Posts tagged ‘Netflix’

Investors Slowly Waking to Technology Tailwinds

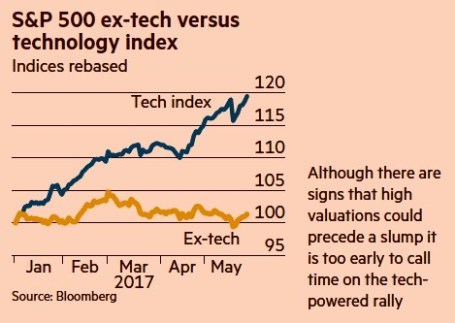

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Netflix: Burn It and They Will Come

In the successful, but fictional movie, Fields of Dreams, an Iowa farmer played by actor Kevin Costner is told by voices to build a field for baseball playing ghosts. After the baseball diamond is completed, the team of Chicago White Sox ghosts, including Shoeless Joe Jackson, come to play.

Well, in the case of the internet streaming giant Netflix Inc (NFLX), instead of chasing ghosts, the company continues to chase the ghosts of profitability. Netflix’s share price has already soared +63% this year as the company continues to burn hundreds of millions in cash, while aggressively building out its international streaming footprint. Unlike Kevin Costner, Netflix investors are likely to eventually get spooked by the by the stratospheric valuation and bleeding cash.

At Sidoxia, we may be a dying breed, but our primary focus is on finding market leading franchises that are growing cash flows at reasonable valuations. In sticking with my nostalgic movie quoting, I believe as Cuba Gooding Jr. does in the classic movie, Jerry Maguire, “Show me the money!” Unfortunately for Netflix, right now the only money to be shown is the money getting burned.

Burn It and They Will Come

In a little over three years, Netflix has burned over -$350 million in cash, added $2 billion in debt, and spent approximately -$11 billion on streaming content (about -$4.6 billion alone in the last 12 months). As the hemorrhaging of cash accelerates (-$163 million in the recent quarter), investors with valuation dementia have bid up Netflix shares to a head-scratching 350x’s estimated earnings this year and a still mind-boggling valuation of 158x’s 2016 Wall Street earnings estimates of $3.53 per share. Of course the questionable valuation built on accounting smoke and mirrors looks even more absurd, if you base it on free cash flow…because Netflix has none. What makes the Netflix story even scarier is that on top of the rising $2.4 billion in debt anchored on their balance sheet, Netflix also has commitments to purchase an additional $9.8 billion in streaming content in the coming years.

For the time being, investors are enamored with Netflix’s growing revenues and subscribers. I’ve seen this movie before (no pun intended), in the late 1990s when investors would buy growth with reckless neglect of valuation. For those of you who missed it, the ending wasn’t pretty. What’s causing the financial stress at Netflix? It’s fairly simple. Beyond the spending like drunken sailors on U.S. television and movie content (third party and original), the company is expanding aggressively internationally.

The open check book writing began in 2010 when Netflix started their international expansion in Canada. Since then, the company has launched their service in Latin America, the United Kingdom, Ireland, Finland, Denmark, Sweden Norway, Netherlands, Germany, Austria, Switzerland, France, Belgium, Luxembourg, Australia, and New Zealand.

With all this international expansion behind Netflix, investors should surely be able to breathe a sigh of relief by now…right? Wrong. David Wells, Netflix’s CFO had this to say in the company’s recent investor conference call. Not only have international losses worsened by 86% in the recent quarter, “You should expect those losses to trend upward and into 2016.” Excellent, so the horrific losses should only deteriorate for another year or so…yay.

While Netflix is burning hundreds of millions in cash, the well documented streaming competition is only getting worse. This begs the question, what is Netflix’s real competitive advantage? I certainly don’t believe it is the company’s ability to borrow billions of dollars and write billions in content checks – we are seeing plenty of competitors repeating the same activity. Here is a partial list of the ever-expanding streaming and cord-cutting competitive offerings:

- Amazon Prime Instant Video (AMZN)

- Apple TV (AAPL)

- Hulu

- Sony Vue

- HBO Now

- Sling TV (through Dish Network – DISH)

- CBS Streaming

- YouTube (GOOG)

- Nickelodeon Streaming

Sadly for Netflix, this more challenging competitive environment is creating a content bidding war, which is squeezing Netflix’s margins. But wait, say the Netflix bulls. I should focus my attention on the company’s expanding domestic streaming margins. This is true, if you carelessly ignore the accounting gimmicks that Netflix CFO David Wells freely acknowledges. On the recent investor call, here is Wells’s description of the company’s expense diversion trickery by geography:

“So by growing faster internationally, and putting that [content expense] allocation more towards international, it’s going to provide some relief to those global originals, and the global projects that we do have, that are allocated to the U.S.”

