Posts tagged ‘presidential elections’

Groundhog Day All Over Again

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2016). Subscribe on the right side of the page for the complete text.

It’s that time of the year when the masses gather in eager anticipation of Groundhog Day to predict whether the furry rodent will see its shadow in 2016, thereby extending winter for an additional six weeks.

In the classic movie Groundhog Day, actor Bill Murray plays character Phil Connors, an arrogant, self-centered TV weatherman who, during an assignment covering the annual Groundhog Day event in Punxsutawney, Pennsylvania, finds himself stuck in a time loop, repeating the same day over and over. With a feeling of nothing to lose, Phil repeatedly decides to indulge in reckless hedonism and criminal behavior. After being resigned to perpetually reliving the same day forever, Phil begins to re-examine his life and falls in love with his co-worker Rita Hanson (see scene here). Ultimately, Phil’s pure focus on the important priorities of life allows himself to break the painful monotonous time loop and win Rita’s love.

Stock market investors are lining up in a similar fashion to predict whether the financial winter experienced in January will persist through the rest of the year. The groundhog, equipped with a thick fur coat, certainly would have been more optimally prepared for the icy January financial market conditions. More specifically, the S&P 500 index declined -5.1% for the month and the Dow Jones fell -5.5%.

Unfortunately for many investors, they too have been trapped in a never-ending news cycle, which painfully buries the public with a monotonous loop of daily pessimistic headlines. As a result of the eternally distorted media cycle, many investors have lost sight of important priorities like Phil Connors. Since the beginning of 2011, the investors who have endured the relentless wave of media gloom have been handsomely rewarded. From 2011-2016, the S&P 500 stock index has ascended approximately 54%, even after accounting for the significant January 2016 decline.

Unless you were burrowed in a hole like a groundhog, you will probably recognize a number of these ominous headlines spanning across the 2011 – 2015 headlines:

- 2011: Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% correction)

- 2012: Arab Spring/Greek “Gr-Exit” Fears (-11% correction)

- 2013: Fed Taper Tantrum (-8% correction)

- 2014: Ebola Outbreak (-10% correction)

- 2015: China Slowdown Fears (-13% correction)

Similar to the Groundhog Day movie, the headlines of 2016 match the tone and mood we’ve seen in recent years. Here’s an abbreviated list of the recurring worries-du-jour in January:

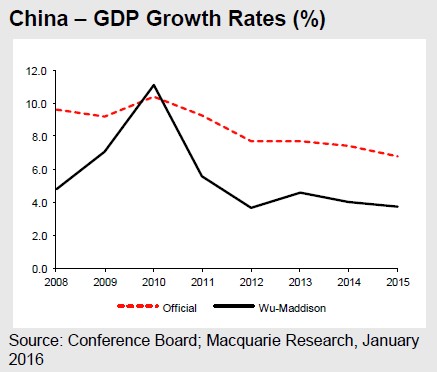

China Slowdown: Is this something new? As you can see from the chart below, China has been slowing since 2010. Due to the law of large numbers, and as the second largest economy on the globe, it is natural to see such an enormous economic engine eventually slow. Rather than panic over China’s slowing, observers should be applauding. China’s Q4 GDP growth recently came in at +6.8%, almost 10x the level recorded by the U.S. in Q4 (+0.7%). Even if you mistrust the official Chinese government’s reported data, our economy would kill for the still impressive independently reported growth statistics (see chart below). While the concerted effort of the political regime to migrate the country from an export-driven economy to a consumption-based one has caused some growing pains, nevertheless in recent months we have seen China report record automobile purchases, retail sales, oil consumption, and industrial production.

Rise of the U.S. Dollar: This is a legitimate concern that has had tangible negative impacts on the U.S. economy. As you can see from the chart below (blue line), in less than one year, the value of the U.S. dollar spiked by approximately +25%. If you are a multinational company exporting a product to Europe for $100, and consumers wake up a year later having to pay $125 for the same product, it should come as no surprise to anyone that this phenomenon is squeezing profits. The good news is that U.S. corporations have already absorbed the worst of this currency pain dating back to early 2015, so if the stabilizing foreign exchange trends remain near current levels, as they have over the last year, there should be no additional economic drag.

