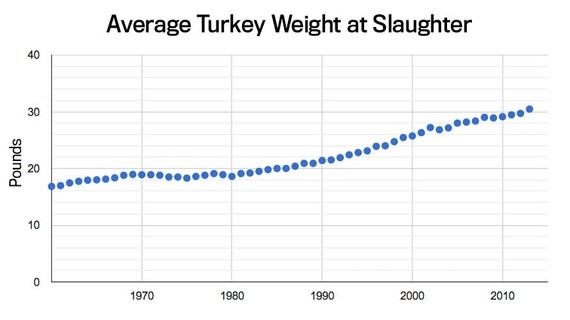

Turkey-lovers are in a great position to understand the predicted stock crash expected by many of the naysayers. As you can see from the chart below, the size of turkeys over the last 50+ years has reached a record weight – and therefore record prices per turkey:

Source: The Atlantic

Does a record size in turkeys mean turkey meat prices are doomed for an imminent price collapse? Absolutely not. A key reason turkey prices have hit record levels is because Thanksgiving stomachs have been buying fatter and fatter turkeys every year. The same phenomenon is happening in the stock market. The reason stock prices have continued to move higher and higher is because profits have grown fatter and fatter every year (see chart below). Profits in corporate America have never been higher. CEOs are sitting on trillions of dollars of cash, and providing stock-investors with growing plump dividends (see also The Gift that Keeps on Giving), $100s of billions in shareholder friendly stock buybacks, while increasingly taking leftover profits to invest in growth initiatives (e.g., technology investments, international expansion, and job hiring).

Source: Calafia Beach Pundit

Despite record turkey prices, I will make the bold prediction that hungry Americans will continue to buy turkey. More important than the overall price paid per turkey, the statistic that consumers should be paying more attention to is the turkey price paid per pound. Based on that more relevant metric, the data on turkey prices is less conclusive. In fact, turkey prices are estimated to be -13% cheaper this year on a per pound basis compared to last year ($1.58/lb vs. $1.82/lb).

The equivalent price per pound metric in the stock market is called the Price-Earnings (P/E) ratio, which is the price paid by a stock investor per $1 of profits (or earnings). Today that P/E ratio sits at approximately 17.5x. As you can see from the chart below, the current P/E ratio is reasonably near historical averages experienced over the last 50+ years. While, all else equal, anyone would prefer paying a lower price per pound (or price per $1 in earnings), any objective person looking at the current P/E ratio would have difficulty concluding recent stock prices are in “bubble” territory.

However, investor doubters who have missed the record bull run in stock market prices over the last five years (+210% since early 2009) have clung to a distorted, overpriced measurement called the CAPE or Shiller P/E ratio. Readers of my Investing Caffeine blog or newsletters know why this metric is misleading and inaccurate (see also Shiller CAPE Peaches Smell).

Don’t Be an Ostrich

While prices of stocks arguably remain reasonably priced for many Baby Boomers and retirees, the conclusion should not be to gorge 100% of investment portfolios into stocks. Quite the contrary. Everyone’s situation is unique, and every investor should customize a globally diversified portfolio beyond just stocks, including areas like fixed income, real estate, alternative investments, and commodities. But the exposures don’t stop there, because in order to truly have the diversified shock absorbers in your portfolio necessary for a bumpy long-term ride, investors need exposure to other areas. Such areas should include international and emerging market geographies; a diverse set of styles (e.g., Value, Growth, Blue Chip dividend-payers); and a healthy ownership across small, medium, and large equities. The same principles apply to your bond portfolio. Steps need to be taken to control credit risk and interest rate risk in a globally diversified fashion, while also providing adequate income (yield) in an environment of generationally low interest rates.

While I’ve spent a decent amount of time talking about eating fat turkeys, don’t let your investment portfolio become stuffed. The year-end time period is always a good time, after recovering from a food coma, to proactively review your investments. While most non-vegetarians love eating turkey, don’t be an investment ostrich with your head in the sand – now is the time to take actions into your own hands and make sure your investments are properly allocated.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Winning via Halftime Adjustments

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (July 1, 2014). Subscribe on the right side of the page for the complete text.

In the game of sports and investing there are a lot of unanticipated dynamics that occur during the course of a game, season, or year. With the second quarter of 2014 now coming to a close, we have reached the half-way point of the year. Along the way, the coach (and investors) may need to make some strategic halftime adjustments. Reassessing or reflecting on the positioning of your investment portfolio once or twice per year in the context of your investment objectives, time horizon, and risk tolerance level is never a bad idea – especially when there are unforeseen events continually materializing during the game.

