Posts tagged ‘PMI’

The SaaSpocalypse Has Arrived…Or Has It?

Well, the new month has started with a bang. Financial markets have not only experienced a bang from another military strike on Iran, but also an explosion of AI paranoia. As hundreds of billions of AI investment dollars flood into the economy, fears are intensifying that the AI displacement of workers could have a detrimental impact on the economy and financial markets.

The Monthly Scorecard

It was a mixed performance in the market last month. Geopolitical headlines surrounding Iran and the Middle East are currently front and center, but under the surface, the real story isn’t just geopolitics—it’s a growing investor anxiety around artificial intelligence and its disruptive potential. Here’s what happened last month:

- S&P 500: -0.9%

- Dow Jones Industrial Average: +0.2%

- NASDAQ: -3.4%

The “SaaSpocalypse” and the Tech Identity Crisis

Software stocks are currently under assault, plunging -9.7% for the month and a staggering -22.8% for the start of the year (as measured by the IGV iShares Software index). Analysts are calling this the “SaaSpocalypse” (Software as a Service)—a phenomenon where the market fear is that AI is “eating” software companies.

High-profile casualties have added fuel to the fire. IBM, for example, suffered its worst trading day in 25 years, dropping -13% in a single day. Concerns came to light that new AI agent coding tools like Anthropic’s Claude Code could threaten IBM’s legacy dominance in COBOL-based mainframe systems.

Paranoia vs. Reality

This “AI Paranoia” has spread far beyond Silicon Valley, infecting industries like transportation, banking, travel, real estate, and food delivery. Two major catalysts fueled this fire:

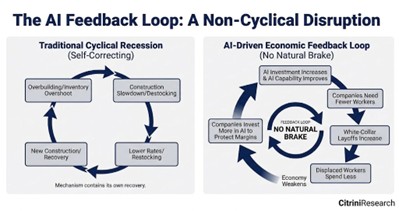

The Citrini Report: A viral, dystopian report from described an “avalanche” of white-collar firings (see chart below). The report argues that while the government may try to intervene with stimulus, it “won’t change the fact that an AI Claude agent can do the work of a $180,000 product manager for $200/month.”

Source: Citrini Research

- Corporate Reductions: High-profile cuts have validated these fears. Block Inc. (led by Jack CEO Dorsey, former Twitter Founder) announced it is slashing 40% of its workforce due to AI advancements, while Amazon recently eliminated 30,000 white-collar positions (10% of its corporate staff).

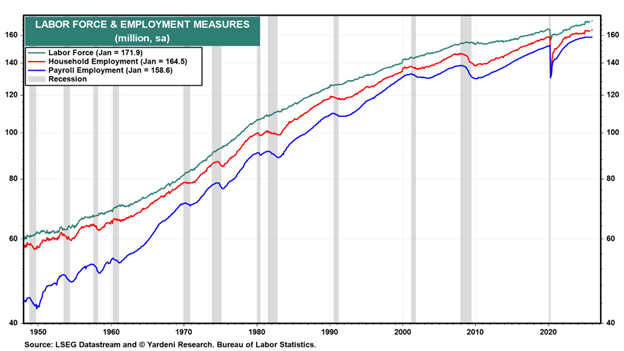

However, there is a silver lining to that perspective. While software jobs have flattened since ChatGPT arrived in late 2022, we have yet to see the “cliff dive” in total employment that many predicted. In fact, employment (165 million employed) and labor force (172 million) figures are near record levels, so we have not seen AI kill the economy quite just yet (see chart below).

Source: Yardeni Research and Bureau of Labor Statistics

The Great Rotation: Looking for “HALO”

As investors try to decipher the winners and losers, they are migrating away from technology and rotating into HALO stocks (Hard Asset, Low Obsolescence). These companies are seen as less susceptible to AI disruption. Evidence of this shift is clear in the outperformance of value, small-cap, and mid-cap stocks. Notably, the Dow Jones Industrial Average, an index heavy with hard asset exposure, just posted its 10th consecutive month of gains despite the broader technology stock volatility.

