Posts tagged ‘rally’

Even Winning Teams Occasionally Lose

The stock market has been a winning team for years, generating outsized returns for investors. But so far this year, the winning streak appears to be coming to an end. For 2022, the S&P 500 index is down -21%, including -8% last month. However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). In recent years, the U.S. stock market has been winning by a large margin (2019: +29%, 2020: +16%, 2021: +27%) and a significant contributor to the team’s win streak has been the Federal Reserve, or the designated hitter (DH).

Jerome Powell, the Fed Chair, has been a very effective clean-up hitter for the stock market, not only leading the stock market team to victories, but also appreciation in almost all global-risk asset classes. By keeping interest rates (the Federal Funds Rate target) essentially at 0% over the last few years, since the initial COVID pandemic outbreak, many investors are blaming Mr. Powell for elevated inflation rates. If that were truly the case, then we probably wouldn’t see the ubiquitous inflation globally, as we do now. Just as you would expect with any baseball team, any single player does not deserve all the credit for wins, nor should any single player receive all the blame for losses – the same principle applies to the Federal Reserve.

Regardless, the stock market’s best hitter is now injured. In addition to pushing interest rates higher, the Fed is hurting the team through its monetary policy of quantitative tightening or QT (i.e., selling bonds off the Fed’s balance sheet). Theoretically, QT should cause interest rates to move higher, all else equal, and thereby slow down growth in the economy, and help tame out-of-control inflation.

The stock market was also thrown a curve ball when Russia invaded Ukraine, which added gasoline to an already flaming inflation fire. Globally, consumers and businesses have witnessed exploding oil/gasoline prices, in addition to escalated food prices caused by a lack of grain and other commodity exports out of Ukraine.

Lastly, a wild pitch has been thrown at the U.S. stock market by China with its zero-COVID policy, which has essentially shut down the world’s 2nd largest economy and further delayed the full reopening of the global economic game. As a result of China’s hardline lockdown stance, global supply chain disruptions have intensified and import prices have mushroomed higher.

Although this all sounds like horrible news, in the game of investing, nobody wins all the time. As history teaches us, the stock market is generally up around 70% of the time. It just happens to be that we are in the middle of a 30% losing period.

