Posts tagged ‘private equity’

March Madness – Dividend Grandness & Volatility Blandness

March Madness has arrived once again. This NCAA basketball event, which has been around since 1939, begins with a selection committee choosing the top 68 teams in the country. These teams are matched up against each other through a single-elimination tournament until a national champion is throned. The stock market does not have a selection committee that picks teams from conferences like the SEC, Big East, Pac-12, and ACC, but rather millions of investors select the best investments from asset classes like stocks, bonds, real estate, commodities, venture capital, and private equity.

In the investment world, there are no win-loss records, but rather there are risk-return profiles. Investors generally migrate towards the asset classes where they find the optimal trade-off between risk and return. Speculators, day-traders, and momentum traders may define risk differently, but regardless, over the long-run, capital goes where it is treated best. And over the last six years, the U.S. stock market hasn’t been a bad place to be (the S&P 500 has about tripled).

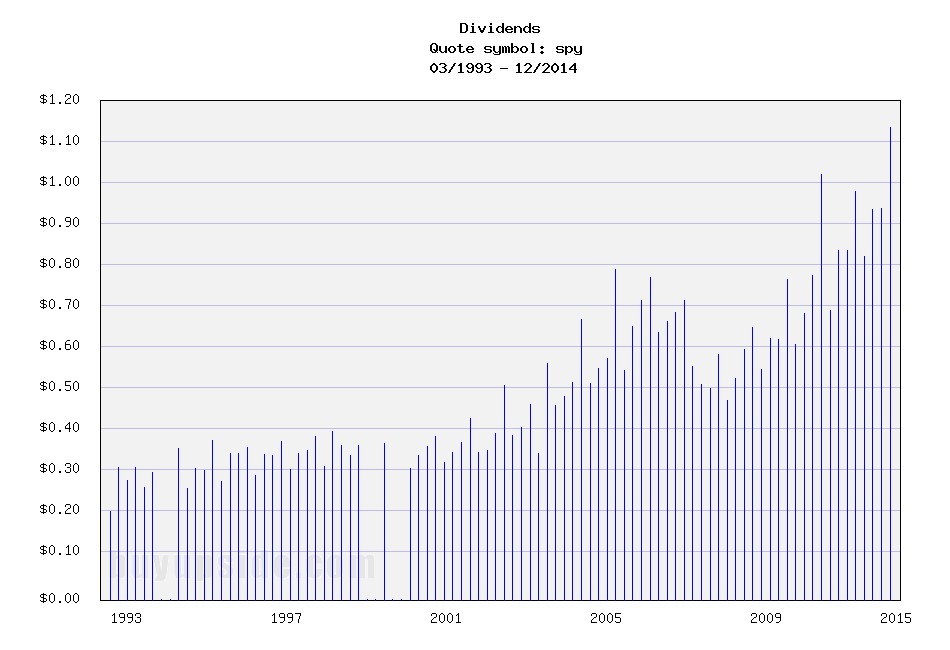

Why such outperformance in stocks? Besides a dynamic earnings recovery from the 2008-2009 financial crisis, another major factor has been the near-0% interest rate environment. When investors are earning near nothing in their bank and savings accounts, it is perfectly rational for savers to look for riskier options, if they are compensated for that risk. In addition to loose central bank and quantitative easing policies fueling demand for stocks, rising dividends have increased the attractiveness of the stock market. In fact, as you can see from the chart below, dividends have about doubled from 2008-2009 and about tripled from the year 2000.