A Massive Bet on the Future

Despite the “bubble” murmurs, the AI juggernauts are doubling down. OpenAI just closed the largest private financing in history, raising $110 billion—including $50 billion from Amazon, $30 billion from NVIDIA, and $30 billion from SoftBank. The demand for compute and data centers remains insatiable, supported by the $700 billion being spent by the large hyperscalers (Amazon, Alphabet-Google, Microsoft, and Meta Platforms) this year.

Geopolitical and Legal Headwinds

Adding to the month’s complexity are external shocks:

- Middle East Tensions: Military strikes on Iran recently killed the Iranian Supreme Leader, Ali Khamenei, and other key leaders, injecting significant geopolitical risk.

- Tariff Uncertainty: The Supreme Court recently ruled against the IEEPA tariffs instituted by the Trump administration. While temporary alternatives are in place, the markets are waiting for a permanent solution to work through the courts.

Resilience in the Face of Technological Change

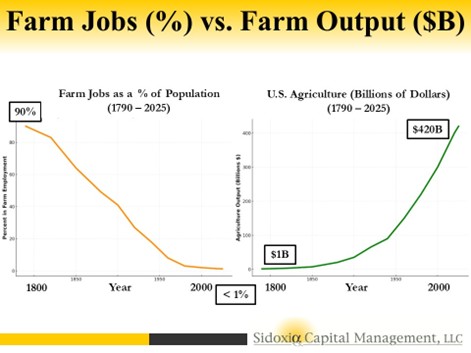

It is easy to get lost in the dystopian narrative, but history offers a more hopeful guide. Technology has been replacing human workers for centuries—from the looms of the Industrial Revolution to the tractors of the Agricultural Revolution – see chart below (1790 – 2025). In every instance, while specific roles were displaced, new industries emerged that not only soaked up the unemployed but expanded the labor force into areas we couldn’t have previously imagined (see also The Fallacy Behind Technological Innovation).

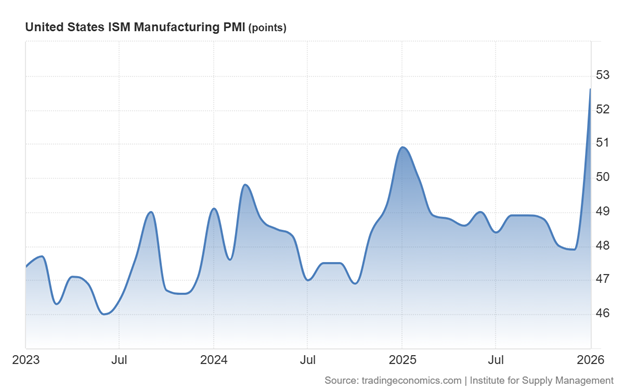

The reality today is that the economy remains remarkably strong. Employment data is resilient, labor force participation is near record levels, and corporate profits are breaking out to new all-time highs. Furthermore, the ISM Manufacturing PMI (Purchasing Managers Index) recently spiked to 52.6, signaling an expansion in a sector that had been declining for years (see chart below).

Source: Trading Economics

We are not witnessing the end of work, but rather a high-speed evolution. As we’ve seen before, the human capacity for innovation and adaptation usually outruns the machines.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (Mar. 2, 2026). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AMZN, GOOGL, META, MSFT, NVDA, certain exchange traded funds (ETFs), but at the time of publishing had no direct position in IBM, XYZ or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Aaaaaaaah: Turbulence or Nosedive?

We’ve all been there on that rocky plane ride…clammy hands, heart beating rapidly, teeth clenched, body frozen, while firmly bracing the armrests with both appendages. The sky outside is dark and the interior fuselage rattles incessantly until….whhhhhssssshhh. Another quick jerking moment of turbulence has once again sucked the air out of your lungs and the blood from your heart. The rational part of your brain tries to assure you that this is normal choppy weather and will shortly transition to calm blue skies. The irrational and emotional, part of our brains (see Lizard Brain) tells us the treacherous plane ride is on the cusp of plummeting into a nosedive with passengers’ last gasps saved for blood curdling screams before the inevitable fireball crash.

