Posts tagged ‘Politics’

The Rocket Science of Investing – Armageddon Yet to Arrive

In the face of an incredibly scary global pandemic, the stock market completed a phenomenal year (S&P 500 rocketed +27%) closing at a new all-time monthly record high, after also posting incredible results in 2020 (+16%) and 2019 (+29%). Naturally, the follow-on question I get most is, “What about next year?” And to this question, I annoyingly provide the same answer as the most successful long-term investor of all-time, Warren Buffett, “I have no idea.”

But with that said, despite lacking the skill of 100% clairvoyance, my investment firm Sidoxia Capital Management and our strategies have performed quite well over the long-run for numerous reasons. As it turns out, the power of compounding, coupled with low-cost, tax-efficient investing can produce quite spectacular results. Throw in some good stock picking, and that is frosting on a cake recipe of success. Thank you Amazon.com Inc. +5,544%, Apple Inc. +2,394%, and Alphabet Inc. 880%, among many other fruitful investments since Sidoxia’s inception in 2008.

Lessons Learned Over 30 Years

I’ve been doing this thing called investing for about three decades now and I’ve learned a few things over the years, most prominently that investing is not rocket science. Warren Buffett has correctly described investing as similar to dieting. In other words, both are easy to understand but difficult to execute because they require discipline.

If you want your investments to succeed, consider some of these investing nuggets:

- Invest for the Long-Run: Markets move in all directions, but if you can avoid myopia and short-termism, you will be much better positioned for investment success.

- Avoid Investment Fads: Invest where you get the most bang for your buck – stick to sound investments selling at reasonable prices. Stay away from expensive, speculative, frothy areas, or at least keep that exposure of your portfolio to a minimum.

- Turn off the TV and Silence your Phone: Regardless of what you hear, the world is not ending. COVID, inflation, and Federal Reserve monetary policies may dominate the headlines du jour but this is nothing new. The stock market has increased more than 7-fold in value since the 2009 stock market lows, even in the face of many frightening news stories (see Ed Yardeni’s list of panic attacks since 2009).

- Understand Stock Prices Do Go Down: We have been spoiled in recent years with above-average returns, but that does not mean you need to panic when prices do decline or that you need to try to time the market. There can be years when stock prices do not appreciate (reference the post-2000 and post-2008 periods), however, those who wisely rebalanced and dollar-cost-averaged positions in their portfolio were handsomely rewarded for their discipline and patience over the long-run.

- Volatility Can Be a Good Thing: Periods of volatility offer you the ability to rebalance your portfolio and take advantage of opportunities that disruption creates.

- Optimize Your Investments Based on Your Time Horizon and Risk Tolerance: At Sidoxia, we customize investment portfolios to meet our clients’ unique circumstances and risk appetite. It’s important to have your investments diversified across a broad array of asset classes in a low-cost, tax efficient manner.

- Get Assistance: If you don’t have the time, discipline, or interest to manage your investments, find an experienced professional who is a fiduciary (i.e., someone who legally places your interests first) and implements time-tested investment strategies. Sidoxia should be able to assist you in identifying an appropriate investment manager. 😉

What Now for 2022?

As I made clear earlier, at Sidoxia, we do not attempt to predict the directions of markets, but rather we look to opportunistically take advantage of many different dynamic areas that we believe provide the best risk-adjusted return potential for our clients.

However, although we freely admit we are not Nostradamus, we do closely follow a wide spectrum of areas in financial markets to best position our investments. Here are some thoughts on some hot-button issues that are top-of-mind as we enter 2022.

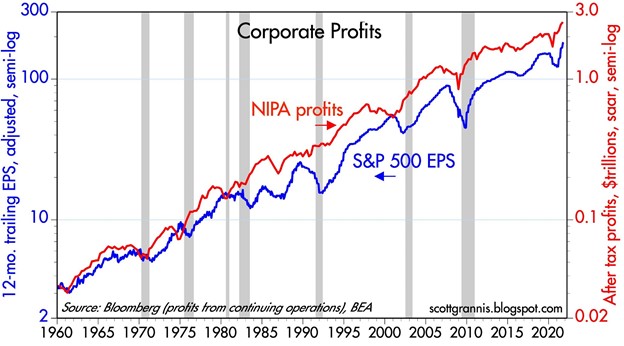

Stocks Remain Attractive: Stocks are still attractively priced broadly considering where interest rates stand today. Most people don’t realize that stock prices are actually cheaper today than they were a year ago because earnings will be up roughly +50% in 2021 (see chart below) and stock prices are only up +27%. Stated differently, the price of the market as measured by the forward price-earnings ratio (P/E) has declined, even though the stock market has melted up. Under a different lens, stocks are also attractively priced if you consider bonds are generally yielding 1-2% versus the 4-5% on stocks as measured by the earnings yield of the S&P 500 index (corporate earnings/price of the index), which can be calculated as an inverse P/E ratio. Regardless, if stock prices do indeed decline this year, while bond yields remain in the same general ballpark, then stocks will only become even more attractive.

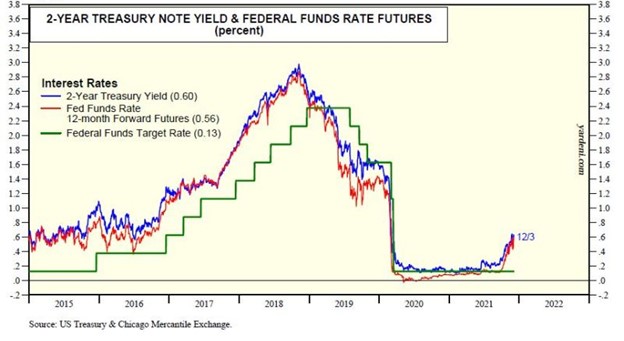

Federal Reserve Tightening Doesn’t Mean Game Over for Stocks: We have seen this movie before (see chart below). What happened the last time quantitative easing (QE) stopped and the Fed raised its Federal Funds interest rate target? Ten-year interest rate yields went down, and stock prices went up – not necessarily immediately, but ultimately investors were compensated for not knee-jerk selling.

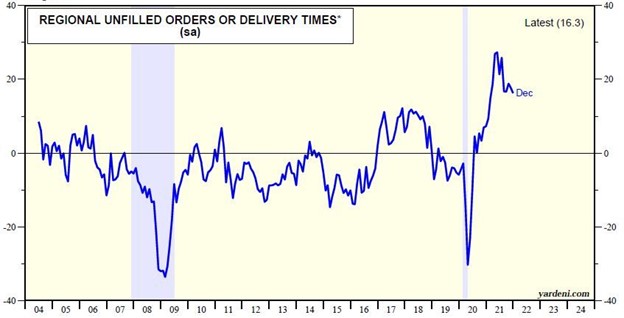

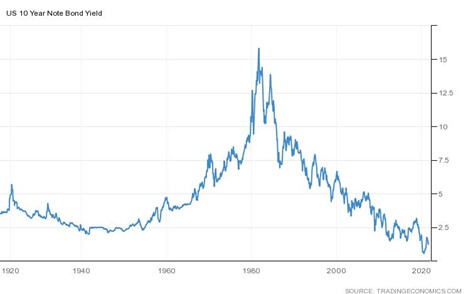

Inflation Does Not Appear to Be Spiraling Out of Control: Just take a look at the paltry yield of the 10-year Treasury Note, currently at 1.51%. And please do not just consider the low interest rates here in the U.S., but also internationally in markets like Germany with negative 10-year interest rates (-0.18%) or near-0% interest rates in Japan (0.07%). If inflation were indeed considered a systemic risk, global yields in large developed markets would not be hovering around 0%. Furthermore, COVID-related supply chain bottlenecks appear to be abating. As you can see from the chart below, the average business delivery times have been coming down in recent months as supply disruptions subside – an improving trend for overall prices.

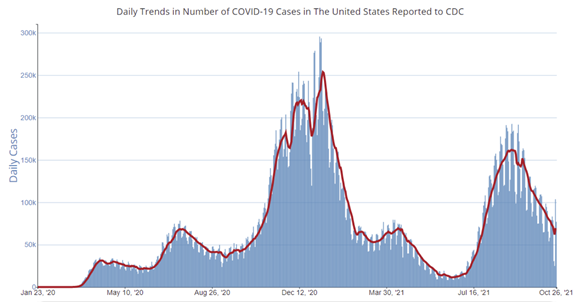

The Global Pandemic Deserves Watching: There are plenty of reasons to remain concerned, however science and natural immunity may have brought us closer to neutralizing this health crisis. A worldwide focus on creating vaccines, antiviral drugs, monoclonal antibodies, and other COVID treatments has allowed the global health community to more effectively treat those infected with COVID, while simultaneously lowering the number of related hospitalizations and deaths. There is even hope for areas that have lower vaccination rates than the U.S., for example India (see chart below), which you can see has experienced a dramatic fall-off in COVID cases in part because of the large number of previous infections and subsequent natural immunity created.

There are always talking heads and so-call pundits predicting Armageddon in the stock market, but as you can see from the facts presented, record highs in the stock market aren’t currently painting this picture for 2022. Profits have been gargantuan, interest rates remain near generational lows, valuations remain reasonable, and there are reasons to be optimistic regarding the COVID pandemic. Investing is never easy, but it is not rocket science, if you remain disciplined and patient. Follow this advice and your portfolio should benefit in 2022 and beyond.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 3, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ohhh Omicron! From Panic to Possibility

If you have recovered from your Thanksgiving turkey and stuffing food coma, you have probably woken up to the sound of a new health scare alarm …Omicron. Where does the name Omicron come from, and why is it named after a Greek alphabet letter? The short answer is the system was created to avoid public confusion with complicated scientific names (e.g., B.1.1.529) and also to mitigate the stigma assigned to a region of origination. Apparently, Spaniards weren’t happy with the name “Spanish Flu” and China didn’t appreciate the “Wuhan Virus” moniker. More specifically, Omicron is the new COVID variant originating from South Africa and believed to be more contagious than other forms of COVID, albeit potentially not as severe.

