Posts tagged ‘msft’

A.I. Field of Dreams

In the 1989 Academy Award–nominated film Field of Dreams, the lead character Ray Kinsella (played by Kevin Costner) hears a mysterious voice whisper, “If you build it, he will come.” Acting on blind faith, Ray builds a baseball diamond in the middle of his Iowa cornfield, risking financial ruin. Against all logic, the field draws a flood of visitors.

Today, a similar “field of dreams” is being built—not with corn, but with data centers. Instead of baseball players, it is artificial intelligence (AI) models, applications, and users who are coming.

The Market’s AI Momentum

The AI boom has already reshaped markets with all three benchmarks hitting record highs. Last month, the S&P 500 climbed +1.9%, while the NASDAQ rose +1.6% and Dow Jones Industrial Average surged +3.2%. Year to date, the indexes are up +10%, +11%, and +7%, respectively.

Behind this surge lies an unprecedented wave of AI infrastructure investment. Hyperscalers—Amazon.com (AMZN), Microsoft Corp. (MSFT), Google-Alphabet (GOOGL), Meta Platforms (META), and others—are pouring hundreds of billions into AI, much of it flowing directly to NVIDIA Corp. (NVDA), the undisputed leader in GPUs (Graphic Processing Units) powering the world’s AI engines. How large is the spending? NVIDIA CEO Jensen Huang estimates $3 trillion to $4 trillion will be spent this decade to fuel the AI revolution.

Source: Visual Capitalist

The Scale of AI’s Buildout

To put this into perspective:

- Amazon is projected to spend over $100 billion in 2025 alone, more than its cumulative capital expenditures from 2000–2020 combined.

Meta is constructing its $10 billion+ Hyperion data center in Louisiana—a sprawling 4 million sq. ft. complex across 2,250 acres, powered by a $4 billion natural gas plant. The footprint is so gargantuan it could cover much of Manhattan (see graphic below).

- xAI’s Colossus, a 750,000 sq. ft. data center in Memphis, Tennessee was completed in just 122 days—equivalent to building 418 homes in half the time it normally takes to construct one house (see slide below).

Source: BOND (Global Technology Investment Firm)

This breakneck pace of spending underscores the urgency and competitive pressure driving the global AI arms race.

The Origin of the AI Floodgates Opening

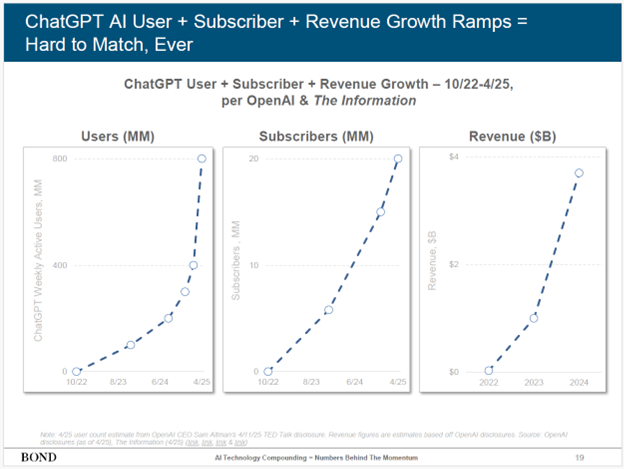

The spark was lit on November 30, 2022, when OpenAI released its LLM (large language model) called ChatGPT. Within two months, it amassed 100 million users.

Today, ChatGPT’s metrics have blasted much higher (see slide below):

- 800 million weekly active users

- 20 million paid subscribers

- $3.7 billion in revenue (as of April 2025)

Source: BOND (Global Technology Investment Firm)