Well, we’re now beginning to experience some small turbulence in the financial markets, and at the center of the storm is a collapsing Argentinean peso and a perceived slowing in China. In the case of Argentina, there has been a century-long history of financial defaults and mismanagement (see great Scott Grannis overview). Currently, the Argentinean government has been painted into a corner due to the depletion of its foreign currency reserves and financial mismanagement, as evidenced by an inflation rate hitting a whopping 25% rate.

On the other hand, China has created its own set of worries in investors’ minds. The flash Markit/HSBC Purchasing Managers’ Index (PMI) dropped to a level of 49.6 in January from 50.50 in December, which has investors concerned of a market crash. Adding fuel to the fear fire, Chinese government officials and banks have been trying to reverse excesses encountered in the country’s risky shadow banking system. While the size of Argentina’s economy may not be a drop in the bucket, the ultimate direction of the Chinese economy, which is almost 20x’s the size of Argentina’s, should be much more important to global investors.

At the end of the day, most of these mini-panics or crises (turbulence) are healthy for the overall financial system, as they create discipline and will eventually change irresponsible government behaviors. While Argentinean and Chinese issues dominate today’s headlines, these matters are not a whole lot different than what we have read about Greece, Ireland, Italy, Spain, Portugal, Cyprus, Turkey, and other negligent countries. As I’ve stated before, money goes where it’s treated best, and the stock, bond, and currency vigilantes ensure that this is the case by selling the assets associated with deadbeat countries. Price declines eventually catch the attention of politicians (remember the TARP vote failure of 2008?).

Is This the Beginning of the Crash?!

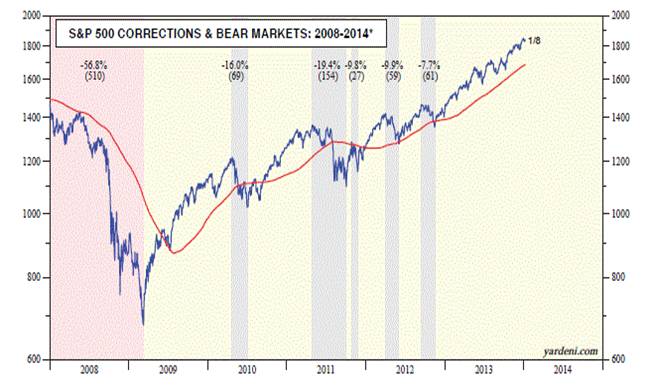

What goes up, must come down…right? That is the pervading sentiment I continually bump into when I speak to people on the street. Strategist Ed Yardeni did a great job of visually capturing the last six years of the stock market (below), which highlights the most recent bear market and subsequent major corrections. Noticeably absent in 2013 is any major decline. So, while many investors have been bracing for a major crash over the last five years, that scenario hasn’t happened yet. The S&P chart shows we appear to be due for a more painful blue (or red) period of decline in the not-too-distant future, but that is not necessarily the case. One would need only to thumb through the history books from 1990-1997 to see that investors lived through massive gains while avoiding any -10% correction – stocks skyrocketed +233% in 2,553 days. I’m not calling for that scenario, but I am just pointing out we don’t necessarily always live through -10% corrections annually.

Source: Dr. Ed’s Blog

Even though we’ve begun to experience some turbulence after flying high in 2013, one should not panic. You may be better off watching the end of the airline movie before putting your head in between your legs in preparation for a nosedive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

To Taper or Not to Taper…That is the Question?

