Posts tagged ‘PIIGS’

Double Dip Expansion?

Ever since the 2008-2009 financial crisis, every time the stock market has experienced a -5%, -10%, or -15% correction, industry pundits and media talking heads have repeatedly sounded the “Double Dip Recession” alarm bells. As you know, we have yet to experience a technical recession (two reported quarters of negative GDP growth), and stock prices have almost quadrupled from a 2009 low on the S&P 500 of 666 to 2,378 today (up approximately +257%).

Over the last nine years, so-called experts have been warning of an imminent stock market collapse from the likes of PIIGS (Portugal/Italy/Ireland/Greece/Spain), Cyprus, China, Fed interest rate hikes, Brexit, ISIS, U.S. elections, North Korea, French elections, and other fears. While there have been plenty of “Double Dip Recession” references, what you have not heard are calls for a “Double Dip Expansion.”

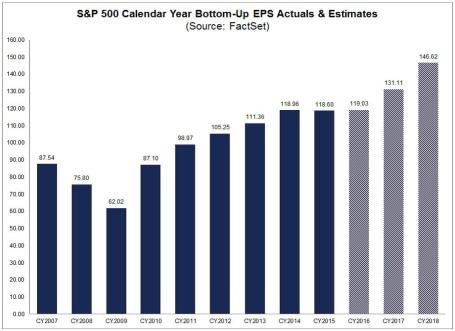

Is it possible that after the initial 2010-2014 economic expansionary rebound, and subsequent 2015-2016 earnings recession caused by sluggish global growth and a spike in the value of the U.S. dollar, we could possibly be in the midst of a “Double Dip Expansion?” (see earnings chart below)

Source: FactSet

Whether you agree or disagree with the new political administration’s politics, the economy was already on the comeback trail before the November 2016 elections, and the momentum appears to be continuing. Not only has the pace of job growth been fairly consistent (+235,000 new jobs in February, 4.7% unemployment rate), but industrial production has been picking up globally, along with a key global trade index that accelerated to 4-5% growth in the back half of 2016 (see chart below).

Source: Calafia Beach Pundit

This continued, or improved, economic growth has arisen despite the lack of legislation from the new U.S. administration. Optimists hope for an improved healthcare system, income tax reform, foreign profit repatriation, and infrastructure spending as some of the initiatives to drive financial markets higher.

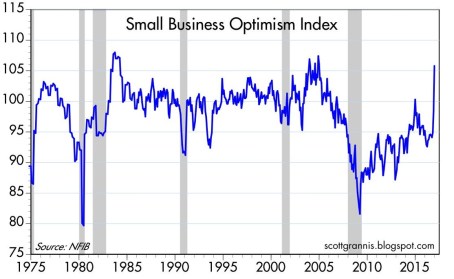

Pessimists, on the other hand, believe all these proposed initiatives will fail, and cause financial markets to fall into a tailspin. Regardless, at least for the period following the elections, investors and companies have perceived the pro-business rhetoric, executive orders, and regulatory relief proposals as positive developments. It’s widely understood that small businesses supply the largest portion of our nation’s jobs, and the upward spike in Small Business Optimism early in 2017 is a welcome sign (see chart below).

Source: Calafia Beach Pundit

Yes, it is true our new president could send out a rogue tweet; start a trade war due to a tariff slapped on a critical trading partner; or make a hawkish military remark that isolates our country from an ally. These events, along with other potential failed campaign promises, are all possibilities that could pause the trajectory of the current bull market. However, more importantly, as long as corporate profits, the mother’s milk of stock price appreciation, continue to march higher, then the stock market fun can continue. If that’s the case, there will likely be less talk of “Double Dip Recessions,” and more discussions of a “Double Dip Expansion.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Floating Hedge Fund on Ice Thawing Out

These days, pundits continue to talk about how the same financial crisis plaguing Greece and its fellow PIIGS partners (Portugal, Ireland, Italy & Spain) is about to plow through the eurozone and then ultimately the remaining global economy with no mercy. If all the focus is being placed on a diminutive, calamari-eating, Ouzo-drinking society like Greece, whose economy matches the size of Maryland, then why not evaluate an even more miniscule, PIIGS prequel country…Iceland.

