Posts tagged ‘nanotechnology’

NVEC: A Cash Plump Activist Target…For Icahn?

Some might call Carl Icahn a greedy capitalist, but at the core, the 78 year old activist has built his billions in fortunes by unlocking shareholder value in undervalued companies. His targets have come in many shapes and sizes, but one type of target is cash bloated companies without defined capital allocation strategies. A recent high profile example of a cash ballooned target of Icahn was none other than the $591+ billion behemoth Apple Inc. (AAPL).

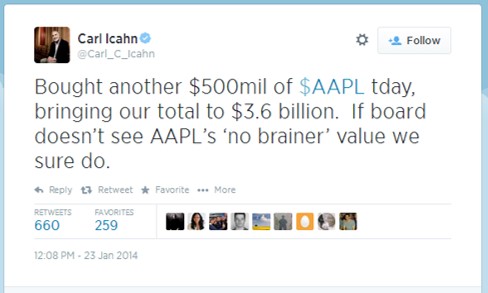

His initial tweet on August 13, 2013 announced his “large position” in the “extremely undervalued shares” of Apple ($67 split adjusted). We have been long-term shareholders of Apple ourselves and actually beat Carl to the punch three years earlier when the shares were trading at $35 – see Jobs: The Gluttonous Cash Hog. Icahn doesn’t just nonchalantly make outrageous claims…he puts his money where his mouth is. After Icahn’s initial proclamation, he went onto build a substantial $3.6 billion Apple position by January 2014.

Icahn initially demanded Apple’s CEO Tim Cook to execute a $150 billion share repurchase program before downgrading his proposal to a $50 billion buyback. After receiving continued resistance, Icahn eventually relented in February 2014. But Icahn’s blood, sweat, and tears did not go to waste. His total return in Apple from his initial announcement approximates +50%, in less than one year. And although Icahn wanted more action taken by the company’s management team, Apple has repurchased about $50 billion in stock and paid out $14 billion in dividends to investors over the last five quarters. Despite the significant amount of capital returned to shareholders over the last year, Apple still holds a gargantuan net cash position of $133.5 billion, up approximately $3 billion from the 2013 fiscal third quarter.

Icahn’s Next Cash Plump Target?

Mr. Icahn is continually on the prowl for new targets, and if he played in the small cap stock arena, NVE Corp. (NVEC) certainly holds the characteristics of a cash bloated company without a defined capital allocation strategy. Although I rarely write about my hedge fund stock holdings, followers of my Investing Caffeine blog may recognize the name NVE Corp. More specifically, in 2010 I picked NVEC as my top stock pick of the year (see NVEC: Profiting from Electronic Eyes, Nerves & Brains). The good news is that NVEC outperformed the market by approximately +25% that year (+36% vs 11% for the S&P 500). Over the ensuing years, the performance has been more modest – the +42% return from early 2010 has underperformed the overall stock market.

Rather than rehash my whole prior investment thesis, I would point you to the original article for a summary of NVE’s fundamentals. Suffice it to say, however, that NVE’s prospects are just as positive (if not more so) today as they were five years ago.

Here are some NVE data points that Mr. Icahn may find interesting:

- 60% operating margins (achieved by < 1% of all non-financial companies FINVIZ)

- 0% debt

- 15% EPS growth over the last seven years ($1.00 to $2.29)

- Cutting edge, patent protected, market leading spintronic technology

- +7% Free Cash Flow yield ($13m FCF / $194 adjusted market value) $294m market cap minus $100m cash.

- $100 million in cash on the balance sheet, equal to 34% of the company’s market value ($294m). For comparison purposes to NVE, Apple’s $133 billion in cash currently equates to about 23% of its market cap.

Miserly Management

As I noted in my previous NVE article, my beef with the management team has not been their execution. Despite volatile product sales in recent years, it’s difficult to argue with NVE CEO Dan Baker’s steering of outstanding bottom-line success while at the helm. Over Baker’s tenure, NVE has spearheaded meteoric earnings growth from EPS of $.05 in 2009 to $2.29 in fiscal 2013. Nevertheless, management not only has a fiduciary duty to prudently manage the company’s operations, but it also has a duty to prudently manage the company’s capital allocation strategy, and that is where NVE is falling short. By holding $100 million in cash, NVE is being recklessly conservative.