It’s not Hamlet who is providing theatrical intrigue in the financial markets, but rather Federal Reserve Chairman Ben Bernanke. Watching Bernanke decide whether to taper or not to taper the $85 billion in monthly bond purchases (quantitative easing) is similar to viewing an emotionally volatile Shakespearean drama. The audience of investors is sitting at the edge of their seats waiting to see if incoming Fed Chief will be plagued with guilt like Lady Macbeth for her complicit money printing ways or will she score a heroic and triumphant victory for her hawkish stance on quantitative easing (QE). No need to purchase tickets at a theater box office near you, the performance is coming live to your living room as Yellen’s upcoming Senate confirmation hearings will be televised this upcoming week.

Bad News = Good News; Good News = Bad News?

In deciding whether to slowly kill QE, the Fed has been stricken with the usual stream of never-ending economic data (see current data from Barry Ritholtz). Most recently, investors have followed the script that says bad news is good news for stocks and good news is bad news. So-called pundits, strategists, and economists generally believe sluggish economic data will lead the Fed to further romance QE for a longer period, while robust data will force a poisonous death to QE via tapering.

Good News

Despite the recent, tragically-perceived government shutdown, here is the week’s positive news that may contribute to an accelerated QE stimulus tapering:

- Strong Jobs: The latest monthly employment report showed +204,000 jobs added in October, almost +100,000 more additions than economists expected. August and September job additions were also revised higher.

- GDP Surprise: 3rd quarter GDP registered in at +2.8% vs. expectations of 2%.

- IPO Dough: Twitter Inc (TWTR) achieved a lofty $25,000,000,000 initial public offering (IPO) value on its first day of trading.

- ECB Cuts Rates: The European Central Bank (ECB) lowered its key benchmark refinancing rate to a record low 0.25% level.

- Service Sector Surge: ISM non-manufacturing PMI data for October came in at 55.4 vs. 54.0 estimate.

Bad News

Here is the other side of the coin, which could assist in the delay of tapering:

- Mortgage Apps Decline: Last week the MBA mortgage application index fell -7%.

- Jobless # Revised Higher: Last week’s Initial jobless Claims were revised higher by 5,000 to 345,000.

- Investors Too Happy: The spread between Bulls & Bears is highest since April 2011 as measured by Investors Intelligence

Much Ado About Nothing

With the recent surge in the October jobs numbers, the tapering plot has thickened. But rather than a tragic death to the stock market, the inevitable taper and eventual tightening of the Fed Funds rate will likely be “Much Ado About Nothing.” How can that be?

As I have written in an article earlier this year (see 1994 Bond Repeat), the modest increase in 2013 yields (up +1.35% approximately) from the July 2012 lows pales in comparison to the +2.5% multi-period hike in the 1994 Federal Funds rate by then Fed Chairman Alan Greenspan. What’s more, inflation was a much greater risk in 1994 with GDP exceeding 4.0% and unemployment reaching a hot 5.5% level.

Given an overheated economy and job market in 1994, coupled with a hawkish Fed aggressively raising rates, the impact of these factors must have been disastrous for the stock market…right? WRONG. The S&P 500 actually finished the year essentially flat (~-1.5%) after experiencing some volatility earlier in the year, then subsequently stocks went on a tear to more than triple in value over the next five years.

To taper or not to taper may be the media question du jour, however the Fed’s ultimate decision regarding QE will most likely resemble a heroic Shakespearean finale or Much Ado About Nothing. Panicked portfolios may be in love with cash like Romeo & Juliet were with each other, but overreaction by investors to future tapering and rate hikes may result in poisonous or tragic returns.

Referenced article: 1994 Bond Repeat or 2013 Stock Defeat?

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page. Some Shakespeare references were sourced from Kevin D. Weaver.

Nail Not in Emerging Market Coffin Yet

I wouldn’t say the nail is in the emerging market coffin quite yet. During the financial crisis, the EMSCI Emerging Market Index (EEM) was left for dead (down -50% in 2008) before resurrection in 2009 and 2010 (up +74% and +16%, respectively). For the last two years however, the EMSCI index has underperformed the S&P 500 Index massively by more than -30%. Included in this international index are holdings from China, Russia, India, Brazil, South Korea, and South Africa, among others.

