Posts tagged ‘quantitative easing’

Why 0% Rates? Tech, Globalization & EM (Not QE)

Recently I have written about the head-scratching, never-ending, multi-decade decline in long-term interest rates (see chart below). Who should care? Well, just about anybody, if you bear in mind the structure of interests rates impacts the cost of borrowing on mortgages, credit cards, automobiles, corporate bonds, savings accounts, and practically every other financial instrument you can possibly think of. Simplistic conventional thinking explains the race to 0% global interest rates by the loose monetary Quantitative Easing (QE) policies of the Federal Reserve. But validating that line of thinking becomes more challenging once you consider QE ended months ago. What’s more, contrary to common belief, rates declined further rather than climb higher after QE’s completion.

Source: Calafia Beach Pundit

More specifically, if you look at rates during this same time last year, the yield on the 10-Year Treasury Note had more than doubled in the preceding 18 months to a level above 3.0%. The consensus view then was that the eventual wind-down of QE would only add gasoline to the fire, causing bond prices to decline and rates to extend an indefinite upwards march. Outside of bond guru Jeff Gundlach, and a small minority of prognosticators, the herd was largely wrong – as is usually the case. As we sit here today, the 10-Year Note currently yields a paltry 2.26%, which has led to the long-bond iShares 20-Year Treasury ETF (TLT) jumping +22% year-to-date (contrary to most expectations).

The American Ostrich

Like an ostrich sticking its head in the sand, us egocentric Americans tend to ignore details relating to others, especially if the analyzed data is occurring outside the borders of our own soil. Unbeknownst to many, here are some key country interest rates below U.S. yields:

- Switzerland: 0.33%

- Japan: 0.34%

- Germany: 0.60%

- Finland: 0.70%

- Austria: 0.75%

- France: 0.88%

- Denmark: 0.89%

- Sweden: 0.98%

- Ireland: 1.29%

- Spain: 1.69%

- Canada 1.80%

- U.K: 1.85%

- Italy: 1.93%

- U.S.: 2.26% (are our rates really that low?)

Outside of Japan, these listed countries are not implementing QE (i.e., “Quantitative Easing”) as did the United States. Rather than QE being the main driver behind the multi-decade secular decline in interest rates, there are other more important disinflationary forces at work driving interest rates lower.

Technology, Globalization, and Emerging Market Competition (T.G.E.M.)

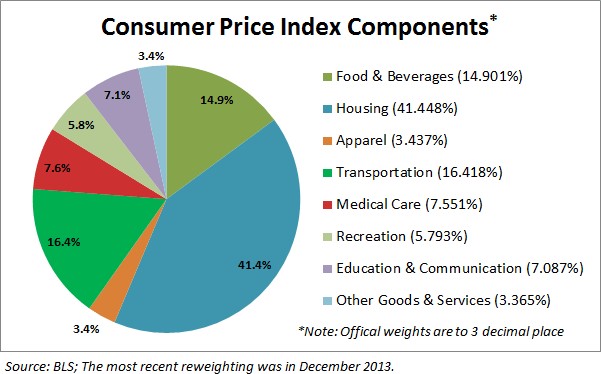

While tracking the endless monthly inflation statistics is a useful exercise to understand the tangible underlying pricing components of various industry segments (e.g., see 20 pages of CPI statistics), the larger and more important factors can be attributed to the somewhat more invisible elements of technology, globalization, and emerging market competition (T.G.E.M).

Starting with technology, to put these dynamics into perspective, consider the number of transistors, or the effective horsepower, on a semiconductor (a.k.a. computer “chip”) today. The overall impact on global standards of living is nothing short of astounding. Take an Intel chip for example – it had approximately 2,000 transistors in 1971. Today, semiconductors can cram over 10,000,000,000 (yes billions – 5 million times more) transistors onto a single semiconductor. Any individual can look no further than their smartphone to understand the profound implications this has not only on pricing in general, but society overall. To illustrate this point, I would direct you to a post highlighted by Professor Mark J. Perry, who observed the cost to duplicate an iPhone during 1991 would have been more than $3,500,000!

There are an infinite number of examples depicting how technology has accelerated the adoption of globalization. More recently, events such as the Arab Spring point out how Twitter (TWTR) displaced costly military engagement alternatives. The latest mega-Chinese IPO of Alibaba (BABA) was also emblematic of the hunger experienced in emerging markets to join the highly effective economic system of global capitalism.

I think New York Times journalist Tom Friedman said it best in his book, The World is Flat, when he made the following observations about the dynamics occurring in emerging markets:

“My mom told me to eat my dinner because there are starving children in China and India – I tell my kids to do their homework because Chinese and Indians are starving for their jobs”.

“France wants a 35 hour work week, India wants a 35 hour work day.”

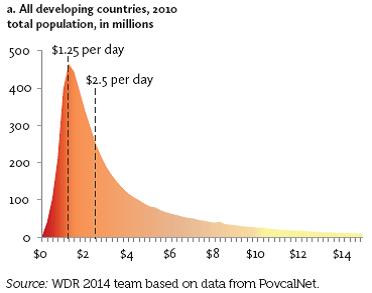

There may be a widening gap between rich and poor in the United States, but technology and globalization is narrowing the gap across the rest of the world. Consider nearly half of the world’s population (3 billion+ people) live in poverty, earning less than $2.50 a day (see chart below). Technology and globalization is allowing this emerging middle class climb the global economic ladder.

