Posts tagged ‘mergers’

F.U.D. and Dividend Shock Absorbers

As the existential question remains open on whether Greece will remain a functioning entity within the eurozone, investor anxiety and manic behavior continues to be the norm. Rampant fear seems very counterintuitive for a stock market that has more than tripled in value from early 2009 with the S&P 500 index only sitting -3% below all-time record highs. Common sense would dictate that euphoric investor appetites have contributed to years of new record highs in the U.S. stock market, but that isn’t the case now. Rather, the enormous appreciation experienced in recent years can be better explained by the trillions of dollars directed towards buoyant share buybacks and mergers.

With a bull market still briskly running into its sixth year, where can we find the evidence for all this anxiety? Well, if you don’t believe all the nail biting concerns you hear from friends, family members, and co-workers about a Grexit (Greek exit from the euro), Chinese stock market bubble, Puerto Rico collapse, and/or impending Fed rate hike, then here are a few confirming data points.

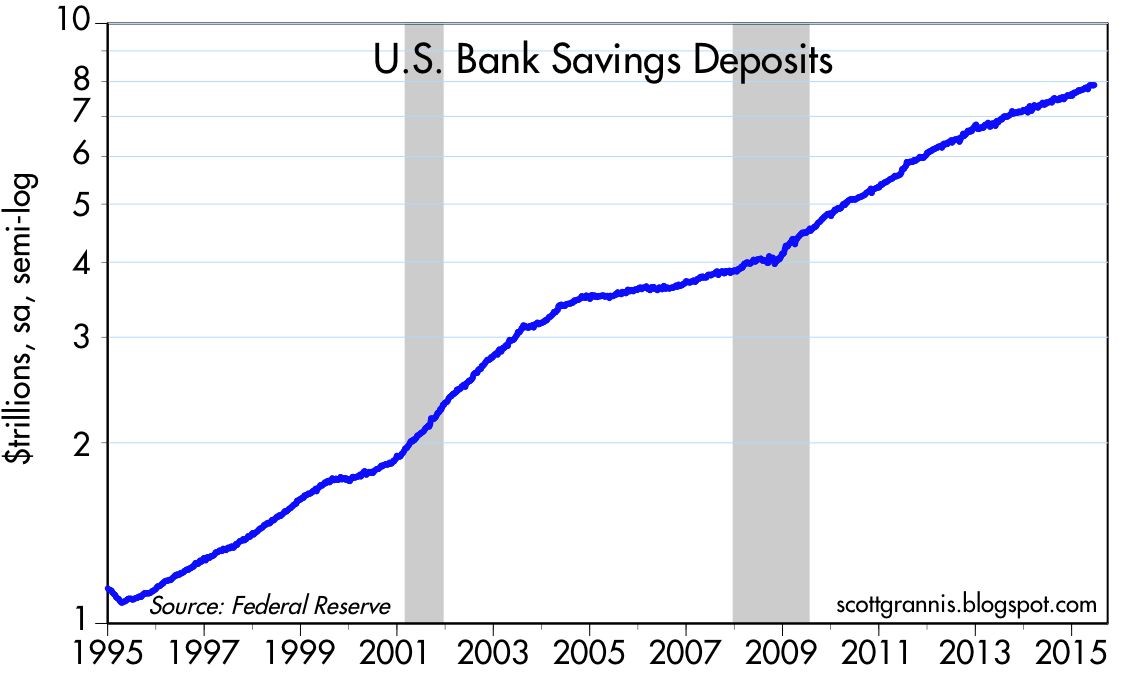

For starters, let’s take a look at the record $8 trillion of cash being stuffed under the mattress at near 0% rates in savings deposits (see chart below). The unbelievable 15% annual growth rate in cash hoarding since the turn of the century is even scarier once you consider the massive value destruction from the eroding impact of inflation and the colossal opportunity costs lost from gains and yields in alternative investments.