During the first half of the year, the financial markets have experienced numerous surprises:

- Declining Interest Rates: Under the auspices of a massive 2013 gain in stock prices, expectations were for an accelerating economy and rising interest rates in 2014. Instead, the 10-Year Treasury Note has seen its yield counterintuitively plunge from 3.03% to 2.52%.

- Geopolitical Tensions (Ukraine/Syria/Iraq): The stock market has ground higher this year in spite of geopolitical tensions in Ukraine, Syria, and now Iraq. These skirmishes make for great TV, radio, and blog content, but the reality is these conflicts will likely be forgotten/ignored in favor of other fresher clashes in the coming months and quarters.

- Unabated Tapering: It’s true the Federal Reserve signaled the reduction in its bond buying stimulus program last year, however the more surprising aspect has been the pace of the taper. From the beginning of the year, the $85 billion program has already been reduced to $35 billion and will likely be reduced to $0 by the fall.

- Polar Vortex/GDP: Weather is very unpredictable, and regardless of your views on global warming, the unseasonably cold weather on the eastern half of the country had a severely negative impact on first half GDP (Gross Domestic Product). In fact, first quarter GDP was revised lower to a contraction of -2.9%. The good news is expectations are for an improved second half of the year according to Merrill Lynch.

While it would be wonderful to live in Utopia, unfortunately for investors, there is always uncertainty and risk. These elements come with the investing territory. Of course, you can always compensate for that unwanted uncertainty by accepting low interest-paying options (e.g., stuffing your money under a mattress, in a CD, savings account, Treasury bonds, etc.).

Despite the unexpected first half events, the market continues to grind higher. During the first half of the year, the S&P 500 index rose 6.1% (+1.9% in June); the Dow Jones Industrials edged higher by +1.5% (+0.7% in June); and the Nasdaq climbed +5.5% (+3.9% in June). But stocks weren’t the only winning investment team in town – bonds tasted victory during the first half also, notching gains of +2.8% (AGG – Aggregate Bond), almost double the Dow’s performance.

Investor Psyche Pendulum Swinging in Positive Direction

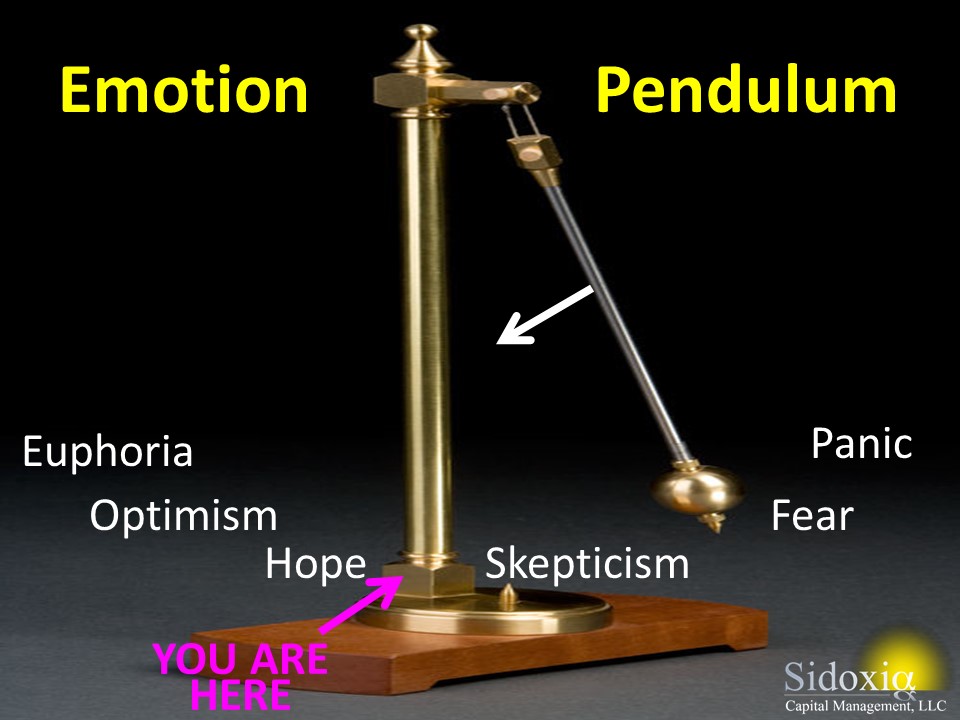

As I have written in the past, investor psyches continually swing along an emotional pendulum (see also Sentiment Pendulum article) from a state of “Panic” to “Euphoria”. While the pendulum has clearly swung in a positive direction, away from the emotional states of “Panic & Fear,” we appear to now be between “Skepticism & Hope.” The timing of when we get to the latter stages of “Optimism & Euphoria” is dependent on the pace of the economic recovery, risk appetites of consumers/businesses, and the trajectory of risky assets like stocks. Just because the ride has been fun for the last five years, does not mean the ride is over. However, as the pendulum continues to swing to the left, long-term investors need to fight the tempting urge to increase risk appetite just as the allure of high stock returns appears more achievable.