These impoverished individuals may not be imminently stealing our current jobs and driving general prices lower, but their children, and the countless educated millions in other international markets are striving for the same economic security and prosperity we have. The educated individuals in the emerging markets that have tasted capitalism are giving new meaning to the word “urgency”, which is only accelerating competition and global pricing pressures. It comes as no surprise to me that this generational migration from the poor to the middle class is putting a lid on inflation and interest rates around the world.

Declining costs of human labor from emerging markets however is not the only issue putting a ceiling on general prices. Robotics, an area in which Sidoxia holds significant investments, continues to be an area of fascination for me. With human labor accounting for the majority of business costs, it’s no wonder the C-suite is devoting more investment dollars towards automation. Rather than hire and train expensive workers, why not just buy a robot? This is not just happening in the U.S. – in fact the Chinese purchased more robots than Americans last year. And why not? An employer does not have to pay a robot overtime compensation; a robot never shows up late; robots never sue for discrimination or harassment; robots receive no healthcare or retirement benefits; and robots work 24 hours/day, 7 days/week, and 365 days/year.

While newspapers, bloggers, and talking heads like to point to the simplistic explanation of loose, irresponsible monetary policies of global central banks as the reason behind a four decade drop in interest rates that is only a small part of the story. Investors and policy makers alike should be paying closer attention to the factors of technology, globalization, and emerging market competition as the more impactful dynamics systematically driving down long term interest rates and inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including long positions in certain exchange traded fund positions and INTC (short position in TLT), but at the time of publishing SCM had no direct position in BABA, TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Pain of Diversification

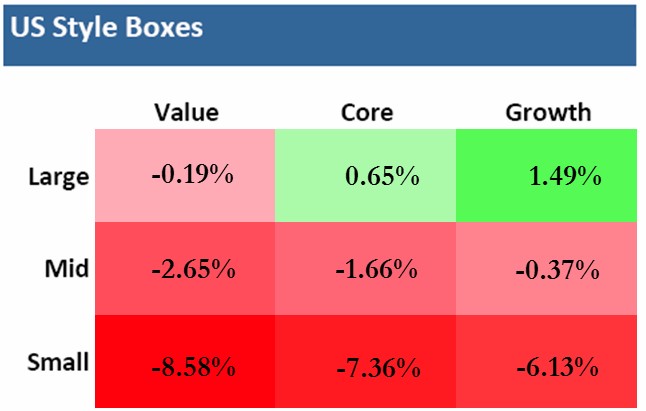

The oft-quoted tenet that diversification should be the cornerstone of any investment strategy has come under assault in the third quarter. As you can see from the chart below, investors could run, but they couldn’t hide. The Large Cap Growth category was the major exception, thanks in large part to Apple Inc.’s (AAPL) +8% appreciation. More specifically, seven out of the nine Russell Investments style boxes were in negative territory for the three month period. The benefits of diversification look even worse, if you consider other large asset classes and sectors such as the Gold/Gold Miners were down about -14% (GDX/GLD); Energy -9% (XLE); Europe-EAFE -6% (EFA); Utilities -5% (XLU); and Emerging Markets -4% (EEM).

*Results are for Q3 – 2014 (Source: Vanguard Group, Inc. & Russell Investments)

On the surface, everything looks peachy keen with all three major indices posting positive Q3 appreciation of +1.3% for the Dow, +0.6% for S&P 500, and +1.9% for the NASDAQ. It’s true that over the long-run diversification acts like shock absorbers for economic potholes and speed bumps, but in the short-run, all investors can hit a stretch of rough road in which shock absorbers may seem like they are missing. Over the long-run, you can’t live without diversification shocks because your financial car will eventually breakdown and the ride will become unbearable.

What has caused all this underlying underperformance over the last month and a half? The headlines and concerns change daily, but the -5% to -6% pullback in the market has catapulted the Volatility Index (VIX or “Fear Gauge”) by +85%. The surge can be attributed to any or all of the following: a slowing Chinese economy, stagnant eurozone, ISIS in Iraq, bombings in Syria, end of Quantitative Easing (QE), impending interest rate hikes, mid-term elections, Hong Kong protests, proposed tax inversion changes, security hacks, rising U.S. dollar, PIMCO’s Bill Gross departure, and a half dozen other concerns.

In general, pullbacks and corrections are healthy because shares get transferred out of weak hands into stronger hands. However, one risk associated with these 100 day floods (see also 100-Year Flood ≠ 100-Day Flood) is that a chain reaction of perceptions can eventually become reality. Or in other words, due to the ever-changing laundry list of concerns, confidence in the recovery can get shaken, which in turn impacts CEO’s confidence in spending, and ultimately trickles down to employees, consumers, and the broader economy. In that same vein, George Soros, the legendary arbitrageur and hedge fund manager, has famously written about his law of reflexivity (see also Reflexivity Tail Wags Dog). Reflexivity is based on the premise that financial markets continually trend towards disequilibrium, which is evidenced by repeated boom and bust cycles.

