Posts tagged ‘PE’

Searching for the Growth Stock Holy Grail

Remember Research in Motion (now Blackberry Limited – BBRY)? What about Krispy Kreme Doughnuts? How about Crocs (CROX)? Or maybe even Webvan, the online grocery delivery company that went bankrupt during the bursting of the dot-com bubble? These are all examples of once heralded growth companies that lost their mojo along their growth expansion ways.

Not every stock can grow to the $80+ billion market cap stratosphere like Apple Inc. (AAPL), Starbucks Corp. (SBUX), and Wal-Mart Stores (WMT), so finding companies with the right mixture of growth characteristics can be challenging. Objective stock market observers can disagree on the ingredients of a successful growth stock recipe, but generally speaking, the real explosive appreciation in stock prices come from those companies that can compound earnings growth over longer periods of time.

But how can one discover the Holy Grail of compounding earnings? At Sidoxia Capital Management, there are a handful of key factors we look for in successful growth companies. In the hyper-competitive global marketplace, these are crucial questions we want adequately answered before we invest our clients’ money:

- Does the company sell a product or service that cuts costs?

- Does the company offer a product or service with unique entertainment value?

- Does the company offer a superior product or service compared to its competitors?

Even if a target investment can affirmatively answer two or three of these questions, often the most important question is the following:

- Does the company have a sustainable competitive advantage in providing a product or service?

If the company does not have some type of durable competitive advantage, then some other company can just copy the product or service, and sell it at a lower price. This sadly leads to margin and P/E (Price-Earnings) multiple compression – both negative outcomes.

The aforementioned factors are not the end-all, be-all for successful growth stocks, but rather the minimum price of admission. Even if the previous criteria boxes are sufficiently checked off, the company being researched must still be fairly or attractively priced. For example, it doesn’t take a genius to figure out Apple is a successful company with unique advantages. More specifically, the company has $240 billion in cash, $50 billion in profits, and $215 billion in revenue. The real question becomes, is the stock fairly or attractively priced?

Although Apple appears attractively valued at current prices, in many other instances that is not the case. Often, great companies have been discovered by a large swath of investors, and therefore trade at significant premiums, which increases the risk profile or reduces the upside potential of the investment.

Sucking the Last Puff

If a company’s product or service isn’t superior, cut costs, or entertain at a reasonable/attractive valuation, then investing is like taking the last puff or drag out of a cigarette butt. Some value investors are good at this craft, but often these managers get caught into so-called “value traps” – ask Bill Ackman about Valeant Pharmaceuticals (VRX). Many value investors thought they found a bargain when they bought Valeant shares after it fell -80% in price. The stock subsequently has fallen another -50%…ouch!.

It’s worth noting that growth can come from many different areas. Even mature industries can produce periods of cyclical growth, however identifying cyclical winners is challenging. The art for the investment manager is determining whether growth in a target investment is sustainable. In many instances, companies temporarily benefit from a rising tide that lifts all boats, before the tide goes out and sinks fundamentals down to lower levels.

Growth investing can be a dangerous hobby for short-term traders because the price volatility stemming from ever-changing earnings growth expectations creates excessive trading, taxes, and transaction costs. However, for long-term investors, the great growth manager, T. Rowe Price, summed it up best here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

Growth investing is both a science and an art, but does not require a degree in rocket science. If you can focus on the important growth criteria, and combine it with a long-term disciplined valuation process, you will be well on your way to discovering the growth stock Holy Grail.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in VRX, BBRY, SBUX, WMT, CROX, Krispy Kreme, Webvan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Winning the Loser’s Game

During periods of heightened volatility like those recently experienced, it’s easy to get caught up in the emotional heat of the moment. I find time is better spent returning to essential investing fundamentals, like the ones I read in the investment classic by Charles Ellis, Winning the Loser’s Game – “WTLG”. To put my enthusiasm in perspective, WTLG has even achieved the elite and privileged distinction of making the distinguished “Recommended Reading” list of Investing Caffeine (located along the right-side of the page). Wow…now I know you are really impressed.

The Man, The Myth, the Ellis

For those not familiar with Charley Ellis, he has a long, storied investment career. Not only has he authored 12 books, including compilations on Goldman Sachs (GS) and Capital Group, but his professional career dates back prior to 1972, when he founded institutional consulting firm Greenwich Associates. Besides earning a college degree from Yale University, and an MBA from Harvard Business School, he also garnered a PhD from New York University. Ellis also is a director at the Vanguard Group and served as Investment Committee chair at Yale University along investment great David Swensen (read also Super Swensen) from 1992 – 2008.

For those not familiar with Charley Ellis, he has a long, storied investment career. Not only has he authored 12 books, including compilations on Goldman Sachs (GS) and Capital Group, but his professional career dates back prior to 1972, when he founded institutional consulting firm Greenwich Associates. Besides earning a college degree from Yale University, and an MBA from Harvard Business School, he also garnered a PhD from New York University. Ellis also is a director at the Vanguard Group and served as Investment Committee chair at Yale University along investment great David Swensen (read also Super Swensen) from 1992 – 2008.

With this tremendous investment experience come tremendous insights. The original book, which was published in 1998, is already worth its weight in gold (even at $1,384 per ounce), but the fifth edition of WTLG is even more valuable because it has been updated with Ellis’s perspectives on the 2008-2009 financial crisis.

Because the breadth of topics covered is so vast and indispensable, I will break the WTLG review into a few parts for digestibility. I will start off with the these hand-picked nuggets:

Defining the “Loser’s Game”

Here is how Charles Ellis describes the investment “loser’s game”:

“For professional investors, “the ‘money game’ we call investment management evolved in recent decades from a winner’s game to a loser’s game because a basic change has occurred in the investment environment: The market came to be dominated in the 1970s and 1980s by the very institutions that were striving to win by outperforming the market. No longer is the active investment manager competing with cautious custodians or amateurs who are out of touch with the market. Now he or she competes with other hardworking investment experts in a loser’s game where the secret to winning is to lose less than others lose.”