I am not an epidemiologist and also not a COVID expert, but I do know it is a little early to panic over something scientists have not fully researched with fewer than 100 identified cases as of last week. The good news is that early data is showing mild symptoms in infected individuals and the vast majority of these people impacted by Omicron have been unvaccinated (87%), therefore implying the vaccines are indeed providing protection.

Omicron isn’t the first COVID variant and will likely not be the last. Like the flu, which produces new strains every year, new COVID strains such as Omicron are likely to surface on a regular basis. Luckily, our country is home to the world’s most prolific vaccine makers and reformulated boosters are likely to be a common staple in our healthcare regimen. In fact, the CEO of Pfizer, Inc. (PFE) believes it’s possible to have an Omicron vaccine in 100 days, if needed.

Even if Omicron ends up spreading faster than other variants like Alpha, Beta, Gamma, Delta, Lambda, Mu, and Nu, our healthcare system is much better equipped to deal with Omicron compared to previous pandemic variants. Not only do we have access to the strongest supply of vaccines on the planet, but the United States also has built a stronger testing infrastructure (the CDC shows more than 13 million tests conducted over the last week, excluding California). What’s more, pharmaceutical companies have created very effective therapeutics, including Paxlovid, a game-changing antiviral pill manufactured by Pfizer. The recent Paxlovid trial conducted in combination with the antiviral drug ritonavir showed a reduction in hospitalization and deaths by -89%.

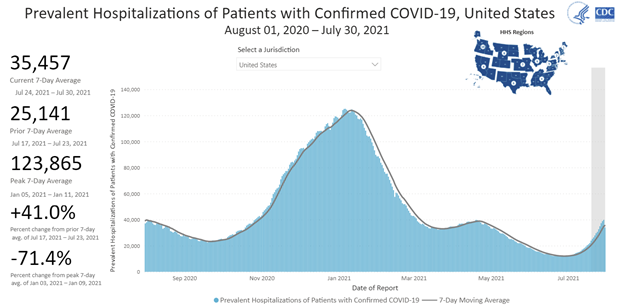

Another fortunate aspect to this new variant is that the rise of Omicron is occurring amidst an improving backdrop of plummeting hospitalizations and COVID-related deaths here in the U.S. (deaths after the recent surge are down more than -50%).

Markets Remain Near Record Highs

With all these scary Omicron headlines, one would expect a collapse in equity markets. Well, at least not yet. The S&P 500 was actually down less than -1% for the month and remains up a whopping +22% for 2021 (see 5-year chart above). And the tech-heavy NASDAQ index did even better, closing slightly higher for the month and up a similar amount for the year (+21%).

Driving the buoyant stock market performance this year, on the heels of a strong stock market last year (S&P 500 climbed +16%), has been the surge in corporate profits (see chart below). As I like to point out to investors, over the long-run, stock prices follow the direction of earnings, whether we are talking about the overall stock market or individual stocks. Although prices and earnings have both moved up and to the right, neither prices nor profits move in a straight line. One must assume price volatility (i.e. risk) if you want to experience the reward (i.e., long-term returns that substantially beat inflation).

Other Flies in the Ointment

Besides Omicron, there are still some prominent flies in the ointment. Federal Reserve Chairman Jerome Powell just signaled to Congress yesterday that the Fed’s reduction in its bond-buying stimulus program (i.e., “tapering”) could finish a few months early. In other words, the Fed could remove the punch bowl sooner than anticipated – perhaps by as early as this March. Subsequent to the completion of the tapering, industry observers now expect a greater than 50% probability for the first interest hike to occur by June 2022.

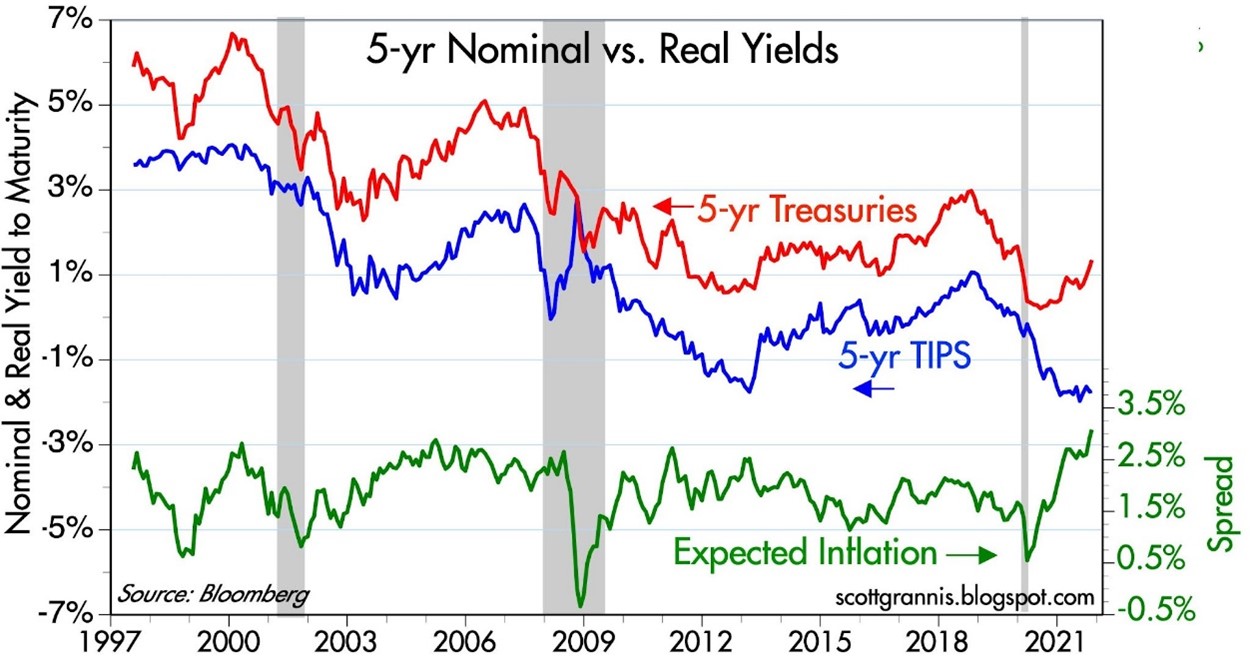

If this is not enough to ruffle your post-Thanksgiving feathers, then consider the threat of persistent inflation. Even Fed Chair Powell threw in the towel by officially removing the word “transitory” from his description of inflation. Inflation is not exploding to the double-digit extremes of the 1980s, but as you can see from the chart below (green line), five-year inflation expectations now exceed 3%.

Lastly, the other date to mark on your December calendar, besides the Christmas holiday, is the 15th because that is the date Congress could hit the debt ceiling limit. This high-stakes game of chicken occurs every year or so. This contest between Democrats and Republicans is used as a negotiating tool in the hopes of advancing political agendas. If an agreement is not reached to increase the debt limit, a government shutdown, and then ultimately a government default would transpire. History tells us this will never happen, but the mere game of political brinksmanship could rattle markets in the short-run.

All these risks and fears are nothing new. Financial markets have flourished in the face of worse crises than Omicron, monetary policy changes, inflation, and debt ceilings. The key to sustainable wealth creation is taking a long-term view and being opportunistic in the face of volatility. Shrewdly pivoting your perspective from panic to possibility is essential on the path to prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No Red Blood, Just Green Flood

Normally, investors equate the month of October with scary, blood-curdling screams because horrifying losses during the 1929 and 1987 crashes occurred during this month. Fortunately, for those invested in stocks, they experienced the opposite this last month – a flood of green (new all-time record highs), despite a whole host of frightening factors, including the following:

· Inflation

· Supply chain disruptions

· Federal Reserve monetary policy

· COVID variants

· Evergrande’s impact on China and commercial real estate

· Cryptocurrency volatility

· Expanding government deficits and debt (stimulus/infrastructure)

· Government debt ceiling negotiations

· Declining corporate profit margins

· Meme stocks

· And more…boo!

Even though this Halloween season has introduced these many spooky fears, investors still experienced a sugar-high during October. More specifically, the S&P 500 catapulted +6.9% this month (+22.6% Year-to-Date), Dow Jones Industrial Average +5.8% (+17.0% YTD); and NASDAQ +7.3% (+20.3% YTD). With the COVID Delta variant subsiding (see chart below), economic activity rising (Q4 GDP is estimated at +4.8%), and corporate profits going gang busters (33% growth and 84% of corporations are beating Q3 estimates), it should come as no surprise that stock market values continue to rise.

As I mention regularly to my readers, there is never a shortage of things to worry about when it comes to your investments, money, and savings. Emotions tend to highjack rational reasoning as non-existent boogeymen scare people into do-nothing decision-making or suboptimal choices. Investing for the long-run requires dedication and discipline, and if you do not have the time and fortitude to do so, it behooves you to find an experienced, independent professional to assist you.

Rather than getting spooked by supply chain fears and inflation plastered all over the newspapers and media outlets, the real way to compound wealth over the long-term is to do what Warren Buffett says, and that is “buy fear, and sell greed.” Unfortunately, our Darwinian instincts embedded in our DNA are naturally designed to do the contrary…”buy greed, and sell fear.” The goal is to buy low and sell high (not buy high and sell low).

Yes, it’s true that over the last year, semiconductor lead times have almost doubled to 22 weeks, and Chinese container shipping costs have about increased 10-fold to over $20,000 (see charts below). However, the economic laws of supply and demand remain just as true today as they did in 1776 when Adam Smith wrote Wealth of Nations (see also Pins, Cars, Coconuts & Chips). Chip makers are building new fabs (i.e., manufacturing plants) and worker shortages at the ports and truck driver deficiencies are slowly improving. Supply scarcity and higher prices may be with us for a while, but history tells us betting against capitalism isn’t a wise decision.

Not worrying about all the economic goblins and witches can be difficult when contemplating your investments and savings. Nevertheless, as I have consistently reminded my investors and readers, the key pillars to understanding the health of the investment environment are the following (see also The Stool):

· Interest rates

· Earnings (Corporate profits)

· Valuations (How cheap or expensive is the market?)

· Sentiment (How greedy or fearful are investors?)