While, at Sidoxia, we’re still finding more equity opportunities amidst these volatile markets, what this environment shows us is conventional wisdom is rarely correct. Going into this year, the consensus view regarding interest rates was the economy is improving, and the tapering of QE would cause interest rates to go significantly higher. Instead, the yield on the 10-Year Treasury Note has gone down significantly from 3.0% to 2.3%. The performance contrast can be especially seen with small cap stocks being down-10% for the year and the overall Bond Market (BND) is up +3.1% (and closer to +5% if you include interest payments). Despite interest rates fluctuating near generational lows with paltry yields, the power of diversification has proved its value.

While there are multiple dynamics transpiring around the financial markets, the losses across most equity categories and asset classes during Q3 have been bloody. Nonetheless, investing across the broad bond market and certain large cap stock segments is evidence that diversification is a valuable time-tested principle. Times like these highlight the necessity of diversification gain to offset the current equity pain.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, BND, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in EEM, GDX, GLD, EFA, XLE, XLU, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Perception vs. Reality: Interest Rates & the Economy

There is a difference between perception and reality, especially as it relates to the Federal Reserve, the economy, and interest rates.

Perception: The common perception reflects a belief that Quantitative Easing (QE) – the Federal Reserve’s bond buying program – has artificially stimulated the economy and financial markets through lower interest rates. The widespread thinking follows that an end to tapering of QE will lead to a crash in the economy and financial markets.

Reality: As the chart below indicates, interest rates have risen during each round of QE (i.e., QE1/QE2/QE3) and fallen after the completion of each series of bond buying (currently at a pace of $85 billion per month in purchases). That’s right, the Federal Reserve has actually failed on its intent to lower interest rates. In fact, the yield on the 10-year Treasury Note stands at 2.94% today, while at the time QE1 started five years ago, on December 16, 2008, the 10-year rate was dramatically lower (~2.13%). Sure, the argument can be made that rates declined in anticipation of the program’s initiation, but if that is indeed the case, the recent rate spike of the 10-year Treasury Note to the 3.0% level should reverse itself once tapering begins (i.e., interest rates should decline). Wow, I can hardly wait for the stimulative effects of tapering to start!

Source: Calafia Beach Pundit

Fact or Fiction? QE Helps Economy

Taken from a slightly different angle, if you consider the impact of the Federal Reserve’s actions on the actual economy, arguably there are only loose connections. More specifically, if you look at the jobs picture, there is virtually NO correlation between QE activity and job creation (see unemployment claims chart below). There have been small upward blips along the QE1/QE2/QE3 path, but since the beginning of 2009, the declining trend in unemployment claims looks like a black diamond ski slope.

Source: Calafia Beach Pundit

Moreover, if you look at a broad spectrum of economic charts since QE1 began, including data on capital spending, bank loans, corporate profits, vehicle sales, and other key figures related to the economy, the conclusion is the same – there is no discernible connection between the economic recovery and the Federal Reserve’s quantitative easing initiatives.

I know many investors are highly skeptical of the stock market’s rebound, but is it possible that fundamental economic laws of supply and demand, in concert with efficient capital markets, could have something to do with the economic recovery? Booms and busts throughout history have come as a result of excesses and scarcities – in many cases assisted by undue amounts of fear and greed. We experienced these phenomena most recently with the tech and housing bubbles in the early and middle parts of last decade. Given the natural adjustments of supply and demand, coupled with the psychological scars and wounds from the last financial crisis, there is no clear evidence of a new bubble about to burst.

While it’s my personal view that many government initiatives, including QE, have had little impact on the economy, the Federal Reserve does have the ability to indirectly increase business and consumer confidence. Ben Bernanke clearly made this positive impact during the financial crisis through his creative implementation of unprecedented programs (TARP, TALF, QE, Twist, etc.). The imminent tapering and eventual conclusion of QE may result in a short-term hit to confidence, but the economy is standing on a much stronger economic foundation today. Making Ben Bernanke a scapegoat for rising interest rates is easy to do, but in actuality, an improving economy on stronger footing will likely have a larger bearing on the future direction of interest rates relative to any upcoming Fed actions.

Doubters remain plentiful, but the show still goes on. Not only are banks and individuals sitting on much sturdier and healthier balance sheets, but corporations are running lean operations that are reporting record profit margins while sitting on trillions of dollars in cash. In addition, with jobs on a slow but steady path to recovery, confidence at the CEO and consumer levels is also on the rise.

Despite all the negative perceptions surrounding the Fed’s pending tapering, reality dictates the impact from QE’s wind-down will likely to be more muted than anticipated. The mitigation of monetary easing is more a sign of sustainable economic strength than a sign of looming economic collapse. If this reality becomes the common perception, markets are likely to move higher.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No Free Lunch, No Free Sushi

Everybody loves a free lunch, myself included, and many in Japan would like free sushi too. Despite the short term boost in Japanese exports and Nikkei stock prices, there are no long-term free lunches (or free sushi) when it comes to global financial markets. Following in the footsteps of the U.S. Federal Reserve, the Bank of Japan (BOJ) has embarked on an ambitious plan of doubling its monetary base in two years and increasing inflation to a 2% annual rate – a feat that has not been achieved in more than two decades. By the BOJ’s estimate, it will take a $1.4 trillion injection into economy to achieve this goal by the end of 2014.

Lunch is tasty right now, as evidenced by a tasty appetizer of +3.5 % Japanese first quarter GDP and this year’s +46% spike in the value of the Nikkei. Japan is hopeful that its mix of monetary, fiscal, and structural policies will spur demand and increase the appetite for Japanese exports, however, we know fresh sushi can turn stale quickly.

