Posts tagged ‘Middle East’

Mideast War an Investor Bore as Markets Soar

If I told you at the beginning of the year that the U.S. would bomb key nuclear sites in Iran, would you have guessed that Middle East stability would follow—and that global financial markets would soar to record highs? Personally, I wouldn’t have bet on that outcome. But that’s exactly what happened last month. While geopolitical dynamics remain fluid, markets shrugged off the chaos. The S&P 500 rallied +5.0%, the Dow Jones Industrial Average climbed +4.3%, and the NASDAQ catapulted +6.6%, powered largely by artificial intelligence stocks like NVIDIA Corp., which surged +16.9% for the month to a market value of $3.9 trillion (more on AI below). This is an important reminder that trading off of news headlines is a fool’s errand.

Economy Resilient Despite Tariffs and Geopolitical Turmoil

Source: Calafia Beach Pundit

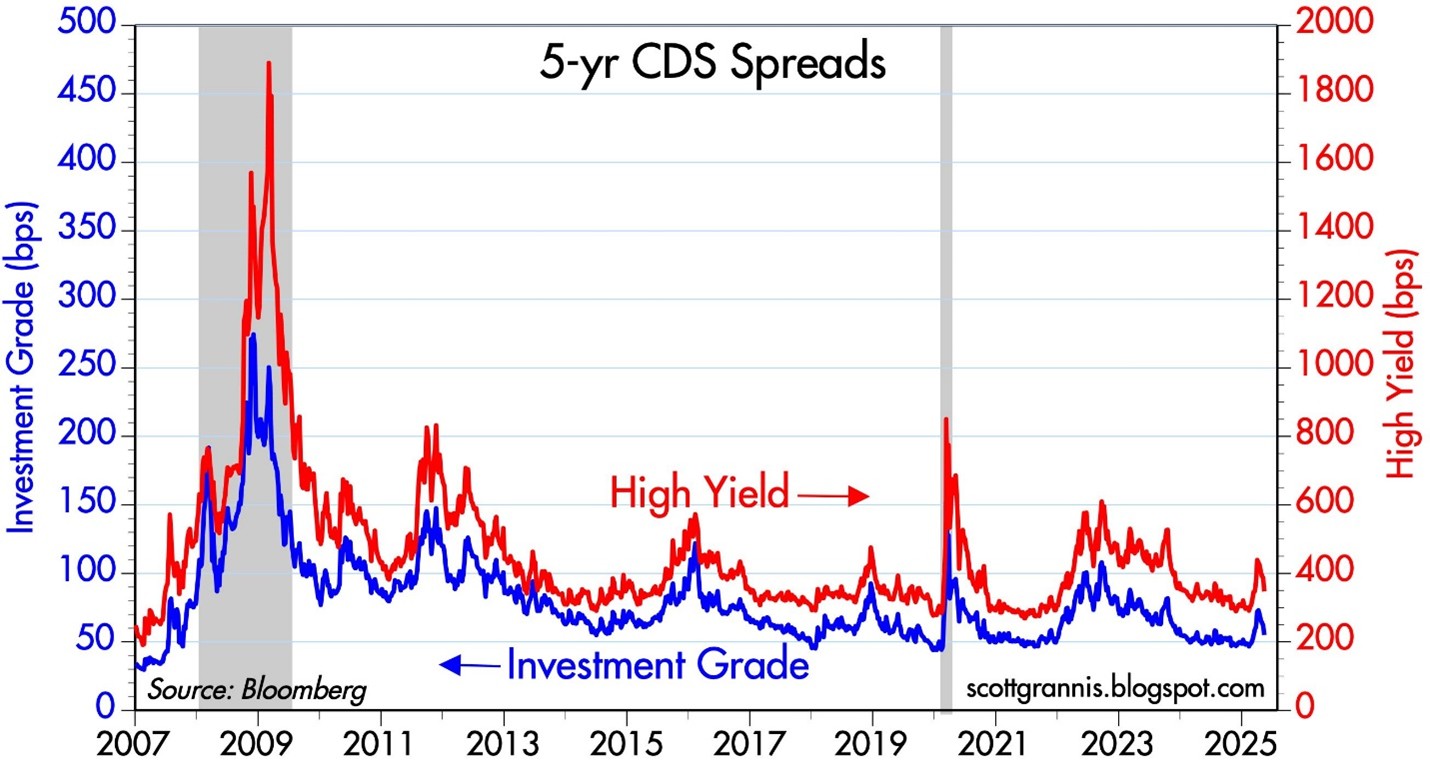

Credit Default Swaps (CDS) act as insurance contracts that protect investors against corporate debt defaults. During financial stress—like the 2008 crisis or the COVID crash in 2020—CDS prices surge as investors seek protection. Today, however, CDS prices are falling across both high-yield (junk bonds) and investment-grade (Blue Chip) debt. As seen in the chart above, the cost to insure corporate bonds has declined steadily over the past two years. This signals bond investors aren’t worried about a recession or a wave of defaults, despite tariff policy uncertainty, geopolitical risk, and modest GDP growth.