In other words, Wells admits shoving a lot of domestic content costs into the international segment to make domestic profit margins look better (higher). Longer term, perhaps this allocation could make some sense, but for now I’m not convinced viewers in Luxembourg are watching Orange is the New Black and House of Cards like they are in the U.S.

Technology: Amazon Doing the Heavy Lifting

If check writing and accounting diversions aren’t a competitive advantage, does Netflix have a technology advantage? That’s tough to believe when Netflix effectively outsources all their distribution technology to Amazon.com Inc (AMZN).

Here’s how Netflix describes their technology relationship with Amazon:

“We run the vast majority of our computing on [Amazon Web Services] AWS. Given this, along with the fact that we cannot easily switch our AWS operations to another cloud provider, any disruption of or interference with our use of AWS would impact our operations and our business would be adversely impacted. While the retail side of Amazon competes with us, we do not believe that Amazon will use the AWS operation in such a manner as to gain competitive advantage against our service.”

Call me naïve, but something tells me Amazon could be stealing some secret pointers and best practices from Netflix’s operations and applying them to their Amazon Prime Instant Video offering. Nah, probably not. Like Netflix said, Amazon wouldn’t steal anything to gain a competitive advantage…never.

Regardless, the real question surrounding Netflix should focus on whether a $35 billion valuation should be awarded to a money losing content portal that distributes content through Amazon? For comparison purposes, Netflix is currently valued at 20% more than Viacom Inc (VIA), the owner of valuable franchises and brands like Paramount Pictures, Nickelodeon, MTV, Comedy Central, BET, VH1, Spike, and more. Viacom, which was spun off from CBS 44 years ago, actually generated about $2.5 billion in cash last year and paid out about a half billion dollars in dividends. Quite a stark contrast compared to a company accelerating its cash losses.

I openly admit Netflix is a wonderful service, and I have been a loyal, longtime subscriber myself. But a good service does not necessarily equate to a good stock. And despite being short the stock, Sidoxia is actually long the company’s bonds. It’s certainly possible (and likely) Netflix’s stock will underperform from today’s nosebleed valuation, but under almost any scenario I can imagine, I have a difficult time foreseeing an outcome in which Netflix would go bankrupt by 2021. Bond investors currently agree, which explains why my Netflix bonds are trading at a 5% premium to par.

Netflix stockholders, and crazy disciples like Mark Cuban, on the other hand, may have more to worry about in the coming quarters. CEO Reed Hastings is sticking to his “burn it and they will come” strategy at all costs, but if profits and cash don’t begin to pile up quickly, then Netflix’s “Field of Dreams” will turn into a “Field of Nightmares.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AAPL, GOOGL, AMZN, long Netflix bond position, long Dish Corp bond, and a short position in NFLX, but at the time of publishing, SCM had no direct position in VIA, TWX, SNE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Whitney the Netflix Waffler

Source: Photobucket

No, I am not talking about Meredith Whitney (see Cloudy Crystal Ball), but rather Whitney Tilson, a well-known value and hedge fund manager at T2 Partners LLC. Less than eight weeks ago, Tilson boldly and brashly exclaimed why Netflix Inc. (NFLX) was an “exceptional short” and provided reasons to the world on why Netflix was his largest short position (read Tilson’s previous post). Fifty-five days later, Mr. Tilson evidently was overtaken by a waffle craving and decided to throw in the towel by covering his Netflix short position.

What Changed in Seven and Half Weeks?

Margin Thesis Compromised: Tilson explains, “The company reported a very strong quarter that weakened key pillars of our investment thesis, especially as it relates to margins.” Really? Netflix has grown revenues for nine straight years since its IPO (Initial Public Offering) in 2002, and growth has even accelerated for two whole years (as Netflix has shifted to streaming content over snail-mail), and just in Q4 he became surprised by this multi-year trend? The Q4 growth caught Tilson off-guard, but I guess Tilson wasn’t surprised by the 7.5 million subscribers Netflix added in 2009 and first three quarters of 2010. Never mind the five consecutive years of operating margin expansion either (source: ADVFN), nor the stealthy share price move from $30 to around $225. Apparently Tilson needed the recently reported Q4 financial results to hit him over the head.

