Posts tagged ‘Obama’

Politics & COVID Tricks

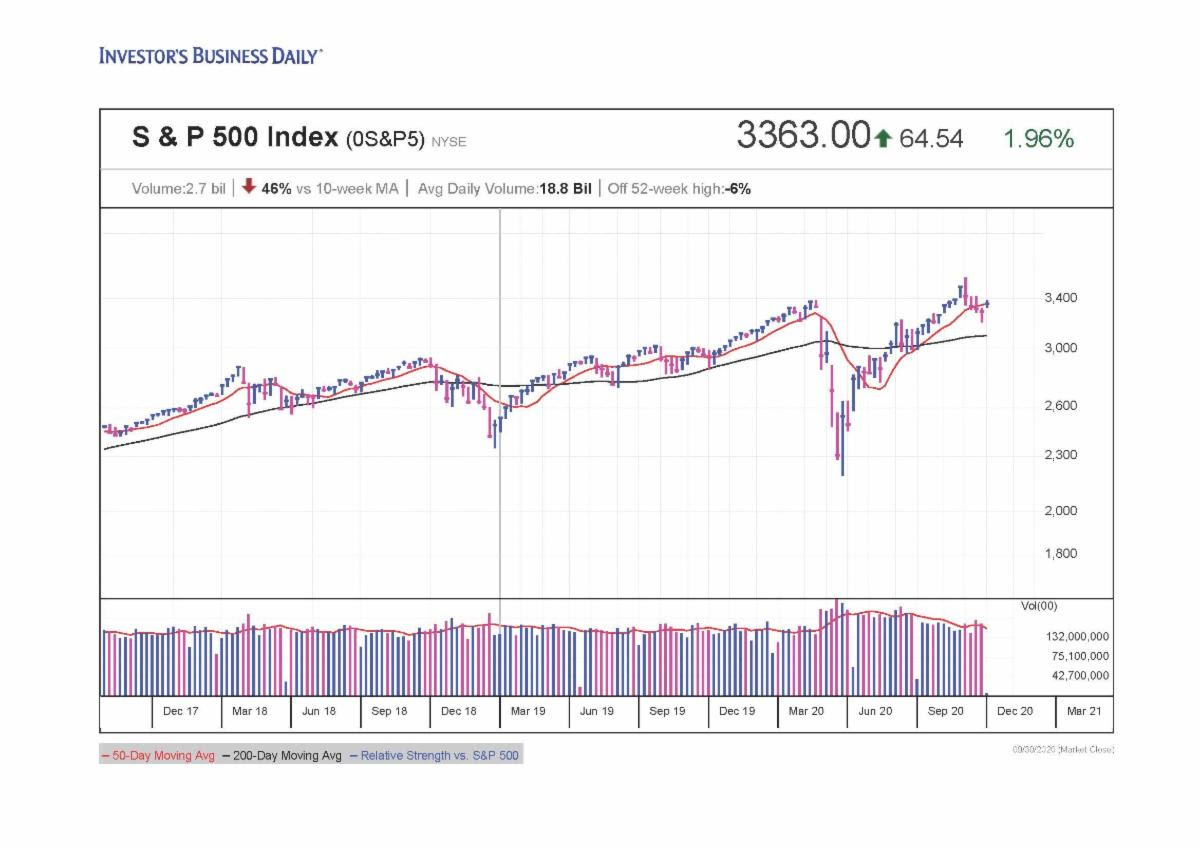

Thanks to a global epidemic, trillions of dollars instantly disappeared during the first quarter of this year, and then, abracadabra…the losses turned into gains and magically reappeared in the subsequent two quarters. After a stabilization in the spread of the COVID-19 virus earlier this year, the stock market rebounded for five consecutive months, at one point rebounding +64% (from late March to early September) – see chart below. However, things became a little bit trickier for the recent full month as concerns heightened over the outcome of upcoming elections; uncertainty over a potential coronavirus-related stimulus package agreement; and fears over a fall resurgence in COVID-19 cases. Although the S&P 500 stock index fell -3.9% and the Dow Jones Industrial Average slipped -2.3% during September, the same indexes levitated +8.5% and +7.6% for the third quarter, respectively.

Source: Investors.com

Washington Worries

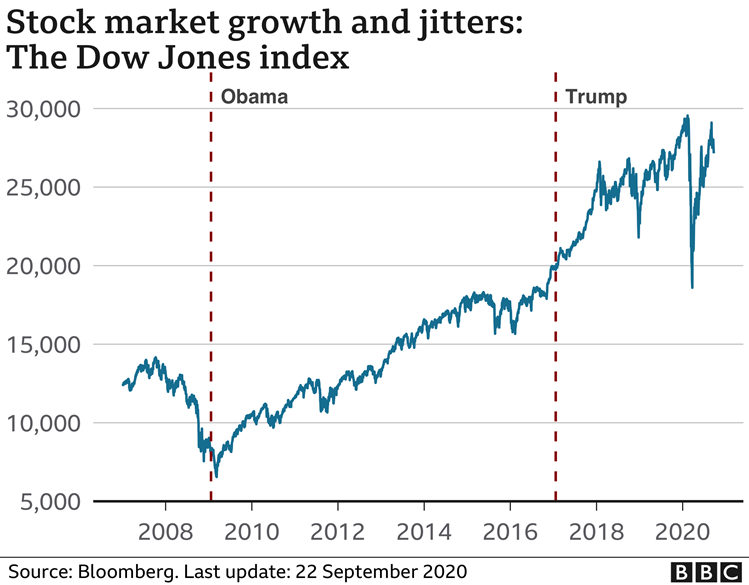

Anxiety over politics is nothing new, and as I’ve written extensively in my Investing Caffeine blog, history teaches us that politics have little to do with the long-term performance of the overall stock market (e.g., see Politics & Your Money). Nobody knows with certainty how the elections will impact the financial markets and economy (myself included). But what I do know is that many so-called experts said the stock market would decline if Barack Obama won the presidential election…in reality the stock market soared. I also know the so-called experts said the stock market would decline if Donald Trump won the presidential election… in reality the stock market soared. So, suffice it to say, I don’t place a lot of faith into what any of the so-called political experts say about the outcome of upcoming elections (see the chart below).