The question now becomes, can the emerging markets resurrect themselves from the dead again? Recent signs are flashing “yes”. Over the last three months, the emerging markets have outperformed the S&P 500 by more than +8%, but these stocks still have a lot of ground to make up before reaching the peak levels of 2007. Last year’s slowing growth in China and a European recession, coupled with talks of the Federal Reserve’s “tapering” of monetary stimulus, didn’t provide the EMSCI index any help over the last few years.

With all the distracting drama currently taking place in Washington D.C., it’s a relief to see some other indications of improvement. For starters, China’s most recent PMI manufacturing index results showed continued improvement, reaching a level of 51.1 – up from August and signaling a reversal from contraction earlier this year (levels above 50 point to expansion). Chinese government leaders are continuing their migration from an externally export-driven economy to an internally consumer-driven economy. Despite the shift, China is still targeting a respectable +7.5% GDP economic growth target, albeit a slower level than achieved in the past.

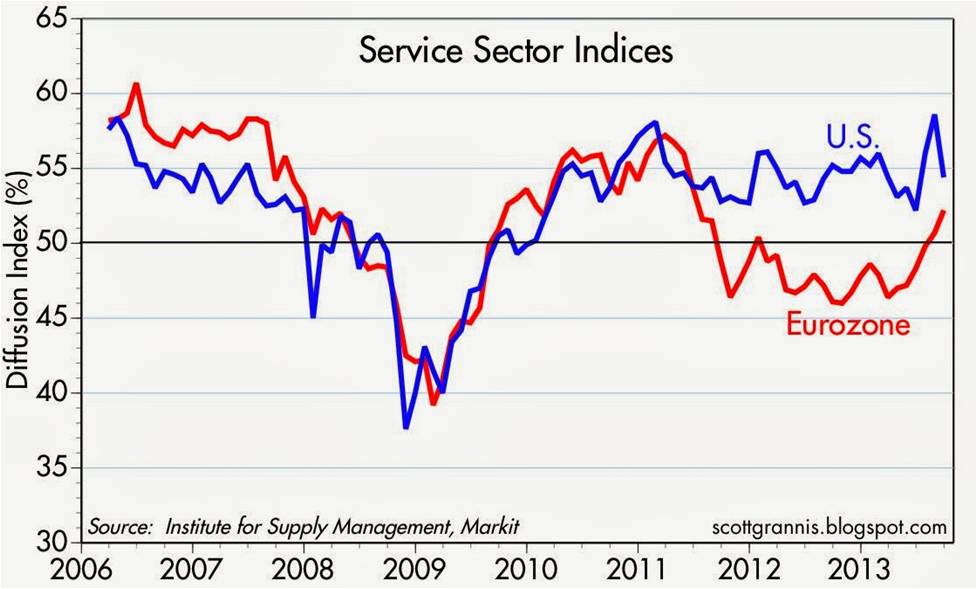

Adding to emerging market optimism is Europe’s apparent economic turnaround (or stabilization). As you can see from the chart below, the European Institute for Supply Management (ISM) service sector index has lately shown marked improvement. If the European and Chinese markets can sustain these recovering trends, these factors bode well for emerging market financial returns.

