Posts tagged ‘medicare’

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

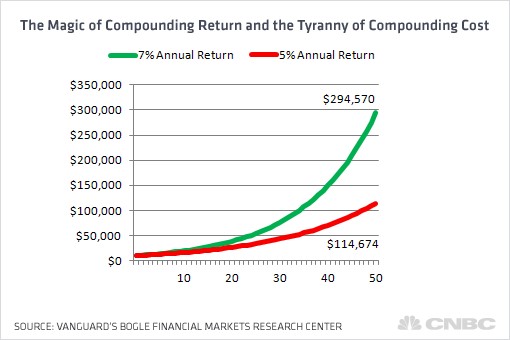

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

USA Inc.: Buy, Hold or Sell?

If the U.S. was a company, would you buy, hold, or sell the stock? A voluminous report put out last year by Mary Meeker sought to answer that very question. Since we’re in the thick of the presidential elections, why not review the important financial state of our great nation.

For those of you who may not know who she is, Mary Meeker is the well-known partner at Kleiner Perkins Caufield & Byers, who is also affectionately known as the “Queen of Internet.” Apparently, beyond her renowned expertise in analyzing and valuing tech companies and start-ups, she also has the knack of dissecting government statistics and distilling wonky numbers down to understandable terms for the masses. “Distilling” may be a generous term, given the massive size of her 460-page report, USA Inc., but nevertheless, I am going to attempt to synthesize this gargantuan report even further.

As a visual learner, I think some key cherry-picked slides from her report will help put our multi-trillion debts and deficits in context, so here goes…

The Scope of the Problem

If one spends a few hundred billion dollars here, and a few hundred billion dollars there, before you know it, a trillion dollars will have piled up. Currently our government has run $1 trillion+ budget deficits for three years, and the estimated deficit is for another trillion dollar deficit this fiscal year. If you have ever wondered how many football fields it takes to fill with a trillion dollars of cash, then today is your lucky day. The answer: 217 football fields.

Financial Statements: The Health Thermometer

In order to determine the relative health of USA Inc., Meeker created financial statements for our country, starting with the income statement. As you can see from the chart below, unfortunately USA Inc.’s expenses have been significantly larger than its revenues, creating a “discouraging” trend of negative cash flows (deficits). An entity that takes in $2.2 trillion in revenue and spends $3.5 trillion, cannot sustainably continue this trend for long, before significant financial problems arise. The largest contributing factor to our country’s losses (deficits) has been the exploding costs of entitlements, including Medicare, Medicaid, and Social Security.

As the pie chart shows, the major categories of entitlements comprise a whopping 58% of USA Inc.’s 2010 total expenditures.

Trillion dollar deficits have been the norm over the last three years.

Why Entitlement Spending is a Problem

Why are entitlements such a massive problem? The plain and simple answer to why entitlements are a major issue is that government expenditures are growing too fast. You can’t have expenses growing significantly faster than revenues for 45 years and expect to be in happy financial place.

Another reason for the abysmal spending record is due to politicians horrendous forecasting abilities. Future promises are made by politicians to garner votes today, and when they make overly rosy estimates about the costs of those promises, future generations are left holding the underfunded bag. Meeker points out that when Medicare was instituted in 1966, total future spending of $110 billion turned out to be about 10x more expensive (see chart below) than originally planned…ouch!

No Defense for Defense

Trillion dollar deficits and debts can’t be solely blamed on entitlements, but $700 billion in annual defense expenditures is not exactly chump change. The inopportune timing of the financial crisis in 2008-2009 didn’t help either, while two unfunded wars were being fought. Even if you strip out the wars, defense spending is still obscenely high. Given our poor state of financial affairs, we cannot afford to be the globe’s babysitter (see Impoverished Global Babysitter). Legacy Cold War spending on obsolete ground warfare needs to be reprioritized to 21st Century threats (i.e. focus on unmanned drones and coordinated intelligence). When a government spends more than the top 25 countries combined (see chart below), that country can certainly find some defense fat to trim.

Demographic Headwinds

The out-of-control gluttonous government spending is a threat to our national security, and although I wish I could say time alone will heal our fiscal wounds, unfortunately the opposite is true. Time is our enemy because the ticking demographic time bomb is about to explode, unless government acts to solve our spending problems. For starters, Americans are living longer, which means entitlement spending has accelerated faster than revenues collected, and life expectancy consistently continues to rise. As you can see below, life expectancy has outpaced Social Security age adjustments by +23% over a 74 year period.