Underperformance by Active Managers

Readers that have followed Investing Caffeine for a while understand how I feel about passive (low-cost do-nothing strategy) and active management (portfolio managers constantly buying and selling) – read Darts, Monkeys & Pros. Ellis’s views are not a whole lot different than mine – here is what he has to say while not holding back any punches:

“The basic assumption that most institutional investors can outperform the market is false. The institutions are the market. They cannot, as a group, outperform themselves. In fact, given the cost of active management – fees, commissions, market impact of big transactions, and so forth-85 percent of investment managers have and will continue over the long term to underperform the overall market.”

He goes on to say individuals do even worse, especially those that day trade, which he calls a “sucker’s game.”

Exceptions to the Rule

Ellis’s bias towards passive management is clear because “over the long term 85 percent of active managers fall short of the market. And it’s nearly impossible to figure out ahead of time which managers will make it into the top 15 percent.” He does, however, acknowledge there is a minority of professionals that can beat the market by making fewer mistakes or taking advantage of others’ mistakes. Ellis advocates a slow approach to investing, which bases “decisions on research with a long-term focus that will catch other investors obsessing about the short term and cavitating – producing bubbles.” This is the strategy and approach I aim to achieve.

Gaining an Unfair Competitive Advantage

According to Ellis, there are four ways to gain an unfair competitive advantage in the investment world:

1) Physical Approach: Beat others by carrying heavier brief cases and working longer hours.

2) Intellectual Approach: Outperform by thinking more deeply and further out in the future.

3) Calm-Rational Approach: Ellis describes this path to success as “benign neglect” – a method that beats the others by ignoring both favorable and adverse market conditions, which may lead to suboptimal decisions.

4) Join ‘em Approach: The easiest way to beat active managers is to invest through index funds. If you can’t beat index funds, then join ‘em.

The Case for Stocks

Investor time horizon plays a large role on asset allocation, but time is on investors’ side for long-term equity investors:

“That’s why in the long term, the risks are clearly lowest for stocks, but in the short term, the risks are just as clearly highest for stocks.”

Expanding on that point, Ellis points out the following:

“Any funds that will stay invested for 10 years or longer should be in stocks. Any funds that will be invested for less than two to three years should be in “cash” or money market instruments.”

While many people may feel stock investing is dead, but Ellis points out that equities should return more in the long-run:

“There must be a higher rate of return on stocks to persuade investors to accept risks of equity investing.”

The Power of Regression to the Mean

Investors do more damage to performance by chasing winners and punishing losers because they lose the powerful benefits of “regression to the mean.” Ellis describes this tendency for behavior to move toward an average as “a persistently powerful phenomenon in physics and sociology – and in investing.” He goes on to add, good investors know “that the farther current events are away from the mean at the center of the bell curve, the stronger the forces of reversion, or regression, to the mean, are pulling the current data toward the center.”

The Power of Compounding

For a 75 year period (roughly 1925 – 2000) analyzed by Ellis, he determines $1 invested in stocks would have grown to $105.96, if dividends were not reinvested. If, however, dividends are reinvested, the power of compounding kicks in significantly. For the same 75 year period, the equivalent $1 would have grown to $2,591.79 – almost 25x’s more than the other method (see also Penny Saved is Billion Earned).

Ellis throws in another compounding example:

“Remember that if investments increase by 7 percent per annum after income tax, they will double every 10 years, so $1 million can become $1 billion in 100 years (before adjusting for inflation).”

The Lessons of History

As philosopher George Santayana stated – “Those who cannot remember the past are condemned to repeat it.” Details of every market are different, but as Ellis notes, “The major characteristics of markets are remarkably similar over time.”

Ellis appreciates the importance of history plays in analyzing the markets:

“The more you study market history, the better; the more you know about how securities markets have behaved in the past, the more you’ll understand their true nature and how they probably will behave in the future. Such an understanding enables us to live rationally with markets that would otherwise seem wholly irrational.”

Home Sweet International Home

Although Ellis’s recommendation to diversify internationally is not controversial, his allocation recommendation regarding “full diversification” is a bit more provocative:

“For Americans, this would mean about half our portfolios would be invested outside the United States.”

This seems high by traditional standards, but considering our country’s shrinking share of global GDP (Gross Domestic Product), along with our relatively small share of the globe’s population (about 5% of the world’s total), the 50% percentage doesn’t seem as high at first blush.

Beware the Broker

This is not new territory for me (see Financial Sharks, Fees/Exploitation, and Credential Shell Game), and Ellis warns investors on industry sales practices:

“Those oh so caring and helpful salespeople make their money by convincing you to change funds. Friendly as they may be, they may be no friend to your long-term investment success.”

Unlike a lot of other investing books, which cover a few aspects to investing, Winning the Loser’s Game covers a gamut of crucial investment lessons in a straightforward, understandable fashion. A lot of people play the investing game, but as Charles Ellis details, many more investors and speculators lose than win. For any investor, from amateur to professional, reading Ellis’s Winning the Loser’s Game and following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Going Shopping: Chicken vs. Beef

The headlines haven’t been very rosy over the last week, but when is that ever not the case? Simply put, gloom and doom sells. The Chinese stock market is collapsing; the Yuan is plummeting; there are rising tensions in the Middle East; terrorism is rising to the fore; and commodity prices are falling apart at the seams. This is only a partial snapshot of course, and does not paint a complete or accurate picture. Near record-low interest rates; record corporate profits (outside of energy); record-low oil prices; unprecedented accommodative central bank policies; and attractive valuations are but a few of the positive, countervailing factors that rarely surface through the media outlets.

