Posts tagged ‘Recovery’

Return to Rationality?

As the worst pandemic in more than a generation is winding down in the U.S., people are readjusting their personal lives and investing worlds as they transition from ridiculousness to rationality. After many months of non-stop lockdowns, social distancing, hand-sanitizers, mask-wearing, and vaccines, Americans feel like caged tigers ready to roam back into the wild. An incredible amount of pent-up demand is just now being unleashed not only by consumers, but also by businesses and the economy overall. This reality was also felt in the stock market as the Dow Jones Industrial Average powered ahead another 654 points last month (+1.9%) to a new record level (34,529) and the S&P 500 also closed at a new monthly high (+0.6% to 4,204). For the year, the bull market remains intact with the Dow gaining almost 4,000 points (+12.8%), while the S&P 500 has also registered a respectable +11.9% return.

The story was different last year. The economy and stock market temporarily fell off a cliff and came to a grinding halt in the first quarter of 2020. However, with broad distribution of the vaccines and antibodies gained by the previously infected, herd immunity has effectively been reached. As a result, the U.S. COVID-19 pandemic has essentially come to an end for now and stock prices have continued their upward surge since last March.

Insanity to Sanity?

With the help of the Federal Reserve keeping interest rates at near-0% levels, coupled with trillions of dollars in stimulus and proposed infrastructure spending, corporate profits have been racing ahead. All this free money has pushed speculation into areas such as cryptocurrencies (i.e., Bitcoin, Dogecoin, Ethereum), SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (GameStop Corp, AMC Entertainment), and highly valued, money-losing companies (e.g., Spotify, Uber, Snowflake, Palantir Technologies, Lyft, Peloton, and others). The good news, at least in the short-term, is that some of these areas of insanity have gone from stratospheric levels to just nosebleed heights. Take for example, Cathie Wood’s ARK Innovation Fund (ARKK) that invests in pricey stocks averaging a 91x price-earnings ratio, which exceeds 4x’s the valuation of the average S&P 500 stock. The ARK exchange traded fund that touts investments in buzzword technologies like artificial intelligence, machine learning, and cryptocurrencies rocketed +149% last year in the middle of a pandemic, but is down -10.0% this year. The Grayscale Bitcoin Trust fund (GBTC) that skyrocketed +291% in 2020 has fallen -5.6% in 2021 and -48.1% from its peak. What’s more, after climbing by more than +50% in less than four months, the Defiance NextGen SPAC fund (SPAK) has declined by -28.9% from its apex just a few months ago in February. You can see the dramatic 2021 underperformance in these areas in the chart below.

Inflation Rearing its Ugly Head?

The economic resurgence, weaker value of the U.S. dollar, and rising stock prices have pushed up inflation in commodities such as corn, gasoline, lumber, automobiles, housing, and a whole host of other goods (see chart below). Whether this phenomenon is “transitory” in nature, as Federal Reserve Chairman Jerome Powell likes to describe this trend, or if this is the beginning of a longer phase of continued rising prices, the answer will be determined in the coming months. It’s clear the Federal Reserve has its hands full as it attempts to keep a lid on inflation and interest rates. The Fed’s success, or lack thereof, will have significant ramifications for all financial markets, and also have meaningful consequences for retirees looking to survive on fixed income budgets.

As we have worked our way through this pandemic, all Americans and investors look to change their routines from an environment of irrationality to rationality, and insanity to sanity. Although the bull market remains alive and well in the stock market, inflation, interest rates, and speculative areas like cryptocurrencies, SPACs, meme-stocks, and nosebleed-priced stocks remain areas of caution. Stick to a disciplined and diversified investment approach that incorporates valuation into the process or contact an experienced advisor like Sidoxia Capital Management to assist you through these volatile times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, SPOT, UBER, SNOW, PLTR, LYFT, PTON, GBTC, SPAK, ARKK or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

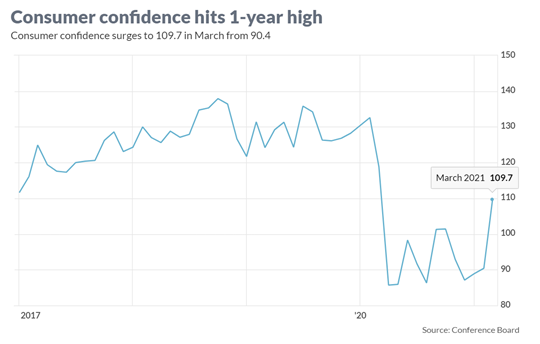

Consumer Confidence Flies as Stock Market Hits New Highs

As the economy starts reopening from a global pandemic that is improving, consumers and businesses are beginning to see a light at the end of the tunnel. The surge in the recently reported Consumer Confidence figures to a new one-year high (see chart below) is evidence the recovery is well on its way. A stock market reaching new record highs is further evidence of the reopening recovery. More specifically, the Dow Jones Industrial Average catapulted 2,094 points higher (+6.2%) for the month to 32,981 and the S&P 500 index soared +4.2%. A rise in interest rate yields on the 10-Year Treasury Note to 1.7% from 1.4% last month placed pressure on technology growth stocks, which led to a more modest gain of +0.4% in the tech-heavy NASDAQ index during March.

Comeback from COVID

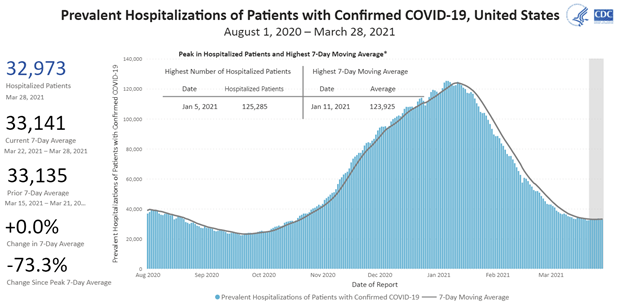

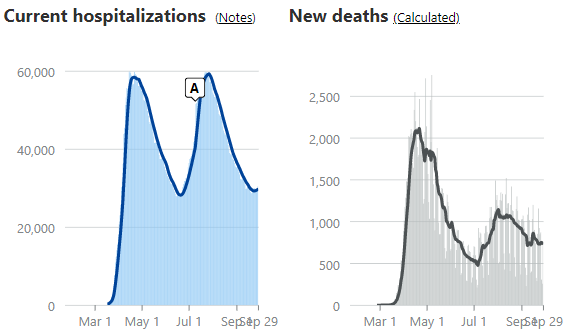

With a combination of 150 million vaccine doses administered and 30 million cumulative COVID cases, the U.S. population has creeped closer toward herd immunity protection against the virus and pushed down hospitalizations dramatically (see chart below).