Another self inflicted problem contributing to our colossal health care costs is the obesity epidemic. Over an 18 year period, the rate of obesity more than doubled to 32%. Individuals can and should shoulder more of the burden for these belt-busting costs, and government should spend more on prevention and education in this area. Bad drivers pay higher premiums for their auto insurance, so why not have bad eaters pay higher premiums? Genetics certainly can play a role in obesity, but so to do eating habits. The same accountability principle should be applied to smokers who overly burden our healthcare system too.

The USA spends more on healthcare than all OECD countries combined and 3x the OECD per capita average, yet as you can see from the chart below, the USA is not getting a life expectancy bang for its buck. The argument that the U.S. has the best healthcare in the world may be true in some instances, but the overall data doesn’t support that assertion.

The Rubber Hits the Road

The problem is easy to identify: Government spending going out the door is running faster than the revenues coming in via taxes. The solution is easy to identify too: Politicians need to cut spending, increase taxes, and/or do a combination of the two options. Like dieting, the solutions are easy to identify but difficult to execute.

Source: Calafia Beach Pundit – Scott Grannis

Almost everyone wants the government to spend less, but at the same time nobody wants their benefits cut. You can’t have your cake and eat it too. Citing two different studies, Meeker shows how 80% of Americans want a balanced budget as a national priority, but only 12% are willing to cut spending on Medicare and Social Security.

The rubber will hit the road in the next few months when politicians in a post-presidential election period will be forced to face these difficult “Fiscal Cliff” choices – $700 billion+ in tax hikes and spending increases that jeopardize the current recovery and our fiscal future.

Source: PIMCO

As market maven Mary Meeker recognizes, our fiscal situation is quite “discouraging”. With that said, although USA Inc. may have earned a current “Sell” rating, Meeker acknowledges that our country can become a positive turnaround situation. If voters actively push politicians to making difficult but necessary financial decisions to lower deficits and debt, investors around the globe will be ready to “Buy” USA Inc.’s stock.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Will the Fiscal Donkey Fly?

Source: TopPayingIdeas.com/blog

Will Barack Obama become a “one-termer” like somewhat recent Presidents, Democrat Jimmy Carter (1977-1981) and Republican George H.W. Bush #41 (1989-1993)? Or will Obama get the Democratic donkey off the ground like Bill Clinton managed to do after the 1994 mid-term election when Republican Newt Gingrich spearheaded the Contract with America, which led to a similar Republican majority in the House of Representatives. Clinton’s approval ratings were in the dumps at the time, comparable to voter’s current lackluster opinion of Obama and his spending spree (see also Profitless Healthcare).

Source: Gallup

Reagan Rebound

Similarly, Republican Ronald Reagan (1981-1989) was picking up the pieces with his lousy approval rating after the 1982 midterm election. Tax cuts, “trickle-down” supply side economics, and a tough stance on the Russian Cold War turned around the economy and his approval rating and catapulted him to reelection in a landslide victory. Reagan carried 49 states with the help of Reagan Democrats (one-quarter of registered Democrats voted for him).

Source: The Wall Street Journal

One should be clear though, popularity is not the only factor that plays into reelection success. George H. W. Bush had the highest average approval rating in five decades (60.9% approval), only superseded by John F. Kennedy (70.1% approval). The economy, international politics, and other external factors also play a large role in the reelection process.

Flying Donkey Time?

If President Obama wants to get the Democratic donkey off the ground and raise his current approval rating of 47% and remedy his self-admitted “shellacking” by the Republicans, then he will need to shift his hard-left political agenda more towards the middle, like Clinton did in 1994. If he leads on ideology alone, then the next two years will likely be a long tough slog for him and his Democratic colleagues.

In order to shift toward the center and gain more Independent voters, Obama will need to find common ground with Republicans and Tea-Partiers. Obama has already conceded in principle to extend the Bush tax cuts, but if he wants to gain more political capital, he will have to gain some ground in the area of fiscal responsibility. With the help of a strong economy, Clinton managed to run surpluses, but front and center today is a $1.3 trillion deficit and over $13 trillion in debt. The first step in building any credibility on the issue will come on December 1st when the president’s bi-partisan commission for deficit reduction will release its report.