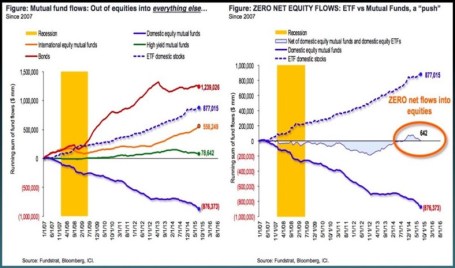

At the end of the day, smart long-term investors understand investing in financial markets is a lot like grocery store shopping. Similarly to stocks and bonds, prices at the supermarket fluctuate daily. Whether you’re comparing beef (bonds) and chicken (stocks) prices in the meat department (stock market), or apple (real estate) and orange (commodities) prices in the produce department (global financial markets), ultimately, shrewd shoppers eventually migrate towards purchasing the best values. Since the onset of the 2008-2009 financial crisis, risk aversion has dominated over value-based prudence as evidenced by investors flocking towards the perceived safety of cash, Treasury bonds, and other fixed income securities that are expensively priced near record highs. As you can see from the chart below, investors poured $1.2 trillion into bonds and effectively $0 into stocks. Consumers may still be eating lots of steaks (bonds) currently priced at $6.08/lb while chicken (stocks) is at $1.48/lb (see U.S. Department of Labor Data – Nov. 2015), but at some point, risk aversion will abate, and consumers will adjust their preferences towards the bargain product.

Some Shoppers Still Buying Chicken

While the general public may have missed the massive bull market in stocks, astute corporate executives and investment managers took advantage of the equity bargains in recent years, as seen by stock prices tripling from the March 2009 lows. As corporate profits and margins have marched to record levels, CEOs/CFOs put their money where their mouths are by investing trillions of dollars into share buybacks and mergers & acquisitions transactions.

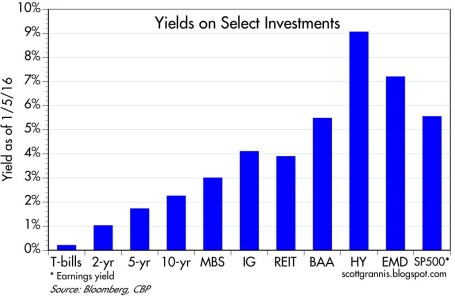

Despite the advance in the multi-year bull market, with the recent sell-off, panic has once again dominated rational thinking. We see this rare phenomenon (a few times over the last century) manifest itself through a stock market dividend yield that exceeds the yield on Treasury bonds (2.2% S&P 500 vs 2.1% 10-Year Treasury). But if we are once again comparing beef vs. chicken prices (bonds vs stocks), the 6% earnings yield on stocks (i.e., Inverse P/E ratio or E/P) now looks even more compelling relative to the 2% yield on bonds. For example, the iShares Core U.S. Aggregate Bond ETF (AGG) is currently yielding a meager 2.3%.

For a general overview, Scott Grannis at Calafia Beach Pundit summarizes the grocery store flyer of investment options below:

While these yield relationships can and will certainly change under various economic scenarios, there are no concrete signs of an impending recession. The recent employment data of 292,000 new jobs added during December (above the 200,000 estimate) is verification that the economy is not falling off a cliff into recession (see chart below). As I’ve written in the past, the positively-sloped yield curve also bolsters the case for an expansionary economy.

Source: Calafia Beach Pundit

While it’s true the Chinese economy is slowing, its rate is still growing at multiples of the U.S. economy. As a communist country liberalizes currency and stock market capital controls (i.e., adds/removes circuit breakers), and also attempts to migrate the economy from export-driven growth to consumer-driven expansion, periodic bumps and bruises should surprise nobody. With that said, China’s economy is slowly moving in the right direction and the government will continue to implement policies and programs to stimulate growth (see China Leaders Flag More Stimulus).

As we have recently experienced another China-driven correction in the stock market, and the U.S. economic expansion matures, equity investors must realize volatility is the price of admission for earning higher long-term returns. However, rather than panicking from fear-driven headlines, it’s times like these that should remind you to sharpen your shopping list pencil. You want to prudently allocate your investment dollars when deciding whether now’s the time to buy chicken (6% yield) or beef (2% yield).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including AGG, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Yellen is “Yell-ing” About High Stock Prices!

Earlier this week, Janet Yellen, chair of the U.S. Federal Reserve, spoke at the Institute for New Economic Thinking conference at the IMF headquarters in Washington, D.C. In addition to pontificating about the state of the global economy and the direction of interest rates, she also decided to chime in with her two cents regarding the stock market by warning stock values are “quite high.” She went on to emphasize “there are potential dangers” in the equity markets.

Unfortunately, those investors who have hinged their investment careers on the forecasts of economists, strategists, and Fed Chairmen have suffered mightily. Already, Yellen’s soapbox rant about elevated stock prices is being compared to former Fed Chairman Alan Greenspan’s “Irrational Exuberance” speech, which I have previously discussed on numerous occasions (see Irrational Exuberance Déjà Vu).

Greenspan’s bubble warning talk was given on December 5, 1996 when the NASDAQ closed around 1,300 (it closed at 5,003 this week). Greenspan specifically said the following:

“But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?”

After his infamous speech, the NASDAQ index almost quadrupled in value to 5,132 in the ensuing three years before cratering by approximately -78%,

Greenspan’s successor, economics professor Ben Bernanke, didn’t fare much better than the previous Fed Chairmen. Unlike many, I give full credit where credit is due. Bernanke deserves extra credit for his nimble but aggressive actions that helped prevent a painful recession from expanding into a protracted and lethal depression.

With that said, as late as May 2007, Bernanke noted Fed officials “do not expect significant spillovers from the subprime market to the rest of the economy.” Moreover, in 2005, near the peak in housing prices, Bernanke said the probability of a housing bubble was “a pretty unlikely possibility.” Bernanke went on to add housing price increases, “largely reflect strong economic fundamentals.” Greenspan concurred with Bernanke. Just a year prior, Greenspan noted that the increase in home values was “not enough in our judgment to raise major concerns.” History has proven how Bernanke and Greenspan could not have been more wrong.