The good news is that a) interest rates are near historically low levels; b) corporate profits are on a tear (+33% as mentioned above); c) valuations have come down because profits have grown faster than stock price appreciation; and d) sentiment remains nervous (a good thing) as measured by the massive inflows going into low (negative) yielding bonds. If you consider all these elements, one should not be surprised that we are at-or-near all-time record highs. Obviously, these investment pillars can reverse directions and create headwinds for investors. Until then, don’t be startled if there is more green flood rather than red blood.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sleeping on Expensive Financial Pillows

Everybody loves a good night’s sleep and that requires a comfortable pillow. Unfortunately, many investors are overpaying for their pillows in the form of overpriced, interest-rate sensitive bonds. If you aren’t careful, your retirement dreams could turn into financial nightmares. More specifically, if the composition of your investment portfolio is overly skewed towards bonds, you stand to lose substantial amounts of money if/when interest rates and inflation persistently increase.

In the short-run, pillows manufactured in the form of bonds can feel cozy in a world of low volatility and generationally-low interest rates. However, investors should also ask themselves, how much longer can this unprecedented 40-year bull market in bonds last? Interest rates approached 20% in 1980 and they stand closer to 1% today (1.24% to be more precise). What may now seem like a cozy bond portfolio may eventually lead to unnerving insomnia.

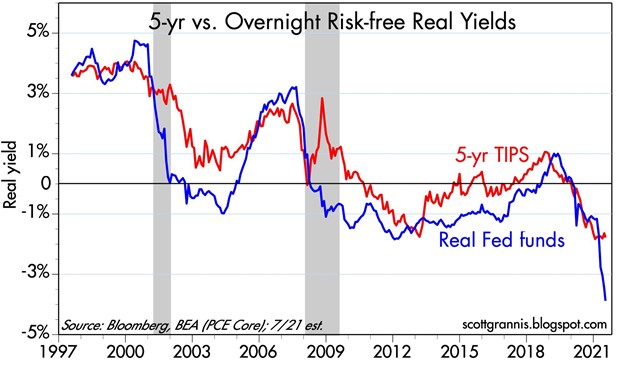

We already have negative interest rates in numerous countries around the world and inflation (a rise in general price levels) is running hot at about 5% annually. What this means is investing in a 10-Year Treasury Note yielding 1.24% effectively means you are losing almost -4% per year in purchasing power, if inflation remains at 5% (see chart below). There are numerous investing strategies used to fight inflation, but historically stocks’ ability to raise prices through pricing power has been a useful vehicle to fend off the melting of money’s value.

Despite short-term increases in inflation, getting a good night sleep hasn’t been an issue in 2021 as it relates to the stock market. For the month, the S&P 500 stock index was up +2.3% to a new record, and for the year it has surged +17%. The story for the Dow Jones Industrial Average looks similar – for the month rising +1.3% and year-to-date to +14%.

Thankfully, there haven’t been any night terrors yet either in the bond market. Nevertheless, short-term results have been more of a mixed bag. For the month, the iShares Aggregate Bond Market ETF (Exchange Traded Fund – AGG) rose +1.0% and for 2021 slipped -2%.

In spite of stocks being a great place to invest over the last decade or so, solely investing in stocks is not always rainbows and unicorns. The price you pay for longer-term stock outperformance is shorter-term volatility, which can be disruptive to your sleeping patterns. Case in point, the -35% drop in the S&P 500 index at the start of the COVID-19 global pandemic when anxiety and volatility were at extreme levels.

Despite the market continuously hitting new highs, investors are not completely out of the woods yet as spiking Delta variant cases threaten the trajectory of the current economic recovery.

Although stocks can feel like stiff, uncomfortable pillows in the short-term, in the long-run, historically those stiff, uncomfortable stocks become vastly more comfortable than bonds. Over the last five years, stock prices have dramatically outperformed bonds by +99% (S&P vs. AGG).

Determining your asset allocation is a monumental decision that should be driven by various factors, including risk tolerance, time horizon, income needs, taxes, and other factors such as your personal objectives. Therefore, even if you subscribe to the premise that stocks outperform in the long run, that doesn’t necessarily mean all retirees should load up solely on a diet of stocks.

Retirees who need income or other risk-averse investors generally can’t afford to lose substantial amounts of their net worth, if stocks tank significantly during a recession. Not only could an all-stock portfolio not generate adequate income, an equity-heavy portfolio could also could lead to emotional sales after market declines, thereby locking in permanent losses at low levels. After these potential losses, there may not be enough time for stock losses to be recouped by retirees. If possible, most investors approaching retirement do not want to be forced to work as a greeter at Wal-Mart to compensate for stock losses.

Everybody’s financial situation is different, and everyone has varying risk tolerances and unique needs. As such, working with an independent, experienced, and professional advisor like Sidoxia Capital Management (www.Sidoxia.com) can assist you with structuring a proper asset allocation, so your investment pillows can help you achieve a good night sleep.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Politics & COVID Tricks

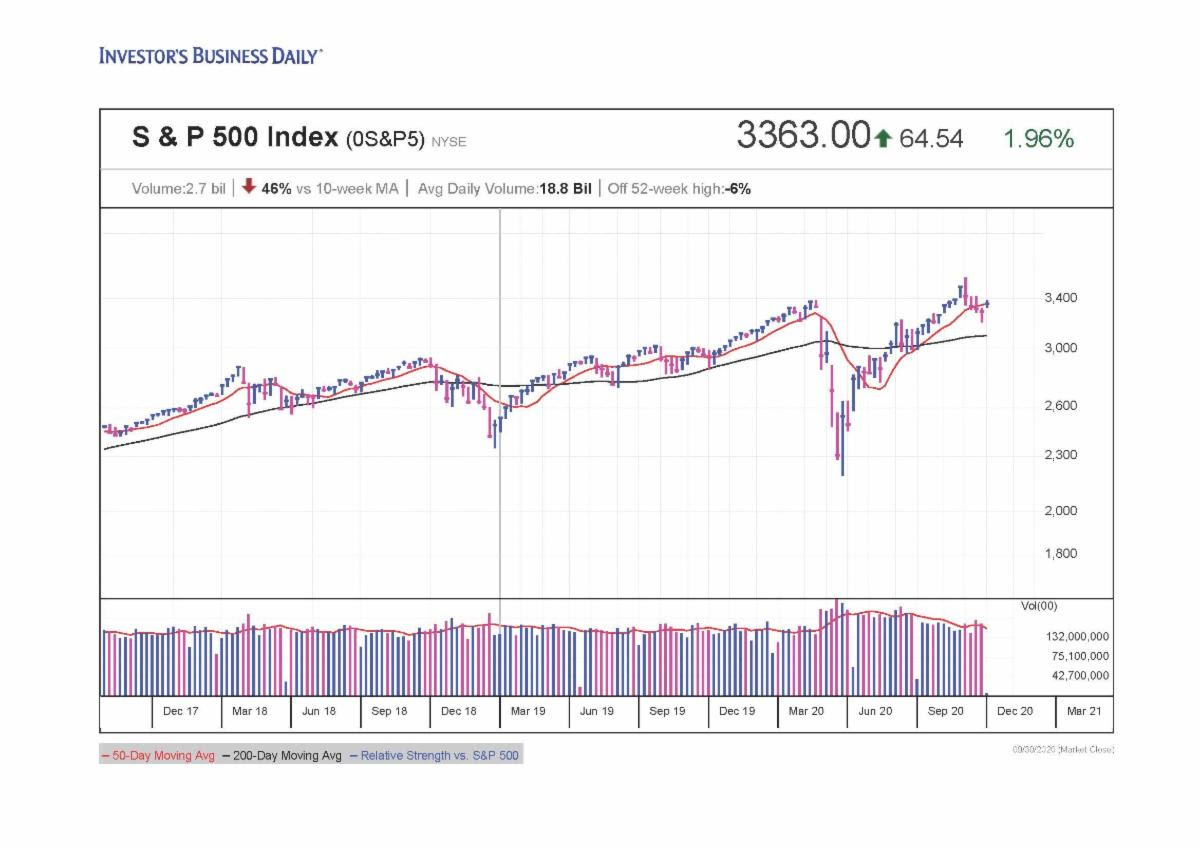

Thanks to a global epidemic, trillions of dollars instantly disappeared during the first quarter of this year, and then, abracadabra…the losses turned into gains and magically reappeared in the subsequent two quarters. After a stabilization in the spread of the COVID-19 virus earlier this year, the stock market rebounded for five consecutive months, at one point rebounding +64% (from late March to early September) – see chart below. However, things became a little bit trickier for the recent full month as concerns heightened over the outcome of upcoming elections; uncertainty over a potential coronavirus-related stimulus package agreement; and fears over a fall resurgence in COVID-19 cases. Although the S&P 500 stock index fell -3.9% and the Dow Jones Industrial Average slipped -2.3% during September, the same indexes levitated +8.5% and +7.6% for the third quarter, respectively.

Source: Investors.com

Washington Worries

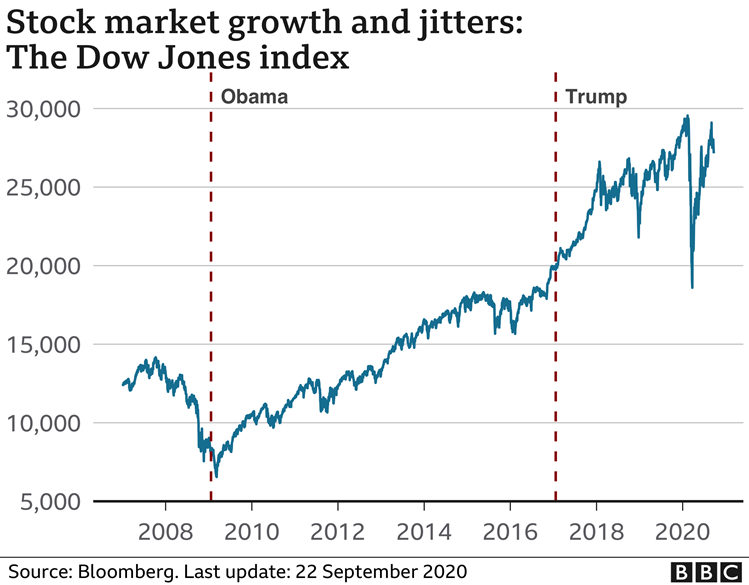

Anxiety over politics is nothing new, and as I’ve written extensively in my Investing Caffeine blog, history teaches us that politics have little to do with the long-term performance of the overall stock market (e.g., see Politics & Your Money). Nobody knows with certainty how the elections will impact the financial markets and economy (myself included). But what I do know is that many so-called experts said the stock market would decline if Barack Obama won the presidential election…in reality the stock market soared. I also know the so-called experts said the stock market would decline if Donald Trump won the presidential election… in reality the stock market soared. So, suffice it to say, I don’t place a lot of faith into what any of the so-called political experts say about the outcome of upcoming elections (see the chart below).