During the second half of this economic cycle, before the next recession, investors need to be more cognizant of controlling risk (the probability of permanent losses) by paying closer attention to valuations, diversification, and rebalancing too heavily weighted equity portfolios.

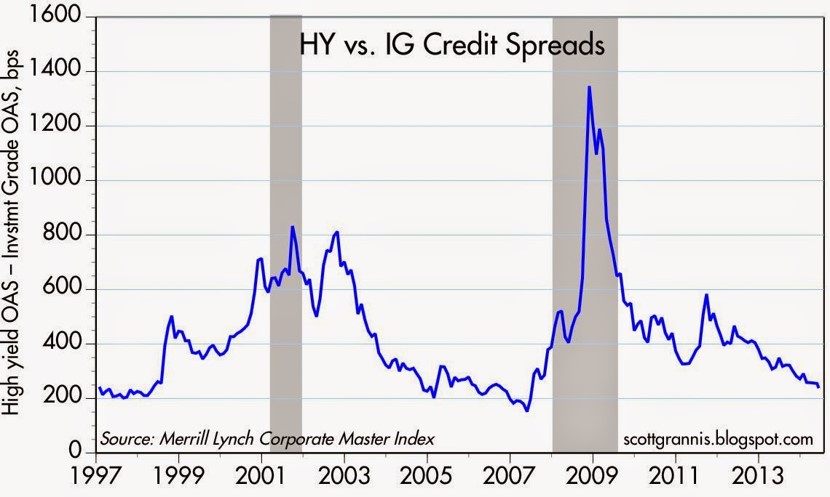

Besides rising stock prices and the beginning of positive fund flows, investors’ increasing appetite for risk is evidenced by the yield chasing occurring in junk bonds, which has raised prices of the lowest quality bonds to lofty levels. The chart below shows this phenomenon happening with the yields narrowing between high yield (HY) bonds and investment grade (IG) corporate bonds.

Source: Calafia Beach Pundit

Even though I pointed out a number of disconcerting surprises in the first half of the year, as you consider making halftime adjustments to your portfolios, do not forget some of the underlying positive currents that are leading to a winning halftime score.

Here are some of the constructive factors supporting stock prices, which have nearly tripled in value from the 2009 lows (S&P 500 – 666 to 1,960):

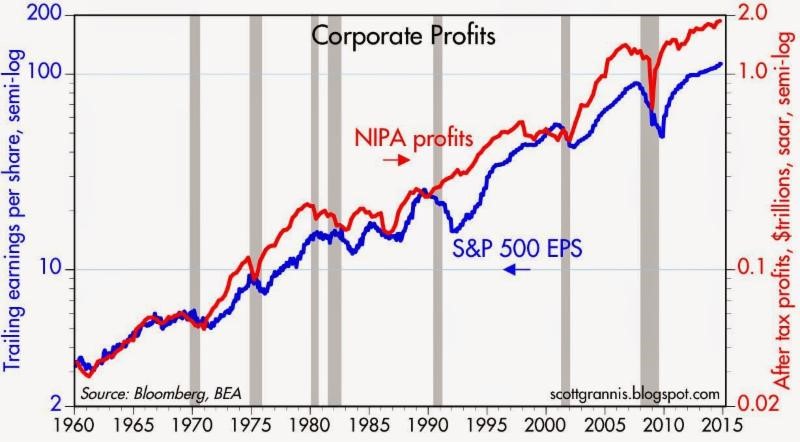

Record Corporate Profits: I constantly bump into skeptics who fail to realize the fundamental power of record profits driving stock prices higher (see chart below). As the late John Templeton stated, “In the long run, the stock market indexes fluctuate around the long-term upward trend of earnings per share.”