Source: Buy Upside

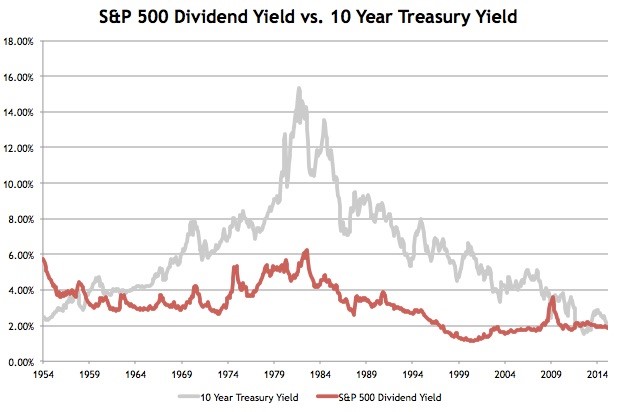

Stock prices have moved higher in concert with rising dividends, which, as you can see from the chart below, has kept the dividend yield flat at around 2% over the last few years. Treasury bond yields, on the other hand, have been on steady declining trend for the last 35 years. So, while coupons on newly issued bonds have been declining for virtually the last three and a half decades, stock dividends have been on a steadily upward moving rampage, excluding recessions (up +13% in the most recent reported period).

Source: Avondale Asset Management

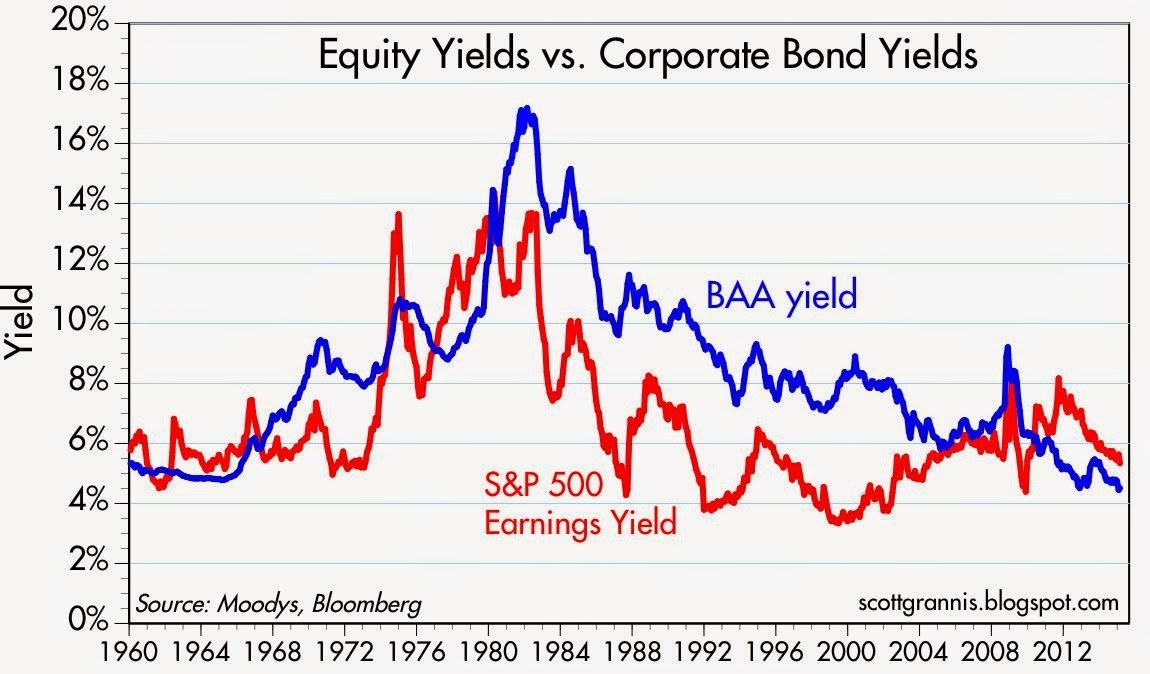

Declining interest rates have made stocks look attractive relative to investment grade corporate bonds too as evidenced by the chart below. As you can see, over the last half-century, corporate bond yields have predominantly offered higher income yields than the earnings yield on stocks – that is not the case today.

Source: Calafia Beach Pundit

What does all this stock dividend, earnings yield stuff mean? In the grand scheme of things, income starving Baby Boomers and retirees are slowly realizing that stocks in general stack up favorably in an environment in which interest payments are going down and dividend payments are going up. One of the areas highlighting the underlying demand for stocks is the Volatility Index (VIX) – a.k.a., the “Fear Gauge.” Despite Greece, Russia, ISIS, the Fed, and the Dollar dominating the headlines, the hunger for yield and growth in a declining interest rate environment is cushioning the blow during these heightened periods of volatility (see also A Series of Unfortunate Events).

