Posts tagged ‘real estate’

Fed Ripping Off the Inflation Band-Aid

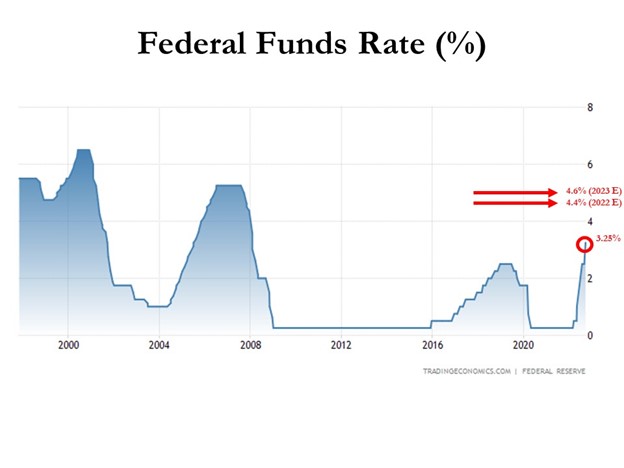

Inflation rates have been running near 40-year highs, and as a result, the Federal Reserve is doing everything in its power to rip off the Band-Aid of insidious high price levels in a swift manner. The Fed’s goal is to inflict quick, near-term pain on the economy in exchange for long-term price stability and future economic gains. How quickly has the Fed been hiking interest rates? The short answer is the rate of increases has been the fastest in decades (see chart below). Essentially, the Federal Reserve has pushed the targeted benchmark Federal Funds target rate from 0% at the beginning of this year to 3.25% today. Going forward, the goal is to lift rates to 4.4% by year-end, and then to 4.6% by next year (see Fed’s “dot plot” chart).

How should one interpret all of this? Well, if the Fed is right about their interest rate forecasts, the Band-Aid is being ripped off very quickly, and 95% of the pain should be felt by December. In other words, there should be a light at the end of the tunnel, soon.

The Good News on Inflation

When it comes to inflation, the good news is that it appears to be peaking (see chart below), and many economists see the declining inflation trend continuing in the coming months. Why do pundits see inflation peaking? For starters, a broad list of commodity prices have declined significantly in recent months, including gasoline, crude oil, steel, copper, and gold, among many others.

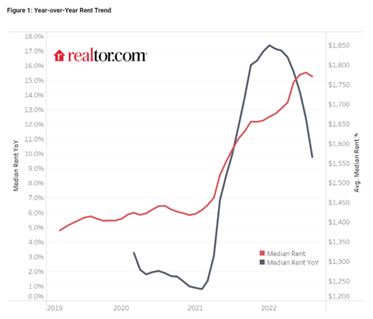

Outside of commodities, investors have seen prices drop in other areas of the economy as well, including housing prices, which recently experienced the fastest monthly price drop in 11 years, and rent prices as well (see chart below).

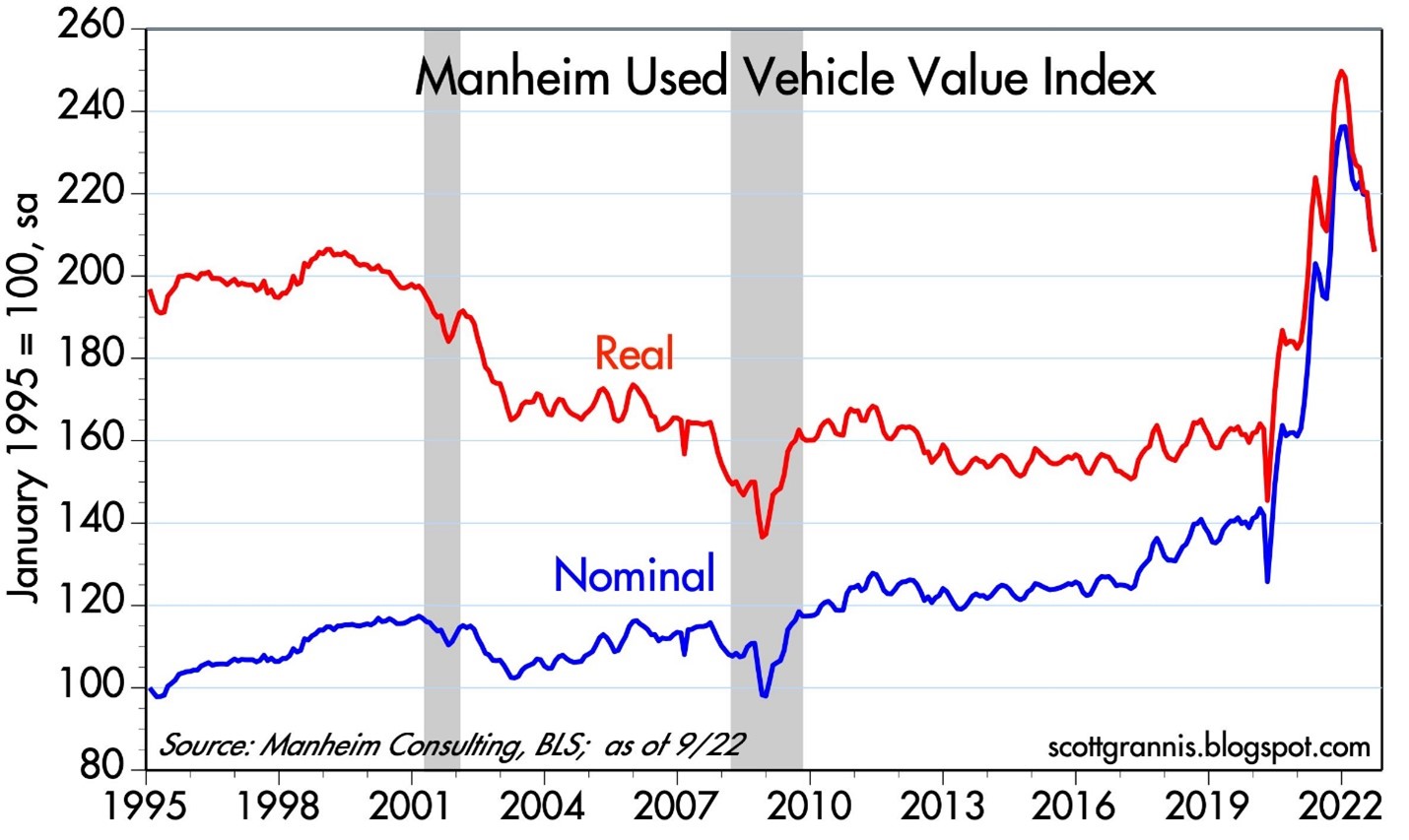

Anybody who was shopping for a car during the pandemic knows what happened to pricing – it exploded higher. But even in this area, we are seeing prices coming down (see chart below), and CarMax Inc. (KMX), the national used car retail chain confirmed the softening price trend last week.