COVID Coming Back?

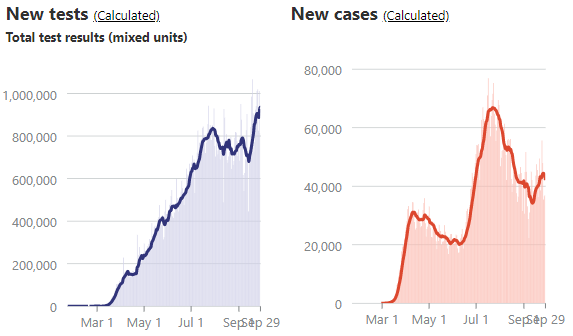

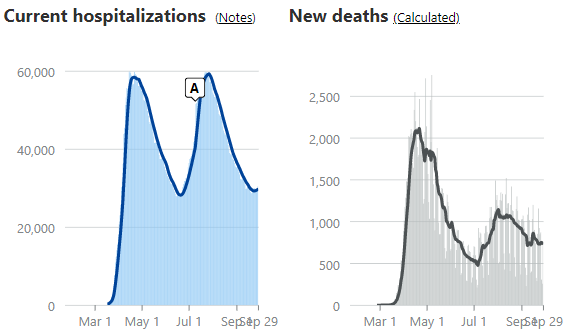

One of the reasons stock prices have risen more than 50%+ is due to a stabilization in COVID-19 virus trends. As you can see from the charts below, new tests, hospitalizations, and death rates are generally on good trajectories, according to the COVID Tracking Project. However, new COVID cases have bumped higher in recent weeks. This recent, troubling trend has raised the question of whether another wave of cases is building in front of a dangerous, seasonally-cooler fall flu season. Traditionally, it’s during this fall period in which contagious viruses normally spread faster.

Source: The COVID Tracking Project

Regardless of the trendline in new cases, there is plenty of other promising COVID developments to help fight this pandemic, such as the pending approvals of numerous vaccines, along with improved therapies and treatments, such as therapeutics, steroids, blood thinners, ventilators, and monoclonal antibodies.