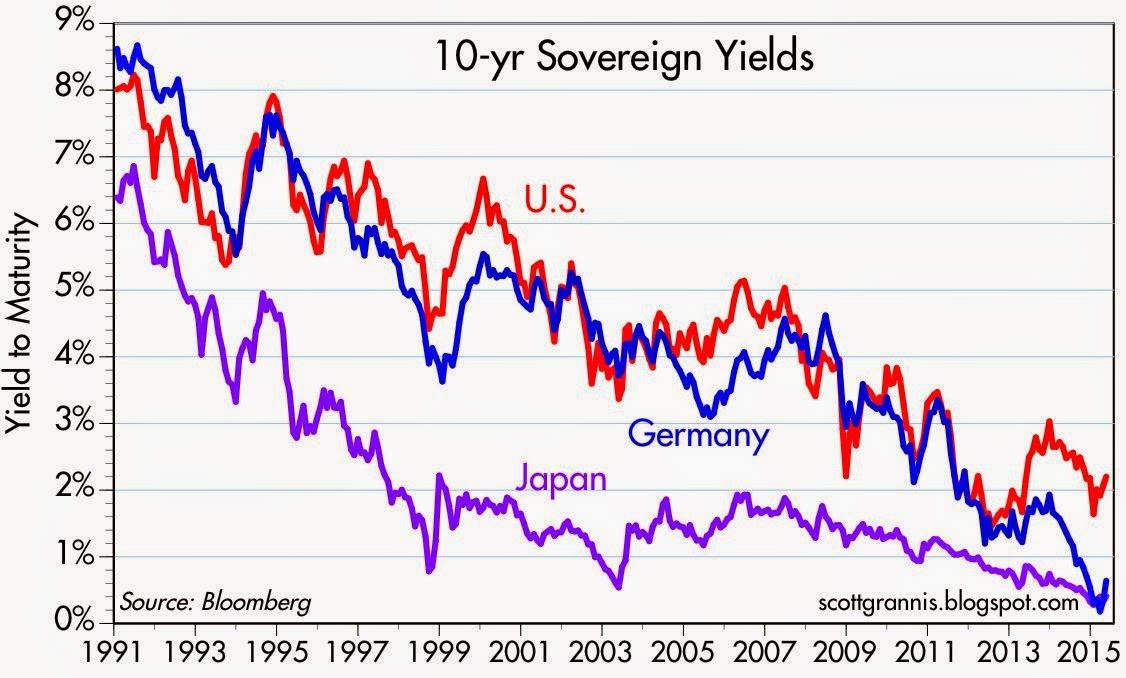

Next, you can witness the irrational risk averse behavior of investors piling into low (and negative) yielding bonds. Case in point are the 10-year yields in developing countries like Germany, Japan, and the U.S. (see chart below).

The 25-year downward trend in rates is a very scary development for yield-hungry investors. The picture doesn’t look much prettier once you realize the compensation for holding a 30-year bond (currently +3.2%) is only +0.8% more than holding the same Treasury bond for 10 years (now +2.4%). Yes, it is true that sluggish global growth and tame inflation is keeping a lid on interest rates, but these trends highlight once again that F.U.D. (fear, uncertainty, and doubt) has more to do with the perceived flight to safety and high bond prices (low bond yields).

In addition, the -$57 billion in outflows out of U.S. equity funds this year is further evidence that F.U.D. is out in full force. As I’ve noted on repeated occasions, when the tide turns on a sustained multi-year basis and investors dive head first into stocks, this will be proof that the bull market is long in the tooth and conservatism should be the default posture.

Dividend Shock Absorbers

There are always plenty of scary headlines that tempt investors to bail out of their investments. Today those alarming headlines span from Greece and China to Puerto Rico and the Federal Reserve. When the winds of fear, uncertainty, and doubt are fiercely swirling, it’s important to remember that any investment strategy should be constructed in a diversified manner that meshes with your time horizon and risk tolerance.

Consistent with maintaining a diversified portfolio, owning reliable dividend paying stocks is an important component of investment strategy, especially during volatile periods like we are experiencing currently. Sure, I still love to own high octane, non-dividend growth stocks in my personal and client portfolios, but owning stocks with a healthy stream of dividends serve as shock absorbers in bumpy markets with periodic surprise potholes.

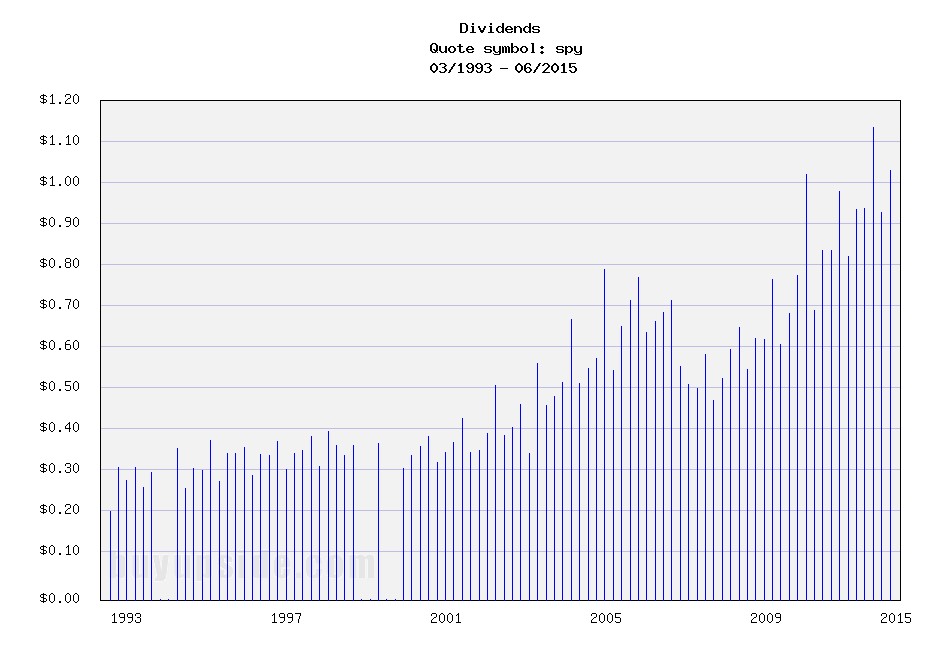

As I’ve note before, bond issuers don’t call up investors and raise periodic coupon payments out of the kindness of their hearts, but stock issuers can and do raise dividends (see chart below). Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500.

