Posts tagged ‘retirement planning’

Motel 6 or Four Seasons? Preparing, Not Panicking, for Retirement

Stock prices go up more often than down, and that was the case again last month. The S&P 500, Dow Jones Industrial Average, and the NASDAQ were all up in April. For the year, the S&P has gained +8.6%, Dow +2.9%, and NASDAQ +16.8%. What’s more, these increases are built upon the appreciation experienced in the fourth quarter of last year – the S&P 500 index has rebounded more than +19% since the last lows seen in the middle of last October.

Even when the unemployment rate currently stands at 3.5%, and GDP continues to grow for the third consecutive quarter, there is never a shortage of concerns (see also A Series of Unfortunate Events) as evidenced by worrying questions like these:

- Is the Federal Reserve going to increase interest rates again?

- Has inflation peaked?

- Are we going into a recession?

- Is Silicon Valley Bank and First Republic Bank the beginning or the end of bank failures?

- Will Vladimir Putin use nuclear weapons in Ukraine?

- What is going to happen with the Debt Ceiling deadline and will the U.S. default on its debt?

- How will elections affect the economy?

- Will AI (artificial intelligence) take all our jobs?

Hope is Not a Strategy

We have lived through an endless number of scary headlines in some shape or fashion throughout our lifetimes. These are all interesting and important questions, but preparation for retirement is much more important than panicking over issues you have no control over. For many investors, however, the more important questions to ask and answer relate to your retirement strategy. The answers to your questions should not contain the word hope – hope is not a strategy. Just guessing and waiting out of fear is unlikely to produce optimal results.

Many Americans spend more time planning a vacation than they do preparing for retirement or planning their finances. Rather than constantly scrolling through headlines on your mobile phone news app, here are some areas of focus and questions you should be asking yourself:

· Investment Strategy: What type of investment strategy should you be utilizing to reach your retirement goals? A passive investment strategy with low-cost index funds and ETFs (Exchange Traded Funds)? Or an active investment strategy with individual stocks, bonds, and mutual funds?

· Diversification: How diversified are your investments? Are you overly concentrated in one asset class, sector, or individual security? If you are over-tilted on one side of your financial boat, it could tip over.

· Risk Tolerance: What is your asset allocation? If you are close to retirement, and you have too much exposure to equities, a retrenchment in the stock market could delay your retirement plans by years. This concept highlights the importance of rebalancing your portfolio as you get closer to retirement.

· Fees: What are you paying in advisor fees and/or product fees? Fees are like a leaky faucet. You may not notice a leak over a day or week, but over a period of a month or longer, you are likely to receive huge water bills. Over the long-run, even a small pin-hole leak can cause extreme water damage to floors, ceilings, and walls just like fees could delay retirement or dramatically reduce your nest egg.

· Tax Planning: Are you maximizing your tax-deferred investment accounts? Whether you are contributing the limit to your IRA (Individual Retirement Account), 401(k) retirement plan at work, or pension (for larger business owner contributions), these are tremendous tax-deferral savings vehicles. By squirreling away savings during your prime earnings years, your investments can enjoy the snowballing effect of compounding over the long-term.

· Retirement Timing: When do you plan to retire? Do you have enough money to retire, and what type of liquidity needs will you need during retirement? Figuring out the timing of Social Security can be another variable that may factor into your retirement timing decision (see also Can You Retire? Getting to Your Number).

· DIY or Hire Advisor: When it comes to managing your investments, do you plan on doing it yourself (DIY) or hiring a financial advisor? Many people are not adequately equipped to manage their own investments, however identifying a proper financial advisor still requires significant legwork and research as well. Check out a recent webinar I produced with key questions to ask when looking for a financial advisor (Click here: Questions to Ask When Looking for a Financial Advisor).

In summary, there are a lot of frightening news headlines, but you will be better off focusing on those things you can control. The harsh reality is Americans are not saving sufficiently for retirement. It is true, you can survive off a smaller nest egg, if you plan to subsist off cat food and live in a tent, but most Americans and retirees have become accustomed to a higher standard of living. Also worth noting, we humans are living longer. Thanks to the miracles of modern medicine, lifespans are expanding, with the pandemic caveat. But inflation remains stubbornly high, and you do not want to outlive your savings. Drained savings during retirement may just land you a job as a greeter at Wal-Mart in your 80s.

Although the summer travel season is fast approaching, if you feel you are not satisfactorily prepared for retirement, this is a perfect time to invest attention to this important area. Do yourself a favor and devote at least as much time to answering the key retirement questions above as you do in planning your summer vacation. You may be partying like a rock star now, but if you have not been properly saving for retirement, I will ask you the following question: During retirement, do you want to vacation at the Motel 6 off a local freeway or would you prefer vacationing at a Four Seasons somewhere in Europe? I know what my answer is.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Want to Retire at Age 90?

Do you love working 40-50+ hour weeks? Do you want to be a Wal-Mart (WMT) greeter after you get laid off from your longstanding corporate job? Do you love relying on underfunded government entitlements that you hope won’t be insolvent 10, 20, or 30 years from now? Are you banking on winning the lottery to fund your retirement? Do you enjoy eating cat food?