If you still believe Yellen is the bee’s knees when it comes to the investing prowess of economists, perhaps you should review Long Term Capital Management (LTCM) debacle. In the midst of the 1998 Asian financial crisis, Robert Merton and Myron Scholes, two world renowned Nobel Prize winners almost single handedly brought the global financial market to its knees. Merton and Scholes used their lifetime knowledge of economics to create complex computerized investment algorithms. Everything worked just fine until LTCM lost $500 million in one day, which required a $3.6 billion bailout from a consortium of banks.

NASDAQ 5,000…Bubble Repeat?

Janet Yellen’s recent prognostication about the valuation of the U.S. stock market happens to coincide with the NASDAQ index breaking through the 5,000 threshold, a feat not achieved since the piercing of the technology bubble in the year 2000. Investing Caffeine readers and investors of mine understand today’s NASDAQ index is much different than the NASDAQ index of 15 years ago (see also NASDAQ Redux), especially when it comes to valuation. The folks at Bespoke put NASDAQ 5,000 into an interesting context by adding the important factor of inflation to the mix. Even though the NASDAQ index is within spitting distance of its all-time high of 5,132 (reached in 2000), the index would actually need to rally another +40% to reach an all-time “inflation adjusted” closing high (see chart below).

Source: Bespoke Investment Group

Economists and strategists are usually articulate, and their arguments sound logical, but they are notorious for being horribly bad at predicting the future, Janet Yellen included. I agree valuation is an all-important factor in determining future stock market returns. Howeer, by Robert Shiller, Janet Yellen, and a host of other economists relying on one flawed metric (CAPE PE), they have not only been wildly wrong year after year, but they are recklessly neglecting many other key factors (see also Shiller CAPE Smells Like BS).

I freely admit stocks will eventually go down, most likely a garden variety -20% recessionary decline in prices. While from a historical standpoint we are overdue for another recession (about two recessions per decade), this recovery has been the slowest since World War II, and the yield curve is currently not flashing any warning signals. When the eventual stock market decline happens, it likely will not be driven by high valuations. The main culprit for a bear market will be a decline in earnings – high valuations just act as gasoline on the fire. Janet Yellen will continue to offer her opinions on many aspects of the economy, but if she steps on her soapbox again and yells about stock market valuations, you will be best served by purchasing a pair of earplugs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Mathematics 101: The Cheap Money Printing Machine

Like many other bloggers and pundits, I have amply pontificated on the relative attractiveness of the stock market. For years, cash and gold hoarding bears have clung to the distorted, money-losing Shiller CAPE P/E ratio (see CAPE Smells Like B.S.), which has incorrectly signaled investors to stay out of stocks and miss trillions of dollars in price appreciation. Apparently, the ironclad Shiller CAPE device has been temporarily neutralized by the Federal Reserve’s artificially cheapening money printing press policies, just like Superman’s strength being stripped by the nullifying powers of kryptonite. The money printing logic seems so elegantly sound, I felt compelled to encapsulate this powerful relationship in an equation:

Interests Rate Cuts + Printing Press On = Stocks Go Higher

Wow, amazing…this is arithmetic any investor (or 3rd grader) could appreciate! Fortunately for me, I have a child in elementary school, so I became emboldened to share my new found silver bullet equation. I initially received a few raised eyebrows from my child when I introduced the phrase “Quantitative Easing” but it didn’t take long before she realized Rate Cuts + QE = Fat Piggy Bank.

After the intensive tutorial, I felt so very proud. With a smile on my face, I gave myself a big pat on the back, until I heard my child say, “Daddy, after looking at this squiggly S&P 500 line from 2007-2014, can you help my brain understand because I have some questions.”

Here is the subsequent conversation:

Me: “Sure kiddo, go ahead shoot…what can I answer for you?”

Child: “Daddy, if the Federal Reserve is so powerful and you should “not fight the Fed,” how come stock prices went down by -58% from 2007 – 2009, even though the Fed cut rates from 5.25% to 0%?”

Me: “Uhhhh….”

Child: “Daddy, if stock prices went down so much after massive rate cuts, does that mean stock prices will go up when the Fed increases rates?”

Me: “Uhhhh….”

Child: “Daddy, if Quantitative Easing is good for stock prices, how come after the QE1 announcement in November 2008, stock prices continued to go down -25%?”

Me: “Uhhhh….”

Child: “Daddy, if QE makes stocks go up, how come stock prices are at all-time record highs after the Fed has cut QE by -$70 billion per month and is completely stopping QE by 100% next month?”

Me: “Uhhhh….”

Child: “Daddy, everyone is scared of rate increases but when the Fed increased interest rates by 250 basis points in 1994, didn’t stock prices stay flat for the year?”

Me: “Uhhhh….” (See also 1994 Bond Repeat)

What started as a confident conversation about my bullet-proof mathematical equation ended up with me sweating bullets.

Math 101A: Low Interest Rates = Higher Asset Prices

As my previous conversation highlights, the relationship between rate cuts and monetary policy may not be as clear cut as skeptics would like you to believe. Although I enjoy the widely covered Shiller CAPE discussions on market valuations, somehow the media outlets fail to make the all-important connection between interest rates and P/E ratios.

One way of framing the situation is by asking a simple question:

Would you rather have $100 today or $110 a year from now?

The short answer is…”it depends.” All else equal, the level of interest rates will ultimately determine your decision. If interest rates are offering 20%, a rational person would select the $100 today, invest the money at 20%, and then have $120 a year from now. On the other hand, if interest rates were 0.5%, a rational person would instead select the option of receiving $110 a year from now because collecting a $100 today and investing at 0.5% would only produce $100.50 a year from now.