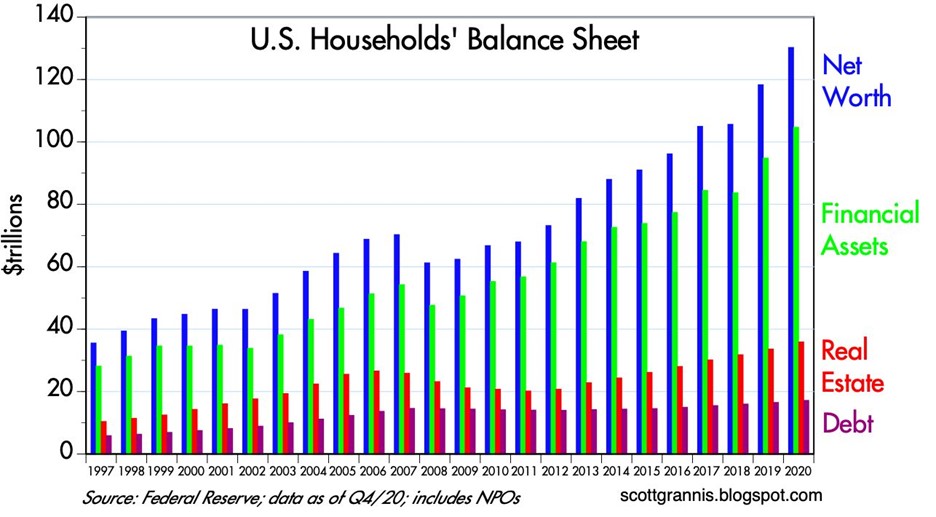

Also contributing to investor optimism have been the rising values of investments and real estate assets thanks to an improving economy and COVID case count. As you can see from the chart below, the net worth of American households has more than doubled from the 2008-2009 financial crisis to approximately $130 trillion dollars, which in turn has allowed consumers to responsibly control and manage their personal debt. Unfortunately, the U.S. government hasn’t been as successful in keeping debt levels in check.

Spending and Paying for Infrastructure Growth

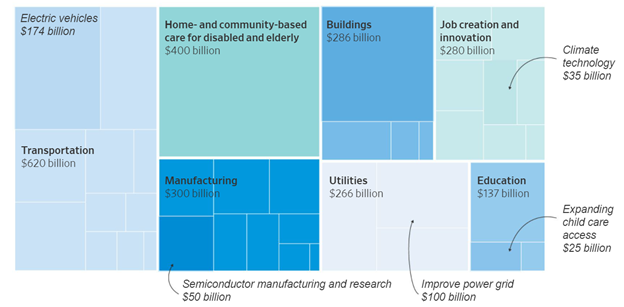

Besides focusing on positive COVID trends, investors have also centered their attention on the passage of a $1.9 trillion stimulus bill last month and a new proposed $2.3 trillion infrastructure bill that President Biden unveiled details on yesterday. At the heart of the multi-trillion dollar spending are the following components (see also graphic below):

- $621 billion modernize transportation infrastructure

- $400 billion to assist the aging and disabled

- $300 billion to boost the manufacturing industry

- $213 billion to build and retrofit affordable housing

- $100 billion to expand broadband access

With over $28 trillion in government debt, how will all this spending be funded? According to The Fiscal Times, there are four main tax categories to help in the funding:

Corporate Taxes: Raising the corporate tax rate to 28% from 21% is expected to raise $730 billion over 10 years

Foreign Corporate Subsidiary Tax: A new global minimum tax on foreign subsidiaries of American corporations is estimated to raise $550 billion

Capital Gains Tax on Wealthy: Increasing income tax rates on capital gains for wealthy individuals is forecasted to raise $370 billion

Income Tax on Wealthy: Lifting the top individual tax rate back to 39.6% for households earning more than $400,000 per year is seen to bring in $110 billion

Besides the economy being supported by government spending, growth and appreciation in the housing market are contributing to GDP growth. The recently released housing data shows housing prices accelerating significantly above the peak levels last seen before the last financial crisis (see chart below).

Although the economy appears to be on solid footing and stock prices have marched higher to new record levels, there are still plenty of potential factors that could derail the current bull market advance. For starters, increased debt and deficit spending could lead to rising inflation and higher interest rates, which could potentially choke off economic growth. Bad things can always happen when large financial institutions take on too much leverage (i.e., debt) and speculate too much (see also Long-Term Capital Management: When Genius Failed). The lesson from the latest, crazy blow-up (Archegos Capital Management) reminds us of how individual financial companies can cause billions in losses and cause ripple-through effects to the whole financial system. And if that’s not enough to worry about, you have rampant speculation in SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (e.g., GameStop Corp. – GME), cryptocurrencies, and NFTs (Non-Fungible Tokens).

Successful investing requires a mixture of art and science – not everything is clear and you can always find reasons to be concerned. At Sidoxia Capital Management, we continue to find attractive opportunities as we strive to navigate through areas of excess speculation. At the end of the day, we remain disciplined in following our fundamental strategy and process that integrates the four key legs of our financial stool: corporate profits, interest rates, valuations, and sentiment (see also Don’t Be a Fool, Follow the Stool). As long as the balance of these factors still signal strength, we will remain confident in our outlook just like consumers and investors are currently.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Politics & COVID Tricks

