Posts tagged ‘oil sands’

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

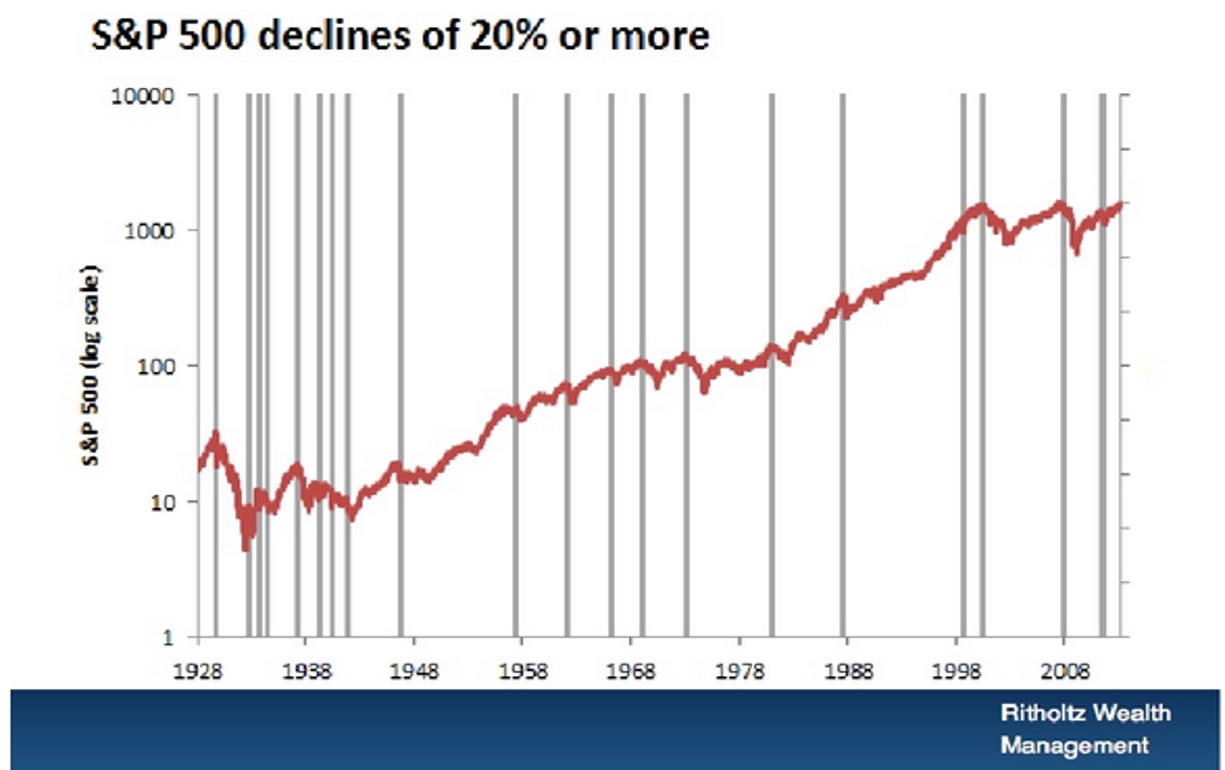

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Green Loses to Greenback

We are currently in a political environment that sees no gray, but rather only sharp contrasts in black and white. As it turns out, these three colors are not the winners or losers – the winner is the almighty “greenback” and the loser is the “green” movement. The so-called environmentally friendly Obama administration recently approved the Alberta Clipper project – a 1,000 mile pipeline being built by Endbridge Energy that is designed to carry 800,000 barrels of fuel from Canada to the U.S.

As our reliance on what New York Times journalist Tom Friedman calls the “petro dictators” has not gone away, the recent decision seems very rational in securing supplies from friendlier neighbors. However, environmental constituents like the Sierra Club feel differently:

“At a time when concern is growing about the national security threat posted by global warming, it doesn’t make sense to open our gates to one of the dirtiest fuels on earth.”

-Carl Pope (Executive Director of the Sierra Club)

As far as I’m concerned, we still import about 2/3 of our oil and until alternative energies become more cost effective, we have little choice but to explore a multitude of strategic supply agreements. Canada is a neighbor and ally, therefore the U.S. should not walk away from any similar future agreement that will bring a stable and reliable source of supply. The scarcity of the critical resource and other commodities is evident by strategic deals and acquisitions being made by China and its government (See previous Investing Caffeine article, “The China Vacuum, Sucking Up Assets”).

As economic hungry emerging markets seek expansionary policies, I expect to see even more of these international types of deals.

The oil-sands region in the Athabasca region (about the size of Florida) of Alberta holds great promise. If you believe famous oil investor/speculator T. Boone Pickens and other pundits, the oil-sands region holds the equivalent amount of reserves as world supply leader Saudi Arabia – about 250 billion barrels.

I concur with recent comments Financial Times article that says the Endbridge Energy deal meets a number of U.S. strategic interests, including:

“Increasing the diversity of oil supplies for the U.S., amid political tension in many major oil-producing regions; shortening the transportation path for crude oil supplies; and increasing crude oil supplies from a major non-Organization of Petroleum Exporting Countries producer.”

I am not a believer in damaging our environment for the pure sake of profits, however in this competitive global economy I think we need to seek an aggressive dual-source supply of energy (alternative energy AND traditional petroleum/coal products). The fact of the matter is that we have been pursuing solar, wind, nuclear, and other alternative energy resources for decades with very limited success. More financial resources and subsidies must be thrown at these alternative resource possibilities, while we simultaneously seek strategic supplies like this Canadian oil-sands deal.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and its clients have direct investment exposure in companies investing in Canadian oil-sand projects (SU) at the time the article was published. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}