Quantitative easing (QE) and monetary stimulus from central banks around the globe have been hailed as a panacea for sluggish global growth – most recently in Japan. Commentators often oversimplify the benefits of money printing without acknowledging the pitfalls. Basic economics and the laws of supply & demand eventually prevail no matter the fiscal or monetary policy implemented. Nonetheless, there can be temporary disconnects between current equity prices and exchange rates, before underlying fundamentals ultimately drive true intrinsic values.

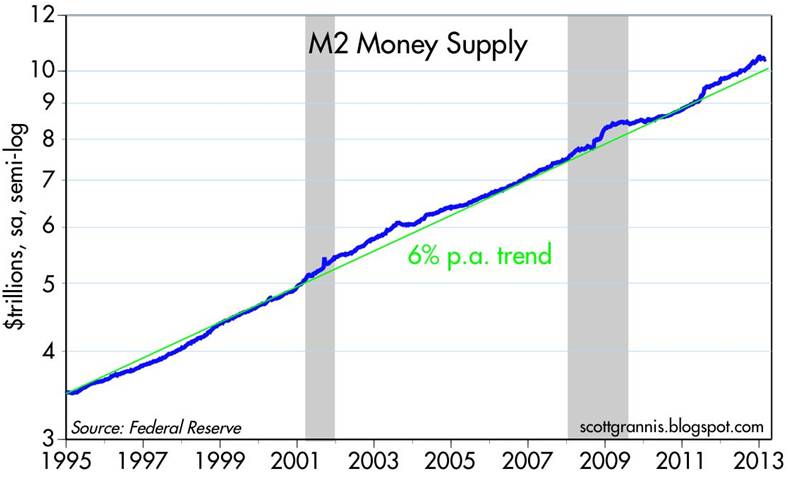

Impassioned critics of the Federal Reserve and its Chairman Ben Bernanke would have you believe the money supply is exploding, and hyperinflation is just around the corner. It’s difficult to quarrel with the trillions of dollars created by the Fed’s printing presses via QE1/QE2/QE3, but the fact remains that money supply growth has continued at a steady growth rate – not exploding (see Calafia Beach Pundit chart below).

Source: Calafia Beach Pundit

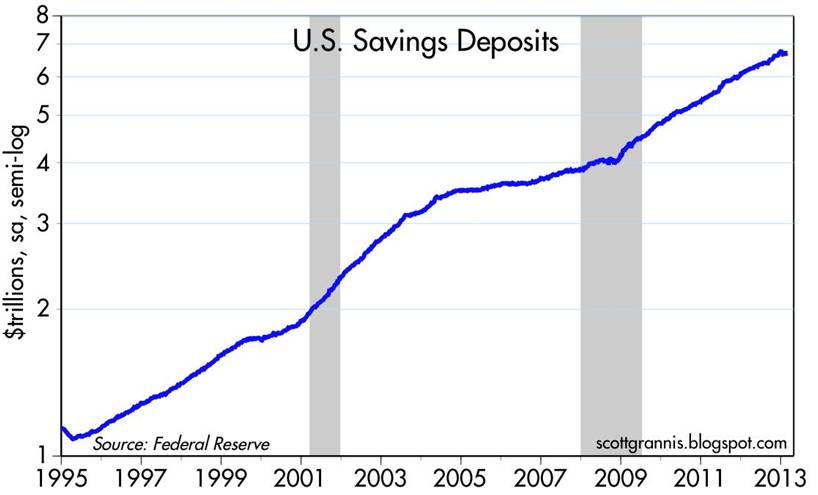

Why no explosion in the money supply? Simply, the trillions of dollars printed by the Fed have sat idly in bank vaults as reserves. Once nervous consumers stop hoarding trillions in cash held in savings deposit accounts (see chart below) and banks begin lending at a healthier clip, then money supply growth will accelerate. By definition, money supply growth in excess of demand for goods and services (i.e., GDP) is the main cause of inflation.

Source: Calafia Beach Pundit

Although inflationary pressure has not reared its ugly head yet, there are plenty of precursors indicating inflation may be on its way. The unemployment rate continues to tick downwards (7.5% in Aril) and the much anticipating housing recovery is gaining steam. Inflationary fear has manifested itself in part through the heightened number of conversations surrounding the Fed “tapering” its $85 billion per month bond purchasing program.

We’ve enjoyed a sustained period of low price level growth, however the Goldilocks period of little-to-no inflation cannot last forever. The differences between current prices and true value can exist for years, and as a result there are many different strategies attempted to capture profits. Like the gambling masses frequenting casinos, speculators can beat the odds in the short-run, but the house always wins in the long-run – hence the ever-increasing size and number of casinos. While a small number of professionals understand how to shift the unbalanced odds into their favor, most lose their shirt. On Wall Street, that is certainly the case. Studies show speculating day traders persistently lose about 80% of the time. Long-term investors are uniquely positioned to exploit these value disparities, if they have a disciplined process with the ability to patiently value assets.

