Posts tagged ‘MArk Perry’

Why 0% Rates? Tech, Globalization & EM (Not QE)

Recently I have written about the head-scratching, never-ending, multi-decade decline in long-term interest rates (see chart below). Who should care? Well, just about anybody, if you bear in mind the structure of interests rates impacts the cost of borrowing on mortgages, credit cards, automobiles, corporate bonds, savings accounts, and practically every other financial instrument you can possibly think of. Simplistic conventional thinking explains the race to 0% global interest rates by the loose monetary Quantitative Easing (QE) policies of the Federal Reserve. But validating that line of thinking becomes more challenging once you consider QE ended months ago. What’s more, contrary to common belief, rates declined further rather than climb higher after QE’s completion.

Source: Calafia Beach Pundit

More specifically, if you look at rates during this same time last year, the yield on the 10-Year Treasury Note had more than doubled in the preceding 18 months to a level above 3.0%. The consensus view then was that the eventual wind-down of QE would only add gasoline to the fire, causing bond prices to decline and rates to extend an indefinite upwards march. Outside of bond guru Jeff Gundlach, and a small minority of prognosticators, the herd was largely wrong – as is usually the case. As we sit here today, the 10-Year Note currently yields a paltry 2.26%, which has led to the long-bond iShares 20-Year Treasury ETF (TLT) jumping +22% year-to-date (contrary to most expectations).

The American Ostrich

Like an ostrich sticking its head in the sand, us egocentric Americans tend to ignore details relating to others, especially if the analyzed data is occurring outside the borders of our own soil. Unbeknownst to many, here are some key country interest rates below U.S. yields:

- Switzerland: 0.33%

- Japan: 0.34%

- Germany: 0.60%

- Finland: 0.70%

- Austria: 0.75%

- France: 0.88%

- Denmark: 0.89%

- Sweden: 0.98%

- Ireland: 1.29%

- Spain: 1.69%

- Canada 1.80%

- U.K: 1.85%

- Italy: 1.93%

- U.S.: 2.26% (are our rates really that low?)

Outside of Japan, these listed countries are not implementing QE (i.e., “Quantitative Easing”) as did the United States. Rather than QE being the main driver behind the multi-decade secular decline in interest rates, there are other more important disinflationary forces at work driving interest rates lower.

Technology, Globalization, and Emerging Market Competition (T.G.E.M.)

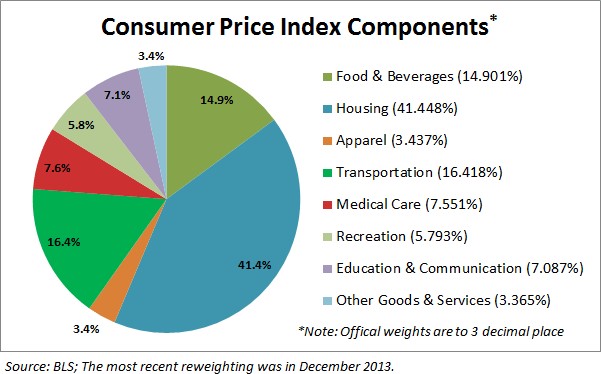

While tracking the endless monthly inflation statistics is a useful exercise to understand the tangible underlying pricing components of various industry segments (e.g., see 20 pages of CPI statistics), the larger and more important factors can be attributed to the somewhat more invisible elements of technology, globalization, and emerging market competition (T.G.E.M).

Starting with technology, to put these dynamics into perspective, consider the number of transistors, or the effective horsepower, on a semiconductor (a.k.a. computer “chip”) today. The overall impact on global standards of living is nothing short of astounding. Take an Intel chip for example – it had approximately 2,000 transistors in 1971. Today, semiconductors can cram over 10,000,000,000 (yes billions – 5 million times more) transistors onto a single semiconductor. Any individual can look no further than their smartphone to understand the profound implications this has not only on pricing in general, but society overall. To illustrate this point, I would direct you to a post highlighted by Professor Mark J. Perry, who observed the cost to duplicate an iPhone during 1991 would have been more than $3,500,000!

There are an infinite number of examples depicting how technology has accelerated the adoption of globalization. More recently, events such as the Arab Spring point out how Twitter (TWTR) displaced costly military engagement alternatives. The latest mega-Chinese IPO of Alibaba (BABA) was also emblematic of the hunger experienced in emerging markets to join the highly effective economic system of global capitalism.

I think New York Times journalist Tom Friedman said it best in his book, The World is Flat, when he made the following observations about the dynamics occurring in emerging markets:

“My mom told me to eat my dinner because there are starving children in China and India – I tell my kids to do their homework because Chinese and Indians are starving for their jobs”.

“France wants a 35 hour work week, India wants a 35 hour work day.”