Source: BuyUpside.com

Markets will continue to move up and down on the news du jour, but dividends overall remain fairly steady. In the worst financial crisis in a generation, dividends dipped temporarily, but as I explain in a previous article (The Gift that Keeps on Giving), dividends have been on a fairly consistent 6% growth trajectory over the last two decades. With corporate dividend payout ratios well below long term historical averages of 50%, companies still have plenty of room to maintain (and grow) dividends – even if the economy and corporate profits slow.

Don’t succumb to all the F.U.D., and if you feel yourself beginning to fall into that trap, re-evaluate your portfolio to make sure your diversified portfolio has some shock absorbers in the form of dividend paying stocks. That way your portfolio can handle those unexpected financial potholes that repeatedly pop up.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

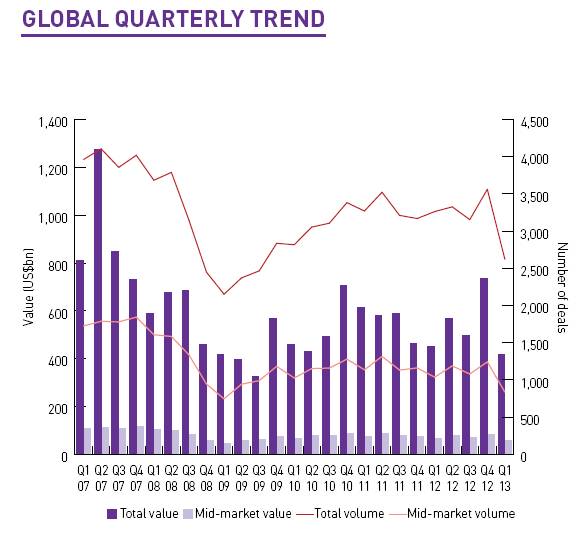

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

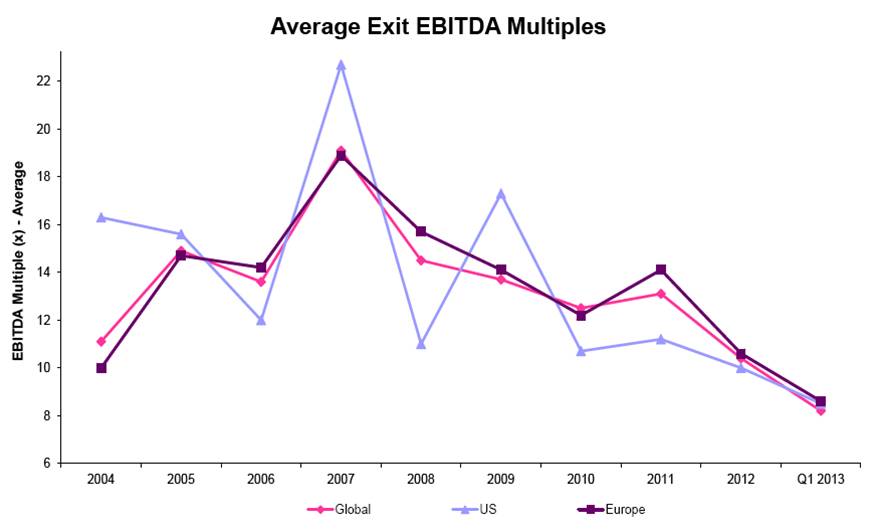

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Microsoft Enters Garbage Recycling Business

Microsoft Inc. (MSFT) is going green in more ways than one. Not only is Microsoft shelling out a lot of green ($8.5 billion) to acquire internet communication company Skype, but Microsoft is also going green by recycling Skype – an asset previously tossed away as garbage by eBay Inc. (EBAY). While I’m certain Microsoft executives did their due diligence and a large cadre of savvy bankers provided their stamp of approval on the deal, recycling a previously disposed item successfully poses some unique challenges.

The Problems

What could possibly go wrong in a sexy, strategic deal that plans to leverage Skype’s power of internet communication across Microsoft’s various businesses including mobile, business software, gaming, and advertising platforms?

- Sticker Shock: The Microsoft-Skype deal is still in its early phases, but the multi-billion price tag has already elicited heartburn from some investors (heart attacks among others). In Microsoft’s defense, what’s a mere $8.5 billion among friends, especially if your wallet is stuffed with over $60 billion in cash like Microsoft? With the 3-month Treasury bill currently yielding 0.02%, the massive wads of cash that Microsoft (and other tech giants) is sitting on appear to be burning a hole in buyers’ pockets. In a kooky internet world where IPO valuations of $70 billion for Facebook, $25 billion for Groupon, and $3 billion for LinkedIn are freely tossed around, an $8.5 billion Skype offer may seem like par for the course (or even a bargain). Sadly, however, I am having difficulty reconciling how Microsoft will take 663 million money-losing customers at Skype and balance the laws of economics by adding further volumes of money-losing customers. Apple Inc. (AAPL) spends about $2 billion per year in research & development, and is expected to produce more than $100 billion in revenues in fiscal 2011, while the $8.5 billion that Microsoft spent on Skype produced less than $1 billion in revenues last year. I presume Microsoft has some aggressive assumptions built into their Skype forecasts to rationalize the price paid for Skype.