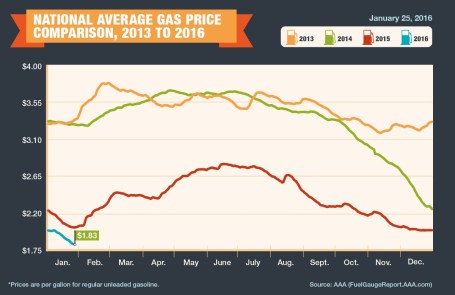

Oil Prices Down: Somehow the U.S. media is trying to convince the public that lower oil prices are bad for the economy. Yes, it is true, the financial restructurings and lost jobs associated with oil price declines will hurt the economy and the banks overall. However, the benefits of lower oil prices on the broader economy (i.e., more money in consumers’ pockets) is unambiguously positive and will overwhelm any indirect damage. Every penny decrease in gasoline prices (now roughly $1.83 per gallon nationally) equates to about a $1 billion tax cut for consumers (see chart below). Many people are worried about oil prices being a signal of weakness, but if you look at the last few recessions, they were all preceded by an oil price spike, not a price collapse.

Source: AAA

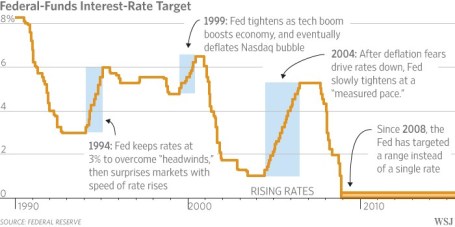

Federal Reserve Monetary Policy: The first interest rate hike in nine years took place in 2015, but that did not prevent investors from fretting about the timing of the next interest rate hike. As I’ve written many times (see Fed Fatigue Setting In), the Fed has barely budged its target rate to 0.375%, so this is much to do about nothing. Wake me up when we get to 2.00%, at which point we will still be far below the long-term average but at a more meaningful level (see chart below).

Source: The Wall Street Journal

Presidential Elections: Congress’s approval rating is abysmal, but like it or not, primary season is just starting and we are stuck in a presidential election cycle until the second Tuesday of November. Guess what? If you want to know the impact of the elections on the financial markets, then I will give you the short answer…it just does not matter who gets elected. History shows us that the markets go up and down under both Republican and Democratic parties. If you are comparing the track record on the political parties’ track record on debt creation, it is a mixed bag as well (see chart below). Arguably, in half the cases, the nomination of the Federal Reserve chairs will have as large (or larger) an impact than the elected president. If you were to factor in the inevitable splits in Congress to the equation, the result is gridlock. I have contended for some time that gridlock is a positive outcome because it structurally forces a lid on disciplined government spending (see Who Said Gridlock is Bad?). If this isn’t a good enough explanation, see Barry Ritholtz’s take on the subject of politics and the stock market…I couldn’t sum it up any better (click here)

Source: Calafia Beach Pundit

Fortunately for groundhogs, and long-term investors, dealing with challenging and volatile climates is nothing new. Both burrowing marmots and emotional investors need to adapt to ever-changing environments…sunny or overcast. In addition to a cold 2016 start, January was also a chilly month in 2014 and 2015, with the S&P 500 down -3.6% and -3.1%, respectively. Despite this seasonal sour sentiment, there is a silver lining. In both instances (2014 & 2015), the market rebounded significantly in subsequent months after the slow start at the beginning of the year. For the remainder of the year, the S&P advanced +15.5% in 2014, and +2.5% in 2015.

In Groundhog Day the movie, Bill Murray relived the same day over and over again, and repeated the same missteps until he learned from his mistakes. Long-term investors will be served best by applying this same philosophy to their investments. Like a groundhog, investors have a tendency to become scared of their own shadows. It’s easy to succumb to the infinite time loop of worrisome headlines, but rather than burrowing away in hibernation, creating a diversified, low-cost, tax-efficient portfolio customized for your specific time horizon, risk tolerance, and liquidity needs is a better way of celebrating this year’s Groundhog Day.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Autumn, Elections and Replacement Refs

Article is an excerpt from previously released Sidoxia Capital Management’s complementary October 1, 2012 newsletter. Subscribe on right side of page.