It will be interesting which party will show leadership in making unpopular spending cuts, just as the 2012 re-election cycle just begins. The elephants in the room are the entitlements (Medicare and Social Security), and although less talked about, efficient cuts to defense spending should be put on the table. Sure, pork barrel spending, inefficient subsidies, tax loopholes, are gaps that need to be filled, but they alone are rounding errors given our country’s unsustainable current circumstances. Whether or not politicians (red or blue) will point out the unpopular elephants in the room will be interesting to watch.

Financial irresponsibility at the consumer and corporate level were major drivers behind the 2008-2009 financial crisis, and both individuals and businesses are responsibly adjusting their expense structures and balance sheets. Our government has to wake up to reality and adjust its expense structure and balance sheet too. Although foreign countries have reacted (i.e., European austerity), egotistical American politicians on both sides of the aisle haven’t quite woken up and smelled the coffee yet. Thank goodness for the democracy that we live in because citizens are pointing to the elephants in the room and demanding reckless spending and debt levels to come under control. If President Barack Obama doesn’t want to become another one-termer, he’ll have to move more to the center and get the finances of our country under control. If the stubborn donkey refuses to deal with reality and remains flightless, hopefully an elephant or ship-full of tea partiers can get this grass roots call for fiscal sanity off the ground.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ration or Tax: Eating Cake Not an Option

We live in an instant gratification society that would like everything for free ( like my pal Bill Maher), which explains why we want to have our healthcare cake and eat it too. I think George Will said it best when discussing universal healthcare coverage, “If you think health care is expensive now, just wait until it is free.” Look, I love free stuff too, like the rest of us, whether it’s free sausage sample at Costco (COST) or a breath mint at the Olive Garden (DRI). But regrettably, exploding deficits come at a price.

With midterm elections coming up, the issue of healthcare is once again front and center. The majority party feels like a checkbook is a solution to healthcare prosperity. Can you really look me in the eyes and say covering additional 32 million uninsured Americans is going to save us money. The government hasn’t exactly built a ton of credibility with the disastrous train-wreck we call Medicare, which is already carrying 45 million covered passengers.

The minority party hasn’t done a lot better with the layering of the 2006 unsustainable Medicare Part D drug plan. Conservatives are campaigning on “repeal and replace” and that is great, but where are the cuts?

There are only two solutions to our current healthcare problem: ration or tax (read Plucking Feathers of Taxpaying Geese). Is healthcare a right or privilege? I don’t know, but if we want to cover current obligations, or add 32 – 50 million more uninsured, then we will be required to cut expenses (ration) to pay for increased benefits and/or increase taxes to cover additional benefits. I would love to cover all Americans, along with the starving children in Africa too, but unfortunately we are limited by our resources. Writing checks with borrowed money will only last for so long.

How severe are the exploding healthcare costs, which are covering the graying of the 76 million baby boomers? Here’s how Forbes describes the unsustainable Medicare obligations:

The Medicare Trustees tell us that Medicare’s expected future obligations exceeded premiums and dedicated taxes by $89 trillion (measured in current dollars). No, that’s not a misprint. To put that number in perspective, Medicare’s liability is about 5 1/2 times the size of Social Security’s ($18 trillion) and about six times the size of the entire U.S. economy.

Not a pretty picture. These estimates look pretty far in the future, but even more bare bone figures arrive at a still frightening $33 trillion. Take a look at healthcare spending forecasts as a percentage of GDP – even the lowest estimates are depressing:

Source: National Center for Policy Analysis via Forbes

In our increasingly flat globalized world, competition between countries is becoming even more intense. We are in a marathon race for improved standards of living, and all these debts and deficits are dragging us down like an anchor tied to our legs. Even without considering other massive entitlements like Social Security, healthcare alone has the potential of grinding our economy to a halt. Politicians are great at promising more benefits and tax cuts in exchange for your votes, but true leadership requires delivering the sour medicine necessary for future prosperity. Before we eat the healthcare cake, let’s raise the money to buy the cake first.