Inflation Tame as Tariffs Loom

President Trump has repeatedly criticized Fed Chair Jerome Powell for not cutting interest rates, calling him everything from a “dummy” to a “major loser” and a “stupid person” to a “numbskull”. While the name-calling is colorful, the economic pressure is real: U.S. GDP contracted -0.5% in Q1 2025. Powell, however, wants to see the full impact of upcoming tariffs before making a move. . A new tariff deadline looms on July 9th, and the market is anxiously awaiting clarity. But even if tariffs are implemented, many economists believe the inflationary impact will be temporary—what’s known as a one-time price shock.

Source: Calafia Beach Pundit

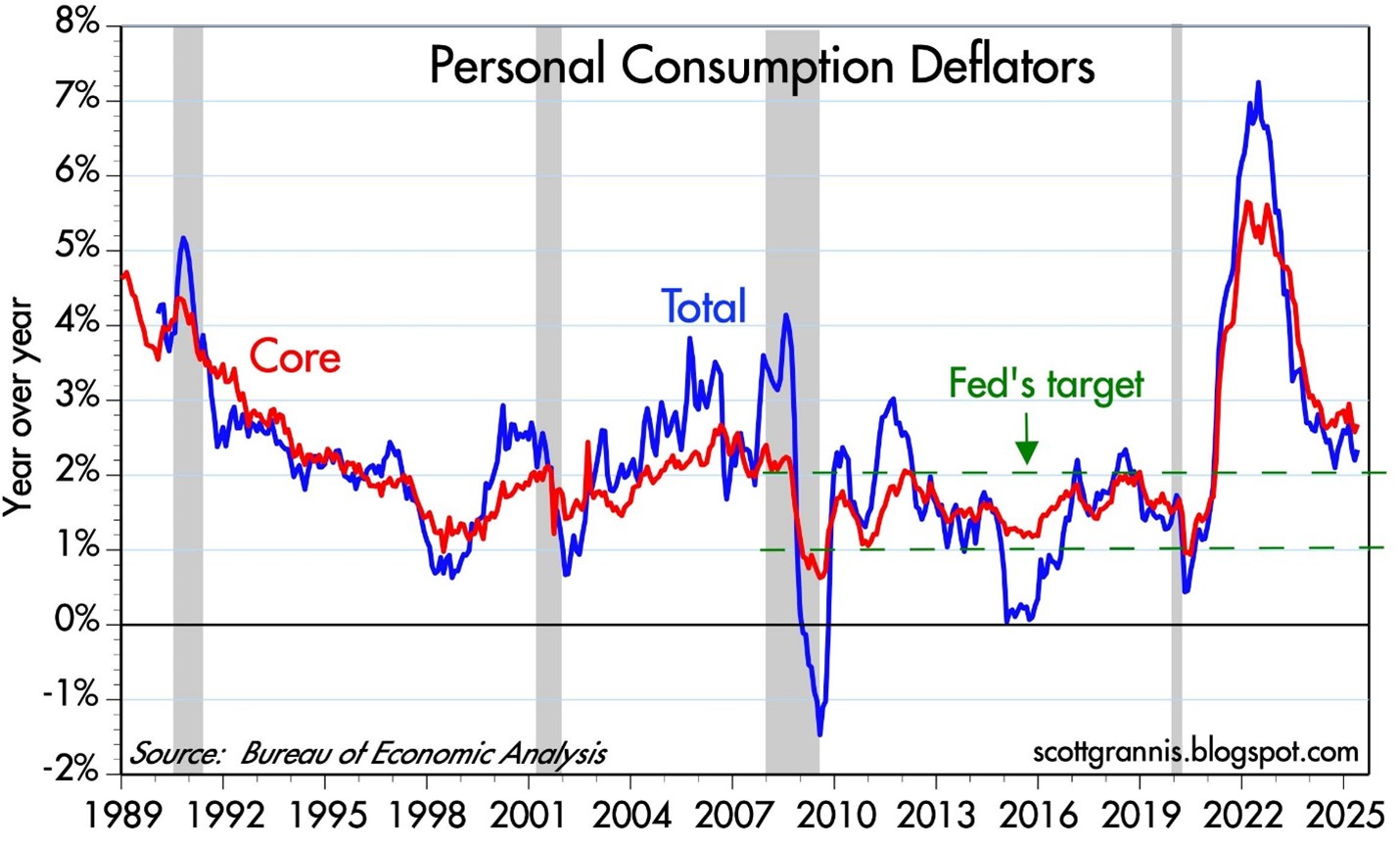

The Fed’s preferred inflation gauge—the Personal Consumption Expenditure (PCE) index—has been easing and is now near the 2% target (see chart above). With inflation cooling, Trump’s case for rate cuts gains credibility. Still, the Fed appears in no rush. It will take time to understand the lasting effects of the tariff rollout.

