Posts tagged ‘Retirement’

Rise of the Robo-Advisors: Paying to Do-It-Yourself

Robots and computers are taking over our lives. We see it in areas of our daily living, including the use of digitally driven cars, cell phones, automated vacuums, and electronic self-serve kiosks at the grocery store. And now robots have come into our investing and financial lives in the form of robo-advisors. With a few clicks of a computer mouse or taps on a smartphone, investors are hoping to find their way to financial nirvana.

What sites am I talking about? Here is a brief, albeit rapidly growing, list of popular robo-advisor sites:

Not all of these robo-sites invest individuals’ money, but nevertheless, there are several factors contributing to the upsurge in in these financial advice websites. For starters, there is a whole new, younger demographic pool of savers who have grown up with their iPhone and shop exclusively online for their goods and services. Many of these financial sites are trying to fill a void for this tech-savvy group looking for a new app to bring wealth and riches.

Another factor contributing to the rise of the robo-advisors is a function of the 2008-2009 financial crisis and the explosive growth of the multi-trillion dollar exchange traded fund (ETF) industry. Many baby boomers who were planning to retire were hit brutally hard by the financial crisis and subsequently asked themselves why they were paying such high fees to their advisors for losing money. With the stock market now increasing for five consecutive years, some investors are gaining confidence in pursuing other lower-cost solutions to their investments outside of the traditional human advisor channel.

Too Good to Be True? The Shortcomings

On the surface, the proposition of clicking a few buttons to create financial prosperity seems quite appealing, but if you look a little more closely under the hood, what you quickly realize is that most of these robo-advisor sites are glorifying the practice of doing-it-yourself (DIY). After conducting some due diligence on the various investment bells-and-whistles of these robo-sites, one quickly realizes individuals can replicate most of the kindergartener-esque ETF portfolios by merely calling 1-800-VANGUARD – without having to pay robo-advisor fees ranging from 0.15% – 0.95%. More specifically, Wealthfront and Betterment use 6-12 ETF security portfolios, integrating many Vanguard funds and other ETFs that can be purchased with a click of a mouse or phone call (without having to pay the robo-advisor middleman). A cynic may also point out these robo-investment sites are nothing more than expensive life-cycle funds that could be replicated at a fraction of the cost.

Despite the sites’ transparency preaching, filtering through robo fee and performance disclosure can be frustratingly tedious too – good luck to the novices. For example, Betterment claims to have created a superior performance track record, despite a hidden disclosure stating the results are manufactured from a computer back-test. The transparency pitch seems a little disingenuous, and I wonder how many of the new robo-site users are also aware of the extra underlying ETF fees? But when marketing a new high-cost start-up, I guess you need to fabricate a fancy chart and track record when you don’t have one. Underlying the robo investment sites is a disparate, hodge-podge of studies anointing Modern Portfolio Theory as the holy grail, but readers of this blog know there are many failings to pure quantitative strategies implemented by academics (see LTCM in Black Swans & Butter in Bangladesh).

The concept of DIY is nothing new. One can look no further than the impact Home Depot (HD) has had on the home improvement industry. In addition, there are plenty of individuals who choose to do their own income taxes with the help of software technology (i.e., Intuit), or those who forego hiring an estate planning attorney by using off-the-shelf legal documents (i.e., Legal Zoom). Many industries in our economy inherently have penny pinching DIY-ers, but despite current and future inroads made by the robo-advisors, there will always be individuals who do not have the capacity, patience, or interest to search out a DIY investment solution.

After watching the stock market rise for five consecutive years, taming investment portfolios may seem like a simple problem for internet software to solve, but experienced investors (not academics) understand successful long-term investing is never easy…with or without technology. The reality of the situation is that when volatility eventually spikes and we hit an inevitable bear market, these robo-sites will fail miserably in supplying the necessary human element to facilitate more prudent investment decisions.

While the rising robo-advisors may have many investment advisory shortcomings, I will acknowledge some appealing aggregating features that provide a helpful holistic view of an individual’s finances (see Mint). Also, these sites are forcing investors to ask their advisors the important and appropriate tough questions regarding fees, compensation, and conflicts of interest. However, in spite of the short-term, blossoming success of the robo-sites, investing has never been more difficult. Investors continue to get overwhelmed with the 24-7, 365 news cycles that proliferates an endless avalanche of global crises via TV, radio, Twitter, Facebook, and the blogosphere.