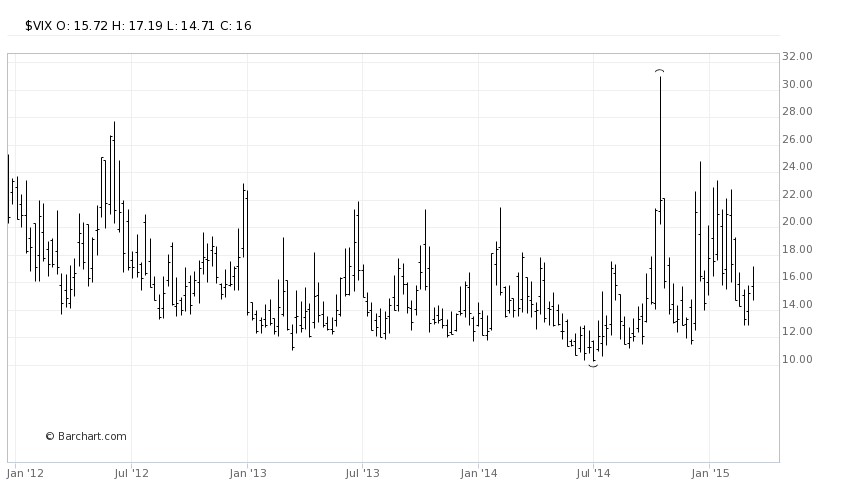

Since the end of 2011, the monthly close of the VIX has stayed above its historical average of approximately 20 only two times (see chart below). In other words, over that timeframe, the VIX has remained below average about 95% of the time. When the VIX has spiked above 20, generally it has only been for brief periods, until cooler heads prevail and bargain hunters come in to buy depressed stock bargains.

Source: Barchart

I’m not naïve enough to believe the bull market in stocks will last forever, but as long as interest rates don’t spike up and/or corporate earnings crater, underlying demand for yield should provide a floor for stocks during heightened periods of volatility. We may be in the midst of March Madness but volatility blandness is showing us that investors are paying attention to dividend grandness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