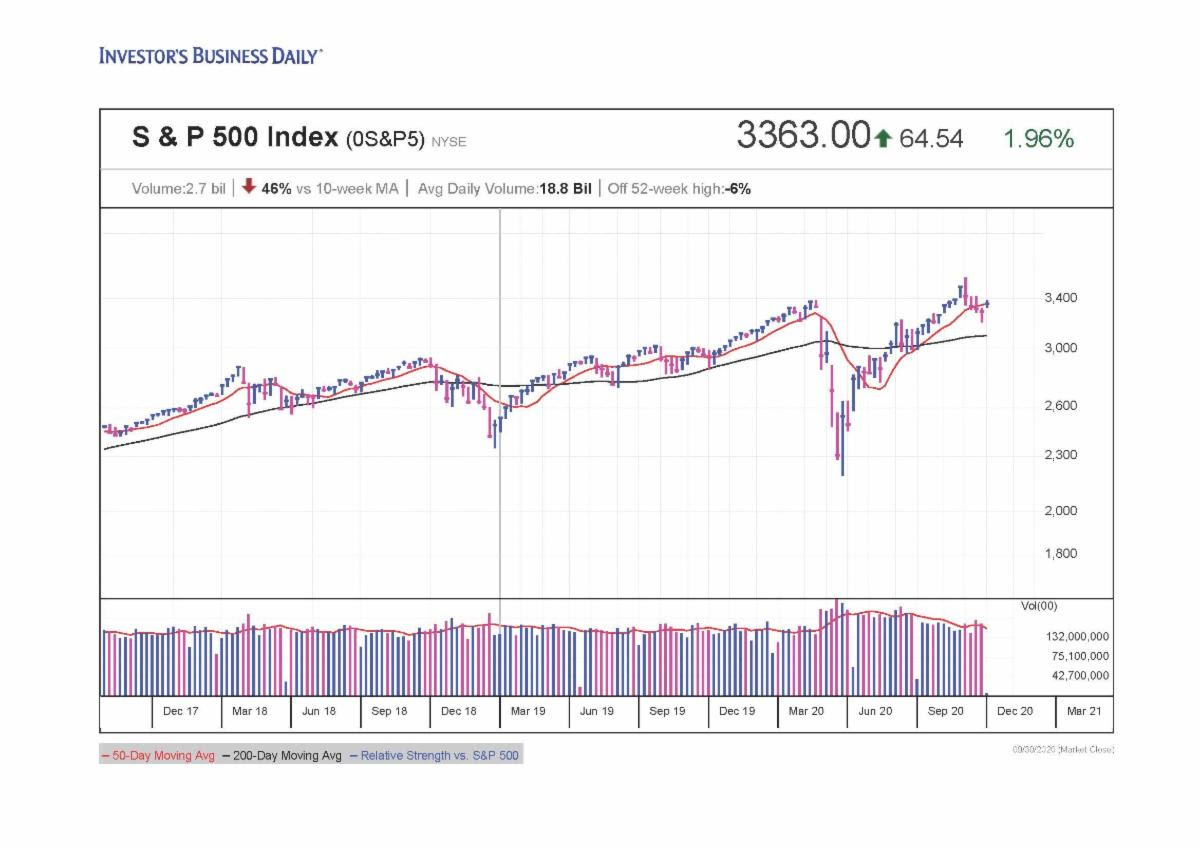

Thanks to a global epidemic, trillions of dollars instantly disappeared during the first quarter of this year, and then, abracadabra…the losses turned into gains and magically reappeared in the subsequent two quarters. After a stabilization in the spread of the COVID-19 virus earlier this year, the stock market rebounded for five consecutive months, at one point rebounding +64% (from late March to early September) – see chart below. However, things became a little bit trickier for the recent full month as concerns heightened over the outcome of upcoming elections; uncertainty over a potential coronavirus-related stimulus package agreement; and fears over a fall resurgence in COVID-19 cases. Although the S&P 500 stock index fell -3.9% and the Dow Jones Industrial Average slipped -2.3% during September, the same indexes levitated +8.5% and +7.6% for the third quarter, respectively.

Source: Investors.com

Washington Worries

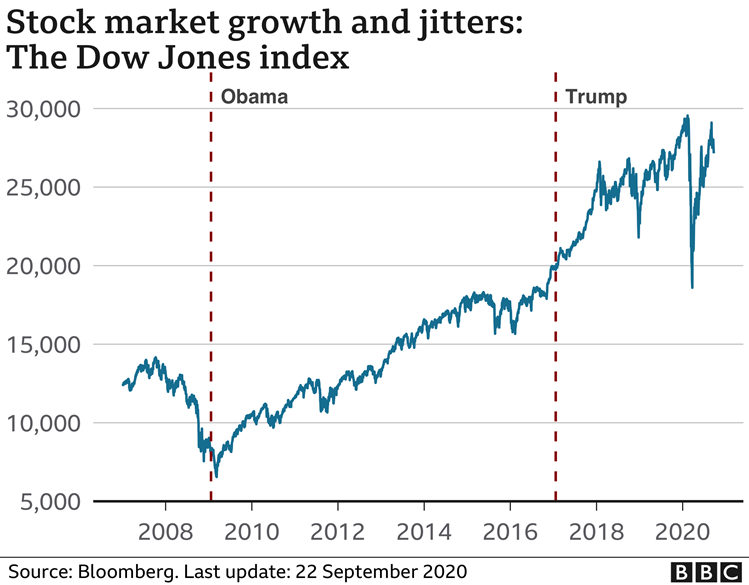

Anxiety over politics is nothing new, and as I’ve written extensively in my Investing Caffeine blog, history teaches us that politics have little to do with the long-term performance of the overall stock market (e.g., see Politics & Your Money). Nobody knows with certainty how the elections will impact the financial markets and economy (myself included). But what I do know is that many so-called experts said the stock market would decline if Barack Obama won the presidential election…in reality the stock market soared. I also know the so-called experts said the stock market would decline if Donald Trump won the presidential election… in reality the stock market soared. So, suffice it to say, I don’t place a lot of faith into what any of the so-called political experts say about the outcome of upcoming elections (see the chart below).

COVID Coming Back?

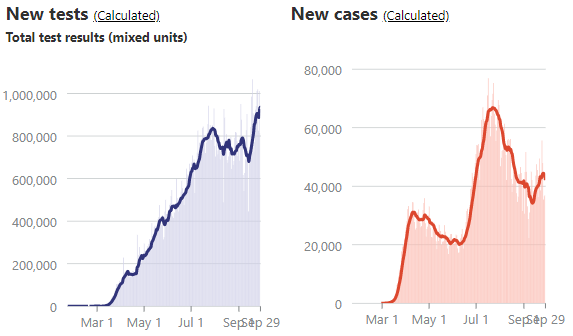

One of the reasons stock prices have risen more than 50%+ is due to a stabilization in COVID-19 virus trends. As you can see from the charts below, new tests, hospitalizations, and death rates are generally on good trajectories, according to the COVID Tracking Project. However, new COVID cases have bumped higher in recent weeks. This recent, troubling trend has raised the question of whether another wave of cases is building in front of a dangerous, seasonally-cooler fall flu season. Traditionally, it’s during this fall period in which contagious viruses normally spread faster.

Source: The COVID Tracking Project

Regardless of the trendline in new cases, there is plenty of other promising COVID developments to help fight this pandemic, such as the pending approvals of numerous vaccines, along with improved therapies and treatments, such as therapeutics, steroids, blood thinners, ventilators, and monoclonal antibodies.