Is there a reason management is being so stingy with their cash hoard? Even with cash tripling over the last five years ($32m to $100m) and operating margins surpassing an incomprehensibly high threshold (60%), NVE still has managed to open their wallets to pursue these costly actions:

- Double Capacity: NVE doubled their manufacturing capacity in fiscal 2013 with minimal investment ($2.8 million);

- Defend Patents: NVE fought and settled an expensive patent dispute against Motorola spinoff (Everspin) as it related to the company’s promising MRAM technology;

- R&D Expansion: The company shored up its research and development efforts, as evidenced by the +39% increase in fiscal 2014 R&D expenditures, to $3.6 million.

The massive surge in cash after these significant expenditures highlights the indefensible logic behind holding such a large cash mound. How can we put NVE’s pile of cash into perspective? Well for starters, $100 million is enough cash to pay for 110 years of CAPEX (capital expenditures), if you simply took the company’s five year spending average. Currently, the company is adding to the money mountain at a clip of $13,000,000 annually, so the amount of cash will only become more ridiculous over time, if the management team continues to sit on their hands.

To their credit, NVE dipped half of a pinky toe in the capital allocation pool in 2009 with a share repurchase program announcement. Since the share repurchase was approved, the cash on the balance sheet has more than tripled from the then $32 million level. To make matters worse, the authorization was for a meaningless amount of $2.5 million. Over a five year period since the initial announcement, the company has bought an irrelevant 0.5% of shares outstanding (or a mere 25,393 shares).

A Prudent Proposal

The math does not require a Ph.D. in rocket science. With interest rates near a generational low, management is destroying value as inflation eats away at the growing $100 million cash hoard. I believe any CFO, including NVE’s Curt Reynders, can be convinced that earning +7% on NVE shares (or +15% if earnings compound at historical rates for the next five years) is better than earning +2% in the bank. Or in other words, buying back stock by NVE would be massively accretive to EPS growth. Conceptually, if NVE used all $100 million of its cash to buy back stock at current prices, NVE’s current EPS of $2.59 would skyrocket to $3.63 (+40%).

A more reasonable proposal would be for NVE management to buy back 10% of NVE’s stock and simultaneously implement a 2% dividend. At current prices, these actions would still leave a healthy balance of about $75 million in cash on the balance sheet by the end of the fiscal year, which would arguably still leave cash at levels larger than necessary.

Despite the capital allocation miscues, NVE has incredibly bright prospects ahead, and the recently reported quarterly results showing +37% revenue growth and +57% EPS growth is proof positive. As a fellow long-term shareholder, I share management’s vision of a bright future, in which NVE continues to proliferate its unique and patented spintronic technology. With market leadership in nanotechnology sensors, couplers, and MRAM memory, NVE is uniquely positioned to take advantage of game changing growth in markets such as nanotechnology biosensors, electric drive vehicles (EDVs), consumer electronic compassing, and next generation MRAM technology. If NVE can continue to efficiently execute its business plan and couple this with a consistent capital allocation discipline, there’s no reason NVE shares can’t reach $100 per share over the next three to five years.

While NVE continues to execute on their growth vision, they can do themselves and their shareholders a huge favor by implementing a shareholder enhancing capital return plan. Carl Icahn is all smiles now after his successful investments in Apple and Herbalife (HLF), but impatient investors and other like-minded activists may be lurking and frowning, if NVE continues to irresponsibly ignore its swelling $100 million cash hoard.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in Apple Inc. (AAPL), NVE Corp. (NVEC), and certain exchange traded funds, but at the time of publishing SCM had no direct position in TWTR, MOT, Everspin, HLF, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