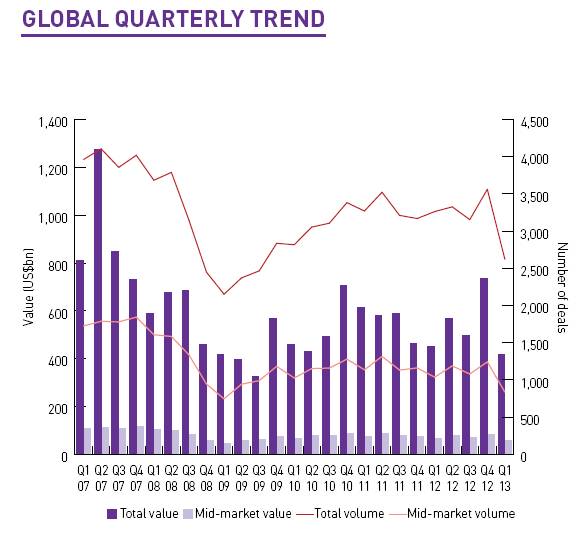

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

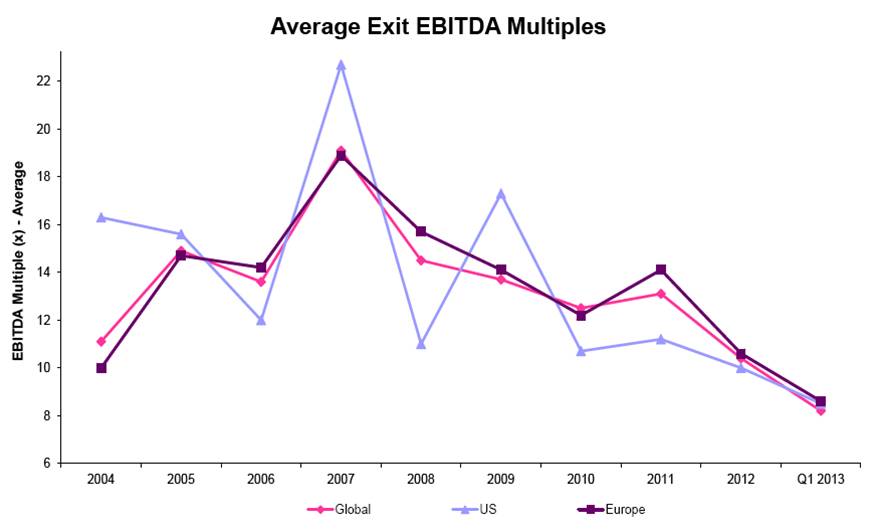

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Private Equity: Parasite or Pollinator?

In the wild, there exist both parasitic and symbiotic relationships. In the case of blood thirsty ticks that feed off deer, this parasitic relationship differs from the symbiotic association of nectar-sucking bees and pollen-hungry flowers. These are merely a few examples, but suffice it to say, these same intricate interactions occur in the business world as well.

Our economy is a complex jungle of relationships, spanning governments, businesses, consumers, investors, and many intermediaries, including private equity (PE) firms. With the November election rapidly approaching, more attention is being placed on how private equity firms fit into the economic food chain. Figuring out whether PE firms are more like profit-sucking parasites or constructive job creating mechanisms has moved to the forefront, especially given presidential candidate Mitt Romney’s past ties to Bain Capital, a successful private equity firm he founded in 1984.

Currently it is politically advantageous to portray PE professionals as greedy, job-cutting outsourcers – I’m still waiting for the political ad showing a PE worker clubbing a baby seal or plucking the legs off of a Daddy Long Legs spider. While I’d freely admit a PE pro can be just as gluttonous as an investment banker, hedge fund manager, or venture capitalist, simplistic characterizations like these miss the beneficial effects these firms provide to the overall economy. Capitalism is the spine that holds our economy together and has allowed us to grow into the greatest superpower on the planet. Private equity is but a small part of our capitalistic ecosystem, but plays a valuable role nonetheless.

While there are many perspectives on the role of private equity in our economy, here are my views on a few of the hot button issues:

Job Creation: Although I believe PE firms are valuable to our economy, I think it is a little disingenuous of Romney and his supporters to say Bain was a net “job creator” to the tune of 100,000+ jobs during his tenure. The fact of the matter is PE firms’ priority is to create profitable returns for its investors, and if that requires axing heads, then so be it – most PE firms have no qualms doing precisely that. Romney et al point to successes like Staples Inc. (SPLS), Dominos Pizza Inc. (DPZ) and Sports Authority, Inc., where profitability and success ultimately led to job expansion. From my viewpoint, I believe these examples are more the exception than the rule. Not surprisingly, any job losses executed in the early years of a PE deal will eventually require job additions if the company survives and thrives. Let’s face it, no company can cut its way to prosperity in perpetuity.

Competitveness: Weak, deteriorating, or bankrupt companies cannot and will not hire. Frail or mismanaged companies will sooner or later be forced to cut jobs on their own –the same protocol applied by opportunistic PE vultures swarming around. While PE firms typically focus on bloated or ineffective companies, I think the media outlets overemphasize the cost-cutting aspects of these deals. Sure, PE companies cut jobs, outsource functions, and cut benefits in the name of profits, but that alone is not a sustainable strategy. Trimming fat, by replacing complacent management teams, investing in modern software/equipment, expanding markets, and implementing accountability are all paramount factors in making these target companies more efficient and competitive in the long-run.

Financial Markets-Arbiter: At the end of the day, I think the IPO/financial markets are the final arbiters of how much value PE firms create, not only for investors, but also for the economy overall. If greedy PE firms’ sole functions were to saddle companies with massive debts, cut heads off, and then pay themselves enormous dividends, then there would never be a credible exit strategy for investors to cash out. If PE firms are correctly performing their jobs, then they will profitably create leaner more efficient durable companies that will be able to grow earnings and create jobs over the long-term. If they are unsuccessful in this broad goal, then the PE firm will never be able to profitably exit their investment via a corporate sale or public offering.