Source: Dr. Ed’s Blog

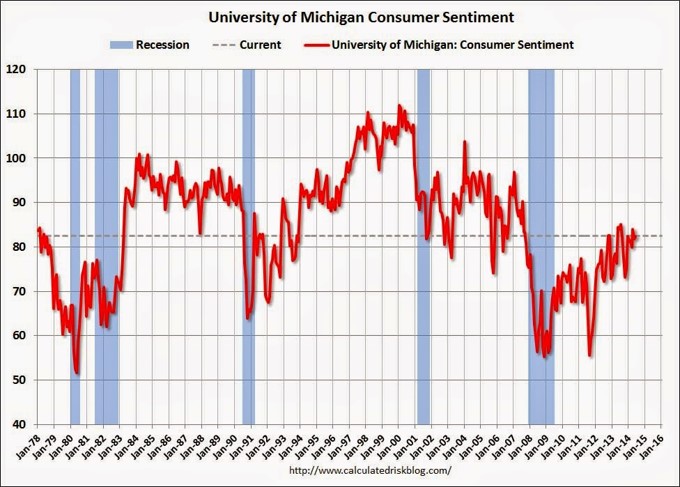

Improving Consumer Confidence: The University of Michigan consumer sentiment index increased to 82.5 for June from May. The confidence score came in above the consensus forecast of 82.0. Confidence has increased significantly from the 2009 lows but as the chart below shows, there is plenty of room for this metric to advance – consistent with the emotion pendulum discussed previously.

Source: Calculated Risk

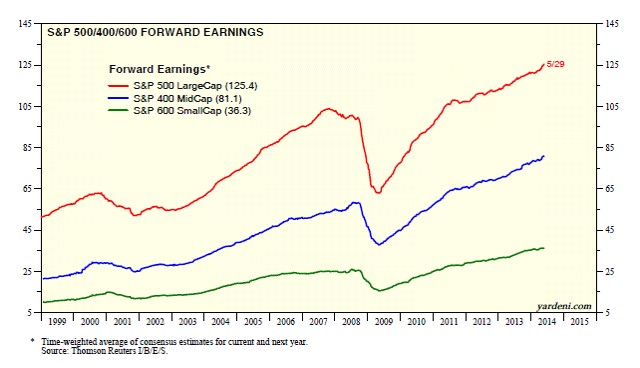

Dividends & Share Buybacks Near Record Levels: A bird in the hand is worth two in the bush. Corporations have realized this investor desire and as a result companies are returning record levels of money (“capital”) to stock shareholders via increasing dividends and share buybacks (see chart below).

Source: Dr. Ed’s Blog

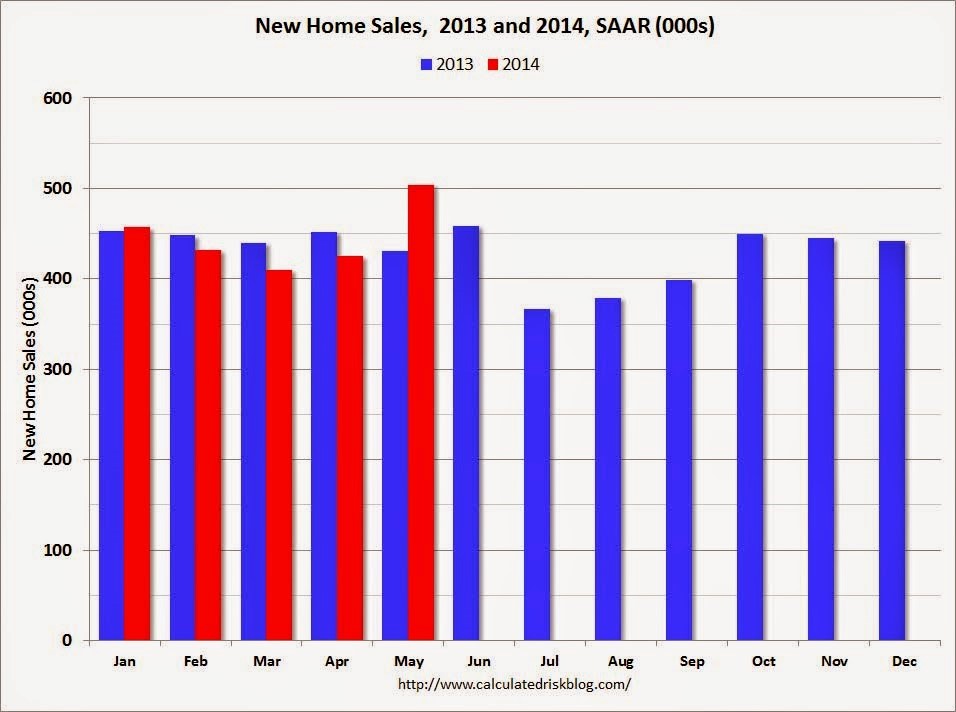

Housing on the Mend: The housing market has improved in fits and starts, but the most recent data point of new home sales shows significant improvement. More specifically, May’s new home sales were up +18.6% from the previous month (see chart below), the highest level seen since 2008. Although this data is encouraging, there is still plenty of room for improvement, as current sales remain more than 50% below 2005 peak levels.