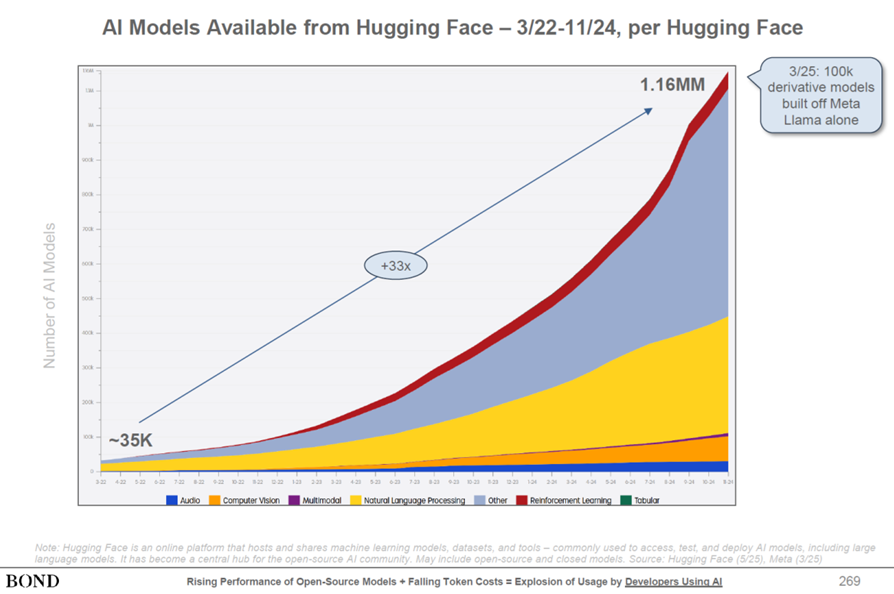

But OpenAI is far from alone. Google (Gemini), xAI (Grok), Anthropic (Claude), Meta (LLaMA), Amazon (Titan), Perplexity, and DeepSeek are all competing with their own LLMs. In total, over 1 million machine learning models now exist (see slide below) — each requiring costly compute power and pricey data centers.

Source: BOND (Global Technology Investment Firm)

Bubble or Productivity Breakthrough?

With trillions flowing into AI, a natural question arises: Is this a bubble?

Even OpenAI CEO Sam Altman admits we’re in an AI bubble :

“When bubbles happen, smart people get overexcited about a kernel of truth…Someone is going to lose a phenomenal amount of money… and a lot of people are going to make a phenomenal amount of money.”

Both realities can be true:

- Yes, hyperscalers are spending like “drunken sailors.”

- Yes, AI demand and productivity benefits are real and growing exponentially.

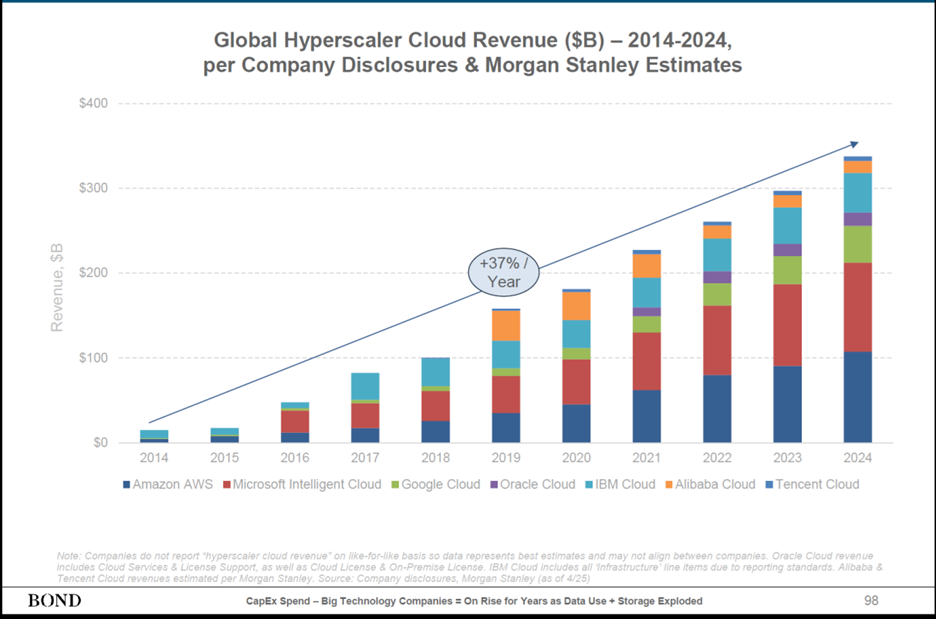

Consider the trajectory of global cloud revenues: from nearly $0 a decade ago to $300 billion today—a +37% CAGR (see chart below).