Business Bounce

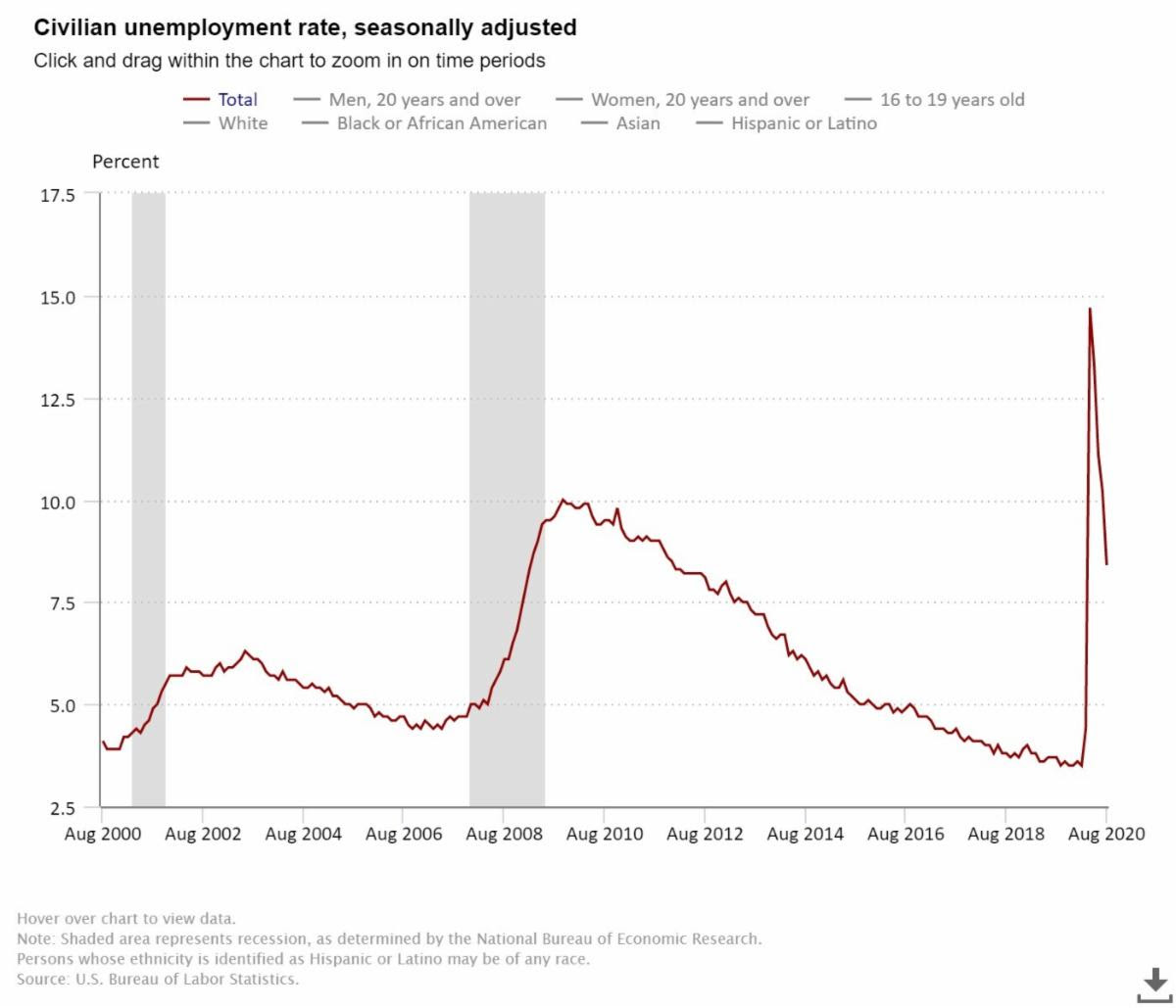

From the 10,000-foot level, despite worries over various political outcomes, the economy is recovering relatively vigorously. As you can see from the chart below, the rebound in employment has been fairly swift. After peaking in April at 14.7%, the most recent unemployment rate has declined to 8.4%, and a closely tracked ADP National Employment Report was released yesterday showing a higher than expected increase in new private-sector monthly jobs (749,000 vs. 649,000 median estimate).

Source: U.S. Bureau of Labor Statistics

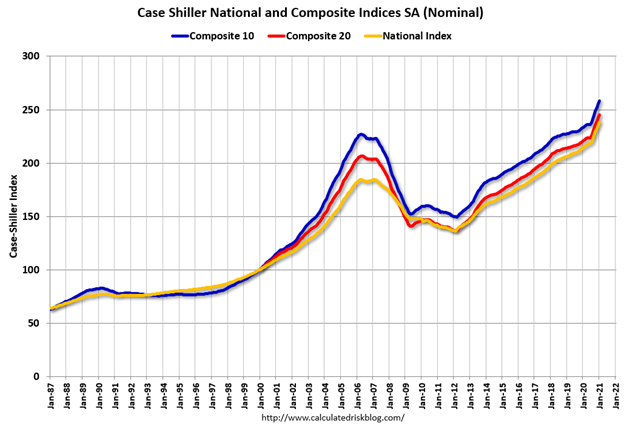

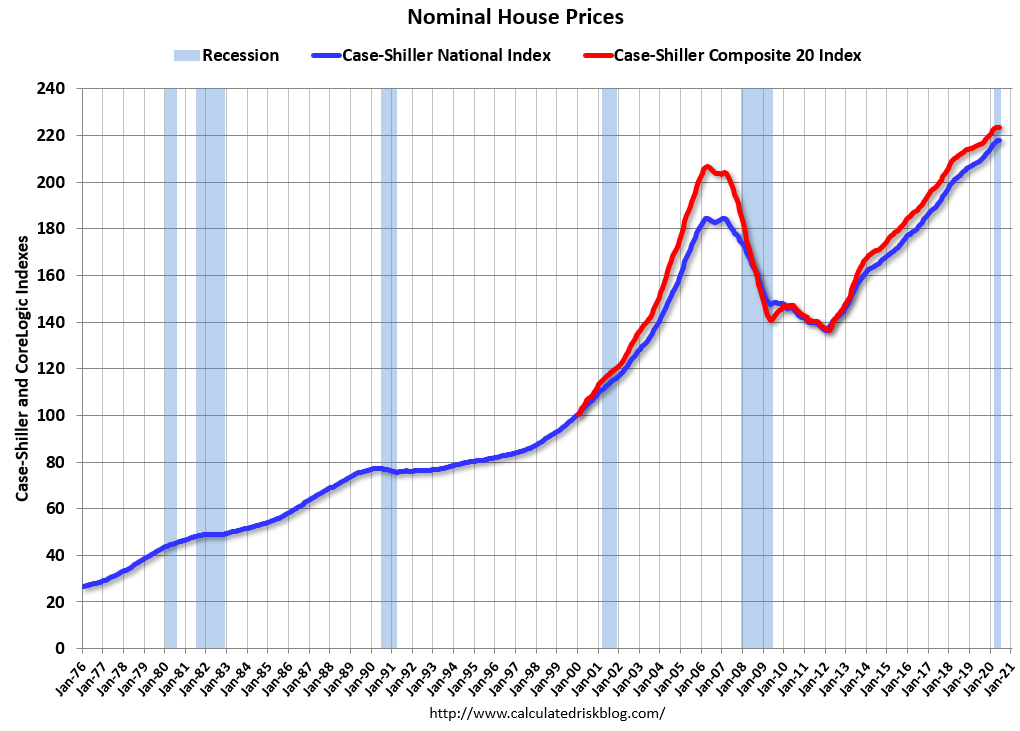

From a housing perspective, house sales have been on fire. Record-low interest rates, mortgage rates, and refinancing rates have been driving higher home purchases and rising prices. Urban flight to the suburbs has also been a big housing tailwind due to the desire for more socially distanced room, additional home office space, and expansive backyards. Adding fuel to the housing fire has been record low supply (i.e., home inventories). The robust demand is evident by the record Case-Shiller home prices (see chart below).