Source: Calculated Risk

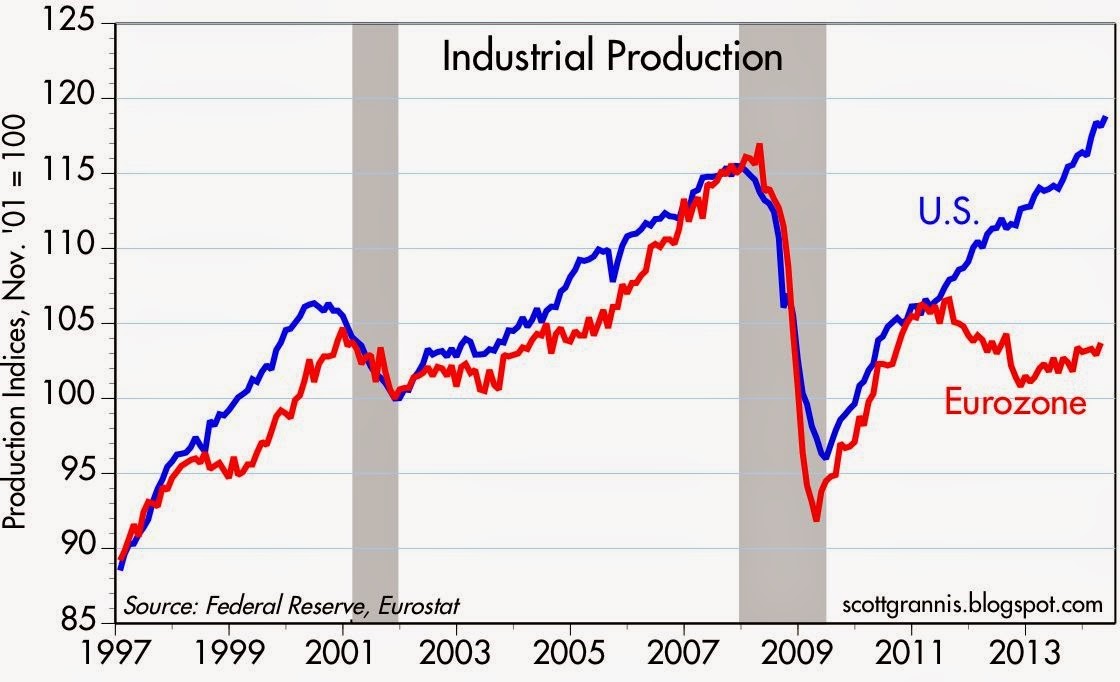

Record Industrial Production: Adding support to the improving economic outlook are the industrial production figures, which also hit a record (see chart below). This data also adds credence to why the U.S. stock market has outperformed the European markets during the economic recovery from 2009.