Business Bounce

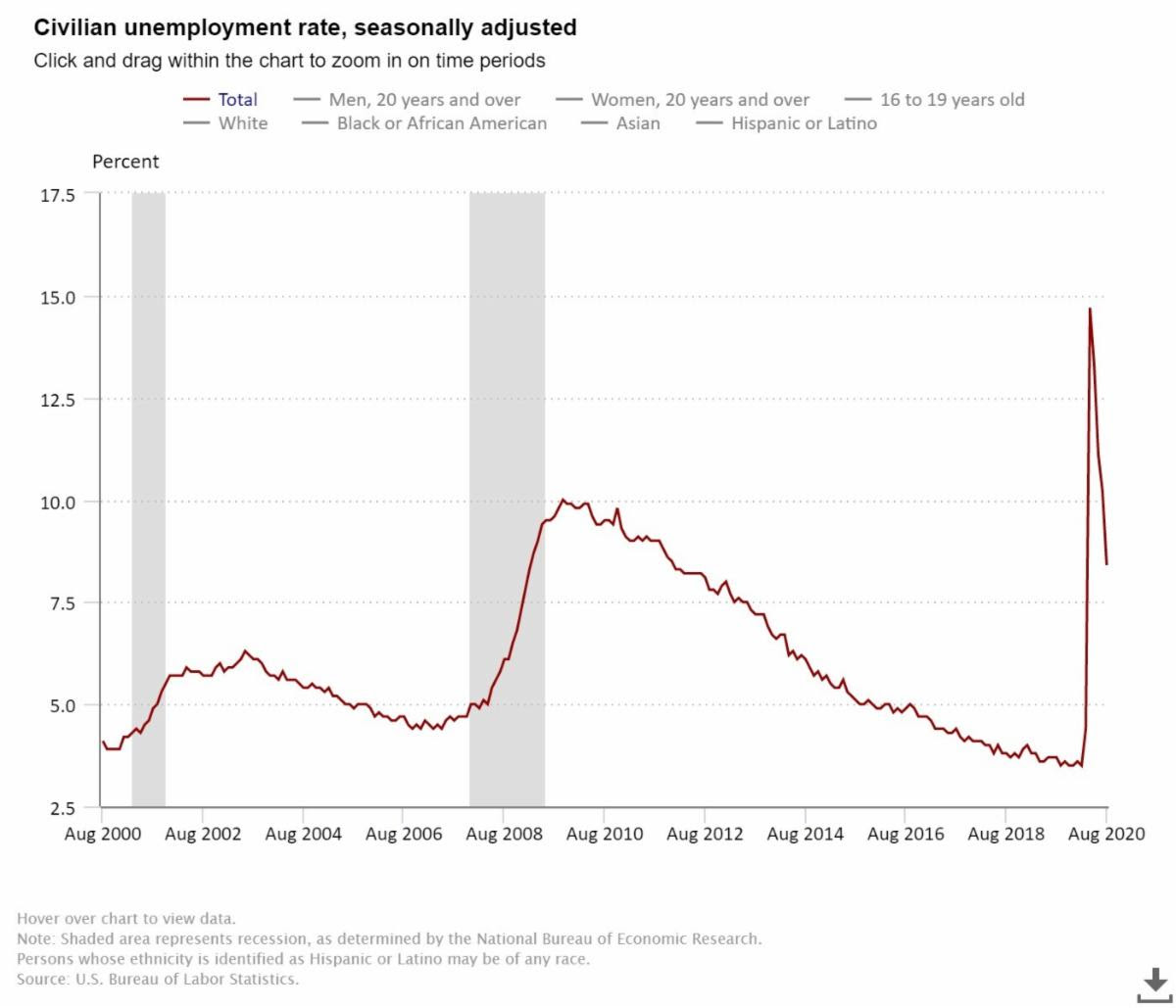

From the 10,000-foot level, despite worries over various political outcomes, the economy is recovering relatively vigorously. As you can see from the chart below, the rebound in employment has been fairly swift. After peaking in April at 14.7%, the most recent unemployment rate has declined to 8.4%, and a closely tracked ADP National Employment Report was released yesterday showing a higher than expected increase in new private-sector monthly jobs (749,000 vs. 649,000 median estimate).

Source: U.S. Bureau of Labor Statistics

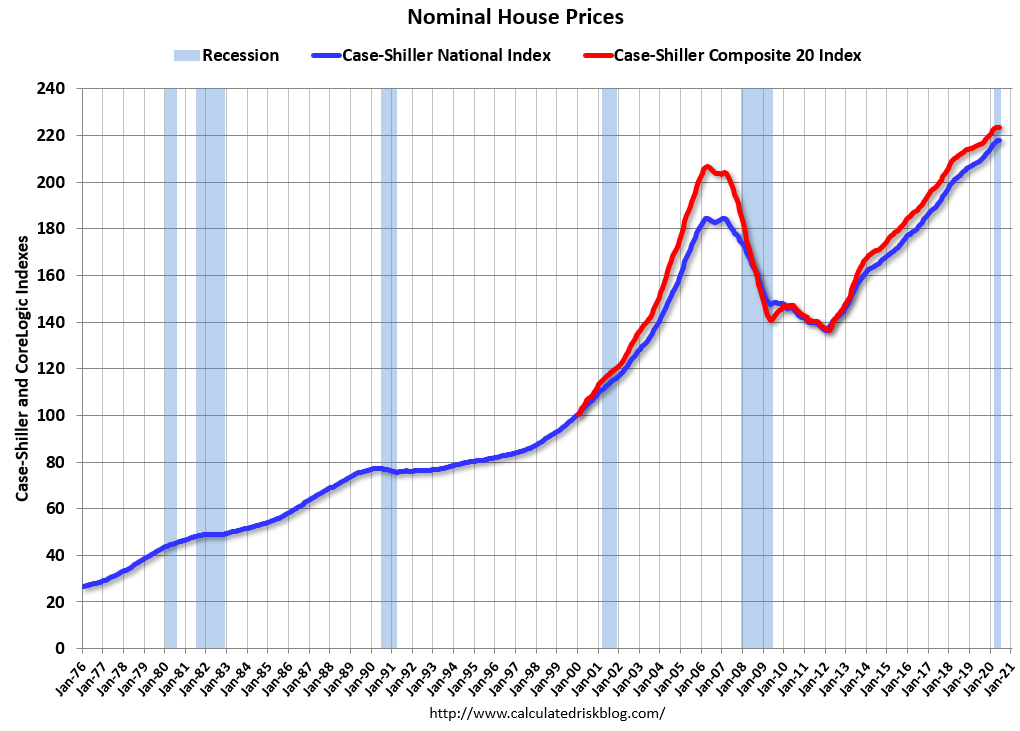

From a housing perspective, house sales have been on fire. Record-low interest rates, mortgage rates, and refinancing rates have been driving higher home purchases and rising prices. Urban flight to the suburbs has also been a big housing tailwind due to the desire for more socially distanced room, additional home office space, and expansive backyards. Adding fuel to the housing fire has been record low supply (i.e., home inventories). The robust demand is evident by the record Case-Shiller home prices (see chart below).