Source: Calafia Beach Pundit

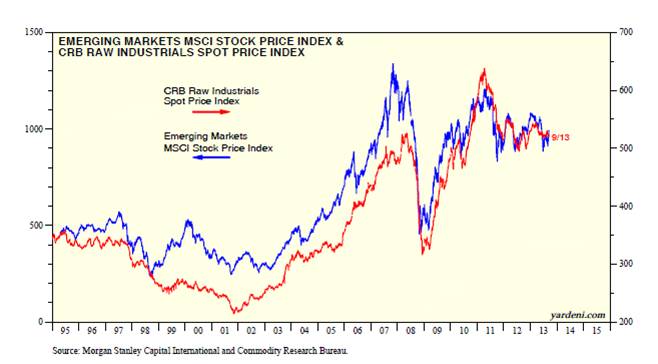

While it is clear these developments are helping the rebound in emerging market indices, it is also clear the supply-demand relationship in commodities will coincide with the next big up or down move in developing markets. Ed Yardeni, strategist and editor of Dr. Ed’s Blog, recently wrote a piece showing the tight correlation between emerging market stock prices and commodity prices (CRB Index). His conclusions come as no surprise to me given these resource-rich markets and their dependence on Chinese demand along with commodity needs from other developed countries. Expanding populations and rising standards of living in emerging market countries have and will likely continue to position these countries well for long-term commodity price appreciation. The development of new, higher-value service and manufacturing sectors should also lead to sustainably improved growth in these emerging markets relative to developed economies.

Source: Dr. Ed’s Blog

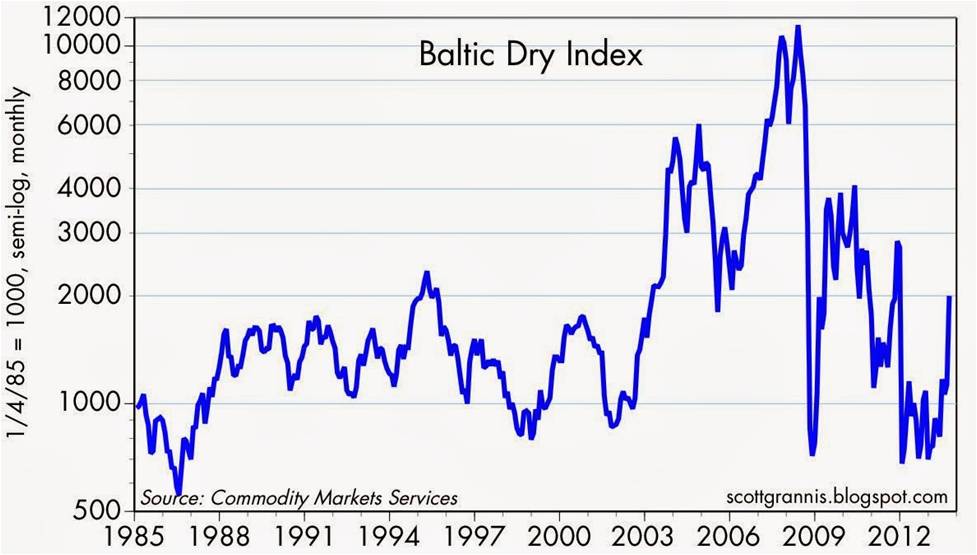

Adding fuel to the improving emerging market case is the advancement in the Baltic Dry Index (see chart below). The recent upward trajectory of the index is an indication that the price for moving major raw materials like coal, iron ore, and grains by sea is rising. This statistical movement is encouraging, but as you can see it is also very volatile.

Source: Calafia Beach Pundit

While the emerging markets are quite unpredictable and have been out-of-favor over the last few years, a truly diversified portfolio needs a healthy dosage of this international exposure. You better check a pulse before you put a nail in the coffin – the emerging markets are not dead yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, but at the time of publishing, SCM had no direct position in EEM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Magical Growth through Manufacturing Decline

In a data driven world, we can never get enough numbers. The market magicians and the media machines have no problem overhyping or overselling the importance of each pending data-point. With a quick economic sleight of hand, the industry pundits have converted the average investor into a frothing Pavlovian dog, begging for another market shaking statistic. One of the supposed earth-rattling data points is the monthly ISM Manufacturing Index figure, but the release of the ISM number alone isn’t enough for the audience. The real fun comes in determining whether the monthly number registers above or below a schizophrenic 50 level – a number above 50 indicates the manufacturing economy is generally expanding (August came in at 50.6).