That’s right, the same Iceland that just four years ago people were calling a “hedge fund on ice.” You know, that frozen island that had more foreign depositors investing in their banks than people living in the country. Before Icelandic banks became more than 75% of the overall stock market, and Gordon Gekko became the country’s patron saint, Iceland was more known for fishing. The fishing industry accounted for about half of Iceland’s exports, and the next largest money maker may have been Bjork, the country’s famed and quirky female singer.

In looking back at the financial crisis of 2008-2009, as it turned out, Iceland served as a canary in the global debt binging coal mine. In order to attract the masses of depositors to Icelandic banks, these financial institutions offered outrageous, unsustainable interest rates to yield-starved customers. How did the Icelandic bankers offer such high rates? Well of course, it was those can’t-lose American subprime mortgages that were offering what seemed like irresistibly high yields. Of course, what seemed like a dream at the time, eventually turned into a nightmare once the scheme unraveled. Ultimately, it became crystal clear that the subprime borrowers could not pay the outrageous rates, especially after rates unknowingly reset to untenable levels for many borrowers.

At the peak of the crisis, the Icelandic banks were holding amounts of debt exceeding six times the Icelandic GDP (Gross Domestic Product) and these lenders suffered more than $100 billion in losses. One of the Icelandic banks was even funding a large condominium project in my neighboring Southern California city of Beverly Hills. When the excrement hit the fan after Lehman Brothers went bankrupt, it didn’t take long for Iceland’s stock market to collapse by more than -95%; Iceland’s Krona to crumple; and eventually the trigger of Iceland’s multi-billion bailout by numerous constituents, including the IMF (International Monetary Fund).

Bitter Medicine First, Improvement Next

Today, four years after the subprime implosion and Lehman debacle, the hedge fund on ice known as Iceland is beginning to thaw, and their economic picture is looking much brighter (see charts below). GDP growth is the highest it has been in four years (4.5% recently); the stock market has catapulted upwards (almost doubling from the lows); and the Iceland unemployment rate has declined from over 9% a few years ago to about 7% today.

Source: Trading Economics

Source: Trading Economics

Re-jiggering a phony economy with a faulty facade cannot be repaired overnight. However, now that the banking system has been allowed to clear out its excesses, Iceland can move forward. One tailwind behind the economy has been Iceland’s weaker currency, which has led to a +17% increase in foreign tourist nights at Icelandic hotels through April this year. What’s more, tourist traffic at Iceland’s airport hit a record in May. Iceland has taken its bitter medicine, adjusted, and is currently reaping some of the rewards.

Although the detrimental effects of austerity experienced by the economies and banks of Greece, Spain, and Italy crowd out most of today’s headlines, Iceland is not the only country to make painful changes to its fiscal ways and then taste the sweetness of progress. Let’s not forget the Guinness drinking Irish. Ireland, like Greece, Portugal, and Spain received a bailout, but Ireland’s banking system was arguably worse off than Spain’s, yet Ireland has seen its borrowing costs on its 10-year bond decrease dramatically from 9.2% at the beginning of 2011 to about 7.4% this month (still high, but moving in the right direction). The same can be said for the United States. Our banks were up against the ropes, but after some recapitalization, tighter oversight, and stricter lending standards, our banks have gotten back on track and have helped assist our economy grow for 11 consecutive quarters (albeit at uninspiring growth rates).