Bain Banter: Whether you agree with PE business practices or not, it is difficult to argue with the financial success of Bain Capital. According to a Wall Street Journal article, Bain Capital deals between 1984 – 1999 produced the following results:

“Bain produced about $2.5 billion in gains for its investors in the 77 deals, on about $1.1 billion invested. Overall, Bain recorded roughly 50% to 80% annual gains in this period, which experts said was among the best track records for buyout firms in that era.”

Critics are quick to point out the profits sucked up by PE firms, but they neglect to acknowledge the financial benefits that accrue to the large number of pension fund, charity, and university investors. Millions of middle-class American workers, retirees, community members, teachers, and students are participating in those same blood sucking profits that PE executives are slurping down.

Even though I believe private equity is a net-positive contributor to competiveness and economic growth in recent decades, there is no question in my mind that these firms participated in a massive bubble in the 2005-2007 timeframe. Capital was so cheap and abundant, prices on these deals escalated through the roof. What’s more, the excessive amounts of leverage used in those transactions set these deals up for imminent failure. PE firms and their investors have lost their shirts on many of those deals, and the typical 20%+ historical returns earned by this asset class have become long lost memories. Attractive returns do not come without risk.

With the presidential election rhetoric heating up, the media will continue to politicize, demonize and oversimplify the challenges surrounding this asset class. Despite its shortcomings, private equity will continue to have a positive symbiotic relationship with the economy…rather than a parasitic one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in SPLS, DPZ, Sports authority, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Darwin Meets Capitalism & Private Equity

Source: Photobucket

A rising discontent is spreading like wildfire in the wake of a massive financial crisis that erupted in the U.S. during 2008, and is now working its way through Europe. Irresponsible governments across the globe succumbed to the deceptive allure of leverage, and as a result racked up colossal debts and gargantuan deficits. Now governments everywhere are toggling between political gridlock and painful austerity. Citizens are feeling the pain through high unemployment, exploding education costs, crumbling social safety nets, and a general decline in the standard of living.

As a result of these dramatic changes, the contributions of capitalism are being questioned by many, whether it’s the Occupy Wall Street movement attack on the top 1%, or more recently the assault on private equity’s relevancy for a presidential candidate.

Although the media may prefer to sensationalize economic stories and tell observers, “This time is different” to boost viewership, usually the truth relies more on the nuanced evolution of issues over time. If Charles Darwin were alive today, he would understand that capitalism and democracies are evolving to massive changes in globalization, technology, and emerging markets. Darwin would appreciate the fact that capitalism can’t and won’t change overnight. Whether capitalism ultimately survives or goes extinct depends on how it adapts. Or as Darwin characterizes evolution:

It is not the strongest of the species that survives, nor the most intelligent, but the most responsive to change.

Will Capitalism Survive?

Capitalism and democracy fit like a hand in a glove, which explains why both have thrived for generations. Never mind that democracies have been around for centuries and their expansion continues unabated (see Spreading the Seeds of Democracy), nevertheless pundits feel compelled to question the sustainability of these institutions.

I guess the real response to all those experts who question the merits of capitalism is what alternative would serve us better? Would it be Socialism like we see grinding Europe to a halt? Or perhaps Communism working its wonders in North Korea and Cuba? If not that, then surely the Autocracies in Egypt and Libya are the winning formulas? The Occupy Wall Streeters may not be happy with their personal plight or the top 1%, but I don’t see them packing their bags for Greece, the Middle East or China.

There is arguably a growing disparity between rich and poor and the game of globalization is only making it more difficult for rising tides of growth to lift up our middle class. The beauty of capitalism is that money goes where it is treated best. Capitalism sucks money to the areas of the world that are the freest, most open, transparent, and practice the rule of law. Some of these components of American capitalism unquestionably eroded over the last decade or so, but the good thing is that in a democracy, citizens have the right to vote and elect growth-promoting leaders to fix problems. Growth comes from competitiveness, and competitiveness is derived from education, innovation, and pro-growth policies. Let’s hope the 2012 elections get agents of change in office.