While a younger, less-affluent DIY demographic may flock to some of these robo-advisors, the millions of aging and retiring baby boomers ensures there will be plenty of demand for traditional advisors. Experienced independent RIA advisors and financial planners, like Sidoxia, who integrate low-cost ETFs into their investment management practices stand to benefit handsomely. Those advisors/sites offering simplistic, commoditized ETF offerings with no wealth planning services will be challenged. While I may not lose sleep over the rise of the robo-advisors, I will continue to dream of a robot that will lower my taxes and win me the lottery.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (including Vanguard ETFs), AAPL, but at the time of publishing SCM had no direct position in HD, TWTR, FB, Legal Zoom, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

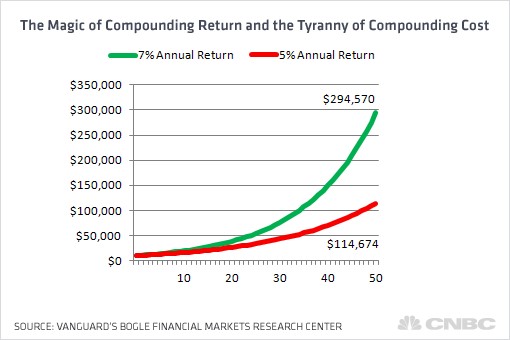

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Skiing Portfolios Down Bunny Slopes

Oh Nelly, take it easy…don’t get too crazy on that bunny slope. With fall officially kicking off and the crisp smell of leaves in the air, the new season also marks the beginning of the ski season. In many respects, investing is a lot like skiing. Unfortunately, many investors are financially skiing their investment portfolios down a bunny slope by stuffing their money in low yielding CDs, money market accounts, and Treasury securities. The bunny slope certainly feels safe and secure, but many investors are actually doing more long-term harm than good and could be potentially jeopardizing their retirements.

Let’s take a gander at the cautious returns offered up from the financial bunny slope products:

Source: Bankrate.com

That CD earning 1.21% should cover a fraction of your medical insurance premium hike, or if you accumulate the interest from your money market account for a few years, perhaps it will cover the family seeing a new 3-D movie. If you also extend the maturity on that CD a little, maybe it can cover an order of chicken fingers at Applebees (APPB)?!

We all know, for much of the non-retiree population, the probability that entitlement programs like Social Security and Medicare will be wiped out or severely cut is very high. Not to mention, life expectancies for non-retirees are increasing dramatically – some life insurance actuarial tables are registering well above 100 years old. These trends indicate the criticalness of investing efficiently for a large swath of the population, especially non-retirees.

Let’s Face It, One Size Does Not Fit All

Bodie Miller & Grandpa

As I have pointed out in the past, when it comes to investing (or skiing), one size does not fit all (see article). Just as it does not make sense to have Bode Miller (32 year old Olympic gold medalist) ski down a beginner’s bunny slope, it also does not make sense to take a 75-year old grandpa helicopter skiing off a cornice. The same principles apply to investment portfolios. The risk one takes should be commensurate with an individual’s age, objectives, and constraints.

Often the average investor is unaware of the risks they are taking because of the counterintuitive nature of the financial market dangers. In the late 1990s, technology stocks felt safe (risk was high). In the mid-2000s, real estate felt like a sure bet (risk was high), and in 2010, Treasury bonds and gold are currently being touted as sure bets and safe havens (read Bubblicious Bonds and Shiny Metal Shopping). You guess how the next story ends?

Unquestionably, coasting down the bunny slopes with CDs, money market accounts, and Treasuries is prudent strategy if you are a retiree holding a massive nest egg able to meet all your expenses. However, if you are younger non-retiree and do not want to retire on mac & cheese or work at Wal-Mart as a greeter into your 80s, then I suggest you venture away from the bunny slope and select a more suitable intermediate path to financial success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and WMT, but at the time of publishing SCM had no direct position in APPB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Filet or Mac & Cheese? Investing for Retirement

The financial crisis of 2008-2009 placed a large swath of investors into paralysis based on a fear the United States and the rest of the world was on the verge of irreversible destruction. Regardless of what the newspaper headlines are reading and television pundits are spouting, individuals have to shrewdly plan for retirement no matter what the economy is doing. So then the question becomes, do you want to be eating macaroni & cheese in retirement, or does filet mignon or alternate five-star cuisine sound more appealing? I vote for the latter.