Source: BOND (Global Technology Investment Firm)

And the primary reason for cloud growth can be attributed to AI productivity benefits. A recent SAP survey found that workers using AI save nearly one hour per day on average. That’s transformative for companies: higher productivity without needing proportional hiring.

AI Use Cases Expanding Aggressively

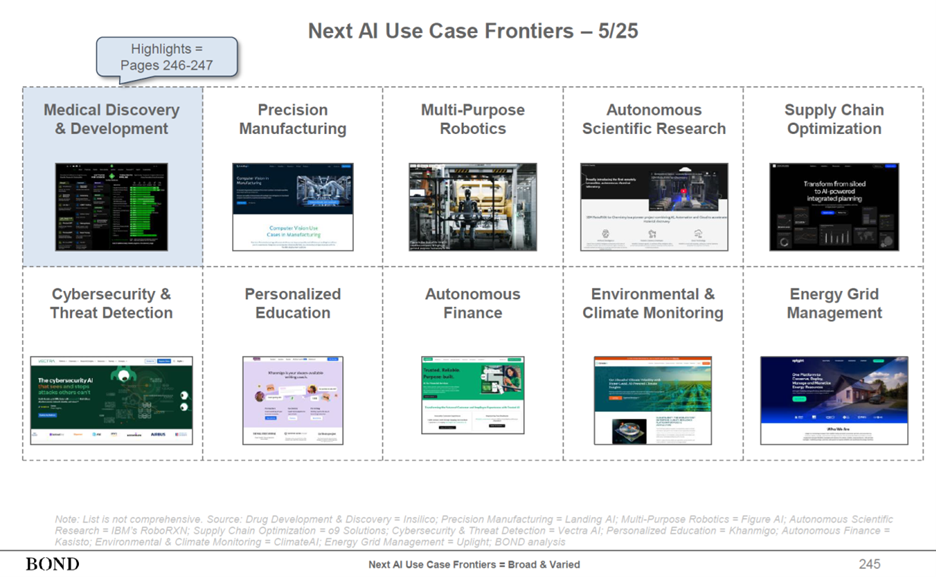

AI’s applications now span nearly every sector (see slide below):

- Technology – software engineering, code generation

- Customer Service & Marketing – customer support and call centers

- Transportation – autonomous vehicles and logistics

- Healthcare – drug discovery and development

- Supply Chains – precision manufacturing and optimization

- Automation – multi-purpose robotics

- Cybersecurity – threat detection and prevention

- Education – personalized lessons and curriculums

- Energy – grid optimization and demand forecasting

Source: BOND (Global Technology Investment Firm)

The New Field of Dreams

Throughout history, every great leap—printing press, steam engine, electricity, internet—has required massive upfront investment before the payoff arrived. AI is following the same path. Today, we are in the midst of building a new AI Field of Dreams. However, now, the data centers are the new baseball fields. And as with Ray Kinsella’s diamond, the masses are indeed coming.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GOOGL, META, AMZN, MSFT, NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SAP or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Mission Accomplished?

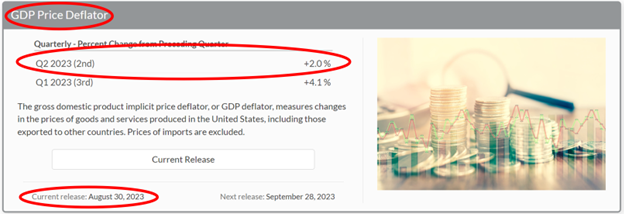

The Federal Reserve has a “dual mandate” designed to “foster economic conditions that achieve both stable prices and maximum sustainable employment.” The “dual mandate” is obviously a moving target, but it appears for now, based on the Fed’s explicit goals, Fed Chairman, Jerome Powell, has accomplished the central bank’s mission. More specifically, inflation, according to the just-reported BEA’s (Bureau of Economic Analysis) GDP Price Deflator statistics, has plummeted dramatically to the Fed’s goal of 2.0% from the sky-high inflation number of 9.1% a year ago (see chart below). Meanwhile, the economy continues to grow (+2.0% GDP growth in the 2nd quarter), and the long-awaited recession boogeyman has yet to appear.

