Posts tagged ‘North Korea’

S.T.I.N.K. – Deja Vu All Over Again

Yogi Berra is a Baseball Hall of Fame catcher and manager who played 18 out of 19 seasons with the New York Yankees. Besides his incredible baseball skills, Berra was also known for his humorous and witty quotes, which were called “Yogi-isms.” Reportedly, one of Berra’s most famous Yogi-isms occurred after he observed fellow teammates, Mickey Mantle and Roger Maris, continually hitting back-to-back home runs:

“It’s déjà vu all over again.”

The Merriam-Webster dictionary defines déjà vu as “a feeling that one has seen or heard something before.” I experienced the same sense last month as I was bombarded with ominous news headlines. Some of you may recall the panic attack over the PIIGS regions during the 2010 – 2012 timeframe (Solving Europe & Deadbeat Cousin). I’m obviously not referring to the pork product, but rather Portugal, Italy, Ireland, Greece, and Spain, which rocked financial markets due to investor fears that Greece’s fiscal irresponsibility may force the country to leave the eurozone and drag the rest of Europe into financial ruin.

Suffice it to say, the imploding Greece/Europe disaster scenario did not happen. If you fast forward to today, the fear has returned again, however with a different acronym spin. Rather than speak about PIIGS, today the talking heads are fretting over S.T.I.N.K. – Spain, Tariffs, Italy, and North Korea.

*Worth noting, the letter “I” in S.T.I.N.K. could also be sustained or replaced by the word Iran, given the Trump administration’s desire to exit the Iran Nuclear Deal. The move comes despite support by our country’s tight NATO (North Atlantic Treaty Organization) allies who want the U.S. to remain in the agreement.

An overview of S.T.I.N.K. unease is summarized here:

Spain: After a reign of six years, Spain’s Prime Minister Mariano Rajoy is on the verge of being ousted to socialist opposition leader, Pedro Sanchez. Corruption convictions involving former members in Rajoy’s conservative Popular Party only increases the probability that the imminent no-confidence vote in the Spanish parliament will lead to Rajoy’s exit.

Tariffs: President Trump is lifting the temporary steel and aluminum tariff exemptions provided to many of our allies, including Canada, Mexico, and the European Union. Recent breakdowns in trade discussions with allies like Mexico and Canada are likely to make the renegotiation of NAFTA (North American Free Trade Agreement) even more challenging. Handicapping President Trump’s global trade rhetoric can be difficult, especially given the periodic inconsistency in Trump’s actions relative to his words. Time will tell whether Trump’s tough trade talk is merely a negotiating tool designed to gain better trade terms for the U.S., or whether this strategy backfires, and trading partner allies choose to retaliate with tariffs of their own. For example, the EU has threatened to impose import taxes on bourbon; Mexico has warned about levying taxes on American farm products; and Canada is focused on the same steel and aluminum tariffs that Trump has been referencing.

Italy: Pandemonium temporarily set in when Italy’s President Sergio Mattarella essentially vetoed the finance minister selection by Italian Prime Minister Giuseppe Conte. Initially, Italian bond prices plummeted and interest rates spiked as fears of an Italian exit from the euro currency, but after the rejection of the original finance chief, the populist Five Star and League coalition parties agreed to institute a more moderate finance minister and bond prices/rates stabilized.

North Korea: The on-again-off-again denuclearization summit between the U.S. and North Korea may actually take place in Singapore on June 12th. In recent days, Secretary of State Mike Pompeo has held face-to-face meetings with North Korean General Kim Yong Chol in New York. The senior North Korean leader is also planning to hand deliver a letter from Korean leader Kim Jong Un to President Trump in preparation for the nuclear summit. The U.S. is attempting to incentivize North Korea with economic relief in return for North Korea giving up their nuclear capabilities.

Thanks to S.T.I.N.K., volatility has risen, but the downdrafts have been relatively muted as evidenced by the moves in the stock averages this month. More specifically, the S&P 500 index rose +2.2% last month, while the technology-heavy Nasdaq index catapulted +5.3%. Nevertheless, not all indexes are created equally as witnessed by the Dow Jones Industrial Index, which climbed a more muted +1.1% for the month. For the year, the Dow is down -1.2%, while the S&P and Nasdaq indexes are higher by +1.2% and +7.8%, respectively.

