Posts tagged ‘recessions’

Don’t Do Something…Just Stand There!

Like a full plane hitting a rough patch of turbulence, investors have been shaken by the recent price volatility in the stock market over concerns of a slowing Chinese economy, plummeting oil prices, and a host of other alarming headlines. As a result, investors are left picking up the pieces of the S&P 500 decline, which currently sits off -11% from its 2015 highs (down -15% at the 1/20/16 low). The picture looks even uglier if you consider the Russell 2000 small cap index, which has collapsed -21% from its 2015 highs (-26% at the 1/20/16 low).

What now, and what does this mean? There has been all kinds of crazy technical trading activity occurring around heavy options expirations, stop-loss selling, and short cover buying. With all the frenetic gyrations in the stock market (e.g., 2,000 point swing in the Dow Jones over the last month), there have been no shortage of opinions on TV, on the internet or at the watercooler. However, the best sage advice probably came from 86-year-old investor legend, John “Jack” Bogle (founder of Vanguard Group – $3.4 trillion in assets under management at 12/31/15), who emphatically told investors to “Don’t do something…just stand there!”

The advice to “stay the course” can be very counter-intuitive to human nature. In periods of stress, our brains tend to revert back to our ancestors’ Darwinian survival instincts, which tell us to flee from the ferocious lion (see also Controlling the Investment Lizard Brain). The fact is these periods of turbulence are normal – no different than a bumpy flight into San Francisco. In fact, we’ve hit quite a few choppy air pockets in recent years:

- Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% in 2011)

- Arab Spring/Grexit Fears (-11% in 2012)

- Fed Taper Tantrum (-8% in 2013)

- Ebola Outbreak (-10% in 2014)

- China Slowdown Fears (-13% in 2015)

Through all of this mayhem, including the current 2016 dip, the stock market has still managed to rise an impressive +77% since the 2011 pullback, which sure beats the sub-1% yield earned on bank CDs.

Inevitably, with the recent price breakdown, speculation has begun to swirl around the dreaded “R”-word (aka, recession) again. In general, this is a fruitless effort. When the smartest Nobel Prize winning economists fail miserably at predicting recessions, it’s hard to believe you or I will have a much better success rate. The great investor Peter Lynch astutely summed up recession forecasting as follows:

“It’s lovely to know when there’s recession. I don’t remember anybody predicting 1982 we’re going to have 14 percent inflation, 12 percent unemployment, a 20 percent prime rate, you know, the worst recession since the Depression. I don’t remember any of that being predicted. It just happened. It was there. It was ugly. And I don’t remember anybody telling me about it. So I don’t worry about any of that stuff. I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

The noted Nobel Prize winning economist Paul Samuelson offered this shrewd observation on recessions as well:

“The stock market has called nine of the last five recessions.”

In other words, the stock market can predict recessions, but often times it is a horrible indicator for the health of the economy (e.g., see 2011-2015 above).

While I am definitely not a Nobel Prize winning economist, I can objectively point to supporting evidence showing we currently are not on the edge of a new recession. It is certainly true that a strong U.S. dollar and a Q4 energy earnings deterioration has been a drag on earnings, but these factors only paint a small part of the picture. Without going into gory economic detail, you do not need to be an expert to understand basic macro trends like employment, housing, auto sales, gasoline prices, and interest rates are providing a buttress to the economy.

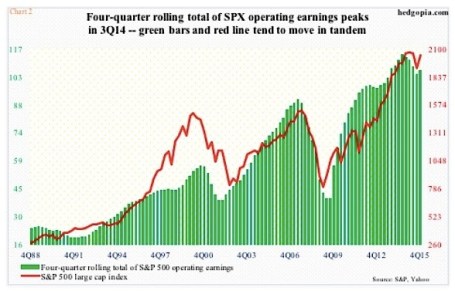

As you can see from the chart below, the -73% cut in Q4 energy sector earnings, along with challenged exports from multinational corporations, has pressured profitability in the S&P 500. However, if you strip out the energy sector, earnings continue to grow. And although it’s early in the 2016 earnings reporting season, so far 73% of companies are beating estimates by 3% on average.