Source: Bureau of Economic Analysis

Rate Pig Moving Through Economic Python

How has inflation plunged so quickly? For starters, in addition to the Fed’s restrictive policy of reducing the balance sheet, since the beginning of last year, the Fed has also effectively slammed the brakes on the economy by taking their target interest rate from 0% to 5.5%. The pace and scale of the interest rate increases have been reduced this year, however it is possible there might be more rate hikes ahead (currently, pundits are betting for no more rate increases this year, although a boost in November is possible if economic data accelerates). Like a pig working its way through the economic python, the large interest rate increases naturally take a while to work their way through the consumer, commercial, and government credit markets.

To put things in better perspective, a study done earlier this year showed the average 30-year monthly mortgage payment for a $500,000 home was higher by more than $800 (up +44%) versus a year ago! But wait, it’s not just consumers feeling the pinch of higher rates. Businesses and governments in all shapes and sizes have felt the pain as well from higher borrowing costs. Post-COVID supply chain constraints and disruptions have eased too, which have helped choke down the high inflation numbers. In the background, let’s not also forget about the disinflationary benefits of ever-expanding technology adoption coupled with the related productivity advantages (see also AI Revolution).

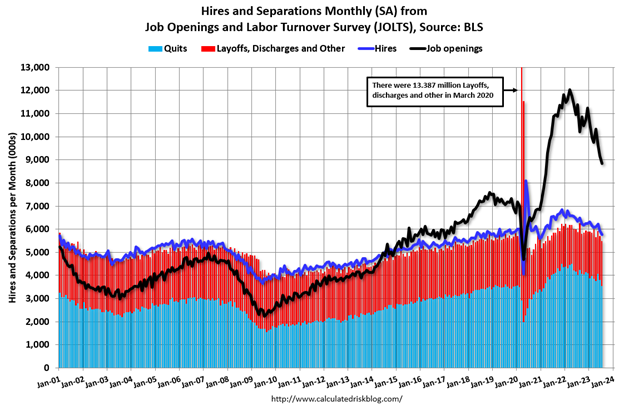

As a result of these dynamics, we are now starting to see cracks appear in our country’s employment foundation as this month’s JOLTs (Job Openings and Labor Turnover – see black line in chart below) and ADP monthly job additions data, which both came in disappointingly low compared to forecasts. Chairman Powell must be ecstatic inflation has plummeted, while the unemployment rate remains near multi-decade lows, and Gross Domestic Product (GDP) growth continues expanding (i.e., no recession in sight).

Source: Calculated Risk and U.S. Bureau of Labor Statistics

Hot Summer, Hot Stocks

Economic activity clearly can and will change, but the stock market has been like the weather this summer…hot. However, after experiencing up-months in six out of the first seven months of 2023, the S&P 500 index decided to take a small breather this month. For August, the S&P slipped -1.8%, but the month was a tale of two cities. By the middle of the month, the index had fallen by roughly -6% on fears of potentially more aggressive interest rate hikes by the Federal Reserve due to better than anticipated economic data. In other words, inflation fears were on the rise and the 10-Year Treasury Note yield temporarily climbed to a 52-week high. By the end of the month, economic data cooled, interest rates dropped a little, and stock prices rebounded smartly by +4.0% to finish the month on a strong note.

For the year, the S&P’s remain strongly positive, up +17.4%. As I have written in the past, the seven largest companies in the S&P 500 index (a.k.a., The Magnificent 7: Apple Inc.; Microsoft Corp.; Alphabet Inc.; Amazon.com, Inc.; NVIDIA Corp.; Tesla, Inc.; and Meta Platforms, Inc.) have contributed to a significant portion of the year’s gains – the average Magnificent 7 stock has skyrocketed an eye-popping +99.0% with NVIDIA being the largest winner, more than tripling in value during the first eight months of the year.