Read more about the Medicare Explosion on Forbes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in COST, DRI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Securing Your Bacon and Oreo Future

Stuffing money under the mattress earning next to nothing (e.g., 1.3% on a on a 1-year CD or a whopping 1.59% on a 5-year Treasury Note) may feel secure and safe, but how protected is that mattress money, when you consider the inflation eating away at its purchasing power?

We’ve all been confronted by older friends and family members proudly claiming, “When I was your age, (“fill in XYZ product here”) cost me a nickel and today it costs $5,000!” Well guess what…you’re going to become that same curmudgeon, except 20 or 30 years from now, you’re going to replace the product that cost a “nickel” with a “$15 3-D movie,” “$200 pair of jeans” and “$15,000 family health plan.” Chances are these seemingly lofty priced products and services will look like screaming bargains in the years to come.

The inflation boogeyman has been relatively tame over the last three decades. Kudos goes to former Federal Reserve Chairman Paul Volcker, who tamed out-of-control double-digit inflation by increasing short-term interest rates to 20% and choking off the money supply. Despite, the Bernanke printing presses smoking from excess activity, money has been clogged up on the banks’ balance sheets. This phenomenon, coupled with the debt-induced excess capacity of our economy, has led to core inflation lingering around the low single-digit range. Some even believe we will follow in the foot-steps of Japanese deflation (see why we will not follow Japan’s Lost Decades).

The Essentials: Oreos and Bacon

Even if you believe movie, jeans, and healthcare won’t continue inflating at a rapid clip, I’m even more concerned about the critical essentials – for example, indispensable items like Oreos and bacon. Little did you probably know, but according to ProQuest’s Historic newspaper database, a package of Oreos has more than quadrupled in price over the last 30 years to over $4.00 per package – let’s just say I’m not looking forward to spending $16.00 a pop for these heavenly, synthetic, hockey-puck-like, creamy delights.

Beyond Oreos, another essential staple of my diet came under intense scrutiny during my analysis. I’ve perused many an uninspiring chart in my day, but I must admit I experienced a rush of adrenaline when I stumbled across a chart highlighting my favorite pork product. Unfortunately the chart delivered a disheartening message. For my fellow pork lovers, I was saddened to learn those greasy, charred slices of salty protein paradise (a.k.a. bacon strips), have about tripled in price over a similar timeframe as the Oreos. Let us pray we will not suffer the same outcome again.

Sliced Bacon Prices (per lb.) – Source (Bureau of Labor Statistics)

It’s Not Getting Any Easier

Volatility aside, investing has become more challenging than ever. However, efficiently investing your nest egg has never been more critical. Why has efficiently managing your investments become so vital? First off, let’s take a look at the entitlement picture. Not so rosy. I suppose there are some retirees that will skate by enjoying their fully allocated Social Security check and Medicare services, but for the rest of us chumps, those luxurious future entitlements are quickly turning to a mirage.

What the financial crisis, rating agency conflicts, Madoff scandal, Lehman Brothers bankruptcy, AIG collapse, Goldman Sachs hearings, FinReg legislation, etc. taught us is the structural financial system is flawed. The system favors institutions and penalizes the investor with fees, commissions, transactions costs, fine print, and layers of conflicts of interests. All is not lost however. For most investors, the money stuffed under the mattress earning nothing needs to be resourcefully put to work at higher returns in order to offset rising prices. Putting together a diversified, low-cost, tax-efficient portfolio with an investment management firm that invests on a fee-only basis (thereby limiting conflicts) will put you on a path of financial success to cover the imperative but escalating living expenses, including of course, Oreos and bacon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in KFT, GS, Lehman Brothers, AIG (however own derivative tied to insurance subsidary), or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Tips for Survival and Prosperity in Challenging Economic Times

Survival requires multiple strategies

We have all been impacted in some shape or form by the worst financial crisis experienced in a generation. The question now becomes what did we learn from this mess and how can we better prepare for a more prosperous financial future?

Here are some important tips to follow:

Save and Invest: Before paying others, pay yourself first. You can achieve this goal by saving and investing your money. Given the weak state of our government “safety net” programs, such as Medicare and Social Security, it has become more important than ever to save. Life spans are extending as well, meaning a larger “nest egg” is needed for retirement. If you don’t have the time, discipline, or emotional make-up to manage your own money, then seek out a fee-only advisor* who does not have a conflict of interest in regards to building your wealth.