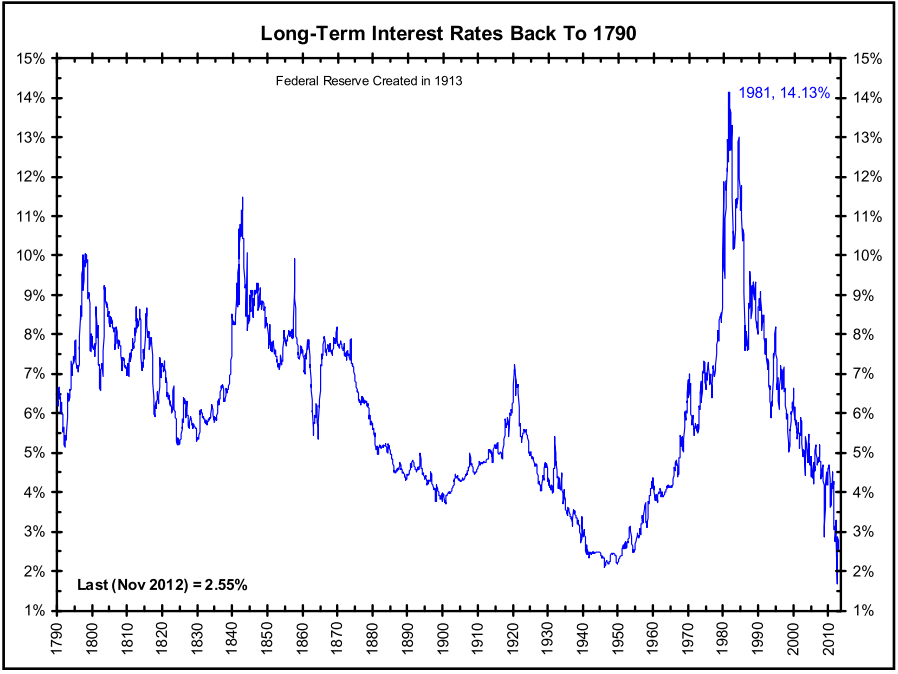

The same time-value-of-money principle applies to any asset, whether you are referring to gold, cars, houses, private businesses, stocks, or other assets. The mathematical fact is, all else equal, a rational person will always pay more for an asset when interest rates are low, and pay less when interest rates are high. As the 200-year interest chart below shows, current long-term interest rates are near all-time lows.

Source: The Big Picture

The peak in interest rates during the early 1980s correlated with a single digit P/E ratio (~8x). The current P/E ratio is deservedly higher (~16x), but it is dramatically lower than the 30x+ P/E ratio realized in the 2000 year timeframe. If none of this discussion makes sense, consider the simple Rule of 20 (see also The Rule of 20 Can Make You Plenty), which states as a simple rule-of-thumb, the average market P/E ratio should be equal to 20 minus the level inflation. With inflation currently averaging about 2%, the Rule of 20 implies an equilibrium of ~18x. If you assume this P/E multiple and factor in a 7-8% earnings growth rate, you could legitimately argue for 20% appreciation in the market to S&P 2,400 over a 12-month period. It’s true, a spike in interest rates, combined with a deceleration in earnings would justify a contraction in stock prices, but even under this scenario, current index values are nowhere near the bubble levels of 2000.

After six long years, the QE train is finally grinding to a halt, and a return towards Fed policy normalcy could be rapidly approaching. Many investors and skeptical bears have tried to rationalize the tripling in the market from early 2009 as solely due to the cheap Fed money printing machine. Unfortunately, history and mathematics don’t support that assertion. If you don’t believe me, perhaps a child may be able to explain it to you better.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

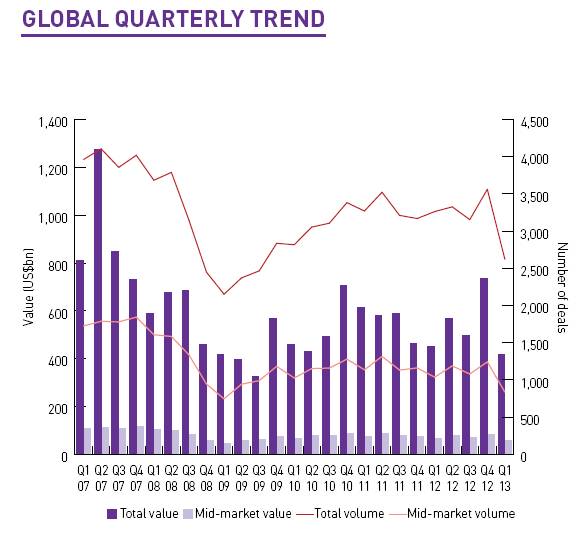

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

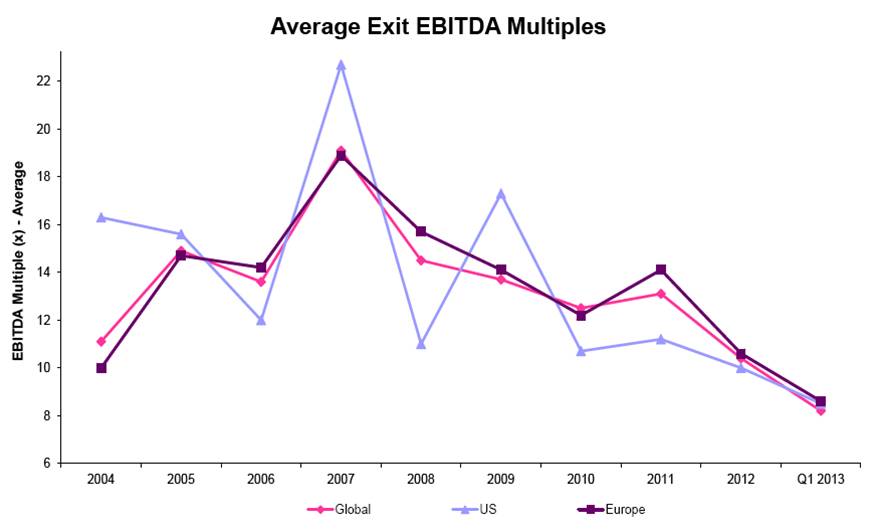

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Private Equity: Parasite or Pollinator?