The austerity versus growth debate will no doubt continue to circulate through media circles. In my view, these arguments are too simplistic and one dimensional. Every country has its unique culture and distinct challenges, but even countries with massive financial excesses can steer themselves back to a path of growth. A floating hedge fund on ice to the north of us has proven that fact to us, as we witness brighter days beginning to thaw Iceland’s chilly economy to expansion again.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman Brothers, Guinness, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The European Dog Ate My Homework

I never thought my daily routine would be dominated by checking European markets before our domestic open, but these days it is appearing like the European tail is wagging the global dog. Tracking Spanish bond yields from the Tesoro Publico and the Italia Borsa index is currently having a larger bearing on my portfolio than U.S. fundamentals. When explaining short term performance to others, I feel a little like an elementary school student making an excuse that my dog ate my homework.

Although the multi-year European saga has gone on for years, this too shall pass. What’s more, despite the bailouts of Portugal, Ireland, and Greece in recent years, the resilient U.S. economy has recorded 11 consecutive quarters of GDP (Gross Domestic Product) growth and added more than 4 million jobs, albeit at a less than desirable pace.

Could it get worse? Certainly. Will it get worse before it gets better? Probably. Is worsening European fundamentals and a potential Greek eurozone exit already factored into current stock prices? Possibly. The truth of the matter is that nobody knows the answers to these questions with certainty. At this point, the probability of an unknown or unexpected event in a different geography is more likely to be the cause of our economic downfall than a worsening European crisis. As sage investor and strategist Don Hays aptly points out, “When everyone is concerned about a problem, that problem is solved.” That may be overstating the truth a bit, but I do believe the issues absent from current headlines are the matters we should be most concerned about.

The European financial crisis may drag on for a while longer, but nothing lasts forever. Years from now, worries about the PIIGS countries (Portugal, Ireland, Italy, Greece, Spain) will switch to others, like the BRICs (Brazil, Russia, India, China) or other worry geography du jour. The issues of greatest damage in 2008-2009, like Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages, didn’t dominate the headlines for years like the European crisis stories of today. As compared to Europe’s problems, these prior pains felt like Band Aids being quickly ripped off.

Correlation Conundrum

Eventually European worries will be put on the backburner, but until some other boogeyman dominates the daily headlines, our financial markets will continue to correlate tightly with European security prices. How does one fight these tight correlations? For starters, the correlations will not stay tight forever. If an investor can survive through the valley of strong security association, then the benefits will eventually accrue.

Although the benefits from diversification may disappear in the short-run, they should not be fully forgotten. Bonds, cash, and precious metals (i.e., gold) proved to be great portfolio diversifiers in 2008 and early 2009. Commodities, inflation protection, floating rate bonds, real estate, and alternative investments, are a few asset classes that will help diversify portfolios. Risk is defined in many circles as volatility (i.e., standard deviation) and combining disparate asset classes can lower volatility. But risk, defined as the potential of experiencing permanent losses, can also be controlled by focusing on valuation. By in large, large cap dividend paying stocks have struggled for more than a decade, despite equity dividend yields for the S&P 500 exceeding 10-year Treasury yields (the first time in more than 50 years). Investing in large companies with strong balance sheets and attractive growth prospects is another strategy of lowering portfolio risk.

Politics & Winston Churchill

Some factors however are out of shareholders hands, such as politics. As we know from last year’s debt ceiling melee and credit downgrade debacle, getting things done in Washington is very challenging. If you think achieving consensus in one country is difficult, imagine what it’s like in herding 17 countries? That’s the facts of life we are dealing with in the eurozone right now.

Although I am optimistic something will eventually get done, I consider myself a frustrated optimist. I am frustrated because of the gridlock, but optimistic because these problems are not rocket science. Rather these challenges are concepts my first grade child could understand:

• Expenses are running higher than revenues. You must cut expenses, increase revenues, or a combination thereof.

• Adding debt can support growth, but can lead to inflation. Cutting debt can hinder growth, but leads to a more sustainable fiscal state of wellbeing.