Tighten Belt: In order to save and invest you need to be in a position where you are creating excess income. Cutting costs is one way to generate additional income. Eating out less, buying used, taking more affordable vacations, conserving energy, purchasing private label goods are a few easy ways to save money that will accumulate over time. If those efforts are still not adequate, one should then contemplate adjusting their living situation (i.e., down-size) or pursue additional income opportunities – either through a pay raise or higher paying job alternatives.

Pay Down Debt: If your credit card company is charging you a 15-20% rate on unpaid credit card balances and gouging you for late-fees and cash advances, then look for other sources of affordable financing. A home equity line of credit or second mortgage may make sense for some, if the fees and lower interest rates make economic sense. Contact a financial planner or tax professional to determine the appropriateness of these debt alternatives. Ultimately, the goal is to reduce debt and create more financial flexibility.

Take Free Money: If your employer offers matching payments to your retirement plan contributions, they are effectively offering you free money. Take it! The government offers you some tax deferral savings through IRA (Individual Retirement Account) contributions, so take advantage of that benefit as well.

Form a 6-Month Emergency Fund: The economy may be in a bottoming-out phase; however we are not out of the woods yet. Unemployment is approaching 10% and many companies and industries continue to struggle. Build a protective financial cushion should you or your family hit a bump in the road.

Invest in Yourself: Investing for retirement is crucial, however investing in yourself is just as, if not more, important than traditional investing. What I’m referring to is job training, education, and health awareness. We live in a globalized economy and in order to compete against those starving for our jobs, we need to improve our skills and education. Lastly, we cannot neglect our health. Finances need to be put in perspective. Our health should be a top priority and a disciplined balance between diet and exercise will not only reduce stress, but it will also improve mental health.

Times have been challenging, but when the going gets rough, the tough go saving. Take control of your financial future rather than letting economic circumstances control you. Financial success however should not come at the expense of your health, so also focus on a balanced program of diet and exercise. There are no free lunches in this world, but following these steps will help lead you on a path to prosperity – even in these challenging economic times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Wade W. Slome, CFA, CFP is President and Founder of Sidoxia Capital Management, LLC (www.Sidoxia.com), a fee-only Registered Investment Advisory firm headquartered in Newport Beach, California.

Maher Cheerleads No Profit Healthcare

Bill Maher, shock-comedian and host of Real Time with Bill Maher on HBO, has made up a new rule in a recent article, “Not Everything in America Has to Make a Profit.”

Hey Bill, that sounds intriguing. I’ve got an idea – how about you decide to work for no profit? If free healthcare is a right for every American, then why should people pay for your stupid jokes? If I have a right to free healthcare, then why not a right to free laughs?

Don’t get me wrong, our system is broke and needs to be fixed. The real question, is insuring an additional 50 million uninsured, by the same bureaucratic healthcare system leading the Medicare train-wreck, our best approach in solving our healthcare crisis? Sure, doing nothing should not be a fallback, but I’m not sure a trillion dollar healthcare plan with Washington bureaucrats is the best idea either? I’m not against government involvement, but before we dive headfirst into the deep-end with additional deficit exploding plans, why not wade in the shallow end and slowly roll-out success-based models that prove their superiority first.

I’m no medical expert, but let’s take the best structures, whether it’s the Mayo Clinic, Cleveland Clinic, or other leading structures and have the government manage a steady roll-out. If the government can prove a lower-cost, more efficient way of serving higher quality care, then by all means…let’s see it. Some argue we don’t have time to test new models, well unfortunately our disastrous system took decades to create and a pork-filled bill through Congress is not going to be an immediate silver-bullet for our dire healthcare problems.

Getting back to Mr. Maher’s profit objections on healthcare, I wonder if he’s ever complained or contemplated the innovations created by the profit-laden healthcare system. Whether it’s an MRI, hip replacement, cholesterol drug, cancer test, glaucoma treatment, ADHD medication or the hundreds of other beneficial advancements, maybe Mr. Maher should ask and understand where all these innovations came from? The answer: good old profits that were invested in critical research and development. Without those profits, there would be fewer and less impactful healthcare innovation for millions of Americans.

