Posts tagged ‘New Abnormal’

The New Abnormal: Living with Negative Rates

Pimco, the $1.5 trillion fixed-income manager located a stone’s throw distance from my office in Newport Beach, famously (or infamously) coined the phrase, “New Normal”. As former Pimco CEO (Mohamed El-Erian) described years ago, around the time of the Great Recession, the New Normal “reflects a growing realization that some of the recent abrupt changes to markets, households, institutions, and government policies are unlikely to be reversed in the next few years. Global growth will be subdued for a while and unemployment high.”

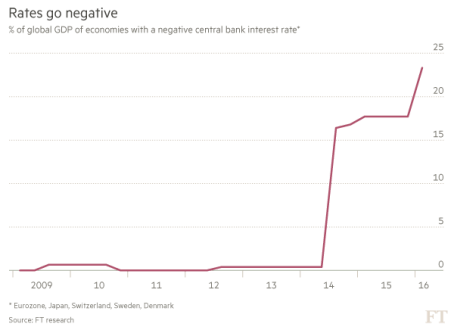

As it turns out, El-Erian was completely wrong in some respects and shrewdly prescient in others. For instance, although the job recovery has been one of the slowest in a generation, 14.5 million private sector jobs have been added since 2010, and the unemployment rate has been more than halved from 10% in early 2009, to below 5% today. However, the pace of global growth has been relatively weak since the 2008-2009 financial crisis, which has forced central banks all over the world to lower interest rates in hope of stimulating growth. Monetary policies around the globe have been cut so much that almost 25% of global GDP is tied to countries with negative interest rates (see chart below).

Source: Financial Times

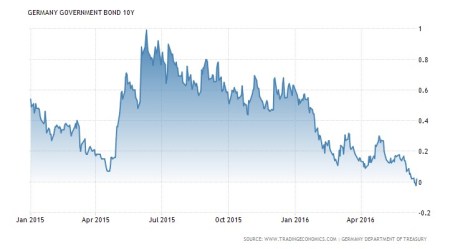

The European central banks started the sub-zero trend in 2014, and the Bank of Japan recently joined the central banks of Denmark, Sweden and Switzerland in negative territory. The negative short-term rate virus has spread further to long-term bonds as well, as evidenced by the 10-Year German Bund (sovereign bond) yield, which crossed into negative territory last week (see chart below).

Source: TradingEconomics.com

The New Abnormal

The unprecedented post-crisis move to a 0% Fed Funds rate target, along with the implementation of Quantitative Easing (QE) by former Federal Reserve Chairman Ben Bernanke, was already pushing the envelope of “normal” stimulative monetary policy. Nevertheless, central banks pushing rates to a negative threshold takes the whole stimulus discussion to another level because investors are guaranteed to lose money if they hold these bonds until maturity.

As we enter this new submerged rate phase, this activity can only be described as abnormal…not normal. Preserving money at a 0% level and losing value to inflation (i.e., essentially stuffing money under the proverbial mattress) is a bitter enough pill to swallow. Paying somebody to lend them money gives “insanity” a good name.

The stimulative objectives of negative interest policies established by central bankers may be purely intentioned, however there can be plenty of unintentional consequences. For starters, negative rates can produce too much of a good thing, in the form of excess borrowing or leverage. In addition, retirees and savers across a broad spectrum of ages are getting crushed by the paltry rates, and bank profit margins (net interest margins) are getting squeezed to boot.

Another unintended consequence of negative rate policies could be a polar opposite outcome to the envisioned stimulative design. Scott Mather, a co-portfolio manager of the $86 billion PIMCO Total Return Fund (PTTRX) is making the case that these policies could be creating more economic contractionary effects than invigorating expansion. More specifically, Mather notes, “It seems that financial markets increasingly view these experimental moves as desperate and consequently damaging to financial and economic stability.”

Eventually, the cheap money deliberately created by central banks will result in a glut of risk-taking and defaults. However, despite all the cries from hawks protesting money printing policies, cautious bank lending behavior coupled with regulatory handcuffs have yet to create widespread debt bubbles. Certainly, oceans of cheap money can create pockets of problems, as I have identified and discussed in the private equity market (see also Dying Unicorns), but supply and demand rule the day at some point.

In the end, as I have repeatedly documented, money goes where it is treated best. Realizing guaranteed losses while trapped in negative rate bonds is no way to treat your investment portfolio over the long-run. In the short-run, the safety and stability of short duration bonds may sound appealing, but ultimately rational and efficient behavior prevails. Why settle for 0% or negative rates when yields of 2%, 4%, and 6% can be found in plenty of other responsible investment alternatives?