Darwin & Private Equity

Republican Presidential primary candidate Mitt Romney has been raked over the coals for his prior professional career at private equity firm, Bain Capital. I’m convinced Charles Darwin would see private equity’s involvement as a critical factor in the process of global commerce. Businesses are like species, and only the fittest will survive.

Private equity firms prey upon weak businesses, looking to restructure and reorganize them to become more competitive. If private equity companies are bullies, then their business targets can be considered weaklings. Beating wimps into shape may not be fun to watch, but is a crucial evolutionary aspect of business. The fact of the matter is that deteriorating, uncompetitive companies cannot hire employees…only profitable, viable entities can createsustainable jobs. So our public policy officials have two choices:

• Prop up uncompetitive businesses inefficiently with tax dollars that save jobs in the short-run, but lead to bankruptcy and massive job losses in the future. Other unproductive tariffs and bailouts may garner short-term political votes, but only lead to long-term stagnancy.

OR

• Trim fat, restructure and reorganize now – similar to the swift pain experienced from extracting a rotted tooth. Jobs may be cut in the short-run, but a long-term competitively positioned company will be able to grow and create sustainable long-term jobs.

I can’t say I agree with all of private equity practices, such as leveraged recapitalizations – the practice in which private equity companies load up the target with debt so big fat dividends can be sucked out by the principals. But guess what? By doing so the principals are only reducing their own future exit value through a potential IPO (Initial Public Offering) or company sale. Moreover, if this is such an evil practice, lenders can curb the practice by simply not giving the private equity companies the needed borrowing capacity.

Capitalism and its private equity subset have gotten quite a bad rap lately, but I believe these forces are essential aspects for the rising standards of living for billions of people across the planet. When first introduced, Charles Darwin’s theory of evolution by natural selection was critically examined by many non-believers. Although capitalism will be forced to adapt to an ever-changing world and its merits have been questioned too, the chances of capitalism going extinct are about as likely as the extinction of Darwin’s evolutionary theory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity: Hitting Maturity Cliff

Photo source: 1Funny.com

Wow, those were the days when money was as cheap and available as that fragile, sandpaper-like toilet paper you find at gas stations. Private equity took advantage of this near-free, pervasive capital and used it to the greatest extent possible. The firms proceeded to lever up and gorge themselves on a never-ending list of target companies with reckless abandon (see also Private Equity Shooting Blanks). Now the glory days of abundant, ultra-cheap capital are history.

Rather than rely on low-cost bank debt, private equity firms are now turning to the fixed income markets – specifically the high yield market (a.k.a. junk bonds). As The Financial Times points out, more than $170 billion of junk bonds have been issued this year, in large part to refinance debt issued in the mid-2000s that has gone sour due to overoptimistic projections and a flailing U.S. economy. In special instances, private equity owners are fattening their own wallets by declaring special dividends for themselves.

Even though some of these over-levered, private equity portfolio companies have received a temporary reprieve from facing the harsh economic realities thanks to these refinancings, the cliff of maturing debt in 2012 is fast approaching. Some have estimated that $1 trillion in maturing debt will roll through the market in the 2012-2014 timeframe. Either the economy (or operating performance) improves enough for these companies to service their debt, or these companies will find themselves falling off these maturity cliffs into bankruptcy.

Junk is Not Risk-Free

Driving this trend of loan recycling is risk aversion to stocks and a voracious appetite for yield in a yield desert. Stuffing the money under the mattress, earning next to nothing on CDs (Certificates of Deposit) and money market accounts, will not help in meeting many investors’ long-term objectives. The “uncertain uncertainty” swirling around global equity markets has nervous investors flocking to bonds. The opening of liquidity in the high yield markets has served as a life preserver for these levered companies desperate to refinance their impending debt. This high-yield debt refinancing window is also an opportunity for companies to lower their interest expense burden because of the current, near record-low interest rates.

But as the name implies, these “junk bonds” are not risk free. For starters, embedded in these bonds is interest rate risk – with a Federal Funds rate at effectively zero, there is only one upward direction for interest rates to go (bad for bond prices). In addition, credit risk is a concern as well. In the midst of the financial crisis, many of these high-yield bonds corrected by more than -40% from their highs in 2008 until the bottom achieved in early 2009. If the economy regresses back into a double-dip recession, many of these bonds stand to get pummeled as default rates escalate (see also, bond risks).