Pain Spread Broadly

When interest rates increase at the fastest pace in 40 years, pain is felt across almost all asset classes. It’s not just U.S. stocks, which declined -9.3% last month (S&P 500), but it’s also housing -8.5% (XHB), real estate investment trusts -13.8% (VNQ), bonds -4.4% (BND), Bitcoin -3.1%, European stocks -10.1% (VGK), Chinese stocks -14.4% (FXI), and Agriculture -3.0% (DBA). The +17% increase in the value of the U.S. dollar this year against a basket of foreign currencies is substantially pressuring cross-border business for larger multi-national companies too – Microsoft Corp. (MSFT), for example, blamed U.S. dollar strength as the primary reason to cut earnings several months ago. Like Hurricane Ian, large interest rate increases have caused significant damage across a wide swath of areas.

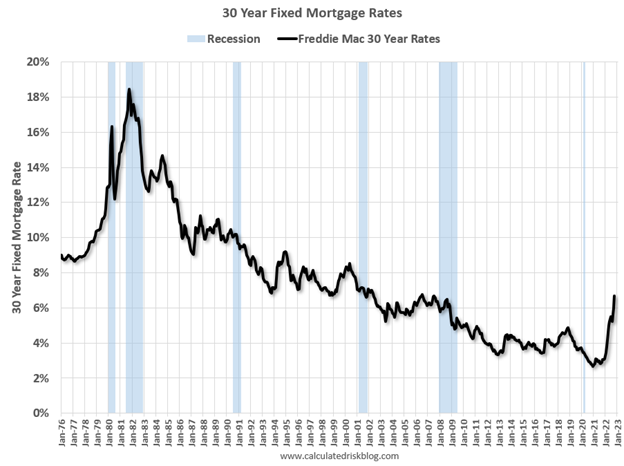

But for those following the communication of Federal Reserve Chairman, Jerome Powell, in recent months, they should not be surprised. Chairman Powell has signaled on numerous occasions, including last month at a key economic conference in Jackson Hole, Wyoming, that the Fed’s war path to curb inflation by increasing interest rates will inflict wide-ranging “pain” on Americans. Some of that pain can be seen in mortgage rates, which have more than doubled in 2022 and last week eclipsed 7.0% (see chart below), the highest level in 20 years.

Now is Not the Time to Panic

There is a lot of uncertainty out in the world currently (i.e., inflation, the Fed, Russia-Ukraine, strong dollar, elections, recession fears, etc.), but that is always the case. There is never a period when there is nothing to be concerned about. With the S&P 500 down more than -25% from its peak (and the NASDAQ down approximately -35%), now is not the right time to panic. Knee-jerk emotional decisions during stressful times are very rarely the right response. With these kind of drops, a mild-to-moderate recession is already baked into the cake, even though the economy is expected to grow for the next four quarters and for all of 2023 (see GDP forecasts below). Stated differently, it’s quite possible that even if the economy deteriorates into a recession, stock prices could rebound smartly higher because any potential future bad news has already been anticipated in the current price drops.

Worth noting, as I have pointed out previously, numerous data points are indicating inflation is peaking, if not already coming down. Inflation expectations have already dropped to about 2%, if you consider the spread between the yield on the 5-Year Note (4%) and the yield on the 5-Year TIP-Treasury Inflation Protected Note (2%). If the economy continues to slow down, and inflation has stabilized or declined, the Federal Reserve will likely pivot to decreasing interest rates, which should act like a tailwind for financial markets, unlike the headwind of rising rates this year.

Ripping off the Band-Aid can be painful in the short-run, but the long-term gains achieved during the healing process can be much more pleasurable.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in MSFT, BND and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in KMX, XHB, VNQ, VGK, FXI, DBA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Become the Landlord of Your Stocks

“Why do you buy stocks?” Unfortunately, many people do not truly understand how to answer that particular question. If they were honest with themselves, many stockholders would respond by saying, “Because they are going up in price,” or maybe, “My neighbor told me to buy stock XYZ.” However, if somebody asked the same question regarding the purchase of a real estate property or an apartment building, would the answer be the same? The short answer is…probably not. There certainly could be some people who answer the stock versus real estate valuation question in the same way, but in general, real estate investors understand the tangibility and relevant factors of a property better than equity investors understand the jargon and abstract nature of most stocks.

There are many ways to value an asset, but in many cases, the value of an asset is spontaneously left in the eye of the beholder. Nevertheless, there is one common approach, applicable across asset classes, which is the net present value or discounted cash flow approach. This valuation methodology basically states any asset is worth the cumulative value of cash inflows minus the value of cash outflows, after adjusting that netted figure for time and interest rates.

In the case of an apartment building, a layman generally understands the basic valuation concept behind adding up the relevant cash inflows and cash outflows. For example, being a landlord of an apartment building involves simple rent collection (cash inflows) in addition to maintenance, repairs, construction costs, employee wages, taxes, and other payments (cash outflows). After making additional assumptions about future rent increases, occupancy levels, wage inflation, and a few other variables, many outside observers could probably come up with a decent estimated value of the property.

The variables relating to an apartment building may be more stable, predictable, and understandable, if compared with the variables of a stock, but the same exact principles apply to both asset classes. Wal-Mart may not collect stable rent checks, but it does collect money from product sales in its 11,500 stores around the world (cash inflows). Wal-Mart’s cash inflows are much less predictable than real estate rent check inflows due to the many retail-specific variables, such as store openings/closings, online competition, promotions, seasonality, inventory levels, and geographic economics. Expenses (cash outflows) are challenging to predict as well due to wage fluctuations, energy cost variability, capital project timing, erratic raw material prices, and other factors. In the end, stock variables may be more volatile and less predictable, but the valuation process should be the same. Valuing stocks requires estimating the cumulative value of cash inflows minus the value of cash outflows, and then adjusting those results for time and interest rates.

