Posts tagged ‘payout ratio’

The Gift that Keeps on Giving

There have been numerous factors contributing to this bull market, even in the face of a slew of daunting and exhausting headlines. Contributing to the advance has been a steady stream of rising earnings; a flood of price buoying stock buybacks; and the all-important gift of growing dividends that keep on giving. Bonds have benefited to a lesser extent than stocks over the last five years in part because bonds lack the gift of rising dividend payouts. Life would be grander for bondholders, if the issuers had the heart to share generous news like this:

“Good day Mr. & Mrs. Jones. As your bond issuer, we value our mutually beneficial relationship so much that we would like to reward you as a bond investor. In addition to the 2.5% we are paying you now, we have decided to increase your annual payments by 6% per year for the next 20 years. In other words, we will increase your $2,500 in annual interest payments to over $8,000 per year. But wait…there’s more! You are such great people, we are going to increase the value of your initial $100,000 investment to $450,000.”

Does this sound too good to be true? Well, it’s not…sort of. However, the scenario is absolutely true, if you invested $100,000 in S&P 500 stocks during 1993 and held that investment until today. Unfortunately, the gift giving conversation above would be unattainable and the furthest from the truth, if you invested $100,000 into bonds. Today, if you decided to invest $100,000 in 20-year government bonds paying 2.5%, your $2,500 in annual payments will never increase over the next two decades. What’s more, by 2034 your initial principal of $100,000 won’t increase by a penny, while inflation slowly but surely crushes your investment’s purchasing power.

To illustrate the magical power of dividend compounding at a 6% CAGR, here is a chart of the S&P 500 dividend stream over the 21-year period of 1993 – 2014:

The trend of increasing dividends doesn’t appear to be slowing either. Here is a table showing the number of S&P 500 companies increasing their dividend payouts:

| COUNT OF DIVIDEND ACTIONS YEAR-TO-DATE | INCREASING THEIR DIVIDEND |

| 2014 YTD | 292 |

| 2013 | 366 |

| 2012 | 333 |

| 2011 | 320 |

| 2010 | 243 |

| 2009 | 151 |

Source: Standard and Poor’s

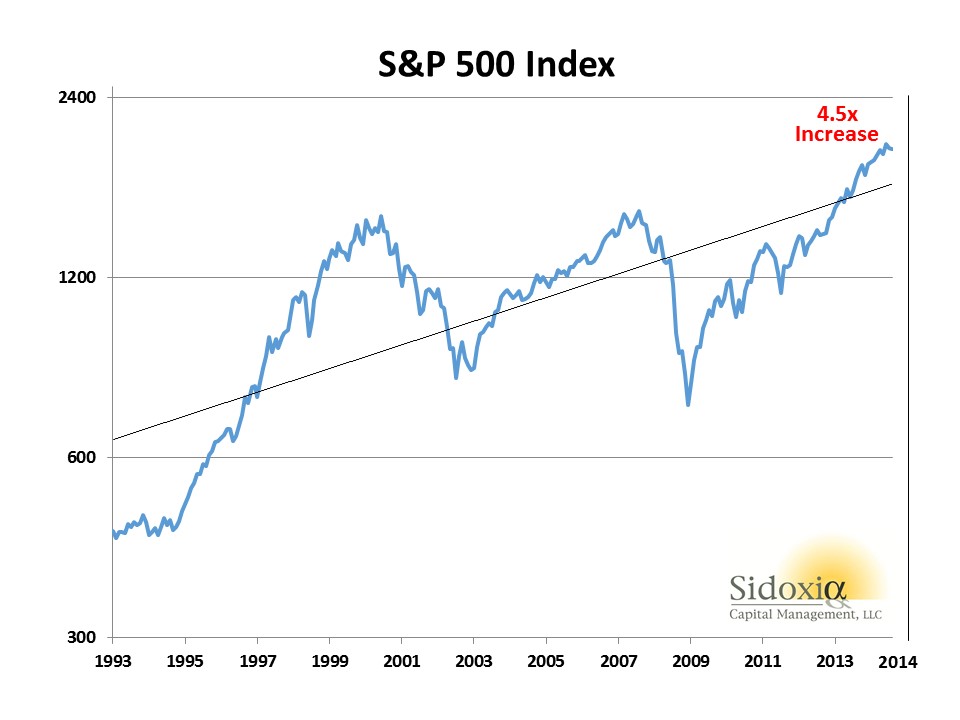

As I mentioned before, while dividends have more than tripled over the last twenty years, stock prices have gone up even more – appreciating about 4.5x’s (see chart below):

With aging demographics increasing retirement income needs, it comes as no surprise to me that the percentage of S&P 500 companies paying dividends has increased from 71% (351 companies) in 2001 to 84% (423 companies) at the end of Q3 – 2014. Interestingly, all 30 members of the Dow Jones Industrial Average currently pay a dividend. If you broaden out the perspective to all S&P Dow Jones Indices, you will discover the strength of dividends is particularly evident over the last 12 months. During this period, dividends increased by a whopping +27%, or $55 billion.