The economic winds are definitely spinning, and we may not be completely through the turbulence, but rather than panicking, you’re probably best served by following the advice of Jack Bogle by standing through the turmoil and look for opportunities when the volatility settles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Coast is Clear Until 2019

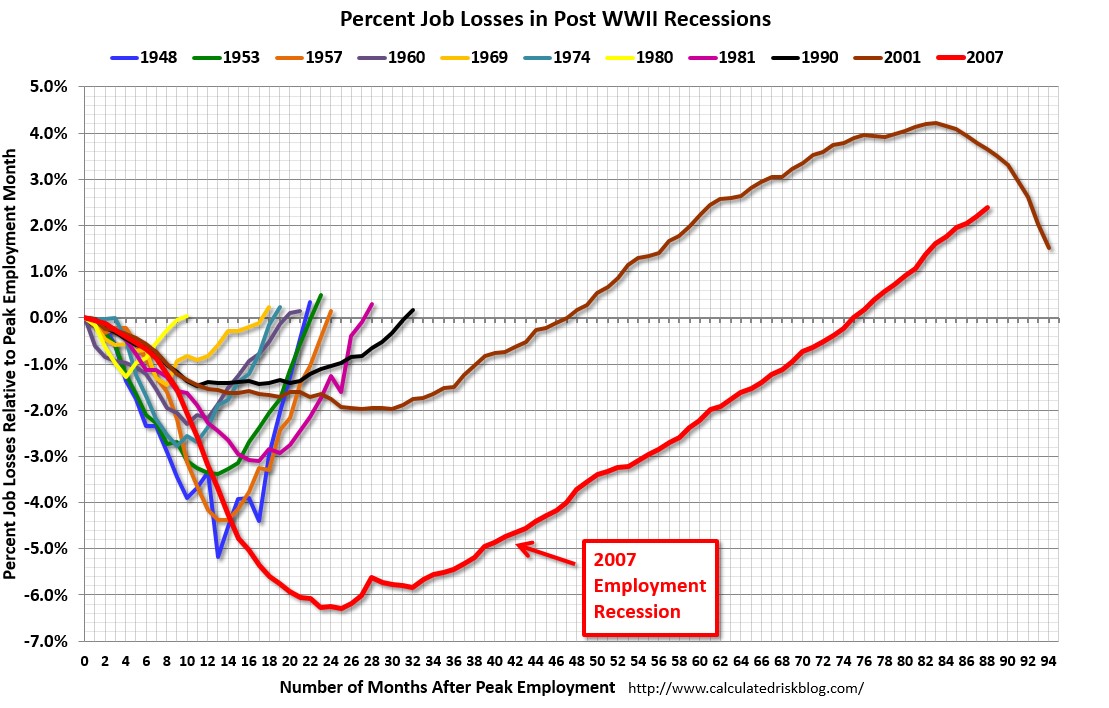

The economic recovery since the Great Financial Crisis of 2008-09 has been widely interpreted as the slowest recovery since World War II. Bill McBride of Calculated Risk captures this phenomenon incredibly well in his historical job loss chart (see red line in chart below):

Source: Calculated Risk

History tells us that the economy traditionally suffers from an economic recession twice per decade, but we are closing in on seven years since the last recession with little evidence of impending economic doom.

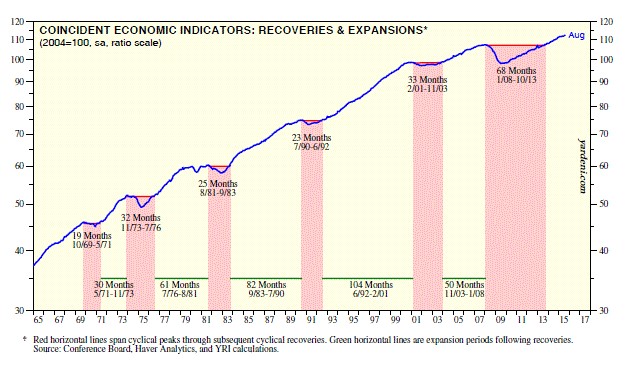

So, are we due for another recession? Logic would dictate that since this recovery has been the slowest in a generation, the duration of this recovery should also be the longest. Strategist Ed Yardeni of Dr. Ed’s Blog uses data from historical economic cycles and CEI statistics (Coincident Economic Indicators) to make the same case. Based on his analysis, Yardeni does not see the next recession arriving until March 2019 (see chart below). If you take a look at the last five previous cycle peaks, recoveries generally last for an additional five and a half years (roughly 65 months). Since the last rebound to a cyclical peak occurred in October 2013, 65 months from then would imply the next downturn would begin in March 2019.