In the wild, there exist both parasitic and symbiotic relationships. In the case of blood thirsty ticks that feed off deer, this parasitic relationship differs from the symbiotic association of nectar-sucking bees and pollen-hungry flowers. These are merely a few examples, but suffice it to say, these same intricate interactions occur in the business world as well.

Our economy is a complex jungle of relationships, spanning governments, businesses, consumers, investors, and many intermediaries, including private equity (PE) firms. With the November election rapidly approaching, more attention is being placed on how private equity firms fit into the economic food chain. Figuring out whether PE firms are more like profit-sucking parasites or constructive job creating mechanisms has moved to the forefront, especially given presidential candidate Mitt Romney’s past ties to Bain Capital, a successful private equity firm he founded in 1984.

Currently it is politically advantageous to portray PE professionals as greedy, job-cutting outsourcers – I’m still waiting for the political ad showing a PE worker clubbing a baby seal or plucking the legs off of a Daddy Long Legs spider. While I’d freely admit a PE pro can be just as gluttonous as an investment banker, hedge fund manager, or venture capitalist, simplistic characterizations like these miss the beneficial effects these firms provide to the overall economy. Capitalism is the spine that holds our economy together and has allowed us to grow into the greatest superpower on the planet. Private equity is but a small part of our capitalistic ecosystem, but plays a valuable role nonetheless.

While there are many perspectives on the role of private equity in our economy, here are my views on a few of the hot button issues:

Job Creation: Although I believe PE firms are valuable to our economy, I think it is a little disingenuous of Romney and his supporters to say Bain was a net “job creator” to the tune of 100,000+ jobs during his tenure. The fact of the matter is PE firms’ priority is to create profitable returns for its investors, and if that requires axing heads, then so be it – most PE firms have no qualms doing precisely that. Romney et al point to successes like Staples Inc. (SPLS), Dominos Pizza Inc. (DPZ) and Sports Authority, Inc., where profitability and success ultimately led to job expansion. From my viewpoint, I believe these examples are more the exception than the rule. Not surprisingly, any job losses executed in the early years of a PE deal will eventually require job additions if the company survives and thrives. Let’s face it, no company can cut its way to prosperity in perpetuity.

Competitveness: Weak, deteriorating, or bankrupt companies cannot and will not hire. Frail or mismanaged companies will sooner or later be forced to cut jobs on their own –the same protocol applied by opportunistic PE vultures swarming around. While PE firms typically focus on bloated or ineffective companies, I think the media outlets overemphasize the cost-cutting aspects of these deals. Sure, PE companies cut jobs, outsource functions, and cut benefits in the name of profits, but that alone is not a sustainable strategy. Trimming fat, by replacing complacent management teams, investing in modern software/equipment, expanding markets, and implementing accountability are all paramount factors in making these target companies more efficient and competitive in the long-run.

Financial Markets-Arbiter: At the end of the day, I think the IPO/financial markets are the final arbiters of how much value PE firms create, not only for investors, but also for the economy overall. If greedy PE firms’ sole functions were to saddle companies with massive debts, cut heads off, and then pay themselves enormous dividends, then there would never be a credible exit strategy for investors to cash out. If PE firms are correctly performing their jobs, then they will profitably create leaner more efficient durable companies that will be able to grow earnings and create jobs over the long-term. If they are unsuccessful in this broad goal, then the PE firm will never be able to profitably exit their investment via a corporate sale or public offering.

Bain Banter: Whether you agree with PE business practices or not, it is difficult to argue with the financial success of Bain Capital. According to a Wall Street Journal article, Bain Capital deals between 1984 – 1999 produced the following results:

“Bain produced about $2.5 billion in gains for its investors in the 77 deals, on about $1.1 billion invested. Overall, Bain recorded roughly 50% to 80% annual gains in this period, which experts said was among the best track records for buyout firms in that era.”

Critics are quick to point out the profits sucked up by PE firms, but they neglect to acknowledge the financial benefits that accrue to the large number of pension fund, charity, and university investors. Millions of middle-class American workers, retirees, community members, teachers, and students are participating in those same blood sucking profits that PE executives are slurping down.

Even though I believe private equity is a net-positive contributor to competiveness and economic growth in recent decades, there is no question in my mind that these firms participated in a massive bubble in the 2005-2007 timeframe. Capital was so cheap and abundant, prices on these deals escalated through the roof. What’s more, the excessive amounts of leverage used in those transactions set these deals up for imminent failure. PE firms and their investors have lost their shirts on many of those deals, and the typical 20%+ historical returns earned by this asset class have become long lost memories. Attractive returns do not come without risk.

With the presidential election rhetoric heating up, the media will continue to politicize, demonize and oversimplify the challenges surrounding this asset class. Despite its shortcomings, private equity will continue to have a positive symbiotic relationship with the economy…rather than a parasitic one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in SPLS, DPZ, Sports authority, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Darwin Meets Capitalism & Private Equity

Source: Photobucket

A rising discontent is spreading like wildfire in the wake of a massive financial crisis that erupted in the U.S. during 2008, and is now working its way through Europe. Irresponsible governments across the globe succumbed to the deceptive allure of leverage, and as a result racked up colossal debts and gargantuan deficits. Now governments everywhere are toggling between political gridlock and painful austerity. Citizens are feeling the pain through high unemployment, exploding education costs, crumbling social safety nets, and a general decline in the standard of living.