Bad News Does Not Mean Bad Stock Market

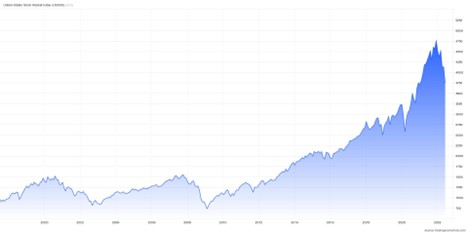

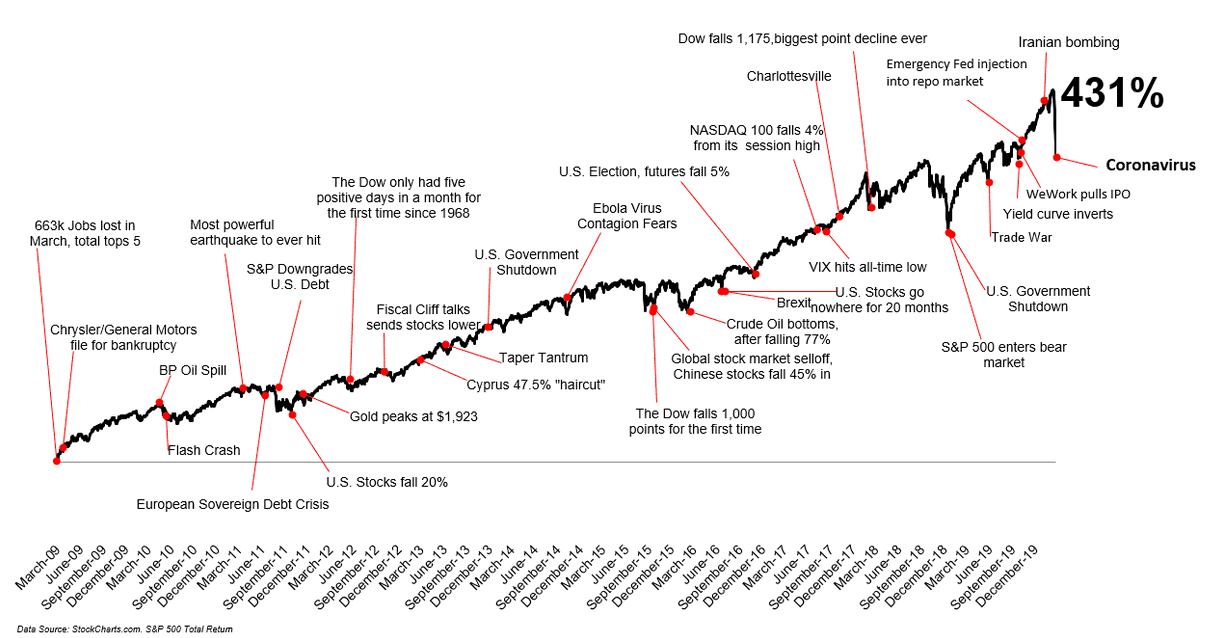

The majority of economists, strategists, and talking heads on television are forecasting a recession in our economy, either this year or next. This should come as no surprise to any experienced investor, as history teaches us that recessions occur on average about twice every decade. Long-term investors also understand that stock prices do not always just go up on good news and down on bad news. Stocks can go down on good news, and up on bad news. In fact, over the last 13 years, since the bottom of the 2008-2009 financial crisis, the stock market has increased about six-fold (even after this year’s -21% correction) in the face of some horrendously scary headlines (also see chart below):

· Ukraine-Russia

· COVID

· Elections / Capitol Insurrection

· Exit from Afghanistan

· Impeachment

· China Trade War & Tariffs

· Inverted Yield Curves

· N. Korea Missile Launches

· Brexit

· ISIS in Iraq

· Ebola

· Russia Takeover of Crimea

· Double Dip Recession Fears

· Eurozone Debt Crisis

S&P 500 Index (1997 – 2022)

Despite the recent headwinds in the stock market, not all the news is bad. Here are some tailwinds:

- PROFITS: Corporate profits remain at or near record levels.

- INFLATION: Inflation appears to be cooling as evidenced by declining commodity prices (TR Commodities CRB Index).

CRB Commodities Index (2022)

- PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., stock prices are on sale).

- SENTIMENT: Sentiment remains fearful – a contrarian buy indicator (an elevated VIX – Volatility Index can signal buying opportunities). As Warren Buffett says, “Be fearful when others are greedy, and greedy when others are fearful.”

VIX – Volatility Index (2021 – 2022)

Even though the U.S. stock market has been a long-term winner, investors have been betting against the winning team by selling stocks. As mentioned earlier, recessions, if we get one, are common and nothing new. The -21% correction in stock prices is already factoring in a mild recession, so we have already suffered near-maximum pain. Could prices go lower? Certainly. But should you quit a 26-mile marathon at mile 25 because the pain is too intense? In most instances, the answer should absolutely be “no” (see also No Pain, No Gain). Eventually, the Fed will stop raising interest rates, inflation will cool, the Russia-Ukraine war will be resolved, and solid growth will return. While many people are betting the stock market will lose this year, many long-term investors recognize betting on stock market success is a winning strategy over the long-run, especially when prices are on sale.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BRKA/B or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Return to Rationality?

As the worst pandemic in more than a generation is winding down in the U.S., people are readjusting their personal lives and investing worlds as they transition from ridiculousness to rationality. After many months of non-stop lockdowns, social distancing, hand-sanitizers, mask-wearing, and vaccines, Americans feel like caged tigers ready to roam back into the wild. An incredible amount of pent-up demand is just now being unleashed not only by consumers, but also by businesses and the economy overall. This reality was also felt in the stock market as the Dow Jones Industrial Average powered ahead another 654 points last month (+1.9%) to a new record level (34,529) and the S&P 500 also closed at a new monthly high (+0.6% to 4,204). For the year, the bull market remains intact with the Dow gaining almost 4,000 points (+12.8%), while the S&P 500 has also registered a respectable +11.9% return.

The story was different last year. The economy and stock market temporarily fell off a cliff and came to a grinding halt in the first quarter of 2020. However, with broad distribution of the vaccines and antibodies gained by the previously infected, herd immunity has effectively been reached. As a result, the U.S. COVID-19 pandemic has essentially come to an end for now and stock prices have continued their upward surge since last March.

Insanity to Sanity?

With the help of the Federal Reserve keeping interest rates at near-0% levels, coupled with trillions of dollars in stimulus and proposed infrastructure spending, corporate profits have been racing ahead. All this free money has pushed speculation into areas such as cryptocurrencies (i.e., Bitcoin, Dogecoin, Ethereum), SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (GameStop Corp, AMC Entertainment), and highly valued, money-losing companies (e.g., Spotify, Uber, Snowflake, Palantir Technologies, Lyft, Peloton, and others). The good news, at least in the short-term, is that some of these areas of insanity have gone from stratospheric levels to just nosebleed heights. Take for example, Cathie Wood’s ARK Innovation Fund (ARKK) that invests in pricey stocks averaging a 91x price-earnings ratio, which exceeds 4x’s the valuation of the average S&P 500 stock. The ARK exchange traded fund that touts investments in buzzword technologies like artificial intelligence, machine learning, and cryptocurrencies rocketed +149% last year in the middle of a pandemic, but is down -10.0% this year. The Grayscale Bitcoin Trust fund (GBTC) that skyrocketed +291% in 2020 has fallen -5.6% in 2021 and -48.1% from its peak. What’s more, after climbing by more than +50% in less than four months, the Defiance NextGen SPAC fund (SPAK) has declined by -28.9% from its apex just a few months ago in February. You can see the dramatic 2021 underperformance in these areas in the chart below.