The Federal Reserve can admit they were late to the game in taming out-of-control inflation, but Fed Chair Powell has been swift in moving to preserve his legacy as an inflation fighter. Now that inflation is coming under control and the economy is beginning to cool, Powell needs to make sure he doesn’t murder the economy into recession with overzealous future interest rate increases. Time will tell if the mission has already been accomplished, but so far, the Fed has been delicately balancing an economic soft landing and stock market investors like it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, MSFT, GOOGL, AMZN, NVDA, TSLA, META, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Microsoft Makes Dividend Splash

Source: ActingLikeAnimals.com

I’ve talked about growing profits and cash piles for a while now (read more), but at some point investors and board members get restless and demand action (Steve Jobs has not yet). The most recent blue-chip company to make a splash, when it comes to capital management, is Microsoft Corp. (MSFT), which just announced a significant +23% increase in its dividend in conjunction with $4.75 billion in debt offerings. These capital structure changes still leave plenty of room for additional share repurchases and acquisitions.

Debt Offering – Are You Sure?

Huh? What in the heck is Microsoft doing borrowing money? I mean, does a company with $44 billion in cash and investments, generating a whopping additional $22 billion in free cash flow in fiscal 2010 (ended in June), really need access to additional capital? The short answer is “NO.” But a company like Microsoft borrowing $4.75 billion is like Donald Trump borrowing $50 on his credit card. Well wait, “The Donald” has actually had some hair and Chapter 11 problems, so the more appropriate analogy would be Bill Gates borrowing $20 on his credit card. Not only is it a rounding error, but it’s a good financial management practice for corporations to take advantage of the debt tax shield (read definition).

What makes Microsoft’s debt issuance that much more incredible is the astonishingly low rates the company is paying investors on the debt. According to Dealogic, Microsoft set a record low for yield paid on corporate unsecured debt. For the separate maturities ranging from 2013 to 2040, Microsoft paid a stunningly low 25-83 basis point spread over Treasuries. I don’t want to get into government credit worthiness today, but who knows, maybe Microsoft will pay lower debt rates than the U.S. Treasury, in the not too distant future?!

Regardless of the array of capital structure management strategies used by other companies, Microsoft is not alone in dealing with its cash hoarding problems. Cisco Systems Inc. (CSCO), another blue-chip cash printing press, just announced the initiation of a 1-2% dividend to be paid by the end of their fiscal year ending in July 2011 (read more about dividend cash “un-hoarding”).

But Who Cares?

Who cares about Microsoft’s wimpy 2.62% yield anyway? Well, for one, I sure care! A 10-year Treasury Note is yielding a measly, static 2.55%. If Microsoft continued on the same dividend path growth over the next five years as it did over the last five years, investors could potentially be talking about a 5.2% yield on our initial investment, and this excludes any potential stock price appreciation. With only roughly a 25% payout ratio on Microsoft’s fiscal 2010 free cash flow, the company has a lot of freedom to hike future dividends, even if earnings don’t grow. Microsoft has also enhanced shareholder value by putting its money where its mouth is by purchasing over $30 billion of company stock over the last three years.

Nice trend in dividend growth.

The extreme case of dividend growth is Wal-Mart Stores (WMT), which if purchased in 1972 would provide a +2,300% yield on the original investment, excluding any benefit from the massive price appreciation ($.05 split-adjusted per share to $53.65). Microsoft is no young chick like Wal-Mart 40 years ago, but you get the gist (read Dividend Sapling to Fruit Tree).

So while strategists and economists fret about the possibilities of a “double dip” recession, in the interim there have been 179 companies in the S&P 500 index that have hiked dividends in 2010 (versus only 3 companies that have cut). Microsoft has been no slouch either, growing revenues by +22% and EPS (Earnings Per Share) by +50% in their most recent fiscal fourth quarter. Although Microsoft’s stock is down -20% for 2010, the capital management and dividend splash recently announced by Microsoft (and other companies) should eventually capture the eye of investors currently earning squat on overpriced bonds and almost worthless Certificates of Deposit.

Read complete Microsoft dividend story

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, CSCO, nd WMT, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Google: The Quiet Steamroller

As Google Inc. (GOOG) has proceeded to steamroll most of its competition on the global advertising roads, they are learning to tread a little more lightly in hopes of avoiding unneeded scrutiny. There are very few places to hide, when your company is on track to achieve more than $20 billion in annual sales and is valued at more than $175 billion in the marketplace.

As Google revenues continue to rise and they look to take over the world (including their position in China), they are enlisting others to assist them in Washington as well. Through three quarters of 2009, the company increased their lobbyist budget by 41% to approximately $3 million, according to the Associated Press (AP).

