Posts tagged ‘Michael Jordan’

Michael Jordan and Market Statistics

Basketball is in the air as the NBA playoffs are once again upon us. While growing up in high school, Michael Jordan was my basketball idol, and he dominated the sport globally at the highest level. I was a huge fanatic. Besides continually admiring my MJ poster-covered walls, I even customized my own limited edition Air Jordan basketball shoes by applying high school colors to them with model paint – I would not recommend this fashion experiment to others.

Eventually the laws of age, physics, and gravity took over, as Jordan slowly deteriorated physically into retirement. On an infinitesimally smaller level, I also experienced a similar effect during my 30s when playing in an old man’s recreational basketball league. Day-by-day, month-by-month, and year-by-year, I too got older and slower (tough to believe that’s possible) as I watched all the 20-somethings run circles around me – not to mention my playing time was slashed dramatically. Needless to say, I too was forced into retirement like Michael Jordan, but nobody retired my number, and I still have not been inducted into the Hall of Fame.

“Air Wade” Before Retirement: No Photoshop in 1988, just an optical illusion created by an 8-foot rim.

Financial markets are subject to similar laws of science (economics) too. The stock market and the economy get old and tired just like athletes, as evidenced by the cyclical nature of bear markets and recessions. Statistics are a beautiful thing when it comes to sports. Over the long run, numbers don’t lie about the performance of an athlete, just like statistics over the long run don’t lie about the financial markets. When points per game, shooting percentage, rebounds, assists, minutes played, and other measurements are all consistently moving south, then it’s safe to say fundamentals are weakening.

I’ve stated it many times in the past, and I’ll state it again, these are the most important factors to consider when contemplating the level and direction of the stock market (see also Don’t Be a Fool, Follow the Stool).

- Profits

- Interest Rates

- Valuations

- Sentiment

While the absolute levels of these indicators are important, the trend or direction of each factor is also very relevant. Let’s review these factors a little more closely.

- Profits: Profits and cash flows, generally speaking, are the lifeblood behind any investment and currently corporate profits are near record levels. When it comes to the S&P 500, the index is currently expected to generate a 2016 profit of $117.47. Considering a recent price closing of 2,092 on the index, this translates into a price-earnings ratio (P/E) of approximately 17.8x or a 5.6% earnings yield. This earnings yield can be compared to the 1.9% yield earned on the 10-Year Treasury Note, which is even lower than the 2.1% dividend yield on the S&P 500 (a rare historical occurrence). If history repeats itself, the 5.6% earnings yield on stocks should double to more than 10% over the next decade, however the yield on 10-year Treasuries stays flat at 1.9% over the next 10 years. The strong dollar and the implosion of the energy sector has put a lid on corporate profits over the last year, but emerging signs are beginning to show these trends reversing. Stabilizing profits near record levels should be a positive contributor to stocks, all else equal.

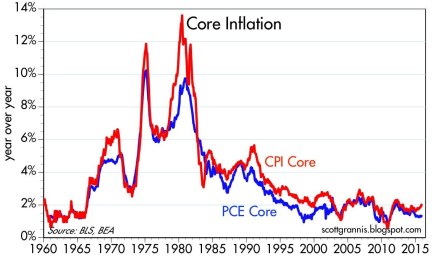

- Interest Rates: Pundits have been pointing to central banks as the sole reason for low/negative interest rates globally (see chart below). NEWS FLASH: Central banks have been increasing and decreasing interest rates for decades, but that hasn’t stopped the nearly unabated 36-year decline in interest rates and inflation (see chart below). As I described in previous articles (see Why 0% Rates?), technology, globalization, and the rise of emerging markets is having a much larger impact on interest rates/inflation than monetary policies. If central banks are so powerful, then why after eight years of loose global monetary policies hasn’t inflation accelerated yet? Regardless, all else equal, these historically low interest rates are horrible for savers, but wonderful for equity investors and borrowers.

Source: Calafia Beach Pundit

- Valuations: The price you pay for an investment is one of the, if not the, most important factors to consider. I touched upon valuations earlier when discussing profits, and based on history, there is plenty of evidence to support the position that valuations are near historic averages. Shiller CAPE bears have been erroneously screaming bloody murder over the last seven years as prices have tripled (see Shiller CAPE smells like BS). A more balanced consideration of valuation takes into account the record low interest rates/inflation (see The Rule of 20).