Even though the Japanese economy and stock market have rebounded handsomely in the short-run, there is never a free lunch over the long-term. Unchecked policies of money printing, deficits, and debt expansion won’t lead to boundless prosperity. Eventually a spate of irresponsible actions will result in inflation, defaults, recessions, and/or higher unemployment rates. Unsustainable monetary and fiscal stimulus may lead to a tasty free lunch now, but if investors overstay their welcome, the sushi may turn bad and the speculators will be left paying the hefty tab.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Helicopter Ben to QE3 Rescue

Faster than a speedy credit default swap, more powerful than a federal funds interest rate cut, and able to leap a tall Mario Draghi in a single bound, look…it’s Helicopter Ben! How did Federal Reserve Chairman Ben Bernanke become a monetary superhero with such a cool nickname as Helicopter Ben (a.k.a. “HB”)? Bernanke, a former Princeton University professor, has widely been known to be a diligent student of the Great Depression, and his aviation nickname stems from a 2002 speech in which he referenced dropping money from a helicopter to combat deflation. While investors may worry about HB’s ability to fight the inflation thugs, there should be no questions about his willingness to implement accommodative, deflation-fighting monetary policies.

Chairman Bernanke may not epitomize your ideal superhero, however this slightly past middle-aged bearded and balding man has helped mastermind some of the most creative and aggressive monetary rescue efforts our country and globe has seen in the history of man (and woman). This week’s money-printing QE3 announcement solidified Bernanke’s historic capital saturating ranking.

Since Helicopter Ben’s heroic appointment as Federal Reserve Chairman in 2006 by George W. Bush, Bernanke has instituted numerous monetary gadgets in hopes of meeting the Federal Reserve’s dual mandate, which is i) to achieve low inflation and ii) to strive for maximum employment. Arguably, given the anemic growth here in the U.S.; the recession in Europe; and slowing growth in the emerging markets (i.e., China, Brazil, India, etc.), slack in the economy and static labor wages have largely kept inflation in check. With the first part of the dual mandate met, Bernanke has had no problem putting his monetary superpowers to work.

As referenced earlier, Bernanke’s bazooka launch of QE3, an open ended MBS (Mortgage Back Securities) bond binging program, will add $40 billion of newly purchased assets to the Fed’s balance sheet on a monthly basis until the labor market improves “substantially” (whatever that means). What’s more, in addition to the indefinite QE3, Bernanke has promised to keep the federal funds rate near zero “at least through mid-2015,” even for a “considerable time after the economic recovery strengthens.”

HB’s Track Record

Throughout superhero history, Superman, Spider-man, and Batman have used a wide-array of superhuman powers, extraordinary gadgets, and superior intellect to conquer evil-doers and injustices across the globe. Bernanke has also forcefully put his unrivaled money-printing talents to work in an attempt to cure the financial ills of the world. Here’s a quick multi-year overview of how Bernanke has put his unique talents to print trillions of dollars and keep interest rates suppressed:

Rate Cuts (September 2007 – December 2008): Before “quantitative easing” was a part of our common vernacular, the Fed relied on more traditional monetary policies, such as federal funds rate targeting, conducted through purchases and sales of open market securities. Few investors recall, but before HB’s fed funds rate cut rampage of 10 consecutive reductions in 2007 and 2008 (the fed funds rate went from 5.25% to effectively 0%), Bernanke actually increased rates three times in 2006.

Crisis Actions (2007 – 2009): Love him or hate him, Bernanke has been a brave and busy soul in dealing with the massive proportions of the global financial crisis. If you don’t believe me, just check out the Financial Crisis Timeline listed at the St. Louis Federal Reserve. Many investors don’t remember, but Bernanke helped orchestrate some of the largest and most unprecedented corporate actions in our history, including the $30 billion loan to JPMorgan Chase (JPM) in the Bear Stearns takeover; the $182 billion bailout of AIG; the conversion of Morgan Stanley (MS) and Goldman Sachs Group Inc. (GS) into bank holding companies; and the loan/asset-purchase support to Fannie Mae (FNMA) and Freddie Mac (FMCC). These actions represented just the tip of the iceberg, if you also consider the deluge of liquidity actions taken by the Fed Chairman.

HB Creates Acronym Soup

In order to provide a flavor of the vastness in emergency programs launched since the crisis, here is an alphabet soup of program acronyms into which the Fed poured hundreds of billions of dollars:

- Term Asset-Backed Securities Loan Facility (TALF)

- Term Auction Facility (TAF)

- Money Market Investor Funding Facility (MMIFF)

- Commercial Paper Funding Facility (CPFF)

- Primary Dealer Credit Facility (PDCF)

- Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF)

- Temporary Reciprocal Currency Arrangements (Swap lines)

- Term Securities Lending Facility (TSLF)

Plenty of acronyms to go around, but these juicy programs have garnered most of investors’ attention:

QE1 (November 2008 – March 2010): In hopes of lowering interest rates for borrowers and stimulating the economy, HB spearheaded the Fed’s multi-step, $1 trillion+ buying program of MBS (mortgage backed securities) and Treasuries.

QE2 (November 2010 – June 2011): Since the Fed felt QE1 didn’t pack enough monetary punch to keep the economy growing at a fast enough clip, the FOMC (Federal Open Market committee) announced its decision to expand its holdings of securities in November 2010. The Committee maintained its existing policy of reinvesting principal payments from its securities holdings and to also purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011 (an equivalent pace of about $75 billion per month).