As September has come to a close, the grand finale of our annual seasons has commenced… autumn. How do we know autumn is here? Well, for starters, the leaves are changing colors; the weather is about to cool; and the NFL replacement referees are watching Sunday football games from their couches.

While 2012 is split into quarters, football games and investment seasons are also divided into four quarters. Right now, the economic fourth quarter has just started and the home team is winning. As we can see from the stock market scoreboard, the S&P 500 index is up +15% this year (+6% in Q3) and the NASDAQ index has catapulted +20% through September (+6% also in Q3). The U.S. home team is winning, but a fumble, blocked kick, or interception could mean the difference between an exciting win and a devastating loss.

Another game divided into four parts is the game of presidential politics. However, presidential elections are divided into four years – not four quarters. Five weeks from now, we’ll find out if our Commander in Chief Obama will get to lead our team for another game lasting four years, or whether backup quarterback Mit Romney will be called into the game. The fans are getting restless due to anemic growth and lingering joblessness, but for now, the coach is keeping the president in the starting lineup. Both President Obama and Governor Romney will take some head-to-head practice snaps against each other in the first of three scheduled presidential debates beginning this week.

Bernanke Changes Rules

The New York Jets have Tim Tebow for their secret weapon (1 for 1 yesterday!), and the United States economy has Ben Bernanke. Although our home team may be winning, it has required some monetary rule-changing policies to be instituted by Federal Reserve Chairman Ben Bernanke to keep our team in the lead. Just a few weeks ago, Mr. Bernake instituted QE3 (3rd round of quantitative easing), which is an open-ended mortgage buying program designed to lower home buying interest rates and stimulate the economy (see Helicopter Ben to QE3 Rescue). The short-term benefits of the $40 billion monthly bond buying binge are relatively clear (lower borrowing costs for homebuyers), but the longer-term costs of inflation are stewing patiently on the backburner.

Source: Calafia Beach Pundit (Scott Grannis)

As you can see from the chart above, August median home prices are up +10% for existing single-family homes over the last year. Housing affordability is at extremely attractive levels, and although the bank loan purse strings are tight, a modest loosening is beginning to unfold.

Economy Playing Injured

Our starters may still be playing, but many are injured, just like the jobless are limping through the employment market. Encouragingly, although unemployment remains stubbornly high, the number of people collecting unemployment checks is a lot lower (-1.25 million fewer than a year ago). Not great news, but at least we are hobbling in the right direction (see chart below).

Source: Calafia Beach Pundit (Scott Grannis)

Time for Fiscal Cliff Hail Mary?

If a team is losing at the end of a game, a “Hail Mary” pass might be necessary. We are quickly nearing this fiscal Armageddon situation as the approximately $700 billion “fiscal cliff” (a painful combo of spending cuts and tax hikes) kicks in at the end of the year (see PIMCO chart below via The Reformed Broker).

Running trillion dollar deficits in perpetuity is not a sustainable strategy, so for most people, a combination of spending cuts and/or tax hikes makes sense to narrow the gap (see chart below). Last year’s recommendations from the bipartisan Simpson-Bowles commission, which were ignored, are not a bad place to start. What happens in the lame-duck session of Congress (after the elections) will dramatically impact the score of the current economic game, and decide who wins and who loses.

Source: Calafia Beach Pundit (Scott Grannis)

Heated debates continue on how the gap between expenses and revenues will be narrowed, but regardless, Democrats will continue to push for capital gains tax hikes on the rich (see tax chart below); and the Republicans will push to cut spending on entitlements, including untenable programs like Medicare and Social Security.

Source: The Wall Street Journal

The game is not quite over, but the fourth quarter promises to be a bloody battle. So while the replacement refs may be back at home, the experienced returning refs have been known to blow calls too. Let’s just hope that autumn, the season of bounteous fecundity, ends up being a continued trend of sweet market success, rather than a political period of botched opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}