Google Eating Bite Sized Acquisitions

Ever since the controversy caused by Google’s $3.1 billion takeover of web advertising network company DoubleClick (2007 announcement), and the failed joint search agreement with Yahoo! (YHOO) in 2008 due to government and advertiser concerns, Google has decided to consume smaller bite-sized companies as part of its acquisition strategy. Over the last five months alone, Google has acquired eight different small companies (generally less than $50 million acquisition price), including the following: 1) Picknik (photo editing website); 2) reMail (mobile search applications); 3) Aardvark (social networking focus); and 4) AdMob ($750 million mobile advertising network deal). Eric Schmidt, Google CEO, has stated he would like to do one smaller-sized acquisition per month. Google management also believes they have lowered the inherent risk in these smaller deals because of legacy ties to target companies – all these sought after companies house former Google employees, says Bloomberg. In addition to remaining below the radar, the string of small deals act as a supplement to Google’s hiring practices, which can become challenging in a scarce qualified engineering hiring environment.

Microsoft Pot Calling Kettle Black

Microsoft (MSFT), the behemoth software giant with monopoly-like market share in the PC operating system market, is now fighting back against growing giant Google. This effectively amounts to the pot calling the kettle black, given Microsoft has already paid about $2.44 billion in fines to EU (European Union) relating to antitrust actions in the past 10 years, according to TechCrunch. Nonetheless, Microsoft CEO Steve Ballmer is not shy about throwing Google under the bus, stating Google is not playing fair in the search market. Furthermore, Microsoft has filed an antitrust complaint against Google in Europe as it relates to Ciao, an online shopping service powered by Microsoft, and cried foul over an agreement Google made with book publishers and authors on a separate project.

Google is not stupid. They have witnessed massive monopolistic companies like Microsoft and Intel (INTC) butt heads with regulators and pay billions in fines. Needless to say, Google will do everything in its power to avoid additional, unwanted oversight, while quietly driving their steamroller over the competition.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and GOOG, but at time of publishing had no direct position in MSFT, INTC, YHOO, or any other security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Equity Life Cycle: The Moneyball Approach

Building a portfolio of stocks is a little like assembling a baseball team. However, unlike a team of real baseball players, constructing a portfolio of stocks can mix low-priced single-A farm players with blue chip Hall of Fame players from the Majors. Billy Beane, the General Manager for the Oakland Athletics, was chronicled in Michael Lewis’ book, Moneyball. Beane creates an amazing proprietary system of building teams more cost-efficiently than his deep-pocketed counterparts by statistically identifying undervalued players with higher on-base and slugging percentages. According to Beane, traditional baseball scouts were overpaying for less relevant factors, such as speed (stolen bases) and hitting (batting percentage).

In the stock world, before you can scout your team, you must first determine where in the life cycle the company lies. If Beane were to name this quality, perhaps he would call it Time-to-Maturity (TTM). Some companies operate in small, mature bitterly competitive industries (e.g. shoe laces), while others may operate in large growing markets (e.g. Google [GOOG] in online advertising and algorithmic search). Some companies because of negative regulation or heightened competition have a very short life cycle from early growth to maturity. Other companies with competitive advantages and untapped growth markets can have very long life spans before reaching maturity (think of a younger Coca Cola [KO] or Starbucks [SBUX]). Like Beane talks about in his book, many young, promising, immature baseball players flame out with short TTMs, nonetheless many scouts overpay for the cache´ such players offer.

Unfortunately, many investors do not even contemplate the TTM of their stock. Buying juvenile stocks (i.e., private companies like Twitter & Facebook – see article) or elderly stocks in and of itself is not a bad thing, but before you price a security it’s advantageous to know what type of discount or premium is deserved. Obviously, I’m looking for undervalued stocks across all age spectrums, however finding an undervalued, undiscovered late-teen just beginning on its long runway of growth combines the best of all worlds. Finding what Peter Lynch calls the “multi-baggers” is easier said than done, like searching for a needle in a haystack, but the rewards can be handsome.