Ever since the 2008-2009 financial crisis, observers have incessantly and anxiously waited for the return of a “stinky” economic and/or geopolitical catastrophe that will wreck the American economy. Unfortunately for the pessimists, stock prices have more than quadrupled in value since early-2009. Yogi Berra may have been correct when he said, “It’s déjà vu all over again,” but just like PIIGS concerns failed to cause global economic contagion, STINK concerns are unlikely to cause significant economic damage either. Over the last year, the only “stink” occurring has been the stink of cool, hard cash.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The September to Remember

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 2, 2017). Subscribe on the right side of the page for the complete text.

Given the volume of recent memorable events, it appears September will become a month to remember. Not only did we witness horrific natural disasters in Texas, Florida, Puerto Rico, and Mexico but Americans have also had to digest the saber rattling by the North Korean “Rocket Man“ leader, Kim Jong Un*. If that wasn’t enough, there were a slew of headlines detailing the Washington gridlock and dysfunction over healthcare legislation / tax reform; hackings at Equifax affecting up to 143 million credit accounts; the planned unwinding of the Federal Reserves $4.2 trillion bond portfolio; and a controversy over NFL football players kneeling during the national anthem.

Despite all these notable events, the Dow Jones Industrial Average just posted its 8th consecutive quarter of advances. For the three months ending in September, the Dow impressively climbed more than 1,000 points (+4.7%) to a new record high of 22,381. For the year, the Dow remarkably has risen approximately +13%, excluding dividends, which translates into a total 2017 return of more than +15%, thus far.

However, not everybody has participated in the financial party. Negative political headlines have by and large paralyzed the hearts and minds of the general public, but as I have been writing for some time, stocks do not care much about governmental affairs – stock prices care about fundamentals. There have been two critical, fundamental components fueling the repetitive new highs experienced in the stock market: 1) The extraordinarily persistent surge in corporate profits (see chart below); and 2) The stubbornly declining interest rates, which are near generationally-low levels. When investors are offered next-to-nothing interest rates in their bank accounts, and coupon payments on Treasury bonds remain paltry (10-Year Treasury closed month at a yield of 2.33%), suddenly stock opportunities can look much more attractive in a scarce investment environment.

Source: Yardeni.com

And geographically speaking, the rise in corporate profits has not been limited to the U.S. There has also been a synchronized escalation in corporate earnings globally. Whether we are talking about Europe, China, or emerging markets, in general, the economic recovery in these regions is now occurring coincidentally with the U.S. Case in point is the Purchasing Managers Index (PMI), which serves as a broad indicator of the economic health of the manufacturing sector. The chart below highlights the clear recovery that has been ongoing in the global manufacturing sector over the last year and a half.

Source: Yardeni.com

In addition to these numerous positive factors, a cheaper (weaker) U.S. dollar has also contributed to our nation’s economic tailwind. More specifically, a lower valued dollar makes American goods sold abroad cheaper for foreign buyers. This currency exchange rate dynamic is important because 43% of Fortune 500 sales (S&P 500) are derived from American products and services sold in foreign countries.

Tax Reform to be Born?

You probably don’t need me to tell you that gridlock in Washington D.C. is alive and well, but new details surrounding potential tax reform legislation that surfaced last week has lifted short-term investor optimism. As you can see from the chart below, the U.S. has the highest corporate tax rate among 35 developed countries in the OECD (Organisation for Economic Co-operation and Development), thereby making U.S. business less competitive globally. In hopes of reversing this trend, a basic framework was introduced by the President that proposed a top corporate rate of 20%, top small business rate of 25%, and streamlined personal tax brackets of 12%, 25%, and 35% (down from 7 brackets). Other key elements of the tax plan include, a doubling of the standard deduction for middle-class Americans; the elimination of the estate tax for the wealthy; the repeal of the alternative minimum tax; and immediate tax write-offs for business capital investments.

Source: The Financial Times

Many other important details have yet to be released and further specifics remain to be negotiated on Capitol Hill. For example, the removal of deductions for state and local taxes was announced, however additional information explaining how the estimated $2.2 trillion in tax cuts will be funded has yet to surface.

