Posts tagged ‘Mario Draghi’

Draghi Provides Markets QE Beer Goggles

While the financial market party has been gaining momentum in the U.S., Europe has been busy attending an economic funeral. Mario Draghi, the European Central Bank President is trying to reverse the somber deflationary mood, and therefore has sent out $1.1 trillion euros worth of quantitative easing (QE) invitations to investors with the hope of getting the eurozone party started.

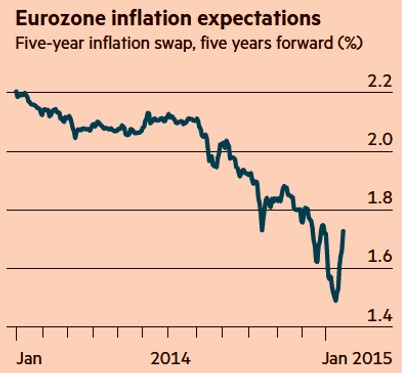

Draghi and the stubborn party-poopers sitting on the sidelines have continually been skeptical of the creative monetary punch-spiking policies initially implemented by U.S. Federal Reserve Chairman Ben Bernanke (and continued by his fellow dovish successor Janet Yellen). With the sluggish deflationary European pity party (see FT chart below) persisting for the last six years, investors are in dire need for a new tool to lighten up the dead party and Draghi has obliged with the solution…“QE beer goggles.” For those not familiar with the term “beer goggles,” these are the vision devices that people put on to make a party more enjoyable with the help of excessive consumption of beer, alcohol, or in this case, QE.

Source: The Financial Times

Although here in the U.S. “QE beer goggles” have been removed via QE expiration last year, nevertheless the party has endured for six consecutive years. Even an economy posting such figures as an 11-year high in GDP growth (+5.0%); declining unemployment (5.6% from a cycle peak of 10.0%); and stimulative effects from declining oil/commodity prices have not resulted in the cops coming to break up the party. It’s difficult for a U.S. investor to admit an accelerating economy; improving job additions; recovering housing market; with stronger consumer balance sheet would cause U.S. 10-Year Treasury Note yields to plummet from 3.04% at the beginning of 2014 to 1.82% today. But in reality, this is exactly what happened.

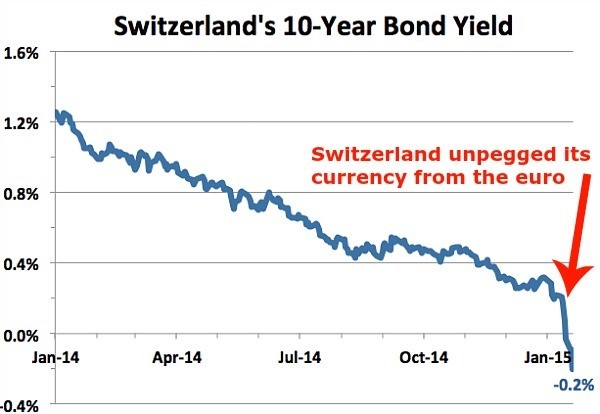

To confound views on traditional modern economics, we are seeing negative 10-year rates on Swiss Treasury Bonds (see chart below). In other words, investors are paying -1% to the Swiss government to park their money. A similar strategy could be replicated with $100 by simply burning a $1 bill and putting the remaining $99 under a mattress. Better yet, why not just pay me to hold your money, I will place your money under my guarded mattress and only charge you half price!

Does QE Work?

Debate will likely persist forever as it relates to the effectiveness of QE in the U.S. On the half glass empty side of the ledger, GDP growth has only averaged 2-3% during the recovery; the improvement in the jobs upturn is arguably the slowest since World War II; and real wages have declined significantly. On the half glass full side, however, the economy has improved substantially (e.g., GDP, unemployment, consumer balance sheets, housing, etc.), and stocks have more than doubled in value since the start of QE1 at the end of 2008. Is it possible that the series of QE policies added no value, or we could have had a stronger recovery without QE? Sure, anyone can make that case, but the fact remains, the QE training wheels have officially come off the economy and Armageddon has still yet to materialize.

I expect the same results from the implementation of QE in Europe. QE is by no means an elixir or panacea. I anticipate minimal direct and tangible economic benefits from Draghi’s $1+ trillion euro QE bazooka, however the psychological confidence building impacts and currency depreciating effects are likely to have a modest indirect value to the eurozone and global financial markets overall. The downside for these unsustainable ultra-low rates is potential excessive leverage from easy credit, asset bubbles, and long-term inflation. Certainly, there may be small pockets of these excesses, however the scars and regulations associated with the 2008-2009 financial crisis have delayed the “hangover” arrival of these risk possibilities on a broader basis. Therefore, until the party ends or the cops come to break up the fun, you may want to enjoy the gift provided by Mario Draghi to global investors…and strap on the “QE beer goggles.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

2012 Party Train Missed Thanks to F.U.D.

Article is an excerpt from previously released Sidoxia Capital Management’s complementary January 2, 2013 newsletter. Subscribe on right side of page.