Real estate has its own industry language, but the language of stocks has an endless number of acronyms, which can be quite challenging if you consider the dozens of industries and thousands of stocks. Here are a few of my favorite obscure acronyms used across the technology, healthcare, energy, and retail sectors:

Technology: 4G, CDMA, DSLAM, LTE, MPLS, SaaS, SRAM

Energy: BCF, BOE, BTU, EIA, Gwh, kWh, LNG, MWh, WTI

Healthcare: AARP, CRM, DRG, EENT, FDA, HIPAA, MI, SARS

Retail: B2B, EDI, EDLP, GMROI, POS, RFID, SCM, SKU, UPC

As noted earlier, the language and complexity for valuing stocks may be more complicated than valuing other more straightforward asset classes, but the methodology is essentially the same.

The opportunities and rewards stemming from stock ownership are almost endless. While it’s true that successful long-term stock investing is rarely easy, anything worthwhile in life is never simple. If you are able to understand the principal concepts of how to become an effective landlord of real estate, then applying the same principles on how to become an effective landlord of your stock portfolio is highly achievable.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in WMT or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Fallibility of Tangibility

Why do so many star athletes end up going bankrupt? Rather than building a low-cost, tax-efficient, diversified portfolio of stocks and bonds that could help generate significant income and compounded wealth over the long-term (yawn…boring), many investors succumb to the allure of over-exposing themselves to costly, illiquid, tangible assets, while assuming disproportionate risk.

After all, it’s much more exciting to brag about the purchase of a car wash, apartment building or luxury condo than it is to whip out a brokerage statement and show a friend a bond fund earning a respectable 4% yield.

Many real estate investors in my Southern California backyard (epicenter of the 2008-2009 Financial Crisis) have experienced both ruin and riches over the last few decades. The appeal and pitfalls associated with owning tangible assets like real estate are particularly exemplified with professional athletes (see also Hidden Train Wreck). Consider the fate suffered by these following individuals:

- Mike Tyson: Famous boxer Mike Tyson tore through $300 million on multiple homes, cars, jewels and pet tigers before filing for bankruptcy in 2003.

- Julius Erving: Hall of Fame NBA player Julius “Dr. J” Erving went financially belly-up in 2010 after his Celebrity Golf Club International was pushed into foreclosure. Dr. J. was also forced to auction off coveted NBA memorabilia (including championship uniforms, trophies, and rings) along with foreclosing on his personal $2 million, 6,600-square foot Utah home.

- Mark Brunell: Pro Bowl quarterback Mark Brunell was estimated to have earned over $50 million during his career. Due to failed real estate ventures and business loans, Brunell filed for bankruptcy in 2010.

- Evander Holyfield: Heavyweight boxing champion Evander Holyfield burned through a mountain of money estimated at $230 million, including a 235-acre Utah estate, which had 109 rooms and included at least one monthly electric bill of $17,000.

Caveat Emptor

Inclusion of real estate as part of a diversified portfolio makes all the sense in the world – this is exactly what we do for clients at Sidoxia. But unfortunately, many investors mistake the tangibility of real estate with “lower risk,” even though levered real estate is arguably more volatile than the stock market – evidenced by the volatility in publicly traded REIT share prices. For example, the Dow Jones SPDR REIT (RWR) declined by -78% from its 2007 high to its 2009 low versus the S&P 500 SPDR (SPY) drop of -57% over the comparable period. Private real estate investors are generally immune from the heart-pumping price volatility rampant in the public markets because they are not bombarded with daily, real-time, second-by-second pricing data over flashing red and green colored screens.

Without experiencing the emotional daily price swings, many real estate investors ignore the risks and costs associated with real estate, even when those risks often exceed those of traditional investments (e.g., stocks and bonds). Here are some of the important factors these real estate investors overlook:

Leverage: Many real estate investors don’t appreciate that the fact that 100% of a 10% investment (90% borrowed) can be wiped out completely (i.e., lose -100%), if the value of a property drops a mere -10%. Real estate owners found this lesson out the hard way during the last housing downturn and recession.

Illiquidity: Unlike a stock and bond, which merely takes a click of a mouse, buying/selling real estate can take weeks, if not months, to complete. If a seller needs access to liquidity, they may be forced to sell at unattractively low, fire-sale prices. Pricing transparency is opaque due to the variability and volume of transactions, although online services offered by Zillow Group Inc. (Z).

Costs: For real estate buyer, the list of costs can be long: appraisal fee, origination fee, pre-paid interest, pre-paid insurance, flood certification fee, tax servicing fee, credit report fee, bank processing fee, recording fee, notary fee, and title insurance. And once an investment property is officially purchased, there are costs such as property management fees, property taxes, association dues, landscaping fees and the opportunity costs of filling vacancies when there is tenant turnover. And this analysis neglects the hefty commission expenses, which generally run 5-6% and split between the buying and selling agent. Add all these costs up, and you can understand the dollars can become significant.

Concentration Risk: It’s perfectly fine to own a levered, cyclical asset in a broadly diversified portfolio for long-term investors, but owning $1.3 million of real estate in a $1.5 million total portfolio does not qualify as diversified. If a portfolio is real estate heavy, hopefully the real estate assets are at least diversified across geographies and real estate type (e.g., residential / commercial / multi-family / industrial / retail mall / mortgages / etc).

Stocks Abhorred, Gold & Real Estate Adored

With the downdraft in the stock market that started in late August, a recent survey conducted by CNBC showed how increased volatility has caused wealthy investors to sour on the stock market. More specifically, the All-America Survey, conducted by Hart-McInturff, polled 800 wealthy Americans at the beginning of October. Unsurprisingly, many investors automatically correlate temporary weakness in stocks to a lagging economy. In fact, 32% of respondents believed the U.S. economy would get worse, a 6% increase from the last poll in June, and the highest level of economic pessimism since the government shutdown in 2013 (as it turned out, this was a very good time to buy stocks). These gloom and doom views manifested themselves in skeptical views of stocks as well. Overall, 46% of the public felt it is a bad time to invest in stocks, representing a 12% gain from the last survey.

With investor appetites tainted for stocks, hunger for real state has risen. Actually, real estate was the top investment choice by a large margin, selected by 39% percent of the investors polled. Real estate has steadily gained in popularity since the depths of the recession in 2008. Jockeying for second place have been stocks and gold with the shiny metal edging out stocks by a score of 25% to 21%, respectively.