Relieving all the excess global leverage is a long, tortuous process. We saw firsthand here in the U.S. what happened to the U.S. real estate market and associated financial institutions when irresponsible debt consumption took place. Fortunately, corporations and consumers adjusted their all-you-can-eat debt buffet habits by going on a diet. As a matter of fact, corporations today are holding records amounts of cash and debt service loads for consumers has been reduced to levels not seen in decades (see chart below). Unlike governments, luckily CEOs and individuals do not need Congressional approval to adapt to a world of reality – they can simply adjust spending habits.

Source: Calafia Beach Pundit (Scott Grannis)

Governments, on the other hand, generally do need legislative approval to adjust spending habits. Regrettably, cutting the benefits of your constituents is not a real popular political strategy for accumulating votes or brownie points. If you don’t believe me, see what voters are doing to their leaders in Europe. Nicolas Sarkozy is the latest European leader to be booted from office due to austerity backlash and economic frustration. No less than nine European leaders have been cast aside since the financial crisis began.

The fate for U.S. politicians is less clear as we enter into a heated presidential election over the next six months. We do however know how the mid-term Congressional elections fared for the incumbents…not all sunshine and roses. Until elections are completed, we are resigned to the continued mind-numbing political gridlock, with no tangible resolutions to the trillion dollar deficits and gargantuan debt load. Obviously, most citizens would prefer a forward looking strategic plan from politicians (rather than a reactive one), but there are no signs that this will happen anytime soon…in either party.

Realistically though, tough decisions made by politicians only occur during crises, and if this slow-motion train wreck continues along this same path, then at least we have something to look forward to – forced resolution. We are seeing this firsthand in Greece. The “bond vigilantes” (see Plumbers & Cops) and responsible parents (i.e., Germany) have given Greece two options:

1.) Fix your financial problems and receive assistance; or

2.) Leave the EU (return to the Drachma currency) and figure your problems out yourself.

Panic has a way of forcing action, and we are approaching that “when push comes to shove” moment very quickly. I believe the Europeans are currently taking a note from our strategic playbook, which basically is the spaghetti approach – throw lots of things up on the wall and see what sticks. Or as Winston Churchill stated, “You can always count on Americans to do the right thing – after they’ve tried everything else.”

There is no question, the European sovereign debt issue is a complete mess, and there are no clear paths to a quick solution. Until voters force politicians into making tough unpopular decisions, or leaders come together with forward looking answers, the default position will be to keep kicking the fiscal can issues down the road. In the absence of political leadership, eventually the crisis will naturally force tough decisions to be made. Until then, I will go on explaining to others how the European dog ate my homework.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in AIG, JNJ, Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dominoes, Deleveraging, and Justin Bieber

Despite significant 2011 estimated corporate profit growth (+17% S&P 500) and a sharp rebound in the markets since early October (+18% since the lows), investors remain scared of their own shadows. Even with trembling trillions in cash on the sidelines, the Dow Jones Industrial Average is up +5.0% for the year (+11% in 2010), and that excludes dividends. Not too shabby, if you think about the trillions melting away to inflation in CDs, savings accounts, and cash. With capital panicking into 10-year Treasuries, hovering near record lows of 2%, it should be no surprise to anyone that fears of a Greek domino toppling Italy, the eurozone, and the global economy have sapped confidence and retarded economic growth.

Deleveraging is a painful process, and U.S. consumers and corporations have experienced this first hand since the financial crisis of 2008 gained a full head of steam. Sure, housing has not recovered, and many domestic banks continue to chew threw a slew of foreclosures and underwater loan modifications. However, our European friends are now going through the same joyful process with their banks that we went through in 2008-2009. Certainly, when it comes to the government arena, the U.S. has only just begun to scratch the deleveraging surface. Fortunately, we will get a fresh update of how we’re doing in this department, come November 23rd, when the Congressional “Super Committee” will update us on $1.2 trillion+ in expected 10-year debt reductions.

Death by Dominoes?