AI Wave Fueling Markets

For a generation, the semiconductor revolution has quietly powered innovation, guided by Moore’s Law—the principle that chip performance doubles roughly every two years (see my article The Traitorous 8). Sixty years after Gordon Moore wrote his seminal article, “Cramming More Components onto Integrated Circuits”, the power of software is catching up. NVIDIA’s Grace Blackwell GB200 chip contains an astronomical 208 billion transistors, supercharging AI software models like ChatGPT.

The AI revolution is fueling trillions in global investment and rapidly transforming industries – from data centers and self-driving cars to robotics and drug discovery. It’s important to realize that this AI arms race is not just occurring in the United States. AI investment spending extends way beyond Silicon Valley to countries like Saudi Arabia, Singapore, and China.

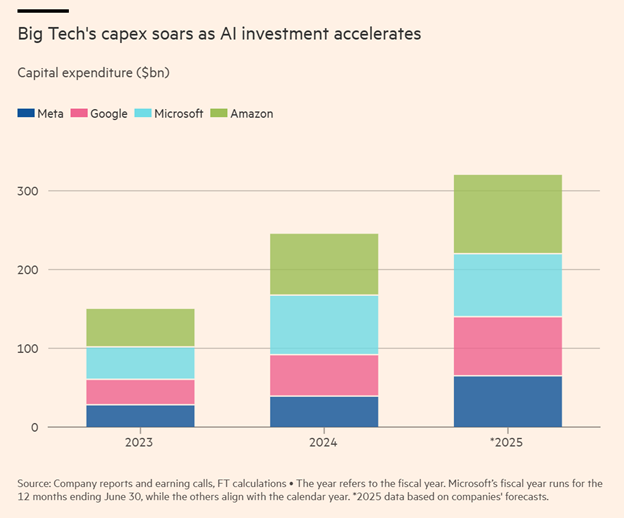

The AI boom is not a U.S.-only phenomenon. Countries like China, Saudi Arabia, and Singapore are pouring capital into AI, creating a global arms race in tech. In the U.S., the four biggest hyperscalers—Amazon, Microsoft, Google, and Meta—are projected to spend over $300 billion on capital expenditures in 2025 alone (see chart below).

To illustrate the scale: Amazon is forecasted to spend more than $100 billion in CapEx this year. For context, that’s 40% more than the company spent over the entire 2000–2020 period combined.

Source: The Financial Times

The Stargate Initiative: AI Infrastructure on a Galactic Scale

A prime example of the AI gold rush is the $500 billion Stargate initiative, with Phase 1 already underway in Abilene, Texas (see rendering below). The initial construction includes two buildings totaling 1,000,000 square feet. Ultimately, the full project will cove about 1,000 acres and be powered by an on-site natural gas facility generating 360 megawatts—enough to support 300,000 homes.

A huge portion of the project costs are dedicated to the budget for NVIDIA super chips. Oracle Corp. has committed $40 billion to purchase 400,000 of NVIDIA’s GB200 chips, making this project a centerpiece of the global AI infrastructure boom. Just this week, Oracle also announced a new $30 billion cloud deal, which will soak up a good chunk of the data center supply created by the database and enterprise software company.

Source: CoStar

The Big Picture: Volatility and Opportunity

There’s no shortage of risk—geopolitics, inflation, Fed uncertainty, tariffs. But the economy is showing surprising resilience. If tariff clarity improves, interest rate cuts materialize, and AI capital spending accelerates, a “boring” market could rapidly turn into a soaring one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Marathon Market Gets a Cramp

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2015). Subscribe on the right side of the page for the complete text.

“Anyone can run a hundred meters, it’s the next forty-two thousand and two hundred that count.”