Regardless of the tax reform outcome, the economy continues to chug along at a healthy clip. Most recently, Gross Domestic Product (GDP), the central statistic in measuring the health of the U.S. economy, was revised higher to a respectable +3.1% rate in the second quarter. The latest natural disasters may clip third quarter growth temporarily, however, the consensus remains the economic expansion stands on firm ground, despite the financial drag of the hurricanes.

While geopolitical, meteorological, and athletic anthem headlines have made this a “September to Remember,” fundamental strength and other factors have contributed to this enduring and unforgettable bull market. There will be many more noteworthy headlines to occur in coming months and years, but placing these events in the proper context and investing wisely will lead to a much more positive, memorable existence.

*The article was written before the Las Vegas tragedy on October 1, 2017.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in EFX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Managing the Chaos – Investing vs. Gambling

How does one invest amid the slew of palm sweating, teeth grinding headlines of Syria, North Korea, Brexit, expanding populism, Trumpcare, French candidate Marine Le Pen, and a potential government shutdown? Facing a persistent mountain of worries can seem daunting to many. With so many seemingly uncontrollable factors impacting short-term interest rates, foreign exchange rates, and equity markets, it begs the question of whether investing is a game of luck (gambling) or a game of skill?

The short answer is…it depends. Professional gambler Alvin “Titanic” Thompson captured the essence when someone asked him whether poker was a game of chance. Thompson responded by stating, “Not the way I play it.”

If you go to Las Vegas and gamble, most games are generally a zero sum-game, meaning there are an equal number of winners and losers with the house (casino) locking in a guaranteed spread (profit). For example, consider a game like roulette – there are 18 red slots, 18 black slots, and 2 green slots (0 & 00), so if you are betting on red vs. black, then the casino has a 5.26% advantage. If you bet long enough, the casino will get all your money – there’s a reason Lost Wages Las Vegas can build those extravagantly large casinos.

The same principles of money-losing bets apply to speculative short-term trading. Sure, there are examples of speculators hitting it big in the short-run, but most day traders lose money (see Day Trading Your House) because the odds are stacked against them. In order to make an accretive, profitable trade, not only does the trader have to be right on the security they’re selling (i.e. that security must underperform in the future), but they also have to be right on the security they are buying (i.e. that security must outperform in the future). But the odds for the speculator get worse once you also account for the trading fees, taxes, bid-ask spreads, impact costs (i.e., liquidity), and informational costs (i.e., front running, high frequency traders, algorithms, etc.).

The key to winning at investing is to have an edge, and the easiest way to have an investing edge is to invest for the long-run – renowned Professor Jeremy Siegel agrees (see Stocks for the Long Run). It’s common knowledge the stock market is up about two-thirds of the time, meaning the odds and wind are behind the backs of long-term investors. Short-term trading is the equivalent of going fishing, and then continually pulling your fishing line out of the water (you’re never going to catch anything). The fisherman is better off by researching a good location and then maintaining the lure in the water for a longer period until success is achieved.

Although most casino games are based on pure luck, there are some games of skill, like poker, that can produce consistent long-term positive results, if you are a patient professional with an advantage or edge (see Dan Harrington article ). Having an edge in investing is crucial, but an edge is not the only aspect of successful investing. How you structure a portfolio to control risk (i.e., money management), and reducing your personal behavioral biases are additional components to a winning investment strategy. Professional poker player Walter Clyde “Puggy” Pearson summed it up best when he described the three critical components to winning:

“Knowing the 60-40 end of a proposition, money management, and knowing yourself.”

At Sidoxia Capital Management, we have also achieved long-term success by following a systematic, disciplined process. A large portion of our investment strategy is focused on identifying market leading franchises with a long runway of growth, and combining those dynamics with positions trading at attractive or fair values. As part of this process, we rank our stocks based on multiple factors, primarily using data from our proprietary SHGR ranking (see Investing Holy Grail) and free cash flow yield analysis, among other important considerations. Based on the risk-reward profiles of our existing holdings and the pool of targeted investments, we can appropriately size our positions accordingly (i.e., money management). As valuations rise, or risk profiles deteriorate, we can make the corresponding portfolio positions cuts, especially if we find more attractive alternative investments. Having a proven, systematic, unbiased process has helped us tremendously in minimizing behavioral pitfalls (i.e., knowing yourself) when we construct client portfolios.