The trick can often be surprising, but more surprising to me is the importance placed on this relatively small, disappearing segment of our economy. With the manufacturing sector now accounting for just 11-13% of GDP (see also Manufacturing – Losing Out?), shouldn’t we be focusing more on the “Services” sector of the economy, which accounts for roughly 75% of our country’s output, up from 62% in 1971 (source: Earthtrends). I believe economist Mark Perry at Carpe Diem captured this phenomenon best in his post from earlier this year (Decline of Manufacturing – The World is Much Better Off ):

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

Déjà Vu All Over Again

This isn’t the first time in our country’s history that we’ve experienced explosive economic growth as legacy segments of the economy decline in relative importance. Consider the share of jobs agriculture controlled in the early 1800s – a whopping 90% of jobs were tied to farms (see chart below). Today, that percentage is less than 2% in the wake of the U.S. becoming the 20th Century global superpower. History has taught us that technology can be a bitch on employment, as robots, machinery, processes, and chemistry replace the demand for human labor. As Perry points out, there is no doubt that “tractors, electricity, combines, the cotton gin, automatic milking machinery, computers, GPS, hybrid seeds, irrigation systems, herbicides, pesticides” replaced millions of farming jobs, but guess what…American ingenuity ruled the day. As it turns out, those economic resources freed up by technology and productivity were redeployed into new, expanding, job-fertile areas of the economy like, “manufacturing, health care, education, business, retail, computers, transportation, etc.”

Source: Carpe Diem

More Apples or More GMs?

The farming lobby still cries for its inefficient, growth-muffling subsidies today, but many unproductive, unionized domestic manufacturing industries are also screaming for government assistance because cheap foreign labor and new technologies are stealing manufacturing jobs by the boatloads. So at the core, the real question is do we want government and investments supporting more companies like Apple Inc. (AAPL) or more companies like General Motors Company (GM)?

As you may know, by flipping over an iPhone, any observer can clearly notice the product is “designed by Apple in California – assembled in China.” It is clear that Apple and its customers value brains over manufacturing brawn. At $371 billion and the most valuable publicly traded stock in the universe, Apple is dominating the electronics world, all the while hiring employees by the thousands. These facts beg the question of whether Apple should revamp their manufacturing supply-chain back to the U.S. to save more domestic jobs? Of course the result of a manufacturing strategy shift to a higher cost region would make Apple less competitive, force them to charge consumers higher prices for Apple products, and open the door for competitors to freely steal market share? Would this strategy create more incremental jobs, or fewer jobs? I think I’ll side with the Steve Jobs philosophy of business, which says “more profitable businesses must fill more job openings.”

If this Apple case study isn’t illustrative enough for you, maybe you should take a look at companies like GM. The U.S. automobile industry has historically been notoriously mismanaged, thanks to a horrific manufacturing cost structure, anchored by unsustainable pension and healthcare costs. Should investors be surprised that an uncompetitive, bloated cost structure leaves companies like GM less money to invest in new products and innovation? This irrational cost management contributed to decades of market share losses to foreigners. If I’m the job creation czar in the U.S., I think I’ll choose the Apple path to job creation over GM’s route.

Global Competitiveness = Jobs

With a 9.1% unemployment rate and the recent introduction of the American Jobs Act, there has been plenty of emphasis and focus on job creation. At the end of the day, what will create durable, long-term job creation is innovative, competitively priced products and services that can be sold domestically and abroad. How do we achieve this goal? We need an education system that can teach and train a workforce sufficiently to meet the discerning tastes of a global marketplace. Government, on the other hand, needs to support (not direct) the private sector by investing in strategic areas to help global competitiveness (i.e., education, energy independence, basic research, infrastructure, entrepreneurial capital for business formation, etc.), while facilitating a business environment that incentivizes growth.

Regardless of the policy mixtures, the common denominator needs to be focused on improving global competitiveness. Excessive focus on a declining manufacturing sector and the monthly ISM data will only distract decision makers from the core issues. If the economic magician’s sleight of hand diverts investor attention for too long, we may see more jobs disappear.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and AAPL, but at the time of publishing SCM had no direct position in GM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

{kind=link}