Despite what the government statistics are saying about the current state of benign inflation, you do not need to be a genius to see medical costs are exploding, energy charges have skyrocketed, and even more innocuous items such as movie ticket prices continue to rise. If that’s not a burden enough, depending on your age, there’s a legitimate concern the Social Security and Medicare safety nets may not be there for you in retirement. It is more important than ever to take control of your financial future by investing your money in a more efficient manner (see Fusion), focusing on long-term, low-cost, tax-efficient strategies. Whatever the direction of the financial markets (up, down, or sideways), if you don’t wisely invest your money, you will run the risk of working as a Wal-Mart (WMT) greeter into your 80s and relegated to eating mac & cheese (for lunch and dinner).

Broaden Your Horizons

The last decade has been tough for domestic equities. It’s true that not a lot of compounding of returns has occurred in the domestic equity markets over the last decade (see Lost Decade), but that weakness is not necessarily representative of the next decade’s performance or the past relative strength seen in areas like emerging markets, materials and certain fixed income markets. These alternatives, including cash, would have added significant diversification benefits to investor portfolios during previous years. Rather than focusing on what’s best for the investor, so much financial industry attention has been placed on high cost, high fee, high commission domestic stock funds or insurance-based products. Due to many inherent conflicts of interest, many individual investors have lost sight of other more attractive opportunities, like exchange traded funds, international strategies, and fixed-income investment vehicles.

Rule of 72

Depending on your risk profile, objectives and constraints, the “Rule of 72” implies your retirement portfolio should double from a $100,000 investment now to roughly $200,000 in seven years (to $400,000 in 14 years, $800,000 in 21 years, etc.), assuming your portfolio can earn a 10% annual return. Unfortunately, this snowballing effect of money growth does not work if you are paying out significant chunks of your returns to aggressive brokers and salespeople in the forms of high commissions, fees, and taxes (see a Penny Saved is Billions Earned). For example, if you are paying out total annual expenses of 2-3% to a broker, advisor, or investment manager, the doubling effect of the Rule of 72 will be stretched out to 9-10 years (rather than the above mentioned seven years). If you do not know what you are paying in fees and expenses (like the majority of people), then do yourself a favor and educate yourself about the fee structures and tax strategies utilized in your investments (see also Investor Confusion). If you haven’t started investing, or you are shoveling out a lot of money in fees, expenses, and taxes, then you should reconsider your current investment stretegy. Otherwise, you may just want to begin stockpiling a lot of macaroni & cheese in your retirement pantry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and shares in WMT, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC “Contact” page for more information.

Building Your Financial Future – Mistakes Made in Investment Planning

Building Your Dream Future Requires a Plan

Building your retirement and financial future can be likened with the challenge of designing and building your dream home. The tools and strategies selected will determine the ultimate cost and outcome of the project.

I constantly get asked by investors, “Wade, is this the bottom – is now the right time to get in the markets?” First of all, if I precisely knew the answer, I would buy my own island and drink coconut-umbrella drinks all day. And secondarily, despite the desire for a simple, get-rich quick answer, the true solution often is more complex (surprise!). If building your financial future is like designing your dream home, then serious questions need to be explored before your wealth building journey begins:

1) Do I have enough money, and if not, how much money do I need to develop my financial future?

2) Can I build it myself, or do I need the help of professionals?

3) Do I have contingency plans in place, should my circumstances change?

4) What tools and supplies do I need to effectively bring my plans to life?

Most investors I run into have no investment plan in place, do not know the costs (fees) of the tools and strategies they are using, and if they are using an advisor (broker) they typically are in the dark with respect to the strategy implemented.

For the “Do-It-Yourselfers”, the largest problem I am witnessing right now is excessive conservatism. Certainly, for those who have already built their financial future, it does not make sense to take on unnecessary risk. However, for most, this is a losing strategy in a world laden with inflation and ever-growing entitlements like Medicare and Social Security. There’s clearly a difference between stuffing money under the mattress (short-term Treasuries, CDs, Money Market, etc.) and prudent conservatism. This is a credo I preach to my clients.

In many cases this conservative stance merely compounds a previous misstep. Many investors undertook excessive risk prior to the current financial crisis – for example piling 100% of investment portfolios into five emerging market commodity stocks.

What these examples prove is that the average investor is too emotional (buys too much near peaks, and capitulates near bottoms), while paying too much in fees. If you don’t believe me, then my conclusions are perfectly encapsulated in John Bogle’s (Vanguard) 1984-2002 study. The analysis shows the average investor dramatically underperforming both the professionally managed mutual fund (approximately by 7% annually) and the passive (“Do Nothing”) strategy by a whopping 10% per year.

Building your financial future, like building your dream home, requires objective and intensive planning. With the proper tools, strategies and advice, you can succeed in building your dream future, which may even include a coconut-umbrella drink.

{kind=link}