The world is under assault…but that has always been the case. Throughout investment history, there have been wars, assassinations, unexpected election outcomes, banking crises, currency crises, natural disasters, health epidemics, and more. Unfortunately, millions have gambled and bet their money away based on these frivolous, ever-changing, short-term headlines. On the other hand, those investors who understand the 60-40 end of a proposition, coupled with the importance of money management and controlling personal biases, will be the skillful winners to prosper over the long-run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Double Dip Expansion?

Ever since the 2008-2009 financial crisis, every time the stock market has experienced a -5%, -10%, or -15% correction, industry pundits and media talking heads have repeatedly sounded the “Double Dip Recession” alarm bells. As you know, we have yet to experience a technical recession (two reported quarters of negative GDP growth), and stock prices have almost quadrupled from a 2009 low on the S&P 500 of 666 to 2,378 today (up approximately +257%).

Over the last nine years, so-called experts have been warning of an imminent stock market collapse from the likes of PIIGS (Portugal/Italy/Ireland/Greece/Spain), Cyprus, China, Fed interest rate hikes, Brexit, ISIS, U.S. elections, North Korea, French elections, and other fears. While there have been plenty of “Double Dip Recession” references, what you have not heard are calls for a “Double Dip Expansion.”

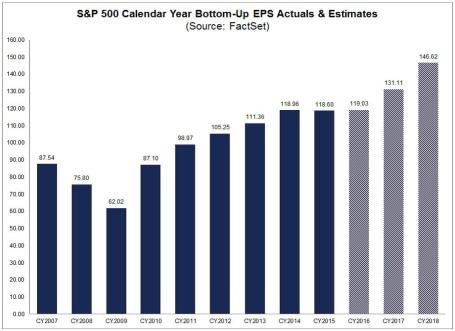

Is it possible that after the initial 2010-2014 economic expansionary rebound, and subsequent 2015-2016 earnings recession caused by sluggish global growth and a spike in the value of the U.S. dollar, we could possibly be in the midst of a “Double Dip Expansion?” (see earnings chart below)

Source: FactSet

Whether you agree or disagree with the new political administration’s politics, the economy was already on the comeback trail before the November 2016 elections, and the momentum appears to be continuing. Not only has the pace of job growth been fairly consistent (+235,000 new jobs in February, 4.7% unemployment rate), but industrial production has been picking up globally, along with a key global trade index that accelerated to 4-5% growth in the back half of 2016 (see chart below).

Source: Calafia Beach Pundit

This continued, or improved, economic growth has arisen despite the lack of legislation from the new U.S. administration. Optimists hope for an improved healthcare system, income tax reform, foreign profit repatriation, and infrastructure spending as some of the initiatives to drive financial markets higher.

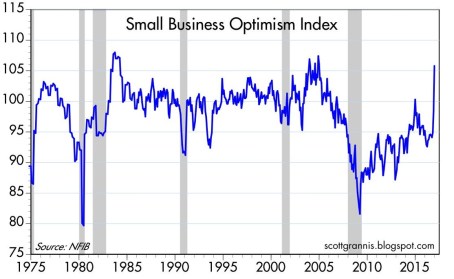

Pessimists, on the other hand, believe all these proposed initiatives will fail, and cause financial markets to fall into a tailspin. Regardless, at least for the period following the elections, investors and companies have perceived the pro-business rhetoric, executive orders, and regulatory relief proposals as positive developments. It’s widely understood that small businesses supply the largest portion of our nation’s jobs, and the upward spike in Small Business Optimism early in 2017 is a welcome sign (see chart below).

Source: Calafia Beach Pundit

Yes, it is true our new president could send out a rogue tweet; start a trade war due to a tariff slapped on a critical trading partner; or make a hawkish military remark that isolates our country from an ally. These events, along with other potential failed campaign promises, are all possibilities that could pause the trajectory of the current bull market. However, more importantly, as long as corporate profits, the mother’s milk of stock price appreciation, continue to march higher, then the stock market fun can continue. If that’s the case, there will likely be less talk of “Double Dip Recessions,” and more discussions of a “Double Dip Expansion.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Another Year, Another Decade

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}