Is now the time to stock your cave with a survival kit, gun, and gold? I’m going to go out on a limb and say we may see some more volatility surrounding the European PIIGS debt hangover (Portugal/Italy/Ireland/Greece/Spain) before normality returns, but Greece defaulting and/or exiting the euro does not mean the world is coming to an end. At the end of the day, despite legal ambiguity, the ECB (European Central Bank) will come to the rescue and steal a page from Ben Bernanke’s quantitative easing printing press playbook (see European Deadbeat Cousin).

Greece isn’t the first country to be attacked by bond vigilantes who push borrowing costs up or the first country to suffer an economic collapse. Memories are short, but it was not too long ago that a hedge fund on ice called Iceland experienced a massive economic collapse. It wasn’t pretty – Iceland’s three largest banks suffered $100 billion in losses (vs. a $13 billion GDP); Iceland’s stock market collapsed 95%; Iceland’s currency (krona) dropped 50% in a week. The country is already on the comeback trail. Currently, unemployment (@ 6.8%) in Iceland is significantly less than the U.S. (@ 9.0%), and Iceland’s economy is expanding +2.5%, with another +2.5% growth rate forecasted by the IMF (International Monetary Fund) in 2012.

Iceland used a formula of austerity and deleveraging, similar in some fashions to Ireland, which also has seen a dramatic -15% decrease in its sovereign debt borrowing costs (see chart below).

Source: Bloomberg.com

OK, sure, Iceland and Ireland are small potatoes (no pun intended), so how realistic is comparing these small countries’ problems to the massive $2.6 trillion in Italian sovereign debt that bearish investors expect to imminently implode? If these countries aren’t credibly large enough, then why not take a peek at Japan, which was the universe’s second largest economy in 1989. Since then, this South Pacific economic behemoth has experienced an unprecedented depression that has lasted longer than two decades, and seen the value of its stock market decline by -78% (from 38,916 to 8,514). Over that same timeframe, the U.S. economy has seen its economy grow from roughly $5.5 trillion to $15.2 trillion.

There’s no question in mind, if Greece exits the euro, financial markets will fall in the short-run, but if you believe the following…

1.) The world is NOT going to end.

2.) 2012 S&P profits are NOT declining to $65.

AND/OR

3.) Justin Bieber will NOT run and overtake Mitt Romney as the leading Republican candidate

…then I believe the financial markets are poised to move in a more constructive direction. Perhaps I am a bit too Pollyannaish, but as I decide if this is truly the case, I think I’ll go play a game of dominoes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Solving Europe and Your Deadbeat Cousin

The fall holidays are quickly approaching, and almost every family has at least one black-sheep member among the bunch. You know, the unemployed second cousin who shows up for Thanksgiving dinner intoxicated – who then proceeds to pull you aside after a full meal to ask you for some money because of an unlucky trip to Las Vegas. For simplicity purposes, let’s name our deadbeat cousin Joe.

Right now the European union (EU) is dealing with a similar situation, but rather than being forced to deal with money-begging cousin named Joe, the EU is being forced to confront the irresponsible debt-binging practices of its own relatives – the PIIGS (Portugal, Ireland, Italy, Greece, and Spain). The European troika (International Monetary Fund/IMF; European Union/EU; and European Central Bank/ECB), spearheaded by German and French persuasion, is contemplating everything from prescribing direct bank recapitalization, bailouts via the leveraging of the EFSF (European Financial Stability Facility), ECB bond purchases, debt guarantees, unlimited central bank loans, and more.

New stress tests are being reevaluated as we speak. Previous tests failed in gaining the necessary credibility because inadequate haircuts were applied to the values of PIIGS debt held by European banks. European Leaders are beginning to gain some religion as to the urgency and intensity of the financial crisis. Just today, Germany’s chancellor (Angela Merkel) and France’s President (Nicolas Sarkozy) announced that they will introduce a comprehensive package of measures to stabilize the eurozone by the end of this month, right before the summit of the G20 leading global economies in Cannes, France.