Source: Calculated Risk

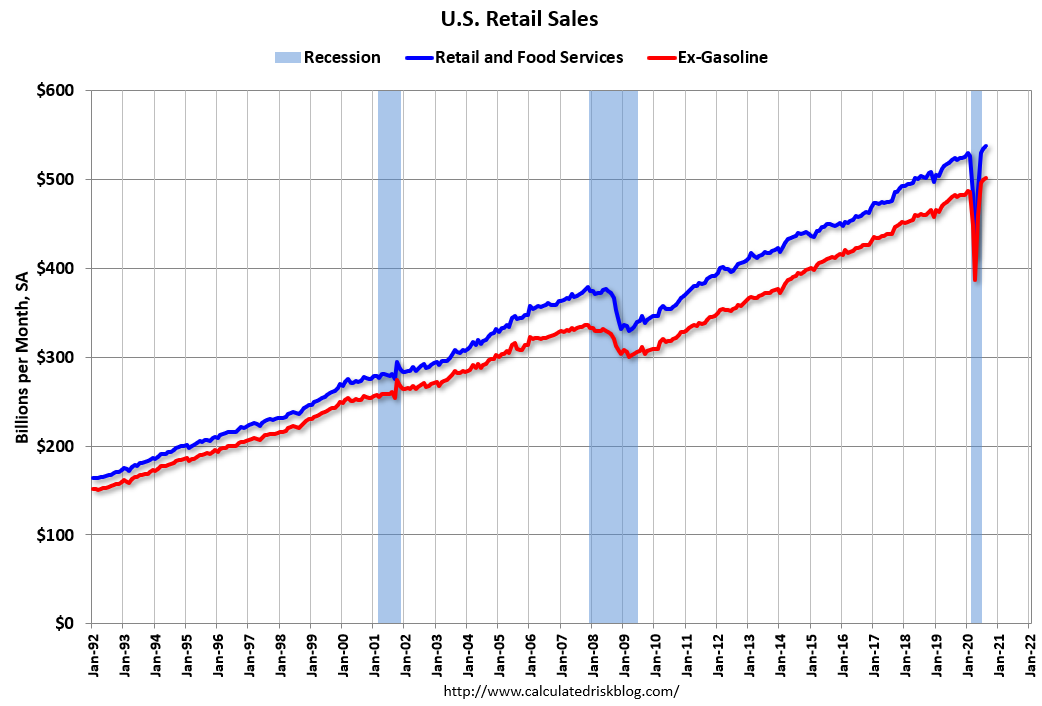

There are plenty of industries hurting, including airlines, cruise lines, hotels, retailers, and restaurants but the economic rebound along with government stimulus (i.e., direct government checks and unemployment relief payments) have led to record retail sales (see chart below). Spending could cool if an additional coronavirus-related stimulus package agreement is not reached, but until the government checks stop flowing, consumers will keep spending.

Source: Calculated Risk

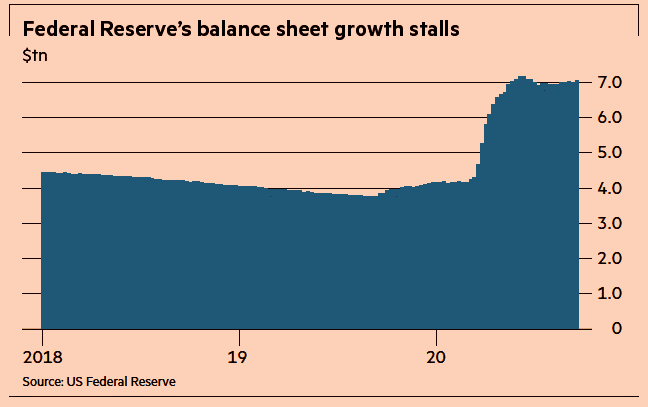

Besides trillions of dollars in fiscal relief injected into the economy, the Federal Reserve has also provided trillions in unprecedented relief (see chart below) through its government and corporate bond buying programs, in addition to its Main Street Lending Program.

Source:The Financial Times

There has been a lot of political hocus pocus and COVID smoke & mirrors that have much of the population worried about their investments. In every presidential election, you have about half the population satisfied with the winner, and half the population disappointed in the winner…this election will be no different. The illusion of fear and chaos is bound to create some short-term financial market volatility over the next month, but behind the curtains there are numerous positive, contributing factors that are powering the economy and stock market forward. Do yourself a favor by focusing on your long-term financial future and don’t succumb to politics and COVID tricks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFS), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Floating Hedge Fund on Ice Thawing Out

These days, pundits continue to talk about how the same financial crisis plaguing Greece and its fellow PIIGS partners (Portugal, Ireland, Italy & Spain) is about to plow through the eurozone and then ultimately the remaining global economy with no mercy. If all the focus is being placed on a diminutive, calamari-eating, Ouzo-drinking society like Greece, whose economy matches the size of Maryland, then why not evaluate an even more miniscule, PIIGS prequel country…Iceland.

That’s right, the same Iceland that just four years ago people were calling a “hedge fund on ice.” You know, that frozen island that had more foreign depositors investing in their banks than people living in the country. Before Icelandic banks became more than 75% of the overall stock market, and Gordon Gekko became the country’s patron saint, Iceland was more known for fishing. The fishing industry accounted for about half of Iceland’s exports, and the next largest money maker may have been Bjork, the country’s famed and quirky female singer.

In looking back at the financial crisis of 2008-2009, as it turned out, Iceland served as a canary in the global debt binging coal mine. In order to attract the masses of depositors to Icelandic banks, these financial institutions offered outrageous, unsustainable interest rates to yield-starved customers. How did the Icelandic bankers offer such high rates? Well of course, it was those can’t-lose American subprime mortgages that were offering what seemed like irresistibly high yields. Of course, what seemed like a dream at the time, eventually turned into a nightmare once the scheme unraveled. Ultimately, it became crystal clear that the subprime borrowers could not pay the outrageous rates, especially after rates unknowingly reset to untenable levels for many borrowers.

At the peak of the crisis, the Icelandic banks were holding amounts of debt exceeding six times the Icelandic GDP (Gross Domestic Product) and these lenders suffered more than $100 billion in losses. One of the Icelandic banks was even funding a large condominium project in my neighboring Southern California city of Beverly Hills. When the excrement hit the fan after Lehman Brothers went bankrupt, it didn’t take long for Iceland’s stock market to collapse by more than -95%; Iceland’s Krona to crumple; and eventually the trigger of Iceland’s multi-billion bailout by numerous constituents, including the IMF (International Monetary Fund).

Bitter Medicine First, Improvement Next

Today, four years after the subprime implosion and Lehman debacle, the hedge fund on ice known as Iceland is beginning to thaw, and their economic picture is looking much brighter (see charts below). GDP growth is the highest it has been in four years (4.5% recently); the stock market has catapulted upwards (almost doubling from the lows); and the Iceland unemployment rate has declined from over 9% a few years ago to about 7% today.

Source: Trading Economics

Source: Trading Economics

Re-jiggering a phony economy with a faulty facade cannot be repaired overnight. However, now that the banking system has been allowed to clear out its excesses, Iceland can move forward. One tailwind behind the economy has been Iceland’s weaker currency, which has led to a +17% increase in foreign tourist nights at Icelandic hotels through April this year. What’s more, tourist traffic at Iceland’s airport hit a record in May. Iceland has taken its bitter medicine, adjusted, and is currently reaping some of the rewards.

Although the detrimental effects of austerity experienced by the economies and banks of Greece, Spain, and Italy crowd out most of today’s headlines, Iceland is not the only country to make painful changes to its fiscal ways and then taste the sweetness of progress. Let’s not forget the Guinness drinking Irish. Ireland, like Greece, Portugal, and Spain received a bailout, but Ireland’s banking system was arguably worse off than Spain’s, yet Ireland has seen its borrowing costs on its 10-year bond decrease dramatically from 9.2% at the beginning of 2011 to about 7.4% this month (still high, but moving in the right direction). The same can be said for the United States. Our banks were up against the ropes, but after some recapitalization, tighter oversight, and stricter lending standards, our banks have gotten back on track and have helped assist our economy grow for 11 consecutive quarters (albeit at uninspiring growth rates).