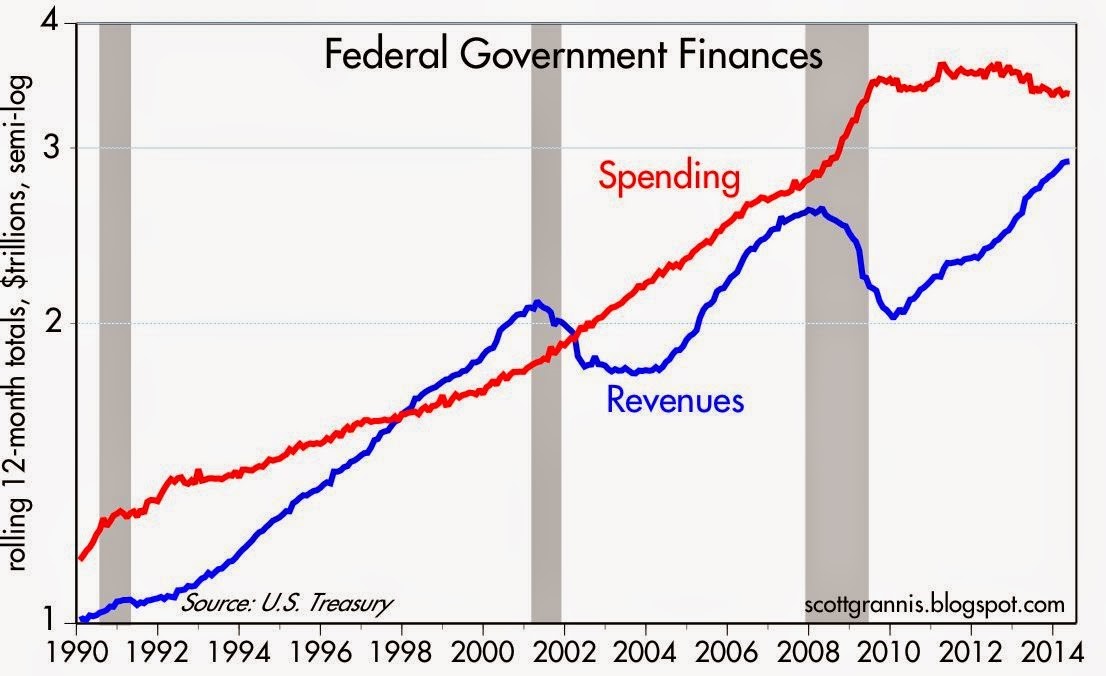

Source: Calafia Beach Pundit

Declining Federal Deficit: The federal deficit continues to narrow (i.e., tax revenues growing faster than government spending), so previous fiscally panicked screams have quieted down. We’re not out of the woods yet, but the trends are encouraging (see chart below):

Source: Calafia Beach Pundit

There have been plenty of bombshells during the first half of 2014 (no pun intended), and there are bound to be plenty more during the second half of the year. By definition, nobody can be fully prepared for a surprise, or else it wouldn’t be called a “surprise”. For those skeptical investors sitting on the sidelines, the record breaking stock market performance has also been astonishing. Regardless of what happens over the next six months, periodically making adjustments to your financial plan is important, whether it’s during the pre-game, post-game, or halftime. And if you’re not interested or capable of making those adjustments yourself, find a professional advisor/coach to assist you.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and AGG, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Searching for the Market Boogeyman

With the stock market reaching all-time record highs (S&P 500: 1900), you would think there would be a lot of cheers, high-fiving, and back slapping. Instead, investors are ignoring the sunny, blue skies and taking off their rose-colored glasses. Rather than securely sleeping like a baby (or relaxing during a three-day weekend) with their investment accounts, people are biting their fingernails with clenched teeth, while searching for a market boogeyman in their closets or under their beds.

If you don’t believe me, all you have to do is pick up the paper, turn on the TV, or walk over to the office water cooler. An avalanche of scary headlines that are spooking investors include geopolitical concerns in Ukraine & Thailand, slowing housing statistics, bearish hedge fund managers (i.e., Tepper Einhorn, Cooperman), declining interest rates, and collapsing internet stocks. In other words, investors are looking for things to worry about, despite record corporate profits and stock prices. Peter Lynch, the manager of the Magellan Fund that posted +2,700% in gains from 1977-1990, put short-term stock price volatility into perspective:

“You shouldn’t worry about it. You should worry what are stocks going to be 10 years from now, 20 years from now, 30 years from now.”

Rather than focusing on immediate stock market volatility and other factors out of your control, why not prioritize your time on things you can control. What investors can control is their asset allocation and spending levels (budget), subject to their personal time horizons and risk tolerances. Circumstances always change, but if people spent half the time on investing that they devoted to planning holiday vacations, purchasing a car, or choosing a school for their child, then retirement would be a lot less stressful. After realizing 99% of all the short-term news is nonsensical noise, the next important realization is stocks are volatile securities, which frequently go down -10 to -20%. As much as amateurs and professionals say or think they can profitably predict these corrections, they very rarely can. If your stomach can’t handle the roller-coaster swings, then you shouldn’t be investing in the stock market.

Bear-markets generally coincide with recessions, and since World War II, Americans experience about two economic contractions every decade. And as I pointed out earlier in A Series of Unfortunate Events, even during the current massive bull market, a recession has not been required to suffer significant short-term losses (e.g., Flash Crash, Greece, Arab Spring, Obamacare, Cyprus, etc.). Seasoned veterans understand these volatile periods provide incredible investment opportunities. As Warren Buffett states, “Be fearful when others are greedy, and be greedy when others are fearful.” Fear and panic may be behind us, but skepticism is still firmly in place. Buying during current skepticism is still not a bad thing, as long as greed hasn’t permeated the masses, which remains the case today.