Inflation Rearing its Ugly Head?

The economic resurgence, weaker value of the U.S. dollar, and rising stock prices have pushed up inflation in commodities such as corn, gasoline, lumber, automobiles, housing, and a whole host of other goods (see chart below). Whether this phenomenon is “transitory” in nature, as Federal Reserve Chairman Jerome Powell likes to describe this trend, or if this is the beginning of a longer phase of continued rising prices, the answer will be determined in the coming months. It’s clear the Federal Reserve has its hands full as it attempts to keep a lid on inflation and interest rates. The Fed’s success, or lack thereof, will have significant ramifications for all financial markets, and also have meaningful consequences for retirees looking to survive on fixed income budgets.

As we have worked our way through this pandemic, all Americans and investors look to change their routines from an environment of irrationality to rationality, and insanity to sanity. Although the bull market remains alive and well in the stock market, inflation, interest rates, and speculative areas like cryptocurrencies, SPACs, meme-stocks, and nosebleed-priced stocks remain areas of caution. Stick to a disciplined and diversified investment approach that incorporates valuation into the process or contact an experienced advisor like Sidoxia Capital Management to assist you through these volatile times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, SPOT, UBER, SNOW, PLTR, LYFT, PTON, GBTC, SPAK, ARKK or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Market Drops as GameStop Pops

The stock market started with a bang this year with the S&P 500 index at first climbing +3% in January before ending with a whimper and a monthly decline of -1%. This performance followed a strong finish to a wild 2020 presidential election year (the S&P 500 rose +16%). There has been plenty of focus on the coronavirus health crisis and vaccine distribution (100 million doses in 100 days), along with debates over a $1.9 trillion proposed relief package by newly elected President Joe Biden, but there has been another story stealing attention in the financial market headlines…GameStop.

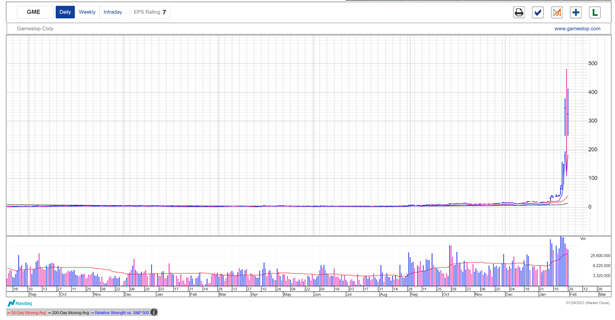

If a global pandemic and a populist attack on the Capitol were not enough for investors, the Reddit (WallStreetBets) and Robinhood revolution coordinated a mass attack on privileged hedge funds and short sellers by squeezing out-of-favor stocks like GameStop (Ticker: GME) to stratospheric levels (up +1,625% to $325/share in January alone) causing an estimated $20 billion of losses for many wealthy elites. To put the meteoric rise into perspective, before GameStop shares reached $325, the stock was valued below $20/share last month and has climbed more than 100x-fold from a low $2.57/share nine months ago (see chart below).

What Exactly Happened?

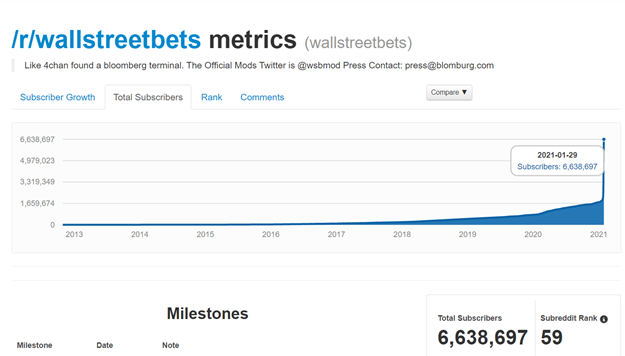

Well, millions of users on the social media platform Reddit banded together on a forum called “wallstreetbets” (see graphic below). WallStreetBets was established in 2012 and had approximately 1 million subscribers at the beginning of 2021 – today it has more than 7 million subscribers. Millions of these anti-establishment WallStreetBets followers effectively colluded together to inflate the share price of GameStop by ganging up on the many short sellers who were betting that GameStop share price would drop. In other words, Reddit-Robinhood buyer gains led to short seller losses. One hedge fund in particular, Melvin Capital, lost billions of dollars on its GameStop short bet and saw its fund performance decline by a whopping -53% in one month…ouch!