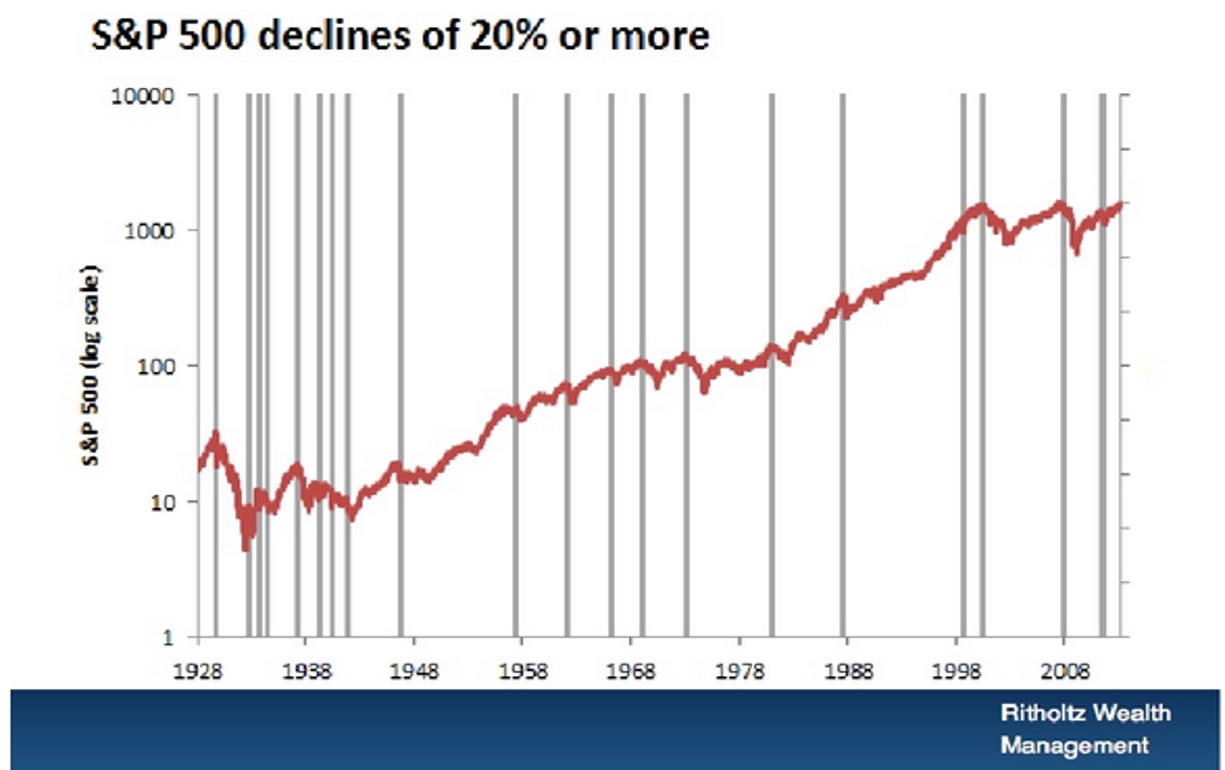

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

NVEC: Profiting from Electronic Eyes, Nerves & Brains

Recently, Seeking Alpha Editor-in-Chief Mick Weinstein interviewed me with the purpose of reviewing an equity investment I find attractive. For the “stock-jock” Investing Caffeine followers, I am publishing the January 5th interview below.

What is your highest conviction stock position in your fund – long or short?

I don’t really have a highest conviction stock, per se, in my fund since I treat all my stocks like children – I love them all. Having said that, NVE Corp. (ticker: NVEC) is a holding of mine that exhibits many of the characteristics I look for in an investment. The Eden Prairie, Minnesota based company is named after “Nonvolatile Electronics,” which refers to memory technology that retains data even when power is removed – a critical attribute for certain applications.

Tell us a bit about the company and what it does.

NVE Corp. is a market leader in nanotechnology sensors, couplers, and MRAM intellectual property (Magnetoresistive Random Access Memory). NVE’s microscopic technology enables the transmission, acquisition, and storage of data across a broad array of applications, including implantable medical devices, mission critical defense weapons, and industrial robots. Major customers include: St. Jude Medical, Inc. (STJ), Starkey Laboratories, Inc., and the U.S. Government.

The company’s coupler and sensor businesses have been ridiculously profitable. Even over a period covering one of the worst global financial crisis in decades, NVE managed to increase its operating margins from an already very respectable 40% range in Fiscal 2007 (ending March) to a stunning 56%+ level in Fiscal 2009.