There was plenty of fear, uncertainty, and doubt (F.U.D.) in 2012, and the gridlock in Washington has been a contributing factor to investors’ angst. As the saying goes, the stock market climbs a “wall of worry” and that was certainly the case this year with the S&P 500 index rising +13.4% (over +15% including dividends), and the Nasdaq index soaring +15.9% before dividends. Short-term investors had ample worries to fret about throughout the year, including a European financial collapse, the presidential elections, fiscal cliff negotiations, and a Mayan doomsday (see this hilarious clip). Despite these fears dominating the daily airwaves and newspaper headlines, long-term investors holding an adequate equity asset allocation jumped on the non-stop 2012 party train.

While Americans were served a full plate of concerns this year, global investors benefited from European Central Bank intervention by Mario Draghi who promised to do “whatever it takes” to save the euro currency (the European dominated EAFE index rose +13.6% in 2012). Growth here in the U.S. slowed as cautious consumers and businesses horded cash, but a rebound in the domestic housing market provided support to the sluggish economic expansion (3rd quarter GDP growth was revised higher to +3.1% vs. 2011).

Now that the presidential elections are over and we achieved a partial fiscal cliff deal, the amount of F.U.D. going into 2013 will diminish, which should provide a tailwind to economic growth and the financial markets. The impending debt ceiling and deficit reduction talks may slow the train down, but if a sufficient resolution can be accomplished, the economic party train can continue chugging along.

Attention: Grab Your Ear Muffs

Economists and strategists will continue to sound smart and be completely wrong about their 2013 predictions (see Strategist Predictions & MacGyver), but that won’t stop average investors from neglecting their long-term investment plans. Investors have commonly overindulged in certain narrow asset classes like overpriced bonds and gold, which both underperformed equities in 2012. Diversification may sound like an overused finance cliché, but the principle is paramount if you are serious about reducing risk, beating inflation, and smoothing out incessant volatility.

2013 New Year’s Resolution: Avoid Personal Fiscal Cliff

With the New Year upon us, just because politicians have financial problems, it doesn’t mean you have to be fiscally irresponsible too. There is no better time than now to make a financial New Year’s resolution to avoid your own personal fiscal cliff. If you are too heavily parked in cash or over-exposed to low-yielding bonds subject to significant interest rate risk, then now is the time to re-evaluate your investment plan.

There is always something to worry about (see also Uncertainty: Love It?), but in order to prevent working into your 80s, a long-term investment plan needs to be implemented, regardless of economic headlines or market volatility. In other words, investors need to replace their short-term microscope for their long-term telescope. By committing to a disciplined fiscal New Year’s resolution, you can earn a ticket on the 2013 party train!

Monthly News Tidbits

The presidential elections dominated the news cycle in November, but there were a whole host of other tidbits occurring over the last thirty-one days. Here are some of the main storylines:

Congress Approves Mini Fiscal Cliff Deal: After months of debate, Congress painfully and reluctantly agreed upon an estimated $600 billion mini fiscal cliff deal that represents the largest tax increase in two decades. Contrary to a $4 trillion “Grand Bargain” deal, this bill amounts to a more modest reduction in the deficit over 10 years. The Senate passed the bill by a margin of 89-8 and the House of Representatives by a spread of 257-167. The fact that any deal got done is somewhat surprising since the gridlock has been especially rampant in the House. As proof of this assertion, one need only point to the chamber’s meager voting activity record – the House has passed the fewest bills in 60 years during its recent term.

Fiscal Cliff Bill Details: Despite the Senate’s convincing voting margin, large numbers of Congressional Democrats and Republicans were unhappy with the bill’s details. The President made good on his campaign promises by securing revenue-raising taxes from wealthy Americans. More specifically, the law contains provisions including a 39.6% rate on earners above $400,000; a 20% capital gains rate increase from 15%; new exemption/deduction limits; an estate tax increase to 40% from 35%; and a measure to help prevent near-term milk price spikes. There are plenty more details, but I will spare your eyeballs and brain from the painful minutiae. If you haven’t had enough partisan politics, no need to worry, you have the debt ceiling debate to look forward to in a few months.

Quantitative Easing Redux (QE4): Federal Reserve Chairman Ben Bernanke helped orchestrate additional monetary policy stimulus via a fourth round of quantitative easing (a.k.a., QE4). As part of this plan, the Fed will vastly expand its $2.8 trillion balance sheet in 2013 with additional monthly purchases of $45 billion of long-term Treasuries. By executing this invigorating QE4 bond buying program, the Fed pledges to keep interest rates in the cellar until the unemployment rate falls below 6.5% or inflation rises above 2.5%.

