Posts tagged ‘M&A’

Supply & Demand: The Key to Oil, Stocks, and Pork Bellies

Commodity prices, including oil, are “crashing” according to the pundits and fears are building that this is a precursor to another stock market collapse. Are we on an irreversible path of repeating the bloodbath carnage of the 2008-2009 Great Recession?

Fortunately for investors, markets move in cycles and the fundamental laws of supply and demand hold true in both bull and bear markets, across all financial markets. Whether we are talking about stocks, bonds, copper, gold, currencies, or pork bellies, markets persistently move like a pendulum through periods of excess supply and demand. In other words, weakness in prices create stronger demand and less supply, whereas strength in prices creates weakening demand and more supply.

Since energy makes the world go round and the vast majority of drivers are accustomed to filling up their gas tanks, the average consumer is familiar with recent negative price developments in the crude oil markets. Eighteenth-century economist Adam Smith would be proud that the laws of supply and demand have help up just as well today as they did when he wrote Wealth of Nations in 1776.

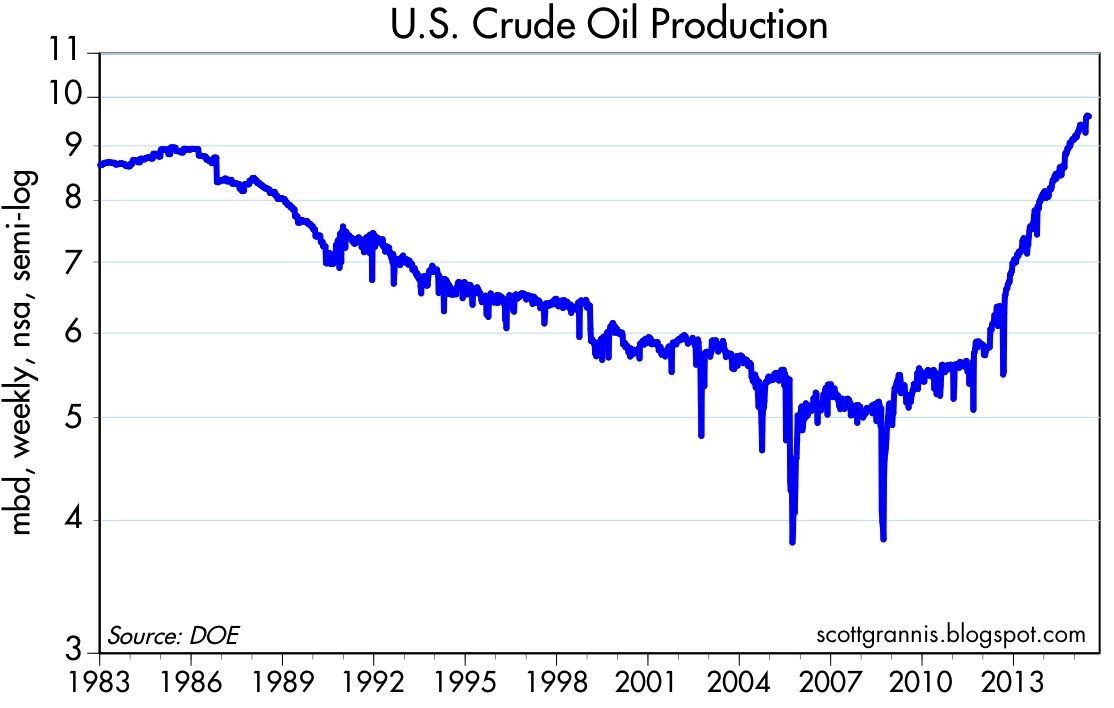

It is true that overall stagnation in global economic demand in recent years, along with the strengthening of the U.S. dollar (because of better relative growth), has contributed to downward trending oil prices. It is also true that supply factors, such as Saudi Arabia’s insistence to maintain production and the boom in U.S. oil production due to new fracking technologies (see chart below), have arguably had a larger negative impact on the more than -50% deterioration in oil prices. Fears of additional Iranian oil supply hitting the global oil markets as a result of the Iranian nuclear deal have also added to the downward pressure on prices.

Source: Scott Grannis

What is bad for oil prices and the oil producers is good news for the rest of the economy. Transportation is the lubricant of the global economy, and therefore lower oil prices will act as a stimulant for large swaths of the global marketplace. Here in the U.S., consumer savings from lower energy prices have largely been used to pay down debt (deleverage), but eventually, the longer oil prices remain depressed, incremental savings should filter into our economy through increased consumer spending.