What creates long runways of growth – the equivalent of winning dynasties in baseball? Well, there are several contributors leading to longer TTMs, including economies of scale, large industries, barriers to entry, competitive advantages, growing industries, superior and experienced management teams, to name a few factors. But like anything, even the great growth companies, including Microsoft (MSFT), turn from teenagers to mature adults. As famed businessman Thomas Brittingham said, “A good horse can’t go on winning races forever, and a good stock eventually passes its peak, too.”

There are many aspects to creating a winning team. If Billy Beane were to draw up factors for a baseball team, I’m confident TTM would be near the top of his list. What you pay for the length of the growth cycle is obviously imperative, but since I’m a strong believer in the tenet that “price follows earnings,” it only makes sense that above average sustainable earnings growth should eventually lead to superior price appreciation. As Bob Smith, successful manager from T. Rowe Price states, “The important thing is not what you pay for the stock, so much as being right on the company.” So if you want to recruit a portfolio of winning stocks, like Billy Beane picks successful baseball players, then include the equity life cycle maturity statistic as a factor in your selection process.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management nor its client accounts have no direct position in MSFT, SBUX, KO, Facebook, or Twitter shares at the time this article was originally posted. Some Sidoxia Capital Management accounts do have a long position in GOOG shares. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

U.S. to China, “What’s Wrong With a Little Porn and Anarchy?”

The U.S. recently scheduled talks with the Chinese government to discuss the appropriateness of automated personal computer (PC) content filtering (including, pornography, Falun Gong, and governmental protest content). Falun Gong is a meditatitve spiritual discipline frowned down upon by the Chinese government.

I can picture it now, U.S. officials calling up Chinese President Hu Jintao and saying, “Hey Hu, why not lighten up a bit on the freedom crackdowns – what’s the big deal with a little pornography and anarchy?” The Chinese government feels that in the absence of structured laws, which would limit access to inappropriate content, the natives will become restless and ultimately disruptive. PC manufacturers would prefer not to reengineer PCs and increase the embedded costs to consumers by adding additional components. However, given the size of the Chinese PC market, the dominant foreign manufacturers are likely to cave to Chinese government demands, given the massive long-term potential of this Asian market. We have already seen Google (GOOG), Yahoo (YHOO), and Microsoft (MSFT) make concessions to the Chinese government in the algorithmic search arena.

The thematic parallels presently occurring in China apply to William Golding’s Lord of the Flies (1954) as well. Lord of the Flies is a story about a group of stranded kids (surviving a plane crash) that battle for survival on a deserted island. Due to the lack of law, adult supervision and questionable tendencies, all hell eventually breaks loose. The Chinese government, managing a population of 1.3 billion people, fears a similarly hellacious outcome if an uncontrolled, lawless population consumes unfettered, unhealthy content. Given mistakes we’ve made abroad (e.g., Abu Ghraib, and Guantanomo), the Chinese and other countries are questioning the strength of our moral compass in judging or guiding other countries’ policies.

The thematic parallels presently occurring in China apply to William Golding’s Lord of the Flies (1954) as well. Lord of the Flies is a story about a group of stranded kids (surviving a plane crash) that battle for survival on a deserted island. Due to the lack of law, adult supervision and questionable tendencies, all hell eventually breaks loose. The Chinese government, managing a population of 1.3 billion people, fears a similarly hellacious outcome if an uncontrolled, lawless population consumes unfettered, unhealthy content. Given mistakes we’ve made abroad (e.g., Abu Ghraib, and Guantanomo), the Chinese and other countries are questioning the strength of our moral compass in judging or guiding other countries’ policies.

Although the U.S. government’s intentions are in the right place to protect the personal freedoms of people globally, we are not currently in the strongest moral position right now to cram our beliefs down other’s throats. Even the freest of societies such as our own limits certain actions – such as underage voting, underage drinking, and public nudity (O.K., I’m stretching a bit).

Regardless of your political views, one can appreciate the fear of anarchy in the hearts of the Chinese government. Practically speaking however, given the openness and rapid expansion of the global internet, the Chinese can only slow the expansion of individuals’ freedoms – recent events in the Middle East just provide additional evidence to this premise.

DISCLOSURE: At the time of publishing, in addition to owning certain exchange traded funds, Sidoxia Capital Management and some of its clients also owned GOOG, but had no direct positions in YHOO, MSFT, or any other security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}