As a result of these dramatic changes, the contributions of capitalism are being questioned by many, whether it’s the Occupy Wall Street movement attack on the top 1%, or more recently the assault on private equity’s relevancy for a presidential candidate.

Although the media may prefer to sensationalize economic stories and tell observers, “This time is different” to boost viewership, usually the truth relies more on the nuanced evolution of issues over time. If Charles Darwin were alive today, he would understand that capitalism and democracies are evolving to massive changes in globalization, technology, and emerging markets. Darwin would appreciate the fact that capitalism can’t and won’t change overnight. Whether capitalism ultimately survives or goes extinct depends on how it adapts. Or as Darwin characterizes evolution:

It is not the strongest of the species that survives, nor the most intelligent, but the most responsive to change.

Will Capitalism Survive?

Capitalism and democracy fit like a hand in a glove, which explains why both have thrived for generations. Never mind that democracies have been around for centuries and their expansion continues unabated (see Spreading the Seeds of Democracy), nevertheless pundits feel compelled to question the sustainability of these institutions.

I guess the real response to all those experts who question the merits of capitalism is what alternative would serve us better? Would it be Socialism like we see grinding Europe to a halt? Or perhaps Communism working its wonders in North Korea and Cuba? If not that, then surely the Autocracies in Egypt and Libya are the winning formulas? The Occupy Wall Streeters may not be happy with their personal plight or the top 1%, but I don’t see them packing their bags for Greece, the Middle East or China.

There is arguably a growing disparity between rich and poor and the game of globalization is only making it more difficult for rising tides of growth to lift up our middle class. The beauty of capitalism is that money goes where it is treated best. Capitalism sucks money to the areas of the world that are the freest, most open, transparent, and practice the rule of law. Some of these components of American capitalism unquestionably eroded over the last decade or so, but the good thing is that in a democracy, citizens have the right to vote and elect growth-promoting leaders to fix problems. Growth comes from competitiveness, and competitiveness is derived from education, innovation, and pro-growth policies. Let’s hope the 2012 elections get agents of change in office.

Darwin & Private Equity

Republican Presidential primary candidate Mitt Romney has been raked over the coals for his prior professional career at private equity firm, Bain Capital. I’m convinced Charles Darwin would see private equity’s involvement as a critical factor in the process of global commerce. Businesses are like species, and only the fittest will survive.

Private equity firms prey upon weak businesses, looking to restructure and reorganize them to become more competitive. If private equity companies are bullies, then their business targets can be considered weaklings. Beating wimps into shape may not be fun to watch, but is a crucial evolutionary aspect of business. The fact of the matter is that deteriorating, uncompetitive companies cannot hire employees…only profitable, viable entities can createsustainable jobs. So our public policy officials have two choices:

• Prop up uncompetitive businesses inefficiently with tax dollars that save jobs in the short-run, but lead to bankruptcy and massive job losses in the future. Other unproductive tariffs and bailouts may garner short-term political votes, but only lead to long-term stagnancy.

OR

• Trim fat, restructure and reorganize now – similar to the swift pain experienced from extracting a rotted tooth. Jobs may be cut in the short-run, but a long-term competitively positioned company will be able to grow and create sustainable long-term jobs.

I can’t say I agree with all of private equity practices, such as leveraged recapitalizations – the practice in which private equity companies load up the target with debt so big fat dividends can be sucked out by the principals. But guess what? By doing so the principals are only reducing their own future exit value through a potential IPO (Initial Public Offering) or company sale. Moreover, if this is such an evil practice, lenders can curb the practice by simply not giving the private equity companies the needed borrowing capacity.

Capitalism and its private equity subset have gotten quite a bad rap lately, but I believe these forces are essential aspects for the rising standards of living for billions of people across the planet. When first introduced, Charles Darwin’s theory of evolution by natural selection was critically examined by many non-believers. Although capitalism will be forced to adapt to an ever-changing world and its merits have been questioned too, the chances of capitalism going extinct are about as likely as the extinction of Darwin’s evolutionary theory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Rule of 20 Can Make You Plenty

There is an endless debate over whether the equity markets are overvalued or undervalued, and at some point the discussion eventually transitions to what the market’s appropriate P/E (Price-Earnings) level should be. There are several standard definitions used for P/Es, but typically a 12-month trailing earnings, 12-month forward earnings (using earnings forecasts), and multi-year average earnings (e.g., Shiller 10-year inflation adjusted P/E – see Foggy P/E Rearview Mirror) are used in the calculations. Don Hays at Hays Advisory (www.haysadvisory.com) provides an excellent 30+ year view of the historical P/E ratio on a forward basis (see chart below).

Blue Line: Forward PE - Red Line: Implied Equilibrium PE (Hays Advisory)

If you listen to Peter Lynch, investor extraordinaire, his “Rule of 20” states a market equilibrium P/E ratio should equal 20 minus the inflation rate. This rule would imply an equilibrium P/E ratio of approximately 18x times earnings when the current 2011 P/E multiple implies a value slightly above 11x times earnings. The bears may claim victory if the earnings denominator collapses, but if earnings, on the contrary, continue coming in better than expected, then the sun might break through the clouds in the form of significant price appreciation.

Just because prices have been chopped in half, doesn’t mean they can’t go lower. From 1966 – 1982 the Dow Jones Industrial index traded at around 800 and P/E multiples contracted to single digits. That rubber band eventually snapped and the index catapulted 17-fold from about 800 to almost 14,000 in 25 years. Even though equities have struggled at the start of this century, a few things have changed from the market lows of 30 years ago. For starters, we have not hit an inflation rate of 13% or a Federal Funds rate of 20% (~3.5% and 0% today, respectively), so we have some headroom before the single digit P/E apocalypse descends upon us.

Fed Model Implies Equity Throttle

Hays Advisory exhibits another key valuation measurement of the equity market (the so-called “Fed Model”), which compares the Treasury yield of the 10-year Note with the earnings yield of stocks (see chart below).