Arguably, in this post financial crisis world we live in, we have transitioned from the New Normal to a New Abnormal environment of negative rates. Pundits and prognosticators will continue spewing fear-filled cautionary advice, but experienced, long-term investors will continue taking advantage of these risk averse markets by investing in a quality, diversified portfolio of superior yielding investments. For now, there are plenty of opportunities to choose from, until the next phase of this economic cycle… when the New Abnormal transitions to the New Normalized.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in PTTRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The New Abnormal – Now and Then

Mohamed El-Erian, bond manager and CEO of PIMCO (Pacific Investment Management Company, LLC) is known for patenting the terms “New Normal,” a period of slower growth, and subdued stock and bond market returns. Devin Leonard, a reporter from BusinessWeek, is probably closer to the truth when he describes our current financial situation as the “New Abnormal.” Accepting El-Erian description is tougher for me to accept than Leonard’s. Calling this economic environment the New Normal is like calling Fat Albert, “fat.” When roughly 15 million people are out of work, not receiving a steady paycheck, am I suppose to be surprised that consumer spending and confidence is sluggish?

Rather than a New Normal, I believe we are in the midst of an “Old Normal.” Unemployment reached 10.8% in 1982, and we recovered quite nicely, thank you, (the Dow Jones Industrial has climbed from a level about 800 in early 1982 to over 11,000 earlier in 2010). Sure, our economy carries its own distinct problems, but so did the economy of the early 1980s. For example:

- Inflation in the U.S. reached 14% in 1982 (core inflation today is < 1%) ;

- The Prime Rate exceeded 20%;

- Mexico experienced a major debt default;

- Wars broke out between the U.K./Falklands & Iran/Iraq;

- Chrysler got bailed out;

- Egyptian President Anwar Sadat was assassinated;

- Hyperinflation spread throughout South America (e.g., Bolivia, Argentina, Brazil)

As I’ve mentioned before, in recent decades we’ve survived wars, assassinations, currency crises, banking crises, Mad Cow disease, SARS, Bird Flu, and yes, even recessions – about two every decade on average. “We’ve had 11 recessions since World War II and we’ve had a perfect score — 11 recoveries,” famed investor Peter Lynch highlighted last year. Media squawkers and industry pundits constantly want you to believe “this time is different.” Economic cycles have an odd way of recurring, or as Mark Twain astutely noted, “History never repeats itself, but it often rhymes.” I agree.

Certainly, each recession and bear market is going to have its own unique contributing factors, and right now we’re saddled with excessive debt (government and consumers), real estate is still in a lot of pain, and unemployment remains stubbornly high (9.5% in June). Offsetting these challenges is a global economy powered by 6 billion hungry consumers with an appetite of achieving a standard of living rivaling ours. Underpinning the surge in developing market growth is the expansion of democratic rule and an ever-sprawling extension of the technology revolution. In 1900, there were about 10 countries practicing democracy versus about 120 today. These political advancements, coupled with the internet, are flattening the world in a way that is creating both new competition and opportunities. The rising tide of emerging market demand for our leading edge technologies not only has the potential of elevating foreigners’ standard of living, but pushing our living standards higher as well.

With the United States economy representing roughly 25% of the globe’s total Gross Domestic Product (~5% of the global population), simple mathematics virtually assures emerging markets will continue to eat more of the global economic pie. In fact, many economists believe China will pass the U.S. over the next 15 years. As long as the pie grows, and the absolute size (not percentage) of our economy grows, we should be happy as a clam as our developing country brethren soak up more of our value-added goods and services.

On a shorter term basis, Leonard profiles several abnormal characteristics practiced by consumers. Here’s what he has to say about the “New Abnormal”:

“The new abnormal has given rise to a nation of schizophrenic consumers. They splurge on high-end discretionary items and cut back on brand-name toothpaste and shampoo. Companies like Apple, whose net income jumped 94 percent in its last quarter, and Starbucks, which is enjoying a 61 percent increase in operating income over the same time frame, are thriving. Mercedes-Benz is having a record sales year; deliveries of new vehicles in the U.S. rose 25 percent in the first six months of 2010. Lexus and BMW were also up. Though luxury-goods manufacturers like Hermýs [sic] and Burberry are looking primarily to Asia for growth, their recent earnings reports suggest stabilization and even modest improvement in the U.S.”

Beyond the fray of high-end products, the masses have found reasons to also splurge at the nation’s largest mall (The Mall of America), home to a massive amusement park and a 1.2 million gallon aquarium. So far this year, the mall has experienced a +9% increase in sales.

So while El-Erian calls for a “New Normal” to continue in the years to come, what might actually be happening is a return to an “Old Normal” with ordinary cyclical peaks and valleys. If this isn’t true, perhaps we will all revert to a “New Abnormal” mindset described by Devin Leonard. If so, I will see you at the Mercedes dealership in my Burberry suit, with $3 latte in hand.

Read Devin Leonard’s Complete New Abnormal Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in Mercedes, BMW, Burberry, Hermy’s, SBUX, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}