But prices are likely not going to stay low forever because producers are responding drastically to the price declines. All one needs to do is look at the radical falloff in the oil producer rig count (see chart below). As you can see, the rig count has fallen by more than -50% within a six month period, meaning at some point, the decline in global production will eventually provide a floor to prices and ultimately provide a tailwind.

Source: Scott Grannis

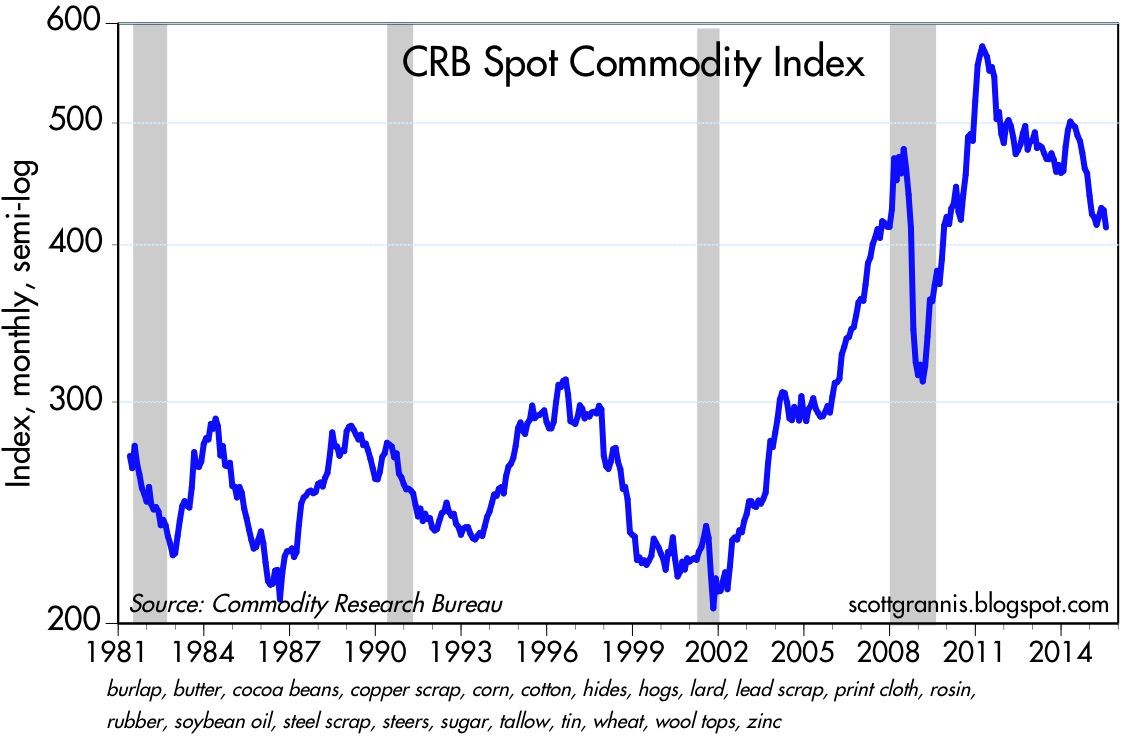

If we broaden our perspective beyond just oil, and look at the broader commodity complex, we can see that the recent decline in commodity prices has been painful, but nowhere near the Armageddon scenario experienced during 2008-2009 (see chart below – gray areas = recessions).

Source: Scott Grannis

Although this conversation has focused on commodities, the same supply-demand principles apply to the stock market as well. Stock market prices as measured by the S&P 500 index have remained near record levels, but as I have written in the past, the records cannot be attributed to the lackluster demand from retail investors (see ICI fund flow data).

Although U.S. stock fundamentals remain relatively strong (e.g., earnings, interest rates, valuations, psychology), much of the strength can be explained by the constrained supply of stocks. How has stock supply been constrained? Some key factors include the trillions in dollars of supply soaked up by record M&A activity (mergers and acquisition) and share buybacks.