The Reddit WallStreetBets forum may have served as the match in this wildfire, but in order to trigger an inferno, a brokerage account is needed. A trading platform allows individual traders on Reddit to level the playing field against the hedge fund professionals and short sellers. The fuel for the GameStop detonation was Robinhood, a fintech (Financial Technology) brokerage firm founded in Silicon Valley in 2013 by two Stanford University graduates. The mission of the company is to “democratize finance for all.” But let’s not forget what Thomas Jefferson noted, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.” The Reddit-Robinhood mob certainly proved this point.

Although Robinhood was initially seen as a saint in the free trading revolution, eventually many of the brokerage company’s disciples became disenfranchised. Many users subsequently turned on the company and considered Robinhood a villain that was rigging the system when CEO Vlad Tenev halted the ability of its 13+ million users to buy GameStop shares.

Many traders came to the conclusion that Robinhood was working to save the perceived hedge fund bad guys by the firm temporarily terminating user purchases in GameStop stock. Mr. Tenev blamed regulatory capital requirements as a reason for disallowing Robinhood-ers to buy GameStop last week, which was a major contributing factor to why the stock price plummeted by -44% on January 28th. The following day, Robinhood partially reversed its stance and subsequently allowed minimal daily purchases of one share.

How Does Short Selling Work?

In the stock market, you can make gains by buying shares that go up in price, or you can make profits by short selling shares that go down in price. If you buy a stock, the most money you could lose is -100% of your original investment. For example, if you invest $1,000 into GameStop stock by buying 50 shares at $20 each, if the stock price goes to $0, the most the investor/trader could lose is 100% of their $1,000 original investment.

On the flip side, if you short a stock, the potential losses are limitless. For example, if you (or a hedge fund manager) shorts $1,000 of GameStop stock by selling 50 shares short at $20 each, if the stock price goes to $60, the short seller just loss -200% of their original investment [($20/shr – $60/shr) X 50 shares] = -$2,000. If GameStop goes to $100, the short seller loses -400%, and if GameStop price goes to $220, the short seller loses -1,000%. As you can see, the higher the price goes, there are infinite potential losses of the investor, trader, or hedge fund manager.

If a stock price continues to move higher, the only way for a short seller to stop the bleeding (i.e., close their short position or “bet”) is to buy shares. As a reminder, a buyer of stock closes their position by selling shares after they originally buy shares. A short seller closes their position by buying shares after they initially sell shares short. So again, if GameStop share price continues to move higher, the only way for GameStop short sellers to stop their losses is to buy more GameStop shares. This is the equivalent of pouring gasoline on a blazing fire because as millions of Reddit/Robinhood-ers are pushing GameStop’s share price higher almost every day, short selling hedge fund managers are left scrambling for the exits and forced to close their positions at even higher prices (i.e., larger losses).

What Does This All Mean?

Whether you are talking about speculation in Bitcoin, the rise of SPACs (Special Purpose Acquisition Companies), the increase in the number of IPOs (Initial Public Offerings), or the Reddit-Robinhood Revolution, risk appetite has been on the rise and long-term investors should proceed very cautiously. Just as many have experienced on trips to Las Vegas, big winnings can quickly turn to huge losses. Although it’s certainly fun to watch the individual Davids take down the hedge fund/short selling Goliaths, if the Reddit-Robinhood community gets too aggressive in its speculation, history shows us they will end up being the ones swimming in their tears or stoned to death.

If you need assistance navigating through all these land mines, please give us a call at Sidoxia Capital Management (949-258-4322) for a complimentary portfolio review.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

This Too Shall Pass

Ever since December 31st last year when China alerted the WHO (World Health Organization) about several cases of unusual pneumonia in Wuhan, a port city of 11 million people in the central Hubei province, the dark coronavirus (Covid-19) clouds began to form. Last week, the storm came rumbling through with a vengeance.

I have been investing for close to 30 years, so facing these temporary bouts of thunder and lightning is nothing new for me. Although the pace of this week’s -3,583 point drop in the Dow Jones Industrial Average was particularly noteworthy, we experienced a more severe -5,000 point correction a little more than a year ago due to China trade war concerns and our Federal Reserve increasing interest rates. What happened after that year-end 2018 drop? Stock prices skyrocketed more than +7,800 points (+36%) to a new record high on February 12th, just a few weeks ago. Over the long-run, stock prices have always eventually moved up to new record highs, but this week reminds us that volatility is a normal occurrence.

This week also reminds us that the best decisions made in life generally are not emotionally panicked ones. The same principle applies to investing. So rather than knee-jerk react to the F.U.D. (Fear, Uncertainty, Doubt), let’s take a look at some of the current facts as it relates to coronavirus (Covid-19):

- The number of deaths this season in the U.S. from the common flu: 18,000. The number of deaths in the U.S. from coronavirus: 2 individuals (both in WA with underlying health conditions).

- The number of new coronavirus cases in China is declining. Confirmed infections have fallen from more than 2,000 per day to a few hundred. People are going back to work and companies like Starbucks are re-opening their China stores for business.