As for the firemen who do not “charge” or make a profit, I would like to remind Mr. Maher who is paying their fair share for those services consumed by hundreds of millions of Americans – it’s those same “soulless vampires making money off human pain” that you castigate. Profitable corporations are funding those essential government services with tax dollars derived from, you guessed it, profits. If we can find a lower-cost, more efficient way of serving the public services by the government, then as Phil Knight from Nike (NKE) says, “Just Do It!” Unfortunately, I prefer to see some tangible proof first, before spending hundreds of billions of tax dollars.

Healthy Incentives

From an early age, even as babies, we are incentivized for certain behavior. Whether it’s offering M&Ms to potty-train a two year old, or submitting six-figure bonuses to a fifty-two year old for hitting department profit targets, incentives always plays a central role in shaping behavior. Figure out the desired behavior and create incentives for your subjects (and penalties for non-compliance).

As the government comes up with a public solution, I have no problem with Washington pressuring insurance companies and the medical industry to become more efficient and provide a higher threshold of care. I’m confident that structures can be put in place that mitigate conflicts of interest (i.e., pure profit motive), while increasing the standard of care and efficiency. Rewarding the healthcare industry with incentives, rather than just simply beating them over the head with lower reimbursements under a single-payer system, may produce longer-lasting, sustainable benefits.

In certain areas of society, such as policemen/women, firefighters, national defense, and doctors there has always been a view that government is better suited for handling certain services. However, sometimes government does not implement the proper incentive plans, which then leads to bureaucracy, inefficiency, and excessive costs. Eventually, these negative trends overwhelm the system into failure, much like sand grinding engine gears to a halt.

Bill, I appreciate your viewpoint, and I like you would love if everything was free. For starters, I’ll look for your press release announcing the cancellation of your multi-million contract with HBO, closely followed by the revelation of your pro-bono comedy work. Here’s to profitless prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in NKE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Healthcare Reform: The Brutal Reality of Aging Demographics

The global population is aging and that is a bad trend for healthcare costs.

There’s no question healthcare reform is required. The Economist’s cover story, This is Going to Hurt, addresses this problem head-on:

“Even though one dollar in every six generated by the world’s richest economy is spent on health—almost twice the average for rich countries—infant mortality, life expectancy and survival-rates for heart attacks are all worse than the OECD average. Meanwhile, because health insurance is so expensive, nearly 50m Americans, an obscene number in such a rich place, have none; those that are insured pay through the nose for their cover, and often find it bankruptingly inadequate if they get seriously ill or injured.”

The real question is not whether we have a problem, but rather how are we going to approach it? Estimates of the current healthcare congressional plans put estimates for reform between $1.2 trillion and $1.6 trillion over 10 years. I tend to side with George Will when discussions center on costs, “If you think health care is expensive now, just wait until it is free.”

One of the reasons healthcare costs are exploding is because of our aging demographics. The 76 million “Baby Boomers” are entering their golden years, and as a result are consuming more healthcare products and services. Because our system is so convoluted and opaque, true healthcare competition cannot flourish. Rather, patients expect a cheap “all-you-can-eat” smorgasbord of services without consideration of cost. Unfortunately, the aging trend of our global population (especially in the developed countries like the U.S.) has put our economy on track for a disastrous train-wreck.

The Economist’s article, A Slow Burning Fuse, crystallizes the aging trend into proper perspective by providing some interesting statistics. At the beginning of the last century, in 1900, the average life expectance at birth was approximately 30. Today, the average life expectancy has more than doubled to 67 years (and 78 years in richer developed countries).

Read Full Economist Article, A Slow Burning Fuse

A second major cause of aging societies is the decline in number of children families are having. During the early 1970s, women on average were having 4.3 children each. Now the average is about 2.6 children (and 1.6 children in developed countries). What these statistics mean is that the taxable younger workforce is shrinking (growing slower), therefore unable to adequately feed the swelling appetites of the aging, healthcare-hungry global populations.

My solution would focus on the following:

Technology: Yes, chopping down trees, wasting years of our lives filling out and storing library-esque piles of medical forms is so 20th Century.

Consolidation of Insurers: And do we need dozens of different insurers on different billing platforms? Reducing inefficient and undercapitalized competitors down to a common technological digital record and billing platform makes common sense to me. Although I love competition, if I look at things like cell phones, cable, or even local grocery stores, there is a law of diminishing return whereby inefficiencies eventually outweigh benefits of competition.