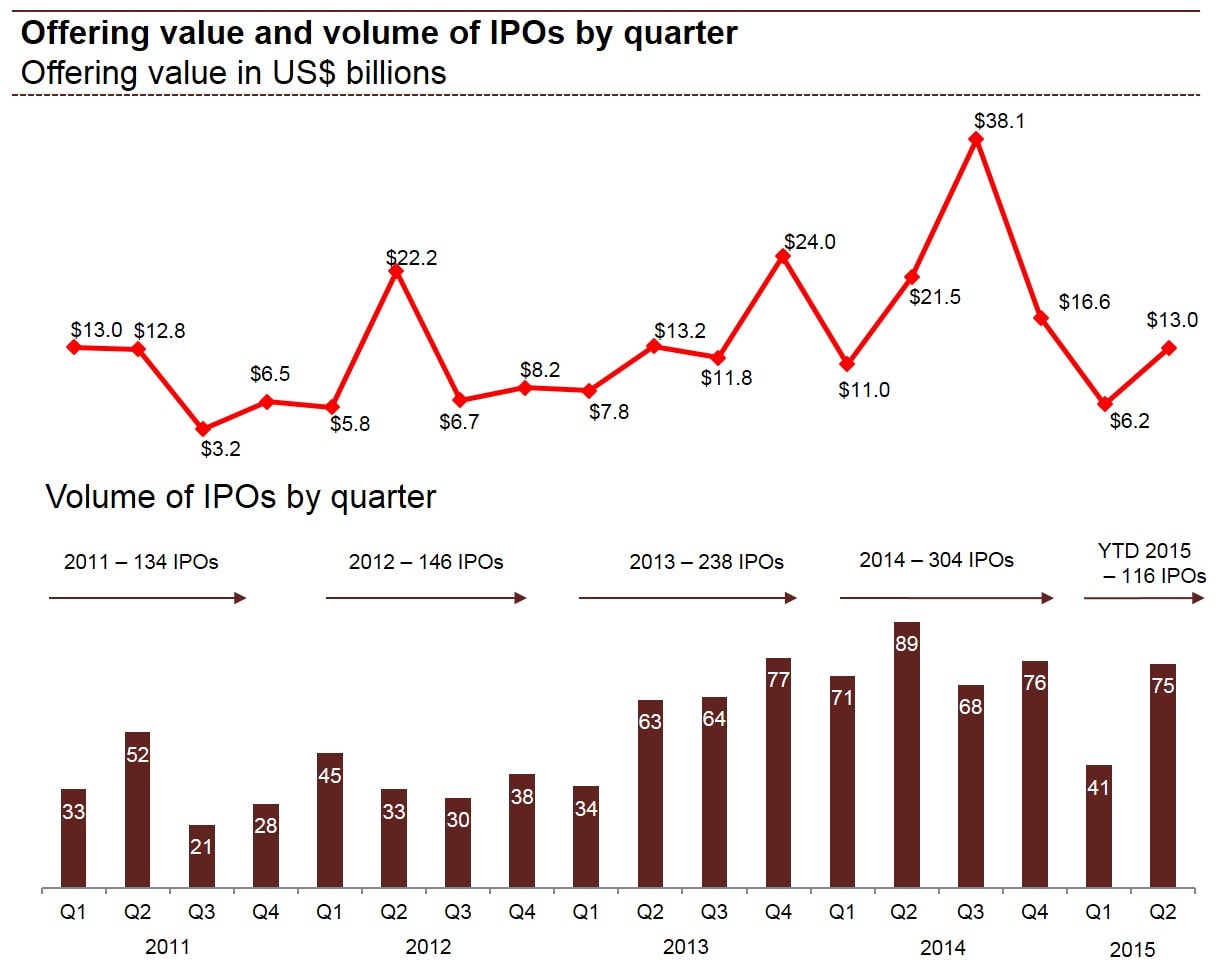

In addition to the declining stock supply from M&A and share buybacks, there has been limited supply of new IPO issues (initial public offerings) coming to market, as evidenced by the declines in IPO dollar and unit volumes in the first half of 2015, as compared to last year. More specifically, first half IPO dollar volmes were down -41% to $19.2 billion and the number of 2015 IPOs has declined -27% to 116 from 160 for the same time period.

Price cycles vary dramatically in price and duration across all financial markets, including stocks, bonds, oil, interest rates, currencies, gold, and pork bellies, among others. Not even the smartest individual or most powerful computer on the planet can consistently time the short-term shifts in financial markets, but using the powerful economic laws of supply and demand can help you profitably make adjustments to your investment portfolio(s).

See Also – The Lesson of a Lifetime (Investing Caffeine)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