- Failure Déjà Vu: Does the desire to integrate wiz-bang technology into existing product platforms sound familiar? It should – eBay Inc. (EBAY) already attempted and failed at integrating Skype before it threw in the white towel at the end of 2009 and sold a majority $1.9 billion stake of Skype shares back to a group of investors, including the Skype founders. Back in 2005, when eBay paid a then bargain of $3.1 billion for Skype (including earnouts), former CEO Meg Whitman evangelized the “Power of 3” (Skype + eBay’s Marketplace + PayPal) – I suppose new CEO John Donahoe must now promote the “Power of 2.” In Skype merger sequel of 2011, Microsoft’s CEO Steve Ballmer is espousing the benefits of Skype across Microsoft properties such as Outlook, Windows Live Messenger, Xbox, Kinect, and its newly created Nokia Corp. (NOK) relationship. Gaudy priced mergers in the internet/social media space have a way of eventually ending up in the deal graveyard. Consider AOL Inc.’s (AOL) 2008 deal with social network Bebo for $850 million – two years later AOL sold it for $10 million. News Corp’s (NWS) high profile purchase of MySpace for $580 million is reportedly looking for a new home at a fraction of the original price ($50 million). Hewlett-Packard Co.’s (HPQ) ostentatious $2.4 billion value (~125 x’s forward earnings) paid for 3Par Inc. during a bidding war with Dell Inc. (DELL) in 2010 is another recent example of a risky high-priced deal.

- Telco Carrier Skepticism: Although Microsoft has ambitions of taking over the world with Skype, the telecom service carrier companies that facilitate Skype traffic may feel differently. As the telcos spend billions to expand the global internet superhighway, if Skype is clogging traffic on their networks then the carriers will likely require additional compensation – no freeloaders allowed.

- Rocky Past Marriages: When it comes to acquisitions, Microsoft historically hasn’t fooled around as much as some other large Fortune 100 companies, nonetheless some important past relationships have gone sour. Take for instance Microsoft’s previous largest $6 billion cash acquisition of aQuantive Inc. in 2007. As Microsoft continues to chase Google Inc. (GOOG) at their heels, Microsoft has little to show for the aQuantive deal, except for a lot of employee turnover. The sizable but smaller $1.1 billion acquisition of Great Plains in 2001 has its critics too. Like Skype, the Great Plains business software deal made strategic sense, but six years after the units were fully integrated founder and owner Doug Burgum packed his bags and left Microsoft.

Consequences

What happens next for Microsoft? I know it’s difficult to imagine that Microsoft’s colossal underperformance since the beginning of 2010 could worsen – Microsoft has underperformed the market by a whopping -38% over that period – but by massively overpaying for Skype’s losses, Microsoft is not making their own job any easier. Although Microsoft has missed many key technology trends over the last few years (e.g., search, mobile, tablets, social media, etc.) and its stock has been in the dumps, the PC behemoth is looking to salvage a previously failed merger into a successful one. Time will tell if Microsoft can recycle a trashed, money losing operation into hefty green profits. If not, investors will be out for blood wondering why $8.5 billion was thrown away like garbage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG, but at the time of publishing SCM had no direct position in MSFT, Skype, EBAY, AOL, HPQ, DELL, NOK, Facebook, MySpace, LinkedIn, Groupon, Bebo, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Buffett on Gold Fondling and Elephant Hunting

Warren Buffett is kind enough to occasionally grace investors with his perspectives on a wide range of subjects. In his recently released annual letter to shareholders he covered everything from housing and leverage to liquidity and his optimistic outlook on America (read full letter here). Taking advice from the planet’s third wealthiest person (see rankings) is not a bad idea – just like getting basketball pointers from Hall of Famer Michael Jordan or football tips from Pro Bowler Tom Brady isn’t a bad idea either.

Besides being charitable with billions of his dollars, the “Oracle of Omaha” was charitable with his time, spending three hours on the CNBC set (a period equal to $12 million in Charlie Sheen dollars) answering questions, all at the expense of his usual money-making practice of reading through company annual reports and 10Qs.

Buffett’s interviews are always good for a few quotable treasures and he didn’t disappoint this time either with some “gold fondling” and “elephant hunting” quotes.

Buffett on Gold & Commodities

Buffett doesn’t hold back on his disdain for “fixed-dollar investments” and isn’t shy about his feelings for commodities when he says:

“The problem with commodities is that you are betting on what someone else would pay for them in six months. The commodity itself isn’t going to do anything for you….it is an entirely different game to buy a lump of something and hope that somebody else pays you more for that lump two years from now than it is to buy something that you expect to produce income for you over time.”

Here he equates gold demand to fear demand:

“Gold is a way of going long on fear, and it has been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money, but the gold itself doesn’t produce anything.”

Buffett goes on to say this about the giant gold cube:

“I will say this about gold. If you took all the gold in the world, it would roughly make a cube 67 feet on a side…Now for that same cube of gold, it would be worth at today’s market prices about $7 trillion dollars – that’s probably about a third of the value of all the stocks in the United States…For $7 trillion dollars…you could have all the farmland in the United States, you could have about seven Exxon Mobils (XOM), and you could have a trillion dollars of walking-around money…And if you offered me the choice of looking at some 67 foot cube of gold and looking at it all day, and you know me touching it and fondling it occasionally…Call me crazy, but I’ll take the farmland and the Exxon Mobils.”