Successful long-term investors like Warren Buffett understand the best returns are earned by going against the grain. As Buffett said, “Be fearful when others are greedy and greedy when others are fearful,” and we know stock investors are fearful. Along those same lines, Bill Miller, the man who beat the S&P 500 index for 15 consecutive years (1991 – 2005), believes now is a perfect time to buy stocks. Investing in real estate is not a bad idea in the context of a diversified portfolio, but investors should not forget the fallibility of tangibility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including SPY, but at the time of publishing, SCM had no direct position in Z, RWR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Building Your All-Star NBA Portfolio

Image by © Royalty-Free/Corbis

You may or may not care, but the NBA (National Basketball Association) playoffs are in full swing. If you were an owner/manager of an NBA team, you probably wouldn’t pick me as a starting player on your roster – and if you did, we would need to sit down and talk. I played high school basketball (“played” is a loose term) in my youth, and even played in my early 40s against other over-aged veterans with knee braces, goggles, and headbands. Once my injuries began to pile up and my playing time was minimized by the spry, millennial team members, I knew it was time to retire and hang up my jockstrap.

The great thing about your investments is that you can create an All-Star NBA portfolio without the necessity of a salary market cap or billions of dollars like Mark Cuban. You can actually put the greatest professional players in the world (stocks/bonds) into your portfolio whether you invest $1,000 or $10,000,000. Sure, transactions costs can eat away at the smaller portfolios, but if investors are correctly managing their funds over years, and not months, then virtually everyone can create a cost-efficient elite team of stocks, bonds, and alternatives.

Now that we’ve established that anyone can create a championship caliber portfolio, the question then becomes, how does an owner go about selecting his/her team’s players? It may sound like a cliché, but diversification is paramount. Although centers Tim Duncan, Dwight Howard, Chris Bosh, Marc Gasol, and DeAndre Jordan may get a lot of rebounds for your team, it wouldn’t make sense to have those five starting centers on your team. The same principle applies to your investment portfolio.

Generally speaking, the best policy for investors is to establish exposure to a broad set of asset classes customized to your time horizon, risk tolerance, objectives, and constraints. In other words, it is prudent to have exposure to not only stocks and bonds, but other areas like real estate, commodities, alternatives, and emerging markets. Everybody has their own unique situation, and with interest rates and valuations continually changing, it makes sense that asset allocations across all individuals will be very diverse.

In basketball terms, the sizes and types of guards, forwards, and centers will be dependent on the objectives of the team’s owners/managers. For example, it is very logical to have Stephen Curry (see great video) as the starting guard for the fast-paced, highest scoring NBA team, Golden State Warriors but Curry would not be ideally suited for the slow, grind-em-up offense of the Utah Jazz (one of the lowest scoring teams in the NBA).

In order to build a consistent winning percentage for your portfolio, you need to have a systematic, disciplined process of choosing your all-star-team, which can’t just consist of picking the hottest player of the day. Not only could it be too expensive, the consequences of over-concentrating your portfolio with an expensive position can be painful….just ask Los Angeles Laker fans how they feel about overpaying for Kobe Bryant’s $23.5 million 2014-2015 salary. Investors who chased the overpriced tech sector in the late 1990s, with stock prices trading at over 100 times trailing 12-month earnings, understand how painful losses can be in the subsequent “bubble” burst.

Having a strong bench of players is crucial as well. This requires a research process that can prioritize opportunities based on quantitative and fundamental processes (at Sidoxia we use our SHGR model). Sometimes your starters get injured, fatigued, or bought out by a competitor. Interest rates, valuations, exchange rates, earnings growth rates and other economic factors are continually fluctuating, so having a bench of suitable investment ideas is critical for different financial environments.

Beating the market is a challenging endeavor, not only for individuals, but also for professionals. If you don’t believe me, then check out what Dalbar had to say about this subject in its annual report entitled, Quantitative Analysis of Investor Behavior:

Dalbar found that in 2014, the average investor in a stock mutual fund underperformed the S&P 500 by a margin of 8.19 percent. Fixed-income investors underperformed the Barclays Aggregate Bond Index by a margin of 4.81 percent.

Ouch! If you want to generate winning returns matching the likes of the 1,000-win club, which includes Gregg Popovich, Phil Jackson, and Pat Riley then you need to avoid some of the most common investor mistakes (see also 10 Ways to Destroy Your Portfolio). Chasing performance, ignoring diversification, emotionally reacting to news headlines, paying high fees, and over-trading are sure fire ways to get technical fouls and ejected from the investment game. Avoiding these mistakes and following a systematic, objective process will make you and your investment portfolio a successful all-star.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

March Madness – Dividend Grandness & Volatility Blandness

March Madness has arrived once again. This NCAA basketball event, which has been around since 1939, begins with a selection committee choosing the top 68 teams in the country. These teams are matched up against each other through a single-elimination tournament until a national champion is throned. The stock market does not have a selection committee that picks teams from conferences like the SEC, Big East, Pac-12, and ACC, but rather millions of investors select the best investments from asset classes like stocks, bonds, real estate, commodities, venture capital, and private equity.

In the investment world, there are no win-loss records, but rather there are risk-return profiles. Investors generally migrate towards the asset classes where they find the optimal trade-off between risk and return. Speculators, day-traders, and momentum traders may define risk differently, but regardless, over the long-run, capital goes where it is treated best. And over the last six years, the U.S. stock market hasn’t been a bad place to be (the S&P 500 has about tripled).

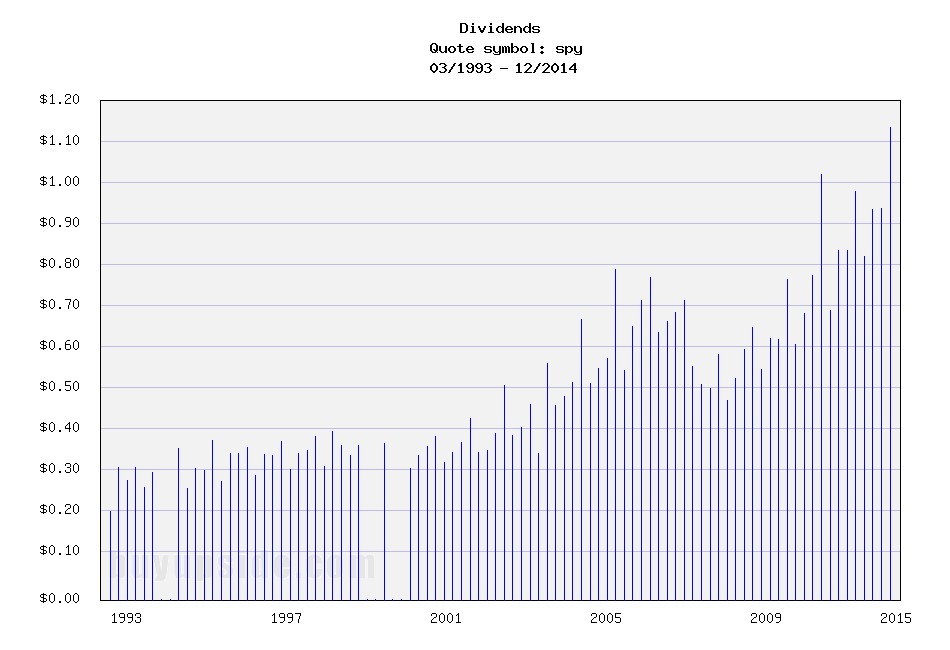

Why such outperformance in stocks? Besides a dynamic earnings recovery from the 2008-2009 financial crisis, another major factor has been the near-0% interest rate environment. When investors are earning near nothing in their bank and savings accounts, it is perfectly rational for savers to look for riskier options, if they are compensated for that risk. In addition to loose central bank and quantitative easing policies fueling demand for stocks, rising dividends have increased the attractiveness of the stock market. In fact, as you can see from the chart below, dividends have about doubled from 2008-2009 and about tripled from the year 2000.