- Coronavirus is relatively benign compared to other contagious pathogens. Roughly 98% of infected individuals fully recover, and deaths are limited to people with weakened immune systems, who in many cases are suffering from other illnesses.

- Previous viral outbreaks, which were significantly more fatal, were all contained, e.g., SARS (2003-04), MERS (2012), and Ebola (2014-16). In each instance, the stock market initially fell, and then subsequently fully recovered.

- Although the coronavirus has accelerated in areas outside of China, there are dozens of different companies currently developing a vaccine. If a working vaccine is discovered, a rebound could occur as fast as the drop.

- Governments and central banks are not sitting on their hands. Coordinated efforts are being instituted to curtail the spread of the virus and also provide liquidity to financial markets.

The actual death toll from the coronavirus is relatively small compared to other pandemics, catastrophes (e.g., 9/11), and wars. However, the hangover effect from the fear, uncertainty, and panic that can manifest in the days, weeks, and months after global events can last for some time. I expect the same to occur in the coming weeks and months as the drip of continued coronavirus headlines blankets social media and the news.

I don’t want to sugar coat the economic impact from a potential pandemic because quarantining 60 million people in China, instituting global travel bans, and closing areas of gathering has and will continue to have a material economic impact. Although history would indicate otherwise, it is certainly possible the current situation could worsen and lead to a global recession. Even if that were the case, I believe we are more likely closer to a bottom, than we are to a top, especially given how low interest rates are now. More specifically, we just hit an all-time record low yield of 1.13% on the 10-Year Treasury. In other words, putting money in the bank isn’t going to earn you much.

In summary, the current situation experienced this week is nothing new – we’ve lived through similar situations many times (see chart above). The short-run headlines can get more painful, but in the meantime, you can wash your hands and bathe in Purell. This too shall pass.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 2, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in SBUX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

January a Ball After Year-End Fall

Investors were cheerfully dancing last month after the stock market posted its best January in 30 years and the best monthly performance since October 2015 (see chart below). More specifically, the S&P 500 index started the year by catapulting +7.9% higher (the best January since 1987), and the Dow Jones Industrial Average climbed 1,672 points to 25,000, or +7.2%. But over the last few months there has been plenty of heartburn and volatility. The December so-called Santa Claus rally did not occur until a large pre-Christmas pullback. From the September record high, stocks temporarily fell about -20% before the recent jolly +15% post-Christmas rebound.

Source: FactSet via The Wall Street Journal

Although investors have been gleefully boogying on the short-run financial dance floor, there have been plenty of issues causing uncomfortable blisters. At the top of the list is China-U.S. trade. The world is eagerly watching the two largest global economic powerhouses as they continue to delicately dance through trade negotiations. Even though neither country has slipped or fallen since the 90-day trade truce, which began on December 1 in Buenos Aires, the stakes remain high. If an agreement is not reached by March 2, tariffs on imported Chinese goods would increase to 25% from 10% on $200 billion worth of Chinese goods, thereby raising prices for U.S. consumers and potentially leading to further retaliatory responses from Beijing.

When it comes to the subjects of intellectual property protection and forced technology transfers of American companies doing business in China, President Xi Jinping has been uncomfortably stepping on President Donald Trump’s toes. Nothing has been formally finalized, however Chinese officials have signaled they are willing to make some structural reforms relating to these thorny issues and have also expressed a willingness to narrow the trade deficit with our country by purchasing more of our exports. Besides procuring more American energy goods, the Chinese have also committed to buy 5,000,000 tons of our country’s soybeans to feed China’s hungry population of 1.4 billion people.

Reaching a trade settlement is important for both countries, especially in light of the slowing Chinese economy (see chart below) and the dissipating stimulus benefits of the 2018 U.S. tax cuts. Slowing growth in China has implications beyond our borders as witnessed by slowing growth in Europe as evidenced by protests we have seen in France and the contraction of German manufacturing (the first time in over four years). Failed Brexit talks of the U.K. potentially leaving the European Union could add fuel to the global slowdown fire if an agreement cannot be reached by the March 29th deadline in a couple months.

Source: Wind via The Wall Street Journal

While the temporary halt to the longest partial federal government shutdown in history (35 days) has brought some short-term relief to the 800,000 government workers/contractors who did not receive pay, the political standoff over border security may last longer than expected, which may further dampen U.S. economic activity and growth. Whether the hot-button issue of border wall funding is resolved by February 15th will determine if another shutdown is in the cards.