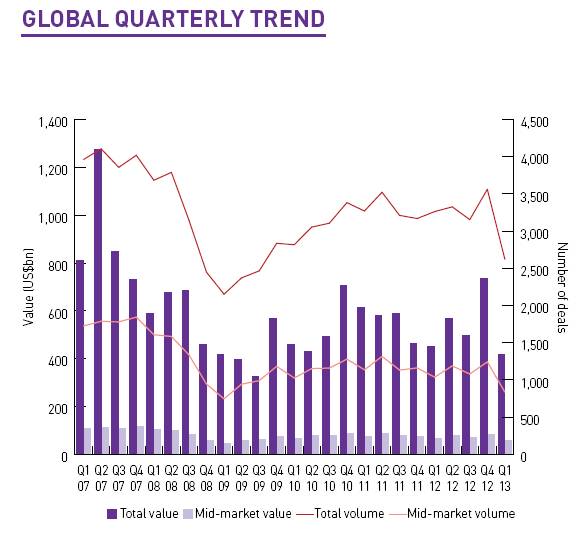

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

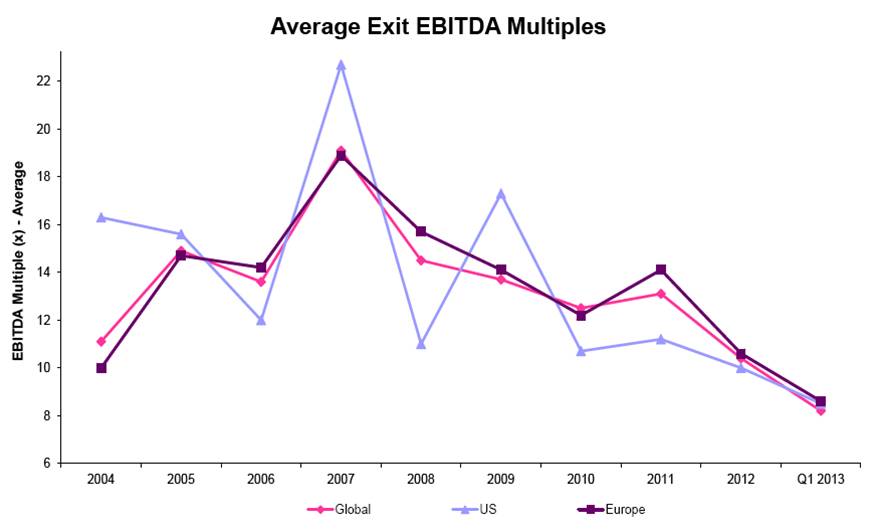

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

2011: Beating Batter into Flat Pancake

As it turns out, 2011 can be characterized as the year of the pancake…the flat pancake. While the Dow Jones Industrial Average (Dow) rose about 6% this year (its third consecutive annual gain), the S&P 500 ended the year flat at 1257.6 (-0.003%), the smallest yearly move in more than four decades. Along the way in 2011, there was plenty of violent beating and whipping of the lumpy pancake batter before the flat cake was cooked for the year. With respect to the financial markets, the 2011 lumps came in the form of various unsavory events:

* Never-Ending Eurozone Financial Saga: After Ireland and Portugal sought bailouts, Greece added its negligent financial storyline to the financial soap opera. Whether European government leaders can manage out-of-control deficits and debt loads will determine if Greece and other peripheral countries will topple larger countries like Italy and Spain.

* Credit Rating Downgrade: Standard & Poor’s, the highest profile credit rating agency, downgraded the U.S.’s long-term debt rating to AA+ from AAA due to high debt levels and Congressional legislators inability to hammer out a deficit-reduction plan during the debt ceiling negotiations.

* Japanese Earthquake and Tsunami: Japan and the global economy were rocked by a magnitude 9.0 earthquake and tsunami on March 11, 2011, which resulted in 15,844 people dead and 3,451 people missing. The ripple effects are still being felt through large industries like the automobile and electronics industries.

* Arab Spring Protests: Protesters throughout the Middle East and North Africa provided additional uncertainty to the global political map as demonstrators demanded regime change and more political freedoms. In the long-run, removing oppressive leaders like Hosni Mubarak (Egypt’s leader for 30 years), Muammar Gadaffi (Libya’s leader for 42 years), and Zine al-Abidine Ben Ali (Tunisia’s president for 23 years) should be beneficial for global stability, but in the short-run, how the new leadership vacuum will be filled remains ambiguous.

* Occupy Movement Voices Disapproval: The Occupy Wall Street movement began on September 17, 2011 in Liberty Square in Manhattan’s Financial District, and spread to over 100 cities in the U.S. There has not been a cohesive articulated agenda, but a common thread underlying all the Occupy movements is a sense that 99% of the population is being treated unfairly due to a flawed corrupt system controlled by Wall Street that is feeding the richest 1%.

All these lumps experienced in 2011 were not settling to investors’ stomachs. As a result individuals continued the trend of piling into bonds, in hopes of soothing their investment tummies. Long-term Treasury prices spiked upwards in 2011 (+29% as measured by TLT Treasury ETF) and soaring 10-year Treasury note prices pushed yields (1.87%) below yields on S&P 500 equities (2.1%). Despite a more than 3,400 point increase in the Dow (+39%) since the end of 2008, investors have still poured $774 billion into bonds versus $33 billion yanked from equities, according to EPFR Global. Over-weighting bonds makes sense for some, including retirees on fixed budgets, but many investors should brace for an inevitable reversal in bond prices. Eventually, the sweet taste of safety achieved from bond appreciation will turn to heartburn, once interest rates reverse their 30 year trend of declines.