Source: Calculated Risk

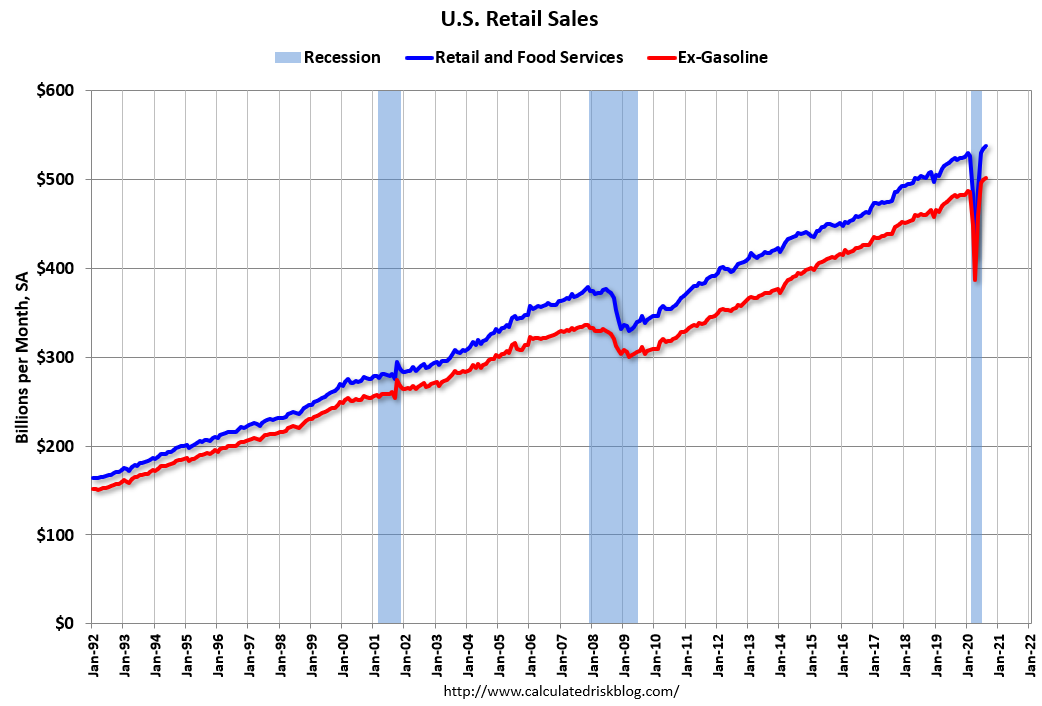

There are plenty of industries hurting, including airlines, cruise lines, hotels, retailers, and restaurants but the economic rebound along with government stimulus (i.e., direct government checks and unemployment relief payments) have led to record retail sales (see chart below). Spending could cool if an additional coronavirus-related stimulus package agreement is not reached, but until the government checks stop flowing, consumers will keep spending.

Source: Calculated Risk

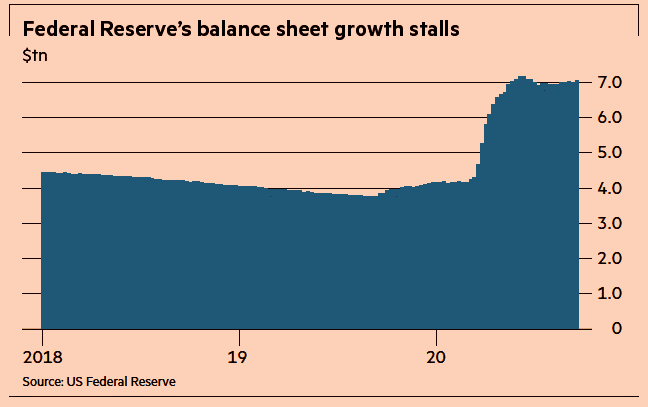

Besides trillions of dollars in fiscal relief injected into the economy, the Federal Reserve has also provided trillions in unprecedented relief (see chart below) through its government and corporate bond buying programs, in addition to its Main Street Lending Program.

Source:The Financial Times

There has been a lot of political hocus pocus and COVID smoke & mirrors that have much of the population worried about their investments. In every presidential election, you have about half the population satisfied with the winner, and half the population disappointed in the winner…this election will be no different. The illusion of fear and chaos is bound to create some short-term financial market volatility over the next month, but behind the curtains there are numerous positive, contributing factors that are powering the economy and stock market forward. Do yourself a favor by focusing on your long-term financial future and don’t succumb to politics and COVID tricks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFS), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Bin Laden Killing Overshadows Royal Rally

Excerpt from No-Cost May Sidoxia Monthly Newsletter (Subscribe on right-side of page)

Before the announcement of the killing of the most wanted terrorist in the world, Osama bin Laden, the royal wedding of Prince William Arthur Philip Louis and Catherine Middleton (Duke and Duchess of Cambridge) grabbed the hearts, headlines, and minds of people around the world. As we exited the month, a less conspicuous royal rally in the U.S. stock market has continued into May, with the S&P 500 index climbing +2.8% last month as the economic recovery gained firmer footing from the recession of 2008 and early 2009. As always, there is no shortage of issues to worry about as traders and speculators (investors not included) have an itchy sell-trigger finger, anxiously fretting over the possibility of losing gains accumulated over the last two years.

Here are some of the attention-grabbing issues that occurred last month:

Powerful Profits: According to Thomson Reuters, first quarter profit growth as measured by S&P 500 companies is estimated at a very handsome +18% thus far. At this point, approximately 84% of companies are exceeding or meeting expectations by a margin of 7%, which is above the long-term average of a 2% surprise factor.

Powerful Profits: According to Thomson Reuters, first quarter profit growth as measured by S&P 500 companies is estimated at a very handsome +18% thus far. At this point, approximately 84% of companies are exceeding or meeting expectations by a margin of 7%, which is above the long-term average of a 2% surprise factor.

Debt Anchor Front & Center: Budget battles remain over record deficits and debt levels anchoring our economy, but clashes over the extension of our debt ceiling will occur first in the coming weeks. Skepticism and concern were so high on this issue of our fiscal situation that the Standard & Poor’s rating agency reduced its outlook on the sovereign debt rating of U.S. Treasury securities to “negative,” meaning there is a one-in-three chance our country’s debt rating could be reduced in the next two years. Democrats and Republicans have put forth various plans on the negotiating table that would cut the national debt by $4 – $6 trillion over the next 10-12 years, but a chasm still remains between both sides with regard to how these cuts will be best achieved.