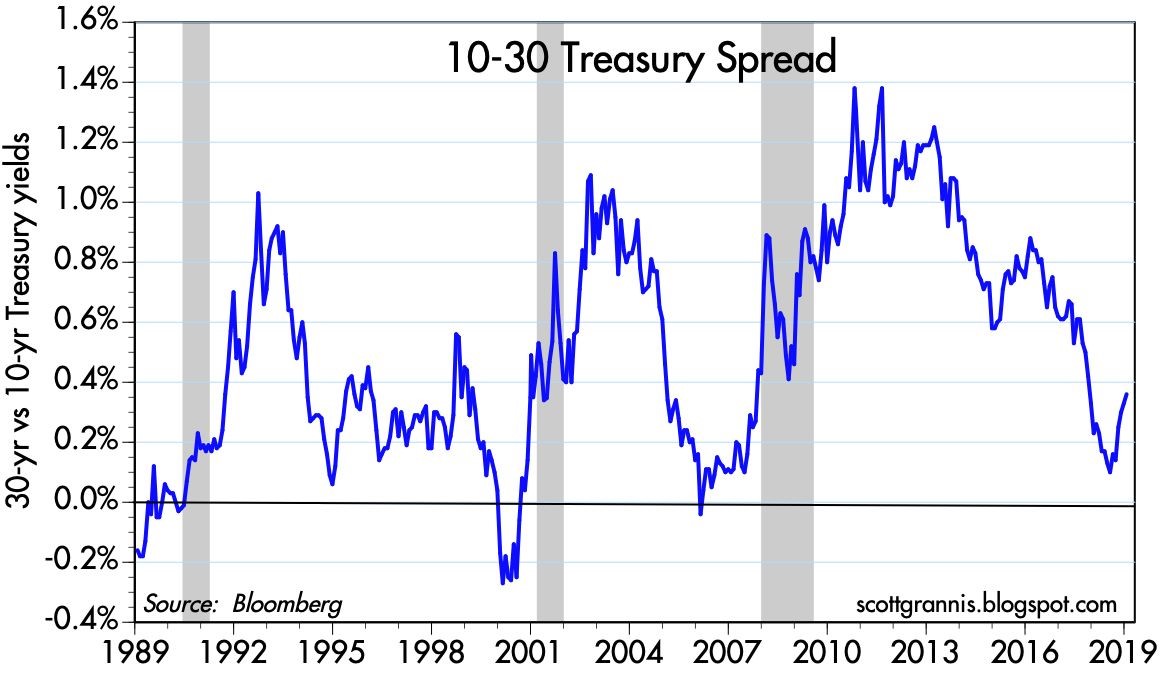

Despite China trade negotiations and the government shutdown deadlock placing a cloud over financial markets, brighter skies have begun to emerge in other areas. First and foremost has been the positive shift in positioning by the Federal Reserve as it relates to monetary policy. Not only has Jay Powell (Fed Chairman) communicated a clear signal of being “patient” on future interest rate target increases, but he has also taken the Fed off of “autopilot” as it relates to shrinking the Fed’s balance sheet – a process that can hinder economic growth. Combined, these shifts in strategy by the Fed have been enthusiastically received by investors, which has been a large contributor to the +15% rebound in stock prices since the December lows. Thanks to this change in stance, the inverted yield curve bogeyman that typically precedes post-World War II recessions has been held at bay as evidenced by the steepening yield curve (see chart below).

Source: Calafia Beach Pundit

Other areas of strength include the recent employment data, which showed 304,000 jobs added in January, the 100th consecutive month of increased employment. Fears of an imminent recession that penetrated psyches in the fourth quarter have abated significantly in January in part because of the notable strength seen in 4th quarter corporate profits, which so far have increased by +12% from last year, according to FactSet. The strength and rebound in overall commodity prices, including oil, seem to indicate any potential looming recession is likely further out in time than emotionally feared.

Source: Calafia Beach Pundit

As the chart above shows, over the last four years, spikes in fear (red line) have represented beneficial buying opportunities of stocks (blue line). The pace of gains in January is just as unsustainable as the pace of fourth-quarter losses were in stock prices. Uncertainties may remain on trade, shutdowns, geopolitics, and other issues but don’t throw away your investing dance shoes quite yet…the ball and music experienced last month could continue for a longer than expected period of time.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What’s Going on with This Crazy Market?!

The massive rally of the stock market since March 2009 has been perplexing for many, but the state of confusion has reached new heights as the stock market has surged another +2.0% in May, surpassing the Dow 15,000 index milestone and hovering near all-time record highs. Over the last few weeks, the volume of questions and tone of disbelief emanating from my social circles has become deafening. Here are some of the questions and comments I’ve received lately:

“Wade, why in the heck is the market up so much?”; “This market makes absolutely no sense!”; “Why should I buy at the peak when I can buy at the bottom?”; “With all this bad news, when is the stock market going to go down?”; “You must be shorting (betting against) this market, right?”