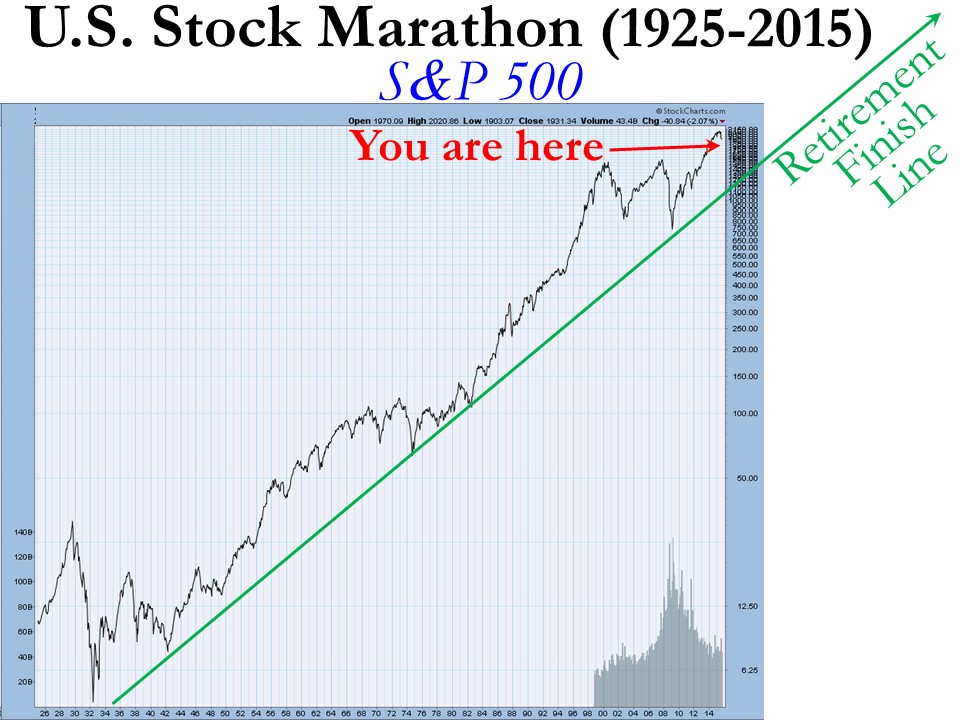

Investing is a lot like running a marathon…but it’s not a sprint to the retirement finish line. The satisfaction of achieving your long-term goal can be quite rewarding, but attaining ambitious objectives does not happen overnight. Along the hilly and winding course, there can be plenty of bumps and bruises mixed in with the elation of a runner’s high. While stocks have been running at a record pace in recent years, prices have cramped up recently as evidenced by the -2.6% decline of the S&P 500 stock index last month.

But the recent correction should be placed in the proper perspective as you approach and reach retirement. Since the end of the 2008 Financial Crisis the stock market has been racing ahead at a brisk rate, as you can see from the total return performance below (excluding 2015):

This performance is more indicative of a triumph than a catastrophe, but if you turned on the TV, listened to the radio, or surfed the web, you may come to a more frightening conclusion.

What’s behind the recent dip? These are some of the key concerns driving the recent price volatility:

- China: Slowing growth in China and collapse in Chinese stock market. China is suffering from a self-induced slowdown designed to mitigate corruption, prick the real estate bubble, and shift its export-driven economy to a more consumer-driven economy. These steps diminish short-term growth (albeit faster than U.S. growth), but nevertheless the measures should be constructive for longer-term growth.

- Interest Rates: Uncertainty surrounding the timing of a 0.25% target interest rate increase by the Federal Reserve. The move from 0% to 0.25% is like walking from the hardwood floor onto the rug…hardly noticeable. The inevitable move by the Fed has been widely communicated for months, and given where interest rates are today, the move will have a negligible impact on corporate borrowing costs. Like removing a Band-Aid, the initial action may cause some pain, but should be comfortably received shortly thereafter.

- Politics: Potential government shutdown / sequestration. The epic political saga will never end, however, as I highlighted in “Who Said Gridlock is Bad?,” political discourse in Washington has resulted in positive outcomes as it relates to our country’s fiscal situation (limited government spending and declining deficits). The government shutdown appears to have been averted for now, but it looks like we will be blanketed with brinkmanship nonsense again in a few months.

- Biotech/Pharmaceuticals: Politics over lofty drug prices and the potential impact of future regulation on the biotech sector. Given the current Congressional balance of power, any heavy-handed Democratic proposals is likely to face rigorous Republican opposition.

- Emerging Markets: Emerging market weakness, especially in Latin America (e.g., Brazil). These developments deserve close monitoring, but the growth in the three largest economic regions (U.S., Europe, and China) will have a much larger effect on the direction of global economic expansion.

- Middle East: Destabilized Middle East and Syria. Terrorist extremism and cultural animosity between various Middle East populations has existed for generations. There will be no silver bullet for a peaceful solution, so baby steps and containment are critical to maintain healthy global trade activity with minimal disruptions.

Worth noting, this current list of anxieties itemized above is completely different from six months ago (remember the Greece crisis?), and the list will change again six months into the future. Investing, like any competitive challenge, does not come easy…there is always something to worry about in the land of economics and geopolitics.