Overly emotional people that make investment decisions with their gut do more damage to their savings accounts than conservative, emotional investors who understand their emotional shortcomings. On the other hand, the problem with investing too conservatively, for those that have longer-term time horizons (10+ years), is multi-pronged. For starters, overly conservative investments made while interest rate levels hover near historical lows lead to inflationary pressures gobbling up savings accounts. Secondly, the low total returns associated with excessively conservative investments will result in a later retirement (e.g., part-time Wal-Mart greeter in your 80s), or lower quality standard of living (e.g., macaroni & cheese dinners vs. filet mignon).

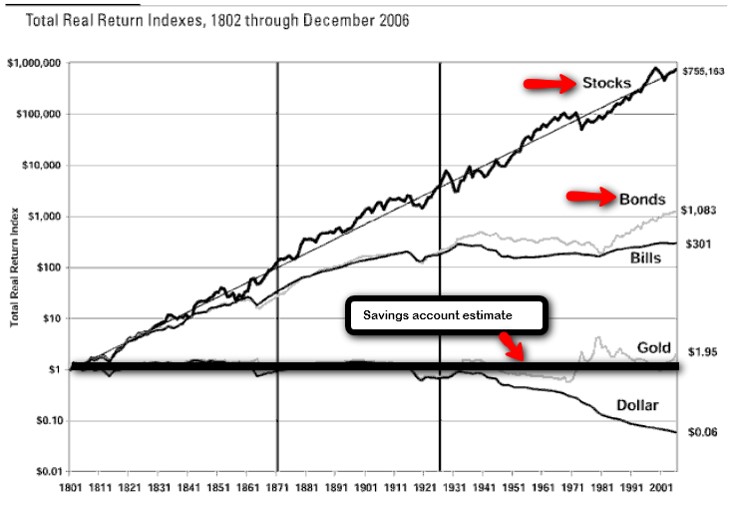

Most people say they understand the trade-offs of risk and return. Over the long-run, low-risk investments result in lower returns than high risk investments (i.e., bonds vs. stocks). If you look at the following chart and ask anyone what their preferred path would be over the long-run, almost everyone would select the steep, upward-sloping equity return line.

Source: Betterment.com / Stocks for the Long Run

Yet, stock ownership and attitudes towards stocks remain at relatively low and skeptical levels (see Gallup survey in Markets Soar and Investors Snore). It’s true that attitudes are changing at a glacial pace and bond outflows accelerated in 2013, but more recently stock inflows remain sporadic and scared money is returning to bonds. Even though it has been over five years, the emotional scars from 2008-2009 apparently still need some time to heal.

Investing in stocks can be very scary and hazardous to your health. For those millions of investors who realize they do not hold the emotional fortitude to withstand the ups and downs, leave the worrying responsibilities to the experienced advisors and investment managers like me. That way you can focus on your job and retirement, while the pros can remain responsible for hunting and slaying the boogeyman.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dealing with Wobbling Risk Tolerances

The words “risk tolerance” are often used loosely, but unfortunately many investors and advisors look at these terms as an objectively definable statistic, like your blood pressure or cholesterol level. Not only is risk tolerance not a definable statistic, but for most people it is also constantly changing.

Given that investment advisors themselves have a great deal of difficulty maintaining an even emotional keel, it should come as no surprise that most invidual investors have even more volatile risk appetites. Because of the nature surrounding the markets – 24/7 news coverage and non-stop tick by tick price scorekeeping –emotions continually tug at investors’ risk tolerances.

Average Investor NOT on Best Behavior

Certainly in my practice, I’ve seen the direct psychological (and physical) impacts volatile financial markets can have on people’s investment decisions. What makes deciphering risk tolerance even more difficult is the absence of any substantive profile definitions (except for vague categories like conservative, moderate, and aggressive). The foggy risk categorizations are compounded by the aforementioned fluctuating risk tolerances, which usually switch in the wrong direction, at the wrong time. Case in point: the technology bubble bursting. In the late 1990s, risk aversion completely disappeared – everyone and their mother wanted to invest in technology stocks. If you fast-forward to the mid-2000s, you will also recall Bessie the hair salonist and Jimmy the cab-driver taking excessive risk at the peak of the housing bubble.