If all the concerns about the Benghazi tragedy, IRS conservative targeting, and Federal Reserve bond “tapering” are warranted, then it begs the question, “How can the Dow Jones and other indexes be setting new all-time highs?” In short, here are a few reasons:

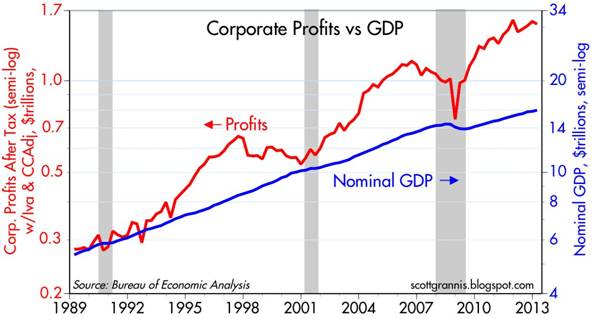

You hear a lot of noise on TV and read a lot of blathering in newspapers/blogs, but what you don’t hear much about is how corporate profits have about tripled since the year 2000 (see red line in chart above), and how the profit recovery from the recent recession has been the strongest in 55 years (Scott Grannis). The profit collapse during the Great Recession was closely chronicled in nail-biting detail, but a boring profit recovery story sells a lot less media advertising, and therefore gets swept under the rug.

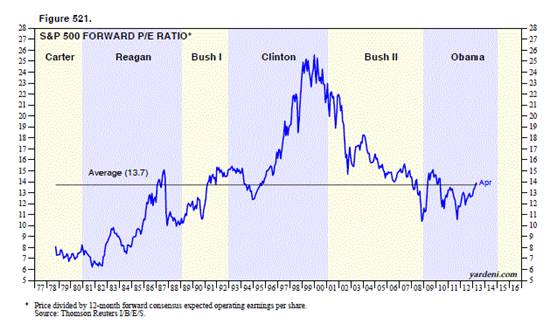

II.) Reasonable Prices (Comparing Apples & Oranges):

Source: Dr. Ed’s Blog

The Price-Earnings ratio (P/E) is a general barometer of stock price levels, and as you can see from the chart above (Ed Yardeni), current stock price levels are near the historical average of 13.7x – not at frothy levels experienced during the late-1990s and early 2000s.

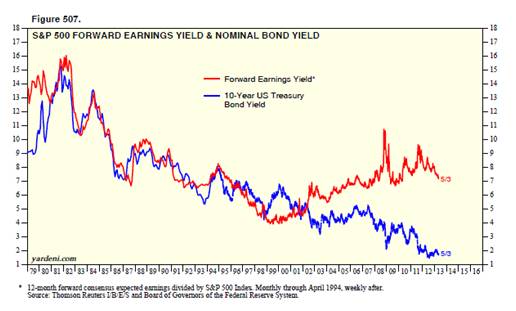

Comparing Apples & Oranges:

At the most basic level of analysis, investors are like farmers who choose between apples (stocks) and oranges (bonds). On the investment farm, growers are generally going to pick the fruit that generates the largest harvest and provide the best return. Stocks (apples) have historically offered the best prices and yielded the best harvests over longer periods of time, but unfortunately stocks (apples) also have wild swings in annual production compared to the historically steady crop of bonds (oranges). The disastrous apple crop of 2008-2009 led a massive group of farmers to flood into buying a stable supply of oranges (bonds). Unfortunately the price of growing oranges (i.e., buying bonds) has grown to the highest levels in a generation, with crop yields (interest rates) also at a generational low. Even though I strongly believe apples (stocks) currently offer a better long-term profit potential, I continue to remind every farmer (investor) that their own personal situation is unique, and therefore they should not be overly concentrated in either apples (stocks) or oranges (bonds).

Source: Dr. Ed’s Blog

Regardless, you can see from the chart above (Dr. Ed’s Blog), the red line (stocks) is yielding substantially more than the blue line (bonds) – around 7% vs. 2%. The key for every investor is to discover an optimal balance of apples (stocks) and oranges (bonds) that meets personal objectives and constraints.