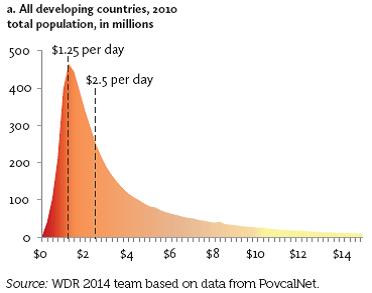

There may be a widening gap between rich and poor in the United States, but technology and globalization is narrowing the gap across the rest of the world. Consider nearly half of the world’s population (3 billion+ people) live in poverty, earning less than $2.50 a day (see chart below). Technology and globalization is allowing this emerging middle class climb the global economic ladder.

These impoverished individuals may not be imminently stealing our current jobs and driving general prices lower, but their children, and the countless educated millions in other international markets are striving for the same economic security and prosperity we have. The educated individuals in the emerging markets that have tasted capitalism are giving new meaning to the word “urgency”, which is only accelerating competition and global pricing pressures. It comes as no surprise to me that this generational migration from the poor to the middle class is putting a lid on inflation and interest rates around the world.

Declining costs of human labor from emerging markets however is not the only issue putting a ceiling on general prices. Robotics, an area in which Sidoxia holds significant investments, continues to be an area of fascination for me. With human labor accounting for the majority of business costs, it’s no wonder the C-suite is devoting more investment dollars towards automation. Rather than hire and train expensive workers, why not just buy a robot? This is not just happening in the U.S. – in fact the Chinese purchased more robots than Americans last year. And why not? An employer does not have to pay a robot overtime compensation; a robot never shows up late; robots never sue for discrimination or harassment; robots receive no healthcare or retirement benefits; and robots work 24 hours/day, 7 days/week, and 365 days/year.

While newspapers, bloggers, and talking heads like to point to the simplistic explanation of loose, irresponsible monetary policies of global central banks as the reason behind a four decade drop in interest rates that is only a small part of the story. Investors and policy makers alike should be paying closer attention to the factors of technology, globalization, and emerging market competition as the more impactful dynamics systematically driving down long term interest rates and inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including long positions in certain exchange traded fund positions and INTC (short position in TLT), but at the time of publishing SCM had no direct position in BABA, TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Magical Growth through Manufacturing Decline

In a data driven world, we can never get enough numbers. The market magicians and the media machines have no problem overhyping or overselling the importance of each pending data-point. With a quick economic sleight of hand, the industry pundits have converted the average investor into a frothing Pavlovian dog, begging for another market shaking statistic. One of the supposed earth-rattling data points is the monthly ISM Manufacturing Index figure, but the release of the ISM number alone isn’t enough for the audience. The real fun comes in determining whether the monthly number registers above or below a schizophrenic 50 level – a number above 50 indicates the manufacturing economy is generally expanding (August came in at 50.6).

The trick can often be surprising, but more surprising to me is the importance placed on this relatively small, disappearing segment of our economy. With the manufacturing sector now accounting for just 11-13% of GDP (see also Manufacturing – Losing Out?), shouldn’t we be focusing more on the “Services” sector of the economy, which accounts for roughly 75% of our country’s output, up from 62% in 1971 (source: Earthtrends). I believe economist Mark Perry at Carpe Diem captured this phenomenon best in his post from earlier this year (Decline of Manufacturing – The World is Much Better Off ):

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

Déjà Vu All Over Again

This isn’t the first time in our country’s history that we’ve experienced explosive economic growth as legacy segments of the economy decline in relative importance. Consider the share of jobs agriculture controlled in the early 1800s – a whopping 90% of jobs were tied to farms (see chart below). Today, that percentage is less than 2% in the wake of the U.S. becoming the 20th Century global superpower. History has taught us that technology can be a bitch on employment, as robots, machinery, processes, and chemistry replace the demand for human labor. As Perry points out, there is no doubt that “tractors, electricity, combines, the cotton gin, automatic milking machinery, computers, GPS, hybrid seeds, irrigation systems, herbicides, pesticides” replaced millions of farming jobs, but guess what…American ingenuity ruled the day. As it turns out, those economic resources freed up by technology and productivity were redeployed into new, expanding, job-fertile areas of the economy like, “manufacturing, health care, education, business, retail, computers, transportation, etc.”

Source: Carpe Diem

More Apples or More GMs?

The farming lobby still cries for its inefficient, growth-muffling subsidies today, but many unproductive, unionized domestic manufacturing industries are also screaming for government assistance because cheap foreign labor and new technologies are stealing manufacturing jobs by the boatloads. So at the core, the real question is do we want government and investments supporting more companies like Apple Inc. (AAPL) or more companies like General Motors Company (GM)?