In a recent Simoleon Sense post, an astute guest contributor (Tim Richards) points to research developed by Carrie Pan and Meir Statman (Santa Clara University – Department of Finance) showing the shortcomings implicit in investor behavior:

“… investors’ risk tolerance varies by circumstances and associated emotions. High past stock returns endow stocks with positive affect and inflate investors’ exuberance, misleading them into the belief that the future holds high stock returns coupled with low risk. Risk tolerance questions asked after periods of high stock returns are likely to elicit answers exaggerating investors’ risk tolerance. Conversely, low past stock returns burden stocks with negative affect and inflate investors’ fear, misleading them into the belief that the future holds low stock returns coupled with high risk. Risk tolerance questions asked following periods of low stock returns are likely to elicit answers underestimating investors’ risk tolerance.”

In addition to ill-advised investor timing, Richards correctly highlights the lack of comparability across various investor types, even if you apply acceptable definitions or numeric levels of risk. Simple allocation to various stock/bond exposure does not adequately capture a client’s risk tolerance. A portfolio with 60% invested in Blue Chip dividend paying companies is a tad different than a portfolio invested 60% in Russian stocks. What an 82-year old retiree in Florida thinks is “aggressive” may differ 180 degrees from what a 32-year old trader on Wall Street may think is “aggressive.”

The Failure of Risk Equations

Academics have attempted to boil the market into elegant mathematical equations, but with the acknowledgement that investing mixes science with behavior, it becomes apparent that the mathematical equations must also incorporate art. However, it can become quite difficult to create an ever changing artistic equation. A perfect example of an equation gone awry is the debacle that unfolded at Long Term Capital Management. Robert Merton and Myron Scholes were world renowned Nobel Prize winners who single handedly brought the global financial markets to its knees in 1998 when it lost $500 million in one day and required a $3.6 billion bailout from a consortium of banks (see also why investors get hurt and Butter in Bangladesh articles).

Even if you are a smart economist who can artistically mix quantitative numbers with investing, the problem becomes people’s preferences and decisions change as the infinite number of variables adjust in the marketplace over time. There certainly are some rules of thumb investors tend to gravitate towards (such as cheap companies with sustainable growth in profits and cash flows), but even for those companies successful at generating income, nobody can unequivocally predict exactly how and when investors will react by pushing prices higher.

Here is what Tim Richardshad to add on the subjects of mathematical models and market efficiency in his Simoleon Sense post:

“So, in recent decades the industry’s approach has been to develop mathematical models which can relegate human behaviour to a set of probability equations, thus allowing profitability and risk to be actuarially managed: fraud is no longer unacceptable – it’s now just a number to be factored into earnings forecasts. This is simply the latest in a long line of industry fads, using the ideas of efficient market theories to design approaches which are right quite a lot of the time and then very, very wrong all at once.”

——————————————————————————————————

“[Markets] are not remotely efficient and it’s just a shame the world had to be brought to the edge of financial meltdown before anyone started listening.”

——————————————————————————————————

“When everyone thinks that markets can’t fail is the time to be very risk adverse, when no-one wants to invest is the time to be greedy. Yet what’s an advisor to do when the know-your-customer questionnaire tells them to do exactly the opposite of what’s in the customer’s best interests?”

Equations can produce detrimental results, so a healthy dosage of skepticism is prescribed.

The Solution: Education, Liquidity, and Income Can Allow More Beauty Sleep

Education about logic pitfalls and the integration of liquidity-based needs into clients’ investment plans is key. Controlling and understanding one’s personal biases can reduce or eliminate common repeated investment mistakes. Covering the investors’ income needs is another essential and practical aspect to investing, especially when it can prevent forced position sales at inopportune times. Extending oneself along the riskier end of the spectrum may have felt comfortable in the mid 2000s, but losses and sleepless nights overwhelmed many investors in 2008 and early 2009. In a bull market, adding too much equity and other risky assets to a portfolio is like pimping heroine to a drug addict – it behooves the advisor to point out the potential dangers of positioning a portfolio too aggressively. Rebalancing your investment portfolio can also act as a natural hedge to prevent exposures from exploding in size or evapaporating away. On the other hand, pitching Armageddon and piling into overpriced risk-free assets during the tail end of a bear market can be just as negligent.

Risk tolerance is an amorphous concept that can lead to suboptimal, knee-jerk investment actions. If you want to earn higher returns, I strongly urge you to pick up a behavioral finance book to sharpen your investment decision-making skills and firm up your wobbling risk tolerance foundation.

Read the whole Simoleon Sense article.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing had no direct positions in any security mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}