Survey Provides Earth-Shattering Results: Tilson conducted an exhaustive study of “more than 500 Netflix subscribers, that showed significantly higher satisfaction with and usage of Netflix’s streaming service than we anticipated.” Come on…Netflix has more than 20 million subscribers, and you are telling me that a questionnaire of 500 subscribers (0.0025%) is representative. Even if these results are a cornerstone of Tilson’s modified thesis, I wonder also why the survey wasn’t taken before Netflix became Tilson’s largest negative short position. In addition, I can’t say it’s much of a revelation that Tilson found “significantly higher satisfaction” among paying subscribers. That’s like me going to a Justin Bieber concert and polling J-Beeb fans whether they like his music – I’ll go out on a limb and say paying customers will generally have a positive bias in their responses.

Feedback Tilts the Scales: Tilson received a “great deal of feedback, including an open letter from Netflix’s CEO, Reed Hastings.” If I received a penny for every time I heard a CEO speak positively about their company, I would be retired on a private island drinking umbrella drinks all day. Honestly, what does Tilson expect Hastings to say, “You know Whitney, you really hit the nail on the head with your analysis…I think you’re right and you should short our stock.”

Some other inconsistencies I’m still trying to figure out in Tilson’s new waffle thesis:

Valuation Head Scratcher: Also frustrating in Tilson’s 180 degree switch is his apparent incongruous treatment of valuation. In his initial bearish piece, Tilson explains how outrageously priced Netflix share are at 63.1x the high 2010 consensus estimate, but somehow a current 75.0x multiple (~20% richer) is reason enough for Tilson to blow out his short.

Competition: Although Tilson went from 100% short Netflix to 0% short Netflix, there does not appear to be any new information regarding Netflix’s competitive dynamics from the Q4 financial release to change his view. Here is what he said in his article eight weeks ago:

“Netflix’s brand and number of customers pale in comparison to its new, direct competitors like Apple (iTunes), Google (GOOG) (YouTube), Amazon.com (AMZN) (Amazon Video on Demand), Disney (DIS) and News Corp. (NWS) (part ownership of Hulu), Time Warner (TWX, TWC) (cable, HBO, etc.), Comcast (CMCSA) (cable, NBC Universal, part ownership of Hulu), and Coinstar’s Redbox (CSTR) (30,000 kiosks renting DVDs for $1/night and email addresses for 21 million customers).”

Little is said in his short covering note, other than these negative dynamics still exist and help explain why he is not long the stock.

Gently Under the Bus

Whitney Tilson was “against Netflix before he was for it,” a stance that could generate a tear of pride from fellow waffler John Kerry. However, I want to gently place Mr. Tilson under the bus with all my comments because his sudden strange reversal shouldn’t be blown out of proportion with respect to his full body of work. As a matter of fact, I have favorably profiled Tilson in several of my previous articles (read Tilson on BP and Tilson on Fat Lady Housing).

One would think given my profitable long position in Netflix that I would be congratulating Tilson for covering his short, but I must admit that I feel a little naked with fewer contrarians rooting against me. The herd is occasionally right, but the largest returns are made by not following the herd. Short interest was about 33% of the float (shares outstanding available for trading) mid-last month, and with the recent melt-up, my guess is that short percentage has shrunk with other short covering doubters. I haven’t decided how much, if any, profits I plan to lock-in with my Netflix positions, but as Tilson points out, they are not giving Netflix away for free.

Credit should also be given to Tilson for having the thickness of skin to openly flog himself and admit failure in such an open forum. I have been known to enjoy a waffle or two in my day as well (more often in the privacy of my own kitchen), and waffling on stocks can be preferable to loving stocks to the grave. Tilson has proven firsthand that eating waffles can be very expensive and detrimental to your profit waistline. By doing more homework on your stock consumption, your waffle eating should be spread further apart, making this habit not only cheaper, but also better for your long-term investment health.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) at the time of publishing had no direct position in DIS, NWS/Hulu, TWX, TWC, CMCSA, and CSTR but SCM and some of its clients own certain exchange traded funds, NFLX, AAPL, AMZN, AAPL, and GOOG, but did not own any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}