Beyond sensors and couplers, NVE Corp. is optimistic about the potential for the MRAM market. However, outside of a few one-time licensing fees, NVE is currently generating effectively $0 revenues from this nascent storage technology. Outside of producing small MRAM devices for niche applications such as tamper prevention, NVE Corp. is looking to leverage their IP portfolio by licensing out the patents and subsequently receiving royalties from MRAM device manufacturers. MRAM technology uses magnetic fields to record information, but unlike tape recorders in which a short section of tape holds magnetic information, with MRAM data is held by electrons with out the need of moving parts to read or write data. Believe it or not, this method is highly reliable and is very power-efficient relative to other storage technology alternatives. Currently, the problem with MRAM is the cost prohibitive manufacturing requirements relative to other memories (such as DRAM, SRAM, and Flash), but costs are expected to come down over time. For some MRAM believers, the technology is considered the “Holy Grail” because it may have the potential to combine the speed of SRAM, the density of DRAM, and the non-volatility of Flash memory in a universal source.

If the unproven potential of MRAM ever blossoms, the broad portfolio of NVE Corp.’s MRAM patents should represent a very sizeable profit opportunity. Of course, NVE Corp. must first establish the validity of its MRAM intellectual property and appropriately charge and collect royalties for IP usage. How big can the MRAM market be? Some size the MRAM market in the billions and Toshiba has stated they expect the MRAM market to surpass the size of the traditional memory markets by 2015.

No matter how one measures the size of the market, there will be a substantial revenue opportunity for NVE Corp. if every smart-phone, gaming device and laptop exclusively uses universal MRAM – rather than a combination of DRAM, SRAM, and Flash technologies.

Can you talk a bit about the industry/sector? How much is this an “industry pick” as opposed to a pure bottom-up pick?

Generally speaking, I am a bottom-up investor. I may have concrete views on a particular industry, but the fundamentals of a company will be the main determinant of my investment thesis. Overall, I am looking for market leading franchises that can sustain above-average growth rates for extended periods of time. These traits can come from either a company operating in a mature, sleepy industry (take for example Google in the advertising world) or from a more dynamic growth industry like nanotechnology in the case of NVE Corp.

I believe the nanotechnology industry is in the very early innings of an innovation revolution with regard to new applications and products. Like semiconductors, the economies of scale and technological advances of NVE Corp.’s “spintronic” technology should continually allow faster, smaller, more reliable solutions at lower bit prices. In my view, this snowballing effect will only increase the penetration of nanotechnology solutions and introduce an ever increasing list of new applications.

Can you describe the company’s competitive environment? How is this company positioned vis a vis its competitors?

NVE Corp. has competitors along all three of its spintronic businesses. In their sensor business, most of the competition comes from the makers of legacy electromechanical magnetic sensors, including HermeticSwitch, Inc., Meder Electronic AG (Germany), and Memscap SA (France).

In the coupler space, NVE Corp. faces a larger list of well capitalized, household semiconductor names, including Avago (AVGO), Fairchild Semiconductor International (FCS), NEC Corporation, Sharp Corporation, Toshiba Corporation, Vishay Intertechnology (VSH), Analog Devices, Inc. (ADI), Silicon Laboratories Inc. (SLAB), and Texas Instruments Incorporated (TXN).

A different set of competitors are searching for the MRAM holy grail, including the following companies: Crocus Technology SA (France), Grandis, Inc., MagSil Corporation, Spintec (France), Spintron (France), Spintronics Plc (UK), and IBM.

There is undoubtedly a ton of competition in the spintronics space, but as of October 2009, NVE Corp. has 52 issued U.S. patents and over 100 patents worldwide (either issued, pending, or licensed from others) – many focused on the potentially lucrative MRAM field. Although NVE Corp. has many competitors, they have dominant share in the coupler/sensor market when it comes to high-end, merchant supplied solutions. Moreover, on the MRAM side of the business, the company has already licensed its intellectual property to several companies, including Cypress Semiconductor (CY), Honeywell International Inc. (HON), and Motorola, Inc. (MOT).

Can you talk about valuation? How does valuation compare to the competitors?

Valuation is a key component for all my stock investments. In my valuation work I pore over the income statement, balance sheet and cash flow statement in deriving my price targets.

One area helping NVE Corp.’s valuation case is its improving trend-line of profitability. Over the last 5 years alone, gross margins have gone from 40% to over 70% – not a bad business model if you can execute it. The company also has a pristine balance sheet. Not only does NVE Corp. have no debt, but it also is sitting on a growing mound of cash/investments (over $43 million), representing more than 20% of the company’s market capitalization. Lastly, the company in my view is attractively priced on a free cash flow basis (cash from operations minus capital expenditures), yielding around 6% of the total company value.