COVID Coming Back?

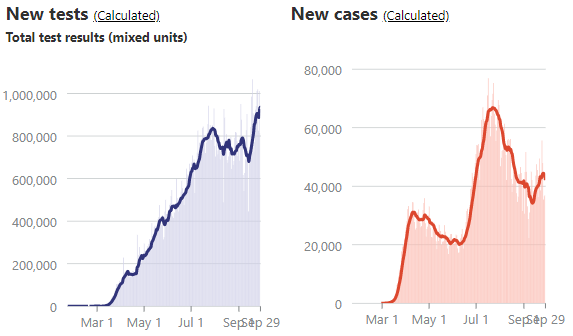

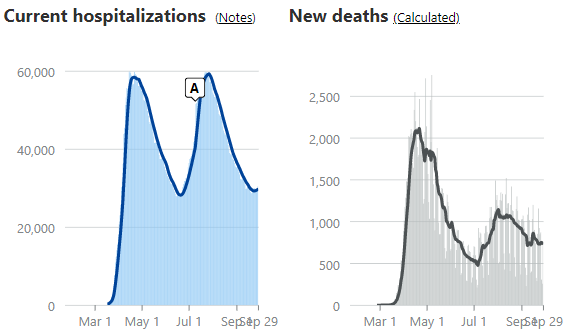

One of the reasons stock prices have risen more than 50%+ is due to a stabilization in COVID-19 virus trends. As you can see from the charts below, new tests, hospitalizations, and death rates are generally on good trajectories, according to the COVID Tracking Project. However, new COVID cases have bumped higher in recent weeks. This recent, troubling trend has raised the question of whether another wave of cases is building in front of a dangerous, seasonally-cooler fall flu season. Traditionally, it’s during this fall period in which contagious viruses normally spread faster.

Source: The COVID Tracking Project

Regardless of the trendline in new cases, there is plenty of other promising COVID developments to help fight this pandemic, such as the pending approvals of numerous vaccines, along with improved therapies and treatments, such as therapeutics, steroids, blood thinners, ventilators, and monoclonal antibodies.

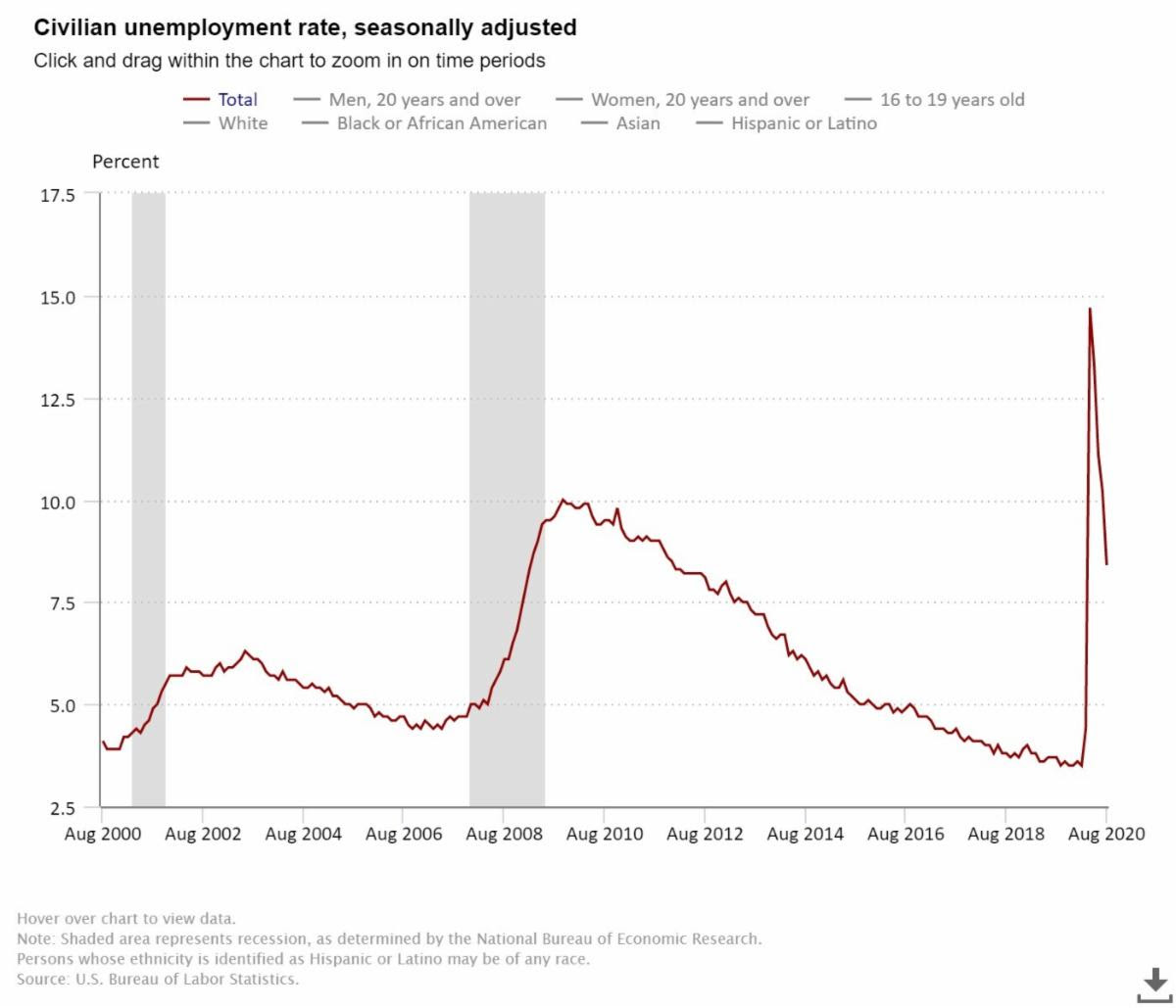

Business Bounce

From the 10,000-foot level, despite worries over various political outcomes, the economy is recovering relatively vigorously. As you can see from the chart below, the rebound in employment has been fairly swift. After peaking in April at 14.7%, the most recent unemployment rate has declined to 8.4%, and a closely tracked ADP National Employment Report was released yesterday showing a higher than expected increase in new private-sector monthly jobs (749,000 vs. 649,000 median estimate).

Source: U.S. Bureau of Labor Statistics

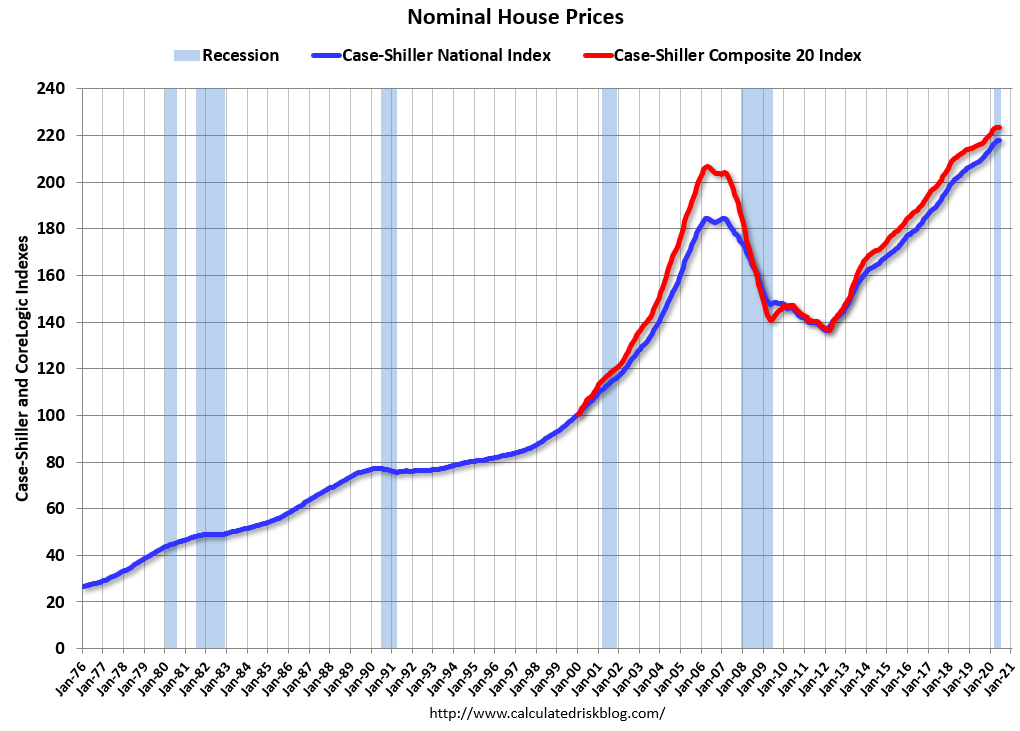

From a housing perspective, house sales have been on fire. Record-low interest rates, mortgage rates, and refinancing rates have been driving higher home purchases and rising prices. Urban flight to the suburbs has also been a big housing tailwind due to the desire for more socially distanced room, additional home office space, and expansive backyards. Adding fuel to the housing fire has been record low supply (i.e., home inventories). The robust demand is evident by the record Case-Shiller home prices (see chart below).