Debt Anchor Front & Center: Budget battles remain over record deficits and debt levels anchoring our economy, but clashes over the extension of our debt ceiling will occur first in the coming weeks. Skepticism and concern were so high on this issue of our fiscal situation that the Standard & Poor’s rating agency reduced its outlook on the sovereign debt rating of U.S. Treasury securities to “negative,” meaning there is a one-in-three chance our country’s debt rating could be reduced in the next two years. Democrats and Republicans have put forth various plans on the negotiating table that would cut the national debt by $4 – $6 trillion over the next 10-12 years, but a chasm still remains between both sides with regard to how these cuts will be best achieved.

Inflation Heating Up: The global economic recovery, fueled by loose global central bank monetary policies, has resulted in fanning of the inflation flames. Crude oil prices have jumped to $113 per barrel and gasoline has spiked to over $4 per gallon. Commodity prices have jumped up across the board, as measured by the CRB (Commodity Research Bureau) BLS Index, which measures the price movements of a basket of 22 different commodities. The CRB Index has risen over +28% from a year ago. Although the topic of inflation is dominating the airwaves, this problem is not only a domestic phenomenon. Inflation in emerging markets, like China and Brazil, has also expanded into a dangerous range of 6-7%, and many of these governments are doing their best to slow-down or reverse loose monetary policies from a few years ago.

Inflation Heating Up: The global economic recovery, fueled by loose global central bank monetary policies, has resulted in fanning of the inflation flames. Crude oil prices have jumped to $113 per barrel and gasoline has spiked to over $4 per gallon. Commodity prices have jumped up across the board, as measured by the CRB (Commodity Research Bureau) BLS Index, which measures the price movements of a basket of 22 different commodities. The CRB Index has risen over +28% from a year ago. Although the topic of inflation is dominating the airwaves, this problem is not only a domestic phenomenon. Inflation in emerging markets, like China and Brazil, has also expanded into a dangerous range of 6-7%, and many of these governments are doing their best to slow-down or reverse loose monetary policies from a few years ago.

Expansion Continues but Slows: Economic expansion continued in the first quarter, but slowed to a snail’s pace. The initial GDP (Gross Domestic Product) reading for Q1 slowed down to +1.8% growth. Brakes on government stimulus and spending subtracted from growth, and high fuel costs are pinching consumer spending.

Expansion Continues but Slows: Economic expansion continued in the first quarter, but slowed to a snail’s pace. The initial GDP (Gross Domestic Product) reading for Q1 slowed down to +1.8% growth. Brakes on government stimulus and spending subtracted from growth, and high fuel costs are pinching consumer spending.

Ben Holds the Course: One person who is not overly eager to reverse loose monetary policies is Federal Reserve Chairman, Ben Bernanke. The Chairman vowed to keep interest rates low for an “extended period,” and he committed the Federal Reserve to complete his $600 billion QE2 (Quantitative Easing) bond buying program through the end of June. If that wasn’t enough news, Bernanke held a historic, first-ever news conference. He fielded a broad range of questions and felt the first quarter GDP slowdown and inflation uptick would be transitory.

Ben Holds the Course: One person who is not overly eager to reverse loose monetary policies is Federal Reserve Chairman, Ben Bernanke. The Chairman vowed to keep interest rates low for an “extended period,” and he committed the Federal Reserve to complete his $600 billion QE2 (Quantitative Easing) bond buying program through the end of June. If that wasn’t enough news, Bernanke held a historic, first-ever news conference. He fielded a broad range of questions and felt the first quarter GDP slowdown and inflation uptick would be transitory.

Skyrocketing Silver Prices: Silver surged ahead +28% in April, the largest monthly gain since April 1987, and reached a 30-year high in price before closing at around $49 per ounce at the end of the month. Speculators and investors have been piling into silver as evidenced by activity in the SLV (iShares Silver Trust) exchange traded fund, which on occasion has seen its daily April volume exceed that of the SPY (iShares SPDR S&P 500) exchange traded fund.

Obama-Trump Birth Certificate Faceoff: Real estate magnate and TV personality Donald Trump broached the birther issue again, questioning whether President Barack Obama was indeed born in the United States. President Obama produced his full Hawaiian birth certificate in hopes of putting the question behind him. If somehow Trump can be selected as the Republican presidential candidate for 2012, he will certainly try to get President Obama “fired!”

Obama-Trump Birth Certificate Faceoff: Real estate magnate and TV personality Donald Trump broached the birther issue again, questioning whether President Barack Obama was indeed born in the United States. President Obama produced his full Hawaiian birth certificate in hopes of putting the question behind him. If somehow Trump can be selected as the Republican presidential candidate for 2012, he will certainly try to get President Obama “fired!”

Charlie Sheen…Losing! The Charlie Sheen soap opera continues. Ever since Sheen has gotten kicked off the show Two and a Half Men, speculation has percolated as to whether someone would replace Sheen to act next to co-star John Cryer. Names traveling through the gossip circles include everyone from Woody Harrelson to Jeremy Piven to Rob Lowe. Time will tell whether the audience will laugh or cry, but regardless, Sheen will be laughing to the bank if he wins his $100 million lawsuit against Warner Brothers (TWX).

Charlie Sheen…Losing! The Charlie Sheen soap opera continues. Ever since Sheen has gotten kicked off the show Two and a Half Men, speculation has percolated as to whether someone would replace Sheen to act next to co-star John Cryer. Names traveling through the gossip circles include everyone from Woody Harrelson to Jeremy Piven to Rob Lowe. Time will tell whether the audience will laugh or cry, but regardless, Sheen will be laughing to the bank if he wins his $100 million lawsuit against Warner Brothers (TWX).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain commodity and S&P 500 exchange traded funds, but at the time of publishing SCM had no direct position in SLV, SPY, TWX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Will the Fiscal Donkey Fly?