The austerity versus growth debate will no doubt continue to circulate through media circles. In my view, these arguments are too simplistic and one dimensional. Every country has its unique culture and distinct challenges, but even countries with massive financial excesses can steer themselves back to a path of growth. A floating hedge fund on ice to the north of us has proven that fact to us, as we witness brighter days beginning to thaw Iceland’s chilly economy to expansion again.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman Brothers, Guinness, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Bears Hibernate During Melt-Up

Source: Photobucket

Here we are 719 days from the market bottom of March 2009, and the S&P 500 has more than doubled from its index low value of 666 to 1343 today. Noticeably absent during the meteoric rise have been the hibernating bears, like economist Nouriel Roubini (aka “Dr. Doom”) or Peter Schiff (see Emperor Schiff Has No Clothes), who blanketed the airwaves in 2008-2009 when financial markets were spiraling downwards out of control. The mere fact that I am writing about this subject may be reason enough to expect a 5-10% correction, but with a +100% upward move in stock prices I am willing to put superstition aside and admire the egg on the face of the perma-bears.

Shape of Recovery

After it became clear that the world was not coming to an end, in late 2009 and throughout 2010, the discussion switched from the likelihood of a “Great Depression” to a debate over the shape of the alphabet letter economic recovery. Was the upturn going to be an L-shaped, V-shaped, square root-shaped, or what Roubini expected – a U-shaped (or bathtub-shaped) recovery? You be the judge — does six consecutive quarters of GDP expansion with unemployment declining look like a bathtub recovery to you?

Chart Source: Yahoo Finance

This picture above looks more like a “V” to me, and the recently reported Institute for Supply Management’s (ISM) manufacturing index figure of 60.8 in January (the highest reading in seven years) lends credence to a stronger resurgence in the economy. Apparently the PIMCO bear brothers, Mohamed El-Erian and Bill Gross, are upwardly adjusting their view of a “New Normal” environment as well. Just recently, the firm raised its 2011 GDP forecast by 40-50% to a growth rate of 3-3.5% in 2011.

The Bears’ Logic

Bears continually explain away the market melt-up as a phenomenon caused by excessive and artificial liquidity creation (i.e., QE2 money printing, and 0% interest rate policy) Bernanke has provided the economy. Similar logic could be used to describe the excessive and artificial debt creation generated by individuals, corporations, and governments during the 2008-2009 meltdown. Now that leveraged positions are beginning to unwind (banks recapitalizing, consumers increasing savings rate, state and government austerity and tax measures, etc.), the bears still offer little credit to these improving trends.

Are we likely to experience another +100% upward move in stock prices in the broader indexes over the next two years? Unlikely. Our structural government debt and deficits, coupled with elevated unemployment and fiercer foreign competition are all factors creating economic headwinds. Moreover, inflation is starting to heat up and a Federal Funds rate policy cannot stay at 0% forever.

The Shapes of Rebounds

To put the two-year equity market recovery in historical perspective, the Financial Times published a 75-year study which showed the current market resurgence (solid red line) only trailing the post-Great Depression rebound of 1935-1938.

Source: Financial Times

Although we are absolutely not out of the economic woods and contrarian sentiment indicators (i.e., Volatility Index and Put-Call ratio) are screaming for a pullback, the foundation of a sustainable global recovery has firmed despite the persisting chaos occurring in the Middle East. Fourth quarter 2010 corporate profits (and revenues) once again exceeded expectations, valuations remain attractive, and floods of itchy retail cash still remain on the sidelines just waiting to jump in and chase the upward march in equity prices. Although the trajectory of stock prices over the next two years is unlikely to look like the last two years, there is still room for optimism (as I outlined last year in Genesis of Cheap Stocks). The low-hanging equity fruit has been picked over the last few years, and I’m certain that bears like Roubini, Schiff, El-Erian, Gross, et.al. will eventually come out of hibernation. For those investors not fully invested, I believe it would be wise to wait for the inevitable growls of the bears to resurface, so you can take further advantage of attractive market opportunities.

Click Here for More on the PIMCO Downhill Marathon Machine

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Unemployment Hypochondria

Average investors feel ill from the 2008-2009 financial mess, and like hypochondriacs they can only find fleeting reassurances by reviewing endless amounts of unemployment data. Volatile monthly data is not sufficient, so even more erratic weekly jobless claims data are relied upon. Why just stop there? With this insatiable appetite for unemployment rate data right now, people can’t get enough, so I am not only petitioning for the release of a daily jobs report, but also an hourly one.

Jobs data are relatively straightforward and simple for most Americans to understand. However, most people have more difficulty connecting with economic acronyms and data points such as GDP, PPI, CPI, industrial production, Philly Fed, capacity utilization, Conference Board LEI, durable goods, factory orders, energy inventories, trade balance, unit labor costs, and other economic figures.

Normal Progression

What’s the big deal surrounding the infatuation with myopic unemployment data? We have these things called “recessions” about twice every decade, and of the last 11 post-WWII recessions we have had 11 recoveries – not a bad batting percentage. Obviously, unemployment is a big deal if you are one of the 15 million or so people with no job, but as Jim Paulsen, Chief Investment Strategist at Wells Capital Management points out in his August Economic and Market Perspective, this current recovery is progressing at the fastest pace of any recovery over the last 25 years, and yes, jobs are being added (albeit slower than hoped).

“The consensus perception that this recovery is the ‘worst ever’ and consequently extremely vulnerable to a potential double-dip recession is overblown…Even if this recovery is weak compared to older postwar norms, it is still stronger than any other recovery in the last 25 years,” states Mr. Paulsen.

As you can see from Paulsen’s table below, our current recovery is not as brisk as the recoveries in the pre-1983 era, but he chalks up this trend to subpar growth in the United States’ labor force.

Source: James Paulsen, Wells Capital Management

Paulsen identified this dampened worker growth since the mid-1980s. He doesn’t attribute moderate growth to the “New Normal,” as described by PIMCO pals Bill Gross and Mohamed El-Erian (see also New Normal is Old Normal), but rather ascribes the phenomenon to a continuing trend. Paulsen adds:

“Whatever is causing the ‘new-normal’ economy has been doing it for the last 25 years. The ‘new normal’ is actually kind of old—at least a quarter century old.”

If you think about it, what businesses carried out over the last two years is clearly consistent with a normal economic recovery:

1) Businesses fired employees swiftly amid great uncertainty.

2) Businesses cut expenses, especially discretionary ones, and now profits and cash are piling up.

3) Businesses are buying more capital equipment. Spending is up +12% (to ~$1.3 trillion) from early 2009 according to Joe Lavorgna, an economist at Deutsche Bank.

4) Business acquisitions are beginning to heat up. Witness BHP Billiton’s (BHP) bid for Potash Corp (POT), and HP’s (HPQ) bid for 3Par (PAR) as examples (read HP’s Winner’s Curse).

5) Businesses are paying larger dividends and buying back more of their own stock.

All these actions are very reasonable given the continued uncertain economic environment and rapidly building cash war chests. Buying back stock, doing acquisitions, and prudently spending on cost saving equipment are, generally speaking, accretive measures for a company’s profit and loss statement. On the other hand, hiring employees is usually a lagging indicator of economic expansion and acts as diluting profit forces – at least in the short-run until workers become more productive. Eventually cash and/or business confidence will rise enough to push human resource departments over the fence to begin hiring again.