Source: Calculated Risk

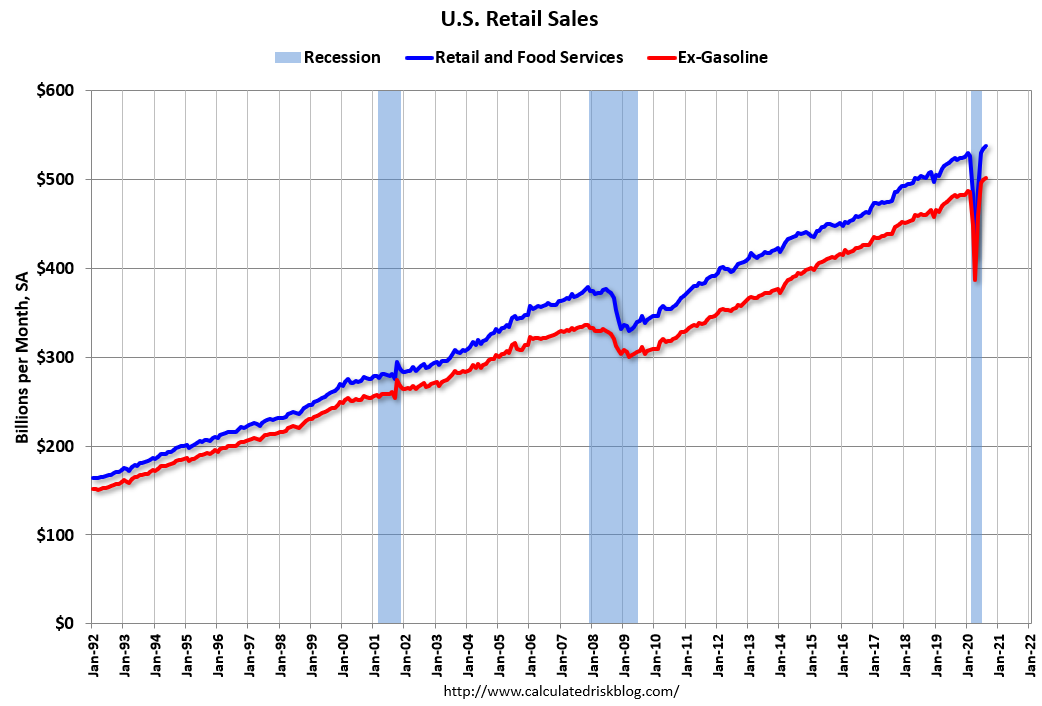

There are plenty of industries hurting, including airlines, cruise lines, hotels, retailers, and restaurants but the economic rebound along with government stimulus (i.e., direct government checks and unemployment relief payments) have led to record retail sales (see chart below). Spending could cool if an additional coronavirus-related stimulus package agreement is not reached, but until the government checks stop flowing, consumers will keep spending.

Source: Calculated Risk

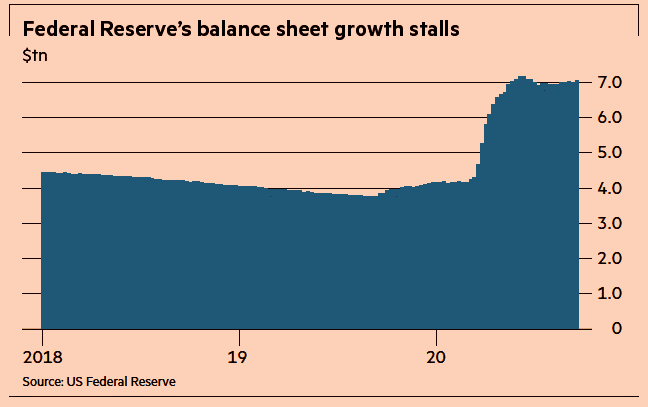

Besides trillions of dollars in fiscal relief injected into the economy, the Federal Reserve has also provided trillions in unprecedented relief (see chart below) through its government and corporate bond buying programs, in addition to its Main Street Lending Program.

Source:The Financial Times

There has been a lot of political hocus pocus and COVID smoke & mirrors that have much of the population worried about their investments. In every presidential election, you have about half the population satisfied with the winner, and half the population disappointed in the winner…this election will be no different. The illusion of fear and chaos is bound to create some short-term financial market volatility over the next month, but behind the curtains there are numerous positive, contributing factors that are powering the economy and stock market forward. Do yourself a favor by focusing on your long-term financial future and don’t succumb to politics and COVID tricks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFS), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Missing the Financial Forest for the Political Trees

In the never-ending, 24/7, polarizing political news cycle, headlines of Ukraine phone calls, China trade negotiations, impeachment hearings, presidential elections, Federal Reserve monetary policy, and other Washington based stories have traders and news junkies glued to their phones, Twitter feeds, news accounts, blog subscriptions, and Facebook stories. However, through the incessant, deafening noise, many investors are missing the overall financial forest as they get lost in the irrelevant D.C. details.

Meanwhile, as many investors fall prey to the mesmerizing, but inconsequential headlines, financial markets have not fallen asleep or gotten distracted. The S&P 500 stock market index rose another +1.7% last month, and for the year, the index has registered a +18.7% return. As we enter the volatile fourth quarter, many stock market participants remain shell-shocked from last year’s roughly -20% temporary collapse, even though the S&P 500 subsequently rallied +29% from the 2018 trough to the 2019 peak.

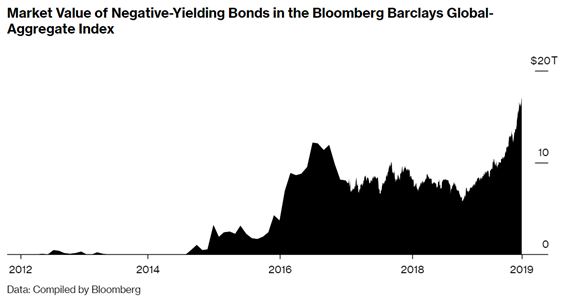

Why are many people missing the financial forest? A big key to the significant rally in 2019 stock prices can be attributed to two words…interest rates. Unlike last year’s fourth quarter, when the Federal Reserve was increasing interest rates (i.e., tapping the economic brakes), this year the Fed is cutting rates (i.e., hitting the economic accelerator). Interest rates are a key leg to Sidoxia’s financial four-legged stool (see Don’t Be a Fool, Follow the Stool). Interest rates are at or near generational lows, depending where on the geographic map you reside. For example, interest rates on 10-year German government bonds are -0.55%. Yes, it’s true. If you were to invest $10,000 in a negative yielding -0.55% German bond for 10-years starting in 2019, if you held the bond until maturity (2029), the investor would get back less than the original $10,000 invested. In other words, many bond investors are choosing to pay bond issuers for the privilege of giving the issuers money for the unpalatable right of receiving less money in the future.

The unprecedented negative-yielding bond market is reaching epic proportions, having eclipsed $17 trillion globally (see chart below). This gargantuan and growing dollar figure of negative-yielding bonds defies common sense and feels very reminiscent of the panic buying of technology stocks in the late 1990s.

Source: Bloomberg

At Sidoxia Capital Management, we are implementing proprietary fixed income strategies to navigate this negative interest rate environment. However, the plummeting interest rates and skyrocketing bond prices only make our bond investing job tougher. On the other hand, declining rates, all else equal, also make my stock-picking job easier. Nevertheless, many market participants have gotten lost in the financial trees. More specifically, investors are losing sight of the key tenet that money goes where it is treated best (go where yields are highest and valuations lowest). With many bonds yielding low or negative interest rates, bond investors are being treated like criminals forced to serve jail time and pay large fines because future returns will become much tougher to accrue. In my Investing Caffeine blog, I have been writing about how the stock market’s earnings yield (current approximating +5.5%) and the S&P dividend yield of about +1.9% are handily outstripping the +1.7% yield on the 10-Year Treasury Note (see Going Shopping: Chicken vs. Beef ).

Unless our economy falls into a prolonged recession, interest rates spike substantially higher, or stock prices catapult appreciably, then any decline in stock prices will likely be temporary. Fortunately, the economy appears to be chugging along, albeit at a slower rate. For instance, 3rd quarter GDP (Gross Domestic Product) estimates are hovering around +2.0%.

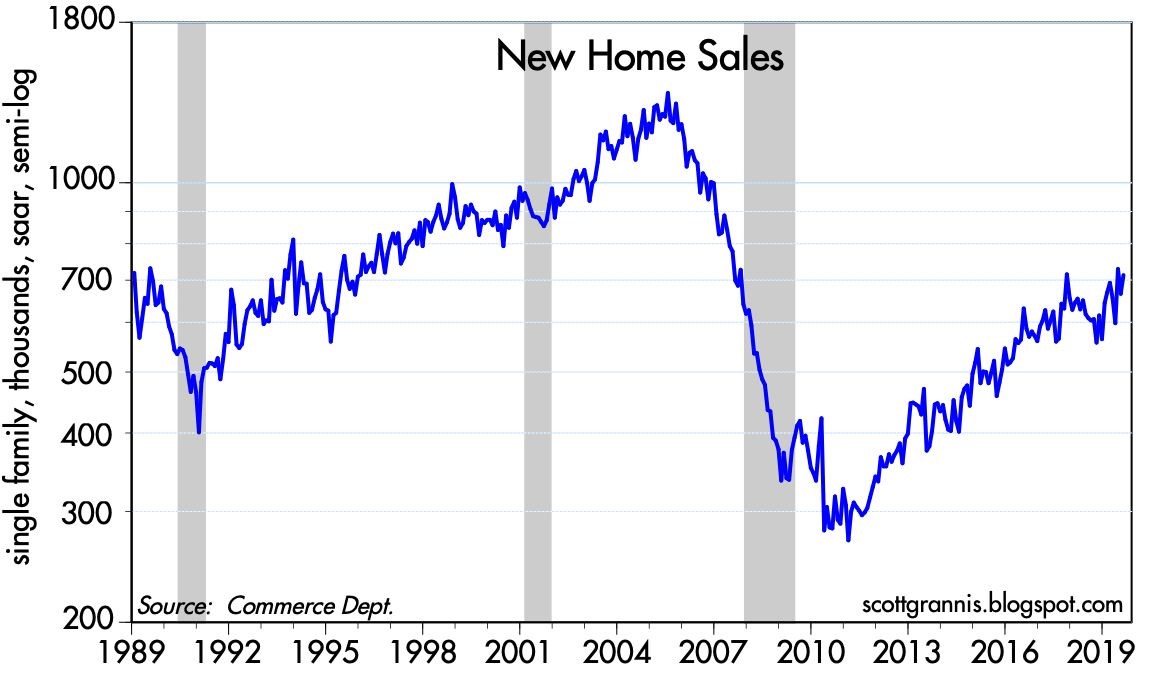

Low Rates Aid Housing Market

Thanks to low interest rates, the housing markets remain strong. As you can see from the chart below, new home sales continue to ratchet higher over the last eight years, and lower mortgage rates are only helping this cause.