Source: TopPayingIdeas.com/blog

Will Barack Obama become a “one-termer” like somewhat recent Presidents, Democrat Jimmy Carter (1977-1981) and Republican George H.W. Bush #41 (1989-1993)? Or will Obama get the Democratic donkey off the ground like Bill Clinton managed to do after the 1994 mid-term election when Republican Newt Gingrich spearheaded the Contract with America, which led to a similar Republican majority in the House of Representatives. Clinton’s approval ratings were in the dumps at the time, comparable to voter’s current lackluster opinion of Obama and his spending spree (see also Profitless Healthcare).

Source: Gallup

Reagan Rebound

Similarly, Republican Ronald Reagan (1981-1989) was picking up the pieces with his lousy approval rating after the 1982 midterm election. Tax cuts, “trickle-down” supply side economics, and a tough stance on the Russian Cold War turned around the economy and his approval rating and catapulted him to reelection in a landslide victory. Reagan carried 49 states with the help of Reagan Democrats (one-quarter of registered Democrats voted for him).

Source: The Wall Street Journal

One should be clear though, popularity is not the only factor that plays into reelection success. George H. W. Bush had the highest average approval rating in five decades (60.9% approval), only superseded by John F. Kennedy (70.1% approval). The economy, international politics, and other external factors also play a large role in the reelection process.

Flying Donkey Time?

If President Obama wants to get the Democratic donkey off the ground and raise his current approval rating of 47% and remedy his self-admitted “shellacking” by the Republicans, then he will need to shift his hard-left political agenda more towards the middle, like Clinton did in 1994. If he leads on ideology alone, then the next two years will likely be a long tough slog for him and his Democratic colleagues.

In order to shift toward the center and gain more Independent voters, Obama will need to find common ground with Republicans and Tea-Partiers. Obama has already conceded in principle to extend the Bush tax cuts, but if he wants to gain more political capital, he will have to gain some ground in the area of fiscal responsibility. With the help of a strong economy, Clinton managed to run surpluses, but front and center today is a $1.3 trillion deficit and over $13 trillion in debt. The first step in building any credibility on the issue will come on December 1st when the president’s bi-partisan commission for deficit reduction will release its report.

It will be interesting which party will show leadership in making unpopular spending cuts, just as the 2012 re-election cycle just begins. The elephants in the room are the entitlements (Medicare and Social Security), and although less talked about, efficient cuts to defense spending should be put on the table. Sure, pork barrel spending, inefficient subsidies, tax loopholes, are gaps that need to be filled, but they alone are rounding errors given our country’s unsustainable current circumstances. Whether or not politicians (red or blue) will point out the unpopular elephants in the room will be interesting to watch.

Financial irresponsibility at the consumer and corporate level were major drivers behind the 2008-2009 financial crisis, and both individuals and businesses are responsibly adjusting their expense structures and balance sheets. Our government has to wake up to reality and adjust its expense structure and balance sheet too. Although foreign countries have reacted (i.e., European austerity), egotistical American politicians on both sides of the aisle haven’t quite woken up and smelled the coffee yet. Thank goodness for the democracy that we live in because citizens are pointing to the elephants in the room and demanding reckless spending and debt levels to come under control. If President Barack Obama doesn’t want to become another one-termer, he’ll have to move more to the center and get the finances of our country under control. If the stubborn donkey refuses to deal with reality and remains flightless, hopefully an elephant or ship-full of tea partiers can get this grass roots call for fiscal sanity off the ground.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Short-Termism & Extremism: The Death Knell of our Future

In recent times, American society has been built on a foundation of instant gratification and immediate attacks, whether we are talking about politics or economics. Often, important issues are simply presented as black or white in a way that distorts the truth and rarely reflects reality, which in most cases is actually a shade of grey. President Obama is discovering the challenges of governing a global superpower in the wake of high unemployment, a fragile economy, and extremist rhetoric from both sides of the political aisle. Rather than instituting a promise of change, President Obama has left the natives restless, wondering whether a “change for worse” is actually what should be expected in the future.

Massachusetts voters made a bold and brash statement when they elected Republican Senator Scott Brown to replace the vacated Massachusetts Senate seat of late, iconic Democratic Senator Edward Kennedy – a position he held as a Democrat for almost 47 years. Obama’s response to this Democratic body blow and his fledging healthcare reform was to go on a populist rampage against the banks with a tax and break-up proposal. Undoubtedly, financial reform is needed, but the timing and tone of these misguided proposals unfortunately does not attack the heart of the financial crisis causes – excessive leverage, lack of oversight, and irresponsible real estate loans (see also, Investing Caffeine article on the subject).

With that said, I would not write President Obama’s obituary quite yet. President Reagan was left for dead in 1982 before his policies gained traction and he earned a landslide reelection victory two years later. In order for President Obama to reverse his plummeting approval ratings and garner back some of his election campaign mojo, he needs to lead more from the center. Don’t take my word for it, review Pew Research’s data that shows Independents passing up both Republicans and Democrats. The overall sour mood is largely driven by the economic malaise experienced by all in some fashion, and unfortunately has contributed to short-termism and extremism.

Technology has flattened the world and accelerated the exchange of information globally at the speed of light. Any action, recommendation, or gaffe that deviates from the approved script immediately becomes a permanent fixture on someone’s lifetime resume. Our comments and decisions become instant fodder for the worldly court of opinion, thanks to 24/7 news cycles and millions of passionate opinions blasted immediately through cyberspace and around the globe.