Although not offered up in this particular interview, here is another classic quote by Buffett on gold:

“[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

For the most part I agree with Buffett on his gold commentary, but when he says commodities “don’t do anything for you,” I draw the line there. Many commodities, outside of gold, can do a lot for you. Steel is building skyscrapers, copper is wiring cities, uranium is fueling nuclear facilities, and corn is feeding the masses. Buffett believes in buying farms, but without the commodities harvested on that farm, the land would not be producing the income he so emphatically cherishes. Gold on the other hand, while providing some limited utility, has very few applications…other than looking shiny and pretty.

Buffett on Elephant Hunting

Another subject that Buffett addresses in his annual shareholder letter, and again in this interview, is his appetite to complete large “elephant” acquisitions. Since Berkshire Hathaway (BRKA/B) is so large now (total assets over $372 billion), it takes a sizeable elephant deal to be big enough to move the materiality needle for Berkshire.

“We’re looking for elephants. For one thing, there aren’t many elephants out there, and all the elephants don’t want to go in our zoo…It’s going to be rare that we are going find something selling in the tens of billions of dollars; where I understand the business; where the management wants to join up with Berkshire; where the price makes the deal feasible; but it will happen from time to time.”

Buffett’s target universe is actually fairly narrow, if you consider his estimate of about 50 targets that meet his true elephant definition. He has been quite open about the challenges of managing such a gigantic portfolio of assets. The ability to outperform the indexes becomes more difficult as the company swells because size becomes an impediment – “gravity always wins.”

With experience and age comes quote-ability, and Warren Buffett has no shortage in this skill department. The fact that Buffett’s investment track record is virtually untouchable is reason enough to hang upon his every word, but his uncanny aptitude to craft stories and analogies – such as gold fondling and elephant hunting – guarantees I will continue waiting with bated breath for his next sage nuggets of wisdom.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities) and commodity related equities, but at the time of publishing SCM had no direct position in BRKA/B, XOM or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

From Merger Wedding to eHarmony

Source: Photobucket

“Keep your eyes wide open before marriage, and half-shut afterwards.”

– Benjamin Franklin

Stocks share a lot of the same dynamics with dating and marriage. Some may choose to play the field through partnerships and joint ventures, while others may choose to remain independent as eternal bachelors/bachelorettes. Others, however, are willing to take the plunge. Unfortunately some marriages don’t last. But if things don’t work out, there is no need to worry because eHarmony.com (or resident investment bank) will always be there to help find your next perfect match.

Unlucky in Love

An example of a bloody divorce is the mega-merger between AOL Inc. and Time Warner (TWX) in 2000. The relationship was so destructive that investors witnessed AOL’s peak value of $222 billion in December 1999 (Fortune) plummet to around $3 billion today…ooooph!

Compared to some relationships, AOL lasted much longer. In fact Yahoo! Inc. (YHOO) didn’t even get to celebrate a honeymoon with Microsoft Corp. (MSFT) in February 2008 when the behemoth software company offered a +62% premium ($31 per share) for the gigantic portal. Microsoft’s $45 billion cash and stock offer was ruled unworthy by Yahoo’s board, so the company decided to leave Microsoft at the altar. Even after considering Yahoo’s latest price spike on acquisition rumors, Microsoft’s original bid is still almost double Yahoo’s current stock price of $16 per share.

Merger Scuttlebutt

As I discussed in my earlier mergers and acquisitions article (M&A) conditions are ripening with large corporate cash piles, a continued economic recovery, improved capital markets availability, and cheap credit costs (at least for those that qualify). With the clouds slowly lifting in the M&A world, suitors are shaking the trees for more potential opportunities.

While some acquirers may have altruistic intentions in combining companies, some marriages are done for pure gold-digging purposes. Private equity firms Blackstone Group (BX) and Silver Lake are rumored to be circling the Yahoo wagons and courting AOL as a potential partner in a joint bid. Whatever the expectations, if private equity plays a role in a Yahoo bid, the internet company should not become disillusioned with romantic warm and fuzzies – private equity firms like to get straight down to dirty business. Yahoo owns a 35% stake in Yahoo Japan and a 43% interest in leading Chinese e-commerce company, Alibaba Group. If a joint private equity bid were ever to win, I believe there would be a strong impetus to realize shareholder value by carving up these non-operating stakes. Consolidating overhead and streamlining expenses would likely be a top priority as well.

The Perfect Marriage

A “perfect marriage” could almost be called an oxymoron because like any relationship, there is significant work required by both parties. The divorce rate is estimated at around 40-50% in North America (Europe around the same), however mergers even fail at a higher 70% rate, according to Bain and Company study. I would argue successfully integrating larger deals are even more difficult, hampering the success rate even further. Merging two poorly managed companies purely for cost purposes is probably not the best way to go. Crashing two garbage trucks together is not going to create a Ferrari. I wouldn’t go as far as to say Yahoo and AOL are garbage trucks, but they face numerous, substantial challenges. Maybe these two companies are more akin to Mazdas transforming into a Toyota Camry (TM).