Source: Dr. Ed’s Blog

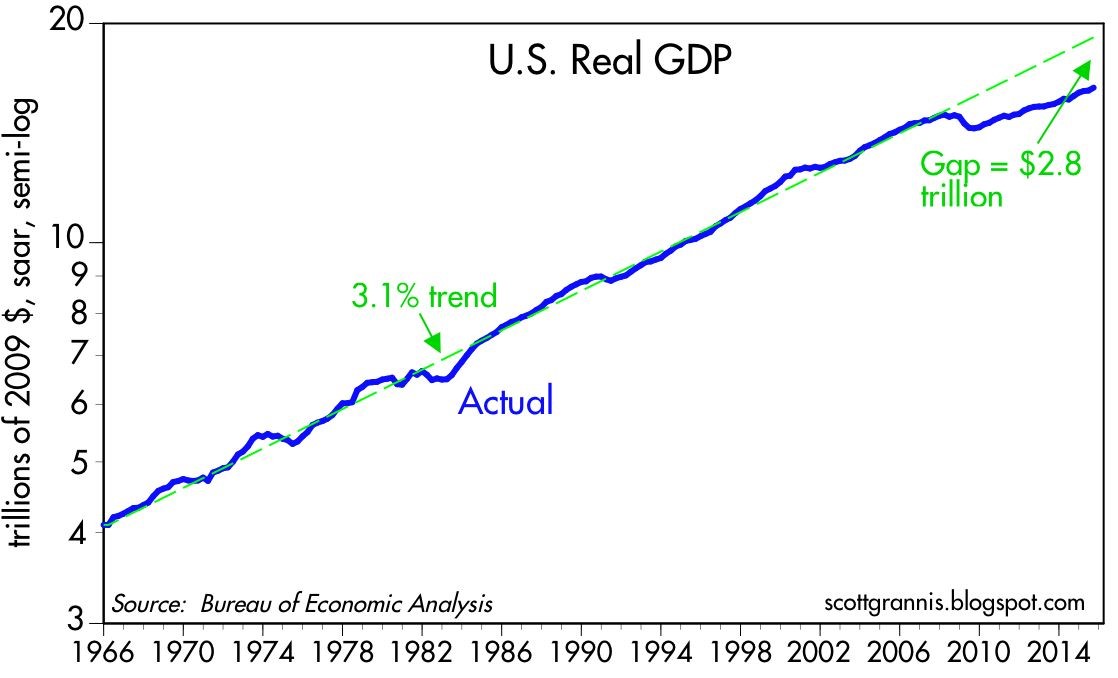

Typically, an economy loses steam and enters a recession after a phase of over-investment, tight labor conditions, and an extended period of tight central bank monetary policies. Over the last seven years, we have experienced quite the opposite. Corporations have been very slow to invest or hire new employees. For those employees hired, many of them are “under-employed” (i.e., working part-time), or in other words, these workers want more work hours. Our country’s slower-than-expected growth has created an output gap. Scott Grannis at Calafia Beach Pundit estimates this gap to approximate $2.8 trillion (see chart below). The CBO expects a smaller gap estimate of about $580 billion to narrow over the next few years. By Grannis’s calculations, there is a reservoir of 5 – 10 million jobs that could be tapped if the economy was operating more efficiently.

Source: Calafia Beach Pundit

Bolstering his argument, Grannis points out that the risk of a recession rises when there are significant capacity constraints and tight money. He sees the opposite happening – an enormous supply of unused capacity remains underutilized as he describes here:

“Today, money is abundant and resources are abundant. Even energy is abundant, because its price has fallen by over 50% in the past year or so. Corporate profits are near record highs, the supply of labor is virtually unconstrained, energy is suddenly cheap, and productive capacity is relatively abundant.”

While new uncertainties have been introduced (e.g., slowing China, potential government shutdown/sequestration, emerging market weakness), the reality remains there is always uncertainty. Even if you truly believe there is more uncertainty today relative to yesterday, the economy has some relatively strong shock absorbers to ride out the volatility.

There are plenty of potentially bad things to worry about, but if it’s a cyclical recession that you are worried about, then why don’t you grab a seat, order a coconut drink with an umbrella, and wait another three and a half years until you reach the circled date of March 2019 on your calendar.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Waiting for the Hundred Minute Flood

Investors have been scarred over the last decade and many retirees have seen massive setbacks to their retirement plans. We have witnessed the proverbial “100 year flood” twice in the 2000s in the shape of a bursting technology and credit bubble in 2000 and 2008, respectively. The instantaneous transmission of data around the globe, facilitated by 24/7 news cycles and non-stop internet access, has only accelerated investor panic attacks – the 100 year flood is now expected every 100 minutes.