Blue Line: 10-Yr Treasury - Red Line: Forward PE (Hays Advisory)

Regardless of your perspective, the divergence will eventually take care of it in one of three ways:

1.) Bond prices collapse, and Treasury yields spike up to catch up with equity yields.

2.) Forward earnings collapse (e.g., global recession/depression), and equity yields plummet down to the low Treasury yield levels.

AND/OR

3.) Stock prices catapult higher (lower earnings yield) to converge.

At the end of the day, money goes where it is treated best, and at least today, bonds are expected to treat investors substantially worse than the unfaithful treatment of Demi Moore by Ashton Kutcher. The Super Committee may not have its act together, and Europe is a mess, but the significant earnings yield of the equity markets are factoring in a great deal of pessimism.

The holidays are rapidly approaching. If for some reason the auspice of gifts is looking scarce, then review the Fed Model and Rule of 20, these techniques may make you plenty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Mr. Market Bullying Investors

Source: Photobucket

There’s been a bully pushing investor’s around and his name is “Mr. Market.” Volatility is Mr. Market’s partner in crime, and over the last 10 trading days Mr. M has used volatility to school equity investors to the tune of 1,600+ point swings, which has contributed to equity investors’ failing grade over the last few months. Who is Mr. Market? Charles Ellis, author of Winning the Loser’s Game (1998) described him best:

“Mr. Market is a mischievous but captivating fellow who persistently teases investors with gimmicks and tricks such as surprising earnings reports, startling dividend announcements, sudden surges of inflation, inspiring presidential announcements, grim reports of commodities prices, announcements of amazing new technologies, ugly bankruptcies, and even threats of war.”

How has Mr. Market been stealing investors’ lunch money? The process really hasn’t been that difficult for him, once you consider how many times investors have been heaved into the garbage can over the last decade, forced to deal with these messy events:

• 2001 technology bubble beating

• 2006 real estate collapse

• 2008 – 2009 financial crisis and recession

• 2010 “flash crash” and soft patch

• 2011 debt ceiling debate and credit rating downgrade

With this backdrop, investors are dropping like flies due to extreme bully fatigue. Over the last four months alone, approximately $75 billion in equities been liquidated, according to data from the Investment Company Institute – this is even more money withdrawn than the outflows occurring during the peak panic months after the Lehman Brothers collapse.

The Atomic Wedgie

Exhibit I (Source: Photobucket)

Mr. Market understands the severity of these prior economic scars, which have been even more painful than atomic wedgies (reference Exhibit I above), so he opportunistically is taking advantage of fragile nerves. Introducing the following scary scenarios makes collecting lunch money from panicked investors much easier for Mr. Market. What is he using to frighten investors?

- A potential Greek sovereign debt default that will trigger a collapse of the Euro.

- Slowing growth in China due to slowing developed market economic activity.

- Possible double-dip recession in the U.S. coupled with an austerity driven downturn in Europe.

- Lack of political policy response to short and long-term economic problems in Washington and abroad.

- Impending deflation caused by decelerating global growth or likely inflation brought about by central banks’ easy monetary policies (i.e., printing money).

- End of the world.

Bully Victim Protection

Of course, not all of these events are likely to occur. As a matter of fact, there are some positive forming trends, besides just improving valuations, that provide protection to bully victims:

- Not only is the earnings yield (E/P – 12-month trailing EPS/share price) trouncing the yield on the 10-year Treasury note (~8% vs. ~2%, respectively), but the dividend yield on the S&P 500 index is also higher than the 10-year Treasury note yield (source: MarketWatch). Historically, this has been an excellent time to invest in equities with the S&P 500 index up an average of 20% in the ensuing 12 months.

- Jobs data may be poor, but it is improving relative to a few years ago as depicted here:

Source: Calafia Beach Pundit

Source: Calafia Beach Pundit

- Record low interest rates and mortgage rates provide a stimulative backdrop for businesses and consumers. Appetite for risk taking remains low, but as history teaches us, the pendulum of fear will eventually swing back towards greed.

Source: Calafia Beach Pundit

As I say in my James Carville peace from earlier this year, It’s the Earnings Stupid, long term prices of stocks follow the path of earnings. Recent equity price market declines have factored in slowing in corporate profits. How severely the European debt crisis, and austerity have (and will) spread to the U.S. and emerging markets will become apparent in the coming weeks as companies give us a fresh look at the profit outlook. So far, we have gotten a mixed bag of data. Alpha Natural Resources (ANR) acknowledged slowing coal demand in Asia and FedEx Corp. (FDX) shave its fiscal year outlook by less than 2% due to international deceleration. Other bellwethers like Oracle Corp. (ORCL) and Nike Inc. (NKE) reported strong growth and outlooks. In the short-run Mr. Market is doing everything in his power to bully investors from their money, and lack of international policy response to mitigate the European financial crisis and contagion will only sap confidence and drag 2011-2012 earnings lower.

Punching Mr. Market

The warmth of negative real returns in cash, bonds, and CDs may feel pleasant and prudent, but for many investors the lasting effects of inflation erosion will inflict more pain than the alternatives. For retirees with adequate savings, these issues are less important and focus on equities should be deemphasized. For the majority of others, long-term investors need to reject the overwhelming sense of fear.

As I frequently remind others, I have no clue about the short-term direction of the market, and Greece could be the domino that causes the end of the world. But what I do know is that history teaches us the probabilities of higher long-term equity returns are only improving. Mr. Market is currently using some pretty effective scare tactics to bully investors. For those investors with a multi-year time horizon, who are willing to punch Mr. Market in the nose, the benefits are significant. The reward of better long-term returns is preferable to an atomic wedgie or a head-flush in the toilet received from Mr. Market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and FDX, but at the time of publishing SCM had no direct position in ANR, ORCL, NKE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}