Fewer Late Life Benefits: Nearly 30 percent of Medicare spending pays for care in the final year of patients’ lives, according to George Will. Does it really make sense to pay such a high proportion of costs for the last 1-2% of our lives? Other countries, including European ones, deny certain costly services for elderly patients. Does spending over $50,000 on certain cancer treatments for a few extra months of life seem equitable? If elderly ill patients are in the financial position to pay, then that’s great. Otherwise, at some point, the ethical question has to be faced – what is an extra month of human life worth?

Not really a rosy subject, but an important one. I’m confident we can solve these problems, if addressed immediately, or else future generations will be saddled with a more disastrous problem to heal.

Wade W. Slome, CFA, CFP® www.Sidoxia.com

Debt: The New Four-Letter Word

D-E-B-T, our country’s new four-letter word, used to be a fun toy the masses played and danced with to buy all kinds of goods and services. Debt was creatively utilized for all types of things, including, our super-sized McMansions purchased with Option ARM (Adjustable Rate Mortgage) Countrywide loans; our 0% financing car binges (thanks to now-bankrupt Chrysler and General Motors); and our no-payment-for-two-years, big screen plasma TVs (financed at now-bankrupt Circuit City). Eventually consumers, corporations, and governments realized excessive debt creates all kinds of lingering problems – especially in recessionary periods. We are by no means out of the woods yet, but consumers are now spending less than they are taking in, as evidenced by a positive and rising savings rate. This slowdown in spending is bad for short-term demand, but eventually these savings will be recycled into our economy leading to productive and innovative value creating jobs that will jumpstart the economy back on a path to sustainable growth.

Click Here For Excellent Article from the Peterson Foundation

In our hot-cold society, where the pendulum of greed and fear swing dramatically from one side to the next, we are also observing an unhealthy level of risk aversion by financial institutions. This excessive caution is unfortunately choking off the health of legitimate businesses that need capital/debt in order to survive. As we continue to see a pickup in the leading indicators for an economic recovery, banks should loosen up the credit purse strings to provide capital for profitable, growing businesses – even if there are hiccups along the way.

National Debt “Blob” Must Be Slowed

In the famous 1958 sci-fi horror film, “The Blob”, a gelatinous, ever-growing creature from outer space threatens to take over the town of Downingtown, Pennsylvania by methodically engulfing everything in its path. Steve McQueen eventually learns that freezing the Blob will halt its progression. In our country, entitlements, in the form of Medicare and Social Security, serve as our 21st century Blob. As the chart above shows, entitlements have expanded dramatically over the last 40 years and stand to expand faster, as the 76 million Baby Boomers reach retirement and demand more Social Security and Medicare benefits. Clearly the current path we are travelling on is not sustainable, and beyond breakthroughs in technology, the only way we can suitably address this problem is by cutting benefits or raising taxes. We only dug ourselves in a deeper financial hole with the enactment of Medicare Part D (prescription drug benefits for Medicare participants). I must admit I have great difficulty in understanding how we are going to expand health care coverage for the vast majority of Americans in the face of exploding deficits and debt burdens. I eagerly await specifics.

With an enlarging national debt burden and widening deficits, the U.S. is only becoming more reliant on foreign investors to finance our shortcomings. This trend too cannot last forever (see chart below). At some point, foreigners will either balk by not providing us the financing, or demanding prohibitively high interest rates on any funding we request – thereby negatively escalating our already high interest payment streams to bondholders.

Regardless of your political view, the problem pretty simply boils down to elementary school math. The government either needs to cut expenses or raise revenue (taxes or growth initiatives). Politically, the stimulative spending path is easier to rationalize, but as we see in California, eventually the game ends and tough cuts are forced to be made.

Regardless of your political view, the problem pretty simply boils down to elementary school math. The government either needs to cut expenses or raise revenue (taxes or growth initiatives). Politically, the stimulative spending path is easier to rationalize, but as we see in California, eventually the game ends and tough cuts are forced to be made.

Let’s hope the painful lessons learned from this financial crisis will steer us back on path to more responsible borrowing – a point where D-E-B-T is no longer considered a dirty four-letter word.

{kind=link}