Same-Sex Marriage: The Supreme Court tackled a long-debated social issue and declared it would rule on the legality of a law denying benefits to same-sex couples in 2013.

New Female President: Additional hormones were added to the gender-skewed global pool of testosterone-filled leaders as South Korea elected its first female president, Park Geun-hye.

Global Bank Fined: Another greedy financial institution got caught with its hand in the cookie jar. UBS agreed to cough up a $1.5 billion penalty to the U.S., U.K., and Swiss authorities as part of an agreement to resolve its involvement in the manipulation of the London Interbank Offered Rate (LIBOR) – see also Wall Street Meets Greed Street.

Sandy Hook Distressing Disaster: The gun control debate was reignited when 20-year-old Adam Lanza gunned down 20 children and 7 adults (including his mother) at a Connecticut elementary school – Sandy Hook Elementary. Besides the examination of an assault weapons ban, the government needs to revisit the inadequate awareness and resources devoted to the serious issue of mental illness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including fixed income ETFs, but at the time of publishing SCM had no direct position in EFA, UBS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Draghi & ECB Pass Trash and Serve Brussels Sprouts

ECB (European Central Bank) President Mario Draghi made it clear with his most recent monetary banking announcements that he is perfectly willing to shovel the sovereign debt trash around the financial system, but he just doesn’t want the ECB to gobble up heaps of the smelly debt.

On the same day that Draghi lowered the key benchmark interest rate by -0.25% to 1.00%, he also reduced the lending credit rating threshold for acceptable banking collateral to “single-A” and offered banks endless three-year loans with . But wait…there’s more! In typical infomercial fashion, Draghi had an additional stimulative gift offering – he halved the reserve requirement ratios for European banks.

Although Draghi is handing out lots of hugs and kisses to the banks, including infinite amounts of three-year loans, he is also providing very little direct love to European debt-laden governments. In other words, Draghi isn’t ready to pull out the printing press bazooka to sop up mounds of trashy sovereign debt (i.e., Greece, Italy, and Spain). Draghi may be willing to make the ECB the lender of last resort for the banks, but he is not signaling the same lender of last resort commitment for careless governments.

Despite Draghi’s public aversion to bond buying (a.k.a. QE or quantitative easing), he indirectly is funding quantitative easing anyway. Rather than having the ECB accelerate the direct purchase of besieged sovereign debt, he indirectly is giving money to the banks to purchase the same struggling bonds. Sneaky, but clever…I like it.

Eat Your Brussels Sprouts!

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi, in dealing with the irresponsible fiscal actions of the sovereigns, is using the same precise “sprout mandate.” In a recent press conference, here’s how Draghi delivered his tough talk:

“All euro-area governments urgently need to do their utmost” for fiscal sustainability. “Policy makers need to correct excessive deficits and move to balanced budgets in the coming years. This will strengthen overall economic sentiment. To accompany fiscal consolidation, the governing council has called for bold and ambitious structural reforms.”

Just as it makes sense for me not to say, “Hey kids, don’t worry about eating your vegetables, save room for the ice cream sundae buffet,” it probably doesn’t make sense for Draghi to inform European leaders, “Hey kids, don’t worry about those massive debts and deficits, the ECB will give you plenty of money to buy up all that trashy sovereign debt of yours.”

Hypocritical Or Shrewd?

I applaud Signore Draghi for implementing his bold actions as lender of last resort for European Banks, but isn’t it a tad bit hypocritical? The ECB President talks seriously about Basel III capital requirements, yet he is easing rules on collateral and reserves. Why is it OK for the ECB to condone reckless behavior and introduce moral hazards for the banks (i.e., limitless ECB backstop), but not for irresponsible governments too? If I am a European bank with continuous access to ECB loans, why not roll the dice and risk shareholder capital in hopes of a big risky payoff? I’m sure Jon Corzine at MF Global (MFGLQ.PK) would appreciate similar financial backing. What’s more, how credible can Draghi be about his tough fiscal love and anti-quantitative easing stances when he is currently offering never-ending amounts of money to the banks and already buying collapsing sovereign bonds as we speak?

No matter the view you hold, the ECB is openly demonstrating it will not sit idle watching the banking system collapse under its own watch, much like the Federal Reserve and Ben Bernanke did not sit idle in 2008-2009. Perhaps Draghi isn’t being hypocritical, but is rather being shrewd? Although Draghi wants governments to eat their fiscal Brussels sprouts, let’s not kid ourselves. Just as Draghi is willing to pass the trash and appease the banking system, if the eurozone sovereign debt crisis continues worsening, don’t be surprised to see Draghi roll out his ice cream sundae buffet of aggressive bond buying. That will taste much better than Brussels sprouts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MF Global (MFGLQ.PK), or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}