Source: Buy Upside

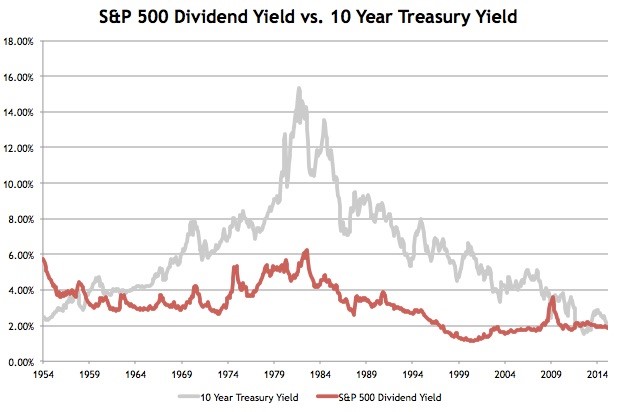

Stock prices have moved higher in concert with rising dividends, which, as you can see from the chart below, has kept the dividend yield flat at around 2% over the last few years. Treasury bond yields, on the other hand, have been on steady declining trend for the last 35 years. So, while coupons on newly issued bonds have been declining for virtually the last three and a half decades, stock dividends have been on a steadily upward moving rampage, excluding recessions (up +13% in the most recent reported period).

Source: Avondale Asset Management

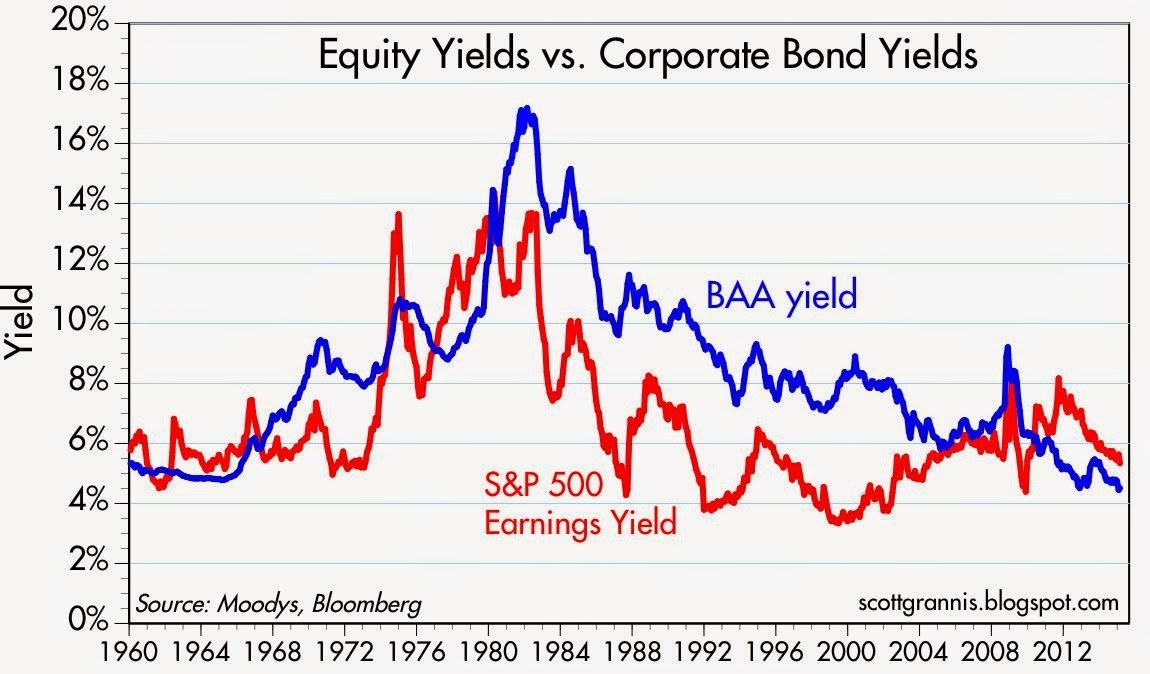

Declining interest rates have made stocks look attractive relative to investment grade corporate bonds too as evidenced by the chart below. As you can see, over the last half-century, corporate bond yields have predominantly offered higher income yields than the earnings yield on stocks – that is not the case today.

Source: Calafia Beach Pundit

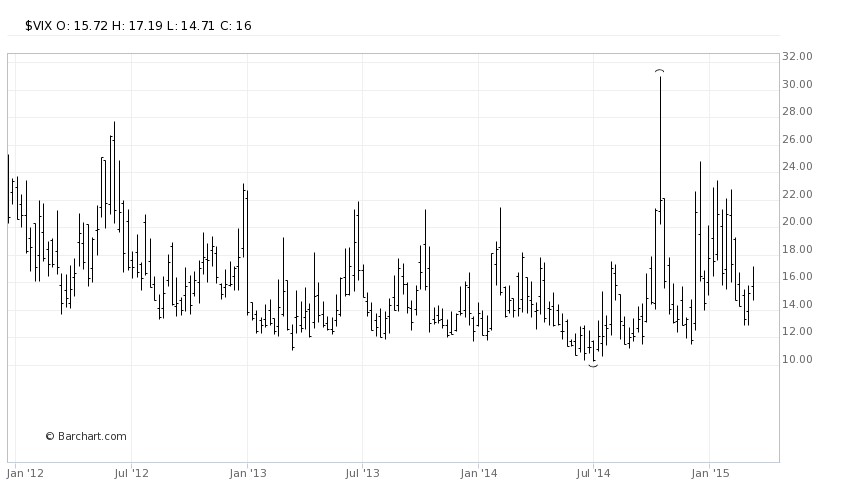

What does all this stock dividend, earnings yield stuff mean? In the grand scheme of things, income starving Baby Boomers and retirees are slowly realizing that stocks in general stack up favorably in an environment in which interest payments are going down and dividend payments are going up. One of the areas highlighting the underlying demand for stocks is the Volatility Index (VIX) – a.k.a., the “Fear Gauge.” Despite Greece, Russia, ISIS, the Fed, and the Dollar dominating the headlines, the hunger for yield and growth in a declining interest rate environment is cushioning the blow during these heightened periods of volatility (see also A Series of Unfortunate Events).