Here’s what the world’s top investor Warren Buffett said a few decades ago (1994) on the topic of politics and economics:

“We will continue to ignore political and economic forecasts which are an expensive distraction for investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.”

In a world of 7.3 billion people and 196 countries there will never be a shortage of fear, uncertainty, and doubt (F.U.D.) – see events chart in The Bungee Market. In an ever-increasing, globally connected world, technology and the media continually amplify molehills into mountains, thereby making the next imagined Armageddon a simple click of a mouse or swipe of a smartphone away.

Today’s concerns are valid but in the vast majority of cases the issues are completely overblown, sensationalized and over-emphasized without context. Context is an integral part to investing, but unfortunately context usually cannot be explained in a short soundbite or headline. On the flip side, F.U.D. thrives in the realm of soundbites and headlines.

While investors may feel fatigued from a strong flow of headline headwinds, financial market race participants should take a break at the water stop to also replenish themselves with a steady tailwind of positive factors, including the following:

- Employment: The unemployment rate has been cut from a recession peak of 10.0% down to 5.1%, and the economy has been adding roughly +200,000 new monthly jobs on a fairly consistent basis. On top of that, there are a record 5.8 million job openings versus 3.7 million two years ago – a sign that the economy continues to hum along.

- Housing/Commercial Real Estate/Mortgage Rates: Housing prices have rebounded by about +30% from the 2012 lows; Housing starts have increased by +25% in the past year and 120% in the past four years; and 30-Year Fixed mortgage interest rates sit at 3.85% – a highly stimulative level within a spitting distance from record lows.

- Auto Sales: Surged to a post-recession record of 17.8 million units in August.

- Interest Rates: Massively stimulative and near generational lows, even if the Fed hikes its interest rate target by 0.25% in October, December or sometime in 2016.

- Capital Goods Orders: Up for three consecutive months.

- Rail Shipments/Truck Tonnage: Both these metrics are rising by about 3-4%.

- Retail Sales: Rising at a very respectable pace of 7% over the last six months.

- Low Energy & Commodity Prices: Inflation has remained largely in check thanks to plummeting commodity prices. Low oil and gas prices are benefiting consumers in numerous ways, including the contribution to car sales, home sales, and/or debt reduction.

While the -10% dip in stock prices from mid-August might feel like a torn knee ligament, long-term investors know -10% corrections historically occur about one-time per year, on average. So, even though you may be begging for a wheelchair, the best course of action is to take a deep breath, stick to your long-term investment plan, rebalance your portfolio if necessary, and continue staying on course towards your financial finish line.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Who Gives a #*&$@%^?!

The stock market is just a big rigged casino, fueled by a reckless money printing Fed that is artificially inflating a global asset bubble, right? That seems to be the mentality of many investors as evidenced by the lack of meaningful domestic stock fund buying/inflows (see also Digesting Stock Gains). Underlying investor skepticism is a foundation of mistrust and detachment caused by the unprecedented 2008-09 financial crisis, when regulators fell asleep at the switch.

Making matters worse, the proliferation of the Internet, smart phones, and social media, has forced investors to digest a never-ending avalanche of breaking news headlines and fear mongering. Here is a partial list of the items currently frightening investors:

- Interest Rates: Will the Federal Reserve raise interest rates in June or September?

- Volatility: The Dow is up 200 points one day and then down 200 the next day. Keep me away.

- Greece: One day Greece is going to exit the eurozone and the next day it’s going to reach a deal with the IMF (International Monetary Fund) and European leaders.

- Terrorism / Middle East: ISIS is like a cancer taking over the Middle East, and it’s only a matter of time before they invade our home soil. And if ISIS doesn’t get us, then the Iranian boogeyman will attack us with their inevitable nuclear weapons.

- Inflation: The economy is slowing improving and as we approach full employment in the U.S., wage pressure is about to kick inflation into high gear. After falling significantly, oil prices are inching higher, which is also moving inflation in the wrong direction.

- Strong Dollar: Now that Europe is copying the U.S. by implementing quantitative easing, domestic exports are getting squeezed and revenue growth is slowing.

- Bubble? Stocks have had a monster run over the last six years, so we must be due for a crash…correct?

Seemingly, on a daily basis, some economist, strategist, analyst, or talking head pundit on TV articulately explains how the financial markets can fall off the face of the earth. Unfortunately, there is a problem with this type of analysis, if your evaluation is solely based upon listening to media outlets. Bottom line is you can always find a reason to sell your investments if you listen to the so-called experts. I made this precise point a few years ago when I highlighted the near tripling in stock prices despite the barrage of bad news (see also A Series of Unfortunate Events).

While I am certainly not asking anyone to blindly assume more risk, especially after such a large run-up in stock prices, I find it just as important to point out the following:

“Taking too much risk is as risky as not taking enough risk.”