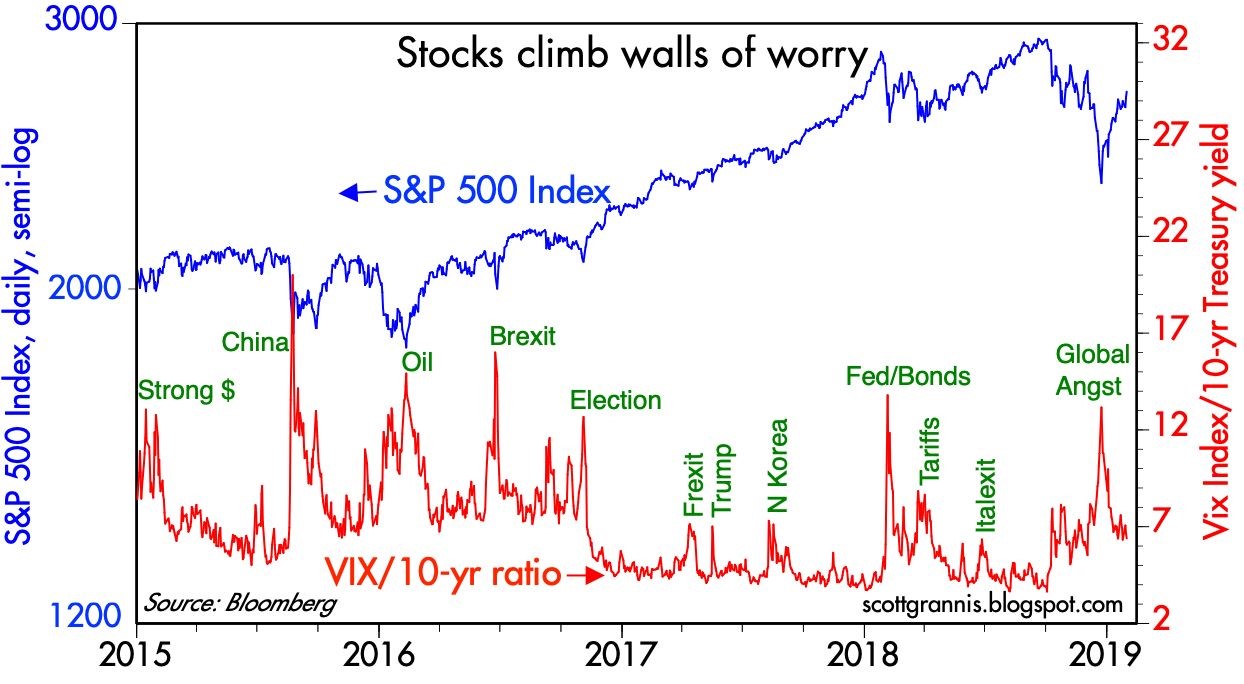

III.) Skepticism (Market Climbs a Wall of Worry):

Source: Calafia Beach Pundit

Although corporate profits are strong, and equity prices are reasonably priced, investors have been withdrawing hundreds of billions of dollars from equity funds (negative blue lines in chart above – Calafia Beach Pundit). While the panic of 2008-2009 has been extinguished from average investors’ psyches, the Recession in Europe, slowing growth in China, Washington gridlock, and the fresh memories of the U.S. financial crisis have created a palpable, nervous skepticism. Most recently, investors were bombarded with the mantra of “Selling in May, and Going Away” – so far that advice hasn’t worked so well. To buttress my point about this underlying skepticism, one need not look any further than a recent CNBC segment titled, “The Most Confusing Market Ever” (see video below):

Source: CNBC

It’s clear that investors remain skittish, but as legendary investor Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” The sentiment pendulum has been swinging in the right direction (see previous Investing Caffeine article), but when money flows sustainably into equities and optimism/euphoria rules the day, then I will become much more fearful.

Being a successful investor or a farmer is a tough job. I’ll stop growing apples when my overly optimistic customers beg for more apples, and yields on oranges also improve. In the meantime, investors need to remember that no matter how confusing the market is, don’t put all your oranges (bonds) or apples (stocks) in one basket (portfolio) because the financial markets do not need to get any crazier than they are already.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Measuring Chaos

![]()

An interesting study was done by Morgan Stanley Europe, in which they looked at the last 19 bear markets and subsequent rallies. I’m not sure how much weight you can put on these results since every bear market is unique in its own right, nonetheless it provides a good frame of reference for debates.

What the Morgan Stanley team found was that the median bear market resulted in a -57% decline over 30 months and the ensuing rally equaled about +71% over 17 months. The problem is that our bear market in the U.S. was much shorter than the median timeframe despite its steepness – the fall effectively began in October 2007 and bottomed in March 2009 (about 17 months in duration). Since the decline was faster in duration, does that mean the advance will be as well? Not sure. Our current rally has lasted about six months, which implies there is about another year for the rally to continue based on this data.

Prieur du Plessis wrote about the Morgan Stanley work for Seeking Alpha

As I alluded to earlier, it’s hard to compare an average to a period in which we had financial institutions dropping like flies (i.e., Bear Stearns, Lehman Brothers, WaMu, Fannie Mae, AIG, etc.) and people were hiding in caves – you knew it was really serious when it even caused voracious consumers to save money…imagine that. At the end of the day, stock and index prices eventually follow earnings. Because of the severity of this downfall, earnings came down faster than prices because fundamentals deteriorated faster than cost cutting could take place. When the economy begins to recover, the opposite will occur – businesses will not be able to hire and spend as fast as earnings are growing. It will be a nice problem to have, but nonetheless characteristic of a typical economic recovery.

In the U.S., the consumer will have a lot to say about the shape of the recovery since they account for about 2/3 of our country’s economic activity. The other “X” factor will be to what extent government legislation will have an impact on the economy. There will be opportunities available domestically and internally, but in order to survive the chaos, one needs to have a diversified and balanced global approach.

Read the Full Seeking Alpha Article Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}