Source: Calafia Beach Pundit

The same tailwind of lower interest rates can be seen below with rising home prices.

Source: Calculated Risk

Consumer Flexes Muscles

At 3.7%, the unemployment rate remains low and the number of workers collecting unemployment is near multi-decade lows (see chart below).

Source: Calafia Beach Pundit

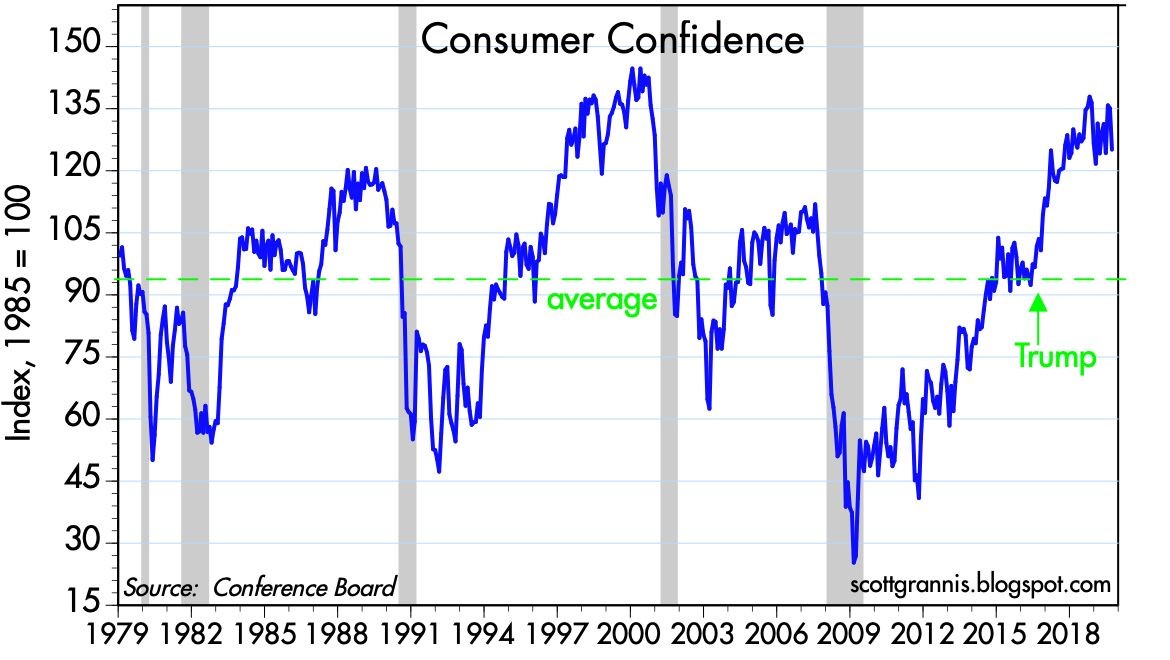

It should come as no surprise that the more employed workers there are collecting paychecks, the more consumer confidence will rise (see chart below). As you can see, consumer confidence is near multi-decade record highs.

Source: Calafia Beach Pundit

Although politics continue to dominate headlines and grab attention, many investors are missing the financial forest because the political noise is distracting the irrefutable, positive effect that low interest rates is contributing to the positive direction of the stock market and the economy. Do your best to not miss the forest – you don’t want your portfolio to suffer by you getting lost in the trees.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

March Madness Leads to Gladness

As usual, there was plenty of “madness” in March, and this year did not disappoint. Just as is the case with the annual NCAA basketball tournament, certain investors suffered the agony of defeat in the financial markets, but overall, the thrill of victory triumphed in March. So much so that the S&P 500 index posted its largest first-quarter gain in more than 20 years. Not only did the major indexes post gains for the month, but the winning record looks even better for the year-to-date results. For 2019, the S&P 500 index is up +13.1%; the Dow Jones Industrial Average +11.2%; and the tech-heavy NASDAQ index +16.5% for the year. The monthly gains in the major indexes were more muted, ranging from 0% for the Dow to +2.6% for the NASDAQ.

Busy? Listen to Wade discuss this article and other topics each week on the Weekly Grind podcast:

While 2018 ended with a painful injury (S&P 500 -6.2% in Q4), on fears of a deteriorating China trade deal and a potentially overly aggressive Federal Reserve hiking interest rates, the stock market ultimately recovered in 2019 on changing perceptions. Jerome Powell, the Federal Reserve Chairman, indicated the Fed would be more “patient” going forward in increasing interest rates, and President Trump’s tweet-storm on balance has been optimistic regarding the chances of hammering out a successful trade deal with China.

With the new cautious Fed perspective on interest rates, the yield on the 10-Year Treasury Note fell by -0.28% for the quarter from 2.69% to 2.41%. In fact, investors are currently betting there is a greater than 50% probability the Fed will cut interest rates before year-end. Moreover, in testimony before Congress, Powell signaled the economic dampening policy of reducing the Fed’s balance sheet was almost complete. All else equal, the shift from a perceived rate-hiking Fed to a potentially rate-cutting Fed has effectively turned an apparent headwind into tailwind. Consumers are benefiting from this trend in the housing market, as evidenced by lower 30-year fixed mortgage rates, which in some cases have dropped below 4%.

Economy: No Slam Dunk

However, not everything is a slam dunk in the financial markets. Much of the change in stance by the Fed can be attributed to slowing economic growth seen both here domestically and abroad, internationally.

Here in the U.S., the widely followed monthly jobs number last month only showed a gain of 20,000 jobs, well below estimates of 180,000 jobs. This negative jobs surprise was the biggest miss in more than 10 years. Furthermore, the overall measure for our nation’s economic activity, growth in Gross Domestic Product (GDP), was revised downward to +2.2% in Q4, below a previous estimate of +2.6%. The so-called “inverted yield curve” (i.e., short-term interest rates are higher than long-term interest rates), historically a precursor to a recession, is consistent with slowing growth expectations. This inversion temporarily caused investors some heartburn last month.

If you combine slowing domestic economic growth figures with decelerating manufacturing growth in Europe and China (e.g. contracting Purchasing Managers’ Index), then suddenly you end up with a slowing global growth picture. In recent months, the U.S. economy’s strength was perceived as decoupling from the rest of the world, however recent data could be changing that view.

Fortunately, the ECB (European Central Bank) and China have not been sitting on their hands. ECB President Mario Draghi announced three measures last month that could cumulatively add up to some modest economic stimulus. First, it “expects the key ECB interest rates to remain at their present levels at least through the end of 2019.” Second, it committed to reinvesting all maturing bond principal payments in new debt “for an extended period of time.” And third, the ECB announced a new batch of “Targeted Long-Term Refinancing Operations” starting in September. Also, Chinese Premier Li Keqiang announced the government will reduce taxes, primarily Value Added Taxes (VAT) and social security taxes (SST). Based on the rally in equities, it appears investors are optimistic these stimulus efforts will eventually succeed in reigniting growth.

Volume of Political Noise Ratcheted Higher

While I continually try to remind investors to ignore politics when it comes to their investment portfolios, the deafening noise was especially difficult to overlook considering the following:

- Mueller Report Completed: Robert Mueller’s Special Counsel investigation into potential collusion as it relates Russian election interference and alleged obstruction of justice concluded.

- Michael Cohen Testifies: Former President Trump lawyer, Michael Cohen, testified in closed sessions before the House and Senate intelligence committees, and in public to the House Oversight Committee. In the open session, Cohen, admitted to paying hush money to two women during the election. Cohen called President Trump a racist, a conman, and a cheat but Cohen is the one heading to jail after being sentenced for lying to Congress among other charges.

- Manafort Sentenced: Former Trump Campaign Chairman Paul Manafort was sentenced to prison on bank and tax fraud charges.

- North Korea No Nuke Deal: In geopolitics,President Trump flew 21 hours to Vietnam to meet for a second time with North Korean leader Kim Jong Un on denuclearization of the Korean peninsula. The U.S. president ended up leaving early, empty handed, without signing an agreement, after talks broke down over sanction differences.

- Brexit Drama Continues: The House of Commons in the lower house of the U.K. Parliament continued to stifle Prime Minister Theresa May’s plan to exit the European Union with repeated votes rejecting her proposals. Brexit outcomes remain in flux, however the European Union did approve an extension to May 22 to work out kinks, if the House can approve May’s plan.

Positive Signals Remain

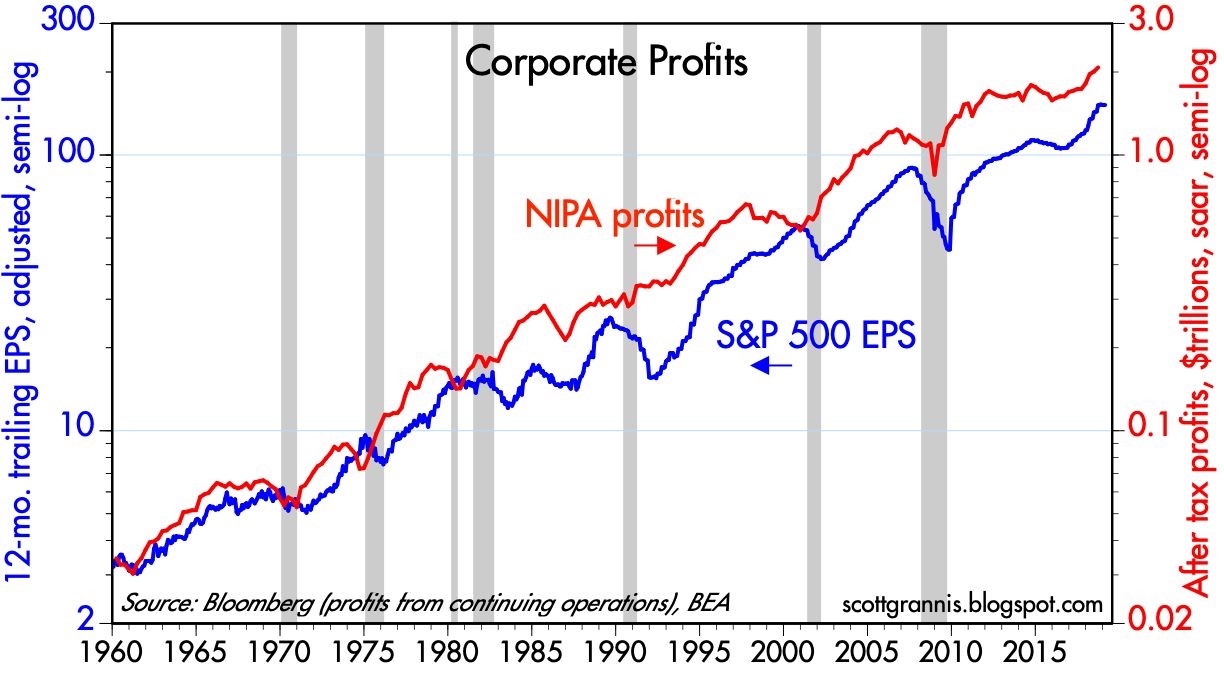

March Madness reminds us that a big lead can be lost quickly, however a few good adjustments can also swiftly shift momentum in the positive direction. Although growth appears to be slowing both here and internationally, corporate profits are not falling off a cliff, and earnings remain near record highs (see chart below).