The weekly unemployment claims chart shows how rapidly improvement has been achieved over the last few decades, even though the improvement has stalled at a lofty level.

Source: ScottGrannis.Blogspot.com (8/13/10).

Japan Case Study: Demographic Double Edged Sword

Be careful what you wish for. Low unemployment is not the end-all, be-all of the world we live in. Take Japan for example. From 1953 until 2010, Japan’s unemployment rate averaged about 2.6%. The last reported rate registered 5.2% in July, double Japan’s average, but almost half of the U.S.’s current 9.6% rate.

Why does Japan have lower unemployment? There are numerous reasons cited – everything from over-employment in the agriculture sector to uncounted married women and protective conglomerates to better disincentives in unemployment insurance program. Overshadowing these reasons is the unmistakable aging of the Japanese population. The National Institute of Population and Social Security Research predicts the Japanese population will fall 30% to 90 million by 2055. Low birthrates, limited immigration, and retirement all increase demand for employment, therefore Japan’s younger-age workforce becomes a scarcer resource and will be more likely to secure and maintain employment. Eventually, I will become old enough in retirement that I will need my underwear and bedpan changed, and create a job for someone in the process – a job that cannot be outsourced I may add. Of course there are very few countries that want a declining population, even if it may lead to an improved unemployment rate. A growing country with liberal immigration laws, healthy birthrates, abundant resources, and pro-business initiatives may have higher unemployment rates but also have more jobs available because of the growing workforce.

Source: UN via Financial Times. Declining Japanese population is putting a growing burden on fewer shoulders.

Eventually the 76 million Baby Boomers born between 1946-1964 are going to be exiting the workforce and will increase the burden on our younger workforce. Do we want to follow in the same path of Japan? Or do we want to adjust our legislative process to meet the draining demands of our aging society? My answers are “No,” and “Yes,” respectively.

The unemployment hypochondriacs can take a deep breath knowing the path we are experiencing is nothing new. Certainly I would like to see better policies implemented to accelerate the economic recovery, but regardless of what inept politicians bungle, our innovative companies, and restless voters are waking up to keep our representatives accountable. This is important because we are like a younger but stronger cousin of Japan, and we do not want to follow along the decaying path of an aging indebted country. In the short-run, we all want to see job growth for the millions of unemployed. In the long-run, retiring Boomers will be stretching the resources of our country even more. So although the unemployment hypochondriacs have little to fear in the near-term as the recovery continues, fiscal responsibility needs to be kept in check or hidden economic illnesses may become reality.

Read James Paulsen’s complete August Economic and Market Perspective

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in BHP, POT, HPQ, PAR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sachs Prescribes Telescope Over Microscope

Jeffrey Sachs, Professor at Columbia University and one of Time magazine’s “100 most influential people” recommends that our country takes a longer-term view in handling our problems (read Sachs’s full bio). Instead of analyzing everything through a microscope, Sachs realizes that peering out over the horizon with a telescope may provide a clearer path to success versus getting sidetracked in the emotional daily battles of noise.

I do my fair share of media and politician bashing, but every once in a while it’s magnificent to discover and enjoy a breath of fresh common sense, like the advice coming from Sachs. Normally, I become suffocated with a wet blanket of incessant, hyper-sensitive blabbering that comes from Washington politicians and airwave commentators. With the advent of this thing we call the “internet,” the pace and volume of daily information (see TMI “Too Much Information” article) crossing our eyeballs has only snowballed faster. Rather than critically evaluate the fear-laced news, the average citizen reverts back to our Darwinian survival instincts, or to what Seth Godin calls the “Lizard Brain. ”

Sachs understands the lingering nature to our country’s problems, so in pulling out his long-term telescope, he created a broad roadmap to recovery – many of the points to which I agree. Here is an abbreviated list of his quotes:

On Short-Termism:

“Despite the evident need for a rise in national saving after 2008, President Barack Obama tried to prolong the consumption binge by aggressively promoting home and car sales to already exhausted consumers, and by cutting taxes despite an unsustainable budget deficit. The approach has been hyper short-term, driven by America’s two-year election cycle. It has stalled because US consumers are taking a longer-term view than the politicians.”

On Differences between China and the U.S.:

“China saves and invests; the US talks, consumes, borrows, and talks some more.”

On Why Tax Cuts and Stimulus Alone Won’t Work:

“Short-term tax cuts or transfers on top of America’s $1,500bn budget deficit are unlikely to do much to boost demand, while they would greatly increase anxieties over future fiscal retrenchment. Households are hunkering down, and many will regard an added transfer payment as a temporary windfall that is best used to pay down debt, not boost spending.”

On Malaise Hampering Businesses:

“Businesses, for their part, are distressed by the lack of direction….Uncertainty is a real killer.”

On 5-Point Plan to a U.S. Recovery:

1) Increased Clean Energy Investments: The recovery needs “a significant boost in investments in clean energy and an upgraded national power grid.”

2) Infrastructure Upgrade: “A decade-long program of infrastructure renovation, with projects such as high-speed inter-city rail, water and waste treatment facilities and highway upgrading, co-financed by the federal government, local governments and private capital.”

3) Further Education: “More education spending at secondary, vocation and bachelor-degree levels, to recognize the reality that tens of millions of American workers lack the advanced skills needed to achieve full employment at the salaries that the workers expect.”

4) Infrastructure Exports to the Poor: “Boost infrastructure exports to Africa and other low-income countries. China is running circles around the US and Europe in promoting such exports of infrastructure. The costs are modest – essentially just credit guarantees – but the benefits are huge, in increased exports, support for African development and a boost in geopolitical goodwill and stability.”

5) Deficit Reduction Plan: “A medium-term fiscal framework that will credibly reduce the federal budget deficit to sustainable levels within five years. This can be achieved partly by cutting defense spending by two percentage points of gross domestic product.”

Rather than succumb to the nanosecond, fear-induced headlines that rattle off like rapid fire bullets, Sachs supplies thoughtful long-term oriented solutions and ideas. The fact that Sachs mentions the word “decade” three times in his Op-ed highlights the lasting nature of these serious problems our country faces. To better see and deal with these challenges more clearly, I suggest you borrow Sachs’s telescope, and leave the microscope in the lab.

Read Full Financial Times Article by Jeffrey Sachs

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Earnings Showing Speedy Growth

With approximately 2/3 of the S&P 500 companies reporting, Thomson Reuters is reporting not only are 78% of those companies beating analyst expectations, but they are also beating them by a large margin (~16%). The financial sector is still rather volatile and is distorting comparisons, but if you look at the non-financial sector, profit growth is on pace to grow +35% this quarter as compared to +18% last quarter. Earnings are not the only thing growing…so are revenues. After four quarters of revenue declines, sales are on track to rise +11% this quarter (versus +8% last quarter) thanks to almost 80% of the S&P 500 companies reporting revenue growth (rather than declines) in the first quarter of 2010.