In other words, driving 35 mph on the freeway may be more life threatening than driving 75 mph. In the world of investing, driving too slowly by putting all your savings in cash or low-yielding securities, as many Americans do, may feel safe. However this default strategy, which may feel comfortable for many, may actually make attaining your financial goals impossible.

At Sidoxia, we create customized Investment Policy Statements (IPS) for all our clients in an effort to optimize risk levels in a Goldilocks fashion…not too hot, and not too cold. Retirement is supposed to be relaxing and stress free. Do yourself a favor and create a disciplined and systematic investment plan. Being apathetic due to an infinite stream of worrisome sounding headlines may work in the short-run, but in the long-run it’s best to turn off the noise…unless of course you don’t give a &$#*@%^ and want to work as a greeter at Wal-Mart in your mid-80s.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

The Bunny Rabbit Market

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (April 1, 2015). Subscribe on the right side of the page for the complete text.

With spring now upon us, we can see the impact the Easter Bunny has had on financial markets…a lot of bouncing around. More specifically, stocks spent about 50% of the first quarter in negative territory, and 50% in positive territory. With interest rates gyrating around the 2% level for the benchmark 10-Year Treasury Note for most of 2015, the picture looked much the same. When all was said and done, after the first three months of the year, stocks as measured by the S&P 500 finished +0.4% and bonds closed up a similarly modest amount of +1.2%, as measured by the Total Bond Market ETF (BND).

Why all the volatility? The reasons are numerous, but guesswork of when the Federal Reserve will reverse course on its monetary policy and begin raising interest rates has been (and remains) a dark cloud over investment strategies for many short-term traders and speculators. In order to provide some historical perspective, the last time the Federal Reserve increased interest rates (Federal Funds rate) was almost nine years ago in June 2006. It’s important to remember, as this bull market enters its 7th consecutive year of its advance, there has been no shortage of useless, negative news headlines to keep investors guessing (see also a Series of Unfortunate Events). Over this period, ranging concerns have covered everything from “Flash Crashes” to “Arab Springs,” and “Ukraine” to “Ebola”.

Last month, the headline pessimism persisted. In the Middle East we witnessed a contentious re-election of Israeli Prime Minister Benjamin Netanyahu; Saudi Arabia led airstrikes against Iranian-backed, Shi’ite Muslim rebels (Houthis) in Yemen; controversial Iranian nuclear deal talks; and President Barack Obama directed airstrikes against ISIS fighters in the Iraqi city of Tikrit, while he simultaneously announced the slowing pace of troop withdrawals from Afghanistan.

Meanwhile in the global financial markets, investors and corporations continue to assess capital allocation decisions in light of generationally low interest rates, and a U.S. dollar that has appreciated in value by approximately +25% over the last year. In this low global growth and ultra-low interest rate environment (-0.12% on long-term Swiss bonds and 1.93% for U.S. bonds), what are corporations choosing to do with their trillions of dollars in cash? A picture is worth a thousand words, and in the case of companies in the S&P 500 club, share buybacks and dividends have been worth more than $900,000,000,000.00 over the last 12 months (see chart below).

Source: Financial Times

Case in point, Apple Inc (AAPL) has been the poster child for how companies are opportunistically boosting stock prices and profitability metrics (EPS – Earnings Per Share) by borrowing cheaply and returning cash to shareholders via stock buybacks and dividend payments. More specifically, even though Apple has been flooded with cash (about $178 billion currently in the bank), Apple decided to accept $1.35 billion in additional money from bond investors by issuing bonds in Switzerland. The cost to Apple was almost free – the majority of the money will be paid back at a mere rate of 0.28% until November 2024. What is Apple doing with all this extra cash? You guessed it…buying back $45 billion in stock and paying $11 billion in dividends, annually. No wonder the stock has sprung +62% over the last year. Apple may be a unique company, but corporate America is following their shareholder friendly buyback/dividend practices as evidenced by the chart below. By the way, don’t be surprised to hear about an increased dividend and share buyback plan from Apple this month.

Source: Investors Business Daily

Despite all the turmoil and negative headlines last month, the technology-heavy NASDAQ Composite index managed to temporarily cross the psychologically, all-important 5,000 threshold for the first time since the infamous tech-bubble burst in the year 2000, more than 15 years ago. The Dow Jones Industrial also cracked a numerically round threshold (18,000) last month, before settling down at 17,779 at month’s end.

While the S&P 500 and NASDAQ indexes have posted their impressive 9th consecutive quarter of gains, I don’t place a lot of faith in dubious, calendar-driven historical trends. With that said, as I eat jelly beans and hunt for Easter eggs this weekend, I will take some solace in knowing April has historically been the most positive month of the year as it relates to direction of stock prices (see chart below). Over the last 20 years, stocks have almost averaged a gain of +3% over this 30-day period. Perhaps investors are just in a better mood after paying their taxes?