Short-termism and extremism can be just as poisonous in the economic world as in the political world. This dynamic became evident in the global financial crisis. Short-termism is just another phrase for short-term profit focus, so when more and more leverage led to more and more profits and higher asset prices, the financial industry became blinded to the long-term consequences of their short-term decisions.

Solutions:

- Small Bites First: Rather than trying to ram through half-baked, massive proposals laced with endless numbers of wasteful pork barrel projects, why not focus on targeted and surgical legislation first? If education, deficit-reduction, and job creation are areas of common interest for Republicans and Democrats, then start with small legislation in these areas first. More ambitious agendas can be sought out later.

- Embrace Globalization: Based on the “law of large numbers” and the scale of the United States economy, our slice of the global economic pie is inevitably going to shrink over time. How does the $14 trillion U.S economy manage to grow if its share is declining? Simple. By eschewing protectionist policies, and embracing globalization. Developing country populations are joining modern society on a daily basis as they integrate productivity-enhancing innovations used by developed worlds for decades. In a flat world, the narrowing of the productivity gap is only going to accelerate. The question then becomes, does the U.S. want to participate in this accelerating growth of developing markets or sit idly on the sideline watching our competitors eat our lunch?

- Hail Long-Termism and Centrism: Regulations and incentives need to be instituted in such a fashion that irresponsible behavior occurring in the name of instant short-term profits is replaced with rules that induce sustainable profits and competitive advantages over our economic neighbors. Much of the financial industry is scratching and screaming in the face of any regulatory reform suggestions. The bankers’ usual response to reform is to throw out scare tactics about the inevitable damage caused by reform to the global competitiveness of our banking industry. No doubt, the case of “anti-competiveness” is a valid argument and any reforms passed could have immediate negative impacts on short-term profits. Like the bitter taste of many medicines, I can accept regulatory remedies now, if the long-term improvements outweigh the immediate detrimental aspects.

The focus on short-termism and extremism has created an acidic culture in both Washington and on “Main Street,” making government changes virtually impossible. If President Obama wants to implement the change he campaigned on, then he needs to take a more centrist view that concentrates on enduring benefits – not immediate political gains.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Article first submitted to Alrroya.com before being published on Investing Caffeine.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds but at the time of publishing had no direct positions in securities mentioned in the article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Flogging the Financial Firefighter

There we were in the fall of 2008, our economic system burning up in flames, as we all watched century-old financial institutions falling like flies. At the center of the inferno was Federal Reserve Chairman Ben Bernanke. In coordination with other government agencies and officials, Bernanke managed to prevent the worse financial crisis since the Great Depression from completely scorching the economy into ruin. After successfully hosing down the flames (at least temporarily), Ben Bernanke is now being singled out as the scapegoat and getting flogged for being a major participant in the financial crisis.

Execution Threatened Water Damage

In hind-sight could Bernanke have made better decisions? Certainly. Despite the Federal Reserve dousing out the flames, politicians are pointing the finger at Bernanke for causing water damage. I’m going to go out on a limb and say water damage is preferable to the alternative – a whole community of properties burned down to a large pile of charred ash.

Democrats are now flailing in the wake of the Massachusetts Democratic Senate seat loss to Republican Scott Brown. Even though I question President Obama’s blame-game tax and overhaul tactics (see Surgery or Amputation article), to his credit Obama realizes the instability of mass proportion that would occur if the reappointment of Bernanke were to come to fruition. If the head of the globe’s largest financial system is going to be kicked to the curb after saving our economy at the edge of an abyss, then heaven please help us.

Politics Will Reign Supreme in 2010

“Change” was promised in the 2008 Presidential election and the impatient natives are not seeing results fast enough, given lofty unemployment rates and unsuccessful implementation of other initiatives (thus far). Needless to say, the media is going to be awash in an orgy of political mudslinging and campaign promises that will overwhelm the airwaves for the balance of the year.

From a market standpoint, Republicans and Democrats, alike, do share some common ground…jobs. As a countervailing trend to the forces dragging down the economy, the unified focus on job creation should provide some support to the financial markets.

Unfortunately, the independence of the Federal Reserve is being dragged into the political ring as Ben Bernanke’s reappointment process cannot escape the Capitol Hill circus. Berkshire Hathaway (BRKA/B) CEO Warren Buffett has likely handicapped the market’s reaction to a failed Bernanke reappointment when he recently stated, “Just tell me a day ahead of time so I can sell some stocks.” If the fires of 2008 concerned you, you may want to have your fire alarm and water hose ready for action if Chairman Bernanke is shown the exit.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and at the time of publishing had no direct positions in BRKA/B. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Banking Surgery or Amputation?

Photo Source: (c)iStockphoto.com Artist: Powerofforever

Deciding whether to sever the proprietary trading arms of the commercial banks, rather than instituting regulation, seems a lot like deciding whether amputation is a healthier path for those suffering terrible frostbite cases. Even if this legislation is unlikely to pass, I find the recommendations severe in relation to other measured alternatives. I’m no right-wing conspiracy theorist, but I don’t think the timing of the Obama administration’s announcement is coincidental. Why is this proposal surfacing two years into the financial crisis and a whole year after the President entered office?