Source: The Wall Street Journal

Signs of Employment Improvement

Unemployment at 9.7% remains stubbornly high, but with corporation’s newfound revenue growth, there are signs companies are becoming more confident in the hiring department as well. Typically the sequence of a business cycle follows the pattern of cutting expenses and increasing layoffs into a recession; building cash at the cycle trough while running leaner expenses and staff; improving productivity with capital expenditures and technology purchases before hiring; and then as the recovery firms up, companies enjoy widening margins with sales growth, resulting in the confidence to hire. Take for example JP Morgan (JPM) mentioned they plan to hire 9,000 workers in the U.S. this year and Intel (INTC) another 1,000 new positions.

Growth is Global

With all the headlines about Greece’s financial woes, one might underestimate the recovery abroad as well. The average earnings growth rate estimates for the G6 stock markets is +41.6% and +21.9% for 2010 and 2011 according to Ed Yardeni, but a majority of the growth is not coming from the Euro zone.

There is still no shortage of issues to worry about, assuming we understand a Utopia does not exist. Besides elevated unemployment, other issues to remain concerned about include: a lack of credit accessibility for small and medium businesses; massive government debt and deficits; and diminishing impacts in the coming quarters from government stimulus and Federal Reserve monetary stimulus.

Regardless of the nervousness, evidence continues to build for a continuation of better than expected earnings. The music will not last forever and eventual stop, but until then, our economy will enjoy the speedier than anticipated earnings growth recovery.

Read Whole Wall Street Journal Article on Earnings (Subscription)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in JPM, INTC, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Clashing Views with Dr. Roubini

The say keep your friends close, and your enemies even closer. Nouriel Roubini, professor of economics and international business at the NYU Stern School of Business, is not an enemy, but I think his fluctuating views (see previous story) and Armageddon expectations are off base. Perma-bears like Roubini and Peter Schiff (view article) have gloated and danced in the media limelight due to their early but eventually right calls. Over the last seven months or so, their forecasts on the U.S. economy and markets have been off the mark. With that said, even those with competing views at times can find common ground. For Nouriel and I, we currently share similar beliefs on gold (see my article on gold).

Here’s what Professor Roubini has to say:

“ I don’t believe in gold. Gold can go up for only two reasons. [One is] inflation, and we are in a world where there are massive amounts of deflation because of a glut of capacity, and demand is weak, and there’s slack in the labor markets with unemployment peeking above 10 percent in all the advanced economies. So there’s no inflation, and there’s not going to be for the time being.The only other case in which gold can go higher with deflation is if you have Armageddon, if you have another depression. But we’ve avoided that tail risk as well. So all the gold bugs who say gold is going to go to $1,500, $2,000, they’re just speaking nonsense. Without inflation, or without a depression, there’s nowhere for gold to go. Yeah, it can go above $1,000, but it can’t move up 20-30 percent unless we end up in a world of inflation or another depression. I don’t see either of those being likely for the time being. Maybe three or four years from now, yes. But not anytime soon.”

My thoughts on oil are less bearish, but nonetheless more cautious given the massive price bounce to around $80 per barrel. Could I see prices coming down to $50 like Roubini feels is appropriate? Certainly. With the $100+ per barrel swing we saw last year, I cannot discount completely the possibility of that scenario. However, unlike gold, oil has a much stronger utility value, and based on the slow adoption of more expensive alternative energies, this commodity will be in strong demand for many years to come. The pace of global economic recovery, especially in countries like China, India, and Brazil provide an underlying demand for the petroleum product. In order to understand the underlying bid for this economic lubricant, all one has to do is look at the appetite of emerging economies like China when it comes to this black gold (see my article on China).

And where does Roubini think markets go from here?

“If the recovery of the economy is going to be anemic, sub-par, below-trend and U-shaped, there is going to be a correction. And therefore my view is to stay away from risky assets. Stay in liquid assets. I don’t know when the correction is going to occur, it could be a while longer, but eventually it will be a pretty ugly correction, across many different asset classes.”

Perhaps Roubini’s “double dip” fears will eventually come true – and he leaves himself plenty of room with vague loose language – however, I follow the philosophy of Peter Lynch: ‘‘If you spend more than 14 minutes a year worrying about the market, you’ve wasted 12 minutes.” Great companies don’t disappear in challenging markets – they become cheaper – and new innovative companies emerge to replace the old guard.

As much as I would like to be right all the time, that’s not the case. In order to learn from past mistakes and continually improve my process, it’s important to get the views of others…even from those with clashing perspectives.

Read IndexUniverse.com Interview with Nouriel Roubini Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and client accounts do not have direct long or short positions in gold positions, however accounts do have long exposure to certain energy stocks and ETFs. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Time to Take Out the Trash: From Garbage to Cream

As we saw with the +50% move in the 2003 NASDAQ recovery when there was a flight to garbage (lower quality stocks), eventually the cream rose to the top in the later stages of the 2002-2007 bull market. Usually investors get what they pay for, yet many of the companies that were left for dead in 2008 (including bankruptcy fears) have rebounded the fiercest. As the “anti-Great Depression” trade has paid off handsomely for those low quality stocks, high quality stocks have patiently waited on the sidelines eager to jump along for the escalating ride. Ben Levisohn, Business Week writer, thinks it’s time for high quality stock’s to outperform their junky brethren. Here’s what Mr. Levisohn had to say:

“The stock market has gained 58% since its bear-market low Mar. 9, but the rally hasn’t lifted all equities equally. As is typical in many market bouncebacks, the worst recovered first. Low-quality companies, those with weak or nonexistent profits, mediocre return on equity, and less-than-stellar balance sheets, outpaced their more solidly profitable peers by nearly a 2-to-1 margin, according to research from Baird Private Wealth Management.”

Intuitively, the “garbage” rally makes sense from the standpoint, the harder you fall, the faster you will bounce. However, the sustainability of such rapid, fierce moves should be questioned. Eventually, fundamentals move up investors’ priority list and the “cream” (quality stocks) rises to the top.

Mr. Levisohn further highlights the disparity between “garbage” and “cream” by noting:

“Baird found that companies not earning a profit gained 92% from the Mar. 9 lows through the end of August, compared with a 47% rise for companies that had the highest profit margins. Companies with the lowest return on equity outperformed those with the highest by more than 2 to 1, according to Baird.”

With the sickly stock rally and the removal of the “global meltdown” scenario apparently behind us, I concur with Mr. Levisohn that now is the time to focus on “quality” stocks. What does “quality” mean? From a quantitative perspective, concentrating on those companies with high returns on invested capital (ROIC), high returns on equity (ROE), companies with low levels of debt (leverage), generating healthy levels of cash flow (See Cash Flow Article), represents “quality” investing to me. From a fundamental standpoint, management teams with a clear track record of success, and companies with deep barriers to entry, and a healthy pipeline of growth opportunities are other quality characteristics I look for.

Companies retaining these higher quality traits generally are not held hostage to the capital markets and banking system (i.e., no bailouts necessary). As a result, these companies have the flexibility to invest additional resources into areas like research & development, marketing, manufacturing, and mergers & acquisitions. Superior companies have the ability to step on the throats of weaker competitors, thereby extending their competitive advantage and garnering additional market share.

We have experienced a massive rebound in the markets since the March lows, but now it’s time to take out the garbage. As I search for high quality stocks through my computer terminal, I’ll be enjoying my delicious coffee…with extra cream.

Read Entire Business Week Article Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}