Source: Calafia Beach Pundit

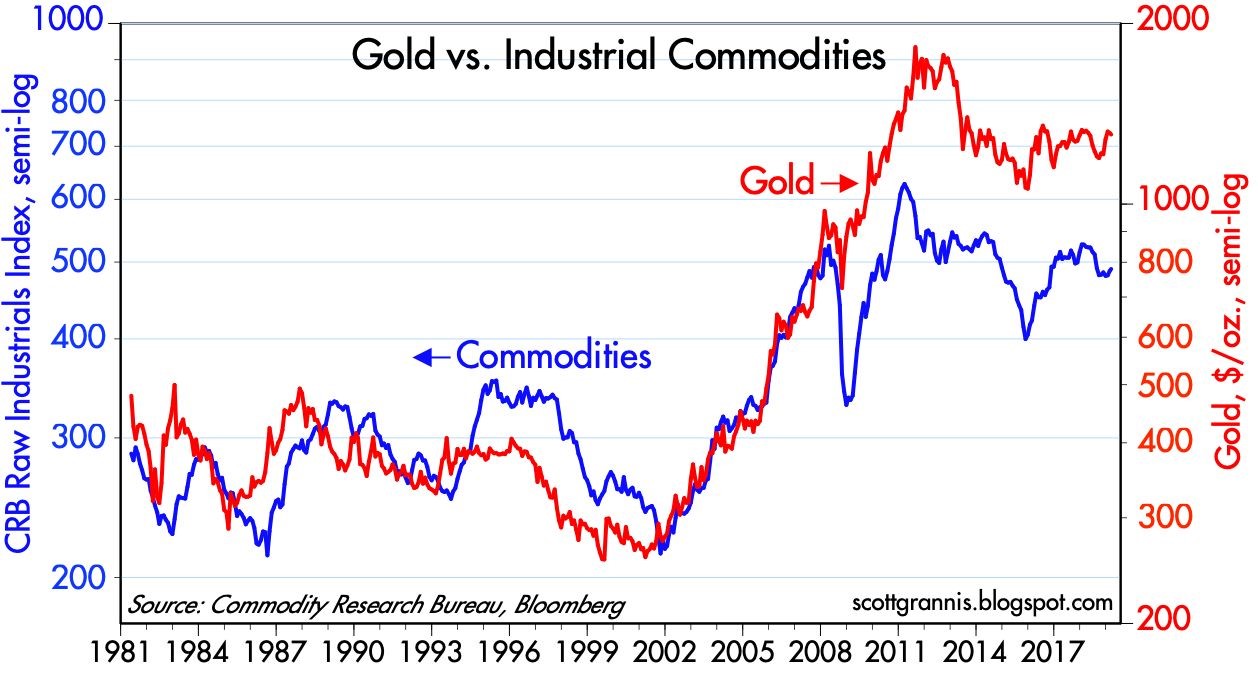

Similar to the stock market, commodities can be a good general barometer of current and future economic activity. As you can see from the chart below, not only have commodity prices remained stable in the face of slowing economic data, but gold prices have not spiked as they did during the last financial crisis.

Source: Calafia Beach Pundit

After 2018 brought record growth in corporate profits and negative returns, 2019 is producing a reverse mirror image – slow profit growth and record returns. The volatile ending to 2018 and triumphant beginning to 2019 is a reminder that “March Madness” does not need to bring sadness…it can bring gladness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Podcast 3/3/19: Week in Review and Share Buybacks

![]()

The Investing Caffeine podcast is designed to wake up your investment brain with weekly overviews of financial markets and other economic-related topics.

Episode 2

Market Review, Stock Ideas, and The Weekly Rant: Share Buybacks

Don’t miss out! Follow us on either SoundCloud or PodBean to get a new episode each week. Or follow our InvestingCaffeine.com blog and watch for new podcast updates each week.

SoundCloud: soundcloud.com/sidoxia

PodBean: sidoxia.podbean.com

Will Santa Leave a Lump of Coal?

As we enter the last month of the year, the holiday season is kicking into full gear, decorations are popping up everywhere, and the burning question arises, “Will Santa Claus bring gifts for stock market investors, or will he leave a lump of coal in their stockings?”

It was a bumpy sleigh ride last month, but we ultimately entered December in a festive mood with joyful monthly gains of +1.7% in the Dow Jones Industrial Average, and +1.8% in the S&P 500. There have been some naughty and nice factors leading to some turbulent but modest gains in 2018. For the first 11 months of the year, the Dow has rejoiced with a +3.3% advance, and the S&P 500 has celebrated a rise of +3.2% – and these results exclude additional dividends of approximately 2%.

Despite the monthly gains, not everything has been sugar plums. President Trump has been repeatedly sparring with the Federal Reserve Chairman, Jerome Powell, treating him more like the Grinch due to his stingy interest rate increases than Santa. As stockholders have contemplated the future path of interest rates, the major stock indexes temporarily slipped into negative territory for the year, until Mr. Powell gave stock and bond investors an early Christmas present last week by signaling interest rates are “just below” the nebulous neutral target. The dovish comment implied we are closer to the end of the economy-slowing rate-hike cycle than we are to the beginning.

Trade has also contributed to the recent spike in stock market volatility, despite the fresh establishment of the trade agreement reached between the U.S., Mexico, and Canada (USMCA – U.S.-Mexico-Canada Agreement), a.k.a., NAFTA 2.0. Despite the positive progress with our Mexican and Canadian neighbors, uncertainty surrounding our country’s trade relations with China has been challenging due to multiple factors including, Chinese theft of American intellectual property, cyber-attacks, forced technology transfer, agricultural trade, and other crucial issues. Fortunately, optimism for a substantive agreement between the world’s two super-powers advanced this weekend at the summit of the Group of 20 nations in Argentina, when a truce was reached to delay an additional $200 billion in tariffs for 90 days, while the two countries further negotiate in an attempt to finalize a comprehensive trade pact.

Source: Financial Times

Economic Tailwinds

Besides positive developments on the interest rate and trade fronts, the economy has benefited from tailwinds in some other important areas, such as the following:

Low Unemployment: The economy keeps adding jobs at a healthy clip with the unemployment rate reaching a 48-year low of 3.7%.

Source: Calculated Risk

Rising Consumer Confidence: Although there was a slight downtick in the November Consumer Confidence reading, you can see the rising long-term, 10-year trend has been on a clear upward trajectory.

Source: Chad Moutray

Solid Economic Growth: As the chart below indicates, the last two quarters of economic growth, measured by GDP (Gross Domestic Product), have been running at multi-year highs. Forecasts for the 4th quarter currently stand at a respectable mid-2% range.

Source: BEA

Uncertain Weather Forecast

Although the majority of economic data may have observers presently singing “Joy to the World,” the uncertain political weather forecast could require Rudolph’s red-nose assistance to navigate the foggy climate. The mid-term elections have created a split Congress with the Republicans holding a majority in the Senate, and the Democrats gaining control of the House of Representatives. As we learned in the last presidential term, gridlock is not necessarily a bad thing (see also, Who Said Gridlock is Bad?). For instance, a lack of government control can place more power in the hands of the private sector. Political ambiguity also surrounds the timing and outcome of Robert Mueller’s Special Counsel investigation into potential Russian interference and collusion, however as I have continually reminded followers, there are more important factors than politics as it relates to the performance of the stock market (see also, Markets Fly as Media Noise Goes By).

From an economic standpoint, some speculative areas have been pricked – for example the decline in FAANG stocks or the burst of the Bitcoin bubble as the price has declined from roughly $19,000 from its peak to roughly $4000 today (see chart below).