Syrupy Factors Help Sweeten Pancakes

Although the aforementioned factors lead to historically high volatility and flat flavors in 2011, there are also some countering sweet reasons that make equities look more palatable for 2012. Here are some of the factors:

* Record Corporate Profits: Even with the constant barrage of fear, uncertainty, and doubt distributed via the media channels, corporations posted record profits in 2011, with an estimated increase of +16% over last year (and another forecasted +10% rise in 2012 – Source: S&P).

* Historic Levels of Cash: Record profits mean record cash, and all those riches have been piling up on non-financial corporate balance sheets at historic levels. At the beginning of Q4 the figure stood at $2.12 trillion. Companies have generally been stingy, but as the recovery progresses, they have increasingly been spending on technology, equipment, international expansion, and even the beginnings of hiring.

* Interest Rates at 60 Year Lows: Interest rates are at record lows and home affordability has never been better with 30-year fixed rate mortgages hovering below 4%. Housing may not come screaming back, but the foundation for a recovery is being laid.

* Improving Economic Variables: Whether you’re looking at broader economic activity (Gross Domestic Product up for nine consecutive quarters); employment growth (declining unemployment rate and 21 consecutive months of private job creation), or consumer spending (consumer confidence approaching multi-year highs), all major signs are currently pointing to an improving outlook.

* Near Record Exports: While the U.S. dollar has made some recent gains against foreign currencies because of the financial crisis in Europe, the relative value of the dollar remains historically low versus the major global currencies. The longer-term depreciation of the dollar has buoyed exports of U.S. goods to near record levels despite the global uncertainty.

* Unprecedented Central Bank Support Globally: Ben Bernanke and the U.S. Federal Reserve is committed to keeping exceptionally low levels of lending interest rates at least through mid-2013, while also implementing “Operation Twist” and potential further quantitative easing (QE3). Translation: Ben Bernanke is going to do everything in his power to keep interest rates low in order to stimulate economic growth. The European Central Bank (ECB) has pulled out its lending fire trucks too, with an unparalleled three-year lending program to extinguish liquidity fires in the European banking sector.

* Improving Mergers & Acquisitions Environment: We may not be back to the 2006 buyout “hay-days,” but U.S. mergers and acquisitions activity increased +24% in 2011. What’s more, high profile potential IPOs like an estimated $100 billion Facebook offering may help kick-start the new equity issuance market in 2012.

* Tasty Fat Dividends: Rarely have S&P 500 dividend yields (currently 2.1%) outpaced the interest rates earned on 10-year Treasury note yields, but now happens to be one of those times. Typically S&P 500 stock dividends have averaged about 40% of the yield on 10-year Treasury notes, and now it is 112%. In Q3 of 2011, dividend increases rose +17% and expectations are for nearly a +11% increase in 2012, said Howard Silverblatt, senior index analyst at S&P.

Any way you cut it (or beat the batter), 2011 was a volatile year. And despite all the fear, uncertainty, and doubt, profits continue to grow and sovereign nations are being forced to deal with their fiscal problems. Unforeseen risks always exist, but if Europe can contain its financial crisis and the U.S. recovery can continue into this new election year, then opportunities in the 2012 attractively priced equity markets should sweeten the flat equity pancake we ate in 2011.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, including a short position in TLT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

From Merger Wedding to eHarmony

Source: Photobucket

“Keep your eyes wide open before marriage, and half-shut afterwards.”

– Benjamin Franklin

Stocks share a lot of the same dynamics with dating and marriage. Some may choose to play the field through partnerships and joint ventures, while others may choose to remain independent as eternal bachelors/bachelorettes. Others, however, are willing to take the plunge. Unfortunately some marriages don’t last. But if things don’t work out, there is no need to worry because eHarmony.com (or resident investment bank) will always be there to help find your next perfect match.

Unlucky in Love

An example of a bloody divorce is the mega-merger between AOL Inc. and Time Warner (TWX) in 2000. The relationship was so destructive that investors witnessed AOL’s peak value of $222 billion in December 1999 (Fortune) plummet to around $3 billion today…ooooph!

Compared to some relationships, AOL lasted much longer. In fact Yahoo! Inc. (YHOO) didn’t even get to celebrate a honeymoon with Microsoft Corp. (MSFT) in February 2008 when the behemoth software company offered a +62% premium ($31 per share) for the gigantic portal. Microsoft’s $45 billion cash and stock offer was ruled unworthy by Yahoo’s board, so the company decided to leave Microsoft at the altar. Even after considering Yahoo’s latest price spike on acquisition rumors, Microsoft’s original bid is still almost double Yahoo’s current stock price of $16 per share.