Since the end of 2011, the monthly close of the VIX has stayed above its historical average of approximately 20 only two times (see chart below). In other words, over that timeframe, the VIX has remained below average about 95% of the time. When the VIX has spiked above 20, generally it has only been for brief periods, until cooler heads prevail and bargain hunters come in to buy depressed stock bargains.

Source: Barchart

I’m not naïve enough to believe the bull market in stocks will last forever, but as long as interest rates don’t spike up and/or corporate earnings crater, underlying demand for yield should provide a floor for stocks during heightened periods of volatility. We may be in the midst of March Madness but volatility blandness is showing us that investors are paying attention to dividend grandness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing, Housing, and Speculating

We all know there was a lot of speculation going on in the housing market during 2005-2007 as risk-loving adventurists loaded up on NINJA loans (No Income, No Job, and No Assets) and subprime CDS (Credit Default Swap) securities. But there is a different kind of speculation going on now, and it isn’t tied directly to housing. Instead of buying a house with no down payment and a no interest loan, speculators are leaping into other hazardous areas of danger. Like a frog jumping from lily pad to lily pad, speculators are now hopping around onto money-chasing industries, including biotech, social media, Bitcoin, and alternative energy.

As French novelist Jean-Baptise Alphonse Karr noted, “The more things change, the more they stay the same.” Irrespective of the painful consequences of the bubble-bursting aftermaths, human behavior and psychology addictively succumb to the ever-seductive emotion of greed. Over the last 15 years, massive fortunes have been gained and lost while chasing frothy financial dreams in areas like technology, housing, and gold.

Most get-rich-quick dream chasers have no idea of how to invest in or value a stock, but they sure know a good story when they hear one. Chasing top performing stocks is lot like jumping off a bridge – anyone can do it, and it feels exhilarating until you hit the ground. However, there is a better way to create wealth. Despite rampant speculation, most individuals understand the principles behind buying a house, which if applied to stocks, can make you a superior investor, and assist you in avoiding dangerous, speculative investments.

Here are some valuable housing insights to improve your stock buying:

#1.) Price is the Almighty Variable: Successful real estate investors don’t make their fortunes by chasing properties that double or triple in value. Buying a rusty tool shed for $1 million makes about as much sense as Facebook paying $19 billion (1,000 x’s the estimated 2013 annual revenues) for a money-losing company, WhatsApp. Better to buy real estate when there is blood in the street. Like the stock market, housing is cyclical. Many traders believe that price patterns are more important than the actual price. If squiggly, technical price moving averages (see Technical Analysis article) make so much money for stock-renting speculators, then how come day traders haven’t used their same crossing-lines and Point & Figure software in the housing market? Yes, it’s true that the real estate transactions costs and illiquidity can be costly for real estate buyers, but 6% load fees, lockup periods, 20% hedge fund fees, and 9% margin rates haven’t stopped stock speculators either.

#2). Cash is King: It doesn’t take a genius to purchase a rental property – I know because practically half the people I know in Southern California own rental properties. For example, if I buy a rental property for $1 million cash, is it a good purchase? Well, it depends on how much after-tax cash I can collect by renting it out? If I can only net $3,000 per month (3.6% annualized return), and be responsible for replacing roofs, fixing toilets, and evicting tenants, then perhaps I would be better off by collecting 6.5% from a low-cost, tax-efficient exchange traded real estate fund, without having to suffer from all the headaches that physical real estate investing brings. Forecasting future asset price appreciation is tougher, but the point is, understanding the underlying cash flow dynamics of a company is just as important as it is for housing purchases.

#3). Debt/Leverage Cuts in Both Directions: Adding debt (or leverage) to a housing or stock investment can be fantastic if prices go up, and disastrous if prices go down. Putting a 20% down payment on a $1 million house works out wonderfully, if the price of the house increases to $1.2 million. My $200,000 down payment is now worth $400,000, or up +100%. The same math works in reverse. If the price of the home drops to $800,000, then my $200,000 down payment is now worth $0, or down -100% (ouch). Margin debt on an equity brokerage account works in a similar fashion, but usually a 50% down payment is needed (less risky than real estate). That’s why I always chuckle when many real estate investors tell me they steer clear of stocks because they are “too risky”.

#4). Growth Matters: If you buy a home for $1 million, is it likely to be worth more if you add a kitchen, tennis court, swimming pull, third floor, and putting green? In short, the answer is yes. The same principle applies to stocks. All else equal, if a company based in Los Angeles, establishes new offices in New York, London, Beijing, and Rio de Janeiro, and then acquires a profitable competitor at a discounted price, chances are the company will be much more valuable after the additions. The key concept here is that asset values are not static. Asset valuations are impacted in both directions, whether we are talking about positive growth opportunities or negative disruptions.

Overall, speculatively chasing performance is tempting, but if you don’t want your financial foundation to crumble, then build your successful investment future by sticking to the fundamentals and financial basics.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct discretionary position in FB, Bitcoin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Organizing Your Investment Basket

With the Easter bunny relaxing after a busy holiday, kids from all over are given the task of organizing the candy and money collected during their hunts. Investors are also constantly reminded that their portfolio eggs should not be solely placed in one basket either. Instead, investors are told to diversify their investments across a whole host of asset classes, geographies, styles, and sizes. In other words, this means investors should be spreading their money across commodity, real estate, international, emerging market, value, growth, small-cap, and large-cap investments. As Jason Zweig, journalist from a the Wall Street Journal points out, much of the diversification benefits can be achieved with relatively small change in the position count of a portfolio:

“As many studies have shown, at least 40% of the variability in returns can be reduced by moving from a single company to 20. Once a portfolio contains 20 or 30 stocks, adding more does little to damp the fluctuations in wealth over time.”

But wait. Going from one banking stock to 20 banking stocks is not going to provide you with the proper diversification you want or need. Rather, what is as important as investing across asset class, geography, style, and size, is to follow the individual stock strategies of guru Peter Lynch. In order to put his performance into perspective, Lynch’s Fidelity Magellan fund averaged +29% per year from 1977 – 1990 – almost doubling the return of the S&P 500 index for that period.