Politicians have always been masterful at introducing coincidental distractions at opportune times, in order to generate patriotic voter sympathies. Some examples include, Margaret Thatcher in the Falkand Islands; George Bush #41 in the Iraqi war; and President Obama’s current ant-banker populist brigade. Perhaps miserable and declining approval ratings and a healthcare bill on the verge of collapse may have something to do with the timing? I want President Obama to succeed, and he may have good intentions, but let’s not rush to an overzealous knee-jerk reactions before other less-draconian solutions are thoroughly explored.

Glass-Steagall Redux

Theoretically, the argument of forcing banks to adopt lower risk sounds great on paper. Overall, I think this initiative is a worthy one Americans could buy into. As a matter of fact, investment guru Jeremy Grantham makes the same argument in my Investing Caffeine article (“Too Big to Sink”). However, I think a more relevant question is, “How do we implement more responsible risk taking by the banks, without a massive overhaul to the system?” Certainly there were some regulators asleep at the switch, and some financial institutions that pushed the envelope on risk assumption, but I’m not convinced a return to Glass-Steagall (or Glass-Steagall Lite) is going to bring miracles. If the regulators cannot adequately curb risk taking by the banks, then cross the more dangerous bridge later. The economy is presently in the midst of a fragile recovery and we do not want to change the airplane engine during mid-flight.

Political Pendulum Swings

This isn’t the first time Washington has reversed previous decisions. If the cries of voters reach a feverish pitch, and these wishes coincide with a politician’s re-election agenda, then the probabilities of sub-optimal, rushed legislation increases. Consider AT&T (T), which because of antitrust concerns was forced to split operations in 1982. Lo and behold, some twenty years later, we witnessed the re-consolidation of the “Baby Bells” back into AT&T. Now, Glass-Steagall is the topic of conversation and with an unambiguous scapegoat needed by politicians, Washington is targeting the banks with taxes and operations splitting.

Hasty legislation is nothing new with the populist flames fanning in the background. Sarbanes-Oxley is another example of less-than-ideal legislation introduced in the wake of relatively low number of corporate scandals, such as Enron, WorldCom, and Tyco (TYC).

Regulation Reform Solution

Here are 3 constructive steps:

1) Institute transparent trading of derivatives (i.e., Credit default Swaps) over exchanges with adequately capitalized clearing houses.

2) Require higher capital requirements for banks conducting proprietary trading and mandate adequate disclosure.

3) Consolidation of regulators, thereby creating a more simplified, accountable structure (see also Regulatory Web article). Savings from redundant costs could be used to hire additional regulatory oversight staff.

Blood is in the streets and with mid-term elections just around the corner, the Obama administration is looking to salvage anything they can bring back to the voters. Frost bite (and greedy bankers) is a painful and horrible predicament, however if healthy functioning limbs can be saved with targeted surgery rather than amputation, then I vote for this solution.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including VFH), and at the time of publishing had no direct positions in T, TYC. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Timothy Geithner, the Eddie Haskell Dollar Czar

Treasury Secretary Timothy Geithner recently stated after a meeting of G-7 financial officials that “it is very important to the United States that we continue to have a strong dollar.”

With comments like this, why does Timothy Geithner remind me so much of Eddie Haskell (played by Ken Osmond) from the 1950s suburban sitcom Leave It to Beaver? Eddie Haskell plays the scheming trouble maker who is extremely polite on the exterior around adults, but reverts to a crafty conniver once the grown-ups leave the room.

I can just picture the conversations between Treasury Secretary Geithner and President Obama before a high powered meeting with Chinese administration officials:

Geithner: “Barack, the skyrocketing debt will be no problem, we can we shovel plenty of this paper on these Chinese.”

Barack: “Uh, oh…Hu is here for our meeting.”

Geithner: “Oh hello Mr. President Jintao – what a lovely trade surplus you have. We look forward to keeping a very fiscally responsible agenda here in the United States, so you can keep buying our valuable debt.”

Where did Timothy Haskell get his crafty dollar oration skills?

According to David Malpass, president of the research firm Encima Global and deputy assistant Treasury Secretary, Geithner training came from “using a code phrase, a carryover from the Bush administration. It means that the U.S. approves of a constantly weakening dollar but doesn’t want a disruptive collapse.”

These tactics and rhetoric can only work for so long. Exploding deficits and skyrocketing debt levels will eventually lead to a dumping of our debt, rising interest rates, crowding-out of private investments, and a damaging decline in the dollar. Sure, the weakening dollar helps us in the short-run with exports but eventually major U.S. debtholders will no longer buy our sweet talking.

With all the “U.S. dollar is going to collapse” talk, one would think a shift to an SDR (Special Drawing Rights) global currency structure is an inevitable outcome. Just six months ago the governor of China’s central bank argued the U.S. dollar’s role as the world’s reserve currency should be restructured. The SDR model has already been implemented by the IMF (International Monetary Fund), so if the Chinese wanted to create an SDR proxy, they could easily purchase euros, sterling, and yen in proper proportions. Would the Chinese want to make any sudden changes? Certainly not, because any quick adjustments would destroy the value of the Chinese’s existing dollar denominated portfolio. The logistics surrounding a legitimate SDR program would require the IMF or some other international agency to act as a global central bank, which would not only need to determine the appropriate mix of currencies in the SDR, but also decide future global liquidity actions. In order to legitimately run a new SDR program, countries like China would need to give up sovereignty – not a likely scenario.

Until a new SDR regime is agreed upon, dollar-reliant countries will continue to have barks bigger than their bites and Timothy Geithner Haskell will continue to sweet talk U.S. dollar owners.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Hear Eddie (or Treasury Secretary) Speak Here:

{kind=link}