Merger Scuttlebutt

As I discussed in my earlier mergers and acquisitions article (M&A) conditions are ripening with large corporate cash piles, a continued economic recovery, improved capital markets availability, and cheap credit costs (at least for those that qualify). With the clouds slowly lifting in the M&A world, suitors are shaking the trees for more potential opportunities.

While some acquirers may have altruistic intentions in combining companies, some marriages are done for pure gold-digging purposes. Private equity firms Blackstone Group (BX) and Silver Lake are rumored to be circling the Yahoo wagons and courting AOL as a potential partner in a joint bid. Whatever the expectations, if private equity plays a role in a Yahoo bid, the internet company should not become disillusioned with romantic warm and fuzzies – private equity firms like to get straight down to dirty business. Yahoo owns a 35% stake in Yahoo Japan and a 43% interest in leading Chinese e-commerce company, Alibaba Group. If a joint private equity bid were ever to win, I believe there would be a strong impetus to realize shareholder value by carving up these non-operating stakes. Consolidating overhead and streamlining expenses would likely be a top priority as well.

The Perfect Marriage

A “perfect marriage” could almost be called an oxymoron because like any relationship, there is significant work required by both parties. The divorce rate is estimated at around 40-50% in North America (Europe around the same), however mergers even fail at a higher 70% rate, according to Bain and Company study. I would argue successfully integrating larger deals are even more difficult, hampering the success rate even further. Merging two poorly managed companies purely for cost purposes is probably not the best way to go. Crashing two garbage trucks together is not going to create a Ferrari. I wouldn’t go as far as to say Yahoo and AOL are garbage trucks, but they face numerous, substantial challenges. Maybe these two companies are more akin to Mazdas transforming into a Toyota Camry (TM).

From my perspective, if companies really are dead set on engaging in acquisitions, then I urge management teams to focus on smaller digestible deals. Specifically, concentrate on those deals with experienced senior management teams who understand and respect the unique culture of the acquirer. Mergers also often fail due to excessive optimism and overly optimistic assumptions. This is an area in which Warren Buffett excels. Rarely do you observe the Oracle of Omaha overpaying for an acquisition, but rather he patiently waits for his fat pitch, and when it floats over the plate, Buffett is quick to throw out a lowball offer that will dramatically increase the probabilities of long-term merger success (think Geico, Sees Candy, Burlington Northern, etc.).

In the end, a joint relationship may not be forged between Yahoo, AOL and private equity firms, but if talks disintegrate, no need to worry – alternative partnerships can be explored on eHarmony.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in YHOO, MSFT, TWX, BX, BRKA, TM, Alibaba, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

September Surge: Stop, Go, or Proceed Cautiously?

The stock market just posted its strongest September and third quarter performance in more than seven decades (S&P 500 +8.8% and +10.7%, respectively), yet people are still waiting for a clear green light to signal blue investment skies ahead. Well of course, once it is apparent to everyone that the economy is obviously back on track, the opportunities persisting today will either be gone or vastly diminished. I’m not a blind optimist, but a sober realist that understands, like Warren Buffett, that it pays to “buy fear and sell greed.” And fear is exactly what we are witnessing today. The $2.6 trillion sitting in CDs earning a horrendously low 1% is simple proof (Huffington Post).

Like the fresh memory of a recent hand burned on the stove, the broader general public is still feeling the pain and recovering from the financial crisis. Each gloomy real estate or unemployment headline triggers agonizing flashbacks (read Unemployment Hypochondria) of the 2008-2009 financial collapse and leads to harmful emotional investment decisions. However, for some of us finance geeks that have cut through the monotony of “pessimism porn” blasted over the airwaves, we have discovered plenty of positive leading economic indicators bubbling up below the surface, like the following:

- Continued Economic Growth: Gross Domestic Product (GDP) grew +1.7% in the second quarter and current estimates stand in the +2.0% to +2.5% range for third quarter GDP, which will mark the fifth consecutive quarter of growth.

- Growing Corporate Profits: S&P 500 earnings are estimated to expand by +45.6% in 2010 and are estimated to grow by another +15% or so next year (Standard & Poor’s September 2010).

- Escalating M&A: Mergers and acquisitions activity increased to $566.5 billion in the third quarter. The value of announced transactions is up +60% from a year ago according to Bloomberg. If you have a tough time comprehending the pickup in M&A, then take a peek here.

- Record Cash Piles: The top 1,000 largest global corporations held a whopping $2.87 trillion in cash (Bloomberg).