Operation Twist (September 2011 – December 2012): What started out as a $400 billion short-term debt for longer-term debt swap program in September 2011, expanded to a $667 billion program in June 2012. With short-term rates excessively low, Bernanke came up with this Operation Twist scheme previously used in the early 1960s. Designed to flatten the yield curve (bring down long-term interest rates) to stimulate economic activity, Bernanke thought this program was worth another go-around. Unlike quantitative easing, Operation Twist does not expand the Fed’s balance sheet – the program merely swaps short-term securities for long-term securities. Currently, the program is forecasted to conclude at the end of this year.

The Verdict on HB

So what’s my verdict on the continuous number of unprecedented actions that Helicopter Ben and the Fed have taken? Well for starters, I have to give Mr. Bernanke an “A-” on his overall handling of the financial crisis. Had his extreme actions not been taken, the pain and agony experienced by all would likely be significantly worse, and the financial hole a lot deeper.

With that said, am I happy about the announcement of QE3 and the explosion in the Fed’s money printing activities? The short answer is “NO”. It’s difficult to support a program with questionable short-run interest rate benefits, when the menacing inflationary pressures are likely to outweigh the advantages. The larger problem in my mind is the massive fiscal problem we are experiencing (over $16 trillion in debt and endless trillion dollar deficits). More importantly, this bloated fiscal position is creating an overarching, nagging crisis of confidence. A resolution to the so-called “fiscal cliff,” or the automated $600 billion in tax increases and spending cuts, is likely to have a more positive impact on confidence than a 0.05% – 0.25% reduction in mortgage rates from QE3. Once adequate and sustained growth returns, and inflation rears its ugly head, how quickly Helicopter Ben tightens policy will be his key test.

Until then, Bernanke will probably continue flying around while gloating in his QE3 cape, hoping his quantitative easing program will raise general confidence. Unfortunately, his more recent monetary policies appear to be creating diminishing returns. Even before QE3’s implementation, Helicopter Ben has witnessed his policies expand the Fed’s balance sheet from less than $900 billion at the beginning of the recession to almost $3 trillion today. Despite these gargantuan efforts, growth and confidence have been crawling forward at only a modest pace.

No matter the outcome of QE3, as long as Ben Bernanke remains Federal Reserve Chairman, and growth remains sluggish, you can stay confident this financial man of steel will continue dumping money into the system from his helicopter. If Bernanke wants to create a true legendary superhero ending to this story, the kryptonite-like effects of inflation need to be avoided. This means, less money-printing and more convincing of Congress to take action on our out-of-control debt and deficits. Now, that’s a comic book I’d pay to read.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in JPM, AIG, MS, GS, FNMA, FMCC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Draghi & ECB Pass Trash and Serve Brussels Sprouts

ECB (European Central Bank) President Mario Draghi made it clear with his most recent monetary banking announcements that he is perfectly willing to shovel the sovereign debt trash around the financial system, but he just doesn’t want the ECB to gobble up heaps of the smelly debt.

On the same day that Draghi lowered the key benchmark interest rate by -0.25% to 1.00%, he also reduced the lending credit rating threshold for acceptable banking collateral to “single-A” and offered banks endless three-year loans with . But wait…there’s more! In typical infomercial fashion, Draghi had an additional stimulative gift offering – he halved the reserve requirement ratios for European banks.

Although Draghi is handing out lots of hugs and kisses to the banks, including infinite amounts of three-year loans, he is also providing very little direct love to European debt-laden governments. In other words, Draghi isn’t ready to pull out the printing press bazooka to sop up mounds of trashy sovereign debt (i.e., Greece, Italy, and Spain). Draghi may be willing to make the ECB the lender of last resort for the banks, but he is not signaling the same lender of last resort commitment for careless governments.

Despite Draghi’s public aversion to bond buying (a.k.a. QE or quantitative easing), he indirectly is funding quantitative easing anyway. Rather than having the ECB accelerate the direct purchase of besieged sovereign debt, he indirectly is giving money to the banks to purchase the same struggling bonds. Sneaky, but clever…I like it.

Eat Your Brussels Sprouts!

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi, in dealing with the irresponsible fiscal actions of the sovereigns, is using the same precise “sprout mandate.” In a recent press conference, here’s how Draghi delivered his tough talk:

“All euro-area governments urgently need to do their utmost” for fiscal sustainability. “Policy makers need to correct excessive deficits and move to balanced budgets in the coming years. This will strengthen overall economic sentiment. To accompany fiscal consolidation, the governing council has called for bold and ambitious structural reforms.”

Just as it makes sense for me not to say, “Hey kids, don’t worry about eating your vegetables, save room for the ice cream sundae buffet,” it probably doesn’t make sense for Draghi to inform European leaders, “Hey kids, don’t worry about those massive debts and deficits, the ECB will give you plenty of money to buy up all that trashy sovereign debt of yours.”

Hypocritical Or Shrewd?

I applaud Signore Draghi for implementing his bold actions as lender of last resort for European Banks, but isn’t it a tad bit hypocritical? The ECB President talks seriously about Basel III capital requirements, yet he is easing rules on collateral and reserves. Why is it OK for the ECB to condone reckless behavior and introduce moral hazards for the banks (i.e., limitless ECB backstop), but not for irresponsible governments too? If I am a European bank with continuous access to ECB loans, why not roll the dice and risk shareholder capital in hopes of a big risky payoff? I’m sure Jon Corzine at MF Global (MFGLQ.PK) would appreciate similar financial backing. What’s more, how credible can Draghi be about his tough fiscal love and anti-quantitative easing stances when he is currently offering never-ending amounts of money to the banks and already buying collapsing sovereign bonds as we speak?