If you answered “Yes” to one or all of these questions, then do I have a sure-fire investment program for you that will make your dreams of retiring at age 90 a reality! Just follow these three simple rules:

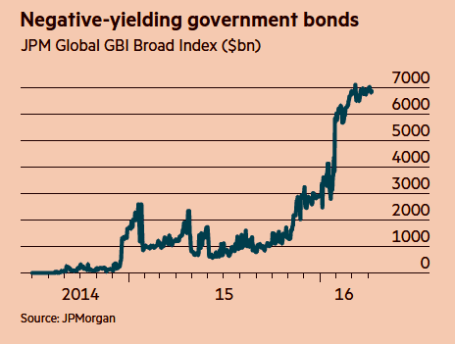

- Buy Low Yielding, Long-Term Bonds: There are approximately $7 trillion in negative yielding government bonds outstanding (see chart below), which as you may understand means investors are paying to give someone else money – insanity. Bank of America recently completed a study showing about two-thirds of the $26 trillion government bond market was yielding less than 1%. Not only are investors opening themselves up to interest rate risk and credit risk, if they sell before maturity, but they are also susceptible to the evil forces of inflation, which will destroy the paltry yield. If you don’t like this strategy of investing near 0% securities, getting a match and gasoline to burn your money has about the same effect.

Source: Financial Times

- Speculate on the Timing of Future Fed Rate Hikes/Cuts: When the economy is improving, talking heads and so-called pundits try to guess the precise timing of the next rate hike. When the economy is deteriorating, aimless speculation swirls around the timing of interest rate cuts. Unfortunately, the smartest economists, strategists, and media mavens have no consistent predicting abilities. For example, in 1998 Nobel Prize winning economists Robert Merton and Myron Scholes toppled Long Term Capital Management. Similarly, in 1996 Federal Reserve Chairman Alan Greenspan noted the presence of “irrational exuberance” in the stock market when the NASDAQ was trading at 1,350. The tech bubble eventually burst, but not before the NASDAQ tripled to over 5,000. More recently, during 2005-2007, Fed Chairman Ben Bernanke whiffed on the housing bubble – he repeatedly denied the existence of a housing problem until it was too late. These examples, and many others show that if the smartest financial minds in the room (or planet) miserably fail at predicting the direction of financial markets, then you too should not attempt this speculative feat.

- Trade on Rumors, Headlines & Opinions: Wall Street analysts, proprietary software with squiggly lines, and your hot shot day-trader neighbor (see Thank You Volatility) all promise the Holy Grail of outsized financial returns, but regrettably there is no easy path to consistent, long-term outperformance. The recipe for success requires patience, discipline, and the emotional wherewithal to filter out the endless streams of financial noise. Continually chasing or reacting to opinions, headlines, or guaranteed software trading programs will only earn you taxes, transaction costs, bid-ask spread costs, impact costs, high frequency trading manipulation and underperformance.

Saving for your future is no easy task, but there are plenty of easy ways to destroy your savings. If you want to retire at age 90, just follow my three simple rules.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in WMT or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

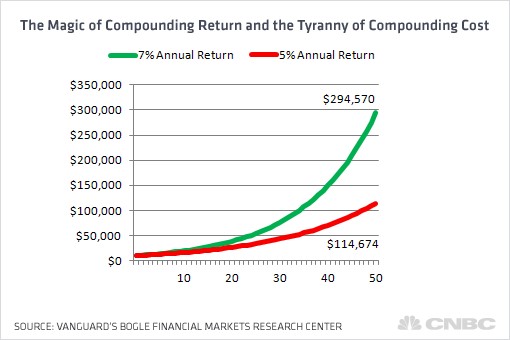

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investor Wake-Up Call

Source: Photobucket

The Pre Wake-Up Conversation

![]()

“Hey Milfred, did you see our brokerage statement? There must be a misprint. It says our portfolio of bonds is down.”

![]()

“Buford, how can that be, when our bond portfolio has been up for 30 consecutive years? I hear Jim Bernanke is trying to artificially inflate the economy by printing money and using it to buy bonds.”

![]() “Sweetheart, you got it wrong…it’s Ben Jernanke.”

“Sweetheart, you got it wrong…it’s Ben Jernanke.”

![]() “Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

“Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

![]() “Sweetie, maybe we should give our broker a call?”

“Sweetie, maybe we should give our broker a call?”

![]() “Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

“Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

![]() “Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

“Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

![]() “Oh I know, Skip is such a nice young man, and so thoughtful.”

“Oh I know, Skip is such a nice young man, and so thoughtful.”

![]() “You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

“You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

![]() “That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

“That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

![]() “What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

“What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

![]() “Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

“Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

![]() “What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

“What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

![]() “I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

“I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

![]() “Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

“Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

![]() “You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

“You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

![]() “I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

“I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

The Wake-Up Reality

I make some of these comments with tongue firmly in cheek, but the fact remains we live in a financial world with a structurally flawed system of loosely regulated, banks, brokerage firms, insurance companies, ratings agencies, hedge funds, mutual funds, and other financial institutions that continue to repeatedly place their interests ahead of clients. If the 2008-2009 financial crisis hasn’t taught you anything, then you should realize it behooves you to take control of your financial situation. At least ask tough questions that result in answers you can understand – not a lot of technical mumbo-jumbo that makes an advisor sound smart. Make life easier on yourself and have a blunt wake-up call conversation, otherwise grab a pen and get ready for Skip’s call – he’s about to come over with some more paperwork.

Related articles:

Beating off the Financial Sharks

Fees, Exploitation and Confusion Hammer Investors

Investment Credentials: The Letter Shell Game

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in TJX, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}