Source: Coindesk

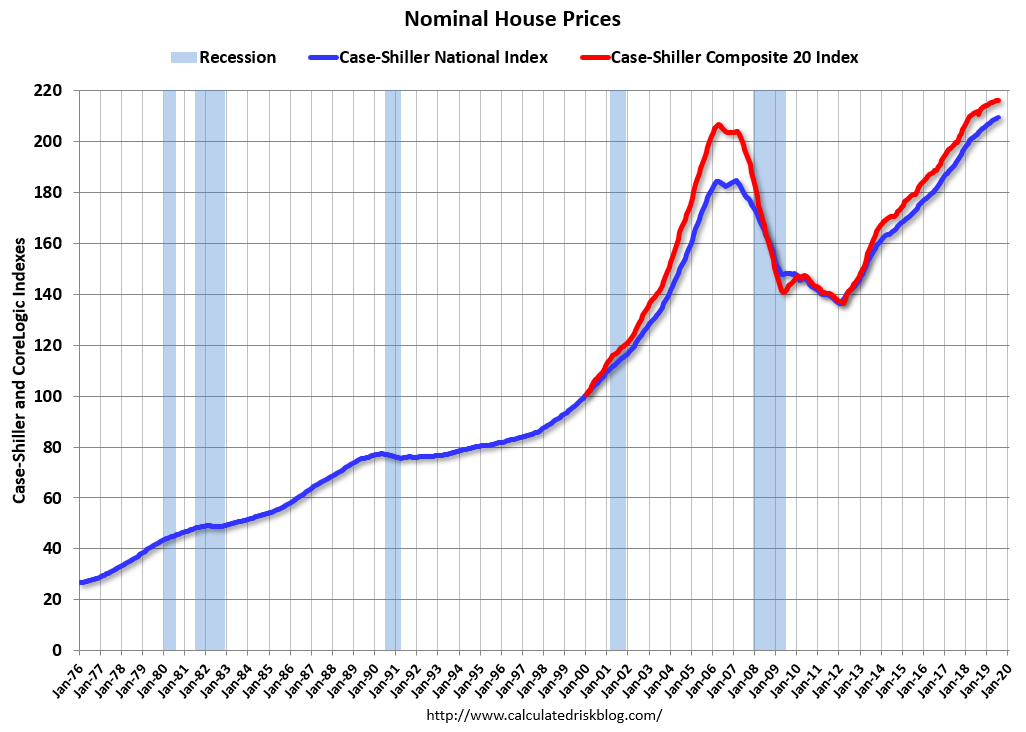

On the housing front, unit sales of new and existing homes have not been immune to the rising interest rate policies of the Federal Reserve. Nevertheless, as you can witness below, housing prices remain at all-time record high prices, according to the recent Case-Shiller data.

Source: Calculated Risk

I like to point out to my investors there is never a shortage of things to worry about. Even when the economy is Jingle Bell Rocking, the issues of inflation and Fed policy inevitably begin to creep into investor psyches. While prognosticators and talking heads will continue trying to forecast whether Santa Claus will place presents or coal into investors’ stockings this season, at Sidoxia we understand predictions are a fool’s errand. Regardless of Santa’s generosity (or lack thereof), we continue to find attractive opportunities for our investors, as we look to balance the risk and rewards presented to us during both stable and volatile periods.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 3, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Will the Halloween Trick Turn into a Holiday Treat?

The interest rate boogeyman came out in October as fears of an overzealous Federal Reserve monetary policy paralyzed investors into thinking rising interest rates could murder the economy into recession. But other ghostly issues frightened the stock market last month as well, including mid-term elections, heightening trade war tensions, a weakening Chinese economy, a fragile European economy (especially Italy), rising oil prices, weakening emerging market economies, anti-Semitism, politically motivated bomb threats, and anxiety over a potential recession after an aged economic expansion embarks on its 10th consecutive year of gains.

This ghoulish short-term backdrop resulted in the Dow Jones Industrial Average suffering a -5.1% drop last month, and the technology-heavy NASDAQ index screamed even lower by -9.2%. The results for the full year 2018 look more constructive – the S&P 500 is up +1.4% and the NASDAQ has climbed +5.8%.

Should the dreadful October result be surprising? Historically speaking, seasonality in the stock market has been quite scary during the month of October, especially if you consider the spooky stock Market Crash of 1929 (-19.7%) , the 1987 Crash (-21.5%), and the bloody collapse during the October 2008 Financial Crisis (-16.8%). There is good news, however. Seasonally, the holiday months of November and December typically tend to treat investors more cheerfully during the so-called “Santa Claus Rally” period. Since 1950 through 2017, the average return for stocks during November has been +1.4% (45 up years and 23 down years). For December, the results are even better at +1.5% (51 up years and 17 down years).

| November (1950-2017) | December (1950-2017) | |||

| Up Years | Down Years | Up Years | Down Years | |

| 2017 2.40% | 2015 -0.02% | 2017 1.08% | 2015 -1.87% | |

| 2016 3.29% | 2011 -0.32% | 2016 1.76% | 2014 -0.33% | |

| 2014 2.45% | 2010 -0.44% | 2013 2.31% | 2007 -0.76% | |

| 2013 2.68% | 2008 -7.48% | 2012 0.70% | 2005 -0.10% | |

| 2012 0.28% | 2007 -4.18% | 2011 0.86% | 2002 -6.03% | |

| 2009 5.74% | 2000 -8.01% | 2010 5.99% | 1996 -2.15% | |

| 2006 1.66% | 1994 -3.93% | 2009 1.48% | 1986 -2.83% | |

| 2005 3.52% | 1993 -1.29% | 2008 1.65% | 1983 -0.87% | |

| 2004 3.86% | 1991 -4.39% | 2006 1.26% | 1981 -3.01% | |

| 2003 0.71% | 1988 -1.89% | 2004 3.25% | 1980 -3.39% | |

| 2002 5.71% | 1987 -8.51% | 2003 5.08% | 1975 -1.15% | |

| 2001 7.52% | 1984 -1.51% | 2001 0.76% | 1974 -1.78% | |

| 1999 1.92% | 1976 -0.78% | 2000 0.41% | 1969 -1.87% | |

| 1998 5.91% | 1974 -5.32% | 1999 5.78% | 1968 -4.16% | |

| 1997 4.46% | 1973 -11.39% | 1998 5.64% | 1966 -0.15% | |

| 1996 7.34% | 1971 -0.25% | 1997 1.57% | 1961 -0.32% | |

| 1995 4.10% | 1969 -3.41% | 1995 1.74% | 1957 -3.31% | |

| 1992 3.03% | 1965 -0.88% | 1994 1.26% | ||

| 1990 6.00% | 1964 -0.52% | 1993 0.98% | ||

| 1989 1.65% | 1963 -1.05% | 1992 1.01% | ||

| 1986 2.15% | 1956 -3.10% | 1991 11.19% | ||

| 1985 6.51% | 1951 -0.95% | 1990 2.48% | ||

| 1983 1.74% | 1950 -0.26% | 1989 2.14% | ||

| 1982 3.60% | 1988 1.48% | |||

| 1981 3.27% | 1987 7.28% | |||

| 1980 10.24% | 1985 4.51% | |||

| 1979 4.26% | 1984 2.24% | |||

| 1978 0.61% | 1982 1.50% | |||

| 1977 2.86% | 1979 1.68% | |||

| 1975 2.47% | 1978 1.16% | |||

| 1972 4.56% | 1977 0.28% | |||

| 1970 4.74% | 1976 5.25% | |||

| 1968 4.80% | 1973 1.79% | |||

| 1967 0.75% | 1972 1.18% | |||

| 1966 0.31% | 1971 8.62% | |||

| 1962 10.16% | 1970 5.68% | |||

| 1961 3.77% | 1967 2.63% | |||

| 1960 2.97% | 1965 0.90% | |||

| 1959 1.52% | 1964 0.39% | |||

| 1958 1.78% | 1963 2.44% | |||

| 1957 3.17% | 1962 1.35% | |||

| 1955 7.64% | 1960 5.08% | |||

| 1954 7.71% | 1959 2.03% | |||

| 1953 0.41% | 1958 4.78% | |||

| 1952 4.31% | 1956 1.50% | |||

| 1955 0.29% | ||||

| 1954 5.85% | ||||

| 1953 0.12% | ||||

| 1952 3.47% | ||||

| 1951 3.62% | ||||

| 1950 3.81% | ||||

While the last 31 days may have been distressing, at Sidoxia we understand that terrifying short-term volatility is a necessary requirement for long-term investors, if you desire the sweet appreciation of long-term gains. Fortunately at Sidoxia our long-term investors have benefited quite handsomely over the last 10 years from our half-glass-full perspective. The name Sidoxia actually is derived from the Greek word for “optimism” (aisiodoxia).

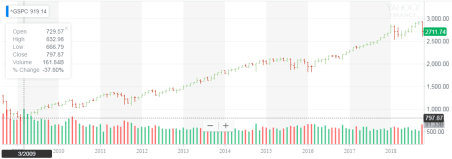

Performance has been fruitful in recent years, but the almost decade-long bull market has not been all smooth sailing (see Series of Unfortunate Events), as you can see from the undulating 10-year chart below (2008-2018). Do you remember the Flash Crash, Debt Ceiling, Greek Crisis, Arab Spring, Crimea, Ebola, Sequestration, and Taper Tantrum, among many other events? Similar to the volatility experienced in recent weeks, all these aforementioned events caused scary downdrafts as well.

The S&P 500 hit a low of 666 in March 2009, but even with the significant fall last month, the stock market has more than quadrupled in value to 2,711 today.

The compounding benefits of long-term investing are quite evident over the last decade when you consider the record profits of the stock market. Compounding benefits apply to individual stocks as well, and Sidoxia and its clients have experienced this first hand through ownership in positions in stocks like Amazon.com Inc. (+2,692% in 10 years), Apple Inc. (+1,324%), and Google (parent Alphabet) (+507%), and many other less-familiar growth companies have allowed our client portfolios and hedge fund to outperform their benchmarks over longer periods of time. Although we are proud of our long-term performance, we have definitely had periods of under performance, and there will come a time in which a more defensive stance will be required. However, panicking is very rarely the best course of action when you are talking about your long-term investment strategy. Staying the course is paramount.

During periods of heightened volatility, like we experienced in October, the importance of owning a broadly diversified portfolio across asset classes (including stocks, bonds, real estate, commodities, emerging markets, growth, value, etc.) is worth noting. Of course an asset allocation should be followed according to a risk tolerance appropriate for your unique circumstances. As financial markets and interest rates gyrate, investors should get in the practice of rebalancing portfolios. For example, at Sidoxia, we are consistently harvesting our gains and opportunistically redeploying those proceeds into unloved areas in which we see better long-term appreciation opportunities. This whole investment process is designed for reducing risk and maximizing returns.

As in some famously scary stock market periods in the past, October turned out to be another frightening month for investors. The good news is that we have seen this scary movie many times in the past, and we have lived to tell the tale. The economy remains strong, corporate profits are at record levels and still rising, consumer and business confidence levels are near all-time highs, and interest rates remain historically low despite the Fed’s gradual interest rate hiking policy. While Halloween has definitely worried many investors, history tells us that previous tricks may turn into holiday treats!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, AMZN, GOOGL, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}