No matter the view you hold, the ECB is openly demonstrating it will not sit idle watching the banking system collapse under its own watch, much like the Federal Reserve and Ben Bernanke did not sit idle in 2008-2009. Perhaps Draghi isn’t being hypocritical, but is rather being shrewd? Although Draghi wants governments to eat their fiscal Brussels sprouts, let’s not kid ourselves. Just as Draghi is willing to pass the trash and appease the banking system, if the eurozone sovereign debt crisis continues worsening, don’t be surprised to see Draghi roll out his ice cream sundae buffet of aggressive bond buying. That will taste much better than Brussels sprouts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MF Global (MFGLQ.PK), or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

QE2 Drowning TIPS Yields Below Water

The holiday season is creeping up on us, and the only question building up more anticipation than what gift kids are going to get from Santa Claus is what investors are going to get from Federal Reserve Chairman Ben Bernanke – in the form of QE2 (Quantitative Easing Part II)? The inevitable QE2 program is an effort designed by the Fed to keep interest rates low and reduce the threat of deflation. In addition, QE2 is structured to stimulate the meager 0.8% core inflation experienced over the last 12 months (Bloomberg) to a Goldilocks level – not too hot and not too cold. Some pundits suggest the Fed should target a 2% inflation rate. QE2 asset purchase estimates are all over the map, but I can safely guess somewhere between a few hundred billion and $2 trillion (very brave of me).

Treasuries Weigh Down TIPS Yields

Ever since QE1 expired in the March timeframe, speculation began about the next potential slug of Treasuries and mortgage backed securities to be purchased by the Fed. As a consequence, this speculation became a contributing factor to 10-Year Treasury yields plummeting from around 4.0% to around 2.5%. Simultaneously, 5-Year TIPS (Treasury Inflation Protection Securities) yields have moved to negative territory.

Scott Grannis at Calafia Beach Pundit has a great chart showing the relationship between nominal Treasury yields, real TIPS yields, and expected inflation for 10-year maturities. As you can see below, over the last ten years there has been a tight correlation between the 10-year Treasury bond versus TIPS, with the former 10-year declining yield acting as a weight drowning the latter TIPS yield:

Source: scottgrannis.blogspot.com

Worth noting, absent the brief period in late-2008 and early-2009, inflation expectations have been remarkably stable in that 1.5% – 2.5% range.

Negative Yields…Who Cares?!

Unprecedented times have created an unprecedented appetite for bonds (see Bubblicious Bonds), and as a result, we just witnessed a historic $10 billion TIPS auction this week producing an eye-catching negative -0.55% yield. Sensationalist commentators characterize the negative yield dynamic as a money losing proposition, whereby investors are forced to pay the government. This assertion is quite a distortion and not quite true – we will review the mechanics of TIPS later.

- Source: scottgrannis.blogspot.com

If we’re not back to a panic filled environment of soup kitchen lines and bank runs, then why are TIPS paying a negative yield?

- QE2: As mentioned above, investor expectations are that Uncle Sam will come to the rescue and deliver lower interest rates (higher prices) through purchases of Treasuries and mortgage-backed securities.

- Rising Inflation Expectations: As fears surrounding future inflation increase, the price of TIPS will rise, and yields will fall.

- Sluggish Economy: Lackluster growth and fear of double dips have pressured rates lower as debates still linger about whether or not the U.S. will follow Japan (see Lost Decade).

Nuts & Bolts of TIPS

TIPS maturities come in terms of 5 years, 10 years and 30 years. Per the Treasury, 5-year TIPS are auctioned in April and October; 10-year TIPS in January, March, May (beginning in 2011), July, September, and November; and 30-year TIPS in February and August.

This table from Barclays Capital below does an excellent job of conceptually displaying the differences between vanilla Treasuries and TIPS.

Some Observations:

1) As you can see, the principal value of the TIPS security adjusts with inflation (Consumer Price Index). The price of the TIPS security, which we cannot see in the example, adjusts upwards (or downwards) with inflation expectations.

2) The TIPS security pays a lower coupon (3.5% vs. 5.0%), but you can see that under a 4% annual inflation assumption (principal value adjusts from $10,000 in Year 0 to $10,400 in Year 1), the ending value of the TIPS comes up significantly higher ($19,172 vs. $15,000).

3) The break-even inflation expectation rate is 1.5% (derived from 5% coupon minus 3.5% coupon). If you think inflation will average more than 1.5%, then buy the TIPS security. If you think inflation will average less than 1.5%, then buy the 10-year Treasury.

TIPS Advantages

- Inflation Protection: At the risk of stating the obvious, if you expect long-term inflation to average substantially more than about 2% (current inflation expectations), then TIPS are a great way of protecting your purchasing power.

- Deflation Protection: Perhaps TIPS should be called DIPS (Deflation Income Protection Securities)? What some investors do not realize is that even if our country were to spiral into long-term deflationary crisis, TIPS investors are guaranteed the original amount of principal. Yes, that’s right…guaranteed. Interest payments could conceivably decline to zero and the principal value could temporarily fall below par, but the government guarantees the original principal regardless of the scenario.

- No Credit or Default Risk: The advantage of the government owning its own printing press is that there is very little risk of default, so preservation of capital is not much of a risk.