Pace Not Slowing

Source: Dealogic via WSJ

Does the appetite for high yield appear to be slowing? Au contraire. In the most recent week, Dealogic noted $15.4 billion in junk bonds were sold. The FT sees the pace of junk deals handily outpacing the record of $185.4 billion set in 2006.

The Wall Street Journal used the following deals to provide a flavor of how companies are using high-yield debt in the present market:

“First Data Corp. sold $510 million of 10-year notes this week, at 9.125%, to pay down bank debt due in 2014. Peabody Energy sold $650 million of 6.5%, 10-year notes to pay off the same amount of higher-priced debt due in three years. MultiPlan Inc., a health-care cost-management provider, sold $675 million of notes this week, at 9.875%, to help fund a buyout of the company. Cott Corp., a maker of store-branded soft drinks, sold $375 million of debt at 8.125% to fund its purchase of another company, Cliffstar Corp.”

The roads on the junk bond highway appear to be pothole free at the moment, however a cliff of debt is rapidly approaching over the next few years, so high-yield investors should travel carefully as conditions in the junk market potentially worsen. As we witnessed in 2008-2009, it can take a while to hit rock bottom in the riskier areas of the credit spectrum.

Read full Financial Times and Wall Street Journal articles on the high yield market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including HYG and JNK), but at the time of publishing SCM had no direct position in First Data Corp., Peabody Energy (BTU), MultiPlan Inc., Cott Corp. (COT), Cliffstar Corp., or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Buy-Out Firms Shooting Blanks

Photo source: Photobucket

During the golden age of the mega-buyouts in the mid-2000s, when banks were lending like drunken sailors, and private equity firms were taking the practically free funding to shoot at almost every company in sight, it’s no wonder managers of these funds were “high-fiving” each other. Unfortunately for the participants, the music ended in 2007, and the heavy debt-loaded guns that previously were killing large elephant deals got replaced with harmless toy guns shooting blanks at phantom transactions.

Peter Morris, a former Morgan Stanley (MS) banker and author of the scornful report, “Private Equity, Public Loss,” took a critical eye at the industry pointing to the reasons these high risk-taking private equity firms are underperforming the S&P 500 significantly. Bolstering his underperformance assertions, Morris points to 542 deals in the Yale endowment that underperformed by -40% once fees were subtracted. The Center for the Study of Financial Innovation, which is affiliated with Morris, cites a 2005 paper by Steven Kaplan (University of Chicago), and Antoinette Schoar (Massachusetts Institute of Technology). The paper shows the average buy-out fund underperformed the S&P 500 index from 1980 – 2001.

Another factor that Morris feels should not be ignored relates to risk. Morris feels the excessive risk profiles associated with these private equity funds have not been adequately considered by many unknowing investors and public taxpayers. Pensioners are vulnerable to these underperforming, risk-adjusted returns, while unassuming taxpayers could also be on the hook if risky private equity bets go bad. Under certain scenarios these potentially rocky private equity investments could bring a financial institution to its knees and force governments to use taxpayer bailout money. The Financial Times features a $6.5 billion investment made by Terra Firma, which was subsequently written down to zero, to make its point about the inherent risk private equity plays in the overall financial system.

Heads We Win, Tails You Lose

What makes the purported underperformance more scathing is the fact that these funds should bear higher returns to compensate investors for the additional liquidity risk and leverage that is undertaken. Like hedge funds, most private equity funds charge a 2% management fee, and a 20% performance fee for results achieved above a certain hurdle rate. The problem, that many outside observers highlight, is that the private equity firms have very little skin in the game, for example as little as 2%. With not a lot of their own dough in the game, the fund managers have a built in incentive to swing for the fences, because a profit windfall will filter to them should they hit it big. Morris characterizes this conflict of interest as “heads we win, tails you lose.” Another knock against investors revolves around return calculations. The opacity surrounding returns makes private equity less attractive, since valuations are only truly accurately reflected upon sale, which often takes many years.