As you may know, by flipping over an iPhone, any observer can clearly notice the product is “designed by Apple in California – assembled in China.” It is clear that Apple and its customers value brains over manufacturing brawn. At $371 billion and the most valuable publicly traded stock in the universe, Apple is dominating the electronics world, all the while hiring employees by the thousands. These facts beg the question of whether Apple should revamp their manufacturing supply-chain back to the U.S. to save more domestic jobs? Of course the result of a manufacturing strategy shift to a higher cost region would make Apple less competitive, force them to charge consumers higher prices for Apple products, and open the door for competitors to freely steal market share? Would this strategy create more incremental jobs, or fewer jobs? I think I’ll side with the Steve Jobs philosophy of business, which says “more profitable businesses must fill more job openings.”

If this Apple case study isn’t illustrative enough for you, maybe you should take a look at companies like GM. The U.S. automobile industry has historically been notoriously mismanaged, thanks to a horrific manufacturing cost structure, anchored by unsustainable pension and healthcare costs. Should investors be surprised that an uncompetitive, bloated cost structure leaves companies like GM less money to invest in new products and innovation? This irrational cost management contributed to decades of market share losses to foreigners. If I’m the job creation czar in the U.S., I think I’ll choose the Apple path to job creation over GM’s route.

Global Competitiveness = Jobs

With a 9.1% unemployment rate and the recent introduction of the American Jobs Act, there has been plenty of emphasis and focus on job creation. At the end of the day, what will create durable, long-term job creation is innovative, competitively priced products and services that can be sold domestically and abroad. How do we achieve this goal? We need an education system that can teach and train a workforce sufficiently to meet the discerning tastes of a global marketplace. Government, on the other hand, needs to support (not direct) the private sector by investing in strategic areas to help global competitiveness (i.e., education, energy independence, basic research, infrastructure, entrepreneurial capital for business formation, etc.), while facilitating a business environment that incentivizes growth.

Regardless of the policy mixtures, the common denominator needs to be focused on improving global competitiveness. Excessive focus on a declining manufacturing sector and the monthly ISM data will only distract decision makers from the core issues. If the economic magician’s sleight of hand diverts investor attention for too long, we may see more jobs disappear.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and AAPL, but at the time of publishing SCM had no direct position in GM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

Living Large – Technology Revolution Raises Tide

It’s hard to believe that my kids will never truly know what it is was like to live without a microwave, VCR, GPS device, internet connection or many of the other modern day inventions. In my elementary school days, when I had to write a report about Alfred Hitchcock, I was forced to drag my mom to the public library, chase down some librarians, and comb through floors of book shelves, only to find the book I needed was already checked-out. Today, it’s amazing to watch my kid, barely old enough to pull the milk container out of the fridge, scamper over to the computer, type in a few search words on Google (GOOG) and access an endless pool of information for a homework assignment. Fortunately for my wife and me, my daughter has not discovered Facebook yet.

Rising Tide Lifts All

In the uncertain times we live in, many people lose sight of the incredible advancements achieved over our generation, and ignore the difficult challenges and problems entrepreneurs are solving today. And many of these advancements have trickled down to wide swaths of the population. The minimum wage worker, cleaning dishes at the local restaurant, may not be able to afford the new $500 iPad from Apple Inc. (AAPL), but technology advancements have benefited the less privileged in different ways. For example, similar computing power used in the iPad has also been used in the logistics and sourcing departments of retail chains like Family Dollar (FDO), thereby making goods cheaper for lower-income consumers.

One person who has not lost sight of these advancements of productivity is Mark J. Perry of the Enterprise Blog. In a recent article, Perry compares what a consumer working 152 hours in 1964, earning an average wage, could purchase versus an average consumer today (46 years later) working the same 152 hours. Beyond the average wage of $2.50 per hour increasing to $19 per hour, Perry shows the unbelievable increase in the quality and number of products.

Perry places the continuing technological revolution in context by stating:

“Americans today can purchase low-priced electronics products that even a billionaire in the past wouldn’t have been able to buy.”

Another person that knows a little about technology, Sergey Brin (Co-Founder of Google Inc.), put recent technology advancements in perspective in the company’s 2008 annual report:

“Our first major purchase when we started Google was an array of disk drives that we spent a good fraction of our life savings on and took several car trips to carry. Today, I walked out of a store with a small box in my hand that stores more than all those drives and cost about $100. Similarly, the processors available today are about 100 times as powerful as those we used in 1998.”

Advancements in our standard of living are not only limited to electronic gadgets and internet searches, but also tangible benefits continue to be realized in the most important elements of our human survival. A picture says a thousand words, and these charts speak volumes about our standard of living:

Lives are Extending and Food More Affordable

Obviously, everything is not a bed of roses and some of these improvements have come at a cost. Our country has lost millions of jobs over the last few years, and globalization has significantly increased foreign competition in broad areas of our economy. But before you succumb to the devastation rhetoric of the nay-sayers, please do not forget about the almost imperceptible rising tide of technological innovations that are allowing us to live better lives, even in uncertain times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct positions in RSH, FDO, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}