More specifically, to achieve these heroic returns, Lynch divided the stocks in his fund into the following categories:

Slow Growers: This group of stocks wasn’t Lynch’s favorite because these companies typically operate in mature industries with limited expansion opportunities. For these single-digit EPS growers, Lynch focused more on identifying high dividend-paying stocks that were trading at attractive valuations. In particular, he paid attention to a dividend-adjusted PEG ratio (Price-to-Earnings Growth). A utility company would be an example of a “Slow Grower.”

Stalwarts: These are large established companies that still have the ability to achieve +10% to +12% annual earnings growth regardless of the economic cycle. Lynch liked these stocks especially during recessions and downturns. Valuations are still very important for Stalwarts, and many of them pay dividends. An investor may not realize a “home run” with respect to returns, but a +30% to 50% return over a few years is not out of the question, if selected correctly. Former examples of “Stalwarts” include Coca Cola (KO) and Procter & Gamble (PG).

Fast Growers: This categorization applies to small aggressive firms averaging about +20% to +25% annual earnings growth. While “Fast Growers” offer the most price appreciation potential, these stocks also offer the most risk, especially once growth/momentum slows. If timed correctly, as Lynch adeptly achieved, these stocks can increase multi-fold in value. The great thing about these “Fast Growers” is they don’t have to reside in fast growth industries. Lynch actually preferred market share gainers in legacy industries.

Cyclicals: These companies tend to see their sales and profits rise and fall with the overall economic cycle. The hyper-sensitivity to economic fluctuations makes the timing on these stocks extremely tricky, leading to losses and tears – especially if you get in too late or get out too late. To emphasize his point, Lynch states, “Cyclicals are like blackjack: stay in the game too long and it’s bound to take all your profit.” The other mistake inexperienced investors make is mistaking a “Cyclical” company as a “Stalwart” at the peak of a cycle. Examples of cyclical industries include airline, auto, steel, travel, and chemical industries.

Turnarounds: Lynch calls these stocks, “No Growers,” and they primarily of consist of situations like bail-outs, spin-offs, and restructurings. Unlike cyclical stocks, “Turnarounds” are usually least sensitive to the overall market. Even though these stocks are beaten down or depressed, they are enormously risky. Chyrysler, during the 1980s, was an example of a favorable Lynch turnaround.

Asset Plays: Overlooked or underappreciated assets such as real estate, oil reserves, patented drugs, and/or cash on the balance sheet are all examples of “Asset Plays” that Lynch would consider. Patience is paramount with these types of investments because it may take considerable time for the market to recognize such concealed assets.

Worth noting is that not all stocks remain in the same Lynch category. Apple Inc. (AAPL) is an example of a “Fast Grower” that has migrated to “Stalwart” or “Slow Grower” status, therefore items such as valuation and capital deployment (dividends and share buyback) become more important.

Peter Lynch’s heroic track record speaks for itself. Traditional diversification methods of spreading your eggs across various asset class baskets is useful, but this approach can be enhanced by identifying worthy candidates across Lynch’s six specific stock categories. Hunting for these winners is something Lynch and the Easter bunny could both agree upon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct position in KO, PG, Chrysler, Fidelity Magellan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Damned if You Do, and More Damned if You Don’t

Source: Photobucket

In the stock market you are damned if you do, and more damned if you don’t.

There are a million reasons why the market should or can go down, and the press, media, and bears come out with creative explanations every day. The “Flash Crash,” debt ceiling debate, credit downgrades, elections, and fiscal cliff were all credible events supposed to permanently crater the market. Now we have higher taxes (capital gains, income, and payroll), sequester spending cuts, and a nagging recession in Europe. What’s more, the pessimists point to the unsustainable nature of elevated corporate profit margins, and use the ludicrous Robert Shiller 10-year Price-Earnings ratio as evidence of an expensive market (see also Foggy Rearview Mirror). If an apple sold for $10 ten days ago and $0.50 today, would you say, I am not buying an apple today because the 10-day average price is too high? If you followed Robert Shiller’s thinking, this logic would make sense.

Despite the barrage of daily concerns and excuses, the market continues to set new record highs and the S&P 500 is up by more than +130% since the 2009 lows – just a tad higher than the returns earned on cash, gold, and bonds (please note sarcasm). Cash has trickled into equities for the first few months of 2013 after years of outflows, but average investors have only moved from fear to skepticism (see also Investing with the Sentiment Pendulum ). With cash and bonds earning next to nothing; gold underperforming for years; and inflationary pressures eroding long-term purchasing power, the vice is only squeezing tighter on the worrywarts.

Are there legitimate reasons to worry? Certainly, and the opportunities are not what they used to be a few years ago (see also Missing the Pre-Party). Although an endangered species, long-term investors understand backwards looking economic news is useless. Or as Peter Lynch wisely stated, “If you spend 13 minutes a year on economics, you’ve wasted 10 minutes.” The fact remains that the market is up 70% of the time, on an annual basis, and has been a great place to beat inflation over time. It’s a tempting endeavor to avoid the down markets that occur 30% of the time, but those who try to time the market fail miserably over the long-run (see also Market Timing Treadmill).

Equity investors would be better served by looking at their investment portfolios like real estate. Homeowners implicitly know the value of their home changes on a daily basis, but there are no accurate, real-time quotes to reference your home value on a minute by minute basis, as you can with stocks. Most property owners know that real estate is a cyclical asset class that is not impacted by daily headlines, and if purchased at a reasonable price, will generally go up in value over many years. Unfortunately, for many average investors, equity portfolios are treated more like gambling bets in Vegas, and get continually traded based on gut instincts.

Volatility is at six-year lows, and investors are getting less uncomfortable with owning stocks. Although everybody and their mother has been waiting for a pullback (myself included), don’t get too myopically focused. For the vast majority of investors, who should have more than a ten year time horizon, you should understand that volatility is normal and recessions will cause stocks to gown significantly, twice every ten years on average. If you are a long-term investor, like you should be, and you understand these dynamics, then you will also understand that you will be more damned if you don’t invest in equities as part of a diversified portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Getting & Staying Rich 101

Fred J. Young worked 27 years as a professional money manager and investment counselor in the trust department at Harris Bank in Chicago. While working there he learned a few things about wealth accumulation and preservation, which he outlines in his book How to Get Rich and Stay Rich.