- Accelerating Share Buybacks: Share buybacks totaled $77.6 billion in the second quarter, up +221% from a record low last year – Barron’s).

- Dividends Galore: S&P 500 companies have lifted their payouts by $15 billion so far this year versus a reduction of $40 billion for the same period last year (The Wall Street Journal). Tech giant Cisco Systems Inc. (CSCO) announced the pending initiation of a dividend, while Microsoft Corp. (MSFT) increased its dividend by a significant +23%.

I’m not naïve enough to believe choppy waters will disappear for good, but despite the depressing headlines there are constructive undercurrents. Beyond the points above, equity market prices remain attractive relative to the broader fixed-income markets (see Bubblicious Bonds) . More specifically, the S&P 500 is priced at about a 25% discount to historic valuation averages over the last 55 years (currently trading at about 12.5 Price/Earnings ratio vs 16.5x historic Price/Earnings ratio – Bloomberg). Now may not be the time to recklessly run a red light, but if you fearfully remain halted in front of the green light then prepare to receive a pricey ticket.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and CSCO, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

M&A: Top or Bottom?

James Stewart at Smart Money recently wrote a piece attempting to debunk the consensus view, which holds the belief that increased mergers and acquisitions (M&A) activities is a leading indicator of positive market returns. There is no doubt, in the desert of positive news headlines, the bulls are searching for signs of an oasis to rescue them. Temporarily quenching the thirst of the bulls were $90 billion of proposed deals last week, including the hefty $40 billion hostile takeover offer of Potash Corp. (POT) by BHP Billiton Ltd. (BHP).

Is this uptick in deal announcements the sign of greener pastures, or is it what Stewart calls a “reverse indicator” of the market’s direction?

Stewart buttresses his argument by showing how record deal activity occurs at peaks of the market. For example, global M&A activity crested at $4.3 trillion in 2007, right before the market cratered in 2008. This peak can be compared to the previous trough of $1.3 trillion in M&A transactions in 2002, just as the economy was freshly recovering out of the recession. The trough to peak period for this M&A cycle lasted about five years (2002-2007), so I’m having a little trouble understanding how Stewart is claiming a peak is imminent after less than 1 year into the new M&A cycle (the recent M&A trough occurred in 2009 at $1.3 trillion)? Wouldn’t his analysis imply a gradual increase in deals until 2014? Well, for now, let’s just go with his rapid orgasm thesis and move onto his next points.

Stewart proceeds to rationalize the spate of new deal announcements with the following reasons:

- Higher Prices Perk Up Previously Reluctant Sellers: The general price rebound in the market from the nadir in March 2009 is one major contributing factor to why previously reluctant targets are now warming up to fresh overtures.

- Suitors More Comfortable: In 2009, buyers weren’t in the mood for paying top dollar for companies experiencing deteriorating fundamentals. Prices may be higher in 2010, but the Armageddon scenarios of early 2009 have momentarily been put on hold.

- Money Can’t Get Any Tighter: The cheap, loosey-goosy lending standards in the pre-2008 M&A golden era no longer exist, but conditions can’t get much worse than the log-jammed lending standards practiced in 2009.

The Real Reason for Deals Rising

Source: The Wall Street Journal

One word…cash. About $1.8 trillion of it is just piling up on the non-financial balance sheets of domestic companies (Financial Times). The tribes are getting restless with the obscene amounts of money earning 1% or less (read Steve Jobs: Gluttonous Hog article) and shareholders want to see more productive strategies applied to their capital. Frankly, I much prefer organic investment (e.g., R&D and marketing), share buybacks, and dividends over large destructive acquisitions any day. Just ask the executives at AOL/Time Warner, Mercedes Benz/Chrysler, and Sprint/Nextel how those large deals worked out for them. For some reason, many men like driving big macho trucks, just as many CEOs like controlling big companies.

One Reason to Buy and Many Reasons to Sell

I can’t disagree with James’s thesis that M&A markets get overheated near market tops, but I think there is a lot of room in deal announcements between the $90 billion in deals announced last week and the $4.3 trillion peak. I also agree that one good week of M&A announcements should not be extrapolated into eternity.

Worth noting as well, I believe there is a substantial difference in the financing market today versus the prior peak. In the BHP/Potash deal for example, BHP offered $40 billion in cash…not stock. BHP is putting its money where its mouth is, particularly its $18 billion in annual cash flow and its healthy balance sheet. Internal financing wasn’t the main priority in the mid-2000s, when companies (including private equity) were more cavalier with OPM (other people’s money), specifically with the endless pools of cheap bank financing.

Currently, companies have deep pockets, but very short arms, and as a result, companies have been very stingy with their capital. However, if we continue to see more internally financed cash deals, I will view that trend as a tremendously positive signal of longer-term fundamental confidence, a characteristic which was absent last year.