TIPS Disadvantages

- Interest Rate Risk: It’s great to be indexed to inflation, but because TIPS include long-range maturities, investors face a significant amount of interest rate risk if the TIPS are not held until maturity. TIPS will likely outperform Treasuries under a rising rate scenario, but will be impacted nonetheless.

- CPI Risk: Even if you are not a conspiracy theorist who believes government CPI figures are artificially depressed, it is still quite possible your personal baskets of purchases do not perfectly align with the arbitrary CPI basket of goods.

- Negative Deflation Adjustments: Although a TIPS investor has an embedded “deflation floor” equivalent to original principal value, interest payments will be negatively impacted by declines in principal value during deflationary periods. Also, previously issued TIPS with accumulated principal values from inflationary adjustments run larger principal loss risks as compared to newly issued TIPS.

Although 5-year TIPS yields may have dunked below water into negative territory, the headline bark is much worse than the bite. There has been a massive rally in bond prices in front of the QE2 bond binge by the Fed. Nevertheless, inflation expectations have remained fairly stable and TIPS still provide defensive characteristics under both a future inflationary or deflationary scenario. If the Fed is indeed successful in manufacturing a reasonable Goldilocks range of inflation then TIPS yields should once again be able to come up for air.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including TIP), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dealing Currency Drug to Export Addicts

Source: Photobucket

With the first phase of the post-financial crisis global economic bounce largely behind us, growth is becoming scarcer and countries are becoming more desperate – especially in developed countries with challenged exports and high unemployment. The United States, like other expansion challenged countries, fits this bill and is doing everything in its power to stem the tide by blasting foreigners’ currency policies in hopes of stimulating exports.

Political Hot Potato

The global race to devalue currencies in many ways is like a drug addict doing whatever it can to gain a short-term high. Sadly, the euphoric short-term benefit form lower exchange rates will be fleeting. Regardless, Ben Bernanke, the Chairman of the Federal Reserve, has openly indicated his willingness to become the economy’s drug dealer and “provide additional accommodation” in the form of quantitative easing part two (QE2).

Unfortunately, there is no long-term free lunch in global economics. The consequences of manipulating (depressing) exchange rates can lead to short-term artificial export growth, but eventually results convert to unwanted inflation. China too is like a crack dealer selling cheap imports as a drug to addicted buyers all over the world – ourselves included. We all love the $2.99 t-shirts and $5.99 toys made in China that we purchase at Wal-Mart (WMT), but don’t consciously realize the indirect cost of these cheap goods – primarily the export of manufacturing jobs overseas.

Global Political Pressure Cooker

Congressional mid-term elections are a mere few weeks away, but a sluggish global economic recovery is creating a global political pressure cooker. While domestic politicians worry about whining voters screaming about unemployment and lack of job availability, politicians in China still worry about social unrest developing from a billion job-starved rural farmers and citizens. The Tiananmen Square protests of 1989 are still fresh in the minds of Chinese officials and the government is doing everything in its power to keep the restless natives content. In fact, Premier Wen Jiabao believes a free-floating U.S.-China currency exchange rate would “bring disaster to China and the world.”

While China continues to enjoy near double-digit percentage economic growth, other global players are not sitting idly. Like every country, others would also like to crank out exports and fill their factories with workers as well.

The latest high profile devaluation effort has come from Japan. The Japanese Prime Minister post has become a non-stop revolving door and their central bank has become desperate, like ours, by nudging its target interest rate to zero. In addition, the Japanese have been aggressively selling currency in the open market in hopes of lowering the value of the Yen. Japan hasn’t stopped there. The Bank of Japan recently announced a plan to pump the equivalent of approximately $60 billion into the economy by buying not only government bonds but also short-term debt and securitized loans from banks and corporations.

Europe is not sitting around sucking its thumb either. The ECB (European Central Bank) is scooping up some of the toxic bonds from its most debt-laden member countries. Stay tuned for future initiatives if European growth doesn’t progress as optimistically planned.

Dealing with Angry Parents

When it comes to the United States, the Obama administration campaigned on “change,” and the near 10% unemployment rate wasn’t the type of change many voters were hoping for. The Federal Reserve is supposed to be “independent,” but the institution does not live in a vacuum. The Fed in many ways is like a grown adult living away from home, but regrettably Bernanke and the Fed periodically get called by into Congress (the parents) to receive a verbal scolding for not following a policy loose enough to create jobs. Technically the Fed is supposed to be living on its own, able to maintain its independence, but sadly a constant barrage of political criticism has leaked into the Fed’s decision making process and Bernanke appears to be willing to entertain any extreme monetary measure regardless of the potential negative impact on long-term price stability.

Just over the last four months, as the dollar index has weakened over 10%, we have witnessed the CRB Index (commodities proxy) increase over 10% and crude oil increase about 10% too.

In the end, artificially manipulating currencies in hopes of raising economic activity may result in a short-term adrenaline boost in export orders, but lasting benefits will not be felt because printing money will not ultimately create jobs. Any successful devaluation in currency rates will eventually be offset by price changes (inflation). Finance ministers and central bankers from 187 countries all over the world are now meeting in Washington at the annual International Monetary Fund (IMF) meeting. We all want to witness a sustained, coordinated global economic recovery, but a never-ending, unanimous quest for devaluation nirvana will only lead to export addicts ruining the party for everyone.

See also Arbitrage Vigilantes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}