From my perspective, if companies really are dead set on engaging in acquisitions, then I urge management teams to focus on smaller digestible deals. Specifically, concentrate on those deals with experienced senior management teams who understand and respect the unique culture of the acquirer. Mergers also often fail due to excessive optimism and overly optimistic assumptions. This is an area in which Warren Buffett excels. Rarely do you observe the Oracle of Omaha overpaying for an acquisition, but rather he patiently waits for his fat pitch, and when it floats over the plate, Buffett is quick to throw out a lowball offer that will dramatically increase the probabilities of long-term merger success (think Geico, Sees Candy, Burlington Northern, etc.).

In the end, a joint relationship may not be forged between Yahoo, AOL and private equity firms, but if talks disintegrate, no need to worry – alternative partnerships can be explored on eHarmony.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in YHOO, MSFT, TWX, BX, BRKA, TM, Alibaba, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Winner’s Curse: HP’s Storage Prize

Congratulations HP (HPQ)…you are the proud winner of 3Par Inc. (PAR), a relatively small enterprise storage hardware and software company, for the bargain price of 125x’s 2011 earnings! Never mind that you were late to the game in your winning $2.4 billion bid against Dell Inc. (DELL), or that you paid more than triple the price ($33 per share) that 3Par was trading just 21 days ago (< $10 per share). At least you have a storage trophy you can show all your friends and you don’t have to carry around all those heavy bills anymore.

Winner’s Curse

In bidding wars and auctions, the victor of the price battle runs the risk of earning the “Winner’s Curse.” The curse falls upon those that bid a price that exceeds an auctioned asset’s intrinsic value. How can this occur? Well for one reason, the bidder may not have complete information regarding the value of the asset. Secondly, there can be emotional factors, or ego, that play a role in the decision and price paid. Lastly, unique factors, such as strategic benefits or synergies may exist that allow one bidder to offer a higher price than other auction participants. For example, consider an exploration and production company (XYZ Drilling Co.) that is bidding for drilling lease rights in Prudhoe Bay, Alaska. If XYZ Drilling Co. has unique existing drilling operations in the same area as the auctioned assets, XYZ Drilling Co. may be in a better position of making a profitable bid relative to its peers.

HP vs. Dell – A Deeper Look

Let’s take a deeper dive into the HP bid of 3Par. While HP generates a lot of cash by selling printers, cartridges, and computers, the company doesn’t exactly have a bullet-proof balance sheet. Unlike let’s say Apple Inc. (AAPL), which has about $46 billion in cash on its balance sheet with no debt (see Steve Jobs: Gluttonous Hog), HP actually carries more debt than cash (about $20 billion in debt and $15 billion in cash). What’s more, HP has little tangible equity, once $42 billion in goodwill and intangible assets are subtracted from the total asset value of the company – leaving HP with an astronomically high ratio of 275x’s price to tangible book value. For most companies operating with a positive net cash position, making acquisitions accretive is not that difficult in this current environment – when cash is decaying away with a paltry 1% return. Unfortunately for HP, their accretive hurdle is higher than a cash-rich company. Their weighted average cost of capital is ratcheted significantly higher due to a net debt position (not net cash).

Here is the viewpoint on the deal from Ashok Kumar, senior technology analyst at Rodman & Renshaw LLC:

“It’s in excess of $3 million per employee. To put it in perspective, today 3Par has about 5 percent [market share] of the very high-end market and for these premiums to pay out, [HP] would have to expand their market share to about 25 percent or about $1.5 billion, which is 5x the projected growth rate. And all of that would come at the expense of incumbents [like] IBM, EMC, Hitachi.”

On the Bright Side

Although the price paid by Hewlett-Packard for 3Par is ridiculously too high, this deal alone is not going to break HP’s piggybank. HP is currently raking in about $8 billion in cash flow per year, so absent aggressive share buybacks or other large acquisitions, HP should be able to pay off the cost of the deal in a few quarters. Secondarily, HP does gain some synergies by integrating 3Par’s blocklevel data storage expertise into HP’s existing portfolio of other storage technologies ( i.e., StoreOnce and IBRIX). Thirdly, HP gains some strategic defensive benefits by keeping 3Par out of Dell’s hands, a potentially formidable competitor in the storage space, given the intensive overlap in customer bases between HP & Dell. Lastly, HP will no doubt be able to introduce and cross-sell 3Par products into Hewlett’s vastly larger customer distribution channels and reap the resulting rewards.

All in all, the 3Par acquisition by HP makes perfect strategic sense, however the price paid will turn out to be a much better deal for 3Par shareholders, rather than HP shareholders. HP ultimately shelled out a hefty price tag to become the victorious party in the 3Par bidding war, but rather than increasing shareholder value, HP ended up achieving the “Winner’s Curse.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in HPQ, PAR, DELL, IBM, EMC, Hitachi, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Google: The Quiet Steamroller

As Google Inc. (GOOG) has proceeded to steamroll most of its competition on the global advertising roads, they are learning to tread a little more lightly in hopes of avoiding unneeded scrutiny. There are very few places to hide, when your company is on track to achieve more than $20 billion in annual sales and is valued at more than $175 billion in the marketplace.