What is the current sentiment on the stock? How does your view differ from the consensus?

With small cap stocks like NVE Corp., sentiment and lack of liquidity can create gut-wrenching volatility. Unlike many growth investors who pay more attention to positive momentum factors (price direction), I welcome volatility as it allows me to find more attractive entry and exit points.

With that said, NVE Corp. hit a peak stock price north of $63 per share in early September fueled by 41% revenue growth in their June quarter (fiscal Q1). Subsequently, in fiscal Q2 (ending September 30th), revenue growth decelerated to +14% causing momentum investors to take NVE Corp.’s shares to the woodshed. With the stock down about -35% from its recent crest, I find the valuation only that much more attractive.

Wall Street estimates are calling for further slowing in revenue growth in the coming quarter, so the short term sentiment may or may not continue to sour? Timing bottoms is inherently dangerous and not something I consider myself an expert at. Absent a major deterioration in fundamentals, I stand ready to add to my position if NVE Corp.’s share price falls and valuation metrics improve.

I would argue the typical consensus view advocates selling shares when revenue growth slows. Many of my best performing stocks have been purchased during transitory periods of slowing or cyclical downturns. Let’s hope that’s the case with NVE Corp.

Does the company’s management play a role in your position? If so, how?

Absolutely. There is a continual debate over what is more important, the jockey or the horse? My investment philosophy puts more weight on the jockey than the horse. Obviously, I’m looking for the combination of a talented management team and a solid business model.

When it comes to NVE Corp., Daniel Baker, Ph.D. has done a phenomenal job managing the hyper-growth profile of the company, while preserving prudent and conservative financial values. For the third year in a row, Dr. Baker was also recognized as one of the best U.S. CEOs in the semiconductors and semiconductor equipment industry by investment research and financial consulting firm DeMarche Associates.

At the end of the day, it’s difficult to argue with a track record of success. Since Dr. Baker took over, revenues have more than tripled and earnings have grown from $0.05 in fiscal 2001 to $2.04 in Fiscal 2009.

What catalysts do you see that could move the stock?

Since I hold a longer term investment horizon, catalysts are not a driving aspect to my investment process. But clearly, any additional evidence unearthed in the marketplace validating the growth in the MRAM market, or announcements confirming the value of NVE Corp.’s MRAM intellectual property, should provide support to the stock price.

Beyond that, given where the stock is trading now, I believe merely continuing the execution on their sensor and coupler business provides adequate upside prospects.

What could go wrong with this stock pick?

Investing in small cap technology stocks comes with a whole host of risks. Although I don’t believe the positive scenario of critical mass MRAM commercialization is baked into the current stock price, nevertheless I understand any setbacks announced relative to NVE Corp.’s MRAM prospects or the industry’s MRAM expectations, will likely result in stock price pressure.

NVE also has significant customer concentration, therefore a loss or cutback in sales from a lead customer will probably contribute to price volatility.

From a macro perspective, the company has battled successfully through the economic crisis and proven itself somewhat recession resistant. Nonetheless, the company has sizeable exposure to the industrial segment and would not be immune from the “double-dip” economic recession scenario.

Surely there are additional hazards to this investment, however these are some of the risks I am currently focused on.

Do you have any closing thoughts?

NVE Corp. is not a stock for the faint of heart. However, for those who can stomach the volatility, I encourage you to do some more homework on NVE Corp. Not only will you learn about a phenomenally managed, very profitable, attractively priced nanotechnology company, but you will also gain insight into a leading force behind the eyes, nerves, and brains powering the electronic systems of our future.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own shares in NVEC (and certain exchange traded funds), but did not have any direct positions in the following companies or stocks mentioned in this article at time of publication: STJ, HermeticSwitch, Inc., Meder Electronic AG, and Memscap SA, AVGO, FCS, NEC Corporation, Sharp Corporation, Toshiba Corporation, VSH, ADI, SLAB, TXN, Crocus Technology SA, Grandis, Inc., MagSil Corporation, Spintec, Spintron, and Spintronics Plc, IBM, CY, HON, and MOT. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}