This trend in increasing dividends can also be seen through the lens of the dividend payout ratio. It is true that over longer timeframes the dividend payout ratio has been coming down (see Dividend Floodgates Widen) because of share buyback tax efficiency. Nevertheless, more recently the dividend payout ratio has drifted upwards to a range of about 32% of profits since 2011 (see chart below):

Source: FactSet

There’s no disputing the benefit of rising stock dividends. Baby Boomers, retirees, and other long-term investors are increasingly reaping the rewards of these dividend gifts that keep on giving.

Other Investing Caffeine articles on dividends:

Dividends: From Sapling to Abundant Fruit Tree

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including SPY, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Microsoft Makes Dividend Splash

Source: ActingLikeAnimals.com

I’ve talked about growing profits and cash piles for a while now (read more), but at some point investors and board members get restless and demand action (Steve Jobs has not yet). The most recent blue-chip company to make a splash, when it comes to capital management, is Microsoft Corp. (MSFT), which just announced a significant +23% increase in its dividend in conjunction with $4.75 billion in debt offerings. These capital structure changes still leave plenty of room for additional share repurchases and acquisitions.

Debt Offering – Are You Sure?

Huh? What in the heck is Microsoft doing borrowing money? I mean, does a company with $44 billion in cash and investments, generating a whopping additional $22 billion in free cash flow in fiscal 2010 (ended in June), really need access to additional capital? The short answer is “NO.” But a company like Microsoft borrowing $4.75 billion is like Donald Trump borrowing $50 on his credit card. Well wait, “The Donald” has actually had some hair and Chapter 11 problems, so the more appropriate analogy would be Bill Gates borrowing $20 on his credit card. Not only is it a rounding error, but it’s a good financial management practice for corporations to take advantage of the debt tax shield (read definition).

What makes Microsoft’s debt issuance that much more incredible is the astonishingly low rates the company is paying investors on the debt. According to Dealogic, Microsoft set a record low for yield paid on corporate unsecured debt. For the separate maturities ranging from 2013 to 2040, Microsoft paid a stunningly low 25-83 basis point spread over Treasuries. I don’t want to get into government credit worthiness today, but who knows, maybe Microsoft will pay lower debt rates than the U.S. Treasury, in the not too distant future?!

Regardless of the array of capital structure management strategies used by other companies, Microsoft is not alone in dealing with its cash hoarding problems. Cisco Systems Inc. (CSCO), another blue-chip cash printing press, just announced the initiation of a 1-2% dividend to be paid by the end of their fiscal year ending in July 2011 (read more about dividend cash “un-hoarding”).

But Who Cares?

Who cares about Microsoft’s wimpy 2.62% yield anyway? Well, for one, I sure care! A 10-year Treasury Note is yielding a measly, static 2.55%. If Microsoft continued on the same dividend path growth over the next five years as it did over the last five years, investors could potentially be talking about a 5.2% yield on our initial investment, and this excludes any potential stock price appreciation. With only roughly a 25% payout ratio on Microsoft’s fiscal 2010 free cash flow, the company has a lot of freedom to hike future dividends, even if earnings don’t grow. Microsoft has also enhanced shareholder value by putting its money where its mouth is by purchasing over $30 billion of company stock over the last three years.

Nice trend in dividend growth.

The extreme case of dividend growth is Wal-Mart Stores (WMT), which if purchased in 1972 would provide a +2,300% yield on the original investment, excluding any benefit from the massive price appreciation ($.05 split-adjusted per share to $53.65). Microsoft is no young chick like Wal-Mart 40 years ago, but you get the gist (read Dividend Sapling to Fruit Tree).

So while strategists and economists fret about the possibilities of a “double dip” recession, in the interim there have been 179 companies in the S&P 500 index that have hiked dividends in 2010 (versus only 3 companies that have cut). Microsoft has been no slouch either, growing revenues by +22% and EPS (Earnings Per Share) by +50% in their most recent fiscal fourth quarter. Although Microsoft’s stock is down -20% for 2010, the capital management and dividend splash recently announced by Microsoft (and other companies) should eventually capture the eye of investors currently earning squat on overpriced bonds and almost worthless Certificates of Deposit.

Read complete Microsoft dividend story

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, CSCO, nd WMT, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}