Source: Bespoke

Even though April has historically been an outperforming month, banker and economist Robert Rubin stated it best, “Nothing is certain – except uncertainty.” We’ve had a bouncing “Bunny Market” so far in 2015, and chances are this pattern will persist. Rather than fret whether the Fed will raise interest rates 0.25% or agonize over a potential Greek exit (“Grexit”) from the EU, you would be better served by constructing an investment and savings plan to meet your long-term financial goals. That’s an eggstra-special idea that even the Easter Bunny would want to place in the basket.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including BND and AAPL (stock), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rebuilding after the Political & Economic Tsunami

Excerpt from Free April Sidoxia Monthly Newsletter (Subscribe on right-side of page)

The Start of the Arab Uprising

The Arab uprising grew its roots from an isolated and disgraced Tunisian fruit vendor (26- year-old Mohammed Bouazizi) who burned himself to death in protest of the persistent, deep-seeded corruption prevalent throughout the government (view excellent 60 Minutes story on Tunisia uprising). The horrific death ultimately led to the swift removal of Egypt’s 30-year President Hosni Mubarak, whose ejection was spurred by massive Facebook-organized protests. Technology has flattened the world and accelerated the sharing of powerful ideas, which has awoken Arab citizens to see the greener grass across other global democratic nations. Facebook, Twitter, and LinkedIn can be incredible black-holes of productivity destroyers (I know firsthand), but as recent events have proven, these social networking services, which handle about 1 billion users globally, can also serve valuable purposes.

As the flames of unrest have been fanned across the Middle East and Northern Africa, autocratic dictators haven’t had the luxury of idly sitting on their hands. Instead, these leaders have been pushed to relent to the citizens’ wishes by addressing previously taboo issues, such as human rights, corruption, and economic opportunity. These fresh events feel like new-found changes, but these major social tectonic shifts have been occurring throughout history, including our lifetimes (e.g., Tiananmen Square massacre and the fall of the Berlin Wall).

Good News or Bad News?

Recent headlines have created angst among the masses, and the uncertainty has investors asking a lot of questions. Besides radioactive concerns in both Japan and the Middle East (one actual, one figurative), the “worry list” of items continues to stack higher. Oil prices, inflation, the collapsing dollar, exploding deficits, a China bubble, foreclosures, unemployment, quantitative easing (QE2), mountainous debt, 2012 elections, and the end of the world among others, are worries crowding people’s brains. Incredibly, somehow the market still manages to grind higher. More specifically, the Dow Jones Industrial Average has climbed a very respectable +6.4% for 2011.

With the endless number of worries, how on earth could the major market indexes still advance, especially after a doubling in value from 24 months ago? For one, these political and economic shocks are nothing new. History has shown us that democratic, capitalistic markets ultimately move higher in the face of wars, assassinations, banking crises, currency crises, and various other stock market frauds and scandals. I’m willing to go out on a limb and say these worrisome events will continue this year, next year, and even over the next decade.

Most baby boomers living in the early 1980s remember when 30-year mortgage rates on homes reached 18.5%, inflation hit 14.8%, and the Federal Funds interest rate peaked near 20%. Boomers also survived Vietnam, Watergate, the Middle East oil embargo, Iranian hostage crisis, 1987 Black Monday, collapse of the S&L banks, the rise and fall of the Cold War, Gulf War I/II, yada, yada, yada. Despite all these cataclysmic events, from the last birth of the Baby Boomers (1964), the Dow Jones Industrial catapulted from about 890 to 12,320. This is no April Fool’s joke! The market has increased a whopping 14-fold (without dividends) in the face of all this gruesome news. You won’t find that story on the front-page of The Wall Street Journal.

Lost Decade Goes on Sale

The gains over the last four and half decades have been substantial, but much more is said about the recent “Lost Decade.” Although it has generally been a lousy decade for most investors in the stock market, eventually the stock market follows the direction of profits. What the popular press negates to mention is that S&P 500 operating earnings have more than doubled from about $47 in 1999 to an estimated $97 in 2011. Over the same period, the price of the market has been chopped by more than half (i.e., the Price – Earnings multiple has been cut from 29x to 13.5x). With stocks selling at greater than -50% off from 1999, no wonder smart investors like Warren Buffett are buying America – Buffett just spent $9 billion in cash on buying Lubrizol Corp (LZ). Retail investors absolutely loved stocks in 2000 at the peak, believing there was virtually no risk. Now the tables have been turned and while stock prices are trading at a -50% discount, retail investors are intensely skeptical and nervous about the prospects for stocks. Shoppers don’t usually wait for prices to go up 30% and then say, “Oh goody, prices are much higher now, so I think I will buy!” but that is what they are saying now.