- Sentiment: There are an endless number of indicators measuring investor optimism vs. pessimism. Generally, most experienced investors understand these statistics operate as valuable contrarian indicators. In other words, as Warren Buffett says, it is best to “buy fear, and sell greed.” While I like to track anecdotal indicators of sentiment like magazine covers, I am a firm believer that actions speak louder than words. If you consider the post-crisis panic of dollars flowing into low yielding bonds – greater than $1 trillion more than stocks (see Chicken vs. Beef ) you will understand the fear and skepticism remaining in investors minds. The time to flee stocks is when everyone falls in love with them.

Readers of Michael Lewis’s book Moneyball understand the importance statistics can play in winning sports. Michael Jordan may not have been a statistician like Billy Beane, because he spent his professional career setting statistical records, not analyzing them. Unfortunately, my basketball career never led me to the NBA or Hall of Fame, but I still hope to continue winning in the financial markets by objectively following the all-important factors of profits, interest rates, valuations, and sentiment.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

ETF Slam Dunk: Mixing Jordan & Rodman

Players in the same game may use different strategies in the hunt for success. Take five-time NBA champ Dennis “The Worm” Rodman vs. Hall of Famer and fourteen-time All-Star Michael Jordan. Rodman’s bad-boy antics, tattoos, and loud hair colors more closely resemble the characteristics of a brash trader or quick-trigger hedge fund manager, which explains why Rodman played for five different NBA teams. Jordan on the other-hand was less impulsive, and like a long-term investor, held a longer term horizon with respect to team loyalty – he spent 13 seasons with one team (Chicago Bulls), excluding a brief, half-hearted return to the Washington Wizards. Despite their differences, they shared one common goal…the ambition to win.

In the investment world, traders and long-term investors in many cases could be even more different than Rodman and Jordan…just think Jim Cramer and Warren Buffett. But when it comes to the exploding trend of Exchange Traded Funds (ETFs) expansion, traders and investors of all types share the common appreciation for lower costs (management fees and trading commissions). Beyond the lower costs, ETFs also offer a wide and growing range of liquid exposures, regardless of whether a trader wants to hold the ETF for five hours or an investor wants to own it for five years. The benefits of low cost and liquidity, relative to traditional actively managed mutual funds, are two key reasons why this market has blossomed to $822 billion in size and is still strengthening at a healthy clip.

Source: SPDR

The flight to bonds and out of equities has been well documented (see chart below), but underneath the surface is a migrating investor trend out of active managers, and into lower cost vehicles for equity exposure (ETFs and Index Funds). The poster child beneficiary of this movement is the Vanguard Group (based in Valley Forge, Pennsylvania), which manages $1.4 trillion in fund assets, including $112 billion in ETFs (Bloomberg). Equity heavy fund management companies like Janus Capital Group Inc. (JNS) and T. Rowe Price Group Inc. (TROW) have felt the brunt of the pain from the disinterested investing public.

Source: Iacono Research

The migration away from expensive actively managed funds has created a cut-throat dog-fight for ETF market share. Competition has gotten so bad that discount brokerage firms like Fidelity Investments ($1.25 trillion in mutual fund assets) and Charles Schwab Corp. (SCHW) have begun offering free ETF trading. Just two days ago Schwab also purchased Windward Investment Management, Inc. (~$3.9 billion in assets under management), for $150 million in stock and cash.

At the end of the day, money goes where it is treated best. Irrespective of differences between long-term investors and short-term traders, the lower costs and improved liquidity associated with ETFs have shifted money away from more costly, actively traded mutual funds. At my firm, Sidoxia Capital Management, I choose to use a diversified hybrid approach via my Fusion investment products (Conservative, Moderate, and Aggressive). Fusion integrates low-cost, tax-efficient investment vehicles and strategies, including fixed income securities (including funds & ETFs), individual stocks, and equity ETFs. Regardless of the differing preferences of hair colors and tattoos, my bet is that Dennis Rodman and Michael Jordan could agree on the importance of two things…winning games and using ETFs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JNS, TROW, SCHW or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}