As Google revenues continue to rise and they look to take over the world (including their position in China), they are enlisting others to assist them in Washington as well. Through three quarters of 2009, the company increased their lobbyist budget by 41% to approximately $3 million, according to the Associated Press (AP).

Google Eating Bite Sized Acquisitions

Ever since the controversy caused by Google’s $3.1 billion takeover of web advertising network company DoubleClick (2007 announcement), and the failed joint search agreement with Yahoo! (YHOO) in 2008 due to government and advertiser concerns, Google has decided to consume smaller bite-sized companies as part of its acquisition strategy. Over the last five months alone, Google has acquired eight different small companies (generally less than $50 million acquisition price), including the following: 1) Picknik (photo editing website); 2) reMail (mobile search applications); 3) Aardvark (social networking focus); and 4) AdMob ($750 million mobile advertising network deal). Eric Schmidt, Google CEO, has stated he would like to do one smaller-sized acquisition per month. Google management also believes they have lowered the inherent risk in these smaller deals because of legacy ties to target companies – all these sought after companies house former Google employees, says Bloomberg. In addition to remaining below the radar, the string of small deals act as a supplement to Google’s hiring practices, which can become challenging in a scarce qualified engineering hiring environment.

Microsoft Pot Calling Kettle Black

Microsoft (MSFT), the behemoth software giant with monopoly-like market share in the PC operating system market, is now fighting back against growing giant Google. This effectively amounts to the pot calling the kettle black, given Microsoft has already paid about $2.44 billion in fines to EU (European Union) relating to antitrust actions in the past 10 years, according to TechCrunch. Nonetheless, Microsoft CEO Steve Ballmer is not shy about throwing Google under the bus, stating Google is not playing fair in the search market. Furthermore, Microsoft has filed an antitrust complaint against Google in Europe as it relates to Ciao, an online shopping service powered by Microsoft, and cried foul over an agreement Google made with book publishers and authors on a separate project.

Google is not stupid. They have witnessed massive monopolistic companies like Microsoft and Intel (INTC) butt heads with regulators and pay billions in fines. Needless to say, Google will do everything in its power to avoid additional, unwanted oversight, while quietly driving their steamroller over the competition.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and GOOG, but at time of publishing had no direct position in MSFT, INTC, YHOO, or any other security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Measuring Profits & Losses (Income Statement)

So far we’ve conducted an introduction to financial statement analysis and a review of the balance sheet statement. Now we’re going to move onto the most popular and familiar financial statement and that is the income statement. One reason this particular financial statement is so popular is because it answers some of the most basic questions, such as, “How much stuff are you selling?” and “How much dough are you making?” With executive compensation incentives largely based off income statement profitability, it’s no surprise this statement is the one of choice. Unlike the balance sheet, which takes a snapshot picture of all your assets at a specific date in time, the income statement is like a scale, which measures gains or losses of a company over a specific period of time.

P&L Motivations

Like a wrestler or an overweight dieter, there can be an incentive to alter the calibration or lower the sensitivity of the financial weight scale. Fortunately for investors and other vested constituents, there are auditors (think of the Big 4 accounting firms) and regulators (such as the Securities and Exchange Commission) to verify the validity of the financial statement measurement systems in place. Sadly, due to organizational complexity, lack of resources, and lackadaisical oversight, the sanctity of the supervision process has been known to fail at times. One need not look any further than the now famous case of Enron. Not only did Enron eventually go bankrupt, but the dissolution of one of the most prestigious accounting firms in the world, Arthur Andersen, was also triggered by the accounting scandal.

Tearing Apart the Income Statement

Determining the profitability of a business through income statement analysis is generally not sufficient in coming to a decisive investment conclusion. Establishing the trend or the direction of profitability (or losses) can be even more important than the actual level of profits. The importance of profit trends requires adequate income statement history in order to ascertain a true direction. Comparability across time periods requires consistent application of rules going back in time. The “common form” income statement (or “percentage income statement”) is an excellent way to evaluate the levels of expenses and profits on an income statement across different periods. This particular format of historical income statement figures also provides a mode of comparing, contrasting, and benchmarking a company’s historical results with those of its peers (or the industry averages alone).

Shredding through the income statement, along with the other financial statements, often creates insufficient data necessary to make informed decisions. Other components of an annual report, such as the footnotes and Management Discussion and Analysis (MD&A) section, help paint a more complete picture. Interactions with company management teams and the investor relations departments can also be extremely influential forces. Regrettably, corporate viewpoints provided to investors are often skewed to an overly optimistic viewpoint. Management comments should be taken with a grain of salt, given the company’s inherent motivation to drive the stock price higher and portray the company in the most positive light.

Tricks of the Trade

One way to achieve profit goals is to improve revenues. If the traditional path to generating sales is unattainable, bending revenues in the desired direction can also be facilitated under the GAAP (Generally Accepted Accounting Principles) rules, or for those willing to risk times behind bars, criminals can attempt to bypass laws.

Due to the flexibility embedded within GAAP standards, corporate executives have a considerable amount of leeway in how the actual rules are implemented. Covering all the shenanigans surrounding income statement exploitation and distortion goes beyond the scope of this article, but nonetheless, here a few examples:

- Customer Credit: The relaxation of credit standards without increasing the associated credit loss reserves could have the effect of increasing short-term sales at the expense of future credit losses.