There is more than one way to skin a cat, and when it comes to getting rich, Young describes the only three ways of getting loaded:

1.) Inherit It: Using this method on the path to richness generally doesn’t take a lot of blood, sweat, and tears (perhaps a little brown-nosing wouldn’t hurt), but young freely admits you can skip his book if you are fortunate enough to garner boatloads of cash through your ancestry.

2.) Marry It: This approach to wealth accumulation can require a bit more effort than method number one. However, Young explains that if the Good Lord intended you to find your lifetime lover through destiny, then if your soul-mate has a lot of dough Young advises, “You [should] graciously accept the situation. Don’t fight it.”

3.) Spend < Earn: Normally this avenue to champagne and caviar requires the most effort. How does one execute option number three? “You spend less than you earn and invest the difference in something you think will increase in value and make you rich,” simply states Young. Sounds straightforward, but what does one invest their excess cash in? Young succinctly lists the customary investment tools of choice for wealth creation:

- Real estate

- Own their own business

- Common stocks

- Savings accounts (thanks to the magic of compound interest rates) – see also Penny Saved is Billions Earned

Rich Luck

If faced with choosing between good luck and good judgment, here is Fred Young’s response:

“You should take good luck. Good luck, by definition, denotes success. Good judgment can still go wrong.”

Like many endeavors, it’s good to have some of both (good luck and good judgment).

The Role of Courage

Courage is especially important when it comes to equity investing because buying stocks includes a very counterintuitive behavioral aspect that requires courage. Following the herd of average investors and buying stocks at new highs is easy and does not require a lot of courage. Young describes the various types of courage required for successful investing:

“The courage to buy when others are selling; the courage to buy when stocks are hitting new lows; the courage to buy when the economy looks bad; courage to buy at the bottom…The times when the gloom was the thickest invariably turned out to have been the best times to buy stocks.”

Keeping the Cash

Becoming rich is only half the challenge. In many cases staying rich can be just as difficult as accumulating the wealth. Young points out the intolerable pain caused by transitioning from wealth to poverty. What is Young’s solution to this tricky problem? Seek professional help. The risks undertaken to build wealth still exist when you are rich, and those same risks have the capability of tearing financial security away.

There are three paths to riches according to Fred Young (inheritance, marriage, and prudent investing). Some of these directions leading to mega-money require more effort than others, but if you are lucky enough to have deep pockets of riches, make sure you have the discipline and focus necessary to maintain that wealth – those deep pockets could have a hole.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Your Portfolio’s Silent Killer

Shhh, if you listen closely enough, you may hear the sound of your portfolio disintegrating away due to the quiet killer…inflation. Inflation is especially worrisome with what we’ve seen happening with commodity prices and the drastic fiscal challenges our country faces. Quantitative Easing (read Flying to the Moon) has only added fuel to the inflation fear flames.

Whether you’re a conspiracy theorist who believes the government inflation data is cooked, or you are a Baby Boomer just looking to secure your retirement, it doesn’t take a genius to figure out that movies, pair of jeans, a tank of gas, concert tickets, or healthcare premiums are all going up in price (See also Bacon and Oreo Future).

Inflation starting to heat up. Source: IMF/Bloomberg via Financial Times

Companies are currently churning out quarterly results in volume and seeing the impact from commodity prices, whether you are McDonald’s Corp. (MCD) facing rising beef prices or luxury handbag maker Coach Inc. (COH) dealing with escalating leather costs, margins are getting crimped. Investors, especially those on fixed income streams, are experiencing the same pain as these corporations, but the problem is much worse. Unlike a market share leading company that can pass on price increases onto its customers, an investor with piles of cash, and low yielding CDs (Certificates of Deposit), and bonds runs the risk of getting eaten alive. Baby Boomers are beginning to reach retirement age in mass volume. Life spans are extending, and this demographic pool of individuals will become ever-large consumers of costlier and costlier healthcare services. If investments are not prudently managed, Baby Boomers will see their nest eggs evaporate, and be forced to work as Wal-Mart (WMT) greeters into their 80s…not that there’s anything wrong with that.

Every day investors are bombarded with a hundred different scary headlines on why the economy will collapse or the world will end. Most of these sensationalist scare tactics distort the truth and overstate reality. What is understated is what Charles Ellis (see Winning the Loser’s Game) calls a “corrosive power”:

“Over the long run, inflation is the major problem for investors, not the attention-getting daily or cyclical changes in securities prices that most investors fret about. The corrosive power of inflation is truly daunting: At 3 percent inflation – which most people accept as ‘normal’ – the purchasing power of your money is cut in half in 24 years. At 5 percent inflation, the purchasing power of your money is cut in half in less than 15 years – and cut in half again in 15 years to just one-quarter.”

In order to bolster his case, Ellis cites the following period:

“From 1977 to 1982, the inflation-adjusted Dow Jones Industrial Average took a five-year loss of 63 percent…In the 15 years from the late 1960s to the early 1980s the unweighted stock market, adjusted for inflation, plunged by about 80 percent. As a result, the decade of the 1970s was actually worse for investors than the decade of the 1930s.”

Solutions – How to Beat Inflation

Although the gold bugs would have you believe it, we are not resigned to live in a world with worthless money, which only has a useful purpose as toilet paper. There are ways to protect your portfolio, if you are properly invested. Here are some strategies to consider:

- TIPS (Treasury Inflation Protection Securities): These government-guaranteed tools are a useful way to protect yourself against rising inflation (see Drowning TIPS).

- Equities (including real estate): Bond issuers do not generally call up there investors and say, “You are such a great investor, so we have decided to increase your interest payments.” However, many publicly traded stocks do exactly that. Wal-Mart Stores (WMT) is an example of such a company that has increased its dividend for 37 consecutive years. As alluded to earlier, stocks are unique in that they allow inflationary pressures placed on operating profits to be relieved somewhat by the ability to pass on price increases to customers.

- Commodities: Whether you are talking about petroleum products, precious metals (those with a commercial purpose), or agricultural goods, commodities in general act as a great inflationary hedge. Another reason that commodities broadly perform better in an inflationary environment is because the U.S. dollar can often depreciate, which commonly increases the value of commodities.

- Short Duration Bonds: Rising rates are usually tied to escalating inflation, therefore investors would be best served by reducing maturity length and increasing coupon.

There are other ways of battling the inflation problem, but number one is saving and investing across a broadly diversified portfolio. If you want to secure and grow your nest egg, you need to use the silent power of compounding (see Penny Saved is Billion Earned) to combat the silent killer of inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, TIP, equities, commodities, and short duration bonds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}