Pick Your Poison

Whatever the path used to mop up debt excesses, the options for solving the financial mess can be lumped together in the following categories:

1. Austerity: Plain, unadulterated spending cuts is one prescription being administerd in hopes of curing bloated European sovereign debt issues. Negatives: Slowing economic growth, slowing tax receipts, potentially widening deficits (reference Greece), and political reelection self interests call into question the feasibility of the austerity option. Positives: Austerity is a morally correct fiscal response, which has the potential of placing a country’s financial situation back on a sustainable path.

2. Bailouts: The troika is also talking about infusing the troubled banks with new capital. Negatives: This action could result in more debt placed on country balance sheets, a potentially lower credit rating, higher costs of borrowing, higher tax burden for blameless taxpayers, and often an impossible political path of success. Positives: Financial markets may respond constructively in the short-run, but providing an alcoholic more alcohol doesn’t solve long-term fiscal responsibility, and also introduces the problem of moral hazard.

3. Haircuts: Voluntary or involuntary haircuts to principal debt obligations may occur in conjunction with previously described bailout efforts, depending on the severity of debt levels. Negatives: There are many different sets of constituents and investors, which can make voluntary haircut/debt restructuring terms difficult to agree upon. If the haircuts are too severe, banking reserves across the EU will become decimated, which will only lead to more austerity, bailouts, and potential credit downgrades. Such actions could hamper or eliminated future access to capital, and the cost of access to future capital could be cost prohibitive for the borrowing countries that defaulted/restructured. Positives: Haircuts eliminate or lessen the need for other more painful austerity or restructuring measures, and force borrowers to become more fiscally responsible, not to mention, investors are forced to conduct more thorough due diligence.

4. Printing Press: Buying back debt with freshly printed euros hot off the press is another strategy. Negatives: Inflation is an invisible tax on everyone, including those constituents who are behaving in a fiscally responsible manner. Positives: Not only is this strategy more politically palatable because the inflation tax is spread across the whole union, but this path to debt reduction also does not require as painful and unpopular cuts in spending as experienced in other options.

The Costs

What is the cost for this massive European debt-binging rehabilitation? Estimates vary widely, but a JP Morgan analyst sized it up this way as explained in the The Financial Times:

“In a worst-case, severe recession scenario, €230bn in new capital is needed to meet Basel III requirements, assuming a 60 per cent debt writedown on Greece, 40 per cent on Ireland and Portugal and 20 per cent on Italy and Spain, and that banks withhold dividends.”

More bearish estimates with larger bond loss haircuts, stricter regulatory guidelines, and harsher austerity measures have generated recapitalization numbers north of €1 trillion euros. Regardless of the estimates, European governments, regulators, and central banks are likely to select a combination of the poisons listed above. There is no silver bullet solution, and any of the chosen paths come with their own unique set of consequences.

As time passes and the European crisis matures, I am confident that you will be hearing more about ECB involvement and the firing-up of the printing presses. Perhaps the ECB will fund and work jointly with the EFSF to soak up debt and/or capitalize weak banks. Alternatively, and more simply, the ECB is likely to follow the path of the U.S. and implement significant amounts of quantitative easing (i.e., provide liquidity to the financial system via sovereign debt purchases and guarantees).

Dealing with irresponsible and intoxicated deadbeat second cousins (or European countries) fishing for money is never a pleasurable experience. There are many ways to address the problem, but ignoring the issue will only make the situation worse. Fortunately, our European friends on the other side of the pond appear to be taking notice. As in the U.S., if government officials delay or ignore the immediate problems, the financial market cops (a.k.a., “bond vigilantes”) will force them into action. In the recent past, European officials have used a strategy of sober talking “tough love,” but signs that the ECB printing presses are now beginning to warm up are evident. Once the euros come flying off the presses to detoxify the debt binging banks, perhaps the ECB can print a few extra euros for my cousin Joe.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}