- Discounts: Offering discounts to accelerate sales is another accounting tactic. Offering price reductions may help sales now, but effectively this strategy merely brings future revenue into the current period at the expense of future sales..

- Adjusting Depreciation: Extending depreciation lives for the purpose of lowering expense and increasing profits may temporarily increase earnings but may distort the necessity of new capital equipment.

- Capitalization of Expenses: This practice essentially removes expenses from the income statement and buries them on the balance sheet.

- Merger Magic: Merger accounting can distort revenues and growth metrics in a manner that doesn’t accurately portray reality. Internally (or organic) growth typically earns a higher valuation relative to discretionary acquisition growth. Although mergers can optically accelerate revenue growth, acquirers usually overpay for deals and academic studies indicate the high failure rate among mergers.

Faux Earnings: Fix or Fraud?

The nature of financial reports has become more creative over time as new and innovative names for earnings have surfaced in press releases, which are not subject to GAAP guidelines. Reading terms such as “core earnings,” “non-GAAP earnings,” and “pro forma earnings” has become commonplace.

In addition, companies on occasion include GAAP approved “extraordinary” charges that are deemed rare and infrequent items. By doing so, income from continuing operations becomes inflated. More frequently, companies attempt to integrate less stringent, non-GAAP compliant, one-time so-called “nonrecurring,” “restructuring,” or “unusual” items. These “big-bath” expenses are designed to build a higher future earnings stream and divert investor attention to the earnings definition of choice. Unfortunately, for many companies, these nonrecurring items have a tendency of becoming recurring. Case in point is Procter & Gamble (PG), which in 2001 had recognized restructuring charges in seven consecutive quarters, totaling approximately $1.3 billion – recognizing these as part of ongoing earnings seems like a better choice. On the flip side, some companies want to include non-traditional gains into the main reported earnings. Take Coca-cola (KO) for example – in 1997 the Wall Street Journal highlighted Coke’s effort to include gains from the sales of bottler interests as part of normal operating earnings.

The review of the income statement plays a critical role in the overall health check of a company. From a stock analysis point, there tends to be an over-reliance on EPS (Earnings Per Share), which can be distorted by inflated revenues (“stuffing the channel”), deferral of expenses (extended depreciation), tax trickery, discretionary share buybacks, and other tactics discussed earlier. Generally speaking, the income statement is more easily manipulated than the cash flow statement, which will be discussed in a future post. Suffice it to say, it is in your best interest to make sure the income statement is properly calibrated when you perform your financial statement analysis.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing had no direct positions in PG, KO or other securities referenced. References to content in Financial Statement Analysis (Martin Fridson and Fernando Alvarez) was used also. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The China Vacuum, Sucking Up Assets

That's not Hoover making that sucking noise - it's China

Shhh, if you listen hard enough you can hear a faint sucking sound coming from the other side of the Pacific Ocean. In the midst of the greatest economic collapse since the Great Depression, China is rolling around the globe sucking up international assets as if it were a Hoover vacuum cleaner. As a member of the current account and budget surplus club, China is enjoying the membership privileges. Evidence is apparent in several forms.

Most recently, Chinese state oil and gas company, Sinopec (China Petrochemical Corporation) has bid close to $7 billion for Addax Petroleum, an oil explorer with significant energy assets in the Kurdistan region of northern Iraq.

Another deal, newly announced not too long ago, occurred on our own soil when another Chinese company (Sichuan Tengzhong Heavy Industrial Machinery Co.) made a bid for the ailing Hummer unit of bankrupt General Motors. Just as we have begun exporting our obesity to China through McDonald’s and KFC, now we are sharing our lovely gas guzzling habits.

In May, The Wall Street Journal reported the following:

Chinese companies and banks have also agreed to a string of credit and oil supply deals worth more than US$40 billion with countries such as Brazil, Russia and Kazakhstan, in line with efforts to secure its energy supply.

Beyond the oil markets, China is also hungry for other hard assets. The failed $20 billion investment in Chinalco (Aluminum Corporation of China) by Rio Tinto garnered a lot of press. But other deals are making headlines too. Metallurgical Corp. of China Ltd. (MCC) is planning a $5.15 billion thermal coal project in Queensland state, Australia in conjunction with Waratah Coal Pty Ltd. China has a voracious appetite for coal -its coal imports are estimated to surpass 50 million tons in 2009.

Cash is king, especially in crises like we are experiencing now, however we want to be careful that we don’t give away the farm out of desperation. Making tough decisions to preserve assets, like cutting expenditures and expenses, is a better strategy versus making fire sale disposals of crown jewels. Becoming energy independent and investing in environmentally sustaining technologies will serve our long term economic interests better as well.

If we’re not careful, that active Chinese Hoover vacuum cleaner is going to come over to our home turf and suck up more than just our loose change.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, RTP and was short MCD, but at the time of publishing SCM had no direct position in YUM, Sinopec (China Petrochemical Corporation), Addax Petroleum, Chinalco (Aluminum Corporation of China), Metallurgical Corp. of China Ltd. (MCC),Waratah Coal Pty Ltd or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}