I don’t want to oversell my enthusiasm, because the deals were dramatically better in March of 2009. Hindsight is 20-20, but at the nadir of the stock market, stock prices traded at bargain basement levels of 7x times 2011 earnings. We may not see opportunities like that again in our lifetime, so sitting in cash may not be the most advisable positioning.

Although I would argue every investor should have some exposure to equities, an investor’s time horizon, objectives, constraints and risk tolerance should be the key determinants of whether your investment portfolio should have 5% equity exposure or 95% exposure.

So while the economic and political dominoes may appear to be tumbling based on the news du jour, don’t let the headlines and the so-called media pundits scare you into paralysis. Bad news and tragedy will continue, but fortunately when it comes to prosperity, history is on our side. As you attempt to organize and pickup the financial pieces of the last few years, make sure you have a disciplined, long-term investment plan that adapts to changing market and personal conditions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in LZ, Facebook, Twitter, LinkedIn, BRKA/B, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Spreading the Seeds of Democracy

Excerpt from Free March Sidoxia Monthly Newsletter (Subscribe on right-side of page)

As we bathe ourselves in petroleum products, it is moments like these that highlight our deeply engrained addiction to oil. The flames of fundamental human rights, freedom, and democracy are spreading like wildfire throughout the Middle East and North Africa, and as a result, the cost of living and doing business has gone up. What started as a random plea by a Tunisian fruit merchant in response to insidious corruption (26 year old Mohammed Bouazizi burned himself to death in revolt to continuous crooked government bribes) has resulted in a broad wave of protesters removing two authoritarian, autocratic Arab leaders. Egyptian President Hosni Mubarak and Tunisian President Zine al-Abidine Ben Ali have been swiftly cast out by energized protesters, and other repressive leaders are likely bound to topple as well.

Who’s next and when? You’ll have to stay tuned, but Colonel Muammar Gaddafi, the Libyan leader, is on the short list. Leaders in Yemen, Bahrain, Jordan, and Algeria are among the other countries that are feeling the heat too. Even though Egypt, Libya, Tunisia, and other aforementioned countries remain relative oil lightweights, fear over a political contagion spreading to more substantive countries like Saudi Arabia has gotten speculators frothing at the mouth, which pushed oil prices above $100 per barrel and gasoline prices to an average of $3.37 per gallon (about $3.60 in California according to AAA motor club).

Source: FT.com - The U.S. population is a fraction of the size of China and India, but we continue guzzling dramatically more crude.

While the bloodshed on the streets has created fodder for great sensationalist headlines for the media outlets, the fact of the matter is that the spread of democracy is nothing new, and the innate desire for basic human rights has never died. Going back to 1900 the world housed about 10 practicing democracies, and today there are arguably more than 100 democratic (and quasi-democratic) countries (see blue line in chart below).

Source: The Financial Times.com

In the U.S., our standard of living has exploded for more than a generation. The internet – and applications like Facebook and Twitter – have flattened the planet and connected the rest of the world to the pleasures available to free, transparent, and open societies. As we have experienced firsthand in Iraq, however, regime changes and moves towards democracy can be messy and costly. Ultimately, the native populations must spearhead the drive toward democratic, political change. Regime change solely rammed through by the U.S. will only create temporary change, and with our fiscal wallets empty, we frankly cannot afford it (see Global Babysitter).

Embracing Alternatives

We didn’t run out of stones in the Stone Age, and we did not run out of steel in the Industrial Revolution. When it comes to oil, the same principle applies. As globalization accelerates the expansion of democratic, emerging middle classes around the world, other oil-rich countries, like Saudi Arabia, understand the havoc that $100-$125 dollar a barrel has on demand destruction. Just like a drug dealer does not want to scare its addicted users, so too oil producers do not want to price consumers out of the market with high prices. Oil may be the lubricant for global commerce, but unlike the empty promises offered by the Jimmy Carter era in the 1970s, technology advancements in the alternative energy industry have reached critical mass. If you don’t believe me, just take a gander at the $17 billion the Chinese are pouring into electric vehicle technology (see Electrifying Profits), or the 20% total energy mandate from renewable sources being instituted in Europe by 2020. Even if we choose to watch from the sidelines and pick our noses, our foreign competitors will wave with delight as they embrace alternative energy resources and race past us. Even if political turmoil temporarily worsens in the Middle East, any additional oil price increases will only make alternative energy resources more economical, and thereby accelerate adoption and make disciples of alternative energy less dependent on some of these oil-rich, corrupt regimes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}