If drowning in the 100 year flood of events surrounding Bear Stearns, Lehman Brothers, Washington Mutual, AIG, Fannie Mae, Freddie Mac, TARP bank bailouts, Bernie Madoff’s Ponzi scheme, and Eliot Spitzer’s prostitute appreciation activities were not enough in 2008, investors (and many bearish bloggers) have been left facing the challenge of reconciling an +80% move in the S&P 500 index and +100% move in the NASDAQ index with the following outcomes (through the bulk of 2009 and 2010):

- Flash crash, high frequency traders, and “dark pools”

- GM and Chrysler’s bankruptcies

- Dubai debt crisis

- Goldman Sachs – John Paulson hearings

- Tiger Woods cheating scandal

- Greece bailout

- BP oil spill

- Healthcare reform

- China real estate bubble concerns

- Congressional leadership changes

- European austerity riots

- North Korea – South Korea provocations

- Insider trading raids

- Ireland bailout

- Next: ?????

With all this dreadful news, how in the heck have the equity markets about doubled from the lows of last year? The “Zombie Bears,” as Barry Ritholtz at The Big Picture has affectionately coined, would have you believe this is merely a dead-cat bounce in a longer-term bear-market. Never mind the five consecutive quarters of GDP growth, the 10 consecutive months of private job creation, or the record 2010 projected profits, the Zombie Bears attribute this fleeting rebound to temporary stimulus, short-term inventory rebuild, and unsustainable printing press activity by Federal Reserve Chairman Ben Bernanke.

Perhaps the Zombie Bears will change their mind once the markets advance another 25-30%? Regardless of the market action, individual investors have taken the pessimism bait and continue to hide in their caves. This strategy makes sense for wealthy retirees with adequate resources, but for the vast majority of Americans, earning next to nothing on their nest egg in cash and overpriced Treasuries isn’t going to help much in achieving your retirement goals. Unless of course, you like working as a greeter at Wal-Mart in your 80s and eating mac & cheese for breakfast, lunch, and dinner.

This Time is Different

The Zombies would also have you believe this time is different, or in other words, historical economic cycles do not apply to the recent recession. I’ll stick with French novelist Alphonse Karr (1808-1890) who famously stated, “The more things change, the more things stay the same.”

As you can see from the data below, the recent recession lasted two months longer than the 16 month cycle average from 1854 – 2009. We have had 33 recessions and 33 recoveries, so I am going to go out on a limb and say this time will not be any different. Could we have a double dip recession? Sure, but odds are on our side for an average five year expansion, not the 18 month expansion experienced thus far.

The Grandma Sentiment Indicator

I love all these sentiment indicators, surveys, and various ratios that constantly get thrown around the blogosphere because it is never difficult to choose one matching a specific investment thesis. Strategists urge us to follow the actions of the “smart money” and do the opposite (like George Costanza) when looking at the “dumb money” indicators. The bears would also have you believe the world is coming to an end if you look at the current put/call data (see Smart Money Prepares for Sell Off). Instead, I choose to listen to my grandma, who has wisely reminded me that actions speak louder than words. Right now, those actions are screaming pure, unadulterated fear – a positive contrarian dynamic.

Over the last few years there has been more than $250 billion in equity outflows according to data from the Investment Company Institute (ICI). Bond funds on the other hand have taken in an unprecedented $376 billion in 2009 and about another $216 billion in 2010 through August.

As investment guru Sir John Templeton famously stated, “Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.” Judging by the asset outflows, I would say we haven’t quite reached the euphoria phase quite yet. I won’t complain though because the more fear out there, the more opportunity for me and my investors.

As I have consistently stated, I have no clue what equity markets are going to do over the next six to twelve months, nor does my bottom-up philosophy rely upon making market forecasts to succeed. Evaluating investor sentiment and timing economic cycles are difficult skills to master, but judging by the panicked actions and bond heavy asset inflows, investors are nervously awaiting another 100 year flood to occur in the next hundred minutes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, and AIG derivative security, but at the time of publishing SCM had no direct position in Bear Stearns, Lehman Brothers, JPM, Washington Mutual, Fannie Mae, Freddie Mac, GS, BP, GM, Chrysler, and any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}