Have all these shortcomings scared off investors? Apparently not. Just recently Blackstone Group (BX) raised a new $13.5 billion fund, the firm’s 6th fund, fresh off of its 5th fund that raised a total of $20 billion. The focus of the new fund will be on Asia and North America. In the short-run, Europe will occupy less of the fund’s attention until the region’s economy recovers.

To the extent more of these studies garner traction, I’m sure the private equity industry will react with a forceful response, especially with billions in potential fees at stake. One thing is for sure, investors have become more demanding and shrewd post the financial crisis, so if private equity managers want to earn the rich fees of yesteryear, they will need to do better than shoot blanks.

Read The Financial Times Buy-Out Study Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MS, BX, Terra Firma or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity Sitting on Stuffed Wallet

The clock is ticking and private equity (PE) firms need to put some $445 billion in their wallets to work. Otherwise, the dreams of outsized returns and hefty fees will have to wait for another Golden Era of deal making. Why such a hurry to use the cash? According to Andrea Auerbach, a Managing Director at Cambridge Associates, “Most funds legally have five or six years to invest that capital…it’s use it or lose it.”

Shop ‘til Wallet Drops

As easy as it sounds, spending half a trillion dollars can be difficult. Here’s how IBD’s Norm Alster characterizes the challenge:

“To realize the outsize profits investors expect, private equity firms would have to borrow two or three times that amount. But for the most part, credit spigots for such deals are still dry. At the same time, pinning down buyout targets is not that easy. Many potential sellers are balking at parting with corporate assets in the midst of a serious downturn.”

The 2010 private equity environment is quite a bit different than the LBO boom era from a handful of years ago, as you can see from the chart below. Thanks to cheap, free-flowing funding from the banks, $1.4 trillion worth of deals were consummated in 2006 and 2007, including large deals like First Data Corp. ($27 billion deal – KKR); Alltel ($28 billion – Goldman Sachs/ Texas Pacific Group); and Harrah’s ($30 billion – Apollo Management/Texas Pacific Group). Unfortunately, deals done during this period were done when valuations and leverage were at extremely high historical levels.

Chart source: Thomson Reuters via IBD

Deal Timeout

What’s causing the current dearth of deals? In many instances, business owners have not calibrated valuation expectations downward enough to account for the bruising financial crisis. Given the 77 leveraged buyout defaults in 2009, investors have become more reticent in committing capital as well. Refinancing the mountains of debt associated with the troubled 2006-07 vintage of deals will require patience and creative financing skills from the banks.

Because of the logjam of deals created by the financial crisis, PE firms are actively looking for exit strategies relating to their portfolio companies. Since private equity inherently involves illiquid investments, typically the industry creates liquidity through initial public offerings (IPOs), merger & acquisitions, and/or recapitalization structures that partially or fully return investor capital.

If the economic malaise lingers and valuations remain depressed, I have no doubt owners will eventually return to the negotiating table while waving a white towel in hand. Until then, private equity firms will continue begging for capital from the banks (i.e., using “other peoples’ money”) and beating down sellers into submission with regards to price expectations. If PE firms are not successful in using that wad of cash by the end of the fund’s term, then investors will be free to walk away with their money without paying lucrative fees to the PE firms.

Don’t Forget Benefits

The PE field is facing its fair share of trials and tribulations, but PE’s diversification benefits should not be forgotten. The success of the “Yale Model,” implemented by David Swensen, has come under attack with the recent bursting of the credit bubble, but with the ever-swinging performance pendulum of various asset classes/styles moving in and out of favor, I am confident a consistent strategy integrating PE as a portion of a diversified portfolio will yield respectable risk-adjusted returns over the long-run. Like other areas in the financial services industry, fees are being scrutinized and transparency requests by investors (limited partners) have been on the rise. But first things first – before attractive PE profits can be made as part of a diversified portfolio, the wad of cash in the wallets of PE firms must find a home in portfolio companies.

Read Norm Alster’s full IBD article originally referenced on TRB

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in GS, Harrah’s or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}