On the topic of insider buying, Peter Lynch pointed out “there is only one reason to buy and many reasons to sell” – the only real reason to purchase is the belief stock prices will move higher. Since the availability of cheap capital has been severely hampered, a wide swath of companies will have to rely on their own cash generation – not OPM. Since outside capital is scarce, the companies with cash flexibility will be more prudent in their M&A due diligence.

Overall, James Stewart may be right about the sustainability of M&A going into next year. However, in the short-run, as the gargantuan corporate cash piles get put to use through more M&A, and share buybacks, simple supply-demand economics indicate a shrinking equity base should bode well for market prices, all else equal. Uncertainty is available in large quantities right now, so time will tell if deal making will diminish into a market top, or gain momentum into a bull market. With all that cash sitting on the sidelines, my guess is we are closer to the trough of the M&A wave versus the top. If I’m wrong, don’t hold your breath for a Microsoft-Google (MSFT/GOOG) or Exxon-Chevron (XOM/CVX) merger anytime soon.

Read Full Smart Money M&A Article Here (Hat-Tip Josh Brown TRB)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in BHP, POT, MSFT, XOM, CVX, AOL/Time Warner (TWX), Mercedes Benz/Chrysler, and Sprint/Nextel (S) or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity Sitting on Stuffed Wallet

The clock is ticking and private equity (PE) firms need to put some $445 billion in their wallets to work. Otherwise, the dreams of outsized returns and hefty fees will have to wait for another Golden Era of deal making. Why such a hurry to use the cash? According to Andrea Auerbach, a Managing Director at Cambridge Associates, “Most funds legally have five or six years to invest that capital…it’s use it or lose it.”

Shop ‘til Wallet Drops

As easy as it sounds, spending half a trillion dollars can be difficult. Here’s how IBD’s Norm Alster characterizes the challenge:

“To realize the outsize profits investors expect, private equity firms would have to borrow two or three times that amount. But for the most part, credit spigots for such deals are still dry. At the same time, pinning down buyout targets is not that easy. Many potential sellers are balking at parting with corporate assets in the midst of a serious downturn.”

The 2010 private equity environment is quite a bit different than the LBO boom era from a handful of years ago, as you can see from the chart below. Thanks to cheap, free-flowing funding from the banks, $1.4 trillion worth of deals were consummated in 2006 and 2007, including large deals like First Data Corp. ($27 billion deal – KKR); Alltel ($28 billion – Goldman Sachs/ Texas Pacific Group); and Harrah’s ($30 billion – Apollo Management/Texas Pacific Group). Unfortunately, deals done during this period were done when valuations and leverage were at extremely high historical levels.

Chart source: Thomson Reuters via IBD

Deal Timeout

What’s causing the current dearth of deals? In many instances, business owners have not calibrated valuation expectations downward enough to account for the bruising financial crisis. Given the 77 leveraged buyout defaults in 2009, investors have become more reticent in committing capital as well. Refinancing the mountains of debt associated with the troubled 2006-07 vintage of deals will require patience and creative financing skills from the banks.

Because of the logjam of deals created by the financial crisis, PE firms are actively looking for exit strategies relating to their portfolio companies. Since private equity inherently involves illiquid investments, typically the industry creates liquidity through initial public offerings (IPOs), merger & acquisitions, and/or recapitalization structures that partially or fully return investor capital.

If the economic malaise lingers and valuations remain depressed, I have no doubt owners will eventually return to the negotiating table while waving a white towel in hand. Until then, private equity firms will continue begging for capital from the banks (i.e., using “other peoples’ money”) and beating down sellers into submission with regards to price expectations. If PE firms are not successful in using that wad of cash by the end of the fund’s term, then investors will be free to walk away with their money without paying lucrative fees to the PE firms.

Don’t Forget Benefits

The PE field is facing its fair share of trials and tribulations, but PE’s diversification benefits should not be forgotten. The success of the “Yale Model,” implemented by David Swensen, has come under attack with the recent bursting of the credit bubble, but with the ever-swinging performance pendulum of various asset classes/styles moving in and out of favor, I am confident a consistent strategy integrating PE as a portion of a diversified portfolio will yield respectable risk-adjusted returns over the long-run. Like other areas in the financial services industry, fees are being scrutinized and transparency requests by investors (limited partners) have been on the rise. But first things first – before attractive PE profits can be made as part of a diversified portfolio, the wad of cash in the wallets of PE firms must find a home in portfolio companies.

Read Norm Alster’s full